INTRODUCTION TO THE AA - Investor presentation H1 17 Interims - AA plc

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

INTRODUCTION TO THE AA Investor presentation H1 17 Interims

CONTENTS, IR CONTACTS AND DEFINITIONS

CONTENTS IR CONTACTS DEFININTIONS THAT APPLY THROUGHOUT

Jill Sherratt • Trading Revenue: Revenue excluding

Head of Investor Relations discontinued operations, business held for

Fundamentals 2 – 16

Email: jill.sherratt@theaa.com sale and exceptional revenue item

Telephone: +44 (0) 20 7395 7301 • Trading EBITDA (earnings before interest,

H1 17 results 17 – 45 Mobile: +44 (0) 7791 137738

tax, depreciation and amortisation): excludes

exceptional items, items not allocated to a

segment and discontinued operations

Transformation James Curran • Cash conversion: net cash flow from

Investor Relations Manager and Analyst continuing operating activities before tax and

(as at 20.4.15) 47 – 56

Email: James.curran@theaa.com exceptional items divided by Trading

EBITDA

Telephone: +44 (0) 20 7395 4443

FY16 results • Adjusted basic continuing EPS: Earnings per

Mobile: +44 (0) 77387 71835

share excluding discontinued operations

(in summary) 58 - 63 adjusts for a number of one-offs of which the

Lisa Shailer largest are exceptional items, items not

Investor Relations Assistant allocated to a segment, the amortisation of

debt issue fees, penalties on early

Email: lisa.shailer@theaa.com

repayment of debt and double-running

Telephone: +44 (0) 20 7395 7442 interest costs on Class B/B2 notes

Mobile: +44 (0) 7950 868371 • Personal Members and Business

Customers: measured as the number at the

www.theaaplc.com period end

1

FUNDAMENTALS

PROVIDING SERVICES TO AA MEMBERS FOR MORE THAN 110 YEARS

Brought under

common

Founded by Patrols on 35% share Launched Patrols issued ownership with DriveTech and

motoring bicycles and of 2m cars on the Roadwatch and with diagnostics Saga in the Auto Windshields IPO

enthusiasts uniforms road Relay equipment Acromas Group acquired 26 June

1905 1907 1909 1912 1939 1949 1973 1992 1999 2003 2004 2007 2009 2010 2014

1st AA insurance Launched New fleet Launched AA members Acquired by BSM acquired,

policy AA Routes and to enable four AA Driving voted to private equity launch Home

AA Stars wheel patrols School demutualize the groups CVC and Services

AA and join Permira Fund

Centrica Group

3

ROADSIDE ASSISTANCE AT THE CORE

Segment

Roadside Assistance Insurance Services Driving Services Ireland⁴

17% 4% 3%

FY16 Trading

EBITDA %1

76%

£361m3 £78m £19m £13m

3.7m personal Members Leading insurance broker Provides driver awareness Leading branded

and 10.2m B2B customers training, fleet management breakdown provider

Offers Motor, Home,

and driver training and leading insurance

c3,000 dedicated patrols; Travel and other specialist

broker in Ireland

c10,000 breakdowns insurance Largest driving school in

Highlights

per day the UK² - AA and BSM Insurance lead with

Cross-sell to existing

brands breakdown usually ad

No 1 with market share of customers

additional benefit

c40% 11% of the highly

Also includes Home

fragmented market

81% personal Member Services and Financial

retention rate Services

1. Segment Trading EBITDA has been expressed as a % of Group Trading EBITDA excluding Head Office Costs

2. By total UK driving pupils.

3. Excluding Glass business disposed of

4. Ireland business sold on 11 August 2016 for EUR 156.6m 4

THE LEADERSHIP TEAM

Bob Mackenzie Martin Clarke

Executive Chairman Chief Financial Officer

Previously Chairman and CEO of National Car Parks Previously Partner and Global Head of Consumer for

and its subsidiary Green Flag Permira

Prior to that CEO of Sea Containers Prior roles at Cinven, Silverfleet and

and Chairman of PHS Group board member of New Look and Gala Coral

Mike Lloyd Janet Connor

Commercial Director Restructuring and Insurance Director

Previously Partner at Oliver Wyman focused on Previously Managing Director at More Than; MD at

Consumer Service businesses in FS, Energy, Home, Ageas-owned over-50s broker RIAS from 2006 to 2011

TV and Telecoms Accountable for broking operating as CEO of AAISL

Responsible for Roadside Assistance and Insurance

Services, marketing and digital functions

Oliver Kunc Kirsty Ross

Operations Director Membership Services Director

Previously Managing Director of Central Heating Previously Strategy and Innovations Director;

Installations at British Gas; prior roles at Barclays, BA Principal at Oliver Wyman

and LEK consulting Responsible for Motoring Services, Media and Driving

Responsible for operations including patrols, School businesses, connected car strategy and

deployment, call centres and technical development Group strategy

5

THE INVESTMENT CASE

Strong fundamentals Strong, stable margins and cash conversion

High barriers to entry, scale cost advantage

Trusted brand The UK’s most trusted commercial brand1

Over 50% of households hold an AA product

Market leadership 3.7m personal Members, 10.2m B2B customers

No 2 motor insurance broker, No 1 driving school

Retention and loyalty High Member retention, long-term B2B contracts

Significant revenues from repeat business

Operational excellence 3.4m breakdowns attended pa

Sophisticated deployment IP and services

Options for growth Trusted brand lends to relevant extensions

20m marketing contacts, strong cross-sell ability

1. Y&R Brand Asset Valuator Survey (2014).

6

RELATIVE RESILIENCE OF MEMBERSHIP SINCE 1975

Broad based under

investment; eg in systems, AA Members (m) AA Membership vs GDP Growth UK GDP growth (%)

brand and capabilities

and legacy of short-term 5.0 20%

decision making

Premium position not

4.0 15%

underpinned by continuous Membership run-up and

investment in proposition reduction following

and no investment in brand demutalisation

marketing for many years 3.0 10%

US savings and

IT platform, except patrol loan crisis Financial

deployment, dated and Oil Crisis

2.0 crisis 5%

constraining growth; limited

and inflexible CRM systems

1.0 0%

Individual business unit

optimisation restricts

commercial opportunity

0.0 -5%

1975 1980 1985 1990 1995 2000 2005 2010 2015

7

FINANCIAL RESILIENCE THROUGH THE ECONOMIC CYCLE

£1,200 Revenue and Trading EBITDA

979 971 974 967 963

£1,000 931 943

893

794 808

£800 755

£600

423 429 415

369 371 395

£400 366

334

273 292

219

£200

£0

Year to Year to 13 months FY09 FY10 FY11 FY12 FY13 FY14 FY15 FY16

Dec 2005 Dec 2006 to Jan 2008

Trading EBITDA Revenue

Note: 2005, 2006, 2008 and 2009 unaudited; FY15 and FY16 Revenue and Trading EBTIDA excludes the Glass business disposed of

8

EXCEPTIONAL CASH GENERATION

Cash flow generation (£m)

102% 97% 101%

94%

Trading EBITDA

£395m £423m £430m £415m

Cash Conversion

Net cash flow from operating FY13 FY14 FY15 FY16

activities before tax and

exceptional items £371m £433m £431m £416m

Favourable working capital dynamics as a function of upfront payments by customers

Underlying maintenance capital expenditure of c£40m pa

9A HIGHLY TRUSTED COMMERCIAL BRAND

Highest test score for a major

“Which?” total test score 2015 provider from ‘Which?’ every

Major providers year since 2007

74% Widely recognised and trusted brand

High level of customer satisfaction

66% 50% of households hold an AA product

64% September 2015: AA ‘Recommended

provider’ in “Which?” survey for both

consumer and manufacturer cover for

10th consecutive year

10SCALE, LEADING MARKET POSITION AND BARRIERS TO ENTRY

Large and resilient roadside market Scale and barriers to entry

Relatively stable market Economies of scale: c3,000; 10,000 breakdown per

day; c3.4m breakdowns pa

High recurring revenue

New entry barriers from investment required in

systems – eg deployment

B2B relationships: 10.2m B2B customers; partner of

choice for major OEMs

Consumer market share B2B market share Breakdowns attended

Others 3.4m

19%

40% B2B 2.5m

GF 67% 63% 0.7m1

50% Consumer

14%

RAC Motor Fleets AVA

27% manufacturers

Source: Industry sources;

Note 1: The number of breakdowns for GreenFlag is last year’s number

11HIGH MEMBER RETENTION AND LOYALTY

Large personal Membership base Strong loyalty

3.7m personal Members

Membership tenure

Rate of decline slowing

• FY16: -2.6%

• FY15: -4.5%

1,500,000

3.3m paid personal Members 800,000

• H117: -0.6%

> 10 years >20 years

Stable over medium/longer term

Average tenure of c12 years

Proprietary long-standing database of c21m

individuals Rising retention rate (81% for FY16)

Competitive advantage for cross-selling

Sophisticated customer rating and pricing

capability based on proprietary information

12LONG TERM B2B CONTRACTS

Selected B2B client base

Recent contract wins:

Added Volkswagen Group, Porsche,

Value Lex Autolease

Accounts

Recent renewals: Toyota,

Northgate, Subaru, Isuzu,

Fleet &

leasing MG, Lexus (Bentley, Ford,

Honda and Jaguar Land

Rover in FY15)

Extended contracts: BT and

OEMs

Vauxhall (Lloyds Banking

Group and TSB in FY15)

Tenure Other developments: VW

with AA 0–5 5-10 >10

emissions programme and

JLR mobile servicing pilot

13OPERATIONAL EXCELLENCE

Technical assets and expertise

High levels of customer service

Unique deployment IP

Modern multi-vehicle service technology

80% of breakdowns repaired at roadside

Skilled and experienced colleagues

AA “moment of truth” survey (%)

Average of 11 years tenure with the AA

22%

26% 31%

Call handling 80% in 20 seconds 57% 66%

53%

Repair rate 82%

App usageSTRONG BRAND IN INSURANCE

Insurance Services

Core insurance revenue breakdown Brand consideration³ for switching Motor Insurance

Other

6%

Home

38% Motor

56%

No 1 motor insurance broker in the UK private car

Jan-12 Jun-12 Nov-12 Apr-13 Sep-13 Feb-14 Jul-14 Dec-14 May-15 Oct-15

insurance market

Admiral AA Direct Line

No 2 private home insurance broker in the UK Churchill Hastings Direct Axa

Tesco Saga

Source: GfK FRS Study March 2016

15TRANSFORMATION STRATEGY

THE CHALLENGES

Core business performance flat

Several years of under-investment under previous ownership

THE STRATEGY

Three years of investment and consolidation to position AA for renewed growth

Refinancing to free up additional cashflow and facilitate dividends

Strengthening the foundations and revolutionising customer experience

• Investment in brand marketing - £10m pa additional marketing spend

• Investment in IT systems and digital capability - £128m over 3 years

• Restructuring and cost initiatives – Savings of £40m off FY15 cost base in FY19; cost of £45m over 3 years

• Investment in Membership growth and price

• Developing new business models – Financial Services and Insurance Underwriter

• New business initiatives – building on the strength of the brand and opportunities in the wider market

Transformation creates the UK’s pre-eminent Membership services organisation

16H117 INTERIM RESULTS 28 SEPTEMBER 2016

GOOD PROGRESS TO DATE IN YEAR 2 OF THE TRANSFORMATION

Results in line with expectations

TRANSFORMATION GAINING MOMENTUM

Transformation firmly on track

Growth in paid personal Members since April

Ireland sold; £106m for debt pay down Roadside retention up to 81%

App usage increased to 14% of personal

Recommend interim dividend of 3.6p per share breakdowns

Productivity improved

Cost savings on target

IT investment on plan

Transformation capex – c. £10m saving

Normalised capex levels in sight

Transforming the AA into the UK’s pre-eminent Membership services organisation

18FINANCIAL HEADLINES Trading Revenue¹ up 2.2% at £467m despite IPT increase • Roadside Trading revenue up 3.1% to £370m due to improved mix Trading EBITDA¹ flat at £192m • Roadside Trading EBITDA up 4.1% to £179m Trading EBITDA margin¹ 41.1% (H116: 42.0%) Adjusted EPS 10.3p (H116: 10.1p) Cash conversion 99% (H116: 114%); Net debt of £2,677m³ (6.7x Trading EBITDA²) post Ireland disposal in August Interim dividend of 3.6p per share declared In line with market expectations ¹ Excluding the Glass and Ireland businesses and exceptional revenue item ² Trading EBITDA for the last 12 months 19 ³ Net debt at 31 July 2016 plus the net proceeds from the sale of Ireland

P&L

£m H117 H116 YoY Items not allocated to segment reflect

Trading Revenue 467 457 +2% pension and share based payments

impact

Trading EBITDA 192 192 - Exceptional items comprise mainly

Items not allocated to a segment (10) (9) +11% restructuring activities and provision for

potential refund of customers with

Depreciation & amortisation (28) (25) +12%

duplicate cover

Exceptional items (22) (26) -15%

Operating profit 132 132 - Decline in net finance cost reflects

reduced interest on external borrowings

Net finance cost (84) (201) -58%

and the absence of one-off costs from the

Profit/(loss) before tax 48 (69) +170% prior year refinancing

Tax (expense)/credit (10) 13 +177%

Tax expense reflects current tax charge of

Profit/(loss) for the period from continuing 38 (56) +168%

operations £10m, in line with current statutory rate

Basic EPS – continuing operations (p/share) 6.2 (9.6) +165%

Adjusted basic EPS of 10.3p reflects the

Adj Basic EPS –continuing operations (p/share) 10.3 10.1 +2% capital structure in place since July 15

20ROADSIDE ASSISTANCE

Trading Revenue¹ up 3.1% to £370m H117 H116 YoY FY16 H1 on

FY

• Retention 81% (H116: 80%)

Personal Members (‘000s) 3,599 3,726 -3% 3,673 -2%

• Paid personal Members -0.6% YoY;

Average income per Member (£) 145 138 +5% 141 +3%

-0.3% on FY16

Personal paid² Members (‘000s) 3,321 3,340 -1% 3,331 flat

• Average income per personal paid

Member +1.9% to £157 (net of 3.5% Average income per paid² Member (£) 157 154 +2% 156 +1%

uplift in IPT)

Business customers (‘000s) 10,179 9,981 +2% 10,216 flat

• Ancillary revenue up 14%

Average income per business customer (£) 19 18 +6% 18 +6%

Trading EBITDA¹ up 4.1% to £179m

Breakdowns attended (‘000s)³ 1,759 1,662 +6% 3,459 n/a

• Growth in income per personal Member

and B2B revenue; lower H1 advertising

spend (£5m vs £7.5m in H116)

• Partially offset by increased workload

from higher level of breakdowns attended

¹ Excluding items held for sale and exceptional revenue item

² Paid Members: Personal Members excluding free Memberships

³ Relevant period basis 21INSURANCE SERVICES

Trading Revenue flat at £64m - lower core (000s) H117 H116 YoY FY16 H1 on FY

insurance offset by increased FS Total insurance 1,962 2,131 -8% 2,074 -5%

policies

Trading EBITDA down £2m to £35m – Motor policies 572 618 -7% 592 -3%

managed decline of total insurance policies

Home insurance 891 913 -2% 899 -1%

• Motor policies down - lower renewal volumes in policies

high rate increase market environment Average income per 67 63 +6% 63 +6%

• Decline in Home Services policies as we cease policy (£)

free policies Financial Services 82 na na 33 +148%

Products

Motor responding positively in last two months

• Successful retention initiatives; direct sales initiatives

• Additional motor policies through in-house

Underwriter

Financial Services

• Performance to plan: matched book of £160m

assets, £160m liabilities

• Revenue up £3m due to marketing and product

development services provided to BoI

22IN-HOUSE UNDERWRITER

DRIVING SERVICES

Underwriter H117 H116 YoY FY16 H1 on FY

• Progressing well Policies 25 na na na na

underwritten

• Motor launched 30 January – 54k policies to date (‘000s)

• Home insurance underwriting launched in August

Driving Services

H117 H116 YoY FY16 H1 on FY

• Trading Revenue down 3% but EBITDA flat at £9m

Driving 2,516 2,602 -3% 2,574 -2%

– Fewer driving school franchisees instructors

reflecting market conditions

– DriveTech police speed awareness

courses stable

– Cost savings support EBITDA

– Short term initiatives to improve driving school

performance

23STRONG OPERATIONAL CASHFLOW

£m H117 H116

Net cash flows before tax and exceptional items¹ 190 218 Capex

Tax, exceptional items and discontinued operations (6) (14)

Net operating cash flows 184 204

Transformation capex (20) (21)

Underlying IT capex (8) (10)

Non-IT capex (7) (9)

Capex accruals (2) (1)

FY 15 FY 16 FY 17e FY 18e FY 19e

Capital repayment of Finance Lease net of disposal

(14) (6)

proceeds Transformation capex

Other (2) (3) Maintenance capex

Net cash flows before refinancing, purchase of own 131 154 Note: Capex includes finance lease capital spend net of vehicle proceeds

shares, interest and dividends

Refinancing transactions - (186)

Purchase of own shares (2) (7)

Interest paid (76) (107)

Dividend paid (33) -

Net increase/(decrease) in cash and cash equivalents 20 (146)

¹Continuing Operations 24DEBT STRUCTURE

Fixed interest rates Leverage 6.7x net debt/EBITDA¹

with LIBOR hedged for Senior Term Facility

Blended cost of debt 4.97%;

Interest 4.36% 4.72% 6.27% 4.25% 3.78% 5.50% increased to 5.07% following pay

rate down of £106m of STF in August

Effective 2019 2018 2025 2020 2019 2022 Weighted average maturity 5 years

maturity

Run rate cash interest cover* close

Final 2019 2043 2043 2043 2043 2043 to 3x

maturity

Class A FCF to DSCR** 3.4x

£2,914m (covenant > 1.35x)

Class B FCF to DSCR** 2.3X

£735m

(covenant > 1.0x)

£475m £500m £500m Senior debt all investment grade

£454m

£158m Next bond refinancing due July

£250m 2018 (Class A1 notes)

Senior Term Class A1 Class A2 Class A3 Class A4 New Cash

Facility notes notes notes notes Class B2 *Run rate cash interest: Trading EBITDA

notes **Free cash flow: debt service cover ratio

¹Trailing 12 month trading EBITDA 25PENSIONS

IAS 19 pension deficit of £622m (31 July 15: £329m)

• Increase in deficit driven by decline in corporate bond yields, particularly since UK referendum

vote to leave the EU

Triennial review of AA UK pension scheme commenced

• Anticipate a significant increase from previous valuation of £202m (31 March 2013) due to

reduction in long term gilt yields

• Deficit likely to be materially below IAS 19 valuation

• Review completion due by June 2017

Review of options to mitigate current and future liabilities

Decline in bond yields provides refinancing opportunity

26FINANCIAL IMPLICATIONS OF THE TRANSFORMATION

Transformation capex: c.£10m saving allowing investment in other areas

Investment in marketing and brand: £10m plus additional spend on the product

proposition

IT opex: c£8m pa

Post-transformation capex run rate: IT c£10m; property & equipment c£10m; net

vehicle costs c£20m

Restructuring costs: £45m over three years

Cost savings: at least £40m in respect of the FY15 cost base in FY19

• Cost savings on target; phase 2 to commence once IT is in place

Driving revenue and earnings growth

27STRATEGY

BUILDING MOMENTUM IN YEAR 2 OF TRANSFORMATION

THE STRATEGIC PRIORITIES THE TIME LINE

1. Strengthen the AA to become the pre-

eminent membership services Year 1 FY16 Stronger foundations delivered

organisation in the UK

2. Revolutionise customer experience Year 2 FY17 Building momentum for change

through investing in the brand and

embracing new technologies

Year 3 FY18 Realise the transformation

3. Reduce Group borrowings and the

associated interest costs Year 4 FY19 Delivering growth

Transforming the AA into the UK’s pre-eminent Membership organisation

29ROADSIDE PERSONAL MEMBERSHIP – REVERSING THE DECLINE

MONTHLY PAID NEW BUSINESS VOLUMES

Growth in paid personal membership numbers

since April and continuing since July

YoY growth (%)

Retention improved to 81% (80% last year)

Stay AA since inception

• Calls to Stay AA down 9%

• Save rate up 7 percentage points

• Discount rate down 7 percentage points

Double-digit growth in new business volumes

• Re-invigorated marketing approach

• Improved digital capabilities

• Lower price increases to drive retention

• Advertising gaining traction

30PRODUCTIVITY IMPROVEMENTS

ROLLING 12 MONTH VARIABLE COST PER CASE*

Productivity improved since the full

implementation of new practices

Which? Recommended provider

for 11th successive year Roadside

training

Investments in productivity

• New technology (Bosch diagnostics, Battery

Sep-14

Feb-15

Sep-15

Feb-16

Jul-14

Aug-14

Jan-15

Jul-15

Aug-15

Jan-16

Jul-16

Oct-14

Oct-15

Mar-15

Mar-16

Dec-14

May-15

Dec-15

May-16

Nov-14

Apr-15

Jun-15

Nov-15

Apr-16

Jun-16

testers, universal spare wheel)

• New communications devices (tablets, i-phones)

FIX TIME PER JOB (MINUTES)

• Updated deployment system (AA Help) currently

being implemented

However 6% increase in breakdowns

attended in H1 compared with H116

Roadside

• £6m increase in total roadside operations costs training

partially offset by £2m of cost savings

Sep-14

Feb-15

Sep-15

Feb-16

Jul-14

Jan-15

Aug-14

Jul-15

Aug-15

Jan-16

Jul-16

Oct-14

Oct-15

Mar-15

Mar-16

Dec-14

May-15

Dec-15

May-16

Nov-14

Apr-15

Nov-15

Jun-15

Apr-16

Jun-16

*Inflation adjusted 31IT SYSTEMS TRANSFORMATION

Progress made across all key elements of the IT transformation programme

INFRASTRUCTURE SERVICE

Installed new IT infrastructure throughout New version of AA Help being rolled out

back office functions All patrols have new communications devices

Reduces manual reconciliations Improves efficiency of patrols

Reduces in house maintenance Improved information flows with call

Leads to efficiencies throughout the centres

business Provides for superior customer service

32IT SYSTEMS TRANSFORMATION

CRM

Marketing element live since March

Full CRM now being rolled out and uploaded

Expected be finalised in Autumn 2017

Improved on-boarding journey

Enables 360-degree view of customer,

integrating customer data

Real-time, automated reporting and

insight

Allows for relevant, personal and iterative

conversations with customers

Enables next best action to drive sales

Will facilitate easier cross sell

33IT SYSTEMS TRANSFORMATION

DIGITAL CONSUMER ROADSIDE ONLINE SALES

New commercial website launched in May YoY change 2013 – 2016

My AA launched in January Launch

of site

App refresh with improved functionality in

September Start of

activity

• App personal breakdown usage 14%

• App registration 23% of the Membership base

Improves online customer journey

Nov-13

Nov-14

Nov-15

Aug-13

Aug-14

Aug-15

Aug-16

Feb-13

Feb-14

Feb-15

Feb-16

May-13

May-14

May-15

May-16

Enables customer self service

Reduces call centre contact points

Gives us insights into customer behaviour

Opportunities to test product changes

34ADVERTISING ACHIEVING GREATER IMPACT

Investment of £5m in H1 with balance of £10m expected in H2

Greater reach and frequency

Additional “outdoor” has added visibility

TV ads delivering branded cut-through well ahead of norms

20161 20151 Norm²

ABC1 adults reached 94% 90% na

Average no of times reached 60 22 na

Execution Cut-through (i.e. remembered the ad) 52% 42% 39%

Brand Link (i.e. remembered that it was the AA) 79% 77% 62%

Branded Cut-through (i.e. remembered it and who 41% 32% 24%

it was)

¹Based on equivalent spend

²Ipsos Norm @ 500 Gross Rating Points (GPRs) i.e. for the same spend

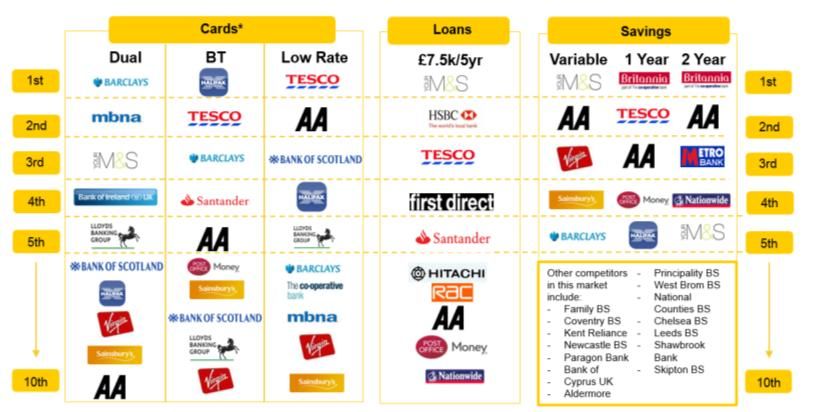

35FINANCIAL SERVICES AND IN HOUSE UNDERWRITER

FINANCIAL SERVICES INSURANCE UNDERWRITER

Launched cards, loans, savings, and mortgages (in Insurance Underwriter launched in January to

August) in partnership with the Bank of Ireland participate on the AA’s motor insurance panel

£160m matched book value 25k policies written by end of July; 54k by end

of September

AA positioned in top 1-5 savings; top 10 for cards

and loans Home insurance launched in August

Too early for material financial contribution but

As at 12th September 2016 early signs are promising

AA UNDERWRITER POLICIES BY ORIGIN

16% Has never been an AA insurance

customer

52% Was once previously an AA

32% insurance customer

An existing AA insurance customer

*For cards, this analysis does not show the fee based long dated balance transfer (BT) card segment. 36SUMMARY

Transformation well on track

• Continue to invest in brand marketing and product proposition

• Targeting cost savings from FY19 of at least £40m pa off the FY15 base

• Saving of c.£10m transformation capex allowing investment in other areas

Growth in Membership numbers - continued improvement into August and September

Free cash flow generation to be enhanced following transformation

Trading in line with market expectations for FY17; building momentum for FY18

Strengthened foundations and revolutionising customer experience

37APPENDIX

REVENUE

% of

£m H117 H116 Change Group

Roadside Assistance 370 359 +3.1% 79% Increase in average revenue per customer and

B2B revenue

Insurance Services 64 64 - 14% Lower policy numbers offset by higher income

per policy

Driving Services 32 33 -3.0% 7% Lower driving school franchises

Insurance 1 1 - -

Underwriting

Trading revenue 467 457 +2.2%

Business held for - 9

sales¹

Exceptional revenue (10) -

provision

Total revenue 457 466 -1.9%

1 In

September 2015, AA plc group completed the sale of its subsidiary Autowindshields (UK) Limited. As a result, this business was presented as held for sale in

the prior period. 39TRADING EBITDA

% of

£m H117 H116 Change Group¹

Roadside Assistance 179 172 +4.1% 81% Revenue up 3.1%

Advertising and Bosch investment timing

difference offset by higher workload

Insurance Services 35 37 -5.4% 16% Lower policies numbers

FS and Home Services business re-set under

way

Driving Services 9 9 - 4% Lower driving school franchisees

Insurance (1) 0 - (1%)

Underwriting

Head office costs (30) (26) +15.4% Incremental IT licensing costs

Total Trading 192 192 -

EBITDA

1% of Group pre head office costs

40SEGMENTAL ANALYSIS

YoY YoY

Roadside Assistance H117 Change Insurance Services H117 Change

Trading Revenue¹ (£m) 370 +3.1% Trading Revenue (£m) 64 Flat

Trading EBITDA¹ (£m) 179 +4.1% Trading EBITDA (£m) 35 -5.4%

Paid Personal Members (‘000s) 3,321 -0.6% Policy numbers² (‘000s) 1,962 -7.9%

Business Customers (‘000s) 10,179 +2.0% Average income per policy (£) 67 +6.3%

Average income per Paid Personal 157 +1.9%

Member (£)

Breakdowns attended (‘000s) 1,759 +5.8% YoY

Driving Services H117 Change

Trading Revenue (£m) 32 -3.0%

Trading EBITDA (£m) 9 Flat

Driving school instructors 2,516 -3.3%

1 Excluding glass business and exceptional revenue items

41PROFIT AND LOSS¹

£m H117 H116

Revenue 457 466

Cost of sales (168) (167)

Gross profit 289 299

Admin & marketing (157) (167)

Operating profit 132 132

Trading EBITDA 192 192

Items not allocated to a segment (10) (9)

Depreciation & amortisation (28) (25)

Exceptional items (22) (26)

Operating profit 132 132

Net finance cost (84) (201)

Profit/(loss) before tax 48 (69)

Tax (expense)/credit (10) 13

Profit/(loss) for the period from continuing 38 (56)

operations

Basic EPS – continuing operations (p/share) 6.2 (9.6)

Adj Basic EPS –continuing operations (p/share) 10.3 10.1

1 Continuing operations

42BALANCE SHEET

£m H117 H116

Goodwill and other intangible assets 1,276 1,271

Property, plant and equipment 117 106

Investments in joint ventures and associates 11 8

Deferred tax assets 107 57

Non-current assets 1,511 1,442

Inventories 6 5

Trade and other receivables 169 185

Cash and cash equivalents 158 155

Current assets 333 345

Assets held for sale 93 3

Total assets 1,937 1,790

Trade and other payables (502) (523)

Current tax payable (11) -

Provisions (21) (7)

Current liabilities (534) (530)

Borrowings and loans (2,922) (2,911)

Finance lease obligations (21) (20)

Defined benefit pension scheme liabilities (622) (329)

Provisions (7) (11)

Insurance technical provisions (4) (4)

Non-current liabilities (3,576) (3,275)

Liabilities held for sale (40) (4)

Total liabilities (4,150) (3,809)

Net liabilities (2,213) (2,019)

43CASH FLOW

£m H117 H116

Operating profit including discontinued operations 139 138

Depreciation and amortisation 29 26

Other items 7 2

Cash exceptional items 9 21

Change in working capital 16 39

Operating cash flow before tax and exceptional items 200 226

Cash exceptional items (9) (21)

Tax paid (7) (1)

Net cash flows from operating activities 184 204

Investing activities

Capital expenditure (37) (41)

Other investing activities 4 (1)

Net cash flows use in investing activities (33) (42)

Financing activities

Refinancing transactions - (186)

Purchase of own shares (2) (7)

Interest paid on borrowings (73) (104)

Payment of finance lease capital (20) (8)

Payment of finance lease interest (3) (3)

Dividends paid (33) -

Net cash flows from financing activities (131) (308)

Net increase/(decrease) in cash and cash equivalents 20 (146)

44DEBT PACKAGE

Run rate cash

Expected interest Principal at 31 Principal at 31

maturity date Interest rate (£m) July 16 (£m) July 15 (£m)

Senior Term Facility 31 January 2019 4.36% 19.8 454 454

Class A1 notes 31 July 2018 4.72% 22.4 475 475

Class A2 notes 31 July 2025 6.27% 31.4 500 500

Class A3 notes 31 July 2020 4.25% 21.3 500 500

Class A4 notes 31 July 2019 3.78% 9.5 250 250

Class B2 notes 31 July 2022 5.50% 40.4 735 735

4.97% 144.8 2,914 2,914

Ring fenced cash and cash equivalents 122 114

Non ring fenced cash and cash equivalents 36 41

Total cash and cash equivalents¹ 158 155

Class A Net Debt: Trading EBITDA 4.9x 4.9x

(STF & Class A notes less ring fenced cash)

Class B Net Debt: LTM EBITDA 6.8x 6.8x

(WBS debt less ring fenced cash)

Total Net Debt : LTM EBITDA (total debt less total cash) 6.7x 6.7x

Class A FCF DSCR 3.4x 3.8x

Class B FCF DSCR 2.3x 2.2x

¹Excludes available and restricted cash balances available for sale

45TRANSFORMATION STRATEGY

BUILDING MOMENTUM IN YEAR 2 OF TRANSFORMATION

THE STRATEGIC PRIORITIES THE TIME LINE

1. Strengthen the AA to become the pre-

eminent membership services Year 1 FY16 Stronger foundations delivered

organisation in the UK

2. Revolutionise customer experience Year 2 FY17 Building momentum for change

through investing in the brand and

embracing new technologies

Year 3 FY18 Realise the transformation

3. Reduce Group borrowings and the

associated interest costs Year 4 FY19 Delivering growth

Transforming the AA into the UK’s pre-eminent Membership organisation

47TRANSFORMATION STRATEGY

Strengthening the foundations and revolutionising customer experience

1. Investment in brand marketing

2. Investment in IT systems and digital capability

3. Restructuring and cost initiatives

4. Investment in Membership growth and price

5. Developing new business models

6. New business initiatives

Transformation creates the UK’s pre-eminent Membership services organisation

481. UNDER INVESTMENT IN THE BRAND

Enhance brand awareness and communicate membership proposition

Substitute brand marketing for past excessive price discounting

Invest £10m in FY16 and beyond

Benefits expected to become apparent from FY17

66%

57%

47%

31%

21% 22%

11%

4% 2%

2006 2007 2008 2009 2010 2011 2012 2013 2014

Total media spend AA Share of voice

Underpins product transformation and membership proposition

Sources: Ebiquity Media Tracking (TV, Press, Radio, Cinema, Outdoor), Road Brand Tracker Survey, IPSOS

492. INVESTMENT IN IT SYSTEMS AND DIGITAL CAPABILITY

De-risk infrastructure and connections Financial implications

• Replace legacy systems • IT transformation capex spend of £128m

over 3 years

• Staged implementation and double running

• Rationalisation of processes and transform call • Thereafter steady state IT capex of £10m pa

(versus £30m previously)

centre effectiveness

• Maintenance spend will increase by £8m in

Enhance commercial agility a full year

• Faster times for price, product and customer

communication changes

Development of digital proposition for

customers

• New App

• Connected car developments including telematics

Drives productivity and revenue growth

503. RESTRUCTURING AND COST INITIATIVES

People and property strategy to cost £45m over 3 years

• Cost savings £40m pa thereafter

Phase 1 announced

• £4m savings in FY16; £8m in a full year

Investment in people and key skills

• New central London office to attract digital and marketing talent

Continued investment in front line people and equipment

Productivity gains and energised culture in the medium term

514. INVESTMENT IN MEMBERSHIP GROWTH AND PRICE

Investment in price to create sustainable base Communicate existing services

• Expect c3% increase in income per Personal • Fuel Assist: 98% fix rate;

Member in FY16 20% member discount on pay-for-use

• Key Assist: dedicated vans; free for gold members

Investment in product

Additional opportunities in ancillary revenue

• Battery sales

• AA tyres

Focus on retention processes

• Stay AA

Investment required to drive retention and Membership

525. DEVELOPING NEW BUSINESS MODELS

Financial Services and Insurance Underwriter Craig Staniland Dominic Bird

CEO Head of Pricing

New partnership model for elements of 30+ years experience in Insurance 10 years experience in Insurance

Financial Services business Previously MD, AXA Personal Previously Head of New Business

Lines Pricing, Direct Line Group

• Expected short term cost of £4m but

Prior to that Founding Underwriting Prior to that Consultant,

significant potential Director, Swiftcover and Head of Towers Watson

Motor Underwriting, RBS

Launch of new in-house underwriter in

Steve Gaywood Tony Peppard

early 2016 Head of Counter-Fraud Head of Claims

• Expected set up costs of £1m 15 yrs Counter-Fraud experience 30+ years Claims and Vehicle

Management experience

Previously Head of Counter-Fraud,

• £7.5m investment AXA Personal Lines and Head of Previously MD, AXA and

Systems and Data Analytics, Swiftcover Claims and MD,

• Experienced team to lead the underwriter Innovation Conversant Data Churchill Claims Services Group

Building on market strengths and brand

53OPERATING AS A BROKER AND INSURER

Activities in personal lines insurance value chain

Price Pricing

New Policy Investment

Lead comparison & Claims

Sales business admin & &

generation & under- handling

fulfilment servicing solvency

quotation writing

Google PCWs Broker – the AA now Insurer – the new model

Effective business model that maximises use of capital AND broker value

New agile IT systems, integrated with AA and high-value external databases

Newly built capabilities drive excellence in data mining and agile pricing

Integrated policy and claims management, unencumbered by legacy systems

Leveraging robust controls and governance, mitigating conflicts

Experienced, proven team that has created and run successful operations

546. NEW BUSINESS INITIATIVES

Adjacent motoring services markets

Key opportunities:

1 Tyres

C £60bn broader Motoring Services

market – the AA currently focused on Used Car SalesFINANCIAL IMPLICATIONS OF THE TRANSFORMATION

Cost rationalisation expected to deliver £40m of cost savings in medium term

• Phase 1 underway and expected to deliver £8m in FY17

IT transformation to modernise the business and enhance customer experience

• Incremental spend of £128m over 3 years

• Additional opex

• Leading to facilitates cost savings and reduced capex

Investment in price – increase in income per Member restricted to 3%

Continuing incremental PLC costs confirmed as £8m pa

Short term uplift in capex to facilitate transformation

• Normalised net capex for IT and vehicles on current assumptions c£40m pa from FY19

56FY16 RESULTS SUMMARY

FY16 REVENUE

% of

£m FY16 FY15 Change Group

Roadside Assistance 724 711 +1.8% 75% Increase in average income per Member

offsetting the decline in personal Members

Insurance Services 131 142 -7.7% 14% Lower policy numbers and income per policy

Driving Services 68 74 -8.1% 7% Lower driving school franchises and Police

courses

Ireland 38 39 -2.6% 4% Impact of lower € - revenue up £3m on

constant FX

Insurance 2 1 - -

Underwriting

Total revenue¹ 963 967 -0.4%

¹ Excluding glass business 58FY16 TRADING EBITDA

% of

£m FY16 FY15 Change Group

Roadside Assistance 361 358 +0.8% 76% Revenue up 1.8%

Advertising and Bosch investment

Insurance Services 78 84 -7.1% 17% Efficiency savings

FS business re-set under way

Driving Services 19 20 -5.0% 4% Lower driving school franchisees and Police

courses

Ireland 13 15 -13.3% 3% EBITDA flat on constant currency

Head office costs (56) (48) +16.7% Incremental PLC and IT licensing costs

Total Trading 415 429 -3.3%

EBITDA¹

Trading EBITDA

43.1% 44.4%

Margin¹

¹ Excluding glass business 59FY16 SEGMENTAL ANALYSIS

Y-o-Y Y-o-Y

Roadside Assistance FY16 Change Insurance Services FY16 Change

Revenue¹ (£m) 724 1.8% Revenue (£m) 131 -7.7%

Trading EBITDA¹ (£m) 361 0.8% Trading EBITDA (£m) 78 -7.1%

Personal Members (‘000s) 3,673 -2.6% Policy numbers (‘000s) 2,074 -4.1%

Business Customers (‘000s) 10,216 6.0% Average income per policy (£) 63 -4.5%

Average income per Personal 141 4.4%

Member (£)

Breakdowns attended (‘000s) 3,459 -2.3%

Y-o-Y Y-o-Y

Driving Services FY16 Change Ireland FY16 Change

Revenue (£m) 68 -8.1% Revenue (£m) 38 -2.6%

Trading EBITDA (£m) 19 -5.0% Trading EBITDA (£m) 13 -13.3%

Driving school instructors 2,574 -3.6% Personal Members (‘000s) 128 7.6%

Insurance policy numbers (‘000s) 185 3.9%

¹ Excluding glass business 60FY16 BALANCE SHEET

£m FY16 FY15

Goodwill and other intangible assets 1,298 1,257

Property, plant and equipment 122 100

Investments in joint ventures and associates 10 4

Deferred tax assets 52 81

Other receivables - 21

Non-current assets 1,482 1,463

Inventories 5 5

Trade and other receivables 172 187

Current tax receivables - 1

Cash and cash equivalents 166 302

Current assets 343 495

Total assets 1,825 1,958

Trade and other payables (525) (498)

Provisions (8) (8)

Current liabilities (533) (506)

Borrowings and loans (2,920) (3,241)

Finance lease obligations (21) (16)

Defined benefit pension scheme liabilities (296) (434)

Provisions (7) (12)

Insurance technical provisions (4) (4)

Non-current liabilities (3,248) (3,707)

Total liabilities (3,781) (4,213)

Net liabilities (1,956) (2,255)

61FY16 CASH FLOW

£m FY16 FY15

Operating profit 305 326

Depreciation and amortisation 54 48

Other items 12 0

Cash exceptional items 37 57

Change in working capital 12 (15)

Operating cash flow before tax and exceptional items 420 416

Cash exceptional items (37) (57)

Tax paid (2) (2)

Net cash flows from operating activities 381 357

Investing activities

Capital expenditure (75) (37)

Other investing activities 4 21

Net cash flows use in investing activities (71) (16)

Financing activities

Refinancing transactions (183) 12

Purchase of own shares (22) -

Interest paid on borrowings (178) (218)

Payment of finance lease capital (34) (31)

Payment of finance lease interest (8) (4)

Dividends paid (21) -

Net cash flows from financing activities (446) (241)

Net increase in cash and cash equivalents (136) 100

62FY16 DEBT PACKAGE

Run rate cash Principal at 31 Principal at 31

Expected interest January 16 January 15

maturity date Interest rate (£m) (£m) (£m)

Senior Term Facility 31 January 2019 4.36% 19.8 454 663

Class A1 notes 31 July 2018 4.72% 22.4 475 475

Class A2 notes 31 July 2025 6.27% 31.4 500 500

Class A3 notes 31 July 2020 4.25% 21.3 500 500

Class A4 notes 31 July 2019 3.78% 9.5 250 250

Class B notes 31 July 2019 - - - 655

Class B2 notes 31 July 2022 5.50% 40.4 735 -

PIK notes 6 November 2019 - - - 175

4.97% 144.8 2,914 3,218

Ring fenced cash and cash equivalents 94 262

Non ring fenced cash and cash equivalents 72 40

Total cash and cash equivalents 166 302

Class A Net Debt: Trading EBITDA 5.0x 4.9x

(STF & Class A notes less ring fenced cash)

Class B Net Debt: LTM EBITDA 6.9x 6.6x

(debt excluding PIK notes less ring fenced cash)

Total Net Debt : LTM EBITDA (total debt less total cash) 6.8x 6.9x

Class A FCF DSCR 3.9x 3.5x

Class B FCF DSCR 2.4x 2.2x

63You can also read