Autofacts EU Market Update & Mobility Outlook ECG Conference Brussels 20-10-2017

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

www.autofacts.com

Autofacts®

EU Market Update & Mobility Outlook

ECG Conference Brussels

20-10-2017

Strictly private

and confidential

October 2017

Growth of new car registrations is beginning to slack off in Q3 – worse to be expected in Q4

After a strong start in the first quarter, registrations started to mellow in Q2. Incoming results of Q3 suggest that growth stalled over the three months, due to almost 9% decline in the

UK and Ireland, and top-line weakness in the German market which is shaken severely by doubts about the viability of Diesel cars. Nevertheless, Italy, France and Spain continued on

their recovery path, topped only by Poland and the Netherlands.

EU+EFTA: New Car Registrations by Top 12 Markets

YTD-Sep 2016 vs YTD-Sep 2017 (millions)

3,0 30%

2,5 20%

2,0 10%

1,5 0%

1,0 -10%

0,5 -20%

0,0 -30%

Germany United Italy France Spain Belgium Poland Netherlands Sweden Austria Ireland Switzerland

Kingdom YTD-Sep 2016 YTD-Sep 2017 YOY Change (R-Axis)

Source: ACEA, Autofacts Analysis

PwC Autofacts ® 2

Economic sentiment is approaching a historical high while growth may soften

GDP growth forecasts are forecasted to slow down in 2018, especially UK, Spain and Germany. In the UK, net investment activity has plunged by more than 30% in 2017, leaving its

show an overall acceleration in the Euro Zone, while several main countries mark on the current year as well as short-and mid-term growth prospects. Italy and France, however, are

expected to accelerate further, in line with high economic sentiment.

EA & Top 5: Real GDP Annual Growth EA & Top 5: Economic Sentiment Indicator

2016 – 2018F (percentage change) Sep 2014 – Sep 2017 (101 = long run average)

120

United

Kingdom

Spain

110

Italy

100

Germany

France 90

Euro Area

80

- 0,5% 1,0% 1,5% 2,0% 2,5% 3,0% 3,5% Sep Dec Mar Jun Sep Dec Mar Jun Sep Dec Mar Jun Sep

2014 2014 2015 2015 2015 2015 2016 2016 2016 2016 2017 2017 2017

2016 2017F 2018F EA DE FR IT ES UK

Source: IHS Markit, European Commission (October 2017)

PwC Autofacts ® 3Europe’s new passenger car market shows an increasing slow-down since Q2 2017

On a rolling 12-month average base, it seems that the European market has hit is cyclical high in summer 2017, and is moving towards a reversal of dynamics as the year continues. This

seems contradictory to recently-updated macroeconomic growth statistics and expectations, but is explicable through increasing insecurity about regulatory changes with ensuing

impacts on residual value expectations and – therefore – cost of financing.

EU+EFTA: Rolling 12 Months Car Registrations EU+EFTA: New Car Registration Variance

Sep 2008 – Sep 2017 (millions) 1990 – 2017F (millions)

17 5

28-year high

(1990-2017)

16

4

2017F

15

2016

3 28-year low

14 (1990-2017)

13

2

12

1

11

10 0

Sep Sep Sep Sep Sep Sep Sep Sep Sep Sep Germany France United Italy Spain Poland Czech

2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 Kingdom Republic

Rolling 12-Month Car Registrations Annual Registrations

Source: ACEA, Autofacts Analysis

PwC Autofacts ® 4Strong growth can appear due to totally different reasons

The Fiat and Mercedes-Benz brands both achieved sales of approximately 500k units year-to-date, and managed to grow at over 7% - only Fiat did so without any new product launch,

while Mercedes’ home market of Germany showed increasing weakness. Fiat, however, was bolstered by increasing demand in its core markets Italy, France and Spain, while Mercedes

continued to churn out new and upgraded products against weaker competition.

EU Top 5 Markets: Brands Sales Volume and Growth Rate* EU Top 5 Markets: Market Share*

YTD Sep 2016 vs. YTD Sep 2017 (thousands) YTD Sep 2016 vs. YTD Sep 2017 (percentage share)

1.000

Volkswagen

10,6%

Volkswagen Renault

800 7,4%

Renault 11,2% Ford

Ford 35,0%

7,3% Opel-Vauxhall

34,1%

600 Opel-Vauxhall Mercedes-Benz 7,3%

Peugeot Mercedes-Benz

7,5%

2017 Sep- 2016 YTD- Peugeot

Audi Fiat

YTD YTD 6,9% 6,3%

400 BMW Fiat

4,0% 5,9%

Audi

Citroen 5,4% 6,0% 6,1%

200 4,0% 5,9% 5,8% BMW

5,3% 6,1%

Citroen

5,8% 6,1%

Other

0

(8%) (6%) (4%) (2%) 0% 2% 4% 6% 8%

Source: ACEA, Autofacts Analysis *Only brands with official sales data included, commercial vehicles not included

PwC Autofacts ® 5Due to incoming actuals, Autofacts has adjusted to full-year forecast for EU to just 2.4% growth

The cyclical slowdown is now expected to continue into 2019 due to adjustments of the fuel and powertrain mix and technical compliance increasing vehicle prices. With weakening

residual values, financing costs for new vehicles will increase even in the absence of a central bank rate hike, pushing some incremental demand back into the used-car market. The

development in the United Kingdom remains a wild-card requiring close monitoring and quick reactions.

EU+EFTA: New Light Vehicle Registrations

2009 – 2023F (millions)

20 10%

18

16 6%

14

12 2%

10

8 (2%)

6

4 (6%)

2

- (10%)

2009 2010 2011 2012 2013 2014 2015 2016 2017F 2018F 2019F 2020F 2021F 2022F 2023F

Car Registrations LCV Registratons YOY Change (R-Axis)

Source: ACEA, Autofacts Analysis

PwC Autofacts ® 6New products and continuous investments in plants are expected to keep utilization above 80%

The European light vehicle assembly is expected to remain strong as domestic and non-domestic OEMs launch new products and invest in plant upgrades and expansions, which could

push volumes to over 20m units by 2020. In 2016, European light vehicle assembly grew by 3.4% to 18.7m units and is assumed to grow more than 250k units to 19.0m units in 2017,

keeping overall plant utilization at a sustainable level of more than 80% in 2017 and for the foreseeable future.

EU: Light Vehicle Assembly

2009 – 2023F (millions)

25 100%

3,4 3,6 3,6 3,6

3,5 3,9

3,7 3,5

20 3,6 80%

4,7 4,1 5,4 4,5

4,7

5,8

15 60%

10 19,6 20,4 20,5 20,5 20,4 40%

18,7 19,0 19,4

18,1

16,2 16,9 16,0 16,1 16,8

14,7

5 20%

- 0%

2009 2010 2011 2012 2013 2014 2015 2016 2017F 2018F 2019F 2020F 2021F 2022F 2023F

Assembly Volume Excess Capacity Utilisation (R-Axis)

Source: Autofacts 2017 Q4 Forecast Release

PwC Autofacts ® 7The enlarged PSA Group still has a long way to realize possible synergies

With expected 3.1 million units production in 2017 and strong growth outlook due to the expansion of the SUV/ Crossover product portfolio, the PSA group is one of the most active

market movers in Europe. Still, as product portfolio and operations are not yet aligned, the economics of the take-over remain challenging. Both Daimler and BMW are expected to

increase their product portfolio and output over the next 5 years, while overseas manufacturers seem locked into their current European footprint.

EU: Top 10 Alliance Groups

2016 vs 2023F (millions)

6 5%

5,4

5,1

5 4%

4 3%

3,5

3,1

3 2%

2,3 2,3

1,9

2 1,8 1,8 1%

1,5 1,5

1,2 1,1 1,2

1 0,7 0,7 0%

0,6 0,5 0,5 0,4

0 -1%

VW PSA* RNM** Daimler BMW FCA Ford Hyundai Tata Toyota

2016 2023F CAGR (R-Axis)

Source: Autofacts 2017 Q4 Forecast Release *PSA incl. GM Europe (Opel-Vauxhall) **Renault-Nissan-Mitsubishi

PwC Autofacts ® 8The mix of powertrains installed in the EU is going to align further to global standards

In order to meet emission requirements, downsizing and electrified vehicles are expected to gain market share in the near future. Since performance is still a valid consumer need,

Autofacts expects manufacturers and technology partners to focus further on turbocharged engines. Further, by 2023 almost 20% of all vehicles, compared to 3.2% in 2016, are

forecasted to have an electrified powertrain – increasing growth of the hybrid figure depends on further decline of Diesel engines.

Average Engine Displacement Technology Outlook Vehicle Propulsion

2016 – 2023F (cubic centimeters) 2016 vs 2023F (percentage share) 2016 vs 2023F (percentage share)

1.800 100%

1,3%

74,7% 74,4%

75%

1.700

50% 48,8%

2016

1.600 47,9%

25% 16,4%

8,0% 9,6% 10,9%

1.500 0%

2016 2017F 2018F 2019F 2020F 2021F 2022F 2023F 2016 2023F

Single Turbo Twin-Turbo Naturally Aspirated

5,2%

5,8%

Engine Share by Cylinder Number Trans. Share by Gear Count

2016 – 2023F (percentage share) 2016 – 2023F (percentage share) 8,7%

100% 100%

75% 75% 46,0%

50% 50% 2023F

25% 25%

0% 0% 34,4%

2016 2017F 2018F 2019F 2020F 2021F 2022F 2016 2017F 2018F 2019F 2020F 2021F 2022F 2023F

I2 I3 I4 I5 I6/H6/V6 V8 Other 4 5 6 7 8 9 10 Electric CVT Diesel Hybrid* PHEV

Source: Autofacts 2017 Q4 Forecast Release *Includes mild & full hybrids

Electric Fuel Cell Gasoline

PwC Autofacts ® 9Alternative drivetrains will become the most important growth area in upcoming years

The installation of alternative drivetrains in light vehicles that are manufactures in the EU is forecasted to grow substantially in numbers by more than 510% or 3.4m units, summing up

to more than 4.0m units by 2023. Fully electric and hybrid powertrains are regarded as necessary to achieve the European CO2 emission targets by lowering fuel consumption –

especially as declining Diesel sales make the challenge even more daunting. Regulations beyond 2021 are still under discussion.

EU Powertrain: Alternative Engine Type Distribution EU Powertrain: Hybrid Distribution**

2016 vs. 2023F (thousands) 2016 vs. 2023F (thousands)

5.000 5.000

4.023

891

4.000 4.000

2.968

973 2.083

3.000 3.000

1.448

2.000 2.000

443

1.000 1.000

606 106

442

- -

2016 Increase Increase Increase Increase 2023F 2016 Increase Increase 2023F

Full Hybrid Mild Hybrid Plug-In Hybrid BEV/FCV* Diesel Gasoline

Hybrid Hybrid

Source: Autofacts 2017 Q4 Forecast Release *BEV = Battery Electric Vehicle, FCV = Fuel Cell Vehicle **excl. BEV/FCV

PwC Autofacts ® 10“It’s gonna be so eascy”

shared

autonomous connected

s

a c

electrified e y yearly

updated

PwC Autofacts ® 11The user will be able to choose from a menu of mobility forms

grouped between the coordinates vehicle driver vs. vehicle owner

The four form of mobility of the future

Machine

Autonomous Autonomous

The primary use-case private-vehicle shared-vehicle Autonomous vehicles will

is car sharing in urban have a positive impact on

areas. Driver sharing-concepts.

An increasing amount of Autonomous and shared

young people living in mobility will expand the scope

cities do not own a car of application for electric

and use the car sharing vehicles.

concept in combination

with public transport. Personally-driven Personally-driven

private-vehicle shared-vehicle

Man

Private Vehicle Owner Shared

Source: PwC eascy-Study

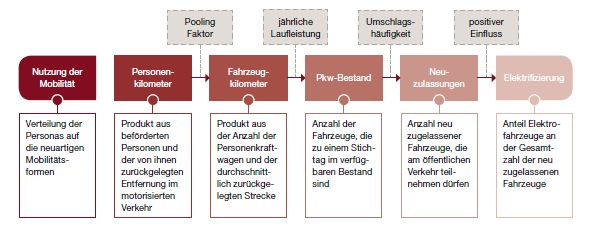

PwC Autofacts ® 13The basis for modelling the results is the forecast of the person-

kilometres and the pooling factor

Pooling Annual Turnover Positive

factor mileage rate effects

Usage of Passenger- vehicle- New

vehicle- Electrification

Mobility kilometres kilometres registrations

Stock

Distribution of Result of the Result of the Amount of Amount of new Electric

the personas transported amount of vehicles that registered vehicles share

to passengers vehicles and have been in vehicles that of the total

the new and their their average stock on a are allowed to number of

mobility forms driven distance mileage certain day participate in new-registered

in motorized the public vehicles

traffic traffic

Source: PwC eascy-Study

PwC Autofacts ® 16Despite current scepticism, it is estimated that 40% of all vehicle

kilometres will be driven autonomously or shared in 2030

Germany: Distribution of mobility forms Germany: Vehicle kilometres

2017-2030 (in percent) 2017-2030 (in billion kilometres)

100% 900

90% 800

80%

700

70%

600

60%

500

50%

400

40%

300

30%

200

20%

10% 100

0% 0

2017 2018 2019 2020 2021 2022 2023 2024 2025 2026 2027 2028 2029 2030 2017 2018 2019 2020 2021 2022 2023 2024 2025 2026 2027 2028 2029 2030

Personally-driven Personally-driven Autonomous Autonomous

Source: PwC eascy-Study private-vehicle shared-vehicle private-vehicle shared-vehicle

PwC Autofacts ® 18In Germany, vehicle stocks could drop by 20% by 2030 - but new

registrations would rise by almost 20 percent in total

Germany: Stock by mobility forms Germany: Registrations by mobility forms

2017-2030 (in million) 2017-2030 (in thousand)

50 6.000

45

5.000

40

35

4.000

30

25 3.000

20

2.000

15

10

1.000

5

0 0

2017 2018 2019 2020 2021 2022 2023 2024 2025 2026 2027 2028 2029 2030 2017 2018 2019 2020 2021 2022 2023 2024 2025 2026 2027 2028 2029 2030

Personally-driven Personally-driven Autonomous Autonomous

Source: PwC eascy-Study private-vehicle shared-vehicle private-vehicle shared-vehicle

PwC Autofacts ® 19In Germany, hybrid drives will play an important role in the

short-term - until 2025 electric vehicles are gaining importance

Germany: Registrations by drive types Germany: Stock of drive types

2017-2030 (in percent) 2017-2030 (in million)

100% 50

90% 45

80% 40

70% 35

60% 30

50% 25

40% 20

30% 15

20% 10

10% 5

0% 0

2017 2018 2019 2020 2021 2022 2023 2024 2025 2026 2027 2028 2029 2030 2017 2018 2019 2020 2021 2022 2023 2024 2025 2026 2027 2028 2029 2030

Combustion Hybrid Electric Combustion Hybrid Electric

Combustion Hybrid Electric

Source: PwC eascy-Study

PwC Autofacts ® 20In 2030, the transition to electrified and (partially) autonomous

vehicles will be in full swing – starting with new registrations

Europe: Vehicle stock Europe: Drive types distribution on new registrations

2017-2030 (in million) 2017-2030 (in million)

350 25

300

20

250

15

200

150

10

100

5

50

0 0

2017 2018 2019 2020 2021 2022 2023 2024 2025 2026 2027 2028 2029 2030 2017 2018 2019 2020 2021 2022 2023 2024 2025 2026 2027 2028 2029 2030

Personally-driven Personally-driven Autonomous Autonomous

Combustion Hybrid Electric

private-vehicle shared-vehicle private-vehicle shared-vehicle

Source: PwC eascy-Study

PwC Autofacts ® 21Contact

Christoph Stürmer

Global Lead Analyst

PwC Germany (Europe)

T: +49 69 9585 6269

E: christoph.stuermer@de.pwc.com

PwC Autofacts ® 22Autofacts – Dedicated to the Automotive Industry

Scan and download the free Autofacts App

Autofacts ®

The information contained in this report represents the culmination of proprietary research conducted by Autofacts, an analytical group within PwC. All material contained in this report was developed independently of any

PwC client relationship and does not represent the firm’s view as an auditor to any legal business entity. While every effort has been made to ensure the quality of information provided, no representation or warranty of any

kind (whether expressed or implied) is given by PwC as to the accuracy, completeness or fitness for any purpose of this document. As such, this document does not constitute the giving of investment advice, nor a part of

any advice on investment decisions. Accordingly, regardless of the form of action, whether in contract, tort or otherwise, and to the extent permitted by applicable law, PwC accepts no liability of any kind and disclaims all

responsibility for the consequences of any person acting or refraining from acting in reliance on this document.

©2016 PwC. All rights reserved. “PwC” refers to PricewaterhouseCoopers LLP (a Delaware limited liability partnership) or, as the context requires, other member firms of PricewaterhouseCoopers International Ltd., each of

which is a separate and independent legal entity. “Autofacts” is a globally registered trademark of PwC.

PwC Autofacts ® 23You can also read