Investor Presentation (Q2 2021) - John Iannone Senior Vice President, Investor & Public Relations

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Investor Presentation (Q2 2021)

(WSBC financials as of the three months ended 31 March 2021)

John Iannone

Senior Vice President, Investor & Public Relations

304-905-7021

Forward-Looking Statements and Non-GAAP Financial Measures

Forward-looking statements in this report relating to WesBanco’s plans, strategies, objectives, expectations, intentions and adequacy of resources, are made

pursuant to the safe harbor provisions of the Private Securities Litigation Reform Act of 1995. The information contained in this report should be read in

conjunction with WesBanco’s Form 10-K for the year ended December 31, 2020 and documents subsequently filed by WesBanco with the Securities and

Exchange Commission (“SEC”), which are available at the SEC’s website, www.sec.gov or at WesBanco’s website, www.WesBanco.com. Investors are

cautioned that forward-looking statements, which are not historical fact, involve risks and uncertainties, including those detailed in WesBanco’s most recent

Annual Report on Form 10-K filed with the SEC under “Risk Factors” in Part I, Item 1A. Such statements are subject to important factors that could cause actual

results to differ materially from those contemplated by such statements, including, without limitation, the effects of changing regional and national economic

conditions including the effects of the COVID-19 pandemic; changes in interest rates, spreads on earning assets and interest-bearing liabilities, and associated

interest rate sensitivity; sources of liquidity available to WesBanco and its related subsidiary operations; potential future credit losses and the credit risk of

commercial, real estate, and consumer loan customers and their borrowing activities; actions of the Federal Reserve Board, the Federal Deposit Insurance

Corporation, the SEC, the Financial Institution Regulatory Authority, the Municipal Securities Rulemaking Board, the Securities Investors Protection Corporation,

and other regulatory bodies; potential legislative and federal and state regulatory actions and reform, including, without limitation, the impact of the

implementation of the Dodd-Frank Act; adverse decisions of federal and state courts; fraud, scams and schemes of third parties; cyber-security breaches;

competitive conditions in the financial services industry; rapidly changing technology affecting financial services; marketability of debt instruments and

corresponding impact on fair value adjustments; and/or other external developments materially impacting WesBanco’s operational and financial performance.

WesBanco does not assume any duty to update forward-looking statements.

In addition to the results of operations presented in accordance with Generally Accepted Accounting Principles (GAAP), WesBanco's management uses, and

this presentation contains or references, certain non-GAAP financial measures, such as pre-tax pre-provision income, tangible common equity/tangible assets;

net income excluding after-tax restructuring and merger-related expenses; efficiency ratio; return on average assets; and return on average tangible equity.

WesBanco believes these financial measures provide information useful to investors in understanding our operational performance and business and

performance trends which facilitate comparisons with the performance of others in the financial services industry. Although WesBanco believes that these non-

GAAP financial measures enhance investors' understanding of WesBanco's business and performance, these non-GAAP financial measures should not be

considered an alternative to GAAP. The non-GAAP financial measures contained therein should be read in conjunction with the audited financial statements

and analysis as presented in the Annual Report on Form 10-K as well as the unaudited financial statements and analyses as presented in the Quarterly

Reports on Forms 10-Q for WesBanco and its subsidiaries, as well as other filings that the company has made with the SEC.

1

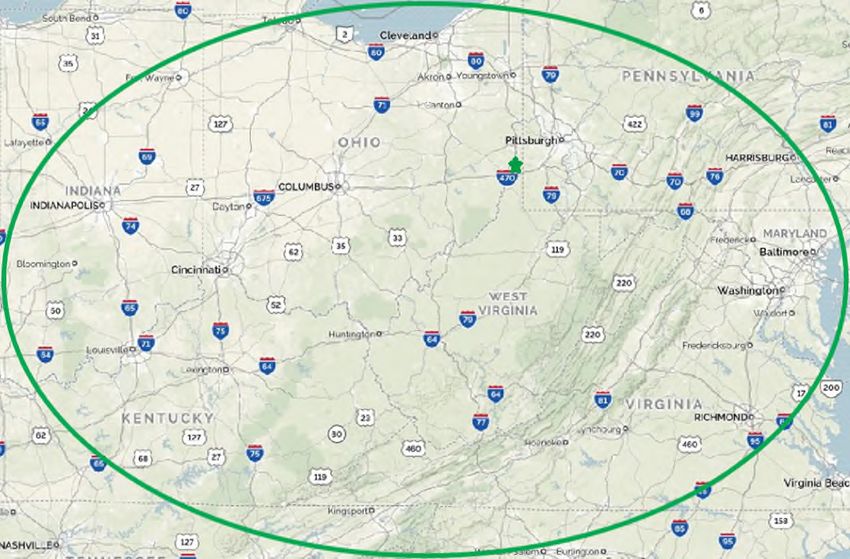

Evolving Regional Financial Services Institution

Strong market Strong Market Presence in Major Markets

presence across

legacy and major #16 in OH Pittsburgh

metropolitan markets Wheeling

#11 Pgh

Indianapolis MSA

Dayton Columbus

#9 in MD

Morgantown

Balanced loan and Cincinnati

Baltimore

deposit distribution Washington D.C.

#3 in WV

across diverse #11 in KY Huntington

Lexington Park

Charleston

regional footprint Louisville Frankfort

Lexington

Fort Knox

Diversified revenue Broad and Balanced Market Distribution

Loans Deposits

generation engines

supported by unique MD

WV MD

19% 17% WV

long-term advantages 24% 29%

KY

15%

KY

Well-executed long- 14%

OH

IN

IN 26% OH

term growth strategies 5% PA

5% PA 13%

21%

12%

Note: loan and deposit data as of 3/31/2021 (loans exclude Small Business Administration’s Paycheck Protection Program (“SBA PPP”) loans); location data as of 5/1/2021; market 2

share based on 2020 deposit rankings (exclusions: Pittsburgh MSA – BNY Mellon; state of OH – National Consumer Cooperative Bank) (source: S&P Global Market Intelligence)

Investment Rationale

Balanced loan and deposit distribution across footprint

Balanced and Diversified earnings streams built for long-term success, led by

Diversified with century-old, $5.2B trust and wealth management business

Unique Long- Strong presence in economically diverse, major markets

Term Advantages supported by positive demographic trends

Robust legacy deposit base provides pricing advantage

Emphasis on digital capabilities and customer service to ensure

relationship value that meets customer needs efficiently and

Distinct and effectively

Well-Executed

Established lending and wealth management teams

Long-Term

Growth Strategies Focus on positive operating leverage built upon a culture of

expense management, enhanced by consolidated back-office

functions in lower cost markets

Legacy of Credit Well-capitalized with solid liquidity and strong credit quality and

Quality, Risk regulatory compliance

Management, and Seven consecutive “outstanding” CRA ratings since 2003

Shareholder Critical, long-term focus on shareholder return through earnings

Focus growth and effective capital management

3

Note: trust assets under management as of 3/31/2021

Strategies for Long-Term

Success

Long-Term Growth Strategies

Diversified

Digital

Loan Franchise-

Long History Banking

Portfolio Enhancing

of Strong Service

with C&I Expansion

Wealth Strategies

and Home within

Management & Core

Lending Contiguous

Capabilities Deposit

Focus Markets

Advantage

Focus on Delivering Positive Operating Leverage

Strong Legacy of Credit Quality, Risk Management, and Compliance

5

Diversified Loan Portfolio

Focus on strategic diversification, $10.7 Billion Loan Portfolio

growth, and credit quality Commercial

Comm'l R/E: & Industrial

Balance disciplined loan origination Improved

Property

15%

with prudent lending standards 47%

Focus on C&I and home equity lending SBA PPP

8%

Key offerings include treasury Consumer

3%

management, foreign exchange, cyber

HELOC

security, and lockbox services 6%

Comm'l R/E: Land,

Strong residential mortgage program Construction Residential R/E

6% 15%

Average loans to average deposits ratio of 85.3% provides opportunity for

continued loan growth

Low cost of deposits provides a competitive advantage in the typical higher

cost Mid-Atlantic market

Manageable lending exposures

De-emphasized consumer and several CRE categories in recent years

6

Note: loan and deposit data as of quarter ending 3/31/2021

Strong Wealth Management Capabilities

Trust & Investments Insurance

Trust Assets

$5.2B of trust and mutual fund (Market Value as of 12/31) ($B) Personal, commercial, title,

assets under management $4.3

$5.2 health, and life

CAGR

6,000+ relationships $2.3 $2.4

$3.2 4.6% Expand title business in all

Growth opportunities from markets

shale-related private wealth Applied quotation software

2002 2008 2012 2018 2021

management 3/31 utilization (personal)

Expansion opportunities in Third-party administrator (TPA)

KY, IN, and the Mid-Atlantic services for small business

WesMark Funds – six healthcare plans

proprietary funds across

equities, bonds, and tactical

assets

Securities Brokerage Private Banking

Securities investment sales $980MM in private banking

Licensed banker program Private Banking Loans and Deposits

loans and deposits

Investment advisory services

(as of 12/31) ($MM)

3,350+ relationships

Regional player/coach program $770

$980

Growth opportunities from

$540 CAGR

Expand external business $270

37% shale-related private wealth

development opportunities

$100 management

Expansion opportunities in KY, 2013 2015 2017 2019 2021 Expansion opportunities in KY,

3/31

IN, and Mid-Atlantic

Loans Deposits IN, and Mid-Atlantic

7

Note: assets, loans, deposits, and clients as of 12/31/2020; chart financials as of 12/31 unless otherwise stated

Digital Platforms Drive Engagement & Efficiency

Digital banking utilization

~74% of retail customers utilize online digital banking services

~4.5 million web and mobile logins per month

• Mobile 50% of total, with an average of 17 monthly logins per customer

Mobile wallet & mobile deposits increased 55% & 50% YoY, respectively

Zelle® to be utilized as a payment service beginning 2H2021

Digital acquisition

~50% of residential mortgage applications submitted via online portal

~200 deposit accounts opened per month

WesBanco Insurance Services launched white-label insurance capabilities

with a web-based term-life insurance platform, and a fully-integrated digital

property & casualty insurance for consumers and small businesses

Core upgrade in 2021

Omni-channel presence – real-time account activity across all channels

Improved customer service through reduced manual activities

More efficient processing cost structure

Cloud-based architecture utilization

Early adoption to leverage modernized data and application platforms,

combined with significant expense and performance benefits

Actively harnessing advanced artificial intelligence (AI) and robotic process

automation (RPA) technologies to automate business processes

Note: digital statistics as of 1Q2021; online residential mortgage applications and deposit account opening capabilities launched July 2019; WesBanco Insurance Services online term-life and P&C 8

insurance capabilities launched November 2020 and January 2021, respectively

Benefits of Core Deposit Funding Advantage

Robust legacy deposit base, enhanced by shale energy-related royalties,

provides funding advantage in Mid-Atlantic market

Reflecting the significantly lower interest rate environment, aggressively

reduced deposit rates since March 2020

During the last five years:

Total deposits (excluding CDs) have grown organically at a 11% CAGR

Total demand deposits have grown organically at a 15% CAGR to represent

~57% of total deposits

Avg Deposits as of 3/31/2016 Avg Deposits as of 3/31/2020 Avg Deposits as of 3/31/2021

CDs Non-int

CDs Non-int CDs Non-int 12% Bearing

26% Bearing 18% Bearing DD

DD

DD 33%

21% Total

29%

DD

Savings

40%

18%

Total

Total DD

Int Savings DD 56%

Bearing 18% 50%

DD

19%

Savings Int Money Int

18% Bearing Mkt Bearing

Money 14% DD

Money DD

Mkt 23%

Mkt 21%

16%

14%

Funding Cost Funding Cost Funding Cost

Interest-Bearing = 0.32% Interest-Bearing = 0.55% Interest-Bearing = 0.20%

Total Deposits = 0.25% Total Deposits = 0.39% Total Deposits = 0.14%

[Peer Average Total Deposit Cost = 0.29%] [Peer Average Total Deposit Cost = 0.67%] [Peer Average Total Deposit Cost = 0.21%]

Note: text reflects period-end data and pie charts reflect quarterly averages; peer bank group includes all U.S. banks with total assets of $10B to $25B (as of most recent period) 9

from S&P Global Market Intelligence (as of 5/3/2021) and represent simple averagesFranchise Expansion

Targeted acquisitions in existing Contiguous Markets Radius

markets and new higher-growth

metro areas

ESB &

FSBI

Long-term focus on appropriate AmTrust

branches

capital management to enhance OAKF

shareholder value OLBK

FFKT FTSB

YCB

Strong capital and liquidity, along

with strong regulatory compliance

processes, provides ability to

execute transactions quickly

Franchise-Enhancing Acquisitions

Diligent efforts to maintain a OLBK: announced Jul-19; closed Nov-19

community bank-oriented, value- FFKT: announced Apr-18; closed Aug-18

FTSB: announced Nov-17; closed Apr-18

based approach to our markets

YCB: announced May-16; closed Sep-16

ESB: announced Oct-14; closed Feb-15

History of successful acquisitions FSBI: announced Jul-12; closed Nov-12

that have improved earnings AmTrust: announced Jan-09; closed Mar-09

OAKF: announced Jul-07; closed Nov-07

10

Note: AmTrust was an acquisition of five branchesFocus on Positive Operating Leverage

Disciplined growth, balanced by a fundamental focus on expense

management and supported by franchise-enhancing acquisitions, in order

to deliver positive operating leverage and enhance shareholder value

Start of

“Durbin Pandemic &

ESB YCB Amendment” Fed Funds

Merger Merger Impact Begun Rate Cut to

Assets Fidelity

(Feb-15) (Sep-16) (Jul-19) 0.0-0.25%

up 218% Merger (Mar-20)

(Nov-12)

Efficiency Ratio

$10B Asset FTSB Merger OLBK

down 410bp Lending & Revenue Threshold (Apr-18) Merger

Diversification Preparations FFKT Merger (Nov-19)

Strategy Begun Begun (Aug-18)

$18.0

60.81% 60.98% 60.99% 62.00%

$17.0

$16.0

$15.0

59.50% 59.59% 60.00%

$14.0

$13.0

$12.0 57.05% 56.69% 56.68% 56.71%

58.00%

$11.0 56.44% 56.38%

$10.0

$9.0 56.00%

$8.0 54.60%

$7.0

$6.0 54.00%

$5.0

$4.0

$3.0 52.00%

$2.0

$1.0 $5.4 $5.5 $6.1 $6.1 $6.3 $8.5 $9.8 $9.8 $12.5 $15.7 $16.4 $17.1

$0.0 50.00%

2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021

3/31

Operating

Leverage 9.6x 4.2x 0.7x 1.6x 10.9x 2.2x 1.9x 1.8x 2.5x 1.4x 1.8x 2.2x

Assets ($B) Efficiency Ratio (YTD)

Note: financial data as of 12/31; current year-to-date (YTD) data as of 3/31/2021; balance sheet data as of period ends; Efficiency Ratio presented on a fully taxable-equivalent (FTE) 11

and annualized basis; please see the reconciliations in the appendixStrong Risk Management and Capital Position

Strong legacy of credit and risk management and regulatory compliance

Based upon conservative underwriting standards and approval processes

supported by centralized back-office and loan funding functions

Mature enterprise risk management program headed by Chief Risk Officer

addressing key risks in all business lines and functional areas

Enhanced compliance and risk management system and testing platform

Strong and scalable BSA/AML function

Examined by CFPB for consumer compliance supervision

Seven consecutive “outstanding” CRA ratings since 2003

Strong and improving regulatory capital ratios significantly above

regulatory requirements, and high tangible common equity (TCE) levels

Tier 1 Risk-Based Capital Ratio Tier 1 Leverage Capital Ratio

10.47% 10.59%

13.66% 10.27%

13.41%

12.81% 12.90% 9.85%

12.66% memo 9.56% memo

Well- Well-

Capitalized Capitalized

8.0% 5.0%

14.12% 15.09% 12.89% 14.72% 14.95% Required 10.39% 10.74% 11.30% 10.51% 10.74% Required

6.0% 4.0%

2017 2018 2019 2020 1Q21 2017 2018 2019 2020 1Q21

WSBC $10-25B Banks WSBC $10-25B Banks

Note: capital ratios enhanced by August 2020 issuance of $150MM of preferred stock; effective 4Q2019, as required by the Dodd- Frank Act for financial institutions with total assets

>$15B, Tier 1 Capital Ratios negatively impacted by the movement of ~$130MM of TruPS from Tier 1 to Tier 2 risk-based capital; peer bank group includes all U.S. banks with total 12

assets of $10B to $25B (as of each period) from S&P Global Market Intelligence (as of 5/3/2021) and represent simple averagesRecent Successes and Accolades

Based 100% on customer satisfaction and consumer feedback, WesBanco Bank

was again named, for the third year, one of the World’s Best Banks in an

independent ranking

WesBanco Bank received the America Saves Designation of Savings Excellence

for Banks, a designation from America Saves

For the 11th time since the list’s inception in 2010, WesBanco Bank was named to

the Forbes list of the Best Banks in America – coming in as the 12th best bank

Named to Newsweek magazine's inaugural ranking of America's Best Banks,

recognizing those banks that best serve their customers needs, as well as being

named the Best Big Bank in the state of West Virginia

Bauer Financial again awarded WesBanco their highest rating as a “five-star” bank

The Central Ohio market of WesBanco Bank was awarded a “Top Workplaces”

honor by Columbus C.E.O. magazine for the fifth consecutive year

The Western Pennsylvania market of WesBanco Bank was awarded a “Top

Workplaces” honor by The Pittsburgh Post Gazette for the third consecutive year

The FDIC awarded WesBanco Bank it’s 7th consecutive composite “Outstanding”

rating for its most recent CRA performance

Kroll Bond Rating Agency assigned senior unsecured debt ratings of BBB+ to

WesBanco, Inc. and A- to WesBanco Bank, Inc.

13

Note: Kroll Bond Rating Agency rating report issued 8/4/2020Financial Overview

Q1 2021 Financial and Operational Highlights

Strong growth in pre-tax, pre-provision income Pre-Tax, Pre-Provision Income(1)

$64.2 million, +3.6% YoY

Continued emphasis on expense management

Improving macro-economic factors drove a $28 Net Income Available to Common

million release of provision for credit losses Shareholders and Diluted EPS(1)

$71.3 million; $1.06/diluted share

Key credit quality metrics remained at low levels

and favorable to peer bank averages Efficiency Ratio(1)

56.71%

Positive growth in both loans and deposits

Mortgage banking income increased due to a Mortgage Banking Income

high volume of originations $4.3 million, +234.2% YoY

WesBanco is well-capitalized with solid liquidity Loan Growth

and a strong balance sheet

+3.4% YoY

Recent Board authorized stock repurchase

program, when combined with the remainder of the

previous authorization, represents approximately Deposit Growth (x-CDs)

5% of outstanding shares +28.9% YoY

Note: financial and operational highlights during the quarter ended March 31, 2021; loan growth includes approximately $824 million of loans funded through the Small Business

Administration’s Paycheck Protection Program (“SBA PPP”), as established by the CARES Act 15

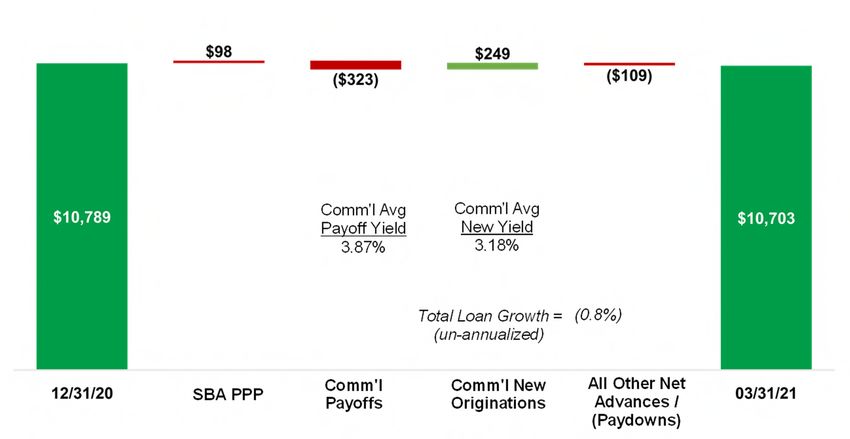

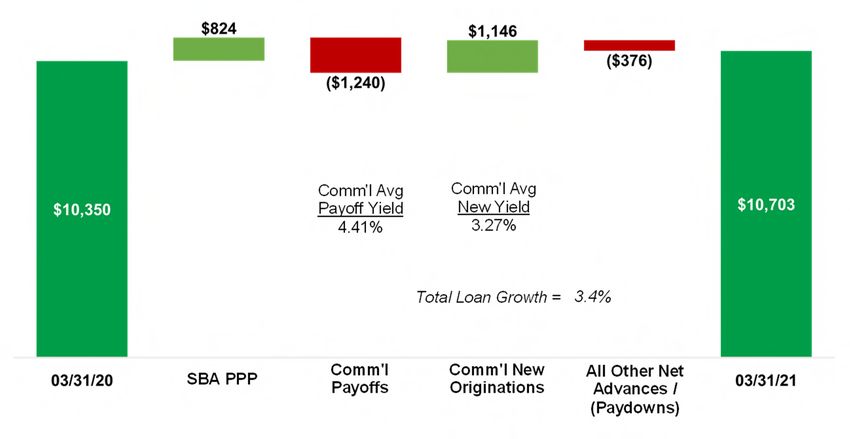

(1) Non-GAAP measure – please see reconciliation in appendixQ1 2021 Total Portfolio Loans ($MM)

~7,750 SBA PPP loans totaling

~$824 million (as of 3/31/2021)

During Q1 2021, ~2,330 customers

applied for and received forgiveness

of their 2020 SBA PPP loans totaling

$223 million; and, assisted >3,240

businesses with 2021 SBA PPP

loans totaling ~$344 million

C&I loan levels (x-SBA PPP) were

down year-over-year primarily due to

lower utilization of revolving lines of

credit (~33% vs. ~43% last year)

Q1 2021 residential real estate loan

levels impacted by retaining ~40% of

the $326 million of origination dollar

volume (~57% refi) on balance sheet

Home equity and consumer loan

levels negatively impacted by payoffs

driven by utilization of residential

mortgage refinancing and higher

personal savings

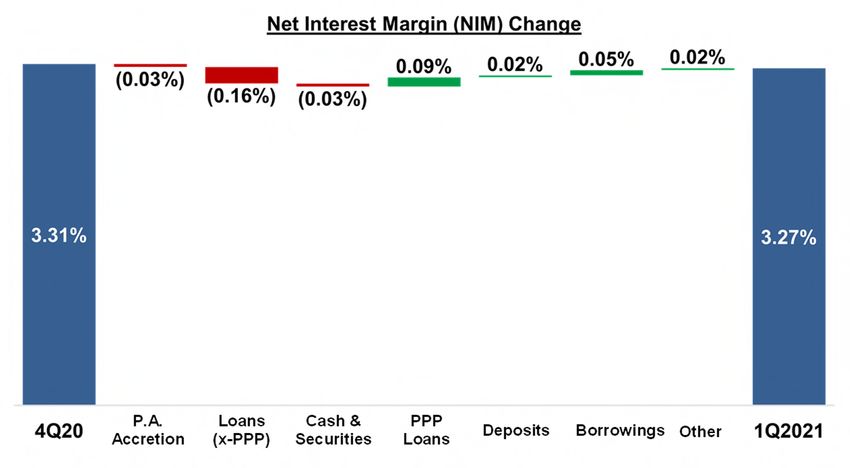

16Q1 2021 Net Interest Margin (NIM)

NIM negatively impacted by the low

interest rate environment

As a result of higher cash balances,

investment securities increased by

$0.9 billion during Q1 2021, mostly

during March

Aggressively reduced deposit rates

throughout the past year

Q1 2021 interest-bearing deposit

funding costs 20bp, or, when

including non-interest bearing

1Q2021 Commercial Loan Portfolio Index Mix

Variable Commercial Loan Repricing

deposits, 14bp

Variable

48 to 60

Rate >60 Months

65%

Months

47% 3% Period-end FHLB borrowings of

$0.4 billion, with remaining average

Fixed life of less than one year, down $1.2

Rate

35% 24 to 48 billion year-over-year

Months

3%

3 to 24

SBA PPP loans benefited Q1 2021Q1 2021 Non-Interest Income

Quarter Ending % H / (L) % H / (L)

Mortgage banking fees increased

due to an ~50% year-over-year

($000s) 03/31/21 03/31/20 12/31/20 increase in 1-to-4 family residential

mortgage origination dollar volume,

Trust fees $7,631 9.8% 13.0% and the associated sale of ~60% of

those into the secondary market

Service charges on deposits 4,894 (26.0%) (13.7%)

Trust fees increased due to equity

Electronic banking fees 4,365 2.6% (1.3%)

market improvement and organic

growth in trust assets

Net securities brokerage revenue 1,524 (9.2%) 8.7% Other income increased due to

higher loan swap-related income,

Bank-owned life insurance 1,709 (3.4%) (2.4%) which was primarily the result of

$2.8 million of fair market value

Mortgage banking income 4,264 234.2% (21.6%)

adjustments in the current period as

compared to a negative $2.8 million

Net securities gains 279 (81.3%) (59.7%)

adjustment last year

Net gain on OREO & other assets 175 3.6% nm Service charges on deposits were

lower due to higher consumer

Other income 8,367 120.1% 27.7% deposits associated with the three

rounds of stimulus to-date and

Total non-interest income $33,208 18.6% 1.5%

lower general consumer spending,

resulting in fewer eligible account

fees

18

Note: OREO = other real estate ownedQ1 2021 Non-Interest Expense

Quarter Ending % H / (L) % H / (L) Total operating expenses remained

well-controlled through company-

($000s) 03/31/21 03/31/20 12/31/20 wide efforts to manage open

positions and certain discretionary

Salaries and wages $36,890 (5.2%) (5.7%)

expenses

Employee benefits 10,266 (1.0%) (3.2%) Efficiency ratio improved 98bp year-

over-year to 56.71%

Net occupancy 7,177 1.3% 6.0% Lower salaries and wages reflect the

recent financial center closures and

Equipment 6,765 12.0% (0.7%)

the management of FTEs

Marketing 2,384 109.5% 42.3%

Anticipated gross cost savings of ~$6

million from closures remain on track

FDIC insurance 1,282 (39.3%) 0.3%

to be fully realized during Q2 2021

Marketing expense was higher due to

Amortization of intangible assets 2,896 (14.2%) (13.0%) increased product advertising and

brand awareness campaigns that

Other operating expenses 17,816 4.0% (0.9%)

were delayed from 2020 due to the

Sub-total non-interest expense $85,476 (0.8%) (2.4%)

COVID-19 pandemic

Q1 restructuring & merger-related

Restructuring & merger-related 851 (83.5%) 75.8% charges related to the financial

center optimization plan that was

Total non-interest expense $86,327 (5.5%) (2.0%)

completed during January 2021

19Comparable Operating Metrics

Disciplined execution upon growth strategies providing strong performance

compared to all U.S. banks with total assets from $10B to 25B

(note: 2020 comparability impacted by timing of the adoption of CECL accounting standard and economic assumptions used by each bank)

Return on Average Tangible Equity Return on Average Assets

1.74%

17.8% 18.4%

1.39% 1.34%

15.1% 1.09%

13.9% 1.34% 1.34% 1.35%

15.5% 0.77%

14.9% 14.6% 1.04%

9.2%

0.89%

11.5% 11.3%

12.2% 16.2% 14.0% 8.6% 18.2% 0.96% 1.26% 1.24% 0.73% 1.72%

2017 2018 2019 2020 2021 (3/31) 2017 2018 2019 2020 2021 (3/31)

WSBC (x- merger & DTA revalue costs) WSBC $10-25B Banks WSBC (x- merger & DTA revalue costs) WSBC $10-25B Banks

Efficiency Ratio Net Interest Margin

3.86% 3.79%

3.71%

57.2% 3.35%

56.1% 3.15%

55.4% 55.2%

54.0%

56.4% 54.6% 56.7% 56.4% 56.7% 3.44% 3.52% 3.62% 3.37% 3.27%

2017 2018 2019 2020 2021 (3/31) 2017 2018 2019 2020 2021 (3/31)

WSBC $10-25B Banks WSBC $10-25B Banks

Note: financial data as of 12/31 YTD; current YTD data as of 3/31/2021; Current Expected Credit Losses (“CECL”) accounting standard adopted January 1, 2020 by WSBC; peer

bank group includes all U.S. banks with total assets of $10B to $25B (as of each period) from S&P Global Market Intelligence (as of 5/3/2021) and represent simple averages

(ROATE & ROAA are S&P calculations; Efficiency & NIM are company-reported); Efficiency & NIM presented on a fully taxable-equivalent (FTE) and annualized basis; please see 20

the reconciliations in the appendixSolid Legacy of Credit Quality

Favorable asset quality measures compared to all U.S. banks with total

assets from $10B to 25B

(note: 2020 ACL comparability impacted by timing of the adoption of CECL accounting standard and economic assumptions used by each bank)

Criticized & Classified Loans as % of Total Loans Non-Performing Assets as % of Total Assets

4.76% 0.89%

3.76% 0.71%

3.16% 0.60% 0.60% 0.57%

2.98% 3.02%

1.17% 1.08% 2.17% 4.59% 4.26% 0.50% 0.35% 0.35% 0.25% 0.23%

2017 2018 2019 2020 2021 (3/31) 2017 2018 2019 2020 2021 (3/31)

WSBC $10-25B Banks WSBC $10-25B Banks

Net Charge-Offs as % of Average Loans (annualized) Allowance for Credit Losses as % of Total Loans

0.22% 0.22%

0.20% 0.20%

1.51% 1.49%

0.13% 0.95% 0.87% 0.80%

0.71% 0.64% 0.51% 1.72% 1.50%

0.13% 0.06% 0.09% 0.06%

0.02% 2017 2018 2019 2020 2021 (3/31)

2017 YTD 2018 YTD 2019 YTD 2020 YTD 2021 (3/31)

WSBC $10-25B Banks WSBC $10-25B Banks

Note: financial data as of quarter ending 12/31; current year data as of 3/31/2021; Current Expected Credit Losses (“CECL”) accounting standard adopted January 1, 2020 by WSBC; 21

peer bank group includes all U.S. banks with total assets of $10B to $25B (as of each period) from S&P Global Market Intelligence (as of 5/3/2021) and represent simple averagesReturning Value to Shareholders

Focus on appropriate capital allocation to provide financial flexibility while

continuing to enhance shareholder value through earnings growth and

effective capital management

Capital management strategy: dividends, share repurchases, acquisitions

Q1 2021 dividend yield 3.5%, compared to 2.2% for bank group

On April 22, 2021, WesBanco’s Board of Directors authorized the adoption of a

new stock repurchase program, which, when combined with the remainder of

the previous authorization, represents ~5% of outstanding shares

Quarterly Dividend per Share ($) Tangible Book Value per Share ($)

$0.33 $22.21

+136% +84%

$12.09

$0.14

4Q10 1Q21 4Q10 1Q21

Note: dividend through February 2021 declaration announcement; WSBC dividend payout ratio based on earnings per share excluding merger-related costs and including impact from

adoption of the Current Expected Credit Losses (“CECL”) accounting standard; WSBC dividend yield based upon 5/3/2021 closing stock price of $37.28; peer bank group includes all 22

U.S. banks with total assets of $10B to $25B (as of most recent period) from S&P Global Market Intelligence (as of 5/3/2021) and represent simple averagesAppendix

Q1 2021 Key Metrics

Quarter Ending H / (L) H / (L)

03/31/21 03/31/20 12/31/20

Return on Average Assets (1)(2) 1.74% 104bp 52bp

PTPP Return on Average Assets (1)(2) 1.57% (1bp) 1bp

Return on Average Tangible Equity (1)(2) 18.39% 1,021bp 511bp

PTPP Return on Average Tangible Equity (1)(2) 16.78% (97bp) (22bp)

Tangible Book Value per Share ($) (1) $22.21 4.0% 2.1%

Efficiency Ratio (1)(2) 56.71% (98bp) (35bp)

Net Interest Margin 3.27% (27bp) (4bp)

Non-Performing Assets to Total Assets 0.23% (3bp) (2bp)

Net Loan Charge-offs to Average Loans (annualized) 0.02% (16bp) 0bp

Note: PTPP = pre-tax, pre-provision

(1) Non-GAAP measure – please see reconciliation in appendix 24

(2) Excludes restructuring and merger-related expensesQ1 2021 Current Expected Credit Loss (CECL)

The decrease in the allowance was driven by improvement in the macroeconomic

forecast and changes in portfolio mix slightly offset by COVID-19 pandemic related

adjustments

Allowance coverage ratio of 1.50%, or, excluding SBA PPP loans, 1.62%

Excludes fair market value adjustments on previously acquired loans representing 0.34%

of total portfolio loans

($000s)

Changes in

prepayment

Changes to Qualitative

speeds

macroeconomic adjustments for

variables COVID-19

pandemic, regional Changes in

portfolio mix

Includes changes macroeconomic

in both quantitative factors, and

hospitality industry Changes in

and qualitative

credit quality

economic factors classification loans

Aging of existing

portfolio

Economic Pandemic Portfolio

Factors Qualitative Factors Changes / Other

Note: ACL at 3/31/2021 excludes off-balance sheet credit exposures of $6.7 million; on January 1, 2020, WSBC adopted the CECL accounting standard (prior to this date, the 25

allowance for credit losses was calculated under the incurred method)Reconciliation: Efficiency Ratio & Operating Leverage

Three Months Ending Twelve Months Ending

($000s) 03/31/20 12/31/20 03/31/21 12/31/10 12/31/11 12/31/12 12/31/13 12/31/14 12/31/15 12/31/16 12/31/17 12/31/18 12/31/19 12/31/20

Non-Interest Expense $91,333 $88,069 $86,327 $141,152 $140,295 $150,120 $160,998 $161,633 $193,923 $208,680 $220,860 $265,224 $312,208 $354,845

Restructuring & Merger-Related

($5,164) ($484) ($851) ($175) $0 ($3,888) ($1,310) ($1,309) ($11,082) ($13,261) ($945) ($17,860) ($16,397) ($9,725)

Expense

Non-Interest Expense (excluding

restructuring & merger-related $86,169 $87,585 $85,476 $140,977 $140,295 $146,232 $159,688 $160,324 $182,841 $195,419 $219,915 $247,364 $295,811 $345,120

expense)

Net Interest Income (FTE-basis) $121,346 $120,790 $117,517 $172,235 $175,885 $175,027 $192,556 $200,545 $246,014 $263,232 $300,790 $352,760 $405,222 $483,999

Non-Interest Income $28,009 $32,705 $33,208 $59,599 $59,888 $64,775 $69,285 $68,504 $74,466 $81,499 $88,840 $100,276 $116,716 $128,185

Total Income $149,355 $153,495 $150,725 $231,834 $235,773 $239,802 $261,841 $269,049 $320,480 $344,731 $389,630 $453,036 $521,938 $612,184

Efficiency Ratio 57.69% 57.06% 56.71% 60.81% 59.50% 60.98% 60.99% 59.59% 57.05% 56.69% 56.44% 54.60% 56.68% 56.38%

Net Interest Income (before provision

$120,162 $119,712 $116,478 $166,092 $169,365 $168,351 $185,487 $193,228 $236,987 $253,330 $290,295 $347,236 $399,904 $479,480

expense)(non-FTE)

Non-Interest Income $28,009 $32,705 $33,208 $59,599 $59,888 $64,775 $69,285 $68,504 $74,466 $81,499 $88,840 $100,276 $116,716 $128,185

Total Revenue $148,171 $152,417 $149,686 $225,691 $229,253 $233,126 $254,772 $261,732 $311,453 $334,829 $379,135 $447,512 $516,620 $607,665

YoY Change in Total Revenue $1,515 $2,730 $3,562 $3,873 $21,646 $6,960 $49,721 $23,376 $44,306 $68,377 $69,108 $91,045

YoY Change in Non-Interest Expense

(excluding restructuring & merger- ($693) ($6,856) ($682) $5,937 $13,456 $636 $22,517 $12,578 $24,496 $27,449 $48,447 $49,309

related expense)

Operating Leverage 2.2x 9.6x 4.2x 0.7x 1.6x 10.9x 2.2x 1.9x 1.8x 2.5x 1.4x 1.8x

Note: “efficiency ratio” is non-interest expense excluding restructuring and merger-related expense divided by total income; FTE represents fully taxable equivalent; Old Line Bancshares

merger closed November 2019; Farmers Capital Bank Corporation merger closed August 2018; First Sentry Bancshares merger closed April 2018; Your Community Bankshares merger26

closed September 2016; ESB Financial merger closed February 2015; Fidelity Bancorp merger closed November 2012; AmTrust 5 branch acquisition closed March 2009Reconciliation: Pre-Tax, Pre-Provision Income (PTPP) and Ratios

Three Months Ending

($000s) 03/31/20 12/31/20 03/31/21

Income before Provision for Income Taxes $27,017 $64,557 $91,317

Provision for Credit Losses 29,821 (209) (27,958)

Pre-Tax, Pre-Provision Income ("PTPP") $56,838 $64,348 $63,359

Restructuring and Merger-Related Expense 5,164 484 851

PTPP (excluding restructuring and merger-related expense) $62,002 $64,832 $64,210

PTPP (excluding restructuring and merger-related expense) $62,002 $64,832 $64,210

Average Total Assets 15,784,939 16,546,761 16,636,258

PTPP Return on Average Assets 1.58% 1.56% 1.57%

PTPP (excluding restructuring and merger-related expense) $62,002 $64,832 $64,210

Amortization of Intangibles 3,374 3,327 2,896

PTPP before Amortization of Intangibles (excluding restructuring and merger-related expense) $65,376 $68,159 $67,106

Average Total Shareholders' Equity $2,594,069 $2,744,936 $2,770,416

Average Goodwill and Other Intangibles (net of deferred tax liability) (1,112,327) (1,150,184) (1,148,171)

Average Tangible Equity $1,481,742 $1,594,752 $1,622,245

PTPP Return on Average Tangible Equity 17.75% 17.00% 16.78%

27

Note: Old Line Bancshares merger closed November 2019Reconciliation: Net Income, EPS & Tangible Book Value per Share

Three Months Ending

($000s, except earnings per share) 12/31/10 03/31/20 12/31/20 03/31/21

Net Income Available to Common Shareholders n/a $23,396 $50,210 $70,584

Restructuring and Merger-Related Expense (net of tax) n/a 4,080 383 672

Net Income Available to Common Shareholders (excluding restructuring

n/a $27,476 $50,593 $71,256

and merger-related expense)

Net Income Available to Common Shareholders per Diluted Share ($) n/a $0.35 $0.75 $1.05

Restructuring and Merger-Related Expense (net of tax) n/a 0.06 0.01 0.01

Net Income Available to Common Shareholders per Diluted Share ($)

n/a $0.41 $0.76 $1.06

(excluding restructuring and merger-related expense)

Average Common Shares Outstanding – Diluted (000s) n/a 67,587 67,304 67,335

Total Shareholders's Equity (period-end) $606,863 $2,586,060 $2,756,737 $2,785,522

Goodwill & Other Intangible Assets (net of deferred tax liability)(period-end) (285,559) (1,154,033) (1,149,161) (1,146,874)

Preferred Shareholders' Equity 0 0 (144,484) (144,484)

Tangible Common Equity (period-end) $321,304 $1,432,027 $1,463,092 $1,494,164

Common Shares Outstanding (period-end) (000s) 26,587 67,058 67,255 67,282

Tangible Common Book Value per Share ($) $12.09 $21.36 $21.75 $22.21

28

Note: Current Expected Credit Losses (“CECL”) accounting standard adopted January 1, 2020 by WSBC; Old Line Bancshares merger closed November 2019Reconciliation: Return on Average Assets

Three Months Ending Twelve Months Ending

($000s) 03/31/20 03/31/21 12/31/17 12/31/18 12/31/19 12/31/20

Net Income Available to Common Shareholders $23,396 $70,584 $94,482 $143,112 $158,873 $119,400

Restructuring and Merger-Related Expenses (net of tax) $4,080 $672 $614 $14,109 $12,954 $7,683

Net Income Available to Common Shareholders (excluding restructuring

$27,476 $71,256 $107,876 $157,221 $171,827 $127,083

& merger-related expense)

Average Assets $15,784,939 $16,636,258 $9,854,312 $11,337,379 $12,853,920 $16,442,704

Return on Average Assets 0.60% 1.72% 0.96% 1.26% 1.24% 0.73%

Return on Average Assets (excluding restructuring & merger-related

0.70% 1.74% 1.09% 1.39% 1.34% 0.77%

expense)

Note: Current Expected Credit Losses (“CECL”) accounting standard adopted January 1, 2020 by WSBC; Old Line Bancshares merger closed November 2019; Farmers Capital 29

Bank Corporation merger closed August 2018; First Sentry Bancshares merger closed April 2018; Your Community Bankshares merger closed September 2016Reconciliation: Return on Average Tangible Equity

Three Months Ending Twelve Months Ending

($000s) 03/31/20 03/31/21 12/31/17 12/31/18 12/31/19 12/31/20

Net Income Available to Common Shareholders $23,396 $70,584 $94,482 $143,112 $158,873 $119,400

Amortization of Intangibles (1) $2,665 $2,288 $3,211 $5,514 $8,169 $10,595

Net Income Available to Common Shareholders before Amortization

$26,061 $72,872 $97,693 $148,626 $167,042 $129,995

of Intangibles

Restructuring and Merger-Related Expenses (net of tax) $4,080 $672 $614 $14,109 $12,954 $7,683

Net Income Available to Common Shareholders before Amortization

$30,141 $73,544 $111,087 $162,735 $179,996 $137,678

of Intangibles and Restructuring & Merger-Related Expenses

Average Total Shareholders Equity $2,594,069 $2,770,416 $1,383,935 $1,648,425 $2,119,995 $2,651,402

Average Goodwill & Other Intangibles, Net of Deferred Tax Liabilities ($1,112,327) ($1,148,171) ($584,885) ($732,978) ($927,974) ($1,141,528)

Average Tangible Equity $1,481,742 $1,622,245 $799,050 $915,447 $1,192,021 $1,509,874

Return on Average Tangible Equity 7.07% 18.22% 12.23% 16.24% 14.01% 8.61%

Return on Average Tangible Equity Excluding Restructuring & Merger-

8.18% 18.39% 13.90% 17.78% 15.10% 9.12%

Related Expenses

(1) amortization of intangibles tax effected at 21% for 2018 forward, and 35% for all prior periods

Note: Current Expected Credit Losses (“CECL”) accounting standard adopted January 1, 2020 by WSBC; Old Line Bancshares merger closed November 2019; Farmers Capital 30

Bank Corporation merger closed August 2018; First Sentry Bancshares merger closed April 2018; Your Community Bankshares merger closed September 2016You can also read