INSIDE DEBT - Thomson Reuters

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

INSIDE DEBT

WEDNESDAY, NOVEMBER 10, 2021

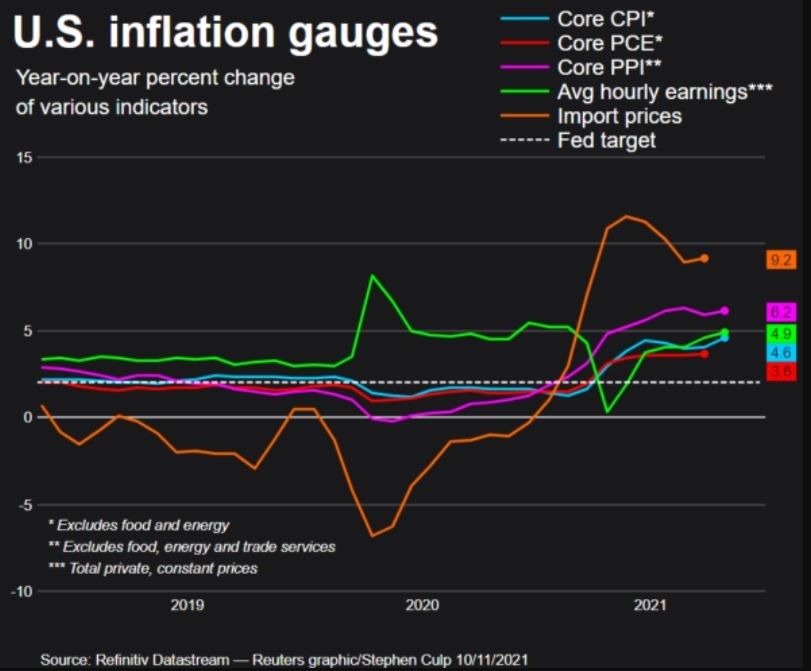

U.S. consumer prices post largest annual rise since 1990

TOP NEWS

Surging gasoline, food prices fan U.S. inflation; labor market tightening

U.S. consumer prices accelerated in October as Americans paid more for gasoline and food, leading to the biggest

annual gain in 31 years, more signs that inflation could stay uncomfortably high well into 2022 amid snarled global

supply chains. The CPI jumped 0.9% last month after climbing 0.4% in September, the Labor Department said. That

hoisted the annual CPI increase to 6.2%, the biggest year-on-year rise since November 1990. Core CPI gained 0.6%

last month after climbing 0.2% in September. It jumped 4.6% on a year-on-year basis, the largest increase since August

1991. Inflation pressures are also brewing in the labor market, where an acute shortage of workers is driving wages

higher. The Labor Department said initial claims for state unemployment benefits fell 4,000 to a seasonally adjusted

267,000 for the week ended Nov. 6. That was the lowest level since the middle of March in 2020. Separately, the

Commerce Department said that wholesale inventories increased 1.4%, instead of 1.1% as estimated last month.

Wholesale inventories jumped 13.1% in September from a year earlier.

China's factory inflation hits 26-year high as power crunch bites

China's factory gate inflation hit a 26-year high in October as coal prices soared amid a power crunch in the country's

industrial heartland, further squeezing profit margins for producers and heightening stagflation concerns. The PPI

climbed 13.5% from a year earlier, faster than the 10.7% rise in September, the National Bureau of Statistics said in a

statement. It matched a pace not seen since July 1995. The PPI inched up 2.5% on a monthly basis, compared with the

1.2% uptick in September. Consumer price rises also quickened, although at a slower pace than factory gate prices. CPI

rose 1.5% in October year-on-year, compared with September's 0.7% rise. Core inflation stood at 1.3% rise in October

from the previous year. Meanwhile, data released by the People's Bank of China showed banks extended new loans of

826.2 billion yuan in October, down sharply from 1.66 trillion in September. The new loans were higher than 689.8 billion

yuan a year earlier.

Fed's Daly: Inflation will moderate, uncertainty requires us to wait

San Francisco Fed President Mary Daly said she expects high inflation to moderate once COVID-19 recedes, and

repeated that it would be "quite premature" to raise rates now or even to speed up the Fed's bond-buying taper. Any

interest rate hikes would be expected to start after the bond-buying winddown is complete, with the slightly majority of

Fed policymakers as of September believing that they should not begin before 2023. That timeframe is drawing criticism

from some quarters for potentially putting the U.S. central bank behind the curve on fighting inflation. Commenting on a

government report, Daly said that the data shows high inflation, but believed it is being driven by supply-chain

bottlenecks and high consumer demand for goods that will pass as COVID-19 fades. Fed monetary policy cannot affect

supply-side issues, Daly said, and if it tightens policy now that could actually raise the cost of investments and actually

slow progress on addressing bottleneck issues.

1

Government advisers cut German growth forecasts, see more inflation

Economic advisers to the German government cut their growth forecast for next year, creating a policy headache for the

three parties that are in talks on forming Germany's new government. The advisers cut their 2021 growth outlook to

2.7%, down from the 3.1% they expected in March, but raised their outlook for next year by six percentage points to

4.6%. The darkening mood blamed by the advisers on supply-chain bottle necks and inflationary pressure afflicting the

global economy is likely to create additional problems for the would-be coalition parties in carrying out promises of

transformational investments into greening the economy and a return to strict debt limits from 2023 without raising taxes.

The advisers also said in their report that they expected the current inflationary spurt to continue well into 2022. Inflation,

driven by high input prices, would come in at 3.1% this year, and at 2.6% in 2022.

Europe's pandemic productivity growth surge may wane: ECB study

Euro zone labour productivity growth surged at the onset of the pandemic as firms rushed to adapt digital technologies

but much of the gains are at risk of erosion, an ECB study showed. Europe's productivity growth has been anaemic for

years, keeping a lid on overall economic expansion and some economists hoped that a rapid adaption of digital

solutions could be the COVID-19 pandemic's silver lining. Data so far suggest that this is happening as labour

productivity is now more than 2% higher than in the final quarter of 2019, even if it has declined somewhat since the

onset of the recovery, the ECB said in an Economic Bulletin article. As containment measure forced businesses to halt

many face-to-face interactions, usually low productivity tasks, activity was redistributed, accounting for 30% to 40% of

the labour productivity growth, the ECB said.

DEEP DIVE

ANALYSIS-Flexible inflation targets a recipe for bond market turbulence

For markets trying to navigate the pathway for stickier-than-expected inflation, a move to asymmetric price targets at the

world's two biggest central banks may be a recipe for wild and increasingly frequent bond price swings.

COLUMN-A winter of market confusion: Mike Dolan

If any investor tells you they are sure of what happens next in macro markets, they are likely to be fibbing. Such is the

confusion in policy and investment circles right now over the course of inflation, output, jobs, financial prices and central

bank policy that the next 3-6 months is likely impossible to predict with any conviction.

PROMOTION

LiveChats on the Reuters Global Markets Forum (Nov 11) - To view all scheduled chats and join the conversation,

click here

Viraj Patel, global macro strategist at Vanda Research, speaks on the global outlook in Q4, expectations for central

bank policy and the impact on asset prices (1600 GMT/1100 ET).

2

CHART OF THE DAY

MARKETS TODAY

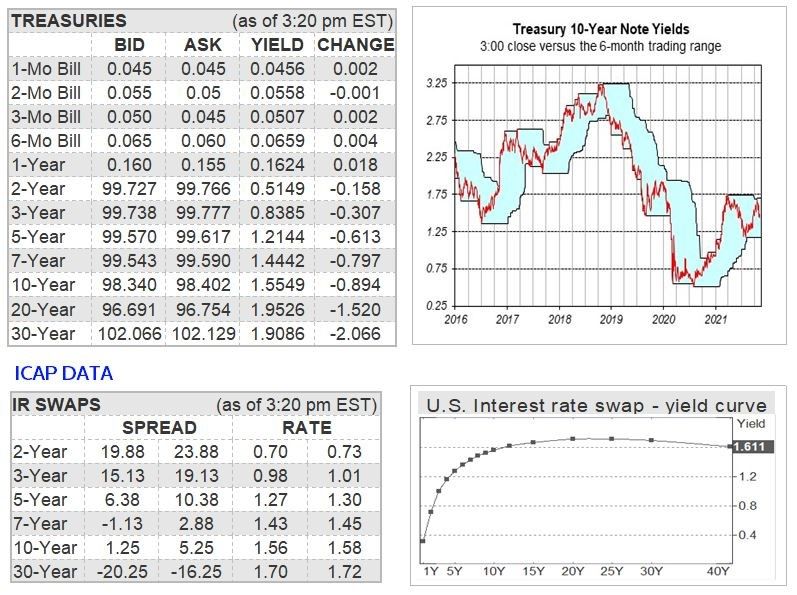

TREASURIES: Treasury debt yields shot higher as the market was battered by the biggest annual gain in U.S.

consumer prices in 31 years and a weak 30-year bond auction. Inflation expectations soared, with the five-year

breakeven inflation rate reaching a record-high 3.113% and the 10-year breakeven rate rising to 2.72%, the highest

since May 2006. The Treasury Department sold $25 bln in 30-year bonds at a high yield of 1.940%. The bid-to-cover

ratio was 2.20. Benchmark 10-year notes dropped 1-2/32, yielding 1.56%. 2-year notes dipped 7/32 to yield 0.51%. 5-

year notes slipped 24/32, yielding 1.22%.

FOREX: The dollar index jumped sharply, hitting its highest level since July 2020, after U.S. consumer prices surged to

their highest rate since 1990, fueling speculation that the Federal Reserve may raise interest rates sooner than

expected. The dollar index climbed 0.99% to 94.884, after reaching a high of 94.876, its highest level in more than 15

months. The euro was last down 0.97% at $1.1479, after earlier touching $1.1480, its lowest level since July 21, 2020.

The British pound dipped 1.10% to $1.3405. Against the Japanese yen, the dollar rose 0.95% to 113.92 yen.

CORPORATES: Corporate bond spreads widened after U.S. consumer inflation surged to its highest since 1990, raising

concerns that the Fed will tighten monetary policy sooner than expected. The CDX-IG.37 index widened by 1 bps to 51

bps.

STOCKS: Wall Street ended the session in negative territory as investor risk appetitive was curbed by surging consumer

prices, which stoked worries of a protracted wave of hot inflation. Electric vehicle maker Rivian Automotive surged

29.1% as it made its splash as a publicly traded company in an offering expected to raise nearly $107 billion. Apple fell

1.9%. Microsoft was down 1.5%. The Dow fell 241.69 points, or 0.67%, to 36,078.29, the S&P 500 lost 38.54 points, or

0.82%, to 4,646.71 and the Nasdaq dropped 264.41 points, or 1.66%, to 15,622.13.

C&E: Oil prices slumped, hit by a surge in the dollar after U.S. President Joe Biden said his administration was looking

for ways to reduce energy costs amid a broader surge in inflation. U.S. crude inventories rose by 1 million barrels in the

most recent week, short of estimates for a 2.1 million build in crude stocks. U.S. crude slumped 3.42% to $81.27 a

barrel. Brent fell 2.56% to $82.61 a barrel. Gold added 1.10% to $1851.63 an ounce.

3NEX DATA

LATAM NEWS

Brazil Oct inflation highest in almost 20 years as fuel costs rise

Brazilian consumer prices jumped in October by the most in nearly two decades, driven in part by rising fuel costs, which

pushed annual inflation to 10.67%. Consumer prices measured by the benchmark IPCA index rose by 1.25% last month,

government statistics agency IBGE said, above the median economist forecast of 1.05%. That was the fastest inflation

rate for the month since October 2002, when consumer prices rose 1.31%. Inflation in Brazil this year has been driven

partly by a drought that has sapped hydroelectric power generation and pushed up energy bills as well as a weakening

real currency. In an attempt to get inflation back under control, the central bank has increased interest rates aggressively

this year to 7.75%.

LATAM MARKETS

4EYE ON ASIA

POLL- India October inflation likely stable, gives RBI room on rates

India's retail inflation likely hovered near a six-month low in October as higher food and fuel prices were offset by an

overall favourable comparison with prices one year ago, leaving the central bank room for now to leave interest rates

steady. The median forecast from Reuters poll of 43 economists predicted inflation edged down to 4.32% from 4.35% in

September. If realised, it would mark the fourth consecutive month inflation has been within the Reserve Bank of India's

(RBI) tolerance band of 2%-6%. Poll respondents again highlighted inflation was subdued mainly because of

comparisons with a stronger period one year ago, and the current mild trend is expected to continue only for a few more

months.

POLL- Malaysia's GDP likely contracted in Q3 on renewed COVID-19 curbs

Malaysia's battered economy likely slipped back into contraction in the third quarter as coronavirus-induced restrictions

brought economic activity to a near-standstill, a Reuters poll found. After bouncing back from its worst recession in more

than two decades in the second quarter, the economy shrank 1.3% in July-September from a year earlier, according to

the median forecast of 20 economists in the poll. Renewed COVID-19 lockdowns dampened a nascent economic

recovery, pushing Malaysia's central bank to slash its 2021 growth forecast to 3.0%-4.0% from 6.0%-7.5% previously.

The government expects Malaysia's economy to grow 5.5%-6.5% next year, driven by normalisation of economic

activity, resumption of projects, higher commodity prices and strong external demand.

ASIA ECON WATCH (For Nov 11)

Japan Corp Goods Price MM for Oct: Expected 0.4%; Prior 0.3%

Japan Corp Goods Price YY for Oct: Expected 7.0%; Prior 6.3%

Australia Employment for Oct: Expected 50.0k; Prior -138.0k

Australia Participation Rate for Oct: Expected 64.9%; Prior 64.5%

Australia Unemployment Rate for Oct: Expected 4.8%; Prior 4.6%

5For additional information and to find out more about how NEX's range of market For additional information and to find out more about how ICAP's range of

information can help your business, contact market information, commentary and research solutions can help your

enquiries@nexdata.com or contact your local NEX Data office. EMEA +44 20 7818 9911 | business, contact icapinformationservices@icap.com. Americas: +1 212 341

US + 1 212 704 5470 | Singapore +65 6831 0991 | Hong Kong 9789

+85 2 2878 6068

ICAP plc, its subsidiaries (“ICAP”) and third parties own portions of the

This Information is not, and should not be construed as, an offer or solicitation to sell or copyright to information, data and content (“Information”) and to certain

buy any product, investment, security or any other financial instrument or to participate in service marks and logos herein. The Information is for informational

any particular trading strategy. The Information is not to be relied upon and is not purposes only; is not intended as investment, financial or accounting advice;

warranted, either expressly or by implication, as to completeness, timeliness, accuracy, and should not be construed as an offer, bid or solicitation in relation to any

merchantability or fitness for any particular purpose. All representations and warranties financial instrument. All information is provided "as is" without any

are expressly disclaimed. Access to the Information by anyone other than the intended representations or warranties of any kind. ICAP and third parties shall not

recipient is unauthorised and any disclosure, copying or redistribution is prohibited without be responsible or liable for any damages whatsoever arising out of or

NEX’s prior written approval. relating in any way to the Information herein.

In no circumstances will NEX be liable for any indirect or direct loss, or consequential loss

or damages including without limitation, loss of business or profits arising from the use of,

any inability to use, or any inaccuracy in the Information.

NEX and the NEX logo are trademarks of the NEX group. For further information, please

see www.nex.com.

©NEX Group plc 2019

The Financial and Risk business of Thomson Reuters is now Refinitiv.

INSIDE DEBT is produced by Reuters in partnership with NEX and ICAP.

Edited and compiled by Sravanthi Bhamidi in Bengaluru.

For questions or comments about this report, email us at:

For Market Snapshot, NEX provides OTC capital markets data, Refinitiv provides

exchange data. All economic indicators in the Econ Watch and Asia Events sections

are mentioned in the country's local currency, unless mentioned otherwise.

Visit the Thomson Reuters Fixed Income Community Site at:

If you like to receive this in your mailbox, please subscribe at:

6You can also read