Industry Name - Engineering & Construction Quarterly Update | Q1 2022 - MNP

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Engineering & Construction

Quarterly Update | Q1 2022

[Industry Name]

MNPCF.ca

Industry Overview

M&A Transactions & Performance

NORTH AMERICAN ENGINEERING & CONSTRUCTION M&A ACTIVITY

2.5 25

2.2

Transaction Volume (Number of Deals)

2.0 20

Transaction Value ($ Billions)

1.6

1.5 1.4 1.4 15

1.3

1.0 0.9 0.9 0.9 10

0.9

0.5 0.5 0.6

0.5 0.4 5

0.3 0.4

0.2

- -

Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1

Canadian Transaction Value US Transaction Value

Canadian Transaction Volume US Transaction Volume

Source: Capital IQ. Data as of March 31, 2022.

Above noted mid-market M&A activity includes disclosed transactions not exceeding a total transaction value of $500 million. All figures are in CAD.

Transaction value is only inclusive of total transaction values which have been disclosed within Capital IQ.

Q1 Transactions (Canada) Q1 Transaction Value (Canada) Q1 Transaction Value (US) Q1 Transactions (US)

1 $145 million $1.2 billion 11

(-45% vs. Q4 2021) (+434.5% vs. Q4 2021) (-10.7% vs. Q4 2021) (-50% vs. Q4 2021)

Engineering and construction merger and acquisition (M&A) activity in Q1 2022 exceeded $1.2 billion in disclosed

transaction value across 12 deals in Canada and the US. US transactions accounted for 11 of these deals,

representing the largest quarterly volume in the past four years. The largest transaction in the quarter was US

based, and involved CalPortland Company’s acquisition of certain West Coast cement and ready mixed concrete

operations of Martin Marietta Materials, Inc. for $317 million. In the last 12 months, the majority of acquirers have

been strategic. Strategic acquisitions continue to drive industry activity, as participants target expansion into new

markets and mitigating skilled labour shortages.

Private Equity Deal Multiples PE Sponsored Multiples

10.0x (Engineering Services) 8.0x (Heavy & Civil Construction) 7.1x

7.9x 6.5x

8.0x 6.0x 5.3x

4.9x

EV / EBITDA

EV / EBITDA

6.0x 5.1x 5.1x

4.0x

4.0x

2.0x

2.0x

0.0x 0.0x

10 - 25 25 - 50 50 - 250 10 - 25 25 - 50 50 - 100 50 - 250

Total Enterprise Value Range ($ millions) Total Enterprise Value Range ($ millions)

Source: GF Data. Data as of April 2022. Page 2

Select Recent M&A Transactions

• Brookfield Renewable Corporation owns and

Closed Feb. 7, 2022 operates a portfolio of renewable energy power

generating facilities primarily in the US, Europe,

EV $819.1 million Colombia, and Brazil.

Acquired • Urban Grid Solar develops and operates utility-scale

EV/EBITDA N/A solar and renewable energy projects.

• The acquisition will allow Brookfield Renewable

Location Toronto, ON Corporation to strengthen its renewable energy

(Vendor)

service offerings.

• Orion Energy Systems, Inc. researches, designs,

develops, manufactures, markets, sells, installs, and

Closed Jan. 1, 2022 implements energy management systems for

commercial office and retail, exterior area lighting,

Acquired EV $5.6 million and industrial applications in North America.

• Stay-Lite Lighting Inc. provides interior/exterior

EV/Revenue 0.5x lighting maintenance and electrical services to

industrial, commercial, and retail businesses in the

Location Manitowoc, United States.

(Vendor) WI

• The acquisition allows Orion Energy Systems to

expand their service capabilities to a larger customer

base.

• MYR Group Construction Canada, Ltd. constructs

Closed Jan. 4, 2022 electrical transmission, substation, and distribution

systems for electric utilities and government agencies.

Acquired EV $145.4 million • Powerline Plus Ltd. offers engineering, procurement,

and construction services to utility companies.

EV/EBITDA N/A • The acquisition will allow MYR Group Construction

Canada Ltd. to strengthen its market share, while

Location Henderson, being able to expand its service offerings

(Vendor) CO simultaneously.

• Johns Lyng Group Limited provides integrated

building services in Australia and internationally.

Closed Jan. 1, 2022 systems for electric utilities and government agencies.

• Reconstruction Experts Inc., is a general contracting

EV $254.3 million company that provides reconstruction, restoration,

Acquired renovation, and remodeling services for residential,

EV/EBITDA 7.8x commercial, and industrial properties in Colorado,

California, Texas, Arizona, Nevada, and Wyoming.

Location Australia • The acquisition will allow Johns Lyng Group Limited

(Vendor)

to expand their service offerings in existing and new

geographic markets.

Source: Capital IQ.

All figures are in CAD. Page 3

Industry Overview

Engineering Services in Canada

The Engineering Services industry applies the physical laws and principles of engineering in the design,

development and use of machines, materials, instruments, structures, processes, and systems.

Products and Services

Industry Glance

Segmentation (2022)

2022 Revenue

$35.7B 13%

30%

Annual Growth 2017 – 2022 8%

2.1%

Projected Annual Growth 2022 – 2027 23%

2.1% 25%

Number of Businesses in 2022 Advisory Services

28,020 Energy and Mining

Residential and Commercial

Power Generation

Transportation

Heavy Engineering Construction in Canada

Heavy Engineering Construction performs new construction, reconstruction, rehabilitation, and repairs.

Industry Glance Products and Services

Segmentation (2021)

2021 Revenue

$53.9B 9%

9%

Annual Growth 2016 – 2021 36%

1.8% 14%

Projected Annual Growth 2021 – 2026

2.5%

19% 14%

Number of Businesses in 2021

2,742

Electric Power Land Transportation

Repair and Maintenance Mining Engineering

Marine and Waterworks Other

Source: IBISWorld Industry Report 54133CA Engineering Services in Canada March 2022.

Source: IBISWorld Industry Report 23799CA Heavy Engineering Construction in Canada. December 2021. Page 4

Macroeconomic Indicators

Key external drivers that affect the Engineering & Construction industry in Canada include the value of non-

residential construction (expenditures on office buildings, hospitals, factories, power plants, mining shafts,

communication lines, farms, railroads, and schools), aggregate private investment (investment in gross fixed capital

formation and inventories), government expenditure and investment (the total value of services produced by

federal, provincial, and local governments as well as investment in fixed assets), and the interbank overnight

lending rate in Canada.

Canada’s major cities such as Toronto experienced another quarter of acceleration in house prices. Supply was

scarce in the winter months compared to demand, which resulted in multiple bidding wars driving up prices.

However, there may be some easement on housing price acceleration due to a combination of interest rate

increases and new policies. In March 2022, the Bank of Canada increased interest rates by 0.25%, followed by

another 0.5% increase subsequent to Q1 in April 2022. In addition, the Federal Government is proposing new

measures to improve affordability such as a temporary ban for purchasing homes on individuals and companies

who are not Canadian residents. Lastly, inflation reached a high of 6.7%, putting downward pressure on Canadian’s

budgets and ability to purchase a home.

VALUE OF NON-RESIDENTIAL VALUE OF RESIDENTIAL CONSTRUCTION -

CONSTRUCTION - CANADA CANADA

200 200

175

150 150

$CAD Billions

$CAD Billions

125

100 100

75

50 50

25

- -

Historical Forecast Historical Forecast

GOVERNMENT EXPENDITURE AND INVESTMENT AGGREGATE PRIVATE INVESTMENT -

- CANADA CANADA

600 475

575 450

550

525 425

$CAD Billions

400

$CAD Billions

500

475 375

450

350

425

400 325

375 300

350 275

325

300 250

Historical Forecast Historical Forecast

Source: IBISWorld Business Environment Reports.

“F” indicates forecast. “CAGR” indicates compound annual growth rates. Page 5

Public Comparable Analysis

Growth, Margins & Multiples

LTM REVENUE GROWTH NTM REVENUE GROWTH

Heavy Civil 10% AVG: 11.0% Heavy Civil 4% AVG: 8.7%

Engineering 4% Engineering 6%

Construction Engineering 16% Construction Engineering 9%

Aggregate Supplier 14% Aggregate Supplier 15%

0% 5% 10% 15% 20% 0% 5% 10% 15% 20%

LTM EBITDA MARGIN NTM EBITDA MARGIN

Heavy Civil 9% Heavy Civil 7%

AVG: 15.7% AVG: 13.2%

Engineering 11% Engineering 10%

Construction Engineering 14% Construction Engineering 10%

Aggregate Supplier 29% Aggregate Supplier 27%

0% 10% 20% 30% 40% 0% 5% 10% 15% 20% 25% 30%

LTM EV/EBITDA NTM EV/EBITDA

Heavy Civil 6.9x Heavy Civil 6.0x

AVG: 10.9x AVG: 10.2x

Engineering 13.9x Engineering 13.3x

Construction Engineering 8.9x Construction Engineering 8.9x

Aggregate Supplier 14.0x Aggregate Supplier 12.7x

0.0x 5.0x 10.0x 15.0x 0.0x 5.0x 10.0x 15.0x

Source: Capital IQ. Data as of March 31, 2022.

Valuation details provided on page 8.

“LTM” refers to last twelve months. “NTM” refers to next twelve months. Page 6

Public Comparable Analysis

Performance Analysis

Engineering and Construction Peer Group

Share Price Performance – Q1 2022

7.08%

-7.63%

-10.08%

-13.75%

Share Price Performance – LTM

22.85%

10.70%

5.21%

-8.25%

Historical LTM EV/EBITDA – LTM

16.05x

10.02x

9.11x

6.87x

Source: Capital IQ. Data as of March 31, 2022.

Further details provided on page 8.

“LTM” refers to last twelve months. Page 7

Public Comparable Analysis

Trading Multiples & Operating Statistics

We have selected a group of publicly traded engineering and construction entities for this high-level analysis.

These public companies help act as a proxy for the industry and provide strong industry context.

LTM Operating Figures NTM Consensus Estimates Valuation

Market Enterprise Revenue EBITDA Revenue EBITDA NTM LTM

Company Capitalization Value Revenue Growth EBITDA Margin Growth Margin EV/EBITDA EV/EBITDA LTM EV/REV

Heavy Civil

EMCOR Group, Inc. $7,406 $7,056 $12,724 15.8% $1,074 8.4% (100.0%) N/A 8.3x 6.5x 0.6x

Primoris Services Corporation $1,585 $2,366 $4,426 0.2% $472 10.7% 7.1% 8.0% 6.4x 5.1x 0.5x

Construction Partners, Inc. $1,717 $2,042 $1,272 25.4% $134 10.5% 16.9% 11.3% 12.5x 15.5x 1.6x

Tutor Perini Corporation $689 $1,772 $5,874 (12.7%) $549 9.3% 0.3% 6.1% 5.1x 3.3x 0.3x

Granite Construction Incorporated $1,879 $1,633 $3,735 (2.2%) $181 4.8% 5.9% 7.6% 5.7x 8.5x 0.4x

Sterling Construction Company, Inc. $1,011 $1,515 $2,093 16.0% $223 10.7% 15.2% 10.5% 6.3x 7.2x 0.8x

Aecon Group Inc. $1,032 $1,279 $4,209 15.3% $161 3.8% 4.4% 6.2% 4.8x 7.5x 0.3x

Bird Construction Inc. $490 $453 $2,220 47.6% $122 5.5% 13.1% 4.5% 4.0x 3.7x 0.2x

Median $1,309 $1,703 $3,972 15.6% $202 8.9% 6.5% 7.6% 6.0x 6.9x 0.5x

Mean $1,976 $2,264 $4,569 13.2% $364 8.0% (4.6%) 7.8% 6.6x 7.2x 0.6x

Engineering

Jacobs Engineering Group Inc. $22,232 $26,509 $17,980 4.9% $2,176 12.1% 12.4% 9.5% 14.6x 13.5x 1.5x

WSP Global Inc. $19,564 $21,422 $10,279 16.8% $1,245 12.1% (16.1%) 17.1% 14.5x 17.2x 2.1x

AECOM $13,554 $16,110 $16,824 (0.2%) $1,373 8.2% 7.5% 6.5% 14.0x 11.9x 1.0x

KBR, Inc. $9,532 $11,745 $9,478 33.4% $1,087 11.5% (9.2%) 10.1% 14.5x 10.5x 1.3x

Stantec Inc. $6,986 $8,694 $3,636 (1.3%) $527 14.5% 19.5% 15.9% 12.6x 16.5x 2.4x

SNC-Lavalin Group Inc. $5,284 $6,857 $7,371 5.2% $479 6.5% 0.3% 9.2% 9.7x 14.3x 0.9x

Fluor Corporation $5,058 $3,971 $15,736 (12.2%) $528 3.4% 11.2% 3.2% 7.2x 7.6x 0.3x

NV5 Global, Inc. $2,571 $2,733 $894 7.2% $176 19.7% 12.6% 18.4% 15.3x 15.7x 3.1x

Willdan Group, Inc. $493 $626 $448 (9.5%) $23 5.2% 31.4% 9.1% 12.0x 27.3x 1.4x

Mistras Group, Inc. $244 $539 $855 16.7% $84 9.8% 8.2% 9.1% 6.3x 6.2x 0.6x

Median $6,135 $7,776 $8,425 5.0% $528 10.6% 9.7% 9.4% 13.3x 13.9x 1.3x

Mean $8,552 $9,921 $8,350 6.1% $770 10.3% 7.8% 10.8% 12.1x 14.1x 1.5x

Construction Engineering

Quanta Services, Inc. $23,445 $28,162 $16,426 15.9% $2,448 14.9% 26.6% 10.1% 13.8x 11.7x 1.7x

MasTec, Inc. $8,121 $10,520 $10,063 25.8% $1,876 18.6% 25.4% 9.6% 8.9x 5.7x 1.1x

Dycom Industries, Inc. $3,522 $4,242 $3,995 (2.1%) $378 9.5% 9.0% 9.8% 10.2x 11.5x 1.1x

MYR Group Inc. $1,991 $1,920 $3,174 9.5% $216 6.8% 14.0% 6.6% 8.6x 8.9x 0.6x

Argan, Inc. $796 $201 $648 29.9% $88 13.6% 11.8% 9.5% 2.4x 2.2x 0.3x

Median $3,522 $4,242 $3,995 15.9% $378 13.6% 14.0% 9.6% 8.9x 8.9x 1.1x

Mean $7,575 $9,009 $6,861 15.8% $1,001 12.7% 17.3% 9.1% 8.8x 8.0x 1.0x

Aggregate Supplier

Martin Marietta Materials, Inc. $29,982 $36,827 $6,658 19.5% $1,840 27.6% 21.5% 28.5% 16.7x 18.4x 5.8x

Vulcan Materials Company $30,455 $36,017 $7,521 23.6% $1,953 26.0% 22.1% 25.4% 16.3x 19.1x 5.2x

Eagle Materials Inc. $6,331 $7,401 $2,267 13.1% $783 34.5% 12.3% 35.4% 8.3x 9.6x 3.3x

Summit Materials, Inc. $4,604 $6,220 $3,049 3.3% $683 22.4% 0.5% 22.6% 9.1x 9.2x 2.1x

Median $18,156 $21,709 $4,854 16.3% $1,312 26.8% 16.9% 26.9% 12.7x 14.0x 4.3x

Mean $17,843 $21,616 $4,874 14.9% $1,315 27.6% 14.1% 28.0% 12.6x 14.1x 4.1x

Source: Capital IQ. Data as of March 31, 2022.

“LTM” refers to last twelve months. “NTM” refers to next twelve months. Page 8

About Us

MNP Corporate Finance (MNPCF) has a dedicated team of over 100 Recently Closed Deals

M&A and due diligence professionals across Canada. MNPCF

works with clients in virtually all industries as they prepare, plan (National)

and execute transactions.

Our typical transactions range in value between $3 million and

$300 million.

Local and International Reach

MNP is a participating firm within Praxity, a unique global alliance of

independent accounting/advisory firms created to answer global

business needs. As a member of Praxity, we are able to offer access

to corporate finance, accounting and tax advisory services

worldwide. We are also affiliated with Corporate Finance Cross

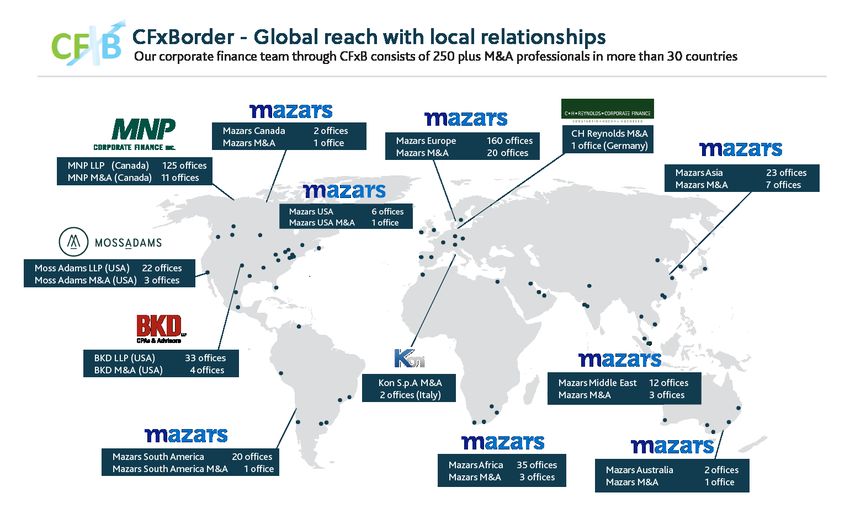

Border, which consists of 250+ M&A professionals in more than 30

countries.

Services

• Divestitures • Due Diligence

• Acquisitions • Transaction Advisory

• Debt Financing Services

Page 9

About Us

Deal Experience Recently Closed Deals

(National)

Since our inception, our team has advised on hundreds of

transactions, in a wide range of industries with diverse enterprise

values. In the past eight years alone we have completed over 200

transactions worth over $3.5 billion (not including due diligence

engagements).

Industry Experience

• Food & Beverage • Transportation

• Retail & Distribution • Construction

• Manufacturing • Software

• Agriculture • Financial Services

• Automotive • Technology

• Materials • Energy

• Health Care • Oilfield Services

• Pharmaceutical • Real Estate

Hands-on Approach

Current M&A transactions require a hands-on approach from start

to finish including the active engagement of senior resources. Our

senior resources are dedicated to our clients and are available as

necessary and appropriate. We keep our clients regularly informed

of the engagement status, issues we are encountering, successes

and overall progress.

Integrated Service Offering

We draw on the vast experience and deep specialist knowledge

network of our partners locally, nationally and internationally as

specialty issues arise, such as pre-transaction tax planning,

transaction structuring, estate planning, valuation, due diligence,

performance improvement and risk management.

Page 10Leadership Team

Transaction Leadership

Brett Franklin Aleem Bandali Mark Regehr Mike Reynolds

President Managing Director Managing Director Managing Director

Winnipeg Vancouver Edmonton Calgary

Brett.Franklin@mnp.ca Aleem.Bandali@mnp.ca Mark.Regehr@mnp.ca Mike.Reynolds@mnp.ca

204.336.6190 778.374.2140 780.969.1404 587.702.5909

Erik St-Hilaire Stephen Shaw Dan Porter Kevin Tremblay

Managing Director Managing Director Managing Director Managing Director

Winnipeg Toronto Toronto Toronto

Erik.St-Hilaire@mnp.ca Stephen.Shaw@mnp.ca Dan.Porter@mnp.ca Kevin.Tremblay@mnp.ca

204.336.6200 416.515.3883 416.515.3877 647.943.4051

Jon Edgett Patrick Khouzam Jonathan Banford Éric Grondin

Managing Director Managing Director Managing Director Managing Director

Waterloo Montreal Chicoutimi Sherbrooke

Jon.Edgett@mnp.ca Patrick.Khouzam@mnp.ca Jonathan.Banford@mnp.ca Éric.Grondin@mnp.ca

519.772.7460 514.228.7874 418.696.3924 819.823.3290

Due Diligence Leadership

Jean-Raymond Lafond Craig Maloney Johnny Earl John Caggianiello

Managing Director Managing Director Managing Director Managing Director

Drummondville Halifax Vancouver Toronto

Jean-Raymond.Lafond@mnp.ca Craig.Maloney@mnp.ca Johnny.Earl@mnp.ca John.Caggianiello@mnp.ca

819.473.7251 902.493.5430 604.637.1504 416.513.4177

MNPCF.ca

Page 11You can also read