Investor Day 2021 Cerved Group - March 26, 2021 - Cerved Company

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Investor Day 2021 Cerved Group March 26, 2021

Agenda

1. Introduction by the Chairman (G. De Bernardis – Executive Chairman)

2. Cerved investment case (A. Mignanelli - CEO)

3. Cerved for Italy (A. Mignanelli - CEO)

4. Data intelligence (A. Mignanelli - CEO)

− Offering

− Channels

5. Credit management (A. Mignanelli - CEO)

6. Talents, technology, sustainability (A. Mignanelli – CEO)

7. Financials & strategic outlook 2021-2023 (E. Bona – CFO)

A brief overview of Cerved’s history

Institutional ownership Private equity ownership Public ownership

1974 2009 2014 2021

SPIN-OFF SECOND LBO

100% FREE

BY INFOCAMERE FLOAT

Italian banks Public company

INCEPTION FIRST LBO IPO TODAY

1995 2013 2015

Cerved history and governance reinforce its institutional role and fully independent positioning 3

A success story documented by our 1st and 2nd Investor Days

Since its IPO in June 2014 Cerved has been a success story of resilience, growth and cash

flow resulting in its shares almost doubling over the period

1 s t an d 2 nd

I n v e stor D a y s

in 2016 and 2018

2020 Revenues €488m, +47% from 2014 Share price +86% since June 2014 IPO of €5,1

2020 Adj. EBITDA €204m, +27% from 2014 €242m dividends paid out 2015-2019

4

Now gearing up for the next phase with our 3rd Investor Day

Cerved is setting its strategy and financial targets until 2023, with a refocus on Data

Intelligence, and an ambitious set of targets for the medium term

3 r d I n v e s tor D a y

2 6 M a rch 2 0 2 1

a Post Covid recovery outlook

a Strategic refocus on data business

a Focus on organization and execution

5

Assessing strategic alternatives for Credit Management to refocus on DAT

Credit Management has been an Refocus on the core Data Additional firepower to create

outstanding success story for Intelligence businesses, capitalising shareholder value via M&A and

Cerved since 2011 unique market and competitive dividend strategies in line with

strengths track record

The performance of Credit Since mid-2018 Cerved has The disposal would create

Management has been been assessing strategic Italy’s leading player in DAT

strong since the IPO, options for the Credit benefiting from outstanding

c r e a t i n g t h e 2 nd l a r g e s t Management division in cash generation capabilities

Italian player and order to focus on Data, at the service of M&A and

multiplying revenues, Te c h n o l o g i e s a n d A n a l y t i c s dividend policies

EBITDA and AUM by 3x-4x

CM 2014

2014 2020

2020 x x

Cerved Since IPO

Revenues €m 53,3 152,3 2,9x M&A Deals 18

Adj. EBITDA €m 11,2 46,8 4,2x M&A Cash Outflow €m 288

Adj. EBITDA margin 21% 31% Dividends & Buybacks €m 272

AUM €bn 10,3 41,7 4,0x Dividend Yield 2015-2019 3,5%

6

With sustainability at the core to protect from risk and to grow

IDENTITY OFFERING

Our Purpose

We help the country to protect

We help the country to protect

itself from risk and to grow in a ESG ESG

itself from risk and to grow in a commitment solutions

sustainable way

sustainable way

We do it by putting data, technology Client 100%

We do it by putting data, technology Public

and talent at the service of people, satisfaction company

and talent at the service of people,

businesses, banks and institutions

businesses, banks and institutions

People &

talent

7

Prospected voluntary public tender offer

Cerved Group SpA received a prospective voluntary tender offer from Castor Srl on 8 March 2021

The offer was unsolicited and unexpected

The Board of Directors is currently evaluating the relevant terms and conditions of the offer

It will provide all the information useful for the Company’s shareholders to properly evaluate the offer under the

Statement of the Board of Directors to be published by the trading day before the beginning of the tender period

UBS and Mediobanca have been appointed as financial advisers as well as BonelliErede and Carbonetti as legal advisers

Determinations on distribution of part of available reserves

The conditions of the offer explicitly refer to the absence of distribution of reserves and extraordinary dividends

Therefore the Board of Directors took the view that a different determination in this respect could have immediately

resulted in an interference in the execution of the Offer or in the termination of the effectiveness of the Offer and, in

any event, in a possible decrease in the price of the Offer

The Board of Directors will evaluate the opportunity to propose to distribute part of the available reserves over the

next few months, taking into account the scenario and the outcome of the offer

Impact of the offer on Cerved’s day-to-day business activities

No adverse affect Cerved’s day-to-day business activities

The Board of Directors and management are conducting the business in the ordinary course, in the best interest of

Cerved, its shareholders and stakeholders and with the utmost attention for, and in strict compliance with, applicable

laws and regulations

8

Prospected voluntary public tender offer (continued)

Extraordinary transactions at subsidiaries’ level – Credit Management division

The Board of Directors has not yet assumed any final decision on the potential sale of the Credit Management division

The Company has already commented on the rumors (press release dated 7 March 2021)

The Company will provide any update in accordance with the applicable laws and regulations

Publication of the Strategic Outlook 2021-2023

The Strategic Outlook 2021-2023 represents the outcome of a process started before the launch of the offer

The date of the Investor Day was announced with the 2020 preliminary results on February 2021

Therefore, it could not be in any way intended as an act to hinder or undermine the offer

The Strategic Outlook 2021-2023 does not factorize any potential tender offer and change in the ownership

structure of Cerved

Today’s focus is on the Cerved Group stand-alone without any consideration nor impact from the prospected voluntary public

tender offer

In this respect the Q&A session will not address any questions related to such voluntary public tender offer

9

Agenda

1. Introduction by the Chairman (G. De Bernardis – Executive Chairman)

2. Cerved investment case (A. Mignanelli - CEO)

3. Cerved for Italy (A. Mignanelli - CEO)

4. Data intelligence (A. Mignanelli - CEO)

− Offering

− Channels

5. Credit management (A. Mignanelli - CEO)

6. Talents, technology, sustainability (A. Mignanelli – CEO)

7. Financials & strategic outlook 2021-2023 (E. Bona – CFO)Market leader in Italy in Data Intelligence

Data intelligence Credit management

Risk intelligence Marketing intelligence

Credit risk Market & sales intelligence Banking UTP & NPL

Credit & ESG Ratings Digital marketing Corporate receivables

Real estate Advanced analytics Credit operations

Regulatory & compliance Legal services

Revenues 2020: €274.3m Adi. EBITDA: €139.2m Revenues 2020: €59.7m Adi. EBITDA: €16.1m Revenues 2020: €152.3m Adi. EBITDA: €46.8m

Cagr 14–19: +1.4% Adj. EBITDA %: 50.7% Cagr 14–19: + 28.3% Adj. EBITDA %: + 27.0% Cagr 14–19: + 28.3% Adj. EBITDA %: 30.7%

Customer Customer Customer

% of Sales Mkt share % of Sales Mkt share % of Sales Mkt share

satisfaction satisfaction satisfaction

56% >37% 92% 12%Cerved is a public company with a consistent track record of results

Not restated

Revenues (€m) Adj. EBITDA (€m) IFRS 9, 15, 16

CAGR +9.5% -6.3% CAGR +8.1% 14.0%

458 521 4881 2 2132 237 204

331 353 377 394 160 171 180 186

2014 2015 2016 2017 2018 2019 2020 2014 2015 2016 2017 2018 2019 2020

Note: 1) Includes €1.5m of capital gain deriving from the sale of the Turin real estate property Note: 2)2017 and 2018 restated; 2017 Adj. EBITDA includes €4.0m adjustment for IFRS 16

Operating cash flow (€m) Revenues vs. GDP

IPO CV19 CAGR YoY

CAGR +4.3% -12.4% Subprime crisis Sovereign ‘08-’19 ‘19-’20

Financialcollapse debt crisis

Revenues + 7.2% (6.3)%

126 136 144 143 160 158 139

Italian GDP3 (0.3)% (8,9)%

2014 2015 2016 2017 2018 2019 2020 08 09 10 11 12 13 14 15 16 17 18 19 20

Div. Yield 4.4% 3.6% 3.4% 2.8% 3.3%

Note: 3) Italian GDP (volume change - linked to reference year 2015). Source: ISTAT, Mar-21

Resilient business model with a balanced mix of a-cyclical, cyclical and anti-cyclical components 12Bolt-on M&A has always had a key role in Cerved’s strategy

Cerved has a consolidated track record in delivering accretive M&A transactions in its core business areas as

well as in adjacencies

Since IPO:

#19 deals in 7 years

>230 €m acquisitions in terms of enterprise value

(NPL servicing platform)

(joint venture)

(NPL servicing platform)

(NPL servicing

(NPL servicing platform) platform)

CPS

50% 100% 100% 51% 100% 100% 100%

2014 13 2015 2016 2017 2018 2019 2020

#3 #1 #4 #1 #5 #4 #2

13ESG identity and enabler for Italian sustainability transition

ESG identity in line with best practice ESG offering: enabler for the Italian sustainability transition

Strong Foster transparency in the system with

commitment Independent ESG ratings and assessment

Supply chain ESG platform

Top quality ratings

ESG targets in STI Help companies to change Share ESG landscape

in a positive and sustainable view and understanding

Clear roadmap way

ESG ratings on Cerved

Top management

remuneration linked to

ESG targets reflecting

selected SDGs

14Attractive investment case

Best practice public company Unique data set and technologies

A public company with top quality Unique data ecosystem

investor base 6 1 Proprietary scores & algorithms

Best in class corporate governance State-of-the-arts technologies to manage

and analyse data

M&A track record Growth opportunities in data & analytics

5 2

Consolidated track record in accretive M&A Evolve towards new types of

Focus on both core business and adjacencies Risk Intelligence

Ample firepower from capital structure Surf the fast growing Marketing

Intelligence wave

4 3

Strong cash flows and returns Favorable macro trends

Solid capital structure, consistently in the 3x area Cerved positioned to capture favourable

Strong and resilient cash conversion megatrends and macrotrends

Dividend yield has averaged at 3.5% from 2015 to ESG themes moving to the top of the

2019 agenda

151

Unique data ecosystem

Official Chambers of Commerce data Other official data

Financial statements Chamber of Commerce Insolv. proceedings Real Estate Detrimental acts Ownership Workers &

19,9m – from 1984 reports 2,7m (bankruptcy, ❨Registry❨ ❨Registry❨ ❨CONSOB❨ employees

15,1m valid reports liquidation…) 123m real estate 0,9m valid records Owners and shares ❨INPS❨

registered, >95% associated with 774K related to limited 4,9m companies with

National coverage subjects companies # of workers, job

Protests Ownership Corporate members (estimate) detail and type of

0,65m valid ID records 10,8m list owners report 11m owners and managers links

contract

Proprietary data Open data

PayLine Territorial data Beneficial owners Public tenders Public financing Government aid

63m payment experiences on 2,3m +2k Data & Concentration Index 3,8m beneficial owners Opened, closed, winners: 19,6m 1,1m European national register

companies based on Census cells (until 17° level of analysis) (ANAC) and 370K Italian 2,2m aid in 2020

Industries Unregistered Relationships Company groups ISTAT & BANKIT Public Administration Start-up register

32% of Italian economic activities 152m between all 256K Italian groups Statistical (134 variables) and 21,2K public entities and 14,8K (Infocamere)

companies revised (2,2 m) economics subject financial analysis subsidiaries 10K registered start-ups

Web and social data Clients

Partnerships

News Corporate websites Web pages

70K analyzed daily 1,2m Italian corporate websites 500m analyzed weekly Experian Real estate appraisal

Credit Bureau 100K appraisals in 2020 (400K in

the last 5 years)

Enrichment

Social feeds Corporate social pages with

90K analyzed daily 750K social references Client’s data

> 40 years of time series and + 600k business rules to qualify and correlate the dataset 16Cerved’s proprietary scores are the market benchmarks

The biggest data graph in Italy

Proprietary scores & algorithms providing deep connections among

Cerved Group companies, people and real estate

Benchmark credit risk score available on 3 million companies

Score (CGS)

Credit rating Certified ECAI & Rating Tool for solicited and unsolicited ratings

11 million

ESG rating Proprietary methodology to assign ESG ratings and scorres people 8 million

Environmental companies1

Proprietary score based on hydrogeological data of the territory

risk score

Payline score Proprietary payment bureau tracking 63m payment experiences

Open banking

AI-based risk score on SMEs & Individuals via checking account data

(PSD2) score

Collection score Algorithms that assess and prioritize collection of credit portfolios

Real Estate

Proprietary automated valuation model to assess Real Estate values

valuation model

Anti-fraud Score Graph-technology powered score integrated with Credit Bureau 152 million

123 million real

relationships

Growth Score Proprietary score using inter alia companies digital capabilities estate assets

ECAI = External Credit Assessment Institutions; AI = Artificial Intelligence

Note: 1) Including 2,2 Mln Unregistred economics activities

17Natural Language Processing

State-of-the-art technologies

Insight

Graph database: tool for the analysis and Natural language processing concerns the

Data representation of relationships between querying of databases and returning of

visualisation individuals and companies generated results in visual format

Cognitive

ergonomics

Cyber security & encryption: algorithms Blockchain to improve 100% GDPR and

Data usability service design

based on cutting edge methodologies and «notarization» processes compliant

& security Multi Factor Authentication architecture applied to

company’s

processes and

Semantic Platform products

Artificial Intelligence: comprehensive application which exploits

text with >100

Machine & Deep Learning algorithms and technologies (i.e.

Data analytics xgboost, neural network, tensorflow) for data elaboration and analytics APIs

decision-making processes engine to

extract Digital

value from Invoicing

>1.1 >1.000 600m >EUR 40m Data lake algorithms

non

PetaByte Servers events data partitions to read and

Data lake of stored (physical monitored purchased for clients

structured

data certify

data and virtual) annually every year invoices

Raw data Technology Business

API = Application Programming Interface 18Strategy evolution

European

DAT player

Growth path

repositioning Export data intelligence technology,

platforms and algorithms

Diversify the product offering

towards Risk Intelligence and Evolve product offering and IT

Marketing Intelligence architecture to fully move into ‘‘Data

as a Service’’ model

Performance Expand the customer base by number

excellence and segments (Small & Micro

business)

Achieved strong growth in Credit Develop selective international

Management presence

Defended market share and Divest from Credit Management and

profitability on Credit Info refocus resources on Data Intelligence

Acquired new technology and skills to

play in fast growing markets

2014 - 2020 2021 - 2023 2024 - onwards

DAT = Data, Analytics and Technologies 19Cerved strategy

Business strategy M&A strategy

Business

units Risk Marketing

Intelligence Intelligence

Market

segments

- DAT accretive -

Financial

Institutions UPSELL CROSS-SELL - SW driven -

ESG Market Intelligence

Corporate Regulatory/AML Sales Intelligence

TOP/Large - European focus -

Corporate

EXPAND Assessing exit options for

More medium clients Credit Management

SMEs/Micro

Enter small clients segment

DAT = Data, Analytics and Technologies; SW = Software 20Offering evolution

From Risk Management Growth Services

To Risk Intelligence Marketing Intelligence

Move from credit risk to other types of Leverage a unique data ecosystem to boost

risk intelligence: marketing intelligence:

Business

Anti-Money Laundering Market & Sales Intelligence

unit

strategy Anti-fraud Digital Marketing

Regulatory risk Advanced Analytics

Real Estate risk

ESG risk

Data

Analytics

Technologies

21Channels evolution

Financial institutions Corporates

Large

Advisery/ Multi-specialist

Productive external

Medium network

Small Phygital

22Data Intelligence growth strategy

Business unit Service lines

Historical positioning

Recent development

EXPAND

Customer base with dedicated offering and

Target positioning

go-to-market

Credit Risk

RISK INTELLIGENCE Credit & ESG ratings UPSELL

Real Estate Non credit risk services

leveraging BI leadership

Reg & Compliance

Market Intelligence

MARKETING Sales Intelligence X-SELL

INTELLIGENCE Digital Marketing Exploiting scalable and

modular based platforms

Advanced Analytics

Banking UTP & NPLs

CREDIT Corporate Receivables Leverage high performance

organization and diversified

MANAGEMENT Legal Services business model

Credit Operations

LARGE MEDIUM SMALL

BI = Business Information 23M&A strategy

From.. …to …to

Both Data Intelligence and Credit Focus on Data Intelligence: data, analytics and technology-

Management driven in adjacent segments

Only Italy Mainly Italy with gradual expansion in other

European countries

Low multiples and growing in line with Higher multiples growing faster than core business

core business

24Ready for a new season of high quality M&A and international expansion

Client needs Rationale for Cerved

Entry point to deliver Cerved offering to small

businesses

ERP New data sources for credit monitoring and

Attributes of M&A targets marketing insights

DAT Increase high quality Risk & Expand current sales intelligence platform

Marketing data and analytics to Sales Access to new market / new data (e.g.,

accretive

exploit synergies with current georgraphy and alternative data)

+ data set

Increase analytical power of current

Software Invest in scalable platforms for Procurement procurement platorms with Cerved DAT

driven complementary / adjacent use cases Entry point for «supply chain finance» solutions

+ Reg &

Completing Cerved KYC/digital onboarding

Expand from “Italy Only” to offering

European Compliance Leveraging on PSD2/open banking capabilities

European corporate development

focus strategy (detailed in the

following slide) Entering the fast growing digital learning

market

Getting ready for a new season of high Learning Increasing penetration of smaller customer

quality and high value added M&A segment

DAT = Data, Analytics and Technologies; ERP = Enterprise Resource Planning 25International corporate development: execution guidelines

Expand the most exportable & distinctive businesses / technologies

Objectives

Quickly and profitably enter as many EU countries as possible

Service line to grow internationally Guidelines

Credit Ratings #1 ECAI provider Light distribution and delivery model

Intelligence

No champions in EU for SMEs

Exportable (ESMA) License & Methodology Progressive expansion country by country,

Risk

with a clear roadmap

ESG Fast-growing & fragmented market

Ratings

Exportable Methodology Comprehensive data model and data sourcing

strategy for service lines simultaneous

expansion

Sales #1 in ITA

Define a country-specific entry strategy

Intelligence

Intelligence No champions in EU

Marketing

Scalable platform and technologies

Organic vs. M&A (based on opportunities

Market available)

Intelligence Pull from Sales Intelligence (Atoka)

Scalable platform and technologies Data sourcing maps

ECAI = External Credit Assessment Institutions; ESMA = European Securities and Markets Authority 26Strategic outlook 2021-2023

Guidance

Risk Intelligence Low single digit

Corporates: Mid single digit - Financial Institutions: Stable

Divisional organic

revenues Marketing Intelligence Low double digit

(CAGR’20-’23)

Total Data Intelligence Mid single digit

Credit Management High single digit

Revenues 5% - 7%

Consolidated

organic growth Adjusted EBITDA 5% - 7%

(CAGR’20-’23)

Operating Cash Flows 75%-80% cash conversion by 2023

Growth from M&A Adjusted EBITDA

(CAGR’20-’23) 2.0% - 3.5%

from bolt-on M&A

Consolidated organic + Total Adjusted EBITDA 7.0% - 10.5%

M&A growth

(CAGR ’20-’23)

Leverage Target Long-term target of 3.0x Adjusted EBITDA, save for M&A and non-recurring events

Capital Structure Dividend equal to 40%-50% payout of consolidated profits, coupled with variable

Dividend Policy additional dividend/ buybacks, subject to M&A

27Agenda

1. Introduction by the Chairman (G. De Bernardis – Executive Chairman)

2. Cerved investment case (A. Mignanelli - CEO)

3. Cerved for Italy (A. Mignanelli - CEO)

4. Data intelligence (A. Mignanelli - CEO)

− Offering

− Channels

5. Credit management (A. Mignanelli - CEO)

6. Talents, technology, sustainability (A. Mignanelli – CEO)

7. Financials & strategic outlook 2021-2023 (E. Bona – CFO)Our purpose

We help the country to protect itself from

risk and to grow sustainably

We do it by putting data, technology and talent at the service of

people, businesses, banks and institutionsCerved is the reference point for institutions on the Italian economy

We watch the economy from a vantage point Our customers

Rating Agency certified 95% Primary

by ESMA A+ of Italian institutions

Banks using our data Key observer on SMEs for

periodic consultations provided

by article IV (Country

The most comprehensive dataset Surveillance)

on Italian companies, stakeholders

and real estate assets

30k

companies1

Provider of data on

bankruptcy procedures

The biggest Payments Bureau and companies’ Provider of synthetic indicator of

in Italy (Payline) payment periods the risk faced by companies

and FIs

+150 Provider of data on

The biggest independent NPL Public bankruptcy procedures and

Authorities companies’ payment periods

service provider in Italy

ESMA = European Securities and Markets Authority 30

Note: 1) Including Micro companies with purchases on Cervedirect.comCapability of capturing favourable megatrends and macrotrends

TREND

Digital Green Finance & Structural

transition transition new normal reforms

Post-Covid restructuring Italy needs structural reforms to

Zero CO2 emission in EU in

Increase in use of data corporate sector boost growth

2050

DRIVER

Technology trends in AI & ML NPE increase and a larger Many structural reforms

Green finance & green

45€bn from Recovery Fund regulation European market favourable to Cerved:

Reforms to boost the digital 209€bn from the Recovery Bankruptcy reform

Customer preferences

transition Fund Digitalisation of courts

67€bn from the Recovery Fund Institutional investments in SMEs

IMPACT

Cerved is an enabler of SMEs Cerved ESG scores and ratings Cerved can support banks and Structural reforms expected in

digital capabilities and expected to be widely used by institutions to address finance Italy to boost growth for

strongly benefits from firms’ SME, corporations, banks and towards the most productive Cerved and open markets in

digitalization institutional investors firms and to dispose of NPE which Cerved is a key player

AI = Artificial Intelligence; ML = Machine Learning; NPE = Non Performing Exposures 31Digital Green Finance & Structural

transition transition New Normal reforms

Digital & green transitions

Higher digitalization of Italian firms can boost Cerved market ESG tools expected to be widely used in the Italian economy and

penetration and growth sustainability is part of the Cerved strategy

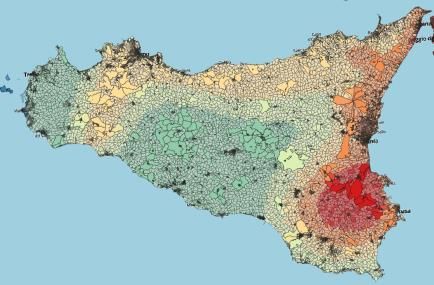

Cerved mkt penetration by companies’ Digital Score1 by size Average probability of default by ESG score Seismic hazard map of Sicily

Cerved On 200 Italian firms with non financial report expected earthquake intensity in 50 years

Digital Score penetration 43%

low 1,0%

32%

medium 5,1% 26% 3.37%

high 9,5% 19% 2.35%

16%

10% 10% 1.15%

7%

1% 2% 3%

0%

ESG ESG low ESG medium ESG high

micro small medium large score (65.64)

Recovery Fund and technology trends expected to strongly increase Boom in green finance and forthcoming regulation: tools to

the digital capabilities of Italian firms measure ESG performance needed

45€bn from Recovery Fund 67€bn from Recovery Fund

Cerved matches PA goals and digitalized firms in Industry 4.0 like New opportunities in adjacent markets (carbon credit register,

incentive schemes (subsidized finance solutions) white certifications, etc.)

A digital academy to support digitalization of SMEs and PA

Cerved becoming the enabler of the Italian digital transition leveraging on Cerved ESG scores, ratings and tools expected to be mission

its comprehensive offering covering the whole Mktg Intelligence cycle critical for SME, corporations, banks and institutional investors

PA = Public Administration

Note: 1) Digital score is a Cerved proprietary score based on machine learning information used to estimate the digital capability of Italian firms;

32Digital Green Finance & Structural

transition transition New Normal reforms

New normal & structural reforms

In the new normal Cerved will support financial institutions to address Structural reforms open markets in which Cerved is a key player

finance to the most productive firms

How to address public intervention in finance: # of firms with public guarantees from the

Fondo Centrale di Garanzia, pre- and post- Covid

Digital public services index1

post-Covid default risk 16 IT

Safe Vulnerable Risky 14 €11,5bn for digital

pre-Covid default risk

12 transformation in

308k 182k 9.3k

Safe

safe impacted impacted

10 Public Administration

8 can help Cerved

284k 181k 6

Vulnerable

non-impacted zombie light increase market

4

2 penetration in PA

81k

Risky 0

zombie

Cerved can support the government to select zombie firms and

economic sustainable firms

Draghi G30 report: finance economic viable firms with equity and/or Bankruptcy reform will incentive credit-risk forward looking

lending, let zombies out of the market methodologies among SMEs

Forthcoming €209bn from Recovery Fund open opportunities in EBA guidelines on LOM (Loan Origination and Monitoring) requires

subsidized finance banks to implement forward looking analyses

60-100bn of NPE expected as a consequence of Covid-19 also

following calendar provisioning and stricter regulation

Cerved information key to support policy makers and banks to Cerved solutions in bankruptcy reform coherent with LOM supporting

address finance to the most productive firms both SMEs and banks (Fw, Alert System, Treasury Management Tool)

PA = Public Administration; EBA = European Banking Authority; FW = Forward Looking

Source: 1) Digital Economy and Society Index (DESI) - European Commission file:///C:/Users/cg12612/Desktop/DESI2020Thematicchapters-Digitalpublicservices.pdf 33Agenda

1. Introduction by the Chairman (G. De Bernardis – Executive Chairman)

2. Cerved investment case (A. Mignanelli - CEO)

3. Cerved for Italy (A. Mignanelli - CEO)

4. Data intelligence (A. Mignanelli - CEO)

− Offering

− Channels

5. Credit management (A. Mignanelli - CEO)

6. Talents, technology, sustainability (A. Mignanelli – CEO)

7. Financials & strategic outlook 2021-2023 (E. Bona – CFO)Offering evolution – Data intelligence

Next slides focus

From Risk Management Growth Services

To Risk Intelligence Marketing Intelligence

Move from credit risk to other types of Leverage a unique data ecosystem to boost

Business risk intelligence: marketing intelligence:

unit

Anti-money laundering Market & sales intelligence

strategy

Anti-fraud Digital marketing

Regulatory risk Advanced analytics

Real estate risk

ESG risk

Data

Analytics

Technologies

35The Risk Intelligence market includes fast growing adjacent segments

Target markets (€m) & Cerved market share Market trends

€bn

CAGR Stable trends in Credit Information:

+17% ‒ Pressure on pricing on standard products

CAGR 1.8 ‒ Increased attention on risk management due to

+6% CAGR higher uncertainty post Covid19

20-23E

1.1 1.1 ‒ Evolution of credit risk assessment logic

1.0 1.0

+34% ‒ Digitalization of products and better UX

0.3 0.4 0.4

Strong growth in Adjacent Risks:

0.7 0.8 0.7 0.8 +2%

‒ Open banking, although early stage

2017 ‒ Higher money laundering & frauds risks due to

2019 2020 2023E

Credit info Adjacent risks

increasing digital interactions

‒ State higher activism with stronger regulations

Cerved mkt share 2019 >37% (e.g. for SMEs)

Source: Cerved Analysis 36Risk Intelligence: low single digit growth expected from 2021 to 2023

Service line Historical trends

2017 2018 2019 2020 CAGR YOY

Revenues (€m) 17-19 19-20 Overall stable performance from 2017 to

90 88 2020, with contraction of Credit Risk

FIs

83 86 -4% 4%

Credit Risk1

segment

A

Corp 143 145 149 Strong Covid-19 impact on Credit Risk for

134 2% -10%

corporate clients in 2020

+

Credit & 7 8 8 8 Growth in Regulatory & Compliance

B ESG Rating 1% 10% benefiting from cross-selling

+ Outlook 2021-2023

Real

C

Estate 35 40 40 32 7% Low single digit growth

-21%

+ Managing pricing pressure by delivering

Reg & 15

D 5 high value services

Compliance 1 2 163% 202%

= Product development on new risks

Risk Products & platforms for medium and

Intelligence 282 284 1.4% -3.5%

276 274 small clients

Note: 1) Credit Risk includes Business Information & Risk Analytics 37A

Credit Risk: market leader with numerous growth opportunities

Business Information Risk Analytics Growth drivers

Business Information platforms Score development Pressure on pricing of data proving and

Cerved Credit Suite for CeBi Convention (standard for

Product

corporates banks’ financial data

standard reports

Silos platform for banks reclassification)

Customized solutions w/APIs Risk analytics consulting

Increased appetite for risk management

products prompted by higher

transactions uncertainty

Unique data ecosystem Market standard products for

Product development to address

Competitive

advantage

Leading technology and credit assessment services

industrialized operations enabling Embedded within bank credit changes in customer needs

market leading SLAs processes

Capabilities c. 200+ analysts, Capabilities of c. 20+ data Regulatory push towards credit risk re-

marketing, product specialists scientists design to integrate forward looking

metrics and alternative data (e.g., PSD2)

Financial Institutions Corporates and Artificial Intelligence

Market. share

Market

High customer penetration and lock-in

>80% 5-7x RMS >45% through risk projects for top clients

2.5x RMS

leveraging data scientists (CeBi) and MBS

API = Application Programming Interface; SLAs = Service Level Agreement (equal to 99.77% uptime for Cerved Credit Suite and 99.96% uptime for Silos); AI = Artificial Intelligence; RMS = Relative Market Share

Source: Cerved analysis

38A

Unique installed base of platforms for credit risk management

Financial institutions Corporates

SILOS CERVED Portfolio analysis

CREDIT CREDIT

DESK SUITE Payment Bureau

16k clients

C Management

Portfolio

600 clients c.50% market

>80% market share share

Full set of platforms to support the entire

credit process Collection Services

Specialized vertical platforms for financial

Decisioning

and sector deep analysis

Best-in-class platform to support commercial credit process

Complete integrated monitoring service on

MONDO any credit position changes 63m payment experiences on 2,5m companies

PAYLINE

Daily checks capturing any changes in Proprietary database and real-time delivery

directors, rating, financial statements, etc.

Data

Analytics

Technologies

39B

Credit & ESG: the leading Italian rating agency with an ESG angle

Credit ratings ESG Solutions Growth drivers

Solicited Ratings ESG Rating and Assessment

Unsolicited Ratings ESG External Reviews

• Italian market of more than 1mln of SMEs1

Product

ECAI Rating Supply Chain ESG Platform in need of credit and ESG ratings for

Research Research accessing sustainable and/or government

guaranteed instruments

• Cross-selling opportunity on solicited

Largest SME Corporate Credit Proprietary ESG methodology and ratings and ESG solutions toward c. 20k

Competitive

Rating Team in EU (120+ analysts) database

advantage

ECAI recognized since 2008 Comprehensive offering for banks, Cerved clients compared to 1k current

(among the first in EU) investors and corporates clients

Highly reputed by banks and Operating from an ESMA

capital markets practitioners regulated entity in anticipation of • ECAI and Credit ratings expected to

forthcoming regulation benefit from banking, insurance and

#1 Rating Agency in EU by number of Sole Rating Agency in Italy

financial markets regulators

corporate ratings1 with ESG mandates from:

• ESG solutions benefiting from capital

Market

Banks

#1 Rating Agency in Italy Corporates market tailwinds and incoming ESG

#2 in EU by revenues among Financial investors Regulation and Supervision (eg, ESMA call

“Challenger” Rating Agencies to action on ESG Ratings and assessment

tools)

ESMA = European Securities and Markets Authority; ECAI = External Credit Assessment Institution

1) N. of Italian Joint stock company SMEs ; 2) Source: CEREP (ESMA Central repository for publishing the rating activity statistics) 40C

Real Estate: leading player in residential evaluation and VIPO services

Real estate appraisals Visure ipocatastali (VIPO) Growth drivers

Residential and commercial appraisals Cadastral data • Market returning to pre-Covid conditions

Technical due diligence Land registry

Product

reports thanks to ample liquidity and mortgages

BPO services

• Increase presence in commercial

appraisals & technical services (ecobonus)

• Development of Automated Valuation

Unique database covering c. 95% of 123m real estate assets Models, including monitoring platforms

Competitive

advantage

100k appraisals in 2020 (400k in the last 5 years)

Technical staff composed of 100+ internal experts and 300+ external for banks, RE companies and RE funds

appraisors boasting a capillary presence in Italy

Comprehensive product offering, fully linked into the Risk Management • Regulatory changes including EBA and

platforms of clients automated RE monitoring and Ecobonus

• Stable market share in both Appraisals

Leader in a mature market of One of the three major players

and VIPO, after years of growth in

Market

Residential Appraisals with the in the Italian market Appraisals

highest profit margins

• Reduced demand for VIPO services due to

Upside in Commercial Appraisals insourcing trends by banks

BPO = Business Process Outsourcing 41D

Regulatory & compliance to deal with regulatory risks & opportunities

KYC Reg Tech Subsid. Finance Growth drivers

End-to-end digital EWS alert systems BPO for Banks for

onboarding • Digitalization of business interactions with

Professional services Gar. Fondo Centrale

Product

AML suite Treasury mgmt. SW “Cerca Bando” higher relevance of AML and fraud risks via

Graph 4 You Advisory for SMEs fast and compliant workflows

Anomaly Detection

• Increase AML penetration on banks via

distinctive modules (eg Visius) and non-

Biggest business graph available Acquisition of banking segments (eg Easy AML)

Competitive

Proprietary or exclusive platforms & Finline in 2019

advantage

workflows 58k dossier

• New regulation with increasingly

Acquisition of Hawk in 2020, AML specialist +120 cliens stringent compliance obligations for SMEs

Largest DB on Italian Companies eg. new Codice della Crisi di Impresa and

forward-looking indicators for banks

• Subsidized finance to continue to benefit

from Government support of SMEs

AML leading player New business Service launched in

Market

(e.g., gaming) with 2019 with the

(€145bn1 requests received to access the

an incumbent on acquisition of Finline Fondo di Centrale Garanzia)

banks

• Cross-selling opportunity toward c.20k

Cerved banking and Corporate clients

Note: 1)Ministero dell'Economia e delle Finanze (MEF)

AML = Anti-money laundering 42Offering evolution – Data intelligence

Next slides focus

From Risk Management Growth Services

To Risk Intelligence Marketing Intelligence

Move from credit risk to other types of Leverage a unique data ecosystem to boost

Business risk intelligence: marketing intelligence:

unit

Anti-money laundering Market & sales intelligence

strategy

Anti-fraud Digital marketing

Regulatory risk Advanced analytics

Real estate risk

ESG risk

Data

Analytics

Technologies

43Marketing Intelligence: low double digit growth from 2021 to 2023

Service line Historical trends

Revenues (€m)

CAGR YOY Acquisition of MBS in 2019 doubled the

17-19 19-20

2017 2018 2019 2020 size of the business unit and improved

growth prospects

A Market & sales

Overall growth in other segments from

intelligence

16 181 21 19 14% -9% 2017 to 2020 despite Covid-19 impact

+ Sales Intelligence benefiting from

Digital contribution of Atoka

B marketing 16

9 12 11 30% -29% Outlook 2021-2023

+ Low double digit Growth

Acquisition of MBS as of

Advanced 1st July 29

analytics 15 Evolve Atoka into market leading tool

D n.m. 101% Launch of new Marketing Intelligence

= platform

Marketing Market expansion on mid and small

Intelligence 60 clients

26 29 51 42% 16%

Selective international expansion

Note: 1) Includes c. €1m one-off impact of internationalisation incentives offered by the State (MISE voucher) 44Comprehensive bouquet of services covering the entire marketing cycle

Cerved positioning & portfolio expansion Market macro-trends

A B C

• Marketing services industry persists

Market Sales Digital Advanced

Intelligence Intelligence Marketing Analytics

in being highly fragmented

Marketing

cycle

Know the Find Engage clients Generate • Growing importance of data &

Market new clients & prospects powerful Insights analytics in driving marketing

decisions

2005 2014 2016 2017 2019

• Digital solutions takes over legacy

Market intel Sales intel Digital traffic Data driven products at growing rate

Business platform platform generation management

portfolio Market research AI for sales From traffic to consulting

Media monitoring Sales analytics value Advanced • Worldwide success of platform-

Digital analytics analytics

based solutions providing real-time

marketing insights

Shared Semantic engine Cerved Dedicated sales network • Increasing appetite of SMEs &

assets DAT 4k media sources Micro companies for Marketing

Business graph Markets specialists

monitored

Intelligence

Source (1) Revenues 2020E: Finance Cerved data 45A

Market Intelligence: unique market insights via a digital platform

Growth drivers

New platform (Q1 2021) KNOW AND • Underpenetrated and highly fragmented

Product

MONITOR

Market & sector analysis

THE MARKET TO

Italian market and unique offering

Data providing FIND inspired by global best practice (eg,

Media monitoring GROWTH

OPPORTUNITIES

GlobalData and Statista)

• Fully scalable business model enabling

shift to a recurring revenues model

Competitive

advantage

Largest and unique database on Italian companies

30-year track record and knowledge of markets • Strong commercial network with 70

Strong team of c. 60 experts, fully in-house dedicated accounts

Synergies with Cerved: data, go-to-market, brand, clients

• Cross-selling opportunity toward c. 20k

Cerved existing clients compared to 1.4k

current clients

Underpenetrated and highly fragmented Italian market

Market

Cerved has a unique offering for the Italian market

• Synergies with Atoka and MBS projects

Only 7% penetration of Cerved Clients

46A

Sales Intelligence: Atoka is the reference sales intelligence solution in Italy

Growth drivers

FIND NEW • Underpenetrated and fragmented Italian

Sales funnel management

Product

Sales intel. Platform CLIENTS market & unique offering inspired by global

Lead generation +6m best practice (eg, ZoomInfo)

Mkt prospect similarity Italian

companies • Cross-selling opportunity toward c. 20k

Cerved existing clients compared to 1,5k

current clients

Competitive

State of the art product, benchmarked to international leaders

advantage

Largest and unique database on Italian companies • Expand on Small & Micro segments

Strong team of c. 29 data scientists, fully in-house

Synergies with Cerved: data, go-to-market, brand, clients

leveraging on (i.) dedicated product (i.e.

Atoka Pocket) as platform and (ii.) digital

channel and sales

Untapped users in Italy >500k within Number of Clients • Potential upside in Europe by leveraging on

financial institutions and corporates partnerships and M&A to accelerate data

Market

1,427 1,535

1,261 1,258 1400

Similar KPIs compared to ZoomInfo 1,132 acquisition and commercial expansion

1200

(users/ client, ARPU)

Q4 19 Q1 20 Q2 20 Q3 20 Q4 20

1000

• Fully scalable business model enabling shift

to a recurring revenues model

47B

Digital Marketing: covering all customers’ digital engagement needs

Growth drivers

Sales SEO, CRO, SEA, SEM • Underpenetrated and highly

ENGAGING

Product

Web analytics CUSTOMERS fragmented Italian market

E-mail marketing VIA ALL DIGITAL

Lead generation CHANNELS • Cross-selling opportunity toward c. 20k

Social media advertising Cerved existing clients compared to 260

current clients

Case study1 of value generation: +97% traffic increase

Fullly compliant with GDPR

• New digital marketing offering: content

110k

Competitive

State-of-the-art offering Increasing

advantage

SEO performance marketing, social selling & Influencer

Comprehensive offering New website marketing, e-commerce development

# visit

the entire digital funnel Old website

Synergies with Cerved:

10k

• Focus on SME market with a dedicated

data, go-to-market, brand, Go Live

SEO platform

clients Time

• Partnerships with best of breed

Digital marketing is rapidly replacing traditional advertising thanks to partners further enrich and expand

Market

superior ROI and segmentation capabilities

offering

Increasing appetite by SMEs in fostering digital visibility and e-

commerce

SEO = Search Engine Optimization; CRO = Conversion Rate Optimization; SEA = Search Engine Advertising; SEM = Search Engine Marketing

Note: 1) Cerved Real Case of value generation for Utility company: +97% traffic increase 2020 vs 2019 following the go live of the new website developed by Cerved 48C

Advanced Analytics: a unique offering combined with Cerved’s dataset

Growth drivers

AA for performance improvement:

Churn prediction • Pursue full exploitation of synergies

POWERFUL INSIGHT

Product

Pricing strategy TO IMPROVE STRATEGY offering MBS Advanced Analytics

Cost excellent program AND BOOST GROWTH AND projects to Cerved clients

Digital interaction model PRODUCTIVITY

Mkt and credit strategy • Selective M&A to fuel competitive

Go to mkt strategy advantage on data-driven consulting

projects

Competitive

100+ consultants with 25 partners with long tenure

advantage

• Potential upside in delivering

Leader in insurance segment

Leader in pricing models for banks Advanced Analytics for medium

Strong performance in 2020 corporates

MBS – Cerved synergies

Strengthens go-to-market and

Mngmt consulting market value at €4bn1 o/w 20% Advanced Analytics client relationship

Helps promote use cases and

Market

Raise of advanced analytics consulting doubling the growth of

For

focus on innovation

traditional advisory (12,7% vs. 6,4%)1

Cross-selling advisory to Italian

Cerved as challanger with strong positioning on specific verticals (e.g., banks

Advanced Analytics project for insurers) Expanding client base

AA = Advanced Analytics

Note: 1) Cerved Estimates on Market Data 49Agenda

1. Introduction by the Chairman (G. De Bernardis – Executive Chairman)

2. Cerved investment case (A. Mignanelli - CEO)

3. Cerved for Italy (A. Mignanelli - CEO)

4. Data intelligence (A. Mignanelli - CEO)

− Offering

− Channels

5. Credit management (A. Mignanelli - CEO)

6. Talents, technology, sustainability (A. Mignanelli – CEO)

7. Financials & strategic outlook 2021-2023 (E. Bona – CFO)Channels evolution

Next slides focus

Financial institutions Corporates

Large

Advisory/ Multi-specialist

Productive external

Medium network

Small Phygital

51Financial institutions channel - performance & outlook

Service line 2017 2018 2019 2020 CAGR YOY Historical trends

Revenues (€m) 17-19 19-20

Stable risk intelligence with contraction

in Credit Risk and Real Estate more than

Mktg intelligence

Market & sales compensated by strong growth in

Intelligence 1 1 6 6 Regulatory & Compliance

103% 5%

Solid organic growth in Market and Sales

Advanced Acquisition of MBS

Analytics 4 Intelligence which benefitted from

2 n.m. 48% increased focus on cross-selling with

Credit risk

regards to the legacy offering and the

90 88 83 86 -4% 4% Atoka service range

Risk intelligence

Credit & 3 3 3 3

ESG ratings -2% 18% Outlook 2021-2023

Real estate 33 38 39 31 Stable outlook in Risk Intelligence,

8% -20% with potential for Credit/ ESG ratings,

Regulatory & 12

compliance 1 2

125% 427% analytics & KYC

Financial institutions Further contribution from Marketing

Channel 131 134 141 2% 5% Intelligence, growing and still largely

128

underpenetrated

52Evolution from provider of data to provider of value-added services

Product innovation New service model

Proprietary systems linked to the Leading

Analytics database allowing banks to improve their Market’s largest salesforce with 30 resources

sales

& Early Warning accuracy ratios within credit processes

and rating models force

Geared toward achieving:

Commercial, technical and

Largest & most complete database consulting skills plus MBS comprehensive coverage &

Data & scores combined with Analytics & Early Warning for data driven solutions

systems creates a unique offering for an and transformational client acquisition Client

estimated 90% of Italian banks initiatives

cross-selling and upselling service

New platform with end-to-end solutions teams

Subsidized

over the credit cycle which in 2020

finance related to approx. EUR 5,5bn of Large banks: 9 groups, 122 licenses,

underlying loan volumes EUR 71 Revenues in 2020

Almost all large banks have new Medium banks: 40 groups, 135 licenses,

contracts or pilots, further EUR 28 Revenues in 2020 FIs

contractualised growth in 2021 cluster

Update of Cerved Group Score to assist Small/ BCC/ Other1: 2 large groups

banks in dealing with Covid-related risks, 308 licenses & other (205 licenses),

CGS Covid

similarly to the Corporate EUR 43 Revenues in 2020

channel offering

Note: 1) Other = Insurance companies, financial firms, car companies 53Clear strategy to defend from pricing pressure and consolidation

Flat Fee Consumption

Contract renewals Bank consolidation

39% 35%

61% 65%

Pressure on Credit Risk data, particularly if Common client overlap

sold stand-alone 2018 2020

Higher bargaining power of enlarged bank

Product innovation within Cerved’s Average residual weighted

Analytics & Early Warning systems life: 1.7 years Lower sophistication of purchased bank,

Latest expiry: Dec 2023 offering product upgrade potential

Stronger cross-selling capabilities > 50% of value expiring in

Dec 2023 High complexity & decommissioning,

Anticipation of contract expiries coupled particularly during mergers

with product innovation and cross-selling Cerved commercial strategy

less oriented on long term Mergers expected to occur mainly between

High complexity & decommissioning contracts, which imply higher Cerved existing client base

discounts and tenders

1% 7%

1% 6%

Strong track record in growing overall revenues (+3,0% CAGR from 2017 Marketing

Intelligence

1% 2% 9%

28% 31%

to 2020) while cross-selling and diversifying the product offering 31% 24%

Othe risks

Increased contribution from Regulatory & Compliance, Marketing

Credit & ESG 70% 67%

Intelligence and Advanced Analytics more than covering contration in rating + R.E.

61% 61%

mature Credit Risk and Covid-related issues with Real Estate Credit Risk

2017 2018 2019 2020

54Channels evolution

Next slides focus

Financial institutions Corporates

Top

Advisory/Multi-specialist

Productive external

Large/ Mid network

Small/ Micro Phygital

55Corporate channel - Cerved performance & outlook

Service line 2017 2018 2019 2020 CAGR YOY Historical trends

Revenues (€m) 17-19 19-20

Mid single digit growth in Risk

Market & Sales

Marketing Intelligence

Intelligence

Intelligence until 2019. Contraction of

15 16

1

15 13 1% -15%

consumption in 2020 due Covid-19 related

Digital impact on underlying business trends

Marketing 9 12 16 11 30% -29%

Solid growth in Marketing Intelligence

Advanced

Analytics

Acquisition of MBS

26 benefiting from cross-selling and enlarged

12 n.m. 111% product offering, with limited impact

Credit Risk 143 145 149 134 2% -10% from Covid-19 mainly thanks to AA

Risk Intelligence

Credit &

4 4 5 5 4% 5%

ESG Ratings Outlook 2021-2023

Real Estate 2 -4% -35%

1 1 1 Mid Single Digit in Risk Intelligence ,

Regulatory & with a focus on KYC

Compliance 0 1 3 3 219% 7%

Corporate Further contribution from Marketing

CM

Receivables 17 21 26 30 21% 16%

Intelligence and Corporate Receivables

Corporates

191 201 227 223 9% -2%

Channel

Note : 1) Includes c. €1m one-off impact of internationalisation incentives offered by the State (MISE voucher)

CM = Credit Management ; AA = Advanced Analytics

56Strategy to foster cross-selling, upselling and new clients

Go-to-market Commercial strategy

Risk Intelligence

& Credit Collection

Marketing Intelligence All business units

Delivery via client service teams with

#25 key accounts commercial and technical skills

#5 advisory accounts Strong focus on projects which

Top 4 industry sectors integrate the service offering

Incorporation of sector characteristics

#70 field sales

3 geographic areas

#160 field sales Develop project s for clients which

#25 Telemarketing staff integrate business information with

Large/Mid 3 geographic areas other Cerved services, via (i.) Usage

4 industry sectors stimulation and specialist account

#50 resources in special dedicated teams, and (ii.) New client

accounts teams (Usage generation

stimulation, Credit collection,

Ratings, Digital marketing)

Small / Micro #20 Teleselling New client generation

Website Develop off the shelf products

Partnerships Push on digital/online approach for

both sales and usage stimulation

57The leading go-to-market in Italy

Corporate channel KPIs Client dynamics for Risk Intelligence products

# of clients 2020 Rev. €m ‘ARPU1 (€k) Churn and new client generation have averaged at

Top Top 1k 92 €94k c. 6% and 5%, respectively, from 2017 to 2020, limited

Covid impact

Large/ Mid 13,7k 119 €9,0k Consumption of existing clients averaged 5% except

2020, due to lower consumption in particular of

Small/ 8,8k 12 €1,4k SME clients due to Covid

Micro

Large/Mid

Corporate Channel Key Objectives Churn Existing New

Top and Large clients: increase ARPU and share of

7.1% 6.9%

wallet 4.6% 3.1% 4.5% 4.3% 4.3%

Medium clients: increase penetration, ARPU and n.

-5.9% -5.1% -5.9%

of clients -7.1% -7.9%

Small and Micro clients: increase number via

dedicated product platforms

2017 2018 2019 2020

Note : 1) Average Revenues per Unit 58Agenda

1. Introduction by the Chairman (G. De Bernardis – Executive Chairman)

2. Cerved investment case (A. Mignanelli - CEO)

3. Cerved for Italy (A. Mignanelli - CEO)

4. Data intelligence (A. Mignanelli - CEO)

− Offering

− Channels

5. Credit management (A. Mignanelli - CEO)

6. Talents, technology, sustainability (A. Mignanelli – CEO)

7. Financials & strategic outlook 2021-2023 (E. Bona – CFO)Truly independent player with a comprehensive product offering

Product offering and client segmentation

# of Banking Corporate Credit Legal

Type of client

clients UTP & NPLs Receivables Operations Service

Cerved is the only player in Italy with a highly

Banks 19 diversified product offering in order to tackle

Investors 8

all client needs

Consumer Finance 26 Leading position in Banking NPEs, having

Utilities & Large comp. 79 completed a number of high-profile and long

SMEs 1,575 term operations with banks and funds

Public Admin. 21

Revenue diversification Client concentration High Revenue diversification with a strong

focus on the Banking NPE segment and the

Banking UTP & NPL Corporate Receivables segment complemented

20% 22% Top 3

Corporate Receivables 12% 4 to 10

by ancillary services

49% 20%

Credit Operations

37% 11 to 20

High client diversification with almost 1700

11% 29% Other

clients, of which top 10 clients chiefly related to

Legal Services

large NPE servicing contracts

60Credit Management: high single digit growth expected to 2023

Historical trends

CAGR YOY

Service line 2017 2018 2019 2020 17-19 19-20 Strong growth to 2019 thanks to organic

Revenues (€m)

growth, high-profile transactions and

Banking diversification

UTP & NPL 88 110 74 68% -32%

39

Decline in 2020 in Banking NPE due to

+ the Covid-19 pandemic, albeit segments

Corporate

Receivables 17 21 26 30 21% 16%

offering growth and resiliency

+ Outlook 2021-2023

Credit

Operations 25 23 32 30 14% -4% High single digit growth

+ Develop UTP servicing for banks

Legal

Services 12 15 18 17 24% -3% New NPL servicing contracts

= Growth in corporate receivables

Credit

Management 93 147 185 152 41% -18% J/V with investors

61NPE servicing market expected to return to growth post Covid-19

NPL servicing market outlook

Total Servicing

Revenue Pool Cerved’s 2018 Investor Day anticipated

AuM (Servicer) stabilising NPE volumes albeit growing

revenues due to performance, macro and

280-300B€ Ancillary Services

1,500M€ The Covid-19 is expected to generate EUR 60-

240B€

100b new NPE volumes, and consequently also

Servicing Revenues

900M€

220B€ Trajectory

in 2018

Healthier banks coupled with new instruments

Investor such as GACS expected to accelerate NPE

Day

440M€ disposal timeframe by banks

Revenue impact

50B€

due to Covid-19

Continuing pressure from BCE on banks to

110M€ maintain balance sheets healthy

2014 2018 2020 2021 2023

Ownership and Large revenue pool

Explosive AUM growth

servicing to be extracted New wave of NPEs due

due to portfolio sales

largely captive to from more liquid to Covid-19 crisis

and outsourcing deals

banks assets

Note: 1) Cerved analysis 62Covid-19 impact has changed the medium to long term perspective

Cerved market positioning

Ranking by AuM as of 30/06/2020 (€396bn total)

Truly independent player well positioned with

#2 player with an 11% share 140 key institutional investors such as Atlante/ DeA,

77 (20% MKT share ex. Purchasers)

AMCO and REV

45 38 30 25 23 17 Knowledgeable and experienced servicer with

data driven expertise on credit towards

DoValue Cerved Intrum Prelios IFIS AMCO Credito Others

corporate and SMEs

Fondiario

Cerved AUM and collection rates (excl. MPS)

Cerved’s NPL AuM (ex. MPS) Avg. recovery rate Target of new AUMs of approx. 2b per annum

from 2021 to 2025, leading to total NPL AUMS

34.2

33.3

3.00%

3.20% remaining stable

2.70%

30.3

30.9

Net NPLs already secured in 2021 of 700m from

AMCO, plus up to €2,5bn in the medium term

via Polis

Dec 2018 Dec 2019 Dec 2020 Feb 2021 2018 2019 2020

Source = PwC - The Italian NPL Market, December 2020 63You can also read