Global Investment Outlook 2022 - From the recovery to mid-cycle ABN AMRO Investment Solutions

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

1 ABN AMRO Investment Solutions Global Investment Outlook 2022 From the recovery to mid-cycle December 2021 This document is for information purposes only and does not constitute investment recommendation. For professional clients only.

Global Investment Outlook 2022 2 Global Investment Outlook 2022 Macro

Global Investment Outlook 2022 3

Macro Outlook

GROWTH INFLATION

KEY TAKEAWAY

We are moving from the recovery phase of the After 40 years of declining inflation, the biggest We think we could be in

MACRO current cycle to its middle phase. The previous

cycle was the longest in history and it ended only

surprise of 2021 has been the goods-led inflation

surge. Structural disinflation factors could reverse

for another

expansion thanks to

long

due to the exogenous shock of the pandemic. If with the energy transition, de-globalization and inventory rebuilding,

anything, we believe that the willingness of fiscal labour’s increasing bargaining power in high profitability and

and monetary authorities to support the cycle is negotiations. We see inflation abating from 2021 investment by firms as

even greater today. but remaining higher than pre-pandemic levels. well as strong balance

sheets of households

while governments and

monetary authorities

MONETARY POLICY POLITICS GEOPOLITICS are willing to intervene.

Inflation and interest

Debt dominance is pre-empting hawkish reactions China’s ongoing strategic reorientation of its The geopolitical context will become more rates could be much

by central banks while they have defined new economy towards “common prosperity” and complex amid the battle for self sufficiency, energy more volatile than in the

priorities and strategies after persistent below “internal circulation” over outright growth is not and technology supremacy. China and US tensions previous business cycle.

target inflation. Central banks became much more only a China phenomenon. Worldwide, political are escalating again while many businesses and

inflation tolerant while prioritizing other objectives and monetary authorities now have more tools, governments are rethinking global value chains in

such as inclusive growth and/or addressing more capacity and more willingness to direct order to make them more resilient to future shocks,

climate change. economic activity than ever before. including natural disasters.

ABN AMRO Investment Solutions: This document is for information purposes only and does not constitute investment recommendation. For professional clients only – December 2021Global Investment Outlook 2022 4

Macro Outlook

Supporting factors 1 & 2: inventory rebuilding and desire to invest for companies

A big inventory cycle may soon unfold. Supply chain disruptions have weighted on inventories. Early indicators about Christmas season suggest that

inventories are soaring as businesses seek to secure goods for sale. Moreover, capital goods new orders, a closely watched proxy for business spending

plans, strongly rebounded for few quarters and remained elevated.

US Retailers : Inventories to Sales ratio Capital Good New Orders

Sources: Fred, monthly data, computations by ABN AMRO Investment Solutions. Sources: Eikon, monthly data, millions of USD and Index 100 in 2015. Computations by ABN AMRO

Investment Solutions.

ABN AMRO Investment Solutions: This document is for information purposes only and does not constitute investment recommendation. For professional clients only – December 2021Global Investment Outlook 2022 5

Macro Outlook

Supporting factors 3 & 4: profitability and cash available

US profit margins are high and can support rising wages and costs, even if productivity growth does not accelerate. This is unusual after a recession to have

so high profit margins while real wages did not adjust on the downside with the recession. Not only firms have strong profitability but balance sheets of

households are solid thanks to a lot of cash waiting for consumption and/or investment.

US profit margins M2 / GDP

Sources: Eikon, monthly data. ABN AMRO Investment Solutions.

ABN AMRO Investment Solutions: This document is for information purposes only and does not constitute investment recommendation. For professional clients only – December 2021Global Investment Outlook 2022 6

Macro Outlook

Supporting factors 5 & 6: very accommodative financial conditions in developed markets and China re-leveraging

In developed markets, normalization of nominal interest rates is coming but will let real interest rates supportive for economic growth and markets. China’s

government explained deleveraging was one of the “five major tasks” for the government in 2021, with a goal of keeping overall leverage – the ratio of debt to

gross domestic product – “generally stable”. But China has reversed his deleveraging campaign later in 2021 amid real estate fragilities and Omicron threat.

YoY growth of M2/GDP in China Real 10Y interest rates on Government Debt (CPI deflated)

Sources: Eikon, quarterly data. ABN AMRO Investment Solutions. Sources: Eikon, monthly data. ABN AMRO Investment Solutions.

ABN AMRO Investment Solutions: This document is for information purposes only and does not constitute investment recommendation. For professional clients only – December 2021Global Investment Outlook 2022 7 Global Investment Outlook 2022 Markets

Global Investment Outlook 2022 8

Market Outlook

KEY TAKEAWAY

EQUITIES STYLES

Faced with a

combination of low and

MARKETS Equities remain our preferred asset class.

Emerging markets equities offer the highest risk-

Despite long-term support (strong fundamentals,

digitization, low interest rates, ESG appetite) for

rising rates and tight

credit spreads,

return trade-off (valuations). Equities are one of growth stocks, rotation risks on cyclical/defensive

investors are likely to

the few asset classes that still offer attractive remain high. We prefer a neutral position on

double down on their

yields with Emerging Debt while less risky debts value-growth through a barbell of active

search for short

are characterized by strong negative real yields. strategies.

duration, floating rates,

and less correlated

sources of income.

We expect, related to

the volatility of inflation

INTEREST RATES CREDIT VOLATILITY and interest rates, a

high volatility of quality

Short-term interest rates should remain Credit spreads remain low and, in our opinion, are Volatility should progressively fall into a low risk and cyclical stocks.

reasonably low, but on a rising path while long- fairly priced. Finding income with modest or no regime and, according to us, a new and long

term yields could go lower with the cycle gaining duration will continue to be the priority, in our expansion phase with volatility spikes depending

maturity. This appears likely to encourage all view, but major market disruptions or significant on the newsflow. Volatility could be much more

types of investors to make larger, more diverse credit issues appear unlikely at few quarters related to inflation figures than in the previous

allocations to alternatives, liquid and illiquid. horizon. business cycle.

ABN AMRO Investment Solutions: This document is for information purposes only and does not constitute investment recommendation. For professional clients only – December 2021Global Investment Outlook 2022 9

Market Outlook

The Macro Financial Clock

With structural shifts towards low inflation (flat Phillips Curve,

digitization, globalization, shrinking worker bargaining power) and

low real interest rates (demographics, capital price, excessive

savings, etc.), end of business cycles are no longer characterized

by inflation and monetary tightening. We have to monitor

business cycle developments with new tools.

Changing US financial conditions over the last three cycles have

been counter-clockwise. Indeed, volatility tends to rise before a

recession and ease with the recovery whilst the yield curve

flattens before a recession and picks up during the recession.

The end of the longest economic cycle in history was precipitated

by the shutdown of the global economic activity to stem the

coronavirus outbreak. Volatilities hit record high while the yield

curve stayed flat, typical movements in crisis time. Now, easing

volatilities and modestly steepening yield curve signal the dawn

of a new business cycle.

Current conditions are corresponding to a phase between

A renewed cycle with more favourable conditions

Recovery and Middle-cycle.

Sources: Datastream, daily data from 01/01/1990 to 10/12/2021. The yellow point represents spot conditions.

ABN AMRO Investment Solutions.

ABN AMRO Investment Solutions: This document is for information purposes only and does not constitute investment recommendation. For professional clients only – December 2021Global Investment Outlook 2022 10

Market Outlook

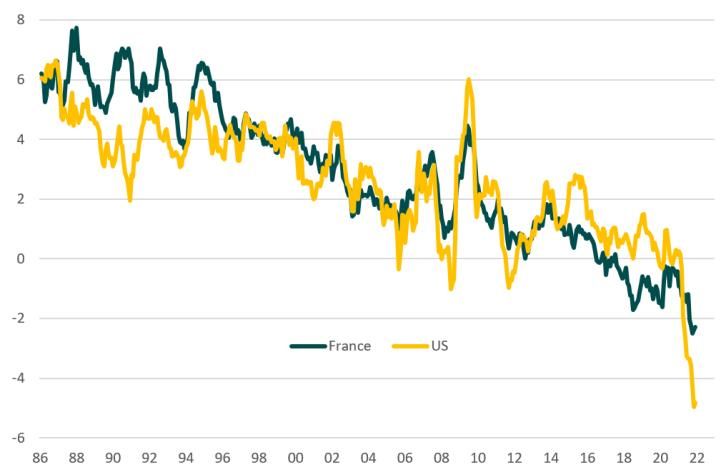

Ultra-low interest rates environment

Central banks across the globe turned more accommodative than ever to support the economic activity. Bond purchase programs and other stimulating tools

drive interest rates to historic lows while spreads remain tight. Fixed income (real) yields are set to stay low for a long time.

18 16 25 8

16

Yield-to-Maturity (%)

14 7

14 20

Spread vs France (%) 12 Global High Yield 6

12

Global IG Corporate

10 5

10 15

8 8 4

6 10

6 3

4

4 2

2 5

2 1

0

-2 0 0 0

2007 2009 2011 2013 2015 2017 2019 2021 1999 2002 2005 2008 2011 2014 2017 2020

Portugal 10Y Sovereign Debt (%) at historic low levels Yields on main fixed-income asset securities continue to fall

Source: Bloomberg, France and Portugal 10Y sovereign bond yield-to-maturity. Source: ICE BofAML, Global High Yield Constrained Regular Rebalanced Index and Global

Investment Grade Non-sovereign Index yield-to-worst.

ABN AMRO Investment Solutions: This document is for information purposes only and does not constitute investment recommendation. For professional clients only – December 2021Global Investment Outlook 2022 11

Market Outlook

Equity low volatility vs cyclical volatility: the TINA effect?

For few quarters, equity markets appear highly robust with pullbacks followed by quick rebounds. Implied volatilities have spiked consequently around their

long-term historical average. Realized volatility was even lower but value-growth excess return volatility remains at very high levels. Significant news were

accompanied by strong rotations between cyclical and defensive stocks instead of a global market correction.

US Equity volatilities EMU Equities volatility

Source: Eikon DS, daily data from 01/01/1998 to 10/12/2021. MSCI indices.

ABN AMRO Investment Solutions: This document is for information purposes only and does not constitute investment recommendation. For professional clients only – December 2021Global Investment Outlook 2022 12 Global Investment Outlook 2022 Risks

Global Investment Outlook 2022 13 Risk Outlook What we are watching in 2022 MACROECONOMICS Price-wage inflation loop Profit margins and financial vulnerability Pandemic new waves and variants The main reason for dovish central banks stance is that With high inflation of producer prices and risk of wage Vaccines are working. The twin decoupling continues: (i) underlying wage pressures remained very limited despite longer acceleration, at least in the short-term, high profit margin are infections are causing far fewer medical complications, and (ii) and higher inflation in 2021. The main risk is to have extreme helping to absorb higher costs. If productivity stays low, strong the medical situation is weighing much less on economic wage inflation pressures strengthening. costs increases could deteriorate firm’s balance sheets quality. performance. But a Covid-resistant variant could jeopardize it. MONETARY POLICY Fed preference for price stability vs employment ECB amid waves Greening ECB A classic debate. Markets were expecting 2-3 hikes in 2022, while The Omicron variant has complicated the ECB's exit from the Among other action points (stress tests, credit rating agencies J. Powel, few weeks after J. Biden renamed him to lead the Fed, emergency measures. We expect the ECB to replace its assessment, etc.), the ECB, in 2022 Q4, will introduce climate seemed slightly more hawkish. Until now, the long-term inflation Pandemic Emergency Purchase Programme with a new disclosure requirements for private sector assets used as expectations remained well anchored despite very high inflation. transitory programme starting April 2022 and a first hike in 2023. collateral and for asset purchases as a new eligibility criterion. POLITICS Populism will continue De-globalization The geopolitics of energy transformation The end of Donald Trump’s presidency is not the end of political The heyday of globalization is behind us. Globalization is on the The Covid-19 crisis has further exacerbated the need to fight populism or its causes, in our view. This likely means continued back foot, with the ratio of trade-to-output moving sideways for inequalities and also put health and environmental issues at the political and geopolitical volatility. In Europe, right-wing populist more than a decade. The risk is that the former “Trade war’ by top of the political agenda. Norms, regulations, carbon price, R&D governments in the east continue to pose challenges to the wider former president Trump will evolve in “securing supply-chain” efforts could jeopardize a state’s relative position in the E.U. and technology sovereignty conflicts. international system. ABN AMRO Investment Solutions. This document is for information purposes only and does not constitute investment recommendation. For professional clients only – December 2021.

Global Investment Outlook 2022 14 Disclaimer

Global Investment Outlook 2022 15 Disclaimer ABN AMRO Investment Solutions - AAIS Limited company with Executive and Supervisory Board capital of 4,324,048 Euros registered with the RCS Paris under number 410 204 390, Head office: 3, avenue Hoche, 75008 Paris, France, Approved by the AMF, dated 20/09/1999, as a portfolio management company under registration number GP99-27 This promotional document prepared by ABN AMRO Investment Solutions (“AAIS”) does not constitute a solicitation to buy, an offer to sell or legal or tax advice. On no account does it constitute a personalised recommendation or investment advice. Before making any investment decision, the investor is responsible for assessing its risks and for ensuring that the decision is consistent with his objectives, his experience and his financial circumstances. The investor’s attention is drawn to the fact that information on the products featured in this document is no substitute for the completeness of the information contained in the fund’s legal documentation that you have been given and/or that is available free of charge on request from AAIS or on the website www.abnamroinvestmentsolution.com Before making any investment, the investor must pay particular attention to the risk factors and carry out his own analysis that takes into account the need to diversify investments. All investors are encouraged to take advice on this matter from their regular legal, tax, financial and/or accounting advisors before making any investment. The information and opinions contained in this document are for general information only. They are taken from sources that AAIS considers trustworthy, but no guarantee can be given as to their accuracy, reliability, validity or completeness. Past performance is not a guide to the future performance of the fund and/or the financial instruments and/or the financial strategy described therein. Performance data do not take into account any commissions paid on the subscription or acquisition of financial instruments. No guarantee can be given that the described products will achieve their objectives. Investing in financial instruments carries risks and investors may get back less than the amount of their investment. When a financial investment is denominated in a currency other than your own, the exchange rate may have an impact on the amount of your investment. The tax treatment differs according to each client’s particular circumstances. It is therefore strongly recommended that, before investing, you take advice on the appropriateness of the investment to your objectives and your legal and tax circumstances. It is your responsibility to ensure that the regulations to which you are subject, depending on your status and your country of residence, do not prevent you from investing in the products or services described in this document. Access to products and services may be restricted for certain persons or in certain countries. For additional information, you should contact your regular advisor. Complaints may be sent free of charge to the AAIS customer service department using the following email address: aais.contact@fr.abnamro.com This document is intended only for its original addressees and may not be used for anything other than its original purpose. It may not be reproduced or distributed, in whole or part, without the prior written consent of AAIS and AAIS shall not be held responsible for any use made of the document by a third party. The names, logos or slogans identifying AAIS’s products or services are the exclusive property of AAIS and may not be used for any purpose whatsoever without the prior written consent of AAIS.

Global Investment Outlook 2022 16

You can also read