How States Can Help Students Harmed by Higher Education Fraud

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

How States Can Help Students Harmed by

Higher Education Fraud

This National Consumer Law Center report surveys states’ Student Protection Funds (SPFs) and

provides a roadmap for how and why all states through the creation or strengthening of SPFs can

provide relief to help students recover financial losses caused by school fraud or sudden closure.

Report

Summary

Appendix A: States with Student Protection Funds (SPFs)

Appendix B: Distance Education and SPF Eligibility

Appendix C: Checklist to Evaluate a State Student SPF

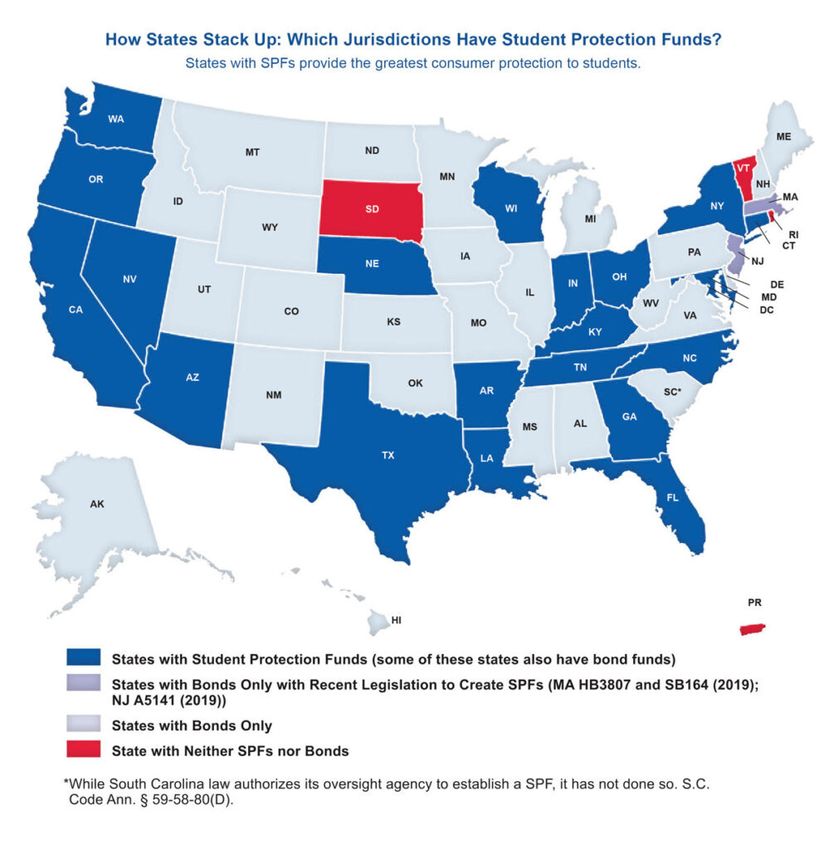

Map: Which Jurisdictions Have SPFs?

Press release

Related Materials

Wake Up Call to State Governments: Protect Online Education Students from For-Profit School

Fraud, Dec. 2015

Ensuring Educational Integrity: 10 Steps to Improve State Oversight of For-Profit Schools, Jun.

2014

Student Loan Law

Published January 14, 2021

©National Consumer Law Center, Inc.

Overview

When a college education is cut short by a school closure or a school engages in fraud, the students

and their families suffer long-term financial distress. Higher education fraud, when unaddressed,

devastates families and their communities, disproportionately impacting low-income, people of color,

and women, who start out economically disadvantaged.

In recent years, several large for-profit school chains, including Corinthian Colleges, ITT Tech, The

Art Institutes, and Education Corporation of America, deceived hundreds of thousands of students

into taking on enormous debts for worthless educations, and then suddenly closed, leaving financial

ruin and trauma for students who attended the schools. Now, as for-profit distance education

increases, students who enroll in out-of-state distance education programs are particularly likely to

be left in the lurch.

Currently, only 20 states have SPFs and most fail to provide adequate relief to harmed students and

many of those should be strengthened to adequately protect student borrowers.

Key Recommendations

The report describes specific ways states can amend their laws to strengthen or create SPFs. The

ideal SPF would do all of the following:

Maintain sufficient funds to pay all student claims and administrative costs;

Require each school to fund a surety bond sufficient to reimburse the SPF for losses caused by

that school;

Be maintained as one single fund that covers all for-profit schools, including degree-granting

schools and out-of-state schools offering distance education programs, as well as sham private

nonprofit schools that financially benefit their board members or owners;

Provide relief to parents and other people who financially contribute to a student’s education;

Establish a SPF claims limitations period, if any, that does not expire as long as any student

debt holder can seek repayment from the student;

Fully reimburse claimants for their total economic loss, including for all loans, grants, and

cash obtained by them or on their behalf to allow them to enroll in a higher education

program;

Provide relief based on group claims submitted by law enforcement agencies; and

Timely resolve SPF applications.

In addition, state agencies should:

Facilitate widespread student access to SPF relief through an easily accessible claims process;

and

Provide periodic public data regarding SPFs to state legislatures and governors.

Additional Resources

Learn more about NCLC’s policy work on student loans

NCLC’s Student Loan Borrower Assistance Project provides information about student loan

rights and responsibilities for borrowers and advocates.

Sign up for NCLC’s Student Loan blog.

Related Publications

For consumers: Surviving Debt (personal finance book) and Consumer Debt Advice (free

articles)

For attorneys: Student Loan Law

Final Debt Collection Rule: Part 2

January 7, 2021

The Consumer Financial Protection Bureau finalized part two of its debt collection rules on

December 18th. This webinar summarizes those rules.

Speakers:

Andrea Bopp Stark, Staff Attorney at the National Consumer Law Center

April Kuehnoff, Staff Attorney at the National Consumer Law Center

116th Congress (2019-20) – Archive

Access to Justice

S. 3913 (Cortez-Masto)/H.R. 7171 (Horsford) End Double Taxation of Successful Consumer

Claims Act. Senate Support Letter. House Support Letter.

S. 2627 (Cortez-Masto) End Double Taxation of Successful Civil Claims Act. Support.

S. 610 (Sen. Blumenthal)/H.R. 1423 (Rep. Johnson), Forced Arbitration Injustice Repeal (FAIR)

Act. Consumer support letter on House and Senate bills.

S. 630 (Sen. Brown) Arbitration Fairness for Consumers Act. Support.

S. 608 (Sen. Durbin) Court Legal Access and Student Support (CLASS) Act. Support.

Auto Sales and Financing

S. 1971 (Blumenthal) Used Car Safety Recall Repair Act. Support.

Bankruptcy Relief

Consumer Bankruptcy Reform Act of 2020 (Warren, Nadler). Support letter.

S. 1414 (Sen. Durbin) Student Borrower Bankruptcy Relief Act of 2019. Support.

H.R. 2648 (Rep. Nadler) Student Borrower Bankruptcy Relief Act, H.R. 2648. Support.

Consumer Financial Protection

(Sen. Harris) Accountability for Wall Street Executives Act of 2019. Support.

H.R. 1500 (Rep. Waters) Consumer First Act. Support letter.Coronavirus Relief

H.R. 8003 (Evans, Clay), Helping HOMES Act of 2020. Support.

H.R. 6800 (Lowey), Health and Economic Recovery Omnibus Emergency Solutions (HEROES)

Act. Support.

S. 3565 (Brown), Small Business and Consumer Debt Collection Emergency Relief Act of 2020.

Support.

Credit Reporting

Credit reporting provisions of the HEROES Act/S.3508. Support Letter.

H.R.5332 Protecting Your Credit Score Act. (Gottheimer). Support Letter

S. 1581/HR 6470 (Merkley, Porter) Medical Debt Relief Act of 2019. Support Letter.

S. 3508 (Schatz, Brown), Disaster Protection For Workers’ Credit Act. Support.

HR 3621 (Rep. Waters) Comprehensive Credit Reporting Enhancement, Disclosure,

Innovation, and Transparency Act of 2020. Support letter.

HR 3614 Restricting Use of Credit Checks for Employment Decisions Act. Support.

HR 3618 Free Credit Scores for Consumers Act. Support.

HR 3622 Restoring Unfairly Impaired Credit and Protecting Consumers Act. Support.

HR 3642 Improving Credit Reporting for All Consumers Act. Support.

HR 3629 Clarity in Credit Score Formation Act. Support.

HR 3621 Student Borrower Credit Improvement Act. Support.

S. 2685 (Senators Reed and Van Hollen) Consumer Credit Control Act. Support letter.

Accurate Access to Credit Information Act of 2019. Support letter.

S. 1336 (Senators Warren and Warner) Data Breach Prevention and Compensation Act.

Support.

S. 3508 (Senators Schatz and Brown) The Disaster Protection for Workers’ Credit Act.

Support.

Criminal Justice

S. 4186, Driving for Opportunity Act of 2020, Support Letter.

MA H 4652, An Act Regarding Decarceration and COVID-19, Support Testimony.

H.R. 6389 (Rep. Rush). Martha Wright Prison Phone Justice Act. Support.

H.R. 6061 (Rep. Nadler). The State Justice Improvement Act. Support.

H.R. 3948 (Rep. Meeks). Debt Collection Practices Harmonization Act of 2019. Support.

S. 1764 (Sens. Duckworth, Portman, Schatz, Booker, King, Markey). Martha Wright-Reed Just

and Reasonable Communications Act of 2019. Support letter.

Debt Collection

S.4697 (Murphy, Van Hollen) Strengthening Consumer Protections and Medical Debt

Transparency Act. Support.

S. 4350 (Van Hollen, Murphy) COVID-19 Medical Debt Collection Relief Act. Support.

MA H. 4694/S. 2734, Debt Collection Fairness Act. House Support Letter. Senate Support

Letter. Group Support Letter.

S. 3841 (Grassley) protecting stimulus payments from garnishment. Joint consumer-bank

support letter.

Conn. H.B. 5427, An Act Concerning Issues Relating to Debt Collection §§ 1, 2 and 3. Support

testimony.

H.R. 5934 (Rep. Bonamici) Securing Consumers against Misrepresented Debt Act of 2020.

Support.H.R. 5330 (Rep. Tlaib), Consumer Protection for Medical Debt Collections Act. Support letter.

H.R. 4403 (Rep. Cleaver), the Stop Debt Collection Abuse Act. Support.

H.R. 5001 (Rep. Clay), Non-Judicial Foreclosure Debt Collection Clarification Act. Support.

H.R.5003 (Rep. Dean), Fair Debt Collection Practices for Servicemembers Act. Support.

H.R. 5021 (Rep. Pressley), Ending Debt Collection Harassment Act of 2019. Support.

H.R. 3948 (Rep. Meeks). Debt Collection Practices Harmonization Act of 2019. Support.

Earned Income Tax Credit

H.R. 3157 (Rep. Kildee), S. 1138 (Sen. Brown) Working Family Tax Relief Act. Support letter to

Senate and House.

Electronic Communications

S. 4159 (Thune), E-Sign Modernization Act. Oppose.

Fair Lending

H.R. 149 (Green), Housing Fairness Act. Support.

H.R. 2324 (Rep. Garcia) /S. 1205 (Sen. Gillibrand), Protections in Consumer Lending Act.

Support.

Housing

H.R. 6729 (Rep. Scott)/ S. 3620 (Senator Reed), COVID-19 Homeowner Assistance Fund Act of

2020. Support.

H.R. 8003 (Evans, Clay), Helping HOMES Act of 2020. Support.

H.R. 6794 (Rep. Vargas), Promoting Access to Credit for Homebuyers Act of 2020. Support.

H.R. 6835 (Rep. Porter), to require residential mortgage servicers receiving certain emergency

relief under the CARES Act to provide reports on loan-level data. Support.

H.R. 7386 (Finkenauer) Helping Owners Meet Essential Standards (HOMES) Act of 2020.

Support.

S. 3509 (Brown) To Protect American Families Facing Financial Hardship or Foreclosure Due

to a Declared Disaster, Including Covid-19. Support.

H.R. 5001 (Rep. Clay), Non-Judicial Foreclosure Debt Collection Clarification Act. Support.

H.R. 5931 (Rep. Clay), Improving FHA Support for Small Dollar Mortgages Act of 2020.

Support.

H.R. 2445 (Rep. Emmer and Foster), Self-Employed Mortgage Access Act of 2019. Support.

H.R. 4783 (Reps. Green, Chu, Garcia and Clay), LEP Data Acquisition in Mortgage Lending Act

of 2019. Support.

H.R. 3141 (Rep. Phillips) FHA Loan Affordability Act of 2019. Support.

S. 2279 (Sen. Cortez Masto)/H.R. 3958 (Rep. Waters), FHA Foreclosure Prevention Act.

Support.

S. 571 (Sen. Merkley) Residential Rent to Own Protection Act. Support.

S. 787 (Sen. Warren) American Housing and Economic Mobility Act of 2019. Support letter.

S. 331 (Sen. Cortez Masto)/H.R. 936 (Rep. Velasquez), Home Loan Quality Transparency Act.

Support.

S. 3508 (Schatz, Brown), Disaster Protection For Workers’ Credit Act. Support.

Overdraft Fees

S. 1595 (Booker), Stop Overdraft Profiteering Act of 2019. Support.

H.R. 4254 (Rep. Maloney), Overdraft Protection Act of 2019. Support.Payday Loans

H.R. 5050 and S. 2833 (Rep. J. Garcia and Sen. Merkley), Veterans and Consumers Fair Credit

Act. Support.

Calif. SB 472. NCLC opposition letter.

Indiana SB 613. NCLC & CRL analysis.

Payments

H.R. 2650 (Payne)/S. 4145 (Menendez), Payment Choice Act. Group Support Letter. Press

Release.

Privacy and Data Breaches

Coalition letter urging Congress to prioritize civil rights in upcoming privacy legislation, Feb.

13, 2019

Student Loans

H.R. (Pressley, Omar), Student Debt Emergency Relief Act. Support.

H.R. 5114, the Stop EITC and CTC Seizures Act, led by Rep. Sylvia Garcia (D-TX).

H.R. 2991, the Protection of Social Security Benefits Restoration Act, led by Rep. Raul Grijalva

(D-AZ).

H.R. 3764 – Justice for Student Borrowers Act (Scanlon). Support.

HR 3621 Student Borrower Credit Improvement Act. Support.

H.R. 5241 (Krishnamoorthi), Protecting Students from Worthless Degrees Act. Support.

H.R. 3512 and S. 867 (Rep. Lee and Sen. Durbin) Borrower Defense Congressional Review Act

repeal. Support letter.

H.R. 2486 and S.1279 (Rep. Adams and Sen. Jones)- FUTURE Act. Support letter to Senate.

S. 1153 (Senators Baldwin, Braun, Shaheen and Fischer) Stop Student Debt Relief Scams Act

of 2019. Support.

NCLC 2021 Federal Priorities

2021 Consumer Protection Federal Priorities

2021 Consumer Protection Priorities for a Covid Stimulus Package

Banking

2021 Banking Agency Predatory Lending and Safe Banking Priorities

Credit Reporting

2021 Credit & Consumer Reporting Priorities to Promote Economic RecoveryDebt Collection

The CFPB Must Issue Emergency Guidance on Debt Collection during the Pandemic

How Congress and the CFPB Can Protect Americans from Abusive Debt Collection

Medical Debt

COVID-19 Medical Debt: First 100 Day Priorities for the Biden Administration

Housing

NCLC Foreclosure Prevention & Mortgage Lending Priorities

Priorities for CFPB

Priorities for HUD, FHFA, & USDA

Robocalls

How Congress and the FCC Can Protect Americans from Invasive and Dangerous Robocalls

and Robotexts

Student Loans

2021 Federal Priorities for the Student Debt Crisis

Utilities and Communications

Energy, Water, and Communications Priorities for COVID Relief & Biden’s First 100 Days

Final Debt Collection Rule: Part 1

November 6, 2020

The Consumer Financial Protection Bureau finalized part one of its debt collection rules on October

30th. This webinar summarizes those rules.

Speakers:

Andrea Bopp Stark, Staff Attorney at the National Consumer Law Center

April Kuehnoff, Staff Attorney at the National Consumer Law CenterSamuel R. Shepard, N. Neal Pike Fellow

Sam Shepard is the N. Neal Pike Fellow at NCLC working to develop

resources that help Americans with physical, intellectual, developmental, or other disabilities use

consumer law protections to seek justice. In 2019, Sam was a Hobbs Fellow at NCLC. Previously, he

worked as a judicial intern for Judge Ojetta Rogeriee Thompson on the First Circuit Court of

Appeals. He received his B.A. from Brown University and graduated cum laude from Boston

University School of Law.

Help 9 Million People Get Their Stimulus

PaymentSpread the Word! Deadlines

Approaching for Unclaimed Stimulus

Payments

The Coronavirus Aid, Relief, and Economic Security (CARES) Act provided economic impact

payments to individuals up to $1,200 and $500 for each qualified child to help dampen the impact of

the economic fallout of COVID-19. Most people have already received their payments.

But about 9 million people who make so little they do not file taxes have not claimed their

payment, and they have a November 21 deadline to do so in order to receive the payment in 2020.

This group includes very low-income families with children, people disconnected from work

opportunities for a long period, many low-income adult-only households, and low-income individuals

who receive Social Security or Supplemental Security Income. A simple IRS form they may not know

about now stands between them and their much-needed stimulus funds.

Help spread the word about the November 21, 2020 deadline for non-filers to

complete the IRS form to receive their full Economic Impact Payment.

The Center on Budget and Policy Priorities (CBPP) estimates there are 9 million people who are

eligible for Economic Impact Payments (EIP) but must file an online form with the IRS by November

21 to claim the funds this year. Otherwise, they must file a 2020 tax return next year to receive the

payment in 2021. The CBPP report provides demographic information, state by state numbers,

and suggestions for steps that states, as well as community and legal service providers, can take to

help the most vulnerable individuals claim the substantial economic stimulus payment.

The best way to claim the payment is to use the Non-Filers: Enter Payment Info Here link on the IRS

website. But it is also possible to print and mail the information. Instructions on how to do so are on

the IRS Economic Impact Payment Information Center in the answers to the questions. “Can I

print information to register me for the Payment if I use the Non-Filers: Enter Payment Info Here

tool?” and “May I mail Form 1040 or Form 1040-SR with information Necessary for my Payment

instead of using the Non-Filers: Enter Payment Info Here tool?”

Resources

Questions about stimulus payments are on the IRS website in the Economic Impact Payment

Information Center and for those on Social Security or retired railroad workers and veterans.

CBPP has resources to support EIP outreach work, including flyers, press release templates, FAQs,

and additional outreach tools. Please also spread the word that people who received an EIP prepaid

card should activate it or replace it to receive their money.

And save the date: Nov. 10 is the National EIP Registration Day to help reach more non-filers.

More information

Center for Budget and Policy Priorities: Aggressive State Outreach Can Help Reach the12 Million Non-Filers Eligible for Stimulus Payment

Center for Budget and Policy Priorities: Stimulus Payments Outreach Resources

NCLC: IRS Sending Letters About Unactivated Stimulus Prepaid Cards

NCLC: The EIP Stimulus Payment Prepaid Card: Not a Scam; How to Avoid Fees

(sample card and mailer)

NCLC’s COVID-19 website (continually updated) has extensive information on responses to

the crisis, including state-by-state information on orders that have been issued

Litigating Bail Cases: Using Consumer Laws

to Challenge Commercial Bail Industry

Practices

July 23, 2020

Lawsuits across the country are challenging commercial bail systems. This webinar will discuss how

consumer laws may be used to challenge abusive and unfair bail industry practices, as well as

litigation strategies and obstacles.

Speakers:

Alex Kornya, Iowa Legal Aid

Ivy Wang, Southern Poverty Law Center

Ariel Nelson, Staff Attorney at the National Consumer Law Center

Urge the Senate to Pass Another Stimulus

Package!Urge your U.S. Senators to

help families and the

economy recover from

COVID-19 by passing the

HEROES Act

The coronavirus crisis is continuing, and the economic crisis is devastating families. With close to 50

million people unemployed, many more with reduced hours, and full economic recovery nowhere in

sight, we need another stimulus package to help the economy recover and to prevent debt loads

from destroying families for years to come.

The U.S. House of Representatives has passed the HEROES Act and now the

Senate must do the same!

The HEROES Act is a $3 trillion dollar package in response to the COVID-19 crisis. In the consumer

area, the bill provides desperately needed help for families dealing with the economic crisis, beyond

the modest start in the previous CARES Act. The HEROES Act:

Provides immensely needed funds to help families cover necessities through increased

stimulus payments, extended unemployment benefits, and, for the poorest families, increased

support for food, rent, home energy, water, and basic broadband service.

Expands recently passed debt forbearance relief to most mortgages, federal and private

student loans, and rent.

Stops debt collection activities that endanger stimulus payments, wages, bank accounts,

homes, utilities, and cars.

Creates a path to recovery by halting negative credit reporting and by requiring creditors to

offer affordable repayment options.

Please email or call your U.S. Senators and tell them we need another

stimulus package to help the economy and families to recover, and ask them

to support the HEROES Act. Find contact information here.

Other Actions You Can Take

Write a letter to the editor of your local paper. Here’s how.

Tweet to your senators to pass the HEROES Act using #HEROESAct and #COVID19.

LEARN MORE about NCLC’s work on COVID-19 & Consumer Protections.

COVID-19 & Consumer Protections

Major Consumer Protections Announced in Response to COVID-19Protecting Against Creditor Seizure of Stimulus Checks

Mortgage Relief for Homeowners Affected by COVID-19

Surviving Debt: Expert Advice For Getting Out of Financial Trouble (free access to the digital

edition during the COVID-19 crisis via this link). Print books may be ordered at NCLC’s Digital

Library bookstore.

An Introduction to CARES Post-Forbearance

Options

May 28, 2020

This session will provide an introduction to post-forbearance options for borrowers obtaining

mortgage relief under the CARES Act. The program will review options available through FHA and

the GSEs based on the most recent guidance and information available.

Speakers:

Andrea Bopp Stark, Attorney at the National Consumer Law Center

Tara Twomey, Of Counsel to the National Consumer Law Center

Geoff Walsh, Attorney at the National Consumer Law Center

*Webinar starts 25 minutes into the recording

Additional Material: Covid-19 Mortgage ChartYou can also read