IL TUFFATORE, THE DEBT-FUELLED DYNAMIC ACCELERATES - HOUSE VIEW MAY 2020 - Banca March

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

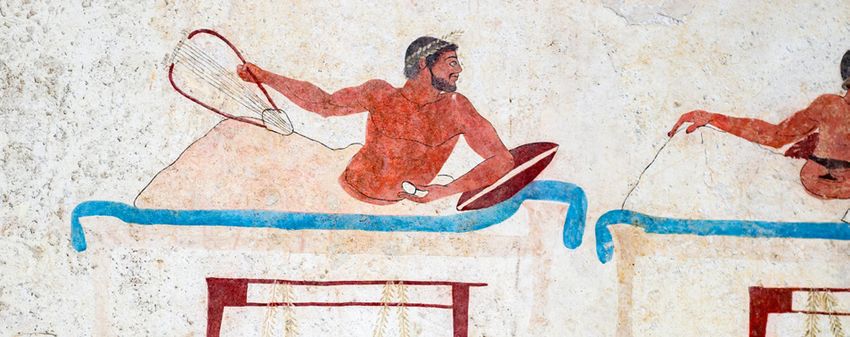

Il Tuffatore. The Tomb of the Diver.

Paestum. Magna Grecia. 450 a.C.

HOUSE VIEW

MAY 2020

IL TUFFATORE,

THE DEBT-FUELLED

DYNAMIC ACCELERATES

HOUSE VIEW. MAY 2020

IL TUFFATORE, THE DEBT-FUELLED DYNAMIC ACCELERATES

Perhaps one of the most accurate representations of what lies ahead for the global economy is depicted in the

images of the Tomb of the Diver, in Paestum. This fresco, located in an Etruscan tomb that dates back 2,500

years, depicts a swimmer diving headfirst from the Pillars of Hercules. As the global economy crashes and the

deepest recession since the Great Depression beckons, the unforgiving gravity that compels the diver towards

the water speaks eloquent volumes. But that is not the only story this fresco tells. A tomb is the place where the

transmutation from death to reconstruction takes place, and the swimmer is a metaphor for the transition from

the world we know to what lies beyond: an unprecedented paralysis of economic activity and a decisive response

by the authorities.

As we discussed last month in The Spring Offensive, or Kaiserschlacht, governments and central banks have

shown steely determination in their response to collapsing economic activity. In some respects, the consequences

of Covid-19 are on a par with the impact of a war; in fact, the death toll from the disease in the US has surpassed

the number of Americans killed in the Vietnam War by 20%. The response by the US government, measured in

terms of fiscal deficit, has been more robust than its response to most past conflicts.

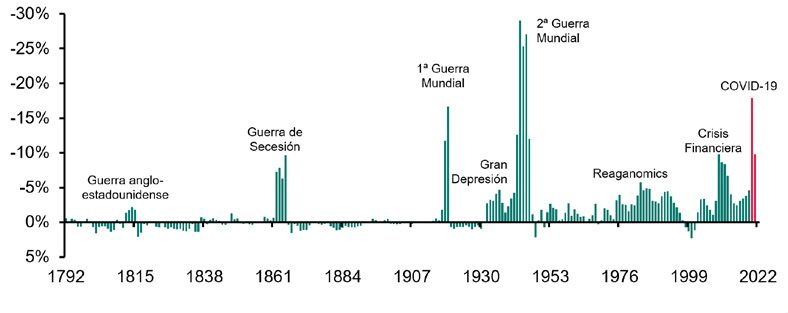

1. FISCAL BALANCE US FEDERAL GOVERNMENT / GDP

Source: US Government Spending. Estimates 2020 and 2021 Congressional Budget Office. Banca March

World War 2

COVID-19

World War 1

Financial

American Civil War

crisis

Great

Depression Reaganomics

War of 1812

Graph 1 provides the historical context for the extraordinary 17.9% deficit to be reached this year, following the US

government’s decision to step up aid for small businesses; the only time the deficit has surpassed this level was in

the Second World War.

As time goes by, the Spring Offensive continues, and the world continues to step up its stimulus measures.

Governments are increasing tax aid packages and expanding credit lines and state-backed loan guarantees, whilst

central banks are ramping up the volume of asset purchases (graph 2). In April, they also lowered the minimum

credit ratings on the assets they are prepared to buy. The Fed is to start buying fallen angels - issuers that lose their

investment grade rating during the crisis - and the ECB has made fallen angel bonds collateral eligible.

IL TUFFATORE, THE DEBT-FUELLED DYNAMIC ACCELERATES 2

HOUSE VIEW. MAY 2020

2. STIMULUS MEASURES 3. CENTRAL BANK BALANCE SHEETS

Source: Bloomberg, Bruegel and Banca March Source: Bloomberg and Banca March

Size of balance sheet (%GDP)

4.000 60% 60

50% 50

COVID-19

+16,7 p.p.

3.000 FED BCE

40%

x €bn

40

2.000 30% Sovereign debt crisis

+10,1 p.p.

QE III

20% 30 +7,9 p.p.

1.000 Financial crisis COVID-19

+23,9 p.p.

10% +5,1 p.p.

20

0 0%

Eurozone United Kingdom US 10

Immediate fiscal support Deferred payments Financial crisis

+9,1 p.p.

Credit lines and guarantees Monetary 0

06 07 08 09 10 10 11 12 13 14 15 16 17 18 19 20

Total % GDP (right)

Graph 3 shows the rate at which central bank balance sheets have swelled; the Federal Reserve, for example, will

double its balance sheet before the end of the year, jumping from 19% of GDP pre-Covid to 43%. The ECB is set

to expand its balance sheet from 39.2% to 56% of GDP. Taking these fiscal measures in conjunction with the lines

of financing and central bank asset purchases, the combined response is enormous; it will total 34% of GDP in

the US and in Europe, where the figures will be impacted more by the lines of credit announced, total stimulus

measures could stand at 48% of GDP. It is important to point out, however, that the immediate fiscal measures

announced in the US are almost three times higher than the measures announced in Europe (9.1% of GDP versus

3.3%, as represented by the dark green lines on graph 2) and that the real, 100% implementation of credit lines

will take time, and remains to be seen.

As we begin to see the first lockdown de-escalation measures and the next set of macro data reveals an ongoing

peak in the paralysis of economic activity, this combined raft of stimulus measures will mitigate the economic

shock, reduce the impact on companies’ solvency, facilitate liquidity and provide a firm support level for credit

and equities. As investors, now the initial panic has subsided, we must focus on the speed at which we are likely

to return to previous growth rates; as we will explore below, this will not happen quickly, and we will need to be

patient.

The only problem with these desperate, effective, practically inescapable measures by regulators is that over the

medium term, there will be even more debt to service, and debt levels were already high. This will hamstring

the growth potential of an economy that was already seeing growth tapering off, which means the debt-fuelled

dynamic - which has grown relentlessly in previous economic crises - has accelerated further still.

The Tomb of the Diver. Left lateral wall. Paestum. 450 BC

IL TUFFATORE, THE DEBT-FUELLED DYNAMIC ACCELERATES 3

HOUSE VIEW. MAY 2020 In The Tomb of the Diver, as well as the diver himself, there is a reclining man holding an egg, the universal symbol of renewal and rebirth. The figure is believed to be Dionysus, the ancient Greek god of wine and fertility. The coronavirus has brought death, quarantine and desperation to find the right measures to help us overcome the struggle. If one thing is clear, however, it is that as we emerge from this crisis, the existing dynamic has accelerated: debt to subsidise a world without growth, interest rates at zero interest and central banks picking up the tab. Our new isolated way of life will also mean more technology, digitalisation and e-commerce. Joan Bonet Majó Chief Investment Strategist IL TUFFATORE, THE DEBT-FUELLED DYNAMIC ACCELERATES 4

HOUSE VIEW MAY 2020 THE FIRST STEPS TOWARDS NORMALITY

HOUSE VIEW. MAY 2020

THE FIRST STEPS TOWARDS NORMALITY

ASSET ALLOCATION

ASSET CLASS -2 -1 NEUTRAL +1 +2

LIQUIDITY

FIXED-INCOME

EQUITY

ALTERNATIVE

FIXED-INCOME -2 -1 NEUTRAL +1 +2

SOVEREIGN DEBT

High quality (AAA)

Peripheral

CORPORATE BONDS

Investment Grade

High Yield

EMERGING DEBT

CONVERTIBLE BONDS

EQUITIES -2 -1 NEUTRAL +1 +2

EUROPE

United Kingdom

UNITED STATES

EMERGING

REST OF THE WORLD

CURRENCIES -2 -1 NEUTRAL +1 +2

U.S. DOLLAR

STERLING POUND

MACROECONOMIC LANDSCAPE

With the worst of the pandemic now behind us, the de-escalation plans commence.

With an official Covid-19 tally of over three million cases, two hundred thousand deaths and more than a million

recoveries, the world is beginning to emerge from the lethargy of lockdown and de-escalation plans are starting to

take shape. The worst is now behind us and we are heading into a new phase, as we slowly seek some semblance

of normality, plagued by the fear that lifting lockdown too soon could trigger a new wave of the epidemic.

THE FIRST STEPS TOWARDS NORMALITY 6HOUSE VIEW. MAY 2020

In Asia, lockdown in the Chinese city of Wuhan was officially lifted on 8 April, and in the rest of China, the

measures were lifted depending on the degree to which each region was affected. The proportion of companies

that have resumed activity in the country as a whole stands at 97.6%, and production is at 82.8%. Schools are

beginning to open, as is domestic tourism, following the symbolic opening of Beijing’s Forbidden City. South

Korea’s successful Covid-19 strategy has been based on information, medicine and technology. In late April, the

country had reported no deaths from the pandemic and economic activity was starting to gain traction.

In Europe, de-escalation plans are getting underway, but will be rolled out more gradually than in China, with

a delay of around one month in Spain. Spearheading the de-escalation are Denmark - schools are open and

hairdressers are operating at a healthy clip - as well as Austria and Germany, where some smaller establishments,

including certain museums, are now open. On the continent, plans to open schools are underway except in Spain,

Italy and Portuguese primary schools.

1. LOCKDOWN PERIOD BASED ON DURATION IN WUHAN

Source: Governments; Banca March

Start End*

Wuhan 23-jan. 8-apr.

Italy 10-mar. 25-may.

Denmark 13-mar. 28-may.

Spain 15-mar. 30-may.

France 15-mar. 11-may 30-may.

Austria 16-mar. 31-may.

NY USA 20-mar. 4-jun.

CA, USA 20-mar. 4-jun.

Germany 23-mar. 7-jun.

United Kingdom 24-mar. 7-may. 8-jun.

Lockdown Economic hibernation Opening of small businesses Opening of schools

In Spain, the official de-escalation began on 4 May, with a four-phase, asymmetrical plan and the goal of reaching

relative normality by late June, when hotels and tourist accommodation should theoretically be able to open. In

Italy, four and a half million people are back at work, and bars in central Rome are offering takeaway meals.

In the US, which has recorded the highest number of cases and deaths, the messaging is more confusing and less

uniform, as the de-escalation plans are recommended at the federal level but how to implement them is decided

independently by each state. The world’s largest economy is moving swiftly towards normality nonetheless; a

total of twelve states are already allowing non-essential businesses to reopen.

2. STATE RESTRICTIONS ON BUSINESS RE-OPENINGS

Source: Kaiser Foundation

WA

MT ME

ND

OR MN WT

ID NH

SD WI NY MA

WY RI

CT

IA PA NJ

NV NE

OH DE

UT IL IN MD

CA CO WV DC

KS VA

MO KY

NC

TN

AZ OK

NM AR SC

MS AL GA

TX LA

AK FL

HI

All closed Fully reopened (some) Partial reopening (all)

Partial reopening (some) Some closed No restrictions

THE FIRST STEPS TOWARDS NORMALITY 7HOUSE VIEW. MAY 2020

Early macroeconomic indicators confirm an abrupt downturn in activity.

The early macroeconomic indicators coming out now, which relate to the period when infections were growing

at their fastest and economies were shutting down, have confirmed our worst fears, reflecting a sharp downturn

in activity. As graph 3 demonstrates, GDP shrank in the three main regions in the first quarter of the year. The

hardest-hit economy in Q1 was China, where the virus spread initially, which saw a quarterly drop in GDP of -9.8%.

The eurozone also sustained a severe blow to economic activity, contracting by -3.3% over the quarter. Even in

the US, which was hit by Covid-19 somewhat later, GDP figures confirm that social isolation measures have had

a direct, fierce impact on consumer spending, which – as we anticipated in previous reports – will be one of the

components that suffers the most.

3. SHARP DOWNTURN IN ACTIVITY 4. PLUMMETING BUSINESS CONFIDENCE

Source: Bloomberg and Banca March Source: Bloomberg and Banca March

4 Quarterly GDP performance (%) 60

2 50

0

40

-2 -1,2

33,4

-4 30

-3,8

-6 -5,2 20

-8 13,6

10 12

-10

-9,8

-12 0

mar.-18 jun.-18 sep.-18 dec.-18 mar.-19 jun.-19 sep.-19 dec.-19 mar.-20 apr.-18 jul.-18 oct.-18 jan.-19 apr.-19 jul.-19 oct.-19 jan.-20 apr.-20

US Eurozone Spain China

Composite PMI Threshold Manufacturing PMI Services PMI

The abrupt downturn in activity has been reflected extremely quickly in employment figures, whilst business

confidence indicators in the eurozone suggest that we will see the worst of the downturn in April and May

(graph 4). The composite PMI for the region fell to a record low of 13.6 in April, auguring the severe contraction

in economic activity this quarter. Whilst industry appears to be holding up relatively well, the service sector has

been impacted heavily by the lockdown measures.

A steeper decline and gradual reopening have led to downgraded forecasts.

The rapid downturn in activity data in Q1, coupled with recent announcements on de-escalation processes, have

led us to downgrade our growth forecasts. In May, we have begun to take the first steps towards normal life, but

the process will be slow and gradual.

We expect to see a deep recession in the first half of the year, with the worst contraction in modern economic

history. However, we continue to believe that the transient nature of lockdown measures and particularly the

robust raft of fiscal and monetary stimulus measures announced, will mean that this recession is short-lived.

THE FIRST STEPS TOWARDS NORMALITY 8HOUSE VIEW. MAY 2020

As graph 5 shows, activity will plummet to record lows in H1, then begin to recover in the second half of the

year. Despite this subsequent recovery, global GDP will be down by 2.9% year on year for 2020 as a whole. This

scenario means we will not claw back late-2019 levels until Q1 2021, and at the end of the forecast period, global

GDP will still be -1.8% lower than we expected at the beginning of this year, as the recovery will now be less steep

than initially forecast (graph 6).

5. GLOBAL GDP 6. REVISIONS TO INITIAL FORECAST

Source: Oxford Economics and Banca March Source: Oxford Economics and Banca March

10 Global GDP forecasts (YoY) 110 Global GDP forecasts (YoY) -1,8%

8

6 105

4

2 100 -6,1%

0

-2 95

-4

-6 90

-8

-10 85

05 06 07 08 09 10 11 12 13 14 15 16 17 18 19 20 21 dic.-18 dic.-19 dic.-20 dic.-21

Adverse Activity resumes in Q3 December 19 Adverse Activity resumes in Q3 December 19

The uncertainty plaguing macroeconomic scenarios remains unusually high and these are only quantitative

estimations of the possible economic impact of the lockdown measures applied. The economic impact of the

health crisis will depend largely on how long the measures needed to contain the virus remain in place, and

the outlook in that respect is constantly changing. If the quarantine measures remain in place for longer than

expected, the economic impact will be more severe. Graph 5 shows a more negative alternative scenario involving

stricter, longer isolation measures in place until after the summer in the northern hemisphere, in which the impact

of deteriorating financial conditions would also cause increased destruction of the business landscape. In this

adverse scenario, the negative impact would be more structural and global GDP would be around -6.1% lower

than was forecast early this year (graph 6).

By regions, we believe the impact of the health crisis will be uneven. Specifically, the eurozone will be one of the

hardest-hit regions, as lockdown measures are having an impact on major economies like Spain, Italy and France;

these economies depend heavily on tourism, which accounts for an average of 12.5% of GDP, and which will be

one of the slowest sectors to recover due to restrictions on movement and consumers’ fears of infection.

7. GDP FORECASTS 8. TOURISM AS A PROPORTION OF GDP

Source: Oxford Economics, World Bank and Banca March Source: Oxford Economics, World Bank and Banca March

The US Eurozone China World 25% Travel and Tourism (%GDP, 2018)

10

8 20%

6 15%

4

10%

2

0 5%

-2

0%

-4

Greece

Portugal

Spain

Italy

China

United Kingdom

France

India

Germany

Brazil

The US

Japan

Canada

The Netherlands

Russia

-6

-8

2019 2020 p 2021 p

THE FIRST STEPS TOWARDS NORMALITY 9HOUSE VIEW. MAY 2020

Spain: one of the hardest-hit economies.

Social distancing measures have had an extremely severe impact on the Spanish economy in the first quarter

of the year which, coupled with the composition of the country’s production model itself, leads us to believe

that the economy will undergo a major contraction this year. In the first quarter, which included just two weeks

of the State of Emergency, GDP shrunk by -5.2% over the quarter and -4.1% year on year, which is the largest

drop in GDP on record. By components, private consumption dropped significantly (-7.5%) as did investment

(-5.8%). On the flipside, GDP from private consumption grew at +1.8%, in line with the increased efforts by public

administrations to tackle the crisis, especially in healthcare.

9. ELECTRICITY DEMAND In the second quarter, high-frequency indicators

Source: Red Eléctrica España and Banca March such as energy consumption show that activity

has continued to fall, with growth bottoming

105

out in April, when all non-essential sectors were

Electricity use

100 shut down. The good news is that before the

de-escalation process, the economy will already

Mov 7d avrg: 1 March = 100

Non-essential activity

Electricity demand (Gwh)

95 State of

Emergency shut down

likely have bottomed out.

90

Reopening of construction

85 and manufacturing

80

75

70

1-mar. 8-mar. 15-mar. 22-mar. 29-mar. 5-apr. 12-apr. 19-apr. 26-apr.

The inherent characteristics of the Spanish economy and the heavy weighting of the service sector - tourism,

hospitality and leisure account for almost 24% of GDP - mean that the economic contraction in 2020 will stand

at over -9% year on year.

10. SPANISH GDP YEAR-ON-YEAR Looking ahead to the rest of the year, the outlook

Source: INE and Banca March is shown from the supply perspective. The service

GDP and components

sector will not recover to the growth levels prior

(Suupply, YoY growth) to the State of Emergency this year, and it will be

0% Industry – and to a lesser degree Construction –

-3,1% that will spearhead the reactivation of economic

-4,1%

-5% activity in the second half of the year.

-10% -10,1%

-15%

-18,7%

-20%

2020 T1 2020 T2 2020 T3 2020 T4

Agriculture Industry Construction Services GDP

THE FIRST STEPS TOWARDS NORMALITY 10HOUSE VIEW. MAY 2020

China will continue to act as a model for what comes next.

However, although the difficulty in predicting the depth of the drop in GDP will continue, we do believe that the

focus should be on anticipating how economic activity will recover once our everyday lives return to a semblance of

normality. In that respect, we continue to believe that China can serve as an example.

As China was the epicentre of the virus, it will continue to be a good indicator of what will happen in the rest of the

world. The latest data coming out of China showed a 6.8% year on year drop in GDP in Q1, but the various economic

components put in uneven performances, revealing important patterns as to what the initial stages of the recovery

will look like in other countries.

11. CHINA: ACTIVITY HAS COLLAPSED, BUT NOT EVENLY As graph 11 shows, during the months when

Source: Bloomberg and Banca March the infection rate was at its peak, consumption

tapered off sharply, but in March, when the

20%

Retail sales

11,6%

restrictions began to be lifted, sales of more

(Restaurants) 8,8% 9,9%

10% 6,1% 6,9% 6,5% durable and technology goods recovered quickly.

Retail sales

1,8% Mobile sales, for example, fell by 8.8% year on

0%

(Auto) year between January and February, but grew by

-10% 6.5% in March. However, the restaurant sector

Retail sales -8,8%

(Mobiles) -13,8% continued to fall, even faster than in previous

-20% -18,1% -18,3% months.

Industrial prod.

-30%

(Cement) -29,5%

-40% -37,0%

Industrial prod. -39,7%

(Computers,

Comms. and -50% -46,8%

Others) dec-19 jan - feb 20 mar-20

The severe economic and social crisis will be followed by an unprecedented recovery, accelerating

structural changes.

The recovery in demand observed in China, 12. CONSUMPTION WILL HAVE TO ADAPT

coupled with behavioural studies, suggest that Source: YouGov and Banca March

after Covid-19, consumption and economic

activity will recover at different speeds depending

Surveys on post Covid-19 behaviour

on the sector. Once the infection rate has been 100% (% of population that will avoid behaviours)

contained and the collapse of the health service

has been avoided, lifting lockdown measures will 75%

not trigger an immediate return to normality,

given the potential change in behaviours we are

50%

likely to see (graph 12).

25%

0%

Spain Italy France Germany United US China India Japan

Kingdom

Avoid crowded places Avoid touching objects in public

THE FIRST STEPS TOWARDS NORMALITY 11HOUSE VIEW. MAY 2020

It is still too soon to say for sure which changes will be structural and long-term, and which impacts will be

temporary. In our view, there will be certain trends in the post-Covid world that will have unavoidable consequences

for the financial markets:

1. More debt, less growth potential and minimal interest rates: the fiscal stimulus required to reactivate

the economy and to inject liquidity into the private sector ahead of the economic shutdown will drive up

public debt levels. Central banks will continue to intervene in the markets and seek to stop financing costs

from spiking. Our baseline macroeconomic outlook in recent years, which envisages a world with lower

growth potential than in past decades and low interest rates for a substantial period, will therefore remain

valid.

2. Globalisation in response to the need to secure production chains: Some companies struggled to

access supplies at the outset of this health crisis, after China had to shut down its economy; this will

impact future decisions on the location of production chains and supplier relations, and will trigger a

resurgence of protectionist measures in some strategic sectors. Economic agents will be more mindful of

the risk involved in globally integrated supply chains.

3. Digitalization, news ways of working and communication: the changes in consumer behaviour and

particularly in interpersonal relationships over these few months will provide added tailwinds for the

digitalisation of the economy. Remote working, e-commerce and distance learning will all now be a more

prominent part of our lives. In the short term, however, people-intensive businesses and sectors like

tourism will need to reinvent themselves.

These trends are already reflected in the figures for online retail sales and education platforms. The

impact of the coronavirus crisis on physical retail outlets has been evident, but it is noteworthy that within

the Spanish tech sector (graph 13), initially it was pure play retailers that saw their share of sales increase.

However, as the public health crisis has advanced, companies that combine both online sales and physical

stores have now equalled that percentage. The change in shopping habits is already a reality, and while

this percentage may reduce once the lockdown is lifted, it is unlikely to return to the former status quo.

13. SALES CHANNELS DURING LOCKDOWN 14. DISTANCE LEARNING

Source: GfK, Udemy and Banca March Source: GfK, Udemy and Banca March

Consumption of technology goods Registration for online courses

(by sales channel) (Udemy)

100% 350%

90% 13% 17%

30%

80% 9% 8% 43% 41%

300%

46%

70% 250%

60% 18%

50% 200%

40% 39%

78% 75% 34% 40% 150%

30%

52%

20% 100%

10% 20% 18% 19%

50%

0%

jan-20 feb-20 mar-20 Week 14 Week 15 Week 16

(20 - 26 april) 0%

Physical stores Click & Mortar Pure Players Italy United Spain Germany India France US Mexico Brazil

Kingdom

% sinde February

Alternative training models are also attracting increasing demand: not only is online education being

used by education centres, but also by professionals who want to expand their training during lockdown,

according to figures released by online training platform Udemy (graph 14).

THE FIRST STEPS TOWARDS NORMALITY 12HOUSE VIEW. MAY 2020

4. Increased spending on healthcare: the need to find a cure for Covid-19 and the challenges of responding

to a global health crisis of this size will lead to additional funds being channelled into this sector. Investment

will come both from the private sector, buoyed by stronger growth forecasts, and from the public sector,

because the health crisis has emphasised the importance of this sector for national security.

There are also other changes which we currently believe to be temporary and secondary, but which must

nonetheless be monitored. The negative impact this health crisis is having in the short term on companies and

liquidity requirements has led many governments to intervene in the private sector through loans and even

capital injections. There are strong examples of this in the eurozone and in sectors like energy and airlines.

These interventions are good news for these companies’ bondholders, as they reduce the risk of disorderly

defaults in the short term; however, the impact on the long-term growth of these businesses and on shareholder

remuneration remains to be seen.

THE FIRST STEPS TOWARDS NORMALITY 13HOUSE VIEW. MAY 2020

CENTRAL BANKS AND FIXED INCOME

Central banks are extending their stimulus measures even further.

In April, the Fed continued to reinforce its stimulus plans and confirmed that its asset purchases will now

include corporate bonds issued by fallen angels, companies which have lost their investment grade ratings. At its

scheduled April meeting – its first non-emergency meeting since January – the Fed maintained its pro-stimulus

discourse in response to data which clearly evidences the downturn in the US economy. The Fed’s actions in

response to Covid-19 are previously unheard-of; from mid-March to late April alone, it expanded its balance sheet

by 54%. That equates to 2.3 trillion dollars, equivalent to two years’ GDP for a country like Spain.

The ECB has also expanded its own monetary policies. It has announced the conditions for TLTRO III and for

its new Pandemic Emergency Longer-term Refinancing Operations (PELTRO), designed to generate liquidity in

the interbank market with more advantageous conditions than the traditional LTROs. The novelty offered by

PELTROs is that the ECB will accept lower-rated collateral and that the interest rate will be -0.25% rather than

the current rate of 0% on its main refinancing operations.

The conditions of TLTRO III are more advantageous still: from June 2020 until June 2021 the rate will drop by

-0.25% to -0.50%, following the reduction announced in March. Banks could even secure financing at 50 bps less

than that rate - i.e., at -1%, if they can demonstrate an increase in their eligible net lending over a year. This move

is designed to channel liquidity into small businesses and households, which do not have access to the capital

markets and depend largely on banks for financing.

Meanwhile, the asset purchase programme remains underway, and between March and April the ECB made net

bond purchases worth 90 billion euros, of which three quarters were sovereign debt. As reflected in graph 15,

the key beneficiaries so far have been Italy, France and Spain, which are the countries that have been hit hardest

by the health crisis. The ambitious programme will continue, with 20 billion euros a month plus the 750 billion

Pandemic Emergency Purchase Programme (PEPP).

15. ECB PUBLIC SECTOR DEBT PURCHASES (PSPP)

Source: Bloomberg and Banca March

40

35

30

25

20

15

10

5

0

-5

-10

apr.-19 jun.-19 aug.-19 oct.-19 dec.-19 feb.-20 apr.-20

Spain Italy France Germany Rest

THE FIRST STEPS TOWARDS NORMALITY 14HOUSE VIEW. MAY 2020

Government bonds post unequal performances: the best-rated debt stabilises as tension

remains in peripheral bonds.

After the highly stressed conditions in March, central bank measures have curbed volatility in the fixed income

markets. The best-rated sovereign bonds remained stable over the month thanks to central bank purchases. US

10-year Treasury yields stabilised in the range of 0.60%–0.65%, and German bund yields held steady at -0.45%

to -0.55%. We expect yields to remain in these ranges over the coming months.

On the flipside, European periphery bonds have suffered occasional episodes of stress, especially when

governments have undertaken further issuances. At the end of April, issuances by Spain and Italy drove sovereign

credit spreads to levels very near to the maximum stress levels registered in March.

However, the key market event came when Fitch downgraded Italy’s sovereign rating to BBB-. Standard and

Poor’s confirmed Italy’s BBB rating, two notches above junk status, but with a negative outlook.

These episodes of volatility, as Brussels rushes to negotiate the finer points of the European Rescue Plan and the

amount that states will not have to repay, afford tactical opportunities to buy.

16. RISK PREMIUM SPAIN AND ITALY

Source: Bloomberg and Banca March

280

Issuance

260

240

Risk premium (bps)

220

S&P

maintains Fitch

200 rating cuts

rating

180

Issuance

160

140

120

100

80

1-mar. 8-mar. 15-mar. 22-mar. 29-mar. 5-apr. 12-apr. 19-apr. 26-apr.

Spain Italy

We continue to see opportunities in credit markets. We recommend being overweight

Investment Grade bonds and we have changed our outlook from underweight to neutral on

High Yield.

The decisions made in April by certain central banks in relation to the minimum credit ratings they are prepared

to accept have had a decisive impact on the performance of credit markets. Specifically, the Fed is to start buying

fallen angels – issuers that lose their investment grade rating during the coronavirus crisis – and the ECB has

made fallen angel bonds eligible as collateral for liquidity.

Spreads have eased substantially since the peak in March, by around 100 bps for global investment grade (IG)

credit and by twice that for high yield (HY). This has mitigated one of the main risks linked to IG credit, which

we discussed in last month’s report: 52% of European IG credit is rated BBB and is therefore exposed to rating

downgrades that could strip it of its IG status.

The Fed’s decision is a drastic one, and evidences the central bank’s concerns around the swift deterioration of

many companies’ ratings. There is no doubt that Q2 will be one of the most tumultuous periods in quite some

time. In April alone, Standard and Poor’s has opened 413 ratings actions on Western European bonds; the average

for the decade is 200 actions in the whole of Q2. In addition, the number of fallen angels soared at the end of

March, when lockdown began (graph 17).

THE FIRST STEPS TOWARDS NORMALITY 15HOUSE VIEW. MAY 2020

17. NUMBER OF POTENTIAL FALLEN ANGELS

Source: Moody’s

80

70

60

Number of issuances

50

40

30

20

10

0

Q1-2013 Q1-2014 Q1-2015 Q1-2016 Q1-2017 Q1-2018 Q1-2019 Q1-2020

BBB negative outlook BBB potential fallen angels

The Fed’s decision backs up our outlook for the asset class, and we believe that if the situation deteriorates in

Europe, the ECB could follow suit. In any case, despite the significant increase in prices over recent weeks, we

believe that the current implicit default rates of 3.5% are too high, especially bearing in mind that in the 2009

crisis, 0.6% of companies defaulted on their debt. At that time, rating downgrades impacted 21% of the IG issuers

and 31% of the HY issuers rated by Moody’s. As the table in graph 18 shows, investors have historically obtained

returns of 8% at 12 months by investing approximately at current levels.

HY also offers attractive valuations and historical data suggests we are currently looking at good entry levels.

Given the unpredictable nature of this crisis, however, we remain cautious in HY debt, as we believe that the

default rates and rating downgrades that will materialise over the quarters ahead will be high despite government

support, and will not, in reality, be far off what current implied default probabilities suggest (Graph 18). What’s

more, most HY debt will not enjoy central bank support, which puts it at a clear disadvantage versus IG.

18. IMPLIED PROBABILITY OF DEFAULT AND YIELDS

Source: Bloomberg and Banca March

35%

Invest. Grade Global Yield at one year if implied probability is…

30% Implied probability of default Around 3% Around 4% Around 5% Around 6%

Implied probability of default

Mean 8,1% 15,2% 21,1% 23,7%

25% 15,6% Median 7,9% 11,9% 22,2% 23,9%

Max. 30,4% 30,4% 30,4% 30,4%

20% Min. -16,1% -16,1% 8,9% 14,5%

15% High Yield Global Yield at one year if implied probability is…

Implied probability of default Around 8% Around 10% Around 12% Around 14%

10% Mean 12,5% 16,8% 22,4% 32,3%

Median 11,0% 15,5% 20,8% 31,8%

5% 3,5%

Max. 71,8% 71,8% 71,8% 71,8%

Min. -33,0% -25,9% -8,7% -4,4%

0%

01 02 04 06 08 10 12 14 16 18 20

IG Global HY Global

THE FIRST STEPS TOWARDS NORMALITY 16HOUSE VIEW. MAY 2020

Emerging market fixed income continues to offer excellent potential.

Emerging market sovereign bonds in hard currency posted gains in April, rising 8.5% from March lows, and

continues to trade at attractive entry levels with an IRR of 7.2%. Spreads remained stable over the month at

around 650 bps and we believe that there could be additional capacity for compression once the cut in oil supply

materialises, benefiting the countries that are most exposed to crude prices (Brazil, Russia and Mexico out of the

major economies). Buying at these spreads, over the last decade, emerging market fixed income in hard currency

has paid average yields of 18.4% at one year.

The probability of default implied from spreads is 10.5%, lower than global HY (15.5%) and very far removed from

what has traditionally been the case. As indicated in graph 19, this default rate has not been reached since 2006,

not even in the 2008 crisis, and on average, only 1.7% of EM issuers default on their payment obligations each

year. The worst year was 2017, when 4% of emerging market sovereign issuers went into default: Mozambique,

Belize, the Republic of the Congo and Venezuela, each for their own different reasons. We therefore believe

that the fear of defaults, currently focused on major oil producers like Russia, Saudi Arabia, Brazil and Mexico, is

excessive, and will gradually dissipate as economic activity begins to pick up.

19. EMERGING MARKETS % COUNTRIES DEFAULTING ON DEBT

Source: Moody’s and Banca March

5%

4,0%

Defaults by emerging market issuers

4%

3% 2,7%

2,3%

2%

1,5%

1,3% 1,2% 1,1% 1,1% 1,0% 1,0%

1%

0%

06 07 08 09 10 11 12 13 14 15 16 17 18

THE FIRST STEPS TOWARDS NORMALITY 17HOUSE VIEW. MAY 2020

EQUITIES

The markets are recovering at speed in an asymmetric ascent focused on the strong

performance of a few select stocks and sectors, which are spearheading the gains.

The decisive action taken by central banks and governments in response to the pandemic has allowed global

equity markets to recover to a significant degree. Gains from trough to peak stand at almost 30%. In April, the

S&P 500 chalked up its best monthly performance since January 1987, and had its third-best month for 80 years.

Despite these figures, it is important to emphasise that only 14% of companies are trending upwards (see graph

21, which shows the percentage of NYSE names that are trading at over their 200-session average), which gives

a clear idea of how asymmetrical the rally has been. Against this backdrop of sector-specific performances,

Technology (+13.5%) and Health (+11.5%) both outperformed, with US biotech stocks posting their strongest

monthly gains for two decades, and Energy, Industrials and Financials registered steep losses.

20. PERFORMANCE OF THE MAIN STOCK 21. S&P 500 AND % OF NYSE SHARES

MARKETS TRENDING UPWARDS

Source: Bloomberg. MSCI indices except Europe (Stoxx 600) and Spain Source: Bloomberg. MSCI indices except Europe (Stoxx 600)

(IBEX 35) and Spain (IBEX 35)

3500 90

3300 80

3100

70

2900

60

2700

50

(%)

2500

40

2300

30

2100

20

1900

1700 10

US Europe China Spain Nasdaq 100 1500 0

ene.-15 ago.-15 mar.-16 oct.-16 may.-17 dic.-17 jul.-18 feb.-19 sep.-19 abr.-20

S&P 500 % shares trending upwards (right)

Following this steep appreciation, the recovery process will be much slower. The lateral

market registered since mid-April is a good indicator of the movements we can expect over

the coming weeks.

The rally from lows in the main stock market indices has been unusually fast and intense, confirming the

importance of holding equity exposure steady and not selling down positions in moments of panic, such as the

second fortnight of March.

From now on, the vertical upward trend will taper, as corporate earnings will continue to fall. We believe it is

premature to consider recovery to pre-Covid earnings levels when forecasts are still being downgraded and these

downgrades will continue until at least Q3, after which the recovery rate will begin to stabilise.

We therefore maintain our recommendation of staying neutral and seeking to harness possible corrections to add

positions. In the short term, until it becomes clearer when the downturn in activity will bottom out and a medical

solution has been found for the health crisis, we will see recurring episodes of volatility.

THE FIRST STEPS TOWARDS NORMALITY 18HOUSE VIEW. MAY 2020

Should investors harness this rally to sell?

No. Despite the uncertainty landscape in terms of health, in which predicting future waves of Covid-19 is

impossible, and the slow de-escalation process that lies ahead, we maintain that the decisive, unprecedented

measures rolled out by central banks and governments will provide a safety net to curb the potential depth of

any future downturns. Direct asset purchases by central banks are an absolutely crucial measure.

The impact of Covid-19 is already evident in Q1 results season.

The quarterly results season is now beginning to peak, and corporate earnings are partly reflecting the impact

of the pandemic and economic slowdown. In the US, more than a third of the S&P500 companies have now

published results, with a 65% positive surprise ratio, the lowest for a decade. EPS is down by 16% excluding the

financial sector, which includes a substantial increase in provisions, and both revenues and profits have remained

flat. Once again, cyclical companies underperformed in relation to defensives and on the whole, Financials (-49%)

and Industrials (-15%) have posted the worst results to date. At the opposite end of the scale, earnings were up

for Real Estate (+17%) and Technology (+11%) and revenues grew for Health (+10%) and Technology (+5%).

In Europe, 40% of the Stoxx600 has posted results to date, and earnings are down by 19%, with a positive surprise

ratio of 54%. The drop in revenues so far stands at 5%. The sectors posting the worst earnings performances are

Consumer Discretionary (-71%) and Energy (-59%). On the positive side, like in the US, revenues grew in Health

(+11%) and Technology (+4).

The earnings downgrades estimated by the consensus of analysts are far less severe than

they were in the 2008 crisis. Earnings forecasts will continue to be downgraded.

As illustrated by graph 22, given the severity of the macro downturn and however swift the recovery may be, we

believe a drop in earnings of almost 15% is insufficient; in 2008/2009, the real correction in earnings was over

30% in the US and 40% in Europe.

22. ESTIMATED EPS GROWTH 2020 BY REGIONS 23. ESTIMATED EPS GROWTH 2020 BY

Source: Bloomberg, Refinitiv and Banca March GLOBAL SECTORS

Source: Bloomberg, Refinitiv and Banca March

15,0 20%

16

10% 6,5%

13 4,1% 2,6%

9,8 0,5%

10 8,9 8,5 0%

-0,4%

7 5,0 -10%

EPS growth

-9,4% -11,0%

EPS growth (%)

4 -20% -14,9% -16,6%

-20,1%

1 -30%

-2 -40%

-5 -50%

-8

-60%

-11 -9,4 -64,2%

-70%

-14 Tech Health Util C. Disc Tel World Mat Ind Fin C. Def Ene

-14,1 -14,7

-17

MSCI AC World S&P 500 Stoxx 600 MSCI EM

03 jan 2020 Current

THE FIRST STEPS TOWARDS NORMALITY 19HOUSE VIEW. MAY 2020

By sectors, Energy, Financials, Industrials and Consumer Discretionary together account for a third of the stock

market rally, but in the short term there is ongoing pressure from earnings downgrades for these sectors, and their

trading ratios remain above average. The earnings downgrades in the Energy sector are particularly interesting,

given that crude prices are at record lows, and we believe these could partially reverse once the economy returns

to a certain degree of normality.

By contrast, recommended sectors like Health and Technology have proven in the past to be more resilient

in downturns and enjoy stronger capacity for recovery when markets rise. Both sectors outperformed in April

(Technology +13.1%; Health +11.5%), but unlike the general index, they offer growing earnings forecasts with

reasonable ratios, fairly close to the average in the case of Tech and even more attractive in the Health sector.

24. TECH AND HEALTH: THE BEST-POSITIONED SECTORS TO WITHSTAND THE CURRENT CRISIS

Source: Bloomberg, Refinitiv and Banca March

Annualised growth last 10 years Performance during GFC and current estimates

350% 324,6% 10% 6,5%

4,1%

300% 0%

250% -3,6%

-10%

EPS growth (%)

-9,4%

EPS growth

200%

-20%

150%

104,7% -30%

100% 90,3%

-40% -36,2%

50% -39,4%

0% -50%

Recovery (2008-2009) Max loss (2008-2009) 2020 E

MSCI World AC Health Technology MSCI World AC Health Technology

In terms of regions, we prefer the US to Europe. We also continue to like Asia within the

emerging markets.

By regions, we are overweight the US versus Europe, as we are more optimistic on the US economy’s capacity for

recovery, largely due to its lower degree of export dependency. Mainly, however, because of the heavier relative

weighting of the sectors and companies where our outlook is most positive, such as Tech (which accounts 26%

of the S&P500) and Health (15%) which, along with other heavily-weighted new economy giants (for example,

Amazon, Facebook and Alphabet, in other sectors, account for a further 10%), will emerge stronger from this

crisis.

In addition, as we mentioned early on in this report, the proportion of government measures with an immediate

economic impact is greater in the US, and the Fed has broader capacity to expand its various programmes.

We continue to recommend positions in Asian emerging markets, which should be the first economies to start

withdrawing lockdown measures. The drop in global demand will continue to hamper international sales by

companies in these economies, but we believe that they are in a more advanced phase of the crisis and the

relatively better performance of recent weeks should continue.

The stronger performance of the Chinese stock market throughout this crisis, its lower volatility and the -4%

losses registered YTD are a reflection of its attractive valuations. Its lower degree of dependency on the service

sector, which has been hit hardest by this crisis and accounts for half of the Chinese economy versus two thirds

in developed markets, coupled with falling energy prices, will support a stronger recovery versus the developed

economies. Graph 25 shows the discounts on valuations in the Asian emerging markets versus the rest of the

world.

THE FIRST STEPS TOWARDS NORMALITY 20HOUSE VIEW. MAY 2020

25. PER 12 MSCI EMERGING ASIA VS MSCI WORD AC

30%

20%

10%

0%

-10%

-20%

-30% -25,78%

-40%

-50%

-60%

96 99 01 03 06 08 10 13 15 17 20

Other structural factors also come into play, such as the substantial weighting of emerging markets within the

global economy (approx. 60%) and their under-representation in the main global indices and a significantly above-

average earnings performance.

THE FIRST STEPS TOWARDS NORMALITY 21HOUSE VIEW. MAY 2020

CURRENCIES

Euro-dollar cross under pressure due to demand for liquidity. Our range is from 1.08 to 1.15

EUR/USD.

At times of crisis like the present, the dollar will continue to benefit from its status as a safe haven, and demand

will remain high. However, the Fed has already launched various programmes aimed at increasing the supply

of dollars in circulation and has even opened up direct liquidity facilities with other central banks. Against this

backdrop, a depreciation of the dollar in the short term looks unlikely, and the currency will continue to have

strong support until after the summer. We therefore maintain our outlook that euro-dollar cross levels of under

1.08 EUR/USD should be harnessed to pare back exposure. In the long term, we continue to believe that based

on economic fundamentals the euro-dollar cross should be around 1.15 EUR/USD, but until we see clear progress

in the EU towards a joint, coordinated response to this health crisis - and the serious increase in public debt - the

euro will remain under pressure versus the dollar.

The pound sterling is stabilising. Range 0.83 - 0.90 EUR/GBP.

The volatility of the pound has eased off thanks to a Covid-19 policy which is more in line with the rest of Europe.

This comes against the backdrop on the ongoing debate as to whether the Bank of England should step up its

existing 645 billion-pound asset purchase programme, as there is virtually no wiggle room in interest rates after

March’s rate cut to 0.1% and the economy is clearly shrinking (the BoE is forecasting a GDP contraction of 14%

for the year).

26. EUR/GBP VOLATILITY

Source: Bloomberg and Banca March

25

Brexit

20

Covid - 19

15

10

5

0

jan.-16 nov.-16 sep.-17 jul.-18 may.-19 mar.-20

The UK also has another important task to tackle: its negotiations with the European Union. The talks appear to

have taken a back seat, and if the UK does not request an extension, the transition period will end on 31 December

2020 and the UK will definitely leave the European Union. Despite the reticence expressed by the UK, the most

likely outcome is that it will end up requesting an extension. This situation could drive a temporary spike in

volatility in the pound. We expect the range for the weeks ahead to stand at 0.83-0.90 EUR/GBP.

Banca March Market Strategy Team:

Joan Bonet Majó

Pedro Sastre

Paulo Gonçalves, CAIA

Luis Coello

Adrián Santos

THE FIRST STEPS TOWARDS NORMALITY 22HOUSE VIEW. MAY 2020

EURIBOR EURIBOR 12 MONTHS (3 YEARS)

LAST 1 MONTH YTD 1 YEAR 0

1 MONTH -0,44 -0,42 -0,45 -0,37 -0,05

3 MONTHS -0,35 -0,36 -0,39 -0,31 -0,1

6 MONTHS -0,28 -0,29 -0,33 -0,23

-0,15

12 MONTHS -0,16 -0,17 -0,24 -0,11

-0,2

-0,25

CURRENCIES -0,3

-0,35

LAST 1 MONTH YTD 1 YEAR

-0,4

EUR/USD 1,0955 1,103 1,120 1,122

-0,45

EUR/GBP 0,870 0,888 0,854 0,860

may.-17 aug.-17 nov.-17 feb.-18 may.-18 aug.-18 nov.-18 feb.-19 may.-19 aug.-19 nov.-19 feb.-20

EUR/CHF 1,058 1,060 1,086 1,143

EUR/JPY 117,4 118,6 122,0 125,0

EUR/USD (3 YEARS)

GOVERNMENT BONDS

1,3

LAST 1 MONTH YTD 1 YEAR

2 YEARS 0,20 0,25 1,57 2,30 1,25

5 YEARS 0,36 0,38 1,67 2,30

USA 1,2

10 YEARS 0,64 0,67 1,88 2,50

30 YEARS 1,28 1,32 2,33 2,90 1,15

2 YEARS -0,76 -0,69 -0,60 -0,58

5 YEARS -0,76 -0,65 -0,47 -0,41 1,1

GERMANY

10 YEARS -0,59 -0,47 -0,19 0,01

1,05

30 YEARS -0,18 0,03 0,35 0,66

2 YEARS -0,22 -0,19 -0,39 -0,34 1

5 YEARS 0,04 0,15 -0,08 0,15 may.-17 aug.-17 nov.-17 feb.-18 may.-18 aug.-18 nov.-18 feb.-19 may.-19 aug.-19 nov.-19 feb.-20

SPAIN

10 YEARS 0,72 0,68 0,47 1,00

30 YEARS 1,46 1,51 1,32 2,16

2 YEARS 0,02 0,14 0,59 0,74

10 YEAR GOVERNMENT YIELDS (SPAIN VS GERMANY)

5 YEARS 0,09 0,21 0,65 0,88

UK

10 YEARS 0,23 0,36 0,87 1,15

2

30 YEARS 0,57 0,83 1,38 1,67

1,5

CORPORATE BONDS (1 YEAR SPREAD) 1

LAST 1 MONTH YTD 1 YEAR

0,5

AA 0,19 0,61 -0,27 -0,23

A 0,32 0,64 -0,26 -0,20 0

BBB 0,76 0,86 -0,16 -0,09

-0,5

-1

COMMODITIES may.-17 aug.-17 nov.-17 feb.-18 may.-18 aug.-18 nov.-18 feb.-19 may.-19 aug.-19 nov.-19 feb.-20

LAST 1 MONTH YTD 1 YEAR

BRENT 25,27 22,74 68,44 72,80

GOLD 1686,5 1577,2 1515,2 1283,5 IBEX (3 YEARS)

12000

EQUITY INDICES (3 YEARS)

LAST 1 MONTH YTD 1 YEAR 11000

MSCI WORLD* 489,17 10,58% -13,33% 7,47%

SP500 2912,43 12,68% -9,59% 22,16% 9000

EUROSTOXX50 2927,93 5,06% -21,89% -17,75%

TOPIXX 1464,03 4,35% -14,95% -4,42% 8000

IBEX35 6922,3 2,02% -27,99% -35,40%

FOOTSIE100 5901,21 4,04% -22,22% -18,08% 7000

MSCI BRAZIL 1233,94 5,28% -48,01% -32,45%

MSCI CHINA 81,36 6,33% -5,41% 19,30% 6000

MSCI EMERGING 924,94 9,00% -17,30% -5,42% may.-17 aug.-17 nov.-17 feb.-18 may.-18 aug.-18 nov.-18 feb.-19 may.-19 aug.-19 nov.-19 feb.-20

* All countries. Data: Bloomberg

THE FIRST STEPS TOWARDS NORMALITY 23HOUSE VIEW. MAY 2020

160%

EQUITY INDICES

PERFORMANCE

(3 YEARS) 140%

Data: Bloomberg

IBEX REL 120%

MSCI EMERGENTES REL

SP500 REL

100%

80%

60%

40%

jun.-17 sep.-17 dec.-17 mar.-18 jun.-18 sep.-18 dec.-18 mar.-19 jun.-19 sep.-19 dec.-19 mar.-20

IBEX rel MSCI Emergentes rel SP500 rel fijo

*DATA AS OF 30 DE APRIL 2020

RETURN DURATION PORTFOLIO DISTRIBUTION

MONTH YTD 1 YEAR CURRENT 1 MONTH AGO FI EQUITY ALT. INV.

MARCH RENDIMIENTO F.I. -0,01% -0,17% -0,45% 0,000 0,258 57,80% 0,00% 0,00%

MARCH RENTA FIJA CORTO PLAZO F.I. 0,54% -1,87% -1,80% 0,000 0,454 81,75% 0,00% 0,00%

MARCH PATRIMONIO C.P. F.I. 0,57% -1,51% -1,51% 0,000 0,696 81,57% 0,00% 0,00%

FONMARCH F.I. 0,84% -3,19% -2,78% 0,000 1,974 92,25% 0,00% 0,00%

MARCH EUROPA F.I. 10,13% -21,01% -29,55% 0,000 0,003 0,00% 100,51% 0,00%

MARCH INTL - VALORES IBERIAN EQUITY 6,22% -23,32% -21,94% 0,003 0,003 0,00% 95,11% 0,00%

MARCH GLOBAL F.I. 8,39% -24,16% -18,47% 0,000 0,003 0,00% 90,70% 0,00%

MARCH INTL - MARCH VINICATENA 8,39% -19,59% -20,04% 0,003 0,003 0,00% 96,39% 0,00%

MARCH INTL - THE FAMILY BUSINESSES FUND 6,23% -17,91% -12,42% 0,003 0,003 0,00% 92,66% 0,00%

MARCH INTL - MEDITERRANEAN FUND 7,99% -19,68% 0,00% 79,32% 0,00%

MARCH NEW EMERGING WORLD F.I.* 9,20% -19,83% -19,52% 0,000 0,003 0,00% 91,23% 0,00%

TORRENOVA DE INVERS. S.I.C.A.V. S.A. 2,17% -5,71% -4,74% 0,847 0,884 67,95% 19,52% 0,00%

CARTERA BELLVER S.I.C.A.V., S.A. 5,08% -11,61% -10,26% 0,742 0,837 38,65% 51,20% 0,00%

LLUC VALORES S.I.C.A.V., S.A. 8,41% -16,28% -13,45% 0,003 0,003 0,00% 85,57% 0,00%

MARCH INTL - TORRENOVA LUX 2,09% -5,86% -5,43% 0,003 0,003 72,04% 19,71% 0,00%

MARCH INTL BELLVER LUX 4,01% -5,51% -7,16% 26,64% 47,37% 0,00%

MARCH INTL LLUX LUX 7,31% -16,41% -17,30% 11,25% 82,60% 0,00%

MARCH PATRIMONIO DEFENSIVO F.I.* 1,54% -3,34% -3,29% 0,000 0,003 57,63% 3,17% 31,50%

MARCH CARTERA CONSERVADORA F.I.* 3,21% -4,91% -3,84% 0,000 0,003 42,60% 19,67% 30,24%

MARCH CARTERA MODERADA F.I.* 5,54% -6,30% -4,09% 0,000 0,003 23,41% 44,30% 24,92%

MARCH CARTERA DECIDIDA F.I.* 8,20% -11,26% -8,62% 0,000 0,003 0,95% 71,52% 19,36%

PLAN PENSIÓN CRECIENTE, F.P. 0,82% -2,67% -2,56% 0,000 1,303 90,77% 0,00% 0,00%

MARCH PENSIONES 80/20, F.P. 2,21% -8,22% -5,84% 0,000 2,026 71,93% 21,33% 0,00%

MARCH PENSIONES 50/50, F.P. 4,02% -11,47% -7,43% 0,000 1,947 49,23% 44,03% 0,00%

MARCH ACCIONES, F.P. 7,72% -18,98% -11,78% 0,000 0,003 0,00% 86,96% 0,00%

MARCH AHORRO, F.P. 3,16% -9,80% -6,48% 0,000 1,967 63,23% 29,90% 0,00%

PLAN ÓPTIMO, F.P. 2,88% -9,38% -6,11% 0,000 1,962 60,17% 26,82% 0,00%

MARCH MODERADO EPSV 1,89% -6,99% -5,27% 0,000 1,582 66,97% 19,12% 0,00%

MARCH ACCIONES EPSV 7,79% -16,25% -8,90% 0,000 0,003 0,00% 86,27% 0,00%

THE FIRST STEPS TOWARDS NORMALITY 24HOUSE VIEW. MAY 2020 IMPORTANT REMARK: The contents of this document are merely illustrative and do not pretend, are not and cannot be considered under any circumstances as an investment recommendation towards the contracting of financial products. This document has only been prepared to help the customer make an independent and individual decision but does not intend to replace any type of advice needed for the contracting of such products. The terms and conditions described in this document are to be viewed as preliminary terms only, subject to discussion and negotiation as well as to the agreement and final drafting of the terms affecting the transaction, which will appear in the contract or certificate to be issued. Consequently, Banca March, S.A.. and its customers are not bound by this document unless both parties decide to embark on a specific transaction and agree on the terms and conditions concerning the final documents to be approved. Banca March, S.A.. does not offer any guarantee, expressly or implicitly, in relation with the information shown in this document. All terms, conditions and prices contained in this document are merely informative and subject to modifications depending on the market circumstances, changes in laws, jurisprudence, administrative procedures or any other issue which may affect them. The customer should be aware that the products mentioned in this document may not be appropriate for his/her specific investment targets, financial situation or risk profile. For this reason the customer must make his/her own decisions by taking into account such circumstances and by obtaining specialised advice in tax, legal, financial, regulatory, accounting issues or any other type of information required. Banca March, S.A.. does not assume any responsibility for any direct or indirect costs or loss which may result from the use of this document or its contents. No part of this document can be copied, photocopied or duplicated in any way or through any means, redistributed or quoted without a previous written authorisation by Banca March, S.A. THE FIRST STEPS TOWARDS NORMALITY 25

You can also read