GLOBAL MARKETS STRATEGY DAILY UPDATE - Thursday, September,24 2020 21.07.2020

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Thursday, September,24 2020 GLOBAL MARKETS STRATEGY DAILY UPDATE

Alexander APOSTOLOV, PhD, MBA

Chief Investment Strategist

FX FOCUS www.bluesuisse.com/en/analysis

analytics@bluesuisse.com

All Eyes on US Election, Fiscal Stimulus and Supreme Court Decision

Market Snapshot

USD: Anticipation continues to build for US presidential debates next week. Continuing with

fiscal and the supreme court, headlines from US government leaders still suggest no fiscal

stimulus anytime soon. President Trump also said that he will announce his Supreme Court Main Quotes Heat Map

nominee Saturday and enough Senate Republicans signalled that they will support the

nomination.

USD: On the COVID-19 front, Bloomberg reports that the US Food and Drug Administration is

soon expected to announce tougher standards for a coronavirus vaccine approval. The bottom-

line impact? It could make it more unlikely to see approval before the November 3 as the FDA

could prefer to do two- months of follow up on final trial results before moving ahead.

Separately, the Washington Post focused on a new study conducted by scientists in Houston. “A

study of more than 5,000 genetic sequences of the coronavirus, which reveals the virus’s

continual accumulation of mutations, one of which may have made it more contagious.”

1 Day Relative % Performance [USD]

USD: Preliminary Markit PMIs remained within expansion territory in September.

Manufacturing PMI is slightly higher to 53.5 from 53.1 while services PMI stayed strong at 54.6.

The 54.6 preliminary service PMI is encouraging especially given the weaker-than-expected

service PMIs in the Eurozone released earlier. More definitive ISM data is due Friday.

EUR: France PMI services unexpectedly fell into contractionary territory. Although Germany

PMI also saw a services miss to 49.1 vs 53.0 consensus expectations, there was a strong

manufacturing print. The index climbed to 56.6 in September, solidly beating consensus

expectations of 52.5 and driven by rebounding export demand. This suggests two things. First,

that the divergence between manufacturing and services is emerging again as a consequence of FX Technical Indicators Summary

rising COVID-19 concerns. It feels like the recovery in the services sector is slowing after the

initial bounce and given the potential return of lockdowns. Secondly, the export-driven economic

recovery in Germany remains on track in September.

GBP: The PMI declines in September were less than expected with manufacturing coming in at

54.3 and services at 55.1. But beneath the surface, the pace of the recovery is slowing. Markit

notes that there were widespread reports that a lack of consumer confidence and persistent

disruptions to business operations due to the pandemic had held back the recovery in

September. However the PMI print may not reflect the latest wave of Covid-19 concerns.

GBP: BlueSuisse.com analysts believe that with the recovery slowing from August to September,

weakening expectations reflect a recognition of more persistent virus concerns and a lower level

of output. BlueSuisse.com analysts expect these to weigh sharply throughout the second half of

the year.

Updates on Commodity Currencies:

•CAD: Details of the Thorne speech, outlining the objectives of the Liberal government: There

were no market reactions to the speech but importantly, the government proposes to extend the

wage subsidy program through next summer. While this is supportive to the economy, it also has

key implications on Canada’s debt burden. The Throne Speech will trigger a confidence vote in

the House of Commons, where members will vote for or against the policy plans outlined in the

speech. As the Liberals control a minority in the House, support of another party (most likely the

New Democratic Party) will be necessary for a majority favorable vote. If the confidence vote

fails, a new election will be triggered. Fresh elections are not BlueSuisse.com base case but we

are watching this possibility.

•NZD: The RBNZ left policy unchanged as broadly expected by markets, with the OCR at 0.25%,

and LSAPs at 100bn. Despite limited reaction in the markets, the overall message sent at the

RBNZ meeting looks dovish again. After the repeated dovish surprises this year, the markets

probably have already priced in additional easing risk to some extent, so the near-term influence

from the RBNZ’s dovishness may remain small. However, the upcoming introduction of

additional easing tools could depress NZD over time, and if there is increased risk avoidance in

the market, weakness in NZD may accelerate.

Chart of the Day Nasdaq 100: Trying to Hold Top of Important Long-term Structure The Nasdaq 100 just pulled back near an important area of big-picture support via the top of the decade-long channel it left behind back in July. It is viewed as an important structure given its prevalence as support and resistance at times over such a long period of time. When price exceeds the top of an upward sloping channel a couple of different things often happen. In one scenario we will see a smallish ‘overthrow’ where price rises for a relatively short period of time before momentum stalls and leads to a decline back inside the channel. At which time a full-on reversal can develop in the wake of a failure to maintain the trajectory. The overthrow is viewed as a sort of last ‘hurrah’, so to speak. In the second scenario, price leaves the confines of the channel and it turns into a massive blow-off top by rising rapidly. While we are seeing the top of the channel get tested now, if price holds onto the upper parallel, then this could still be the case. We do not need to predict how this will play out. The top of the channel is support at the moment and both scenarios could be in play. If we see it break, then switching to an aggressive bearish stance may be warranted. But until the upper threshold gives-way, we must continue to respect it for what it remains – support. Perhaps it continues to hold, and another speculative wave comes in to push the market much higher before fizzling out. In either case, whether we are on the verge of a major decline or a blow-off style rally continues to mount – the days of the tech stocks defying gravity look to be closer to the end than the beginning. • NASDAQ 100 - WEEKLY

Alexander APOSTOLOV, PhD, MBA

Chief Investment Strategist

Capital Markets Overview www.bluesuisse.com/en/analysis

analytics@bluesuisse.com

Stocks suffer steep losses as investors raise cash

Market Snapshot

The S&P 500 dropped 2.4% on Wednesday in a broad-based retreat that reflected cash-raising

efforts. The Nasdaq Composite fell 3.0%, the Russell 2000 fell 3.0%, and the Dow Jones

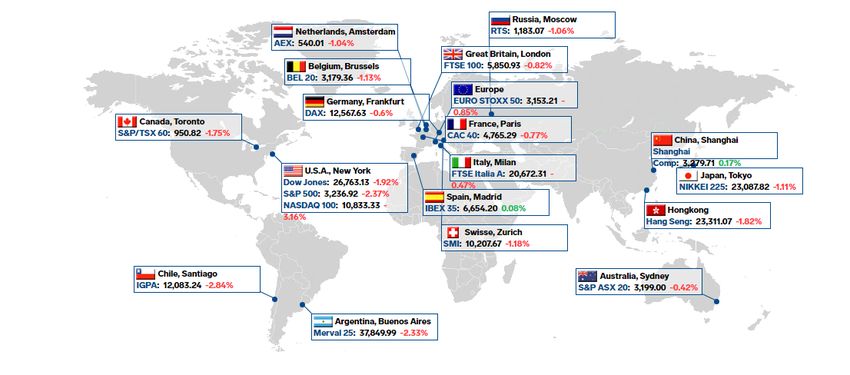

Industrial Average fell 1.9%. All 11 S&P 500 sectors closed sharply lower between 1.1% (health World Exchanges Performance Heat Map

care) and 4.6% (energy), and traditional safe-haven assets did not see the usual appreciation in

times of equity weakness. U.S. Treasuries were little changed, gold futures fell 2.0% to

$1868.90/ozt, and the Japanese yen fell 0.5% against the dollar (94.35, +0.36, +0.4%). It didn`t

start this way. The session had begun on a high note, as the market reacted positively to Johnson

& Johnson (JNJ 144.44, +0.23, +0.2%) advancing its COVID-19 vaccine candidate to Phase 3

trials and Nike (NKE 127.11, +10.24, +8.8%) blowing past quarterly results and raising its FY21

revenue guidance. An initial weakness in the mega-cap stocks, however, gradually spilled over to

the broader market, and the negative price action appeared to reinforce the idea that the

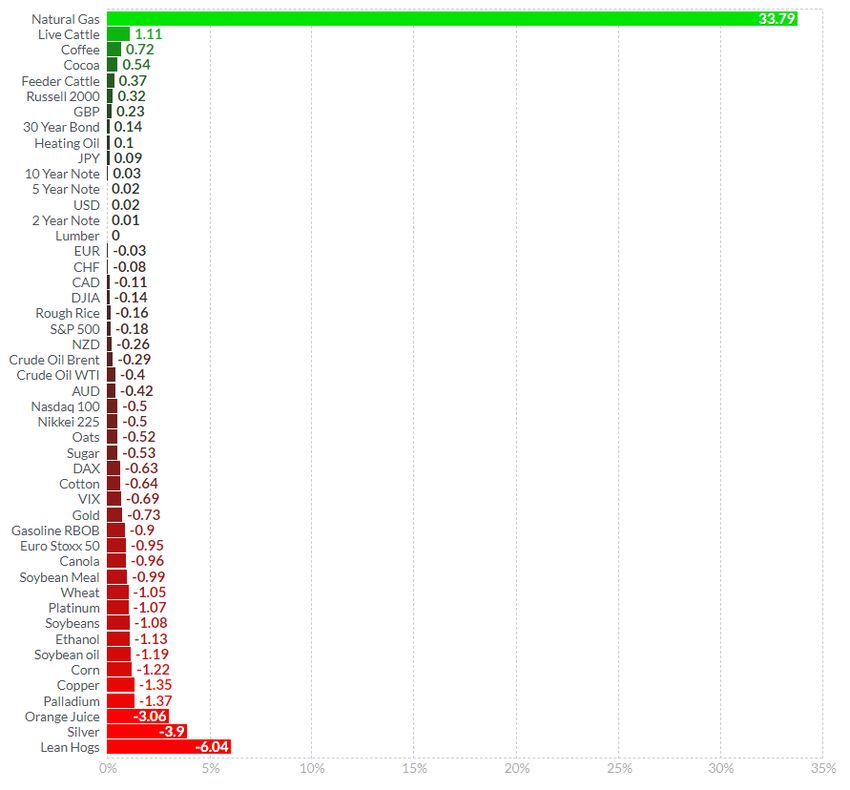

market`s recent pullback may not yet have run its course. The CBOE Volatility Index increased 1 Day Relative Performance

6.4% to 28.58, which was a relatively modest gain. Losses steepened in the afternoon without

much interest to buy the dip. Shares of Apple (AAPL 107.12, -4.69, -4.2%) fell 4% while Tesla

(TSLA 380.36, -43.87, -10.3%) fell 10% post-Battery Day. On a related note, UBS resumed

coverage on Apple with a Neutral rating, versus a prior Buy rating. Separately, the House passed

a government funding bill through Dec. 11 that the Senate is expected to pass later this week.

Notwithstanding this piece of good news, general uncertainty surrounding the election, the

coronavirus, and the economy likely increased the cash appeal. Treasuries, as previously

mentioned, finished near their flat lines. The 2-yr yield was unchanged at 0.13%, and the 10-yr

yield increased one basis point to 0.68%. WTI crude futures gained 1.0%, or $0.39, to $39.94/bbl

but retraced those gains after the settlement time.

Reviewing economic data:

Reviewing Wednesday`s economic data:

• The FHFA Housing Price Index for September increased 1.0% following an upwardly revised

1.0% increase in August (from +0.9%).

• The weekly MBA Mortgage Applications Index increased 6.8% following a 2.5% decline in the

prior week.

Looking Ahead:

• Looking ahead, investors will receive the weekly Initial and Continuing Claims report and New

Technical Indicators Summary

Home Sales for August on Thursday.

Top Market drivers:

• Stocks suffer steep losses amid general uncertainty, cash-raising efforts

• Broad-based retreat, mega-caps were an influential drag

• Encouraging vaccine update from Johnson & Johnson (JNJ)

Stock Market Sectors:

• Strong: Health Care

• Weak: Information Technology, Energy, Communication Services, MaterialsYou can also read