Global EVs (Overweight) - Tesla reshaping the industry landscape

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

2021 Outlook | November 24, 2020 Global EVs (Overweight) Tesla reshaping the industry landscape Yeon-ju Park yeonju.park@miraeasset.com Chuljoong Kim chuljoong.kim@miraeasset.com Minkyung Kim minkyung.kim.a@miraeasset.com Hyunwoo Jin hyunwoo.jin@miraeasset.com Jaekwang Rhee jkrhee@miraeasset.com Analysts who prepared this report are registered as research analysts in Korea but not in any other jurisdiction, including the US PLEASE SEE ANALYST CERTIFICATIONS AND IMPORTANT DISCLOSURES & DISCLAIMERS IN APPENDIX 1 AT THE END OF REPORT.

Contents

[Summary] A world shaped by Tesla 3

I. [2020 review] Tesla and the pandemic 4

II. [2021 outlook] 5

① Tesla to tighten its grip on the market

② European OEMs to play catch-up

③ Inevitable changes for US OEMs

④ Battery innovation to accelerate

⑤ Opportunity in commercial EVs

⑥ Upside potential of US ESS market

⑦ Potential comeback of lithium

⑧ China transitioning to market competition

III. [Medium-term outlook] Transition to gain pace 34

IV. [Investment strategy] Tesla reshaping the landscape 35

V. Global peer valuations 36

VI. [Company analysis] 37

Geely Automobile/LG Chem/Samsung SDI

2 | [2021 Outlook] Global EVs Mirae Asset Daewoo Research

[Summary] A world shaped by Tesla

Adjusting up our medium-term electric vehicle (EV) penetration rate forecasts

33%

Shift to EVs to accelerate

Battery innovation driven by Tesla,

increased policy support, OEMs’

commitment to EV transition, and

Penetration

more compelling models

29%

21%

18%

4%

2020F 2025F 2030F

3 | [2021 Outlook] Global EVs Mirae Asset Daewoo Research

I. [2020 review] Tesla and the pandemic

Enhanced growth • In 2020, stocks of companies in the global EV supply chain have outperformed the broader market.

potential • In particular, Tesla has outperformed on the back of robust earnings and a stronger growth outlook, supported

by increased government subsidies since the COVID-19 outbreak.

• Tesla has been setting new sales records and delivering earnings surprises.

• Governments in Europe have expanded EV subsidies as part of their stimulus packages.

• China, after pledging to achieve carbon neutrality by 2060, announced an aggressive target for EV sales by 2035.

• EV makers (e.g., Tesla) and Chinese battery suppliers have enjoyed share price rallies.

Tesla: 12-month forward EPS consensus YTD share performances of global EV makers/battery suppliers

($) (%)

2021 EPS consensus 2022 EPS consensus

6 400

300

4 200

100

0

2

Tesla BYD CATL LG Chem Samsung SDI

1/20 3/20 5/20 7/20 9/20 11/20

Source: Bloomberg, Mirae Asset Daewoo Research Source: Bloomberg, Mirae Asset Daewoo Research

4 | [2021 Outlook] Global EVs Mirae Asset Daewoo Research

II. [2021 outlook] ① Tesla to tighten its grip on the market

Tesla’s production • The start of China production is what has powered Tesla’s surprise performance in 2020.

capacity in China to • Increased cost competitiveness and subsidies have enabled Tesla to cut the price of its Chinese-made Model 3,

expand leading to volume growth and earnings improvement.

• For the Model Y, production at Gigafactory Shanghai is expected to start in 2021; Tesla will likely offer competitive

pricing to expand its market share (as it did with the Model 3).

• Given that the Model Y and the Model 3 share 70% of their parts, expanded production should lead to a virtuous

circle whereby scale effects lead to additional cost reductions, price cuts, and market share gains.

• We forecast Tesla’s production capacity in China to expand more rapidly than the market is currently anticipating,

reaching 250,000 units at end-2020 and double that level at end-2021.

Tesla Model 3’s selling price in China Model 3 vs. Model Y

(CNY'000)

500 Model 3 Model Y

Standard Range Plus RWD Long Range AWD

Purchase tax Subsidies for

models made

400 in China

Price cut

Additional

300 Additional

Segment Sedan SUV

250,000

488,000

200 Starting price (CNY) (including subsidies and

(likely to be lowered)

tax benefits)

Driving range (km,

430 505

WLTP)

100

0-60mph (s) 5.6 5.1

Battery capacity

54 75

(kWh)

0

Dimensions (mm) 4,694 x 1849 x 1443 4,751 x 1921 x 1624

2019.05 2019.08 2020.01 2020.04 2020.05 2020.09

Note: Including subsidies and tax benefits Source: Press reports, Mirae Asset Daewoo Research

Source: Press reports, Mirae Asset Daewoo Research

5 | [2021 Outlook] Global EVs Mirae Asset Daewoo Research

II. [2021 outlook] ① Tesla to tighten its grip on the market

Gigafactory Berlin to • Gigafactory Berlin is scheduled to come online in Jul. 2021 and produce the Model Y.

come online in mid-2021 • Gigafactory Berlin should be more cost-competitive than the Fremont factory, in light of: 1) tariff exemption in

the eurozone (vs. a 10% tariff on imported cars from the US); 2) transportation cost reductions; and 3) fixed-cost

savings.

• Tesla plans to use Gigafactory Berlin as a testbed for new technologies.

• The Model 3 offers more compelling features than other premium models in the same class, aided by Tesla’s

dedicated platform, scale effects, and superior battery management system (BMS) technology.

• The upcoming start-up of Gigafactory Berlin will help Tesla sharpen its competitive edge in European markets.

Tesla Model 3 (long-range) vs. European premium EVs

Automaker Tesla Mercedes-Benz Audi Volvo BMW Porsche

Model 3

Model EQC e-tron 50 Polestar 2 iX3 Taycan 4S

Long Range AWD

Segment Sedan SUV Midsize Midsize SUV Luxury sedan

Starting price

52.4 71.3 62.7 57.9 68.0 108.9

(EUR‘000)

Driving range

560 417 341 470 460 335–408

(km, WLTP)

0-60mph (s) 4.6 5.1 6.8 4.7 6.8 4.0

Battery capacity

75 80 71 78 80 79.2

(kWh)

Dimensions (mm) 4,694 x 1,849 x 1,443 4,761 x 1,884 x 1,623 4,901 x 1,935 x 1,632 4,606 x 1,479 x 1,985 4,734 x 1,891 x 1,668 4,963 x 1,966 x 1,379

Jan. 2020 (Apr. in the

Release Jul. 2018 Jul. 2019 Jan. 2020 Jun. 2020 End-2020

US)

6 | [2021 Outlook] Global EVs Mirae Asset Daewoo Research

II. [2021 outlook] ① Tesla to tighten its grip on the market

Texas factory and • Tesla's Texas factory is scheduled to come online in mid-2021 and produce the Cybertruck and the Model Y.

Cybertruck • Despite its high price tag, the Cybertruck should generate strong demand thanks to its compelling features and

better fuel economy than conventional vehicle models (F-150 annual fuel cost: US$1,400-1,500). Cybertruck pre-

orders have already exceeded 600,000.

• With the Cybertruck, Tesla is poised to extend its grip beyond the sedan/SUV segments into the pickup segment.

Tesla Cybertruck vs. comparable conventional vehicle models (F-150/F-250)

Tesla Cybertruck Ford F-Series

Model Dual Motor AWD Tri Motor AWD F-150 F-250

Starting price (US$) 49,900 69,900 28,745–71,160 34,035–84,130

Traction force (lbs) 10,000 14,000 6,000~12,000 12,600~

0-60mph (s) < 4.5 < 2.9 6.2 7.2

Driving range (km) 480 800~ - -

Release End-2021 End-2021 - -

Source: Press reports, Mirae Asset Daewoo Research

7 | [2021 Outlook] Global EVs Mirae Asset Daewoo Research

II. [2021 outlook] ① Tesla to tighten its grip on the market

Battery production and • Tesla plans to produce 100GWh of its own battery cells by 2022. A pilot production line (annual capacity of 10GWh)

at the Fremont factory will be completed by end-2020, and mass-production quality assessment is set for 1H21.

costs

• While it remains to be seen how pilot production will turn out, we think Tesla stands a good chance of achieving a

bigger battery cell form factor. Indeed, larger-form-factor cells are already being developed by existing battery

makers, and Tesla has competitive advantages such as superior BMS and automation technology, strong

financing and execution abilities, and scale.

• Tesla’s battery road map has prompted battery cell companies to accelerate their R&D efforts. We believe Tesla

can better position itself for success through partnerships with existing battery makers.

• We expect Tesla to accelerate battery cost reductions through in-house production and/or partnerships with

existing battery makers.

Tesla’s road map to cutting battery costs in half Panasonic working with Tesla on 4680 battery cell production

Source: Tesla, Mirae Asset Daewoo Research Source: Maeil Business Newspaper, Mirae Asset Daewoo Research

8 | [2021 Outlook] Global EVs Mirae Asset Daewoo Research

II. [2021 outlook] ① Tesla to tighten its grip on the market

Tesla’s software • Tesla’s competitive software sets it apart from conventional OEMs.

competitiveness to • Tesla vehicles regularly receive over-the-air software updates that improve driving performance.

increase • Autonomous driving features are popular with consumers, and Tesla has recently increased their prices.

• Tesla’s latest full self-driving (FSD) beta represents a significant step toward complete autonomy. Looking to 2021,

we expect Tesla to enhance its competitiveness on the back of accumulated data, chip upgrades, and the massive

computing power of the Dojo computer.

Software updates to increase Model S’s driving range Tesla’s FSD features and price

(km) (US$)

700 11,000

10,000

9,000

8,000

600

7,000

6,000

5,000

500 4,000

2019 2/20 8/20 11/20 5/19 7/19 11/19 7/20 11/20

9 | [2021 Outlook] Global EVs Mirae Asset Daewoo Research

II. [2021 outlook] ② European OEMs to play catch-up

Tesla has no equal in the • Amid expanded government subsidies, EV sales in Europe have increased sharply. That said, sales have been

concentrated in the mass-market segment (e.g., Renault ZOE and Hyundai Kona).

premium segment

• Premium models that OEMs released to compete against Tesla have fared worse than expected.

• Sales of the EQC are falling short of the 2020 target due to high pricing and lack of appeal. Meanwhile, the launch

of Volkswagen’s ID.3 was delayed due to software problems. We believe Volkswagen continued to market the e-

Golf (for which production had been scheduled to be discontinued) to avoid CO2 penalties.

• European OEMs are finding it difficult to catch up with Tesla and avoid CO2 penalties due to the absence of

dedicated platforms, a lack of scale, and software issues.

Ranking of pure EV models in the EU by sales (Sep. 2020) Volkswagen ID.3’s launch was delayed by software issues

(Units)

18,000

15,000

12,000

9,000

6,000

3,000

0

Tesla Renault VW ID.3 HMC Kona Kia Niro EV Audi Nissan Leaf

Model 3 ZOE EV e-tron

Source: Press reports, Mirae Asset Daewoo Research Source: Verge, Mirae Asset Daewoo Research

10 | [2021 Outlook] Global EVs Mirae Asset Daewoo ResearchII. [2021 outlook] ② European OEMs to play catch-up

European OEMs need to • European OEMs still do not seem fully prepared to shift to EVs, despite their widely publicized commitments to do

so. That said, we expect them to act with greater urgency in 2021 for several reasons:

act faster

• First, the European Commission is considering tighter environmental regulations; under one proposal, average

CO2 emissions from new cars would have to be 50% below 2021 levels by 2030 (vs. 37.5% under the current plan;

decision on the proposal expected by Jun. 2021).

• Second, the EV penetration rate has continued to increase, aided by increased government subsidies.

• Last and most important, Tesla continues to strengthen its competitiveness (e.g., Gigafactory Berlin and efforts to

produce battery cells in-house).

European Commission plans to impose tougher CO2 rules Tesla beginning hiring for Gigafactory Berlin

2020 2025 2030

0

-20

-40

-60

Original New

(%)

Source: Press reports, Mirae Asset Daewoo Research Source: Teslari, Mirae Asset Daewoo Research

11 | [2021 Outlook] Global EVs Mirae Asset Daewoo ResearchII. [2021 outlook] ② European OEMs to play catch-up

European OEMs need to • European OEMs are already planning to roll out more compelling EV models in 2021.

act faster • Volkswagen is set to release its ID.4 electric SUV, and the automaker’s use of a multi-model platform will lead to

increased competitiveness and scale effects.

• Mercedes-Benz and BMW also plan to release long-range (over 400km) EV models in the EUR40,000-60,000 price

range.

• We expect EV demand in Europe to continue to grow, supported by increased subsidies and the release of more

competitive models.

Major European EV models to be released in 2021

Automaker Volkswagen BMW Mercedes-Benz Volvo

Model ID.4 1st i4 EQA XC40

Segment SUV Sedan SUV SUV

Starting price

48.7 65.0 45.0 62.0

(EUR'000)

Driving range

496 600 400 400

(km, WLTP)

0-60mph (s) 8.5 4.0 5.0 4.9

Battery capacity

77 80 60 78

(kWh)

Dimensions (mm) 4,584 x 1,852 x 1,631 4,650 x 1,850 x 1,400 4,450 x 1,810 x 1,500 4,425 x 1,863 x 1,658

Release Early 2021 Early 2021 End-2021 Early 2021

Source: Press reports, Mirae Asset Daewoo Research

12 | [2021 Outlook] Global EVs Mirae Asset Daewoo ResearchII. [2021 outlook] ② European OEMs to play catch-up

European OEMs need to • However, even these new competitive models will likely be no match for Tesla. European OEMs have to move

more quickly, as Tesla’s competitiveness will strengthen further once Gigafactory Berlin comes online.

act faster

• BMW is now developing a dedicated EV platform, reversing its earlier decision to develop a shared platform for

conventional and EV models. The change in strategy reflects BMW’s stronger commitment to the EV transition.

• Going forward, we expect OEMs to increasingly adopt dedicated EV platforms or shift rapidly to next-generation

platforms. We also expect them to raise their EV sales targets and enter large-scale battery sourcing contracts.

Mercedes-Benz EQC sales volume (Jan.-Sep.) vs. initial target for 2020 BMW’s change in EV platform strategy

(Units)

40,000

30,000

20,000

10,000

0

2020 target Jan.-Sep. sales

Source: Press reports, SNE Research, Mirae Asset Daewoo Research Source: The Detroit Bureau, Mirae Asset Daewoo Research

13 | [2021 Outlook] Global EVs Mirae Asset Daewoo ResearchII. [2021 outlook] ③ Inevitable changes for US OEMs

US market backpedaling • In 2020, the US EV market shrank, hurt by the Trump administration’s weaker fuel economy standards, the end of

tax benefits for EVs, and a lack of compelling new EV models.

on EV transition

• The Trump administration rolled back fuel efficiency standards put in place by the Obama administration, citing

the economic slowdown. As a result, major EV models released in Europe did not debut in the US market.

• Contrary to their official stances on the EV transition, US OEMs were not in any hurry to release competitive EV

models.

US EV sales volume Fuel economy regulations: Obama vs. Trump administrations

('000 units) (mpg)

Obama Trump

60 60

PHEV

BEV

50

40

40

20

30

0

20

1/17 1/18 1/19 1/20

2020 2025

Source: SNE Research, Mirae Asset Daewoo Research Source: Press reports, Mirae Asset Daewoo Research

14 | [2021 Outlook] Global EVs Mirae Asset Daewoo ResearchII. [2021 outlook] ③ Inevitable changes for US OEMs

Need for change • In 2021, US OEMs are likely to embrace the EV transition, as: 1) Tesla’s Cybertruck will directly target the pickup

truck market, which is led by US OEMs; 2) global OEMs are set to release new EV models in the US; and 3) fuel

efficiency standards may be tightened under the incoming Biden administration.

• Tesla, which has competed against global premium brands in the sedan and SUV segments, is now extending its

market reach to the pickup segment, presenting a challenge to US OEMs.

• With the Cybertruck poised to achieve rapid market penetration, OEMs must respond.

US pickup M/S breakdown (1Q-3Q20) GM’s M/S by segment (2019)

Nissan Honda

2.2% 1.1%

Other

4%

Passenger cars

Toyota 14%

11.7%

Ford

32.4% Pickup trucks

33%

FCA

22.4%

SUVs

49%

GM

30.1%

Source: MarkLines, Mirae Asset Daewoo Research Source: MarkLines, Mirae Asset Daewoo Research

15 | [2021 Outlook] Global EVs Mirae Asset Daewoo ResearchII. [2021 outlook] ③ Inevitable changes for US OEMs

Need for change • Global OEMs plan to release new EV models in the US.

• Considering tax benefits, the US$40,000-60,000 price range looks attractive.

• In particular, Volkswagen’s ID.4 is scheduled to be released in 2H21 with a starting price of US$40,000. We

anticipate strong demand given the attractive pricing (after a US$7,500 tax benefit).

Major EV models scheduled for US release in 2021

Audi Q4 e-tron Volvo XC40 Recharge Nissan Ariya Mercedes-Benz EQA Volkswagen ID.4

Starting price (US$) 65,900 53,990 40,000 50,000 39,995

Driving range (km) 350 320 480 400 400

Battery capacity

95 78 63 60 82

(kWh)

Horse power (hp) 402 402 215 270 302

Maximum speed

124 112 124 124 99

(mph)

0-60mph (s) 5.5 4.7 5.1 5 8.5

Release schedule End-2020 Early 2021 End-2021 End-2021 Early 2021

Source: Press reports, Mirae Asset Daewoo Research

16 | [2021 Outlook] Global EVs Mirae Asset Daewoo ResearchII. [2021 outlook] ③ Inevitable changes for US OEMs

Need for change • US OEMs have been slow to shift to EVs.

• For example, GM’s EV pickup truck will be released later than the Tesla Cybertruck and will have a higher price tag.

• More agile responses are needed.

Tesla Cybertruck vs. GM’s EV pickup truck

Tesla Cybertruck GMC Hummer EV

Model

Dual Motor AWD Tri Motor AWD Edition 1 EV3X EV2X EV2

Starting price

49,900 69,900 112,595 99,995 89,995 79,995

(US$)

Traction force (lbs) 10,000 14,000 11,500 9,500 7,400 7,400

0-60mph (s)II. [2021 outlook] ③ Inevitable changes for US OEMs

Need for change • On Nov. 21, GM announced a plan to expedite its transition to EVs.

• Under the plan, GM will spend US$27bn by 2025 on EV efforts, up from a previous budget of US$20bn; introduce

30 EV models, including small SUVs (priced at less than US$30,000); accelerate the releases of the Hummer EV

and the Lyriq (Cadillac SUV); and improve battery performance. We expect such strategic changes by US OEMs to

benefit Korean battery firms.

• We also note that LG Chem and GM are set to start a battery joint venture (30GWh) in 2023.

LG Chem-GM battery joint venture’s earnings estimates

On Nov. 21, GM announced a plan to accelerate the EV transition

based on GM’s 2025 EV sales mix outlook

Brand Cadillac Case 1 Case 2

Model Lyriq AWD

US car sales '000 units 3,000 3,000

US EV sales '000 units 600 900

EV sales mix % 20 30

Battery capacity (avg.) kWh 80 80

Battery required GWh 48 72

Battery prices US$/kWh 95 95

Segment SUV Revenue US$mn 4,560 6,840

Starting price (US$) 75,000

OP US$mn 456 684

Driving range

480

(km, EPA)

OP margin % 10 10

0-60mph (s) 3

Battery capacity Depreciation US$mn 34 51

100

(kWh)

Dimensions (mm) 4,815 x 1,905 x 1,685 EBITDA US$mn 490 735

Release Pulled forward to early 2022 (from end-2022)

Source: Press reports, Mirae Asset Daewoo Research Source: Mirae Asset Daewoo Research

18 | [2021 Outlook] Global EVs Mirae Asset Daewoo ResearchII. [2021 outlook] ④ Battery innovation to accelerate

4680 battery cells • We expect battery technology innovation and cost reductions to accelerate, spurred by Tesla.

• Tesla has announced plans to cut costs through its 4680 cells, which can hold five times more energy capacity.

Following Tesla’s announcement, Panasonic revealed plans to produce 4680 cells, and a top-tier battery maker

also unveiled a road map for increasing battery size.

• Just as 2170 cells became the industry standard once Tesla introduced them (moving from 1865 cells), we believe

4680 cells will gain wide acceptance, leading to a broad-based decline in cylindrical battery costs.

• The transition to 4680 cells should drive down cylindrical battery costs through pack-related cost savings.

The move from 1865 to 2170 cells led to battery cost savings LG Chem’s battery development road map

Source: Journal of the Electrochemical Society, Mirae Asset Daewoo Research Source: LG Chem, Mirae Asset Daewoo Research

19 | [2021 Outlook] Global EVs Mirae Asset Daewoo ResearchII. [2021 outlook] ④ Battery innovation to accelerate

The return of LFP • Lithium iron phosphate (LFP) batteries are now being used in EVs, driven by advances in cell-to-pack (CTP) and

BMS technology.

batteries

• CATL has begun supplying CTP-based LFP batteries for the Model 3, while the BYD Han offers the same driving

range at 80% of previous battery capacity.

• With their relatively low entry barriers compared to NCM cells, the application of LFP batteries in EVs has

prompted Chinese battery suppliers to begin expanding LFP capacity. China’s Gotion plans to increase capacity

from 28GWh in 2020 to 80GWh in 2023 and 100GWh in 2025.

• The cost per kWh for CTP-based LFP batteries is believed to be more than 20% lower than that for NCM batteries.

If economies of scale are achieved, we could see additional cost declines.

Comparison of BYD’s pure electric SUVs China-based Gotion’s battery capacity expansion plans

(GWh)

Model Tang EV Han EV 120

100

80

Starting price

260 230

(CNY’000) 60

0-100mph (s) 4.4 3.9

Battery capacity

83 65 40

(kWh)

Driving range

500 506

(NEDC, km)

Range per unit 20

6.0 7.8

(km/kWh)

Size (mm) 4870/1950/1725 4980/1910/1495

0

2020F 2023F 2025F

Source: Press reports, Mirae Asset Daewoo Research Source: Industry data, Mirae Asset Daewoo Research

20 | [2021 Outlook] Global EVs Mirae Asset Daewoo ResearchII. [2021 outlook] ④ Battery innovation to accelerate

NCM/NCA camp also • Fueled by Tesla’s market entry and the expansion of LFP battery makers, technology development in the

NCM/NCA camp is also gaining pace.

ramping up response

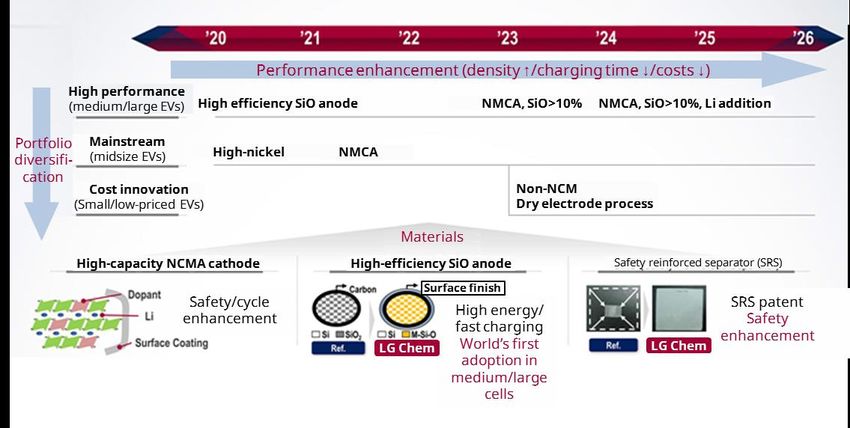

• LG Chem is expected to move forward its application of NCMA batteries, which are anticipated to cut costs of

large pouch cells by more than 20%.

• Samsung SDI also aims to reduce costs by over 20% by introducing large prismatic NCA cells in 2021.

• All in all, we believe battery cost reductions will progress more rapidly than previously expected.

LG Chem’s battery technology development road map

Source: LG Chem, Mirae Asset Daewoo Research

21 | [2021 Outlook] Global EVs Mirae Asset Daewoo ResearchII. [2021 outlook] ⑤ Opportunity in commercial EVs

Commercial EV market to • In 2019, global sales of commercial vehicles, such as buses and trucks, totaled 24.39mn units, representing

roughly 25% of all sales.

be driven by Tesla’s

• Of note, commercial EVs require large-capacity batteries. For that reason, China’s electric buses have essentially

Cybertruck been the only commercial EV market to see growth, thanks to government support.

• However, with battery prices falling and Tesla introducing its Cybertruck, we expect the electrification of

commercial vehicles to gather steam in 2021, led by the US pickup truck market (3mn units annually).

• In 2021, a number of attractive electric pickup trucks besides the Cybertruck are set to be released in the US, such

as Rivian’s R1T.

Major electric trucks set for release in 2021

Manufacturer Rivian Atlis Lordstown Motors

Model R1T launch edition XT Endurance

Starting price (US$) 75,000 45,000 52,500

Towing capacity (lbs) 11,000 10,000 7,500

Power (hp) ≥402 700 600

Driving range (km) ≥480 ≥480 ≥400

0-100km/h (s) 4.9 5.0 NA

Battery capacity (kWh) ≥135 ≥125 109

Release schedule June 2021 2021 Sep. 2021; 50,000 preorders

Source: Press reports, Mirae Asset Daewoo Research

22 | [2021 Outlook] Global EVs Mirae Asset Daewoo ResearchII. [2021 outlook] ⑤ Opportunity in commercial EVs

Demand for NCM/NCA • Electric pickup trucks require large-capacity/high-power batteries ranging from 100kWh to 200kWh (Hummer EV),

because the trucks themselves are heavy and need to drive long distances while carrying freight.

cells to increase

• LFP cells, which are heavier, are unsuitable for electric pickup trucks. CTP-based LFP batteries are still more than

20% heavier per kWh than NCM batteries, meaning battery capacity needs to be even larger. Tesla’s Model Y,

which runs on a 70kWh battery, also relies on NCM batteries because of the cell weight.

• We believe this presents an opportunity for NCM/NCA battery suppliers.

Battery capacity comparison of major EV models Estimated weight of Tesla’s EV models

(GWh) (kg)

300

5000

Curb weight With cargo

4000

200

3000

2000

100

1000

0 0

Tesla Model GM Bolt Tesla Model Cadillac Cybertruck GMC China Model 3 SR+ Model 3 LR Cybertruck Dual Motor AWD

3 SR+ 3 LR Lyriq (est.) Hummer EV electric bus

Source: Press reports, Mirae Asset Daewoo Research Source: Press reports, Mirae Asset Daewoo Research

23 | [2021 Outlook] Global EVs Mirae Asset Daewoo ResearchII. [2021 outlook] ⑥ Upside potential of US ESS market

US ESS market size to • The size of the US energy storage system (ESS) market is forecast to more than triple in 2021 compared to 2020.

more than triple in 2021 • The US is expanding large-scale ESS projects, especially in the West. Residential demand for small-scale ESS is

also growing more rapidly than anticipated. Tesla recently raised its residential ESS prices.

compared to 2020

• In the western part of the US, where the share of renewable energy is increasing, large-scale ESS facilities are

being deployed to address unstable electricity generation. Falling battery prices have made ESS more economical

than gas peaker plants.

• Demand in the residential market is also increasing rapidly amid heightened instability in electricity supply

caused by the increase in natural disasters, such as wildfires and hurricanes.

Tesla recently increased ESS prices, as supply continues to struggle

Wood Mackenzie’s US ESS market forecasts

to keep up with demand

(MW)

8000

Residential

Non-residential

Front of the meter

6000

4000

2000

0

2018 2019 2020E 2021E 2022E 2023E 2024E 2025E

Source: Wood Mackenzie, Mirae Asset Daewoo Research Source: PV Tech, Mirae Asset Daewoo Research

24 | [2021 Outlook] Global EVs Mirae Asset Daewoo ResearchII. [2021 outlook] ⑥ Upside potential of US ESS market

Upside potential • With Biden’s election win, ESS demand growth should accelerate. Biden’s goal of making electricity production

carbon-free by 2035 will likely require expanding annual solar PV installations from 15-20GW to 40-50GW.

• In this regard, we believe that extending the investment tax credit (ITC) for solar power (30%) and legislation on a

stand-alone battery storage ITC will be key.

• In the medium term, ESS demand growth should accelerate as the decline in battery prices accelerates.

• We believe that ESS demand growth in the US presents upside potential to top-tier battery makers’ earnings.

Korean battery companies derive 30-50% of their ESS revenue from the US. Due to the conservative nature of the

electricity-use market, ASP is also high, which bodes well for margins.

Upside potential of US solar PV demand Regional breakdown of LG Chem’s ESS revenue

(GW) US Europe Korea Japan Other

100%

50

40 80%

30

60%

20

40%

10

20%

0

PV demand in 2020 70% 100%

PV demand required to meet 2035 guidance

0%

2019 2020F

Source: Industry data, Mirae Asset Daewoo Research Source: LG Chem, Mirae Asset Daewoo Research

25 | [2021 Outlook] Global EVs Mirae Asset Daewoo ResearchII. [2021 outlook] ⑦ Potential comeback of lithium

Lithium prices at • Lithium prices, after continuously falling amid sagging demand caused by China’s new energy vehicle (NEV)

subsidy cuts in 2019 and the pandemic in 2020, appear to have reached an inflection point.

inflection point

• Indeed, China’s lithium carbonate prices have been rebounding after NEV unit sales returned to YoY growth in

July.

• If the inventory drawdown due to growing demand continues, the rise in prices is likely to be sustained.

China’s monthly NEV unit sales China’s lithium carbonate prices

('000 units)

(CNY/tonne)

200 2019 2020

85,000

75,000

150

65,000

100

55,000

50

45,000

0 35,000

Jan. Feb. Mar. Apr. May Jun. Jul. Aug. Sep. Oct. Nov. Dec. 1/19 3/19 5/19 7/19 9/19 11/19 1/20 3/20 5/20 7/20 9/20 11/20

Source: WIND, Mirae Asset Daewoo Research Source: Fastmarkets, Mirae Asset Daewoo Research

26 | [2021 Outlook] Global EVs Mirae Asset Daewoo ResearchII. [2021 outlook] ⑧ China transitioning to market competition

Arrival of attractive EVs • One of the most notable developments in China’s EV market this year has been consumers purchasing

compelling models at full price.

fueling buyer demand

• Chinese EVs have become much more competitive in terms of performance, battery efficiency, and design.

• Chinese consumers are increasingly buying attractive EVs.

• The country’s EV industry is transitioning into one driven by actual demand rather than subsidies.

• This signals the beginning of a positive cycle between demand and supply.

BYD Han NIO ES6

Source: BYD, Mirae Asset Daewoo Research Source: NIO, Mirae Asset Daewoo Research

27 | [2021 Outlook] Global EVs Mirae Asset Daewoo ResearchII. [2021 outlook] ⑧ China transitioning to market competition

Competitive dynamics • China’s conventional vehicle market is still roughly 10 times the size of its EV market. Reinvesting profits made

from traditional vehicles into EVs is critical.

• Geely generates cash flow from its traditional vehicles and was the first local company to complete a dedicated

EV platform.

• BYD—the no. 1 EV seller among local firms—has achieved vertical integration across core EV parts and is

continuing to roll out compelling new models.

• NIO, which is more focused on premium EVs, counts Tencent as one of its major shareholders and has

successfully positioned itself in a niche market (in terms of price point).

• Guangzhou Automobile Group (GAC) generates cash flow from sales of Toyota/Honda-branded traditional

vehicles and heavily invests in the development of its own EV brand.

China’s EV industry: Positioning map and market size

EVs

Premium EVs

US$4bn

Price war

Affordable-

premium

CNY200-250,000

Upper-mass

CNY150-200,000

Conventional vehicle profits → EV

Upgrade Mass EVs

investments

US$17bn

Mass-market Premium

conventional conventional

Conventional

US$200bn (ICE)

(2019 est. market size)

Source: Mirae Asset Daewoo Research

28 | [2021 Outlook] Global EVs Mirae Asset Daewoo ResearchII. [2021 outlook] ⑧ China transitioning to market competition

Competition in the • Global premium EV makers’ selling prices are likely to come down due to competition, while local EV makers’

selling prices are likely to rise on the rollout of more competitive models.

CNY150,000-250,000 price

• The CNY150,000-250,000 price range is currently a battleground between Tesla, BYD and Xpeng, but global

range to intensify brands like Volkswagen are also expected to enter the space.

• In the long term, we expect Geely and BYD to grab a large share of the mass market, which we believe has the

biggest structural growth potential.

• We project NIO to grow rapidly over the next couple of years, given the company’s positioning in the niche

market that lies between developed market luxury brands and local brands.

Price range of battery EVs by company

(CNY)

900,000

800,000

700,000

600,000

500,000

400,000

300,000

200,000

100,000

0

Hozon

Dongfeng

FAW

Haima

JAC

Xpeng

BAIC

SAIC

GAC

Geely

BYD

Great wall

Chery

Weltmeister

Li Auto

NIO

Tesla

Changan

Source: Mirae Asset Daewoo Research

29 | [2021 Outlook] Global EVs Mirae Asset Daewoo ResearchII. [2021 outlook] ⑧ China transitioning to market competition

Market share forecasts • We expect Tesla and BYD to battle for control of China’s EV market, with Tesla standing out in the

luxury/premium space and BYD in the premium and low/mid-end space.

• GAC (Aion), NIO, SAIC, Great Wall, Xpeng, and Geely look well-positioned to gain market share.

• Volkswagen is likely to aggressively expand its presence in China with the release of the ID.4 and ID.3 (via joint

ventures with SAIC and FAW).

Battery EV M/S by company (Chinese sales)

20% 2018 2019 9M20 2021F

15%

10%

5%

0%

Xpeng

BYD

GM

GAC

BAIC

SAIC

Great Wall

VW

Geely

Renault-

Tesla

NIO

Chery

Weltmeister

Changan

Nissan

Source: MarkLines, Mirae Asset Daewoo Research

30 | [2021 Outlook] Global EVs Mirae Asset Daewoo ResearchII. [2021 outlook] ⑧ China transitioning to market competition

Increasing importance of • Platforms are an essential tool for enhancing EV profit margins and revenue growth. They have the following

benefits:

platforms

• 1) Cost savings (production efficiency, sharing of parts, and R&D cost savings)

• 2) Better performance (power/battery efficiency improvements and software upgrades)

• 3) Shorter development cycle

Current development status of dedicated EV platforms by company

Development status First model release

Geely Unveiled SEA Lynk & Co’s Zero to go on sale in 2021

Under development (to be unveiled in To be unveiled at the 2021 Shanghai

BYD

1H21) Auto Show

MIFA under development + joint Pickup trucks to go on sale in 2021;

SAIC

development with GM Buick Electra concept car unveiled

Three models (SUV and sedans) to be

GAC GEP 3.0 under development

released

Volkswagen Unveiled MEB ID.4 and ID.3 to go on sale in 2021

Source: Mirae Asset Daewoo Research

31 | [2021 Outlook] Global EVs Mirae Asset Daewoo ResearchII. [2021 outlook] ⑧ China transitioning to market competition

Comparison of • Chinese local companies share the common goal of developing Level 3 autonomous cars by 2021, Level 4 by 2023,

and Level 5 by 2025.

autonomous driving

• EVs are optimized for delivering the processing electricity and network connectivity needed to realize

technology; potential for autonomous driving.

business model • Differentiated technology should lead to improvements in EV sales and profit margins.

expansion • Autonomous driving and infotainment packages are likely to emerge as new sources of service income, boosting

margins.

• When autonomous driving is fully realized, vehicles will have evolved into a new type of “mobile IT device.”

Current status of platform development

Level 3 3 (1Q21) 2.5 2 2

Chips Tesla Nvidia Mobileye Mobileye Xilinx

Maps N/A AutoNavi Baidu AutoNavi Baidu

Source: Mirae Asset Daewoo Research

32 | [2021 Outlook] Global EVs Mirae Asset Daewoo ResearchII. [2021 outlook] ⑧ China transitioning to market competition

Major policy measures to China is expected to continue to introduce favorable policy measures to meet its goal of becoming the world’s EV

leader.

speed up conversion to

eco-friendly vehicles

Rules on eco-friendly vehicle conversion rate

• Phasing out of internal combustion engine vehicles from 2035: 50% of all sales to be battery EVs or plug-in hybrid

EVs (PHEVs) and 50% to be hybrid cars

• Sales percentage of battery EVs, PHEVs, and hydrogen fuel-cell cars to be 20% by 2025 (6mn units)

• From 2021, 80% of buses/taxis/trucks deployed in key polluted areas to be eco-friendly vehicles

Infrastructure and technology investments

• Expand charging infrastructure: Lower ratio of NEVs to charging stations from an estimated 2.5 to 1 currently to

around 1 to 1

• Support investments in core technology to make NEVs globally competitive

Internalization of EV supply chain

• Encourage global companies to expand their EV supply chains in China

33 | [2021 Outlook] Global EVs Mirae Asset Daewoo ResearchIII. [Medium-term outlook] Transition to gain pace

Revising up our EV • We revised up our EV penetration rate forecasts for 2025 and 2030 by 3%p and 4%p, respectively, based on the

following rationale:

penetration forecasts

1) Acceleration of battery technology innovation and cost savings, spurred by Tesla and the growing LFP battery

market

2) Acceleration of policy shift, especially in the US

3) Acceleration of EV conversion of major OEMs, with product differentiation to be achieved through dedicated

platforms and autonomous driving technology

Medium-term EV penetration rate and battery price forecasts

(%) EV penetration (previous) EV penetration (new) (US$/kWh)

40 Battery price (previous) Battery price (new) 150

30

120

20

90

10

0 60

20F 25F 30F

Source: Mirae Asset Daewoo Research

34 | [2021 Outlook] Global EVs Mirae Asset Daewoo ResearchⅣ. [Investment strategy] Tesla reshaping the landscape

Maintain Overweight • Despite the rally in 2020, we maintain our positive view on the overall global EV supply chain.

• While expectations have become elevated, we still think the EV market has the potential to grow more rapidly

than anticipated.

• In 2021, we think Tesla’s competitiveness will increase more quickly than current expectations. Traditional OEMs

are also likely to ramp up their EV strategies, which have been somewhat slow to take off.

• Upward revisions to medium/long-term market growth forecasts should lead to multiple expansion across the

supply chain.

Key variables to watch in the 2021 global EV supply chain

- US: Possibility of restoration of tax credits and tightening of emission regulations

Policy - Europe: Possibility of further strengthening of CO2 regulations

- China: 14th five-year plan

- Tesla: Price of Chinese Model Y, in-house battery quality, Cybertruck demand, and FDS

EVs - Acceleration of the EV strategies of global OEMs (particularly US players)

- Potential upward revisions to EV market penetration forecasts

- Re-rating of LG Chem’s energy solution business

Batteries - Quality of Tesla’s batteries and the impact on battery makers’ technology development

- Expansion of the US ESS market and the resulting earnings upside potential

- Multiple expansion fueled by the increasing growth prospects of the EV market

Materials - Potential recovery of lithium prices

Source: Mirae Asset Daewoo Research

35 | [2021 Outlook] Global EVs Mirae Asset Daewoo ResearchV. Global peer valuations

Global EV supply chain players

Market Revenue (Wbn) OP (Wbn) NP (Wbn) P/E (x) P/B (x) ROE (%)

Segment Company Ticker

cap (Wbn) 2020F 2021F 2020F 2021F 2020F 2021F 2020F 2021F 2020F 2021F 2020F 2021F

Tesla TSLA US 516,109 34,161 50,238 2,720 5,295 2,429 4,579 210.9 124.6 29.2 23.5 14.3 21.4

Volkswagen VOW GR 104,157 287,785 316,261 7,673 8,908 5,763 4,292 17.6 7.4 0.7 0.6 3.8 8.5

EVs

NIO NIO US 74,605 2,643 4,940 -821 -516 -839 -470 - - 357.6 - -998.3 - 109.6

BYD 002594 CH 81,361 24,579 29,139 1,246 1,508 705 864 121.3 98.5 8.3 8.9 7.2 7.4

CATL 300750 CH 100,840 8,456 11,560 1,099 1,547 863 1,210 114.9 83.2 10.8 9.6 10.5 12.6

LG Chem 051910 KS 52,732 30,367 37,924 2,396 3,165 1,424 1,993 39.0 27.8 3.1 2.8 8.0 10.3

Samsung SDI 006400 KS 36,239 11,578 14,329 735 1,196 598 1,094 62.4 33.8 2.8 2.6 4.7 8.0

Batteries

Panasonic 6752 JP 28,495 70,231 73,881 1,766 2,874 1,141 1,908 24.1 14.2 1.2 1.2 5.2 8.4

Gotion High-tech 002074 CH 6,509 957 1,204 72 135 53 79 103.8 74.6 3.5 3.5 3.3 3.8

EV Energy 300014 CH 21,858 1,560 2,304 342 506 312 476 57.0 39.3 12.5 9.9 19.4 23.4

Umicore UMI BB 11,649 4,191 4,720 589 741 377 473 30.3 24.8 3.2 3.0 9.9 12.4

POSCO Chemical 003670 KS 4,916 1,600 2,134 65 134 37 108 131.9 47.2 4.6 4.0 3.6 9.3

L&F 066970 KS 1,239 388 622 8 25 4 16 283.4 93.9 6.8 6.3 2.7 7.9

Cathodes

Easpring 300073 CH 3,551 521 807 69 104 59 86 59.4 40.4 6.2 5.3 10.3 13.3

Ecopro BM 247540 KS 3,153 872 1,388 59 107 50 86 63.3 37.6 7.6 6.4 12.6 18.6

Ningbo Shanshan 600884 CH 4,000 1,538 2,004 87 113 59 85 62.8 42.0 1.9 1.9 3.0 4.0

Separators Yunnan 002812 CH 14,964 666 932 221 330 175 264 80.1 54.5 11.4 9.7 17.1 19.7

Iljin Materials 020150 KS 2,089 591 804 61 101 53 81 39.6 25.8 3.4 3.0 8.9 11.8

Elecfoil

Doosan Solus 336370 KS 1,214 475 648 72 99 48 69 28.9 20.5 7.3 5.5 25.4 27.3

Chunbo 278280 KS 1,712 157 252 29 51 25 41 66.1 40.0 7.1 6.0 11.3 16.5

Electrolytes Foosung 093370 KS 894 255 323 9 42 3 31 257.3 28.6 4.2 3.6 1.0 13.7

Guangzhou Tinci 002709 CH 7,364 712 940 135 171 116 140 66.3 54.0 12.8 10.8 20.4 20.5

Albemarle ALB US 15,140 3,393 3,545 602 641 465 481 33.1 31.2 3.2 3.0 9.8 9.8

Metal s SQM SQM/B CI 11,024 2,005 2,363 426 536 227 320 56.1 41.5 5.6 5.4 9.2 13.1

Ganfeng Lithium 002460 CH 16,918 923 1,262 121 277 99 216 165.6 77.8 11.4 10.3 6.9 13.7

Source: Bloomberg, Mirae Asset Daewoo Research

36 | [2021 Outlook] Global EVs Mirae Asset Daewoo ResearchGeely Automobile (175 HK) Top pick

A leading player

Investment points

(Maintain) Buy • Planned listing on the STAR Market and merger with Volvo should help strengthen financials and enhance

product/export competitiveness.

• With its Sustainable Experience Architecture (SEA), Geely Automobile (Geely) became the first Chinese player

to develop a dedicated EV platform (developed in partnership with Volvo).

Target price (HK$, 12M) 35.00

- One or two SEA-based models are scheduled to be launched in 2021; three or four are slated for 2022.

• Geely is displaying strengthening global competitiveness in EVs.

- The Chinese automaker has forged: 1) a joint venture with Daimler for the development of premium EVs and

Current price (11/23/20) 23.40

autonomous vehicles; and 2) battery joint ventures with CATL and LG Chem.

• Geely is expected to deliver the highest ROE among local Chinese players (even after the industry-wide EV

transition is largely completed) and expand net cash holdings.

Expected return 49.6%

• We see high potential for a valuation re-rating as technological (EV)/export competitiveness is increasingly

priced in (target P/E of 30x).

EPS growth (21F, %) 31.1

Catalysts

P/E (21F, x) 25.1

• Listing of shares on the STAR Market to exert upward pressure on valuations; sharp increase in volume for

Market P/E (21F, x) 13.5 Lynk & Co models

Dividend yield (%) 1.1 Risks

Market cap (HK$bn) 228.2

• Uncertainties related to Volvo valuation

(Dec.) 2017 2018 2019 2020F 2021F 2022F

Market cap (Wtr) 32.8

Revenue (CNYmn) 92,761 106,595 97,401 103,388 116,796 132,145

Shares outstanding (mn) 5,736.9 OP (CNYmn) 11,003 13,213 7,462 7,826 9,542 11,324

52-week low (HK$) 10.00 OP margin (%) 11.9 12.4 7.7 7.6 8.2 8.6

NP (CNYmn) 10,634 12,553 8,190 8,233 9,713 11,178

52-week high (HK$) 23.60

EPS (CNY) 1.16 1.37 0.89 0.78 1.02 1.18

(%) 1M 6M 12M ROE (%) 30.9 27.9 15.0 12.3 13.1 13.5

Absolute 39.9 80.8 54.5 P/E (x) 19.0 8.7 15.1 32.9 25.1 21.8

Relative 30.1 67.0 57.2 P/B (x) 5.9 2.4 2.4 3.6 3.3 2.9

Source: Geely Automobile, Bloomberg, Mirae Asset Daewoo Research

37 | [2021 Outlook] Global EVs Mirae Asset Daewoo ResearchGeely Automobile (175 HK)

Strengthening • Geely will likely stay ahead of rivals in terms of cost and technological competitiveness, even after the auto

industry’s transition to EVs is largely completed.

competitiveness in EVs

• The company is set to reap the benefits of joint platform development with Volvo, cost advantages, and mass

and autonomous production on its new EV platform (2021-22).

vehicles • A joint venture with Daimler for the development of premium EVs/autonomous vehicles and a partnership with

Waymo have been forged.

• Geely has established battery joint ventures with CATL and LG Chem (stable supply and cost benefits).

Zhejiang Geely Holding Group: Ownership/partnership structure

Zhejiang Geely Holding & Li Shufu

8.2% 100% 42% 9.7%

AB Volvo Volvo Cars Potential M&A Geely Daimler Waymo

& Volvo

Smart Automobile Partnerships

(joint venture

[Battery joint ventures]

EV platform/autonomous driving technology development

Source: Mirae Asset Daewoo Research

38 | [2021 Outlook] Global EVs Mirae Asset Daewoo ResearchGeely Automobile (175 HK)

Merger with Volvo • The planned merger with Volvo is slated for completion in 1H21.

• The merger, once completed, would enable the firm to: 1) increase scale effects (in production and platform

development); 2) enhance product competitiveness through technological cooperation; and 3) boost export

capabilities.

• The post-merger combined entity will be listed on the Stockholm Stock Exchange, allowing for the expansion of

financing channels in Europe.

Volvo: Valuation overview

Volvo: Equity value estimates

EV/EBIT (2019)

8x 9x 10x 11x 12x 13x 14x

EV 11,706 13,170 14,633 16,096 17,559 19,023 20,486

Net cash 2,836 2,836 2,836 2,836 2,836 2,836 2,836

Equity 14,542 16,006 17,469 18,932 20,396 21,859 23,322

Notes: SEK/CNY = 0.73 (2019 avg.); CNY/USD = 0.14

Source: Mirae Asset Daewoo Research

Volvo and Geely: Sales volume and earnings (2019)

Volvo Geely Pro forma

Vehicle sales (mn units) 694,831 1,361,560 2,056,391

Net revenue (CNYmn) 200,313 97,401 297,714

NP 7,017 8,261 15.279

Net margin 3.5% 8.5% 5.1%

Source: Volvo, company data, Mirae Asset Daewoo Research

39 | [2021 Outlook] Global EVs Mirae Asset Daewoo ResearchGeely Automobile (175 HK)

EV and autonomous • In 2020, Zhejiang Geely Holding and Daimler formed a joint venture named Smart Automobile.

vehicle development via • In February 2018, Zhejiang Geely Holding’s chairman became Daimler’s largest shareholder by acquiring a 9.7%

stake in Daimler for US$9bn (five times the investment in Volvo).

partnership with Daimler

• The purpose of the investment was to secure global competitiveness in EVs and autonomous cars.

Key executives of Smart Automobile (Zhejiang Geely Holding-Daimler joint venture)

Title Company Name Position/role

Director Daimler Hubertus Troska (Current) Responsible for China activities

Britta Seeger (Current) Mercedes-Benz marketing/sales

Markus Schäfer (Current) Mercedes-Benz R&D

Zhejiang Geely Holding Li Shufu (Current) Chairman

(Current) President of Zhejiang Geely Holding

An Conghui

and president and CEO of Geely

(Current) Vice president and CFO of Zhejiang

Daniel Donghui Li

Geely Holding

CEO Smart Automobile Tong Xiangbei (Current) 2015-present

(Former) 1998-2015: Ford (US, China, Asia

Pacific)

Source: Daimler, Mirae Asset Daewoo Research

40 | [2021 Outlook] Global EVs Mirae Asset Daewoo ResearchGeely Automobile (175 HK)

Geely became the first • Geely unveiled SEA, the first dedicated EV platform developed by a Chinese firm, at the Beijing International

Automotive Exhibition 2020 in September.

Chinese firm to unveil

• Going forward, we expect SEA-based models to drive sales volume growth.

an in-house dedicated EV

• Mass production of the Lynk & Co Zero luxury coupe/sedan is set to begin in 2021. (Prices have not been

platform announced yet.)

• The model, which will be equipped with 110kWh CTP batteries, should be capable of traveling more than 700km

(NEDC) on a single charge (120km on a five-minute charge) and sprinting to 100km/h in less than four seconds.

Lynk & Co Zero concept

Source: Lynk & Co, Mirae Asset Daewoo Research

41 | [2021 Outlook] Global EVs Mirae Asset Daewoo ResearchLG Chem (051910 KS) Top pick

EV market growth to accelerate

Investment points

(Maintain) Buy

• We project that EV market growth will outstrip current expectations thanks to Tesla-led battery innovation.

• Global OEMs’ shift to EVs will likely accelerate, particularly in the US; as such, we expect the value of the LG

Target price (12M, W) 1,050,000 Chem-GM joint venture to increase.

• The market for commercial EVs is set to take off, which should benefit NCM batteries (high energy density).

Current price (11/23/20, W) 748,000 • In 2021, we expect the battery business to receive a higher valuation relative to current levels.

Risks

Expected return 40%

• Short-term profit taking could take place given the recent rally.

• If Tesla starts in-house battery production sooner than expected, short-term concerns could take shape.

OP (20F, Wbn) 2,580

Consensus OP (20F, Wbn) 2,493

EPS growth (20F, %) 393.6

P/E (20F, x) 37.9

Market P/E (20F, x) 17.5

KOSPI 2,602.59

Market cap (Wbn) 52,803 270

LG Chem (Dec.) 2017 2018 2019 2020F 2021F 2022F

Shares outstanding (mn) 78 250 KOSPI Revenue (Wbn) 25,698 28,183 28,625 30,536 40,301 49,812

230

Free float (%) 64.3 OP (Wbn) 2,928 2,246 896 2,580 3,321 4,231

210

Foreign ownership (%) 41.7 OP margin (%) 11.4 8.0 3.1 8.4 8.2 8.5

190

Beta (12M) 1.48 NP (Wbn) 1,945 1,473 313 1,547 2,300 2,952

170

52-week low (W) 230,000 150 EPS (W) 24,854 18,812 4,003 19,759 29,377 37,714

52-week high (W) 768,000 130 ROE (%) 12.9 8.9 1.8 8.7 11.8 13.7

(%) 1M 6M 12M 110 P/E (x) 16.3 18.4 79.3 37.9 25.5 19.8

Absolute 15.1 98.4 148.5 90 P/B (x) 1.9 1.6 1.4 3.1 2.8 2.5

70

Relative 4.4 50.2 100.7 Div. yield (%) 1.5 1.7 0.6 0.8 1.1 1.1

19.11 20.1 20.3 20.5 20.7 20.9 20.11

Notes: Under consolidated K-IFRS; NP is attributable to owners of the parent

Source: LG Chem, Mirae Asset Daewoo Research estimates

42 | [2021 Outlook] Global EVs Mirae Asset Daewoo ResearchLG Chem (051910 KS)

Tesla-led changes • EV market growth will likely pick up speed in the medium/long term, fueled by: 1) battery technology innovation;

2) policy shifts in major countries, particularly the US; and 3) major OEMs’ increasing commitment to EVs.

• Since Tesla’s announcement of its plan to produce batteries in-house, established battery suppliers have

accelerated their R&D efforts. Larger cells and nickel-rich cathode materials are likely to be adopted sooner than

expected.

• We believe that the pace of EV penetration will exceed market expectations amid falling battery prices. LG

Chem’s medium-term earnings are likely to exceed its guidance.

Battery price and passenger EV penetration outlook

(%) EV penetration (previous) EV penetration (new) (US$/kWh)

40 Battery price (previous) Battery price (new) 150

30

120

20

90

10

0 60

20F 25F 30F

Source: Mirae Asset Daewoo Research

43 | [2021 Outlook] Global EVs Mirae Asset Daewoo ResearchLG Chem (051910 KS)

Tesla-led changes • Despite their widely publicized plans to focus on EV, global OEMs have been showing relatively slow progress.

• In 2021, however, we expect European OEMs to act with greater urgency, as: 1) the European Commission is

considering tighter CO2 regulations; 2) the EV penetration rate has continued to increase, aided by increased

government subsidies; and 3) Tesla continues to strengthen its competitiveness.

• US OEMs are also likely to pick up the pace, as: 1) the Cybertruck will threaten their hegemony in the pickup truck

market; 2) global OEMs are set to release new EV models in the US; and 3) fuel efficiency standards may be

tightened under the incoming Biden administration.

•

With GM set to ramp up its EV strategy (expedited new model launches, upward sales target revisions, etc.), the

LG Chem-GM joint venture could deliver faster-than-expected earnings growth.

LG Chem-GM joint venture: Earnings estimates based on GM’s 2025 EV

Fuel economy regulations: Obama vs. Trump administrations

sales mix outlook

(mpg) Case 1 Case 2

Obama Trump

60

US car sales '000 units 3,000 3,000

US EV sales '000 units 600 900

50 EV sales mix % 20 30

Battery capacity (avg.) kWh 80 80

Battery required GWh 48 72

40

Battery prices US$/kWh 95 95

Revenue US$mn 4,560 6,840

30 OP US$mn 456 684

OP margin % 10 10

Depreciation US$mn 34 51

20

2020 2025 EBITDA US$mn 490 735

Source: Press reports, Mirae Asset Daewoo Research Source: Mirae Asset Daewoo Research

44 | [2021 Outlook] Global EVs Mirae Asset Daewoo ResearchLG Chem (051910 KS)

Tesla-led changes • The commercial vehicle segment presents a new growth opportunity for the EV industry; in the US, the

Cybertruck is set to usher in the era of electric pickups.

• Electric trucks require huge batteries, as they consume two to four times more energy than EV sedans.

• Accordingly, electric trucks are likely to adopt NCM batteries rather than heavier LFP batteries.

• We think LG Chem, an NCM battery producer, will benefit from the rise of electric trucks.

Battery capacity comparison Tesla: Vehicle weight estimates

(GWh) (kg)

300

5000

Curb weight With cargo

4000

200

3000

2000

100

1000

0 0

Tesla Model GM Bolt Tesla Model Cadillac Cybertruck GMC China Model 3 SR+ Model 3 LR Cybertruck Dual Motor AWD

3 SR+ 3 LR Lyriq (est.) Hummer EV electric bus

Source: Press reports, Mirae Asset Daewoo Research Source: Press reports, Mirae Asset Daewoo Research

45 | [2021 Outlook] Global EVs Mirae Asset Daewoo ResearchLG Chem (051910 KS)

Issue ①: Tesla’s in-house • The market will be able to confirm the quality of Tesla’s mass-produced battery cells sometime in 1H21. Given the

difficulty of mass production, we think the EV maker will continue to cooperate with existing battery suppliers.

battery production

• Even if Tesla is able to successfully mass produce batteries, LG Chem should benefit from the resultant

acceleration in industry-wide innovation and the intensification of global OEMs’ EV initiatives.

• Meanwhile, traditional OEMs’ plans to venture into battery production are unlikely to find success. Unlike Tesla,

most global OEMs are still characterized by heavy technological dependence on battery cell makers and a lack of

economies of scale.

Battery technology has advanced slowly relative to other IT products EV sales volume comparison

(Units)

2019 1-9/20

400,000

300,000

200,000

100,000

0

Tesla BMW Volkswagen Nissan HMC

Source: Battery University, Mirae Asset Daewoo Research Source: SNE Research, Mirae Asset Daewoo Research

46 | [2021 Outlook] Global EVs Mirae Asset Daewoo ResearchLG Chem (051910 KS)

Issue ②: Value of the • We believe that the post-spin-off value of the battery business will be higher than the valuation currently

reflected in LG Chem’s share price, in light of the following factors:

battery business to

1) Accelerating EV market growth should have a positive impact across the battery industry.

expand

2) The unit’s valuation does not appear burdensome relative to CATL’s following the share price pullback

stemming from the spin-off decision.

3) Medium-term earnings estimates are expected to be revised upward, as global automakers’ transition to EVs

has finally started to gain momentum.

4) Battery earnings will likely expand meaningfully from 2022.

LG Chem and CATL: Market cap and net borrowings LG Chem and CATL: Battery business OP (estimates)

(Wbn) (Wbn)

LG Chem CATL LG Chem CATL

120,000 3,000

100,000

80,000 2,000

60,000

40,000 1,000

20,000

0 0

1/19 7/19 1/20 7/20 20F 21F 22F

Source: Bloomberg, Mirae Asset Daewoo Research Source: Bloomberg, Mirae Asset Daewoo Research

47 | [2021 Outlook] Global EVs Mirae Asset Daewoo ResearchLG Chem (051910 KS)

Issue ③: Fire/recall risks • Concerns have grown over the risk of EV battery fires and associated recall expenses. However, we do not think

the recent EV battery fires will be as impactful as the ESS-related fires over the past few years.

• It should be noted that most of Korea’s ESS fires have stemmed from improper operation by small companies

focused on collecting subsidies. We do not see a similar dynamic taking shape in the EV battery space given the

dominant roles of large OEMs with strong reputations.

• Moreover, as recall remedies will mostly involve software updates and/or battery replacement, related costs are

unlikely to be burdensome.

• Risks should ease gradually over the medium term as battery management/operation technology continues to

advance. ESS fires have rarely been reported in developed countries such as the US.

Tesla: No. of fire incidents per driving distance GM reaffirms its EV transition plans despite Bolt recall

(mn miles)

2012-18 2012-19

200

150

100

50

0

Tesla US avg.

Source: Tesla, Mirae Asset Daewoo Research Source: GM, Mirae Asset Daewoo Research

48 | [2021 Outlook] Global EVs Mirae Asset Daewoo ResearchSamsung SDI (006400 KS) Top pick

Set to realize its full potential

Investment points

(Maintain) Buy

• Cylindrical EV cell demand from new customers (Rivian and Tesla) should expand meaningfully.

• We expect to see a more aggressive order-taking strategy over the medium to long term (with intake related

Target price (12M, W) 690,000 to Hyundai Motor Group’s E-GMP platform and Volkswagen’s MPE platform).

• Samsung SDI enjoys several options for funding medium/long-term investments, including the utilization of

Current price (11/23/20, W) 526,000 treasury stock and stake disposals.

• Production costs should fall rapidly with the mass production of 5G EV batteries in 2H21.

Expected return 31%

Risks

• Provisioning related to EV recalls

• Competition from battery-manufacturing automakers

OP (20F, Wbn) 770

Consensus OP (20F, Wbn) 738

EPS growth (20F, %) 48.7

P/E (20F, x) 69.8

Market P/E (20F, x) 17.5

KOSPI 2,602.59

Market cap (Wbn) 36,170 250

Samsung SDI (Dec.) 2017 2018 2019 2020F 2021F 2022F

Shares outstanding (mn) 70 230 KOSPI Revenue (Wbn) 6,347 9,158 10,097 11,818 15,178 19,387

Free float (%) 73.3 210 OP (Wbn) 117 715 462 770 1,310 1,685

Foreign ownership (%) 43.7 190 OP margin (%) 1.8 7.8 4.6 6.5 8.6 8.7

1.36 170

Beta (12M) NP (Wbn) 657 701 357 530 953 1,286

150

52-week low (W) 183,000 EPS (W) 9,338 9,962 5,066 7,534 13,543 18,278

130

52-week high (W) 533,000 ROE (%) 6.0 6.0 2.9 4.2 7.2 9.0

110

(%) 1M 6M 12M P/E (x) 21.9 22.0 46.6 69.8 38.8 28.8

90

Absolute 23.9 56.5 123.4 P/B (x) 1.2 1.3 1.3 2.8 2.6 2.4

70

Relative 12.4 18.5 80.4 19.11 20.1 20.3 20.5 20.7 20.9 20.11 Div. yield (%) 0.5 0.5 0.4 0.2 0.2 0.2

Notes: Under consolidated K-IFRS; NP is attributable to owners of the parent

Source: Samsung SDI, Mirae Asset Daewoo Research estimates

49 | [2021 Outlook] Global EVs Mirae Asset Daewoo ResearchYou can also read