Brand Dubai: The Instant City; or the Instantly Recognizable City

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

International Planning Studies Vol. 12, No. 2, 173 –197, May 2007 Brand Dubai: The Instant City; or the Instantly Recognizable City SAMER BAGAEEN St. Mary’s, University of Aberdeen, UK ABSTRACT With ambitions to become a hub of global commerce, a top tourist destination and a shopping Mecca—a New York/Las Vegas/Miami rolled into one—Dubai has been spending billions of dollars to build an astonishing modern city nearly from scratch in a mere 15 years. To date some $100 billion worth of real estate under construction or in the pipeline continues the boom. Combining the involvement of local businesses and innovative strategies of urban marketing with headline catching projects, Dubai has set out to transform its urban landscape, and its image. Ambitious mixed-use urban developments featuring luxury residences, hotels and office blocks, huge shopping malls and imaginative entertainment complexes are rapidly changing the face of Dubai emirate and are putting the Dubai property market on the world stage. The catalyst for much of this expansion, this paper argues, has been the emirate’s decision to allow non-nationals to purchase freehold property. The paper concludes by questioning the sustainability of this growth but does not attempt to offer any answers, given its rollercoaster nature. Introduction Both Dubai and the UAE are experiencing high growth rates thanks to surging oil income, reaching $305 billion in 2006, a fivefold increase from 1998. All of the emirates and other gulf states are making significant strides in diversifying their economies so that a larger portion of oil and gas surplus revenue is invested in the region before the oil runs out. Dubai, for example, has already developed its economy to the point where oil accounts for only 7 per cent of GDP. Dubai is not the only city engaged in a construction boom of tremendous proportions attracting international interest; Doha (Qatar) and the island state of Bahrain are also in the race, along with other cities in the Middle East. Dubai’s sister emirate, Abu Dhabi, now also wants a slice of the action. These are examples of what we can call ‘instant’ cities or ‘cities within cities’ that are focal points of their government’s efforts to promote real estate development. Even the more traditional Saudis are now seeking to create their own ‘brand’ of urbanism (see Figure 1). Correspondence Address: Samer Bagaeen, Lecturer in Spatial Planning, Geography and Environment, Depart- ment of Geography and Environment, St. Mary’s, Elphinstone Road, University of Aberdeen, Aberdeen AB24 3UF. Email: samer.bagaeen@uclmail.net ISSN 1356-3475 Print/1469-9265 Online/07/020173-25 # 2007 Taylor & Francis DOI: 10.1080/13563470701486372

174 S. Bagaeen

Figure 1. The Kingdom Tower in Riyadh (Saudi Arabia). Source: Bagaeen, 2007

These cities are not therefore like London, Paris or New Delhi, which have been shaped

through a long process of evolution. They are ‘instant’ in that they are the product of a

super-fast urbanism. In Dubai, shopping malls, luxury hotels, residential towers and arti-

ficial islands, one shaped like a Palm and another like a map of the world, are being built;

and the figures show that these attractions are proving popular: around 5 million tourists

visit Dubai per year and the city is planning for 15 million by 2020.

For Dubai, Singapore has been the model proving that combining business with tourism

can be a successful formula for a city state. Thus Dubai has marketed itself as a successful

city state and has turned itself into a transport hub; the existing airport is being expanded

and a new airport is planned with six runways and the capacity to handle 120 million pas-

sengers per year. One of the new runways will be dedicated to cargo aircraft which will

load and unload at the world’s first ‘logistics city’.

Successful Branding

In the West, the transformation and promotion of urban image have become inextricably

linked to the entrepreneurial governance of western cities (see Paddison, 1993 for a

discussion of Glasgow in Scotland). According to Bradley et al. (2002), much of the sup-

posed transformation of former industrial cities has involved a process of investment mar-

keting and the promotion of rejuvenated urban images. I also discuss elsewhere (Bagaeen,

2006) the redevelopment of former military sites where the rationale for redevelopment

has been to attract jobs, tourists and residents to replace former military installations as

opposed to, for example, Glasgow, where the intention has been to replace a declining

former manufacturing economy. Waterfront developments all over the world are also

Brand Dubai: The Instant City 175

Figure 2. The eclectic Grosvenor House Tower in Jumeirah (foreground) and the nightscape of the

cranes at Jumeirah Beach Residences. Source: Bagaeen, 2005

part of this competition between cities to attract investment into previously rundown

locations: London Docklands is now the successful model that cities such as Edinburgh

(Edinburgh Waterfront) and Hamburg (Hafen City) are seeking to emulate.

Competition between cities for new investment and real estate projects is a natural con-

sequence of capitalist space-economies and new urban entrepreneurialism. Real estate

developments, pioneered by Dubai in the Arabian Gulf, have now been taken on by

several other countries in the Middle East to rebuild their cities and redefine and bolster

their image. Urban (2002) notes how the conscious use of images and representations

has increased the competitiveness of different places (see Figure 2) (see also Hall &

Hubbard, 1998; Kearns & Philo, 1993), and in some cities political influence has made

the promotion of a positive image of place an extremely important part of economic regen-

eration (Hall, 1998); Eben Saleh (2001) notes how government officials can promote

design by commissioning buildings and landmarks for ritual, cultural or commodity pur-

poses (Avraham, 2004; Burgess, 1982; Gold & Ward, 1994).

Ambitious mixed-use urban developments in the Middle East featuring luxury

residences, hotels and office blocks, huge shopping malls and imaginative entertainment

complexes are rapidly changing the face of cities like Dubai and are putting the property

market on the world stage. The catalyst for much of this expansion, this paper argues, has

been the emirate’s decision to allow non-nationals, actual and potential consumers, to pur-

chase freehold property.

This ‘demand-oriented’ planning, as defined by Ashworth and Voogd (1990, p. 23) is

something that Dubai has excelled in. In “Does the Road to the Future End at Dubai?”,

176 S. Bagaeen

Davis (2005) analyses Dubai’s boom, noting how, after Shanghai (current population: 15

million), Dubai (current population: 1.5 million) is the world’s biggest building site: an

emerging dream-world of conspicuous consumption and what locals dub “supreme life-

styles”. This tremendous construction activity prompted Nicolson (2006) to write that

“a fifth of the world’s cranes are now based in Dubai”.

A Brief History of Dubai

Modern Dubai is the product of the past 20 years of intensive development. Prior to that,

Dubai was a small trading port that had grown gradually from a fishing village inhabited in

the eighteenth century by members of the Bani Yas tribe.

By the turn of the twentieth century Dubai was a sufficiently prosperous port to attract

settlers from Iran, India and Baluchistan and, by the 1930s, nearly a quarter of the 20,000

population was foreign. Some years later the British also made it their centre on the coast,

establishing a political agency in 1954. In 1971, the British withdrew and Dubai joined

with Abu Dhabi, Sharjah, Ajman, Fujairah, Umm Al Quain and later Ras Al Khaimah

to create the federation of the United Arab Emirates (UAE).

Dubai began to grow at the beginning of the twentieth century into a trading hub. By that

time, Dubai already boasted some 350 shops in the Deira district alone (Dubai Property

Government, 2004). Today, Dubai is the third most important re-export centre in the

world after only Hong Kong and Singapore. Dubai Properties, a member of Dubai

Holding, is the world’s fastest growing global real estate development investment firm.

Dubai’s population, 1.2 million at 2006 estimates, could reach 4 million by 2017. In a

reversal of the situation in the 1930s, of the over 1.2 million people who currently live in

Dubai, 75% are expatriates. Table 1 shows how the population of Dubai has increased

since 1975.

Dubai’s formula for development included several components—visionary leadership,

high quality infrastructure, an expatriate-friendly environment, zero tax on personal and

Table 1. Population growth in Dubai

Year Population

1975 183,187

1980 276,301

1985 370,788

1993 610,926

1995 689,420

2000 862,387

2001 910,336

2002 960,950

2003 1,014,379

2004 1,070,779

2005 1,321,453

2007 (Quarter 1) 1,448,000

Source: Government of Dubai/statistics Centre of Dubai, (accessed 27 June 2007)

http://vgn.dm.gov.ae/DMEGOV/OSI/webreports/401120784SYB04-02-01.pdf

http://vgn.dm.gov.ae/DMEGOV/OSI/webreports/2117025GC05-01-01.pdf

http://vgn.dm.gov.ae/DMEGOV/OSI/webreports/Fig4.pdf

Brand Dubai: The Instant City 177

corporate income and low import duties. The result was that Dubai quickly became a

business and tourism hub for a region that stretches from Egypt to the Indian sub-continent

and from South Africa to the ex-Soviet republics.

The roots of the current property boom in Dubai date back to 2002 with the announce-

ment of the then Ruler of Dubai that freehold ownership of certain properties in Dubai was

available to investors of all nationalities. Since then, several projects have been launched

and sold to foreigners. According to initial results from the building census conducted in

Dubai in 2005 (Al-Mahiri, 2006), the number of housing units stood at 237,728, up from

145,363 in 2000, an increase of nearly 64% that reflects the current building boom in the

city.

The extent of the building boom is such that properties in some projects (Dubai Marina,

Emirates Hills, Jumeirah Islands, Jumeirah Beach Residences, the Meadows, the Springs

and Arabian Ranches) have already been completed and handed over to buyers, with some

already having exchanged hands several times.

Government as Planner vs. Government as Developer

Shanghai is another one of those cities shifting towards a city-state status. This is in

response to the Chinese government adopting a high density vertical city of the kind

that we now see in Dubai. In China, the process had in fact started a long time before

Dubai. In 1984, China opened Shanghai and 13 other coastal cities to foreign investment

as a result of the Chinese Open Door Policy (Lau et al., 2000). The resulting tremendous

shift in Chinese building favouring private developers is highlighted in Table 2; far from

impeding marketization, the state plays the role of accelerating the marketization process

in China (see Quan, 2006).

Dubai is engaged in a construction boom of tremendous proportions and is now begin-

ning to attract heightened international interest. According to Evans (2006), it has been

described from “dull, dull, dull . . . [to] awkward and fragmented”. Whatever the judge-

ment, the building boom gripping Dubai (as illustrated in Figure 3) holds a plethora of

opportunities for modern living, with prices to match, and a marketing campaign (includ-

ing glossy publications, email-shots, and an aggressive sales drive) that has put this former

desert backwater on the world map.

The purpose of all this building has obviously been to create an image of progress and

dynamism where the fastest, biggest, most amazing structures are being built in order to

attract the affluent and the talented, all essential to the consolidation of the successful

Dubai brand, epitomized (at least until such time that the world’s tallest tower is built)

by the 321 metre high Burj Al-Arab hotel. This building (shown in Figure 4) stands in

the sea on an artificial island 280 metres away from the beach on the Dubai shoreline

and is connected to it by a private bridge.

Table 2. The shift towards private housing construction in China

China Public Housing (%) Private Housing (%)

1982–83 100 –

2000 4.8 95.2

Source: Zhu (2006).

178 S. Bagaeen

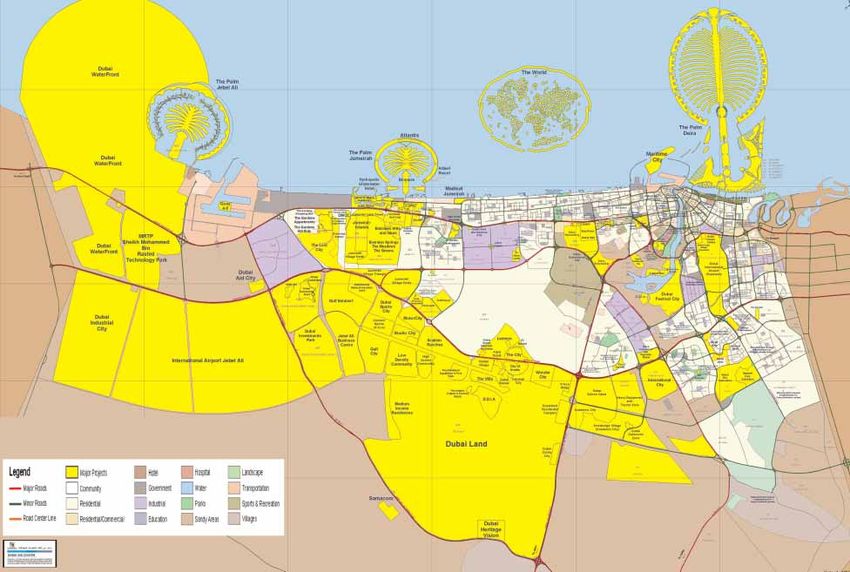

Figure 3. Dubai Urban Projects. Source: Dubai Municipality, http://www.gis.gov.ae/en/downloads/

pdfs/Major%20Projects.pdf

Law of the Land

In the absence of any UAE federal law relating to ownership of land, it is the right of each

individual emirate to pass its own law on matters relating to real estate and property

ownership.

In 2006, Dubai passed such a law confirming the right of non-UAE nationals to own real

estate in certain developments in the city. The new law removes a number of the ambigu-

ities regarding title and ownership and, as such, is a major development for the Dubai

property market.1

In March 2006, and three years after the government first allowed freehold ownership to

expatriates under the three government owned developers, EMAAR Properties, Nakheel

and Dubai Properties (see Appendix 1), Dubai passed a law to legitimize property owner-

ship by foreigners who had previously bought property indirectly through contracts with

these developers. By mid-2006, Rahman (2006) points out that some 13,000 families had

already moved into freehold homes and that another 7000 had been expected to move by

the end of 2006.

Under the old land regime, real estate in Dubai could only be owned by UAE nationals,

and to a lesser extent by nationals of the countries of the Gulf Cooperation Council (GCC)

states. With the new real estate projects in Dubai being marketed to all nationalities on a

freehold basis, essential to the entrepreneurial Dubai brand, the need for clear legislation

on who can own property was paramount.

Under the new law, non-GCC expatriates are given the right to acquire freehold and 99-

year lease property in certain locations marketed by the leading developers, such as the

Palms, Jumeirah Islands, Emirates Hills, the Meadows, the Montgomerie and Arabian

Ranches.

Brand Dubai: The Instant City 179

Figure 4. Burj Al-Arab Hotel. Source: Bagaeen, 2006

Previously, international buyers in Dubai had been buying property off-plan and

dealing directly with the developer, usually the sales team or an in-house legal team.

Buyers were also required to pay an up-front deposit towards the selling price,

usually around 10%. Although developers have been insisting as a condition of sale

that existing buyers are prevented from selling on properties to new buyers in the con-

struction phase and until such time that existing buyers are themselves registered as the

owners, this is not enshrined in the law and is perhaps an attempt by developers to cut

their losses by preventing unwelcome speculation on the price of property which could

undermine the developers’ ability to dispose of unsold units. Developers who have

sanctioned this kind of speculative sale, particularly on the Palm Jumeirah, shared in

the existing buyers’ profits by charging a premium for registering ownership at the

pre-completion stage.

180 S. Bagaeen

Table 3. DAMAC Properties Archived Availability List (2006)

Project/Date The Waves Palm Terrace Palm Springs Lake Terrace Lake View

of sale (1 bed apt) (3 bed apt) (2 bed apt) (2 bed apt) (studio)

1/12/2002 778,000

1/06/2003 800,000 1,415,000 727,000

1/12/2003 818,000 1,600,000 1,136,000 790,000

1/06/2004 900,000 2,225,000 2,325,000 1,168,000 323,000

1/12/2004 920,000 2,937,000 3,025,000 1,237,000 477,000

1/06/2005 1,200,000 4,050,000 4,700,000 1,620,000 625,000

Source: Supplied to author courtesy of DAMAC.

Capital growth in property investment in Dubai continues on an upward trend. Table 3

shows the growth in property prices (all prices in UAE Dirham—AED) for projects under

construction by DAMAC Properties (a Dubai based developer).

Brand Downside? The Impact of Fast Track Real Estate Development on Rents

The real estate boom in Dubai has had a significant impact on the cost of living in the city

and in the adjacent emirates over the last couple of years. For example, residential rents

rose between 20 and 40 per cent in the first half of 2005 (see Westley, 2005) and again

by up to 50 per cent in some parts of the city (Westley, 2006). While an official cap on

rent increases to 15 per cent has been imposed until the end of 2006 to reduce the

frenzy, the increase in rents remains a deep concern in the city.

Table 4 illustrates how rents have changed in Sharjah (within Dubai’s commuter belt)

and Dubai over the last three years. Table 5 also shows how commercial rents in Dubai

have risen to values that are comparable with its main competitors in the region, Hong

Kong and Singapore.

The Impact of Fast Track Real Estate Development on Infrastructure

The challenge for Dubai is to retain its attractiveness for investors and expatriate residents

as not just an attractive place to live and work, but also as a cost-effective location.

The city’s rapid expansion has necessitated a reworking of the city’s infrastructure.

While the city’s population has grown at an average annual rate of 6.4% over the past

three years, the number of cars on the road has increased by 10% each year, soaring

from 350,000 to 750,000 over the period 2004 –2006 (see Lootah, 2006). This is becoming

a problem in many cities in the Gulf as can be seen from Figure 5, which shows the state of

Riyadh’s roads during midday peak period.

Commuting between Dubai and Sharjah is on the increase, particularly given the

cheaper cost of living in Sharjah. Around 350,000 daily trips are made by car between

Dubai and Sharjah, the UAE’s main commuter route, and average daily trips in Dubai

are anticipated to grow from 3.1 million per day to 13.1 million by 2020 (see Ahmed,

2005).

With a $817 million annual road building programme already in place, Dubai’s road

network is under continuous expansion with over 20 major new projects under

Table 4. Rents in Sharjah and Dubai

Average increase Average increase Total increase

Category Year 2004 Year 2005 Year 2006 (March) 2004/05 (%) 2005/06 (M) (%) 2004–2006 (M) (%)

Sharjah

Studio 14,000 – 20,000 16,000– 28,000 20,000– 30,000 29.4 3.6 47

One bedroom 17,000 – 26,000 24,000– 38,000 26,000– 40,000 47.6 6.4 54.7

Two bedroom 25,000 – 45,000 28,000– 55,000 30,000– 60,000 18.5 9.7 28.1

Three bedroom 35,000 – 75,000 38,000– 90,000 40,000– 95,000 16 5.6 21.8

Dubai

Studio 24,000 – 30,000 30,000– 45,000 30,000– 55,000 38.5 16 79

One bedroom 32,000 – 45,000 40,000– 60,000 45,000– 65,000 29.8 10 42.8

Two bedroom 42,000 – 75,000 55,000– 110,000 60,000 – 120,000 41 9 53.8

Brand Dubai: The Instant City

Three bedroom 70,000 – 110,000 75,000– 130,000 85,000 – 135,000 13.8 7.8 22.2

£1 ¼ 6.75 AED; $1 ¼ 3.67 AED.

Source: Saberi (2006).

181

182 S. Bagaeen

Table 5. Occupancy cost (in US$) per sq. ft. commercial space

Dubai London Hong Kong Singapore New York

64.4 119.11 75.85 33.71 53.39

Source: Westley (2005).

construction or recently completed, including a 1.5 kilometre tunnel under the airport and

a new 12-lane bridge across Dubai Creek. This third bridge is intended to take the pressure

off Sheikh Zayed Road, Al Garhoud Bridge, Maktoum Bridge and the Shindagha Tunnel

that link the two sides of the Creek.

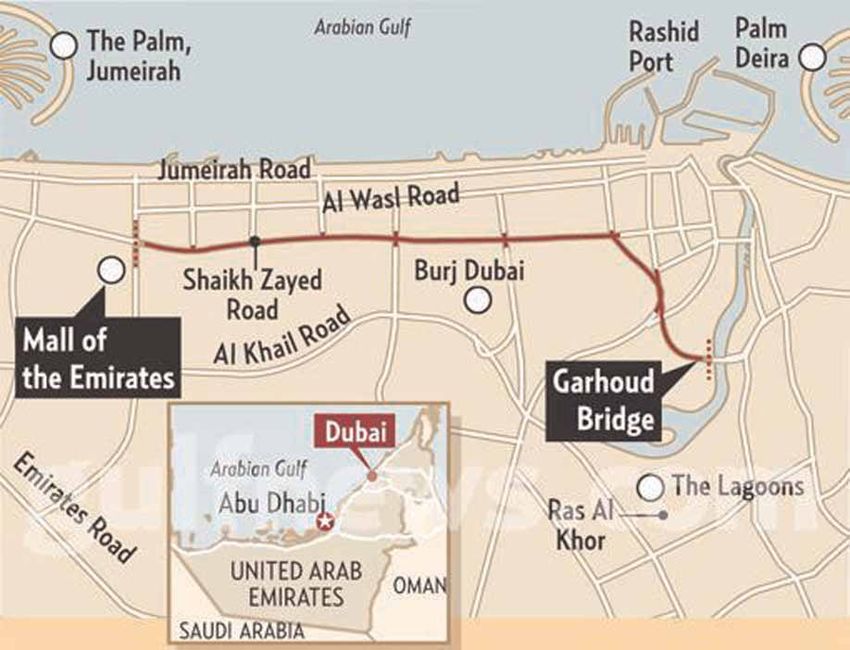

Late in 2006, Dubai Municipality investigated the option of introducing a toll system on

major routes into the city. This was confirmed by the Dubai Roads and Transport

Authority (RTA) on 1 May 2007 (Ahmed, 2007) with the first phase of the toll system,

Salik, coming into effect on 1 July (see Figure 6). There will be two toll gates, one on

Al-Garhoud Bridge and the other on the Fourth Interchange (near the Mall of the Emirates)

on Sheikh Zayed Road. Motorists will be charged as they pass the toll gates. In Arabic

‘salik’ means clear and the word has been chosen as the brand name for the toll system

because it aims to ensure smooth traffic flow.

Investment in public transport is also a major component of Dubai’s plans for the future.

One pillar of this service is the driverless metro being built by Mitsubishi Heavy Industries

of Japan with finance provided by Dubai Municipality, which is targeting an increase of

public transport market share from 4.7% (2005) to around 17% by 2020.

Figure 5. Traffic at a standstill on Riyadh’s main trunk road through the city. Source: Bagaeen, 2007Brand Dubai: The Instant City 183

Figure 6. Dubai toll road. Source: Map courtesy of Gulf News

There appears to be an understanding on behalf of the RTA in the city that developing

sustainable densities and increasing demographic weight and growth along the metro’s

route (see Figure 7) and in certain employment nodes around Dubai would encourage

optimum use of the system. The future will involve linking Dubai to Sharjah and Abu

Dhabi with the priority given to the former.

Figure 7. Dubai metro. Source: Illustration courtesy of Dubai Municipality, 2007184 S. Bagaeen

Following in Dubai’s Footsteps: Abu Dhabi, Bahrain and Doha

Another emirate, Abu Dhabi, is set to become the home of the world’s largest

Guggenheim museum. In July 2006, Abu Dhabi’s Tourism Development and Invest-

ment Company (TDIC) signed a memorandum of understanding with the New York-

based Guggenheim Foundation to establish a world-class museum devoted to modern

and contemporary art (see Ameen, 2006). The museum, to be called the Guggenheim

Abu Dhabi (GAD), designed by Frank Gehry, will be built on Saadiyat Island (an

island off the emirate’s shores dedicated to culture) and is expected to open in

2011. The island is the flagship project of the TDIC, the organization charged with

overseeing the transformation of this unique natural asset into a strategic international

tourism destination.

In Bahrain, Skidmore, Owings & Merrill (SOM) has been selected to develop a set of

comprehensive national planning strategies aimed at enhancing the quality of urban

growth while protecting and enhancing the natural resources of the Gulf island country.

Figure 8. Guggenheim Abu Dhabi. Source: courtesy of TDIC Abu DhabiBrand Dubai: The Instant City 185

Figure 9. The Bahrain Financial Harbour under construction (foreground) with the World Trade

Centre designed by Atkins in the background. Source: Bagaeen, 2006

With the real estate sector booming, Bahrain has also started to build its share of projects

including the Bahrain Financial Harbour where the country’s tallest towers (at 260 metres)

are located (see Figure 9).

Qatar’s economy will exceed $60 billion in value by 2011 as the country enjoys one of

the fastest growth rates in the world. Qatar’s GDP has already doubled from $17.5 billion

to $35 billion in the last five years (Gulf News, 26 February 2006).

Real estate is integral to this growth; the Pearl is the country’s first international real

estate venture, its largest development and the first to offer international investors freehold

in the country. It is a $2.5 billion man-made island covering 400 hectares of reclaimed land

off the Doha waterfront (see Figure 11). It is a four-phase mixed-use development com-

prising ten distinct, themed districts to be developed over five years housing beachfront

villas, elegant town homes, luxury apartments, exclusive penthouses, five-star hotels,

marinas and schools as well as upscale retailers and restaurants.

Conclusions: Sustainable Urban Development?

Little has slowed Dubai’s twenty-first century gold rush, a phenomenon described this way

by architect Ray Hoover, managing principal at TVS, an Atlanta firm with a hand in several

high profile projects: “At best, it’s unbridled optimism. At worst, unbridled chaos. Fire.”2186 S. Bagaeen

Figure 10. Construction on the Doha waterfront. Source: Bagaeen, 2006

Figure 11. An aerial image of the Pearl Qatar under construction. Source: Bagaeen, 2006Brand Dubai: The Instant City 187 While there is no doubting the vision and drive behind the transformation and persistent campaign to sell Dubai to affluent international entrepreneurs, its Disneyland lifestyle is built on, literally, the poorly paid labour of workers from the subcontinent, and is surely unsustainable in terms of both basic humanity and environmental common sense. For one thing, the frenetic pace and character of Dubai’s unprecedented development portends a future of environmental and sustainability problems. Although much of its expansion is still on the drawing board, traffic is already at a standstill for hours during the day along its main artery, Sheikh Zayed Road, and concern is also growing over the long-term impacts of desalination of gulf waters for irrigation and the endlessly growing demand for energy to cool its gleaming glass towers. Development here has generally ignored such fundamental environmental factors as climate or geography, and the consequences of 15 years of heedless expansion and imma- ture design decisions may not be easy to fix. From the air, the Palm projects already create a highly visible impression. And back down at sea level, significant changes in the marine environment are also making their marks. As a result of the dredging and re-depositing of sand for the construction of the islands, the typically clear waters of the Gulf have become clouded with silt. Construction is reportedly damaging the marine habitat, burying coral reefs, oyster beds and subterranean fields of sea grass, threatening local marine species as well as other species dependent on them for food. Oyster beds have been covered in as much as two inches of sediment, while above water beaches are eroding with the dis- ruption of natural currents. The form and the growth of Dubai have followed a variation of the Los Angeles or Las Vegas models. Writing about Los Angeles, Soja (1992, pp. 199– 200) could have been writing about today’s Dubai: With exquisite irony, contemporary Los Angeles has come to resemble more than ever a gigantic agglomeration of theme parks, a life space comprised of Disney- worlds. It is a realm divided into showcases of global village cultures and mimetic American landscapes, all embracing shopping malls and crafty main streets, corporation-sponsored magic kingdoms, high-technology based experimen- tal prototype communities of tomorrow, attractively packaged places for rest and recreation all cleverly hiding the buzzing workstations and labour processes which help to keep it together. Tomorrow’s Dubai, today, is the result of a carefully devised and strategically planned economy where tourism, construction, banking, commerce and trading act as levers for progress that is no longer measured by the oil barrel. To deal with tomorrow problems today, Dubai has launched a blitz of infrastructure projects—ring roads, double-decked highway flyovers, new bridges, a metro and monorail system, even air-conditioned bus stops—to try to solve the problem. But Dubai’s gargantuan, autonomous developments and burgeoning suburban-style subdivisions will pose a formidable challenge. To achieve sustainable development, Dubai has introduced several strategic plans with regard to urban planning and heritage conservation, such as the Strategic Urban Growth Plan for the Emirate of Dubai (2000 – 2050), the Structural Plan for Dubai Urban Area (2000 – 2020), the First Five Year Plan for Dubai Urban Area (2000 – 2005), and several

188 S. Bagaeen

other legislation on land use in Dubai including the inaugural Dubai Forum for Sustainable

Development in March 2006.

Will any of this make a difference? This is where the uncertainly begins as more cities in

the Gulf and the Middle East begin to emulate Dubai. Could the future therefore be one big

bubble of unsustainable real estate developments?

Appendix

The three largest (by portfolio of work) property developers in Dubai

1. Emaar

Emaar is the world’s largest real estate company in terms of market capitalization. It is a

public joint stock company listed on the Dubai Financial Market and has been instrumental

in reshaping the outskirts of Dubai with residential and leisure projects.

Emaar has several real estate projects in various stages of completion: these include

Dubai Marina, Arabian Ranches, Emirates Hills, the Meadows, the Springs, the

Greens, the Lakes, the Views and Emaar Towers and Burj Dubai (billed as the world’s

tallest man-made structure) in downtown Dubai, itself planned to be the most prestigious

one square kilometre on earth. By March 2006, Emaar had built some 13,000 homes in

Dubai, with many more in the pipeline.

Dubai Marina is a US$10 billion project that will be completed over a 20-year period

(Figure 12). The first phase has involved the construction of a 3.5 kilometre canal and

Figure 12. Dubai Marina. Source: Bagaeen, 2005Brand Dubai: The Instant City 189

marina area connected to the sea. A mixed-use development on approximately 578 hec-

tares, the marina is planned as one of the major new centres within the city. Designed

with the intent to create a new focus for high density development, it was conceived as

a “city within the city” that would help shift the perceived centre of Dubai further west

along the shore of the Gulf.

Dubai Marina’s first phase consists of 1026 waterfront apartments in six high rise towers

and 64 villas on a podium containing swimming pools, sports facilities and shops. Dubai

Marina is designed so that residents can arrive home, park their car and walk to take

advantage of all the resources in the community. Retail shops and community services

will be built into grade-level building podiums in neighbourhood centres. Larger shopping

facilities with restaurants and cafes are planned at key locations along the promenade

around the perimeter of the marina and along major boulevards. All residential develop-

ment is within a five-minute walk of the marina promenade.

Emirates Hills, a gated community billed as ‘Dubai’s most prestigious residential devel-

opment’, has been built as a golfing community whose first phase consists of a residential

golf estate, parks, 20 lakes and the 18-hole championship Colin Montgomerie golf course

(Figure 13).

In 2004, Emaar began construction of its most ambitious project within the UAE, the $20

billion Burj Dubai Downtown development. This project includes Burj Dubai—at around

800 metres high, the world’s tallest tower when completed in 2008 (see Figures 14 and 15),

and Dubai Mall—the world’s largest entertainment and shopping mall.

Figure 13. Emirates Hills. Source: Bagaeen, 2005190 S. Bagaeen

Figure 14. Burj Dubai. Source: Courtesy of EMAAR, 2005

Emaar has also been involved in joint ventures and regional projects through its Emaar

International division with projects spanning India, Egypt, Turkey, Morocco, Syria, Paki-

stan, Tunisia and Saudi Arabia. Major international projects include: Uptown Cairo in

Egypt; Boulder Hills, a world-class leisure and residential community in Hyderabad,

India; multiple resort projects in Morocco; Eighth Gate project in Damascus, the city’s

first master planned community; and Lakeside in Istanbul, a landmark development for

Turkey’s cultural and commercial hub.Brand Dubai: The Instant City 191

Figure 15. Burj Dubai under construction. Source: Bagaeen, 2006

Emaar is also heading a consortium of Saudi companies to develop a $26 billion project

in Saudi Arabia known as the King Abdullah Economic City on the Red Sea north of

Jeddah. Situated on 5,500 hectares of Greenfield land with a 35 kilometre shoreline, the

city will be a mixed use development with six components: the Seaport, Industrial District,

Financial Island, Education Zone, Resorts and the Residential Area.

2. Nakheel

Nakheel, one of the United Arab Emirates’s leading property developers, currently has $30

billion worth of projects under development. When complete, these developments, which192 S. Bagaeen

Figure 16. The Palm Jumeirah with the spine on the left and the leaves on the right of the image.

Source: Bagaeen, 2006

include the Palms projects, will have added 1500 kilometres of waterfront to Dubai, once

limited to 70 kilometres.

It was from this need to increase the length of the waterfront that the idea of the Palm

was born—the perfect icon for maximizing beachfront and, at the same time, one that pays

homage to one of Dubai’s most important symbols, the palm tree. Spanning 5 kilometres

Figure 17. Luxury flats on the spine of the Palm under construction. Source: Bagaeen, 2006Brand Dubai: The Instant City 193

Figure 18. Luxury flats on the spine of the Palm under construction. Source: Bagaeen, 2006

in length and five in width, The Palm Jumeirah is one of the world’s largest man-made

islands, creating the shape of a palm tree in the Arabian Gulf. Another project, called

the World, comprises man-made islands shaped like countries which are being sold for

millions of dollars.

Following years of feasibility studies, the Palm was launched in 2001 and reclamation

began that year. At that stage the Palm was its own separate company. However, with

the launch of the second Palm (in Jebel Ali, Dubai’s Port and Free Zone), the name of

the company was changed in 2003 to Nakheel (meaning ‘Palms’ in Arabic).

The first Palm to be finished will be the Palm Jumeirah. It will include 1500 beachside

villas and 2200 shoreline apartments offering luxury beachfront living (see Figures

16 –20).

3. Dubai Holding

Dubai Holding currently has 19 companies operating in a variety of sectors ranging from

health, technology, finance, real estate, research, education, tourism, energy, communi-

cation, industrial manufacturing, biotechnology and hospitality. These companies

include: Dubai Internet City, Dubai Media City, Dubai Healthcare City, Dubailand,

Dubai International Capital, Dubai Industrial City, Dubai Properties, Dubai International

Properties, Dubai Investment Group, Dubai Energy, Dubai Knowledge Village, Dubai

Outsource Zone, International Media Production Zone, E-Hosting Datafort, Empower,

SamaCom, Jumeirah Group, Dubiotech and Dubai Studio City. Jumeirah Beach

Residences and Dubailand are two flagship projects of Dubai Holding.194 S. Bagaeen Figure 19. Luxury flats on the spine of the Palm under construction. Source: Bagaeen, 2006 Figure 20. Luxury flats on the spine of the Palm under construction. Source: Bagaeen, 2006

Brand Dubai: The Instant City 195 Figure 21. Jumeirah Beach Residences. Source: Bagaeen, 2005 Figure 22. Jumeirah Beach Residences. Source: Bagaeen, 2006

196 S. Bagaeen

When complete, Jumeirah Beach Residences will have 36 residential towers comprising

6,400 flats and four hotel towers with 4,000 rooms (see Figures 21 and 22). Wimberly

Allison Tong and Goo, an architectural, planning and consulting firm specializing in hos-

pitality, entertainment and leisure, is providing consultancy services on various construc-

tion aspects, including the architectural design. Six other companies, including Hyder,

Arif & Bintoak, Arenco, Atkins, Dar and RMJM, are supervising the implementation of

quality measures through all phases of the project. Mace International Ltd. is overseeing

the project management, cost management, and facilities management of the entire

development.

Notes

1. The full text of the property law (or The Dubai Real Estate Registration Law No. 7 of 2006) is available at

http://archive.gulfnews.com/articles/06/03/14/10025458.html (accessed 14 March 2006).

2. Quoted in the Atlanta Journal-Constitution accessed on 10 July 2006. Available at http://www.ajc.com/

sunday/content/epaper/editions/sunday/news_44e903d473a1f0b10063.html.

References

Ahmed, A. (2005) Study on water taxi service between Dubai and Sharjah gets underway, Gulf News, 9 August.

Ahmed, A. (2007) Authority dispels fears of clogged Dubai roads, Gulf News, 21 May.

Al-Mahiri, A.O. (2006) Head of the Dubai 2005 Census Committee in an interview with the author.

Ameen, A. (2006) Frank Gehry to design Guggenheim museum, Gulf News, 9 July.

Ashworth, G.J. and Voogd, H. (1990) Selling the City: Marketing Approaches in Public Sector Urban Planning

(London: Belhaven Press).

Avraham, E. (2004) Media strategies for improving an unfavourable city image, Cities, 21(6), pp. 471–479.

Bagaeen, S. (2006) Redeveloping former military sites: competitiveness, urban sustainability and public partici-

pation, Cities, 23(5), pp. 339 –352.

Bradley, A., Hall, T. & Harrison, M. (2002) Selling cities, Cities, 19(1), pp. 61 –70.

Burgess, J.A. (1982) Selling places: environmental images for the executive, Regional Studies, 16(1), pp. 1–17.

Davis, M. (2005) Does the Road to the Future End at Dubai? Available at http://www.tomdispatch.com/

index.mhtml?pid ¼ 5807 (accessed 10 July 2006).

Dubai Government (2004) Dubai Property Investment Guide.

Eben Saleh, M.A. (2001) The changing image of Arriyadh city, Cities, 10(5), pp. 315–330.

Evans, R.H. (2006) Letter from Dubai, RIBA Journal, July, 113(7), p. 6.

Gold, J.R. & Ward, S.V. (Eds) (1994) Place Promotion: The Use of Publicity and Marketing to Sell Towns and

Regions (Chichester: John Wiley and Sons).

Hall, J. (1998) Urban Geography (London: Routledge).

Hall, T. & Hubbard, P. (Eds) (1998) The Entrepreneurial City (Chichester: Wiley).

Kearns, G. & Philo, C. (Eds) (1993) Selling Places: The City as Cultural Capital, Past and Present (Oxford:

Pergamon Press).

Lau, S., Mahyab-uz-Zaman, Q.M. & Mei, S.H. (2000) A high density “instant” city: Pudong in Shanghai, in:

M. & R. Burgess (Eds) Compact Cities: Sustainable Urban Forms for Developing Countries (London: SPON).

Lootah, H.N. (2006) Infrastructure struggling to keep up with Dubai growth, Acari, 2(24), p. 31.

Nicolson, A. (2006) Boom town, The Guardian, 13 February.

Paddison, R. (1993) City marketing, image reconstruction and urban regeneration, Urban Studies, 30(2), pp.

339– 350.

Quan, Z.X. (2006) Institutional transformation and marketisation: the changing patterns of housing investment in

urban China, Habitat International, 30, pp. 327 –341.

Rahman, S. (2006) Master developers to register clients’ freehold assets, Gulf News, 17 March.

Saberi, M. (2006) Flat sharing only option as rents spiral out of control, Gulf News, 16 March.

Soja, E. (1992) Taking Los Angeles apart: towards a post modern geography, in: R.T. LeGates & F. Stout (Eds)

The City Reader, 3rd edition (London: Routledge).Brand Dubai: The Instant City 197

Urban, F. (2002) Small town, big website?, Cities, 19(1), pp. 49–59.

Westley, D. (2005) Is Dubai still good value?, Gulf News, 19 August.

Westley, D. (2006) Is Dubai still good value?, Gulf News, Business Feature, 13 March.

Zhu, J. (2006) Pro-growth urban planning in China. Seminar at the Department of Urban Studies, University of

Glasgow, 17 February.

Useful Websites

The Atlanta Journal-Constitution: http://www.ajc.com.

Bahrain Financial Harbour: http://www.bfharbour.com.

Dubai Holding: http://www.dubaiholding.com.

Dubai Municipality: http://www.dm.gov.ae.

Dubai Statistics: http://vgn.dm.gov.ae/DMEGOV/OSI/dm-osi-mainpage.

Durrat Al Bahrain: http://www.durratbahrain.com.

EMAAR: http://www.Emaar.com.

Nakheel: http://www.nakheel.com.

The Pearl Qatar: http://www.thepearlqatar.com.You can also read