Industry Report - Commercial and Industrial Building Construction in Australia Current Performance with 5 Years Outlook

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Commercial and Industrial Building Construction in Australia July 2020

Industry Report –

Commercial and Industrial

Building Construction in

Australia

CurrentPerformance

Current Performancewith

with55

YearsOutlook

Years Outlook

JULY 2020

QUANTUM HOUSE AUSTRALIA

1

www.quantumhouse.com

Commercial and Industrial Building Construction in Australia July 2020

COVID-19 IBISWorld's analysts constantly monitor the industry impacts of current events in real-time – here is an

(Coronavirus) update of how this industry is likely to be impacted as a result of the global COVID-19 pandemic:

Impact Update

• The spread of COVID-19 is anticipated to have a light effect on building construction industries over

the short term. However, there may be some disruption in the supply chain for component parts,

building materials and skilled labour, which could delay the progress of some construction projects. On

most construction sites, workers are able comply with social distancing rules to control the virus.

• Over the longer term, COVID-19 may discourage foreign investment in commercial and industrial

building projects and the anticipated downturn in the general economy may diminish the capacity of

local property developers to invest in new buildings. Lower interest rates would normally be expected to

stimulate demand for some building construction but potential investors are expected to delay planned

projects due to uncertainty in the Australian and global economy. Industry revenue was projected to

decline during 2020-21 in response to the completion of several major developments and COVID-19 is

projected to contribute to a further 15% decline in industry activity as investors delay projects. See

discussion in Outlook chapter.

• Multiplex has voluntarily shut down its United Kingdom worksites in response to the COVID-19

lockdown arrangements introduced by the UK Government. See

https://www.building.co.uk/news/multiplex-closes-construction-sites-with-immediate-

effect/5105135.article - There are no indications that major Australian construction firms are planning to

shut down worksites.

Note: The content in this report is currently being updated to reflect the trends outlined above.

Snapshot Total Revenue Annual Growth Annual Growth

2020 2015-2020 2020-2025

$48.8bn 7.4% -4.8%

Profit Margin Wages as a share of Revenue Number of Businesses

2020 2020 2015-2020

10.2% 8.5% 3.8%

Industry Level Trend Level Trend

Structure

Life Cycle Mature Regulation Level Medium Increasing

Revenue Volatility High Technology Change Medium

Capital Intensity Low Barriers to Entry Low Increasing

Industry Assistance None Steady Industry Globalization Low Increasing

Concentration Level Low Competition Level High Increasing

2

www.quantumhouse.com

Commercial and Industrial Building Construction in Australia July 2020

Key Industry Data

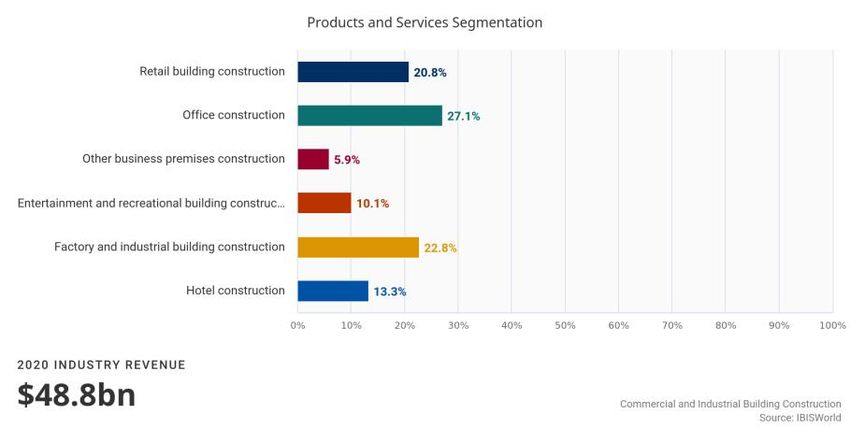

Products &

Services

Segmentation

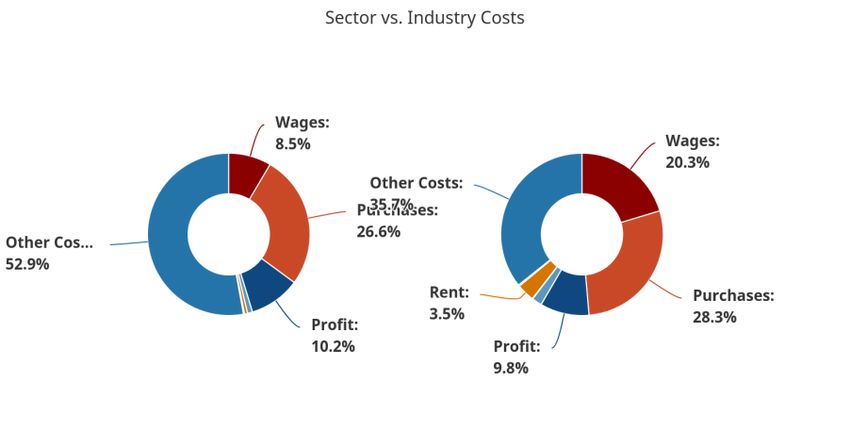

Cost Structure

3

www.quantumhouse.comCommercial and Industrial Building Construction in Australia July 2020

Industry Performance

Performance The Commercial and Industrial Building Construction industry consists of firms that primarily

Summary construct non-residential buildings, such as offices, shopping centres, cinemas, restaurants,

airport terminals, factories and warehouses.

These building projects are mainly funded by private sector property developers and end-users. The

industry has a highly fragmented structure, comprising many small- to medium-scale building firms but

also includes several large-scale firms that are capable of undertaking complex construction projects,

such as high-rise office towers.

The industry has expanded at a strong pace over the past five years, supported by favourable interest

rates and factors driving demand in several building markets. The solid growth in Australia's labour

force has supported investment in office developments while the positive trends in household

consumption and tourism over most of the five-year period have driven investment in shopping centre,

entertainment facility and hotel construction. Demand for industrial building construction has been

supported by strong investment in warehousing and distribution facilities and the current upswing in

factory construction, despite weak trends in the downstream Manufacturing division. Industry revenue is

expected to grow at an annualised 7.4% over the five years through 2019-20, to total $48.8 billion. This

trend includes robust growth by 11.6% in the current year on the back of progress on major building

projects.

The COVID-19 outbreak is anticipated to represent only a minor disruption to industry activity during

2019-20, although the pandemic is forecast to discourage foreign and local investment in commercial

and industrial building projects during 2020-21. The industry's performance is also projected to be

adversely affected over the short term by the imminent completion of major commercial building

projects. Over the five years through 2024-25, industry revenue is forecast to contract at an annualised

4.7%, falling to $38.2 billion. Some firms may benefit from the projected growth of investment in retail

store construction over the next five years, which is likely to be supported by rising household

consumption expenditure and growth in the number of businesses. Investment in new terminal buildings

for the new Western Sydney Airport and major railway developments may provide opportunities for

some of the larger construction firms over the period.

Industry Issues Threat

Growth in the labour force can boost demand for commercial building construction, particularly for

offices and other workplaces. Rapid employment growth usually coincides with strong demand for

existing office stock. Total labour force numbers are expected to increase at a slower pace during 2019-

20, which may constrain demand for new office construction. This trend may threaten the short-term

pace of industry expansion.

Opportunity

The number of businesses in Australia corresponds with demand for commercial and industrial

buildings. Demand for commercial property usually grows as business numbers increase and the

expansion over the past five years has provided an opportunity for industry expansion. However,

businesses numbers are anticipated to decline during 2019-20 in response to the outbreak of COVID-

19, which may dampen demand for new offices, retail buildings and warehousing facilities.

Industry Outlook

4

www.quantumhouse.comCommercial and Industrial Building Construction in Australia July 2020

Outlook The performance of the Commercial and Industrial Building

Construction industry is forecast to contract over the next five

years, in response to reduced investment following the

completion of several large-scale developments in major

capital cities.

Downward pressure on non-residential building

investment and the industry's performance

corresponds with the slower growth in demand

from downstream office and other commercial

property operators. Furthermore, a one-off

slump in investment in the start-up of new

building projects in response to the economic

uncertainty caused by the COVID-19

pandemic is projected to constrain demand for

industry services. The pandemic is forecast to

dampen industry performance over the next

five years due to the anticipated decline of

foreign investment and the diminished capacity

of Australian property developers to invest in

new building projects. However, the

construction of transport terminals for airports,

railways and bus lines represents a significant

opportunity for industry operators to expand over the next five years.

Overall, industry revenue is forecast to decline at an annualised 4.7% over the five years through

2024-25, falling to $38.2 billion. This fall includes a projected sharp contraction in revenue during

2020-21 associated with the completion of several major building developments, along with the one-off

disruption to investment stemming from the outbreak of the COVID-19, as investors delay the start-up

of new projects.. The anticipated downturn in the general economy due to COVID-19 will likely

significantly diminish the capacity of local property developers to invest in new commercial and

industrial buildings. Similarly, foreign investors are likely to be discouraged from investing in the

Australian property market. However, some of this investment is forecast to return over the

subsequent years as the Australian and global economies recover.

FALLING PROFITABILITY AND EMPLOYMENT

Industry profit margins are forecast to narrow sharply over the

next five years as contractors and property developers grapple

with the difficult trading conditions associated with the COVID-

19 outbreak.

However, some of the smaller-scale contractors may have access to Commonwealth Government

stimulus packages aimed at supporting ongoing employment and apprenticeships. Wage costs are

projected to rise as a share of industry revenue over the next five years, principally reflecting the

magnitude of the decline in overall revenue relative to falls in total employment. A forecast decline in

enterprise numbers over the next five years reflects weaker investment trends in most building

segments, consequently discouraging new entrants to the industry and forcing some smaller

contractors to exit the industry.

DECLINING BUILDING MARKETS

5

www.quantumhouse.comCommercial and Industrial Building Construction in Australia July 2020

The value of office construction is projected to decline sharply

over the next five years irrespective of the The value of office

construction is projected to decline sharply over the next five

years irrespective of the influence of COVID-19 on building

investment.

This decline corresponds with the completion of several large-scale developments over 2019 and

2020, including the Australian Unity headquarters and the Collins Arch development in Melbourne and

the Quay Quarter Tower in Sydney. Plans to remove ageing office stock from the existing rental

market are anticipated to generate some demand for new office construction over the next five years,

although these plans may be offset by increasing demand for refurbishing existing office buildings

rather than investment in new building stock.

The value of industrial building construction is forecast to contract over the next five years due to

declines in most building segments, although some industry operators may continue to benefit from

local government rezoning and the development of industrial estates close to new transport links.

Factory construction is projected to decrease significantly over the next five years, coming off its

current cyclical high and reflecting the trend of local manufacturing firms continuing to offshore

production capacity. Similarly, investment in new warehouse and distribution facilities is anticipated to

fall sharply over the next five years, despite the solid growth in merchandise trade and reflecting the

previous accelerated growth in the construction of warehousing and distribution facilities.

GROWTH BUILDING MARKETS

Interest rates are forecast to rise slightly over the next five

years from an historically low level in 2020-21 but is expected

to remain low by historical standards.

Household discretionary income is projected to grow over the period, driving increases in both retail

sales and company profitability. These trends, alongside moderate growth in commercial occupancy

rates, are forecast to encourage investment in redeveloping and upgrading existing shopping centres.

Investment in retail store construction is anticipated to increase due to new shopping centre

developments in the outer regions of major metropolitan areas, driven by the population growing and

moving into new suburban areas. However, the continued loss of bricks-and-mortar retail sales to

online shopping will likely limit investment in retail construction over the period.

Industry operators will likely benefit from strong investment in transport building construction, including

a surge in construction activity over the two years through 2023-24. This trend coincides with the peak

construction of parking facilities, and passenger and freight terminals on the Western Sydney Airport

project. The planned expansion of passenger terminals at Melbourne Airport and the construction of

railway stations, bus depots and car parks is also anticipated to benefit the industry. This activity stems

from the current expansion of metropolitan rail tram and bus networks in most major cities.

Demand for industry services in the entertainment building and recreation building construction

segments is forecast to contract, as major facilities currently under construction reach completion over

the next five years. Current construction is focused on large-scale casino developments in Adelaide,

Brisbane and Sydney, and the New Sydney Football Stadium at Moore Park. Overall, industry revenue

derived from entertainment building and recreation building construction is forecast to remain solid

over the next five years. Conversely, the completion of major hotel developments currently underway

in Perth, Brisbane and Sydney will likely drive a significant decline in the hotel construction segment

over the period.

6

www.quantumhouse.comCommercial and Industrial Building Construction in Australia July 2020

Performance Outlook Data

Revenue IVA Establishments Enterprises Employment Exports Imports Wages Domestic

Year ($m) ($m) (Units) (Units) (Units) ($m) ($m) ($m) Demand ($m)

2019-20 48,755 9,631 10,760 10,500 58,900 N/A N/A 4,148 N/A

2020-21 38,857 7,030 9,550 9,317 48,946 N/A N/A 3,467 N/A

2021-22 37,517 6,708 9,383 9,154 47,662 N/A N/A 3,394 N/A

2022-23 35,815 6,303 9,165 8,941 45,998 N/A N/A 3,292 N/A

2023-24 36,263 6,408 9,222 8,997 46,430 N/A N/A 3,340 N/A

Child Care Services

2024-25 38,230 in Australia

6,870 9,465 9,235 48,250 N/A N/A July

3,487 2020 N/A

2025-26 39,459 7,164 9,615 9,380 49,386 N/A N/A 3,587 N/A

Disclaimer: This industry report has been sourced from IBISWorld Australia. Our firm is not responsible for the correctness of the report.

7

www.quantumhouse.comYou can also read