ICPAK FORENSIC AUDIT SEMINAR - Technology as a driver for fraud detection and investigation

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

www.pwc.com

Technology as a driver for

fraud detection and

investigation

ICPAK FORENSIC AUDIT

October 2017

SEMINAR

Strictl rivate

and Confidential

9October 2017

The ICT and fraud convergence

Technology as a driver for fraud detection and

investigation

Confidential Information for the sole benefit and use of PwC’s Client. 9October 2017

PwC October 2017 2

1 Insert Banner

Definitions and context

1. Fraud is deception intended to result in financial or personal gain

2. Computers & the internet are the two key distinct components of ICT

3. Cybercrime is economic crime using a computer and the internet as the primary

tool to commit fraud.

4. Traditional frauds schemes have been enhanced by computers & the

Technology as a driver for fraud detection and

investigation

Confidential Information for the sole benefit and use of PwC’s Client. 9October 2017

PwC October 2017 3

1 Insert Banner

Key

Statistics

and Trends

Technology as a driver for fraud detection and

investigation

Confidential Information for the sole benefit and use of PwC’s Client. 9October 2017

PwC October 2017 4

2 Insert Banner

Key statistics and trends

Technology as a driver for fraud detection and

investigation

Confidential Information for the sole benefit and use of PwC’s Client. 9October 2017

PwC October 2017 5

3 Insert Banner

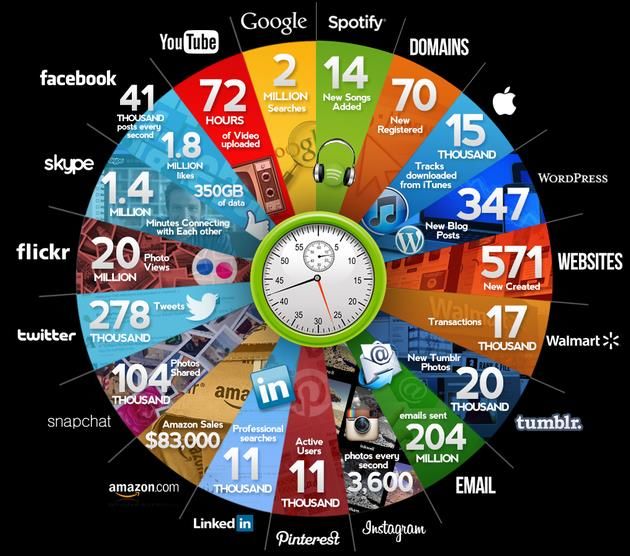

60 seconds online

• Minicomputer & Mainframe Files

• Web Servers

• Application Service Providers

• E-mail Systems

• Smart phones

• Laptop Computers

• Personal (Home) Computers

• Flash disks

• Optical Media & Tape Backups

• Cloud Storage

Technology as a driver for fraud detection and

investigation

Confidential Information for the sole benefit and use of PwC’s Client. 9October 2017

PwC October 2017 6

Key Stats Kenya

Population Population under 24

50.03 M 27.6M (60.22%)

Internet Penetration Annual Growth

40.5 M (91.77%) New users(60.6%)

(2016 - 39.6M)

Mobile Phone Penetration Landline Phones

44.13 M (88.2%) 0.2%

Sources: cck.go.ke

UN statistics

dalberg .com

cia.gov

PwC

3 Insert Banner

Digital Financial Inclusion

More Kenyans have had better access to financial services since the

introduction of mobile money

Technology as a driver for fraud detection and Source: World Bank estimates in 2010

investigation

Confidential Information for the sole benefit and use of PwC’s Client. 9October 2017

PwC October 2017 8

Section 3 – Insert Banner

E-Commerce in Kenya Obstacles to buying products online

Lack of Cost

o 77% of internet enabled mobile phone Security

users in Kenya buy products online

10.2%

o Favourite eCommerce sites include: OLX,

Rupu, Cellulant, Amazon, eBay, Google, 34.0%

Waptrick and your DMAs.

o Automated trading systems since 2009 30.9%

with online feeds and interfaces.

o Makiba – proposed mobile platform to sell

6.4%

government bonds.

Delivery

Lack of 18.6% Time

o The greatest obstacle for buying goods Options

online is lack of security

Internet

Connection

Technology as a driver for fraud detection and investigation

• ICPAK FORENSIC AUDIT SEMINAR Confidential Information for the sole benefit and use of PwC’s Client. 9October 2017

PwC October 2017 9

3 Insert Banner

Statistics on cyber crime and its impact

• Kenya lost Sh 15 Bn through cyber crime according to 2015 Cyber security report

• Public sector lost more that Sh 5 Bn followed by the financial services at Sh 4 Bn ;

• Top attacks came from overseas – US, China etc.

• Kenya has a strong business environment and education system but weaker physical

infrastructure;

• Introduction of cyber security in the Information and Communications Bill 2013; and

• More than 80% of SME’s expect that the internet will help them grow their business

and 70% of those expect to hire new employees as a result.

Technology as a driver for fraud detection and

investigation

Confidential Information for the sole benefit and use of PwC’s Client. 9October 2017

PwC October 2017 103 Insert Banner

Global economic impact of cybercrime in context

Drug

Trafficking USD$ 600B

Cybercrime

USD$ 300B – 1T

Piracy USD$ 1B- 16B

Technology as a driver for fraud detection and

investigation

Confidential Information for the sole benefit and use of PwC’s Client. 9October 2017

PwC October 2017 113 Insert Banner

Cybercrime facts for Kenyan organizations; GECs 2016

33% 61%

reported having reported rapid

been affected increase in perception

cybercrime. of cybercrime.

46%.

Said threat coming from

both internal and external

sources

*69% *18%

Saw IT Department Saw HR Department

as high risk as low risk

* Relatesas

Technology toa2011

driver survey

for fraud detection and

investigation

Confidential Information for the sole benefit and use of PwC’s Client. 9October 2017

PwC October 2017 124 Fraud risks posed by ICT

Fraud risks

posed by ICT

Technology as a driver for fraud detection and

investigation

Confidential Information for the sole benefit and use of PwC’s Client. 9October 2017

PwC October 2017 134 Fraud risks posed by ICT

Offers tremendous appeal to fraudsters

Same reward but fewer risks

Not physically present – less likely to be caught or “hurt” during the crime. Also less likely to

commit “ancillary” crimes like injuring other people or destroying property

Less chance that law enforcement can identify the perpetrator or establish where they were when

the crime was committed – 79% of Kenya respondents lack confidence in law enforcement

Perpetrators often in different jurisdiction – more difficult to identify, arrest and prosecute using

traditional means

FRAUD

Current laws are not mature enough to prosecute cybercriminals with sufficient impact.

Technological advancements are high-paced and therefore developments in cybercrimes too.

Organisations and governments will constantly need to keep updating their responses.

Preventative controls are much harder to implement for cybercrime than for instance asset

misappropriation

Technology as a driver for fraud detection and

investigation

Confidential Information for the sole benefit and use of PwC’s Client. 9October 2017

PwC October 2017 144 Fraud risks posed by ICT

Key risks posed by ICT include…

Function of the computer &

internet in crime:

• As an object – target of crime Data Unauthorised Internet

where contents are destroyed destruction access consumer

& sabotage fraud

• As a subject – provide

environment to commit crime

• As a tool – means of Securities

Identity Disclosure of

committing crime theft confidential

fraud

information

• As a symbol – offers

credibility that is often used to

deceive victims

Loss of Insider Enhances

customer threat conventional

confidence fraud

Technology as a driver for fraud detection and

investigation

Confidential Information for the sole benefit and use of PwC’s Client. 9October 2017

PwC October 2017 154 Fraud risks posed by ICT

Cybercrime has hit and remained in the headlines

Technology as a driver for fraud detection and

investigation

Confidential Information for the sole benefit and use of PwC’s Client. 9October 2017

PwC October 2017 165 Role of technology in preventing and detecting fraud

Role of

technology in

preventing and

detecting fraud

Technology as a driver for fraud detection and

investigation

Confidential Information for the sole benefit and use of PwC’s Client. 9October 2017

PwC October 2017 17Although difficult to examine, reducing computer fraud into

its basic elements often leads to successful determination

1. Lacks traditional paper trail Identify culprits

Methods of

2. Require understanding of technology

Difficulties

manipulation

used to commit fraud

Means of diversion

3. Require understanding of technology on or conversion of

the victim computer funds

4. Often requires use of one or more

specialist to assist the fraud examiner

+ + =

elements

Basic

Inputs Manipulation OutputsPreventing Fraud: Governance

The three lines of defence

What to do

then? Behavioral Deep

analytics learning

3 lines of defence Awareness Data

Forensic

initiatives visualisati- Compliance

– Governance, ons

tools

solutions

Detection

Oversight &

Operations Automated

controls Investigation

cells

They only be Prevention

strengthened by Cyber crime Flexible

response Real time

technology and strategy screening

audit plans

not replaced by

Bench Internal

it. marking controls

Understand

Regular the threat

security

assessmentPreventing Fraud:

Do organisations conduct risk assessments?

30% 26%

of Kenya respondents of Kenya respondents

have an incident say Board members

response plan quarterly review

organisations ability

to deal with cyber

These results are of concern given incidents

the rate at which cybercrime is

increasing, organisations do not Disappointing results in terms of

realise that they are a target of how often Board members within

cybercrime until long after the organisations in Kenya and Africa

damage is done. request information regarding the

organisations’ state of readiness to

deal with cyber incidents.Preventing Fraud: Key questions to ponder over 1.Do you really show the right tone at the top in dealing with cyber crime? 2. Does your organisation have an anti fraud policy / strategy including regular training? 3. How do you deal with fraud allegations? How do you deal with fraudsters when you uncover wrongdoing? 4.Is your organisation head truly “cyber savvy” and is your organisation able to detect and investigate cybercrime? 5.Does your organisation undertake regular cyber security assessment?

Detecting fraud using technology

Strategy

Identify

Capture & Process

Profile & Cull & Process

Search & ReviewDetecting Fraud: Digital Evidence Recovery The key priorities Acquire • Search and seize; and • Secure the evidence Process and preserve • Recover deleted items; • Avoid any tampering; and • Admissible legally Present • Simplify the evidence; and • Beware of inherent weaknesses in the bank’s internal controls.

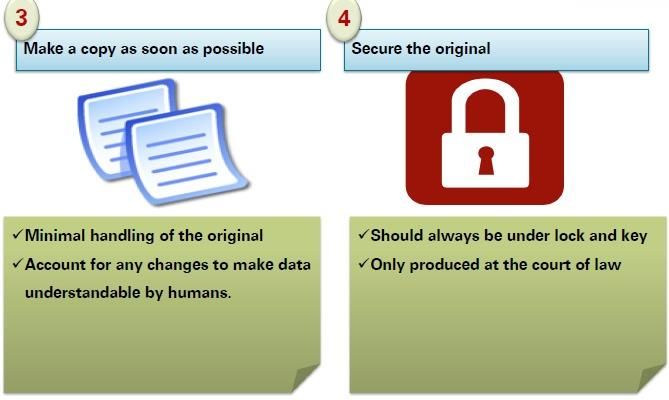

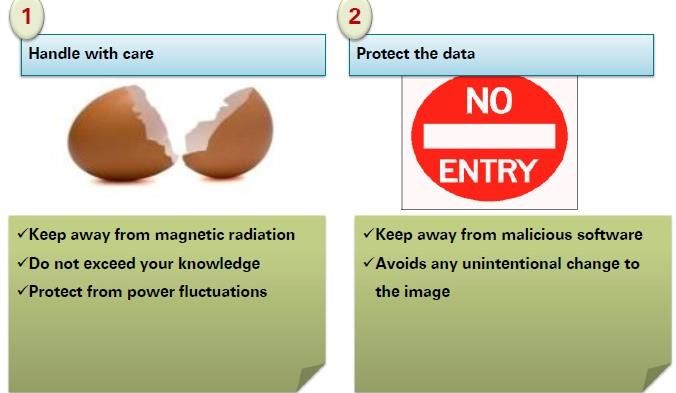

Digital Evidence Recovery: Four important points to remember

Digital Evidence Recovery: Four important points to remember

Detecting Fraud: Data Analytics WHY DATA ANALYTICS ? The primary reason to use data analytics to tackle fraud is because a lot of internal control systems have serious control weaknesses. In order to effectively test and monitor internal controls, organizations need to look at every transaction that takes place and test them against established parameters, across applications, across systems, from dissimilar applications and data sources. Most internal control systems simply cannot handle this. On top of that, as we implement internal systems, some controls are never even turned on. ounce of prevention = pound of cure

Detecting Fraud: Data Analytics

In the past you’d have to hit the lottery to find something big.

With the volume of transactions flowing through organizations today, the velocity of business has

increased tremendously because scrutiny of individual transactions is incredibly difficult to

provide. This lack of scrutiny over individual transactions opens up the gate for people to abuse

systems, perpetrate fraud, and materially impact financial results

“investigate transactions and

see if there’s anything to indicate

fraud or opportunities for fraud

to be perpetrated”Detecting Fraud: Proactive Data Analytics

An example is you’re looking at productions logs and you notice a spike in

Hour 4. What questions do you ask?

Investigate?

Ignore?Detecting Fraud: Sample results of relationship

mapping

Subject employee

Employees from

Shoddy Plumbing

Outsiders

Investigate?Detecting Fraud Do I need to investigate further ???

Detecting Fraud: Analytical Techniques

Remember, you’re looking for things that don’t appear to be normal.

■ Calculate statistical parameters and look for outliers or values that exceed averages or are

outside of standard deviations.

■ Look at high and low values and find anomalies there. Quite often it’s these sorts of anomalies

that are indicators of fraud.

■ Examine classification of data - group your data, all the transactions, into specific groups

based on something like location. Maybe a number of transactions are occurring outside

of statistical parameters. Where are they all from? Are they distributed evenly across the

whole population or are they all limited to a given geographical area? If they are then that’s

material and maybe you should delve deeper.

“Data analysis technology can quantify the

impact of fraud so you can actually see

how much it’s costing the organization and

provide a cost-effective program with

immediate returns.”Detecting Fraud : Application areas for Fraud Detection

“Fraudsters can and will exploit weaknesses

wherever they can find them”

Take a look at your General Ledger, especially

postings done after a closing period. Check into

frequently reversed accounts, or weekend

postings. Look at GL postings on a quarterly

basis and ask:

• Are these being done according to our

internal controls or are people trying to post

to the GL after our closing period?

• Are there certain GL accounts that are

frequently reversed?

• Are there dormant accounts that are used

suddenly?You can also read