Investor & Analyst Presentation - December 2018 Dr. Cornelius Patt, CEO Andreas Grandinger, CFO

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Investor & Analyst Presentation December 2018 Dr. Cornelius Patt, CEO Andreas Grandinger, CFO

Safe Harbor Statement

This document includes supplemental financial measures that are or may be non-GAAP financial measures. These supplemental

financial measures should not be viewed in isolation as alternatives to measures of zooplus’ financial condition, results of

operations or cash flows as presented in accordance with IFRS in its Consolidated Financial Statements. Other companies that

report or describe similarly titled financial measures may calculate them differently.

This document contains statements related to our future business and financial performance and future events or developments

involving zooplus that may constitute forward-looking statements. We may also make forward-looking statements in other

reports, in presentations, in material delivered to stockholders and in press releases. In addition, our representatives may from

time to time make oral forward-looking statements. Such statements are based on the current expectations and certain

assumptions of zooplus’ management, and are, therefore, subject to certain risks and uncertainties. A variety of factors, many of

which are beyond zooplus’ control, affect zooplus’ operations, performance, business strategy and results and could cause the

actual results, performance or achievements of zooplus to be materially different from any future results, performance or

achievements that may be expressed or implied by such forward-looking statements or anticipated on the basis of historical

trends. Further information about risks and uncertainties affecting zooplus is included throughout our most recent annual and

interim reports, which are available on the zooplus website, www.zooplus.de. Should one or more of these risks or uncertainties

materialize, or should underlying assumptions prove incorrect, actual results, performance or achievements of zooplus may vary

materially from those described in the relevant forward-looking statement as being expected, anticipated, intended, planned,

believed, sought, estimated or projected. zooplus neither intends, nor assumes any obligation, to update or revise these forward-

looking statements in light of developments which differ from those anticipated.

Due to rounding, numbers presented throughout this and other documents may not add up precisely to the totals provided and

percentages may not precisely reflect the absolute figures.

Investor & Analyst Presentation – December 2018 | page 2

European pet supplies market is a very attractive

market

Pet supplies market in Europe 2008-2020e (gross sales € bn)

CAGR +3% p.a.

29 » Ownership of pets is on the

26 rise in Europe

25 26

23 24 » Humanization of pets drives

22 23 spending

21

20 20

» Market is resilient through

economic cycles

» Consumables recurring

revenue – subscription like

» No technology and fashion

obsolescence risk

» Low product return rates

2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 … 2020e

Investor & Analyst Presentation – December 2018 | page 3

Source: Euromonitor 2016 and zooplus estimation

The online share is expected to continue to grow

far beyond 2020

Current online share and long-term hypothesis (€ bn)

Total

market 25 26 29 > 30

(gross)

Offline

95-96% 92-90% 80-85% < 50%

share

Online market

> 50% opportunity

> 15

Online 15-20%

share 4-5% 8-10%

2014 2017 2020e Long-term 1

Long-term growth potential of online should leave enough growth for zooplus after 2020

1 zooplus estimation; assuming successful shift of pet food grocery segment to online Investor & Analyst Presentation – December 2018 | page 4

Sales continue to grow super linear – high retention

core of the growth path

+233-255

1,344 –

1,366

+202

New customer

1,111 sales (1st year)

+198

909

+168 9M:

95%1

+136 711 Repeat

93%

93%1 customer sales

+88 543

92%

407 94%1

319 94%

93%1

91%

85%

21% – Sales growth

30% 28% 33% 31% 28% 22% 23% vs. PY

2012 2013 2014 2015 2016 2017 2018e 1) in local currencies

Investor & Analyst Presentation – December 2018 | page 5

zooplus reached No. 2 position in Europe in 2017

and is well on its way towards market leadership

Net sales and growth 2017 – European market (EUR bn)

1 1)

+ 6% Online ~0.06 1.7 (+100 EUR m)

2 +22% 1.1 (+202 EUR m)

Strategic goals

Close the gap towards the

current number 1 in

3

2)

+7% Online ~0.05 1.0 (+65 EUR m) Europe

Working towards market

4 3)

+22% n/a leadership in the total

market (online and offline)

Benefitting from all the advantages of size and market leadership

Source: Company data for 2017 figures; zooplus assumptions 1) Net sales estimated from gross sales 2) Includes services 3) amazon international growth rate

Investor & Analyst Presentation – December 2018 | page 6

zooplus is the online market leader in all geographies of

Europe – double digit sales growth in all regions in 9M 2018

DK, SE,

» Sales growth 9M 2018: FI, NO

+ 23% (+23% fx-adjusted)

70m +24%

4.5%

+21%

96m (fx-adj.)

2.4%

+21% 80m +39%

UK, IE 124m 12.2%

PL

Total market 2017 7.0%

23bn NL, BE, LU

335m

Sales zooplus in +16%

2017 6.2% 62m +39%

Sales growth in

4.5%

1,111m 9M 2018 D,A,CH HU CZ, SK, HU, RO,

187m +22%

zooplus market 4.9% SI, HR, BG, TR,

GR, LV, LT, EE

share in 2017 5.1% FR, MC

90m

+22%

3.7%

66m +27% IT

3.9%

ES, PT

Source: zooplus sales, unaudited data, growth rates compared to 9M 2017;

market shares based on Euromonitor 2016 market data and zooplus estimation Investor & Analyst Presentation – December 2018 | page 7Customer loyalty – the winning factor of the business

model – is at very high levels

Retention rates – Cohort analysis – Sales (€ m)

Ø 93%

1,111

Ø 93%1)

Ø 92%

2017 a

Ø 94%1)

Ø 94% 909 271

Ø 93%1)

2016 a

Ø 91% 711 253 86%

217

2015 a

Ø 85% 543 202 83%

167 86%

144

2014 a

Ø 79% 407 83%

174 145 88%

127 94% 119

319 2013 a

135 78%

105 90% 95 96% 91 97% 88

245 2012 a

2011 a 125 70%

87 91% 79 99% 78 99% 77 99% 77

100 62%

62 90% 56 99% 55 102% 56 100% 56 100% 56

2010 a+1

55 84% 46 98% 45 99% 44 104% 46 101% 46 101% 47Account value and customer account retention

increase with length of customer life

Projected sales per active account out of 2017 (in €)

345 360

331

295 312

285 291 290 Cumulated

270

244 sales per

account created

191 over a+10

years: € 1,730

a: year of

a a+1 a+2 a+3 a+4 a+5 a+6 a+7 a+8 a+9 a+10 acquisition = 2017

Account survival

100%1) 79% 81% 89% 93% 94% 95% 95% 96% 96% 95% rate2)

Share of remaining

100%1) 79% 64% 57% 53% 50% 47% 45% 43% 42% 40%

accounts3)

Sales per

191 192 173 163 154 144 140 142 144 144 142

account created

1) customers with at least one consecutive purchase after first transaction

2) Projected rate based on account retention rate of respective cohort

3) Average projected share of remaining accounts based on account survival rate Investor & Analyst Presentation – December 2018 | page 9Customer lifetime value is strongly positive and

justifies stronger investment focus

a+5 a+10

2017 projected projected

1,730

2017 net sales per

account in EUR (cum.)1 1,017

164

97

19

Customer acquisition CM cumulative 5 years CM cumulative 10 years

costs2 plus acquisition year plus acquisition year

1 Only accounts with repurchasing activity based on cohort specific retention rate (incl. fx-effects)

2 Traffic acquisition costs per new account with repurchasing activity

3 CM = contribution margin = net sales – all variable costs (excl. acquisition costs) = 9.5% Investor & Analyst Presentation – December 2018 | page 10Gross margin stabilization in Q2 2018 confirmed in

Q3 2018

Gross margin1

in % of sales

» Less customer and transactional

discounts

28.6%

» Reduction of non-profitable orders

28.3%

27.1% » Higher charges for shipping

− Changes in free-shipping

thresholds

− Charges for 2nd parcel in

an order

» Margin increase due to better

Q1 2018 Q2 2018 Q3 2018

sourcing

1 Sales – CoGS

Investor & Analyst Presentation – December 2018 | page 11Long-term gross margin decline halted

Gross margin1

in % of sales

37.4%

35.8%

32.3%

30.6%

28.7% 28.5% 28.0%

2012 2013 2014 2015 2016 2017 9M 2018

1Sales – CoGS; years prior to 2018 adjusted from published

external figures to new IFRS 15 Investor & Analyst Presentation – December 2018 | page 12Online private label business gains traction and

should grow to 20% share of food by 2020

12% 13% 4% 5% 1.3 1.5

Share of Share of Growth index

total food first order sales private label / food

Further significant increase in private label share until 2020

Figures for 2016 and 2017 Investor & Analyst Presentation – December 2018 | page 13zooplus investment mode will continue and further

improve zooplus’ market position

1 Competitive » Defending high loyalty of existing customers

pricing » Acquisition of new customers

2 Marketing » New customer acquisition for high customer lifetime value

costs » Increased investment into mobile

3 IT product » Improved product and user experience

development » Improved internal processes and efficiencies

4 » Close white spots in the distribution network

Logistics

» Increase capacity and speed up delivery to customers

5 » Expansion of private label share

Private label

» Development of new brands

Improved strategic position and driver for further growth

Investor & Analyst Presentation – December 2018 | page 14Cost ratio in 9M 2018 impacted by stronger

investment focus since H2 2017

Total margin & cost structure (in % of sales)

29.4% 28.6% Total margin1

28.9% 29.4% » Higher traffic acquisition

1.9%spend

Advertising/

1.7% 2.0% Marketing

» Logistics costs impacted by start-up

costs for new fulfillment centers

Logistics2

19.7% 19.8% » Admin costs impacted by higher

depreciation

1.0% 1.1% Payment

1.1%

IT/Admin/ (incl. 1.0% » Higher 1.0%

personnel costs in perspective

3.2% 3.2% depreciation & interest) of investment in people in IT and

3.3% 3.3% Personnel3 other key functions

9M 2017 9M 2018

1 Gross margin + other income on sales 3 All in, including LTI & SOP

2 Logistics costs reclassified to depreciation and interests according to IAS 17 Investor & Analyst Presentation – December 2018 | page 15Back on improved cost ratio path and

positive EBT in Q3 2018

Total margin & cost structure (in % of sales)

27.5% 28.9% 29.5% Total margin1

29.2% 30.1%

29.0% Advertising/

1.9% Marketing

2.0% 2.0% 1.9%

» Improved value per parcel with

positive impact on logistics costs

Logistics2

20.1% 20.3% 19.1%

» Further progress in routing

efficiencies in logistics network

1.0% 1.1% 1.1% Payment

IT/Admin/ (incl. 1.0% » Scale in IT/Admin, although

1.0%

3.0% 3.4% 3.3% depreciation & interest)

increasing depreciation

3.1% 3.5% 3.5% Personnel3

Q1 2018 Q2 2018 Q3 2018

- 1.7% -1.1% 0.5% EBT margin

1 Gross margin + other income on sales 3 All in, including LTI & SOP

2 Logistics costs reclassified to depreciation and interests according to IAS 17 Investor & Analyst Presentation – December 2018 | page 16Cost efficiency and cost control continue to be

major focus points

Total margin & cost structure (in % of sales)

38.0% 29.5% 29.5% Total margin1

38.8%

4.8% Advertising/

Marketing

29.9%

1.9% 29.0%

2.0%

2.2% 2.0%

24.1%

Logistics2

20.3% 19.1%

1.5%

3.8% 1.0% 1.1% Payment

3.2% 3.3% IT/Admin/ (incl.

4.7% depreciation & interest)

3.1% 3.5%

Personnel3

TY 2012 Q3 2017 Q3 2018

1 Gross margin + other income on sales 3 All in, including LTI & SOP

2 Logistics costs reclassified to depreciation and interests according to IAS 17 Investor & Analyst Presentation – December 2018 | page 17Comparison of cost structure – significant

advantage for zooplus

Cost ratio - selected competitors

48%

43% 41% 43%

40%

29%

Cost advantage for zooplus of more than 10%-points

Source: annual reports 2016 – Fressnapf 2015: all costs except for costs of goods sold, including depreciation and interest

Investor & Analyst Presentation – December 2018 | page 18Strong profitability of repeat customers business invested

to grow the business with long-term perspective

Repeat customer and new customer contribution (€ m)

Repeat customers New customers

(consecutive year’s sales) (sales in the year of acquisition)

Sales % of EBT EBT- Sales % of EBT EBT-

total z+ margin total z+ margin

2016 656 72% 23 + 4% 253 28% -5 - 2%

2017 840 76% 21 + 3% 271 24% - 17 - 6%

Reduction of profit margins in 2017 resulting from deliberate decision of stronger

investment focus to improve overall zooplus strategic position and long-term valuation

.

Investor & Analyst Presentation – December 2018 | page 19zooplus pan-European logistics network is a fully

integrated flexible network

» All centers managed as one

integrated pan-European

network

» All FCs operated by partners 2018

2009 2017

» Capex light approach 2017/18

2013

» SKU allocation, replenishment, 2016 2000/2011

order routing and packing 2015

2017

algorithms intellectual property

2015

of zooplus 2019e

2018

Fulfillment center (FC) Planned FC’s for 2018

Investor & Analyst Presentation – December 2018 | page 20zooplus logistics – significant expansion of pan-

European network in 9M 2018

Coventry (UK)

» Size of UK FC tripled in Q2 incurring

one-off costs and reduced efficiency

for transition period

Krosno (PL)

» New FC Poland started end of

September 2018 – 40,000 sqm

» New FC Spain started in September

2018 – closing of white spot in

network and strong improvement of

delivery speed to customers

Madrid (ES)

» New FC Spain operated by

4th FC partner – XPO Logistics

Investor & Analyst Presentation – December 2018 | page 21Distribution to the customer with the leading local

last mile providers

» Last mile distribution with

external partners (DSPs)

» zooplus operates approx. 60

relations of line hauls (trunk)

and direct DSP connections

2009

» At least two DSPs for every 2017

2017

2013

country offered for better 2016 2000/2011

customer service

2015 2017

» Management of parcel

allocation to FCs and DSPs by 2015

zooplus owned algorithms

» Focus on delivery speed and

efficiency

Fulfillment center (FC)

Hubs (DSP) - shown are selected relations from FC to Hub of DSPs

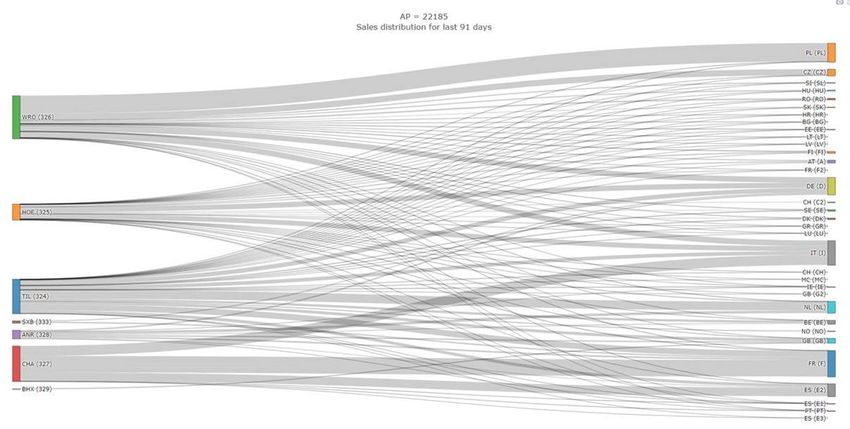

Investor & Analyst Presentation – December 2018 | page 22zooplus logistics system is an intelligent network solution

between fulfillment centers and destination countries

Example Cat‘s Best (cat litter): article flow between fulfillment centers and

country of destination for a period of three months

Fulfillment

center PL

WRO

DE Country of

HOE destination

IT

TIL

SXB NL

ANR GB

CHA FR

BHX ES

Criteria for choice of » No. of products in parcel » DSP chosen

logistics center1: » Top seller/long-tail » Available stock

1 selective

Investor & Analyst Presentation – December 2018 | page 23Operating cash flow continues to be positive – further

improvements in working capital

Cash flow (€ m)

9M 2018

20.4

Major focus on working capital and

operating cash flow improvements

14.3 with main drivers:

-6.1

» Inventory turn

» Payment days

3.1 % 2.5 %

Cash flow from Cash flow from Free cash flow

operating investing

activities activities

Investor & Analyst Presentation – December 2018 | page 24The planned growth should go with a positive

operating cash flow

Working capital development in % net sales

9.5% » Increase in inventory

turnover

8.1%

» More efficient

6.3% replenishment process

5.1% » Improvement in

payment days

Constant working capital in

2018 implies a further

reduction to around 4.2%

of sales, for 2019 to around

2014 2015 2016 2017 3.4% of sales

Investor & Analyst Presentation – December 2018 | page 25Sales and EBT guidance for full year 2018

Sales (€ m) EBT (€ m)

Guidance 2018e +21 to +23%

- 0.5 to + 0.5%

1,344 to 1,366 of net sales

+ 233 to + 255 vs. 2017

Profit guidance 2018 based on current FX levels.

Investor & Analyst Presentation – December 2018 | page 26You can also read