INVESTOR UPDATE TSX & NYSE: ERF - Enerplus

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

TSX & NYSE: ERF

INVESTOR UPDATE

May 2022

Forward looking information and statements

This presentation contains certain forward-looking information and statements ("forward-looking information") within the meaning of applicable securities laws. The use of any of the words "expect", "anticipate", "continue", "estimate",

“guidance”, "ongoing", "may", "will", "project", "plans", “budget”, "strategy" and similar expressions are intended to identify forward-looking information. In particular, but without limiting the foregoing, this presentation contains forward-looking

information pertaining to the following: updated 2022 production and capital spending guidance; expected capital spending levels in 2022; expectations regarding 2022 and future shareholder returns, including payment of dividends and

Enerplus' share repurchase program, the timing and amounts thereof and funding dividends and the share repurchase program from free cash flow; expectations regarding free cash flow generation and capital spending reinvestment rates;

expected operating strategy in 2022 and expectations regarding our drilling program and well costs; 2022 average production volumes and the anticipated production mix; the proportion of our anticipated oil and gas production that is

hedged and the expected effectiveness of such hedges in protecting our cash flow from operating activities and adjusted funds flow; oil and natural gas prices and differentials and expectations regarding the market environment and our

commodity risk management program in 2022; updated and existing 2022 Bakken and Marcellus differential guidance; expectations regarding realized oil and natural gas prices; expected operating, transportation and cash G&A expenses and

production taxes and updated 2022 guidance with respect thereto; expectations regarding net debt and debt reduction; expectations regarding increases to dividends and timing thereof; and expectations regarding renewal of our normal

course issuer bid, including timing and size thereof.

The forward-looking information contained in this presentation reflects several material factors and expectations and assumptions of Enerplus including, without limitation: that we will conduct our operations and achieve results of operations

as anticipated; the continued operation of the Dakota Access Pipeline; that our development plans will achieve the expected results; that lack of adequate infrastructure will not result in curtailment of production and/or reduced realized prices

beyond our current expectations; current and anticipated commodity prices, differentials and cost assumptions; the general continuance of current or, where applicable, assumed industry conditions, the impact of inflation, weather conditions,

storage fundamentals and expectations regarding the duration and overall impact of COVID-19; the continuation of assumed tax, royalty and regulatory regimes; the accuracy of the estimates of our reserve and contingent resource volumes;

the continued availability of adequate debt and/or equity financing and adjusted funds flow to fund our capital, operating and working capital requirements, and dividend payments as needed; the ability to fund increased dividend payments

and the share purchase program from free cash flow as expected and discussed in this presentation; our ability to comply with our debt covenants; the availability of third party services; expected transportation expenses; the extent of our

liabilities; and the availability of technology and process to achieve environmental targets. In addition, our 2022 guidance described in this presentation is based on: a WTI price of US$85.00/bbl, a NYMEX price of US$5.00/Mcf, a Bakken

crude oil price at par with WTI, a Marcellus natural gas price differential of $(0.75)/Mcf below NYMEX and a CDN/USD exchange rate of 0.79. Enerplus believes the material factors, expectations and assumptions reflected in the forward-

looking information are reasonable but no assurance can be given that these factors, expectations and assumptions will prove to be correct. Current conditions, economic and otherwise, render assumptions, although reasonable when made,

subject to greater uncertainty.

The forward-looking information included in this presentation is not a guarantee of future performance and should not be unduly relied upon. Such information involves known and unknown risks, uncertainties and other factors that may

cause actual results or events to differ materially from those anticipated in such forward-looking information including, without limitation: continued instability, or further deterioration, in global economic and market environment, including

from COVID-19, inflation and/or the Ukraine/Russia conflict and heightened geopolitical risks; decreases in commodity prices or volatility in commodity prices; changes in realized prices of Enerplus’ products from those currently anticipated;

changes in the demand for or supply of our products; unanticipated operating results, results from our capital spending activities or production declines; legal proceedings or other events inhibiting or preventing operation of the Dakota Access

Pipeline; curtailment of our production due to low realized prices or lack of adequate infrastructure; changes in tax or environmental laws, royalty rates or other regulatory matters; changes in our capital plans or by third party operators of our

properties; increased debt levels or debt service requirements; inability to comply with debt covenants under our bank credit facilities and/or outstanding senior notes; inaccurate estimation of our oil and gas reserve and contingent resource

volumes; limited, unfavourable or a lack of access to capital markets; increased costs; a lack of adequate insurance coverage; the impact of competitors; reliance on industry partners and third party service providers; changes in law or

government programs or policies in Canada or the United States; and certain other risks detailed from time to time in our public disclosure documents (including, without limitation, those risks identified in our first quarter 2022 MD&A, our

annual information form for the year ended December 31, 2021, our 2021 annual MD&A and Form 40-F as at December 31, 2021).

The forward-looking information contained in this presentation speaks only as of the date of this presentation. Enerplus does not undertake any obligation to publicly update or revise any forward-looking information contained herein, except

as required by applicable laws.

2

Enerplus overview

Differentiated core Bakken position with deep drilling inventory

Committed to capital discipline CDN

WATERFLOODS

Robust free cash flow profile

Long track record of returning capital to shareholders

Consistently operates with low financial leverage BAKKEN MARCELLUS

Deeply integrated approach to ESG

Dual listed: TSX & NYSE

Production by area (1) Production by product(1) Capital allocation(1)

Market capitalization: US$3 billion

28% 53% 83%

2022e production: 98,500 BOE/d (62% liquids)

64% 38%

10%

7%

7%

1% 9%

Bakken Marcellus Canada DJ Crude Oil Natural Gas NGL Bakken Marcellus Canada/DJ

3

1) Charts reflect 2022e production and capital allocation.

Key updates from Q1 2022

INCREASING CASH RETURNS TO SHAREHOLDERS IN 2022

1

Returning $350MM or 50% of free cash flow, whichever is greater, through dividends & share repurchases

ON TRACK TO DELIVER RECORD ANNUAL FREE CASH FLOW

2

Forecasting 2022 free cash flow(1) of approximately $675MM based on $85 WTI and $5 NYMEX

EXECUTION DRIVES PRODUCTION GUIDANCE INCREASE

3

Strong execution increases annual production forecast to 96-101 MBOE/d (+0.5 midpoint)

MANAGING INFLATION IMPACTS

4

Services, equipment & supplies secured to execute efficient operating plan; 2022 capital spending increased 5%(2)

COMMITTED TO CAPITAL DISCIPLINE

5

No increase to activity levels, no plans to chase higher, less efficient growth

1) See Non-GAAP & Other Financial Measures in “Advisories”. 4

2) Capital spending guidance updated to $400-$440MM, from $370-$430MM. Midpoint increased by 5%.

2022: disciplined plan, robust free cash flow generation

Key figures 2022e free cash flow sensitivities (1)(2)

TOTAL $900 30%

PRODUCTION 96,000-101,000 $800 24%

BOE/D 25%

$700 22%

Free cash flow ($ millions)

18%

Free cash flow yield

$600 20%

CAPITAL

SPENDING(1) $400-$440 $500

$ MILLIONS

15%

$400

$300 10%

REINVESTMENT

2022 capital allocation and excess free cash flow at $85 WTI

2022e adjusted funds flow

Based on $85/bbl

WTI & $5/Mcf NYMEX

$1,200 2022e capex: $400-$440MM

~$1,100 ~$640

7% annual production growth(2)

$1,000 3-5% annual organic production growth

(normalized for timing of 2021 acquisitions)

Excess free cash flow:

$800 Annual dividend Share repurchases

PRIORITIZE

US$ millions

Quarterly: Debt reduction

$0.043/share Accretive acquisitions

$600

~$420 ~$40

$400

$200

$0

Adjusted funds flow(1) Capex Dividends Excess free cash flow after

dividends

1) See Non-GAAP & Other Financial Measures in “Advisories”. Based on realized prices through Q1 2022 and flat oil price thereafter (assumes $5.00/Mcf NYMEX). 6

2) 2022e production growth based on the guidance midpoint.

Return of capital to shareholders

2022 return of capital oil price sensitivity(1)

$ millions

2022 RETURN OF CAPITAL COMMITMENT

Total of $350 million or 50% of free cash flow, $400 $370

whichever is greater, to be returned to $350 $350

$350MM

shareholders in 2022 Additional minimum

$300 amount

Returns to be delivered through dividends and

share repurchases $306

$200 $274

Quarterly dividend increased by 30% to $221

50% of

$0.043/share, or ~$40 million annualized FCF

$100

Minimum of $286 million in remaining cash

returns in 2022 $64 $64 $64

$0

$75 WTI $85 WTI $95 WTI

Capital returned to date Capital returns remaining

Capital returns = Dividends + Share repurchases

7

1) Capital returned to date is inclusive of dividends and share repurchases through May 4, 2022. Sensitivity uses $5.00/Mcf NYMEX.

Bakken focused five-year outlook

Bakken focused five-year outlook expected to generate Five-year production and free cash flow outlook

~$2.3bn of free cash flow(1) at $70/bbl WTI (2) 120 $2.5

Cumulative free cash flow ($ billions)

− >80% of capital allocated to the Bakken

Company production (Mboe/d)

100

− >80% of annual cash flow generated from the Bakken $2.0

80

Annual production growth rate of 3-5% supports sustainability $1.5

− Base decline expected to remain between 30-35% 60

− Assumes 1.5-2 rigs operating throughout 5-year period $1.0

40

Outlook assumes current asset portfolio unchanged 20 $0.5

− Divestment process initiated for Canadian assets

0 $0.0

2022 2023 2024 2025 2026

Bakken Marcellus

Five-year outlook based on $70/bbl WTI, $3.00/Mcf NYMEX(2) Canada/DJ Cumulative free cash flow

Annual capital Avg. reinvestment Cumulative free Annual liquids

spending(1) rate (1) cash flow(1) production growth

~$400-450 million ~50% ~$2.3 billion 3-5%

1) See Non-GAAP & Other Financial Measures in “Advisories”. 8

2) 2022 is based on $85/bbl WTI and $5.00 /Mcf NYMEX. Years 2023-2026 are based on $70/bbl WTI and $3.00/Mcf NYMEX..

ENVIRONMENTAL, SOCIAL & GOVERNANCE

Material focus areas

Water Management

2021

TARGETS (1)

PERFORMANCE (1)

GHG emissions intensity reduction targets(2) >20% Methane emissions

intensity reduction

2022 target: 20% reduction in methane emissions Community

2030 target: 50% reduction ~25% GHG emissions Greenhouse Gas

intensity reduction

Emissions Engagement

ESG

Freshwater use reduction targets MATERIAL

31%

2021 target: 25% reduction/well comp. in FBIR Freshwater use reduction

FOCUS

2025 target: 50% reduction/well comp. corporately per completion in 2021 AREAS

Health & Safety target Zero lost time Board Constitution Culture

Reduce LTIF(3) by 25% on average, between 2020- injuries in 2021 & Culture

2023

Health & Safety

1) Targets and 2021 performance are relative to a 2019 baseline.

2) Enerplus’ GHG emissions reduction targets address scope 1 and 2 emissions. Scope 1 emissions are direct emissions from owned and operated facilities. Scope 2 emissions are indirect emissions from the generation of purchased

energy for the Company’s owned and operated facilities. Targets are relative to a 2019 baseline. 9

3) Lost Time Injury Frequency.

DIFFERENTIATED BAKKEN POSITION

10Core Bakken is competitive with the best N.A. oil plays

Third-party data: Breakeven WTI oil prices across North American oil plays(1)(2)

Source: Enverus Intelligence Research

$60

Little Knife & FBIR areas represent ~85%

of Enerplus’ >10-year core inventory

$50

WTI oil price ($/bbl)

$40

$30

$20

$10

$0

UINTA

CARDIUM

BAKKEN-US

PRB

DUVERNAY

DELAWARE

MIDLAND

BAKKEN

DJ

EAGLE FORD

VIKING

LITTLE KNIFE

SCOOP

SHAUNAVON

BAKKEN-CDN

STACK

FBIR

BAKKEN

1) Breakeven prices represent the average WTI price at which wells generate a 10% IRR. Based on wells since 2018. 11

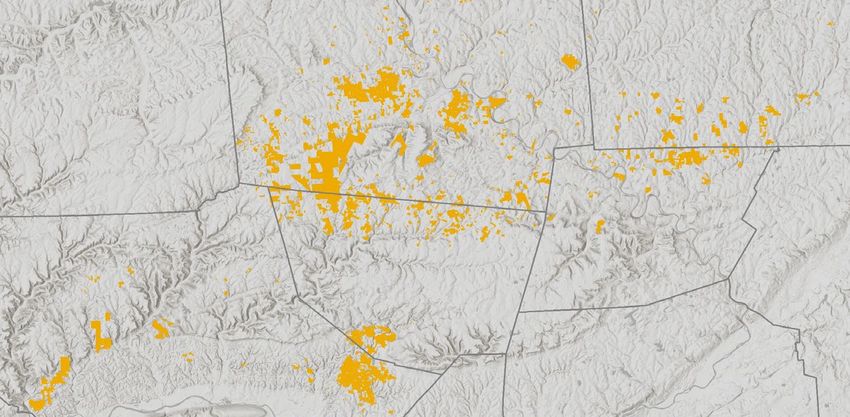

2) Based on oil plays developed with horizontal wells.Enerplus: substantial core acreage, large remaining opportunity set

Lightly drilled acreage Acreage in core & extended core Substantial sub-$50/bbl WTI inventory

Drilling density: wells per DSU Productivity: 6 month BOE/1K foot lateral Contours based on breakeven WTI prices (10% IRR)

Williams

Indicative well NPVs

NPV10 at $80 WTI(1)

FBIR

($MM)

$60 Approx. $4MM+

$50 Approx. $7MM+

Little

Knife $40 Approx. $12MM+

Murphy Creek Enerplus operated acreage

Enerplus non-op acreage

Outlines are Enerplus operated units Outlines are Enerplus operated units

1) Source: Drilling density based on internal mapping. Productivity mapping from Tudor, Pickering, Holt & Co. WTI breakeven analysis and drilling density based on internal research. Well NPVs at $80 & $100 WTI assume a total well cost 12

of $6.5mm. Well NPVs at $60 WTI assume a total well cost of $6.0mm.Enerplus has outsized core inventory relative to production Third-party data: Top Bakken operators - remaining drilling inventory ranked by breakeven WTI price (1)(2) Source: Enverus Intelligence Research Mcap >$10bn Mcap

Deep drilling inventory supports sustainable outlook

1,000

Inventory upsides

900 Lower return locations that offer

800

250

upside through stimulation advances,

well cost improvements, sustained

high oil prices

>Decade

Net drilling locations

700 of Core drilling

600 670 110 Extended Core inventory

Periphery of established core (at development pace

FUTURE

500 Lower returns than Core, but exceeds

DRILLING assumed in 5-year plan)

returns threshold at midcycle prices

LOCATIONS

400 Primarily southern Dunn

IN CORE /

EXTENDED CORE(1)

300

560 Core Additional drilling

200 Established economic core of play inventory in the

Well defined & de-risked Extended Core + Upside

100 FBIR, northern Dunn, eastern locations

Williams

0

45

2022 North Dakota

Onstreams (2) Inventory

1) See “Advisories – Drilling Inventory” for a reconciliation of undrilled locations between those associated with reserves and those not associated with any reserves. As at 1 Jan 2022. Includes operated and non-operated locations. 14

2) 2022 onstreams includes operated and non-operated wells.Operational execution supporting low cost structures

Total well costs 34%

($MM) Reduction driven

primarily by efficiencies

$8.6

Strong track record of drilling and completion Expected increase

efficiency gains driving cost structures lower $5.7

due to inflation

~$6.5

− Almost $3MM reduction in total well costs 2018-2021

Strategic partnerships, technology and innovative

culture are supporting efficiencies

2018 2019 2020 2021 2022e

Inflationary pressures are increasing 2022e well costs

EFFICIENCY GAINS

− Primarily driven by diesel and steel which account for approximately

Drilling days (spud to rig release) Completions (stages/day)

80% of the estimated increase Normalized to 20,700 ft TMD

IMPROVEMENT IMPROVEMENT

15% SINCE 2018 2.7x SINCE 2018

14.6

12.4 13.0

4.9

2018 2021 2018 2021 15Bakken oil price strength supported by spare pipeline capacity

Enerplus Bakken oil price differential vs WTI ($/bbl)

Oil price diffs

Par with WTI

(2.15)

(3.72) (3.78) (3.98)

(5.39) Basin not expected to test egress capacity.

2022

(7.46) GUIDANCE Expect in basin differentials to trade in

(9.44) $0 - $2.00/bbl range below WTI

(12.94)

Pre-DAPL DAPL in service June 2017 COVID / OPEC related oil price shock

Significant rail utilization led to Differentials strengthened due led to reduced basin production &

1.8

Bakken oil production & takeaway(1)

wider differentials to increased pipeline egress increased spare pipeline capacity

1.6 Production forecast

1.4 based on 50 rigs

1.2 DAPL

Millions of bbl/d

1.0

Wood Mackenzie

Production

0.8 Production forecast

based on 30 rigs

0.6 Pipelines

(ex DAPL)

0.4

0.2

Rail volumes(2)

0.0

Jan-14 Jan-15 Jan-16 Jan-17 Jan-18 Jan-19 Jan-20 Jan-21 Jan-22 Jan-23 Jan-24 Jan-25 Jan-26

1) Source: North Dakota Industrial Commission (NDIC), Company estimates, Wood Mackenzie. Production is shown net of local refining demand. 16

2) Forecast rail volumes assume 175 mb/d are contracted going forward.APPENDIX

17Strong liquidity and low financial leverage

Significant liquidity Track record of low financial leverage

Liquidity position at March 31, 2022 ($ millions) Net debt to adjusted funds flow ratio(2)

Enerplus was the first North American E&P to transition its principal credit facility to a Sustainability 5-year track record of operating at or below 1x

Linked Credit Facility, incorporating ESG performance targets ND/FF ratio annually

3x

~$1,030 Net debt as at

March 31, 2022:

$572 million

2x

Cash + Undrawn

Revolving Credit Facility

Credit Facilities 1.0x

Avg. interest rate: 2.83%(1)

1x 0.9x

0.6x 0.6x 0.7x

SENIOR NOTES $278 0.4x

Avg. interest rate: 4.2%

$101 $81 $81 $21 $21

0x

Liquidity 2022 2023 2024 2025 2026 2017 2018 2019 2020 2021 Q1

2022

Undrawn Credit Facilities + Cash Senior Notes Revolving Credit Facility

1) Drawn fees are expected to be approximately 2.83% based on an underlying 3-month LIBOR rate of 1.33%.. Drawn amount is net of amortized debt issuance costs of $2MM. 18

2) See Non-GAAP & Other Financial Measures in the “Advisories”.2022 guidance

2022 ANNUAL GUIDANCE Bakken focused capital budget

2022e capital spending allocation

Capital spending (US$MM)(1) $400 - $440

Total production (Mboe/d) 96 – 101

Liquids production (Mbbl/d) 58.5 – 62.5 Williston Basin

Average production tax rate

7%

(% of net sales, before transportation) 83%

Operating expense (US$/boe) $9.75 - $10.50

Transportation expense (US$/boe) $4.15 $400-$440

MILLION

Cash G&A expense (US$/boe) $1.25

10%

$20 – $30

Current tax expense (US$MM) Marcellus

(2% - 3% of adjusted funds flow before tax(1)) 7%

Bakken oil price differential. vs WTI (US$/bbl) Par with WTI

Canada / DJ Basin

Marcellus natural gas price differential. vs NYMEX (US$/Mcf) $(0.75)

19

1) See Non-GAAP & Other Financial Measures in “Advisories”.COMMODITY HEDGING SUMMARY

Price risk management

CRUDE OIL HEDGES (WTI)(1)(2)(3)

Swaps Collars

Period Purchased

Volume Swaps Volume Sold Put Sold Call

Put

(Mbbl/d) (US$/bbl) (Mbbl/d) (US$/bbl) (US$/bbl)

(US$/bbl)

Apr 1 – Jun 30, 2022 - - 12.5 $58.00 $75.00 $87.63

Apr 1 – Dec 31, 2022 - - 17.0 $40.00 $50.00 $57.91

Jan 1 – Jun 30, 2023 - - 10.0 $60.00 $76.50 $107.38

Jan 1 – Dec 31, 2023 - - 2.0 - $5.00 $75.00

NATURAL GAS HEDGES (NYMEX)(2)

Swaps Collars

Period Volume Swaps Volume Sold Put Purchased Put Sold Call

(Mcf/d) (US$/Mcf) (Mcf/d) (US$/Mcf) (US$/Mcf) (US$/Mcf)

Apr 1 – Oct 31, 2022 40,000 $3.40 60,000 - $3.77 $4.50

1) The total average deferred premium spent on our outstanding hedges is US$1.50/bbl from April 1, 2022 – December 31, 2022 and US$1.25/bbl from January 1, 2023 – June 30, 2023.

2) Transactions with a common term have been aggregated and presented at weighted average prices and volumes.

3) Upon closing of the Bruin Acquisition, Bruin’s outstanding crude oil contracts were recorded at a fair value liability of $76.4 million. At March 31, 2022, the remaining liability was $16.3 million on the Condensed Consolidated Balance Sheets. Realized and unrealized gains

and losses on the acquired contracts are recognized in Condensed Consolidated Statement of Income/(Loss) and the Condensed Consolidated Balance Sheets to reflect changes in crude oil prices from the date of closing of the Bruin Acquisition. See Note 16 to the Interim

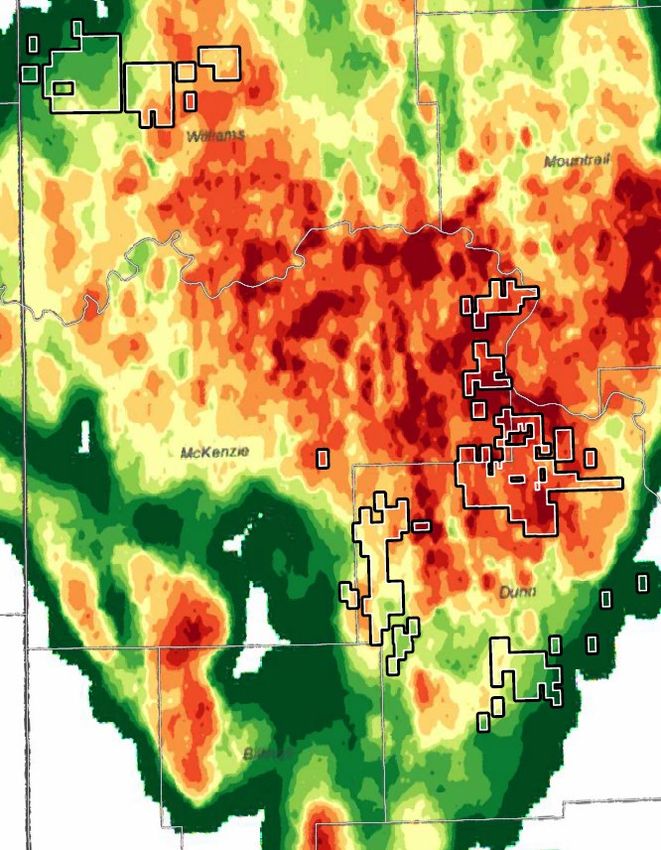

Financial Statements for further details. 20BAKKEN CORE DRILLING INVENTORY

FBIR

Expected average well performance (1) Inventory Distribution

Payout period and NPV10 at $60, $80, $100 per barrel WTI Net future drilling locations

Mountrail

300

WTI NPV10 $MM Williams

$100 $19 EXTENDED 670 FBIR

250 $80 $13 CORE

Cumulative oil production (mbbls)

$60 $7 ~110

locations McKenzie

200 $60

WTI

150 $80

WTI

$100 Billings Dunn

100

WTI

CORE

~560

Development plan

locations

50 ~10 wells per 1,280 ft. spacing unit

Payout: 6 months 60%

FBIR MB

at $80 WTI

0 TF 1

0 2 4 6 8 10 12 14 16 18 20 22 24

Month TF 2 TF2 locations in select areas

Enerplus well $50 WTI breakeven well

$60 WTI breakeven well

21

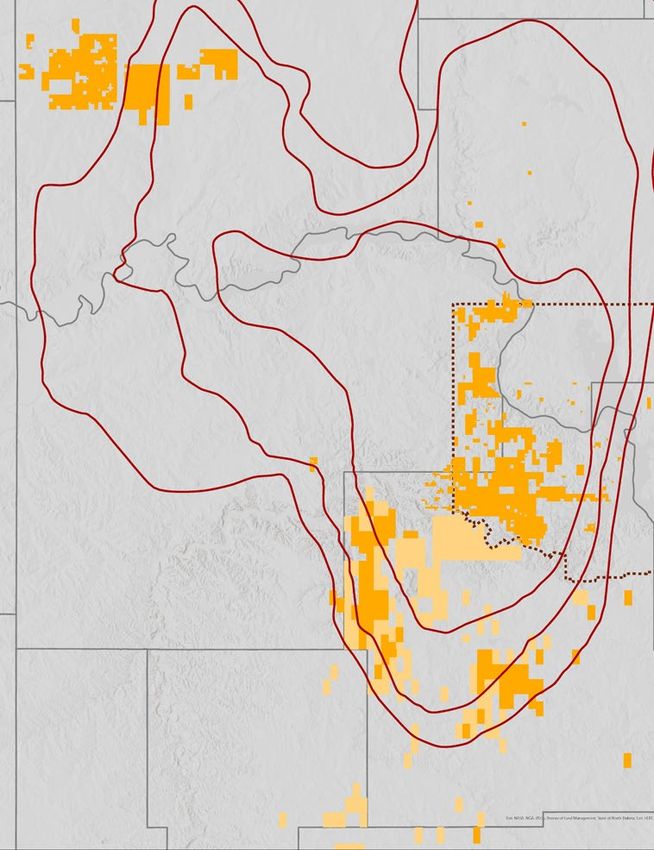

1) See “Expected well performance” in “Advisories”. Well economics at $80 & $100 WTI assume a total well cost of $6.5mm. Well economics at $60 WTI assume a total well cost of $6.0mm.BAKKEN CORE DRILLING INVENTORY

Little Knife

Expected average well performance (1) Inventory Distribution

Payout period and NPV10 at $60, $80, $100 per barrel WTI Net future drilling locations

Mountrail

300

WTI NPV10 $MM Williams

$100 $19 670

250 EXTENDED

$80 $13

CORE

Cumulative oil production (mbbls)

$60 $7 ~110 Little

200 locations McKenzie Knife

$60

$80 WTI

150

WTI 25%

$100 LITTLE KNIFE Billings Dunn

100 WTI CORE

~560 Development plan

locations ~6-9 wells per 1,280 ft. spacing unit

50

Payout: 5 months

MB

at $80 WTI

0 TF 1

0 2 4 6 8 10 12 14 16 18 20 22 24

Month TF 2

Enerplus well $50 WTI breakeven well

$60 WTI breakeven well

22

1) See “Expected well performance” in “Advisories”. Well economics at $80 & $100 WTI assume a total well cost of $6.5mm. Well economics at $60 WTI assume a total well cost of $6.0mm.BAKKEN CORE DRILLING INVENTORY

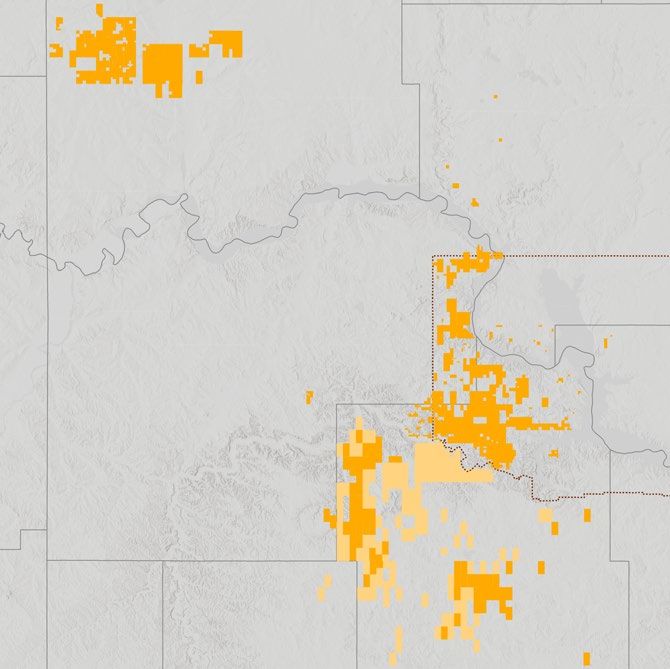

Eastern Williams

Expected average well performance (1) Inventory Distribution

Payout period at $60, $80, $100 per barrel WTI Net future drilling locations

Williams Mountrail

300

WTI NPV10 $MM Eastern

Williams

$100 $16 EXTENDED 670

250 $80 $11 CORE

Cumulative oil production (mbbls)

$60 $6 ~110

locations McKenzie

200 15%

$60

WTI E. WILLIAMS

150 $80

WTI Dunn

$100 Billings

100 WTI CORE

~560 Development plan

locations ~5-6 wells per 1,280 ft. spacing unit

50

Payout: 6 months

MB

at $80 WTI

0 TF 1

0 2 4 6 8 10 12 14 16 18 20 22 24

Month TF 2

Enerplus well $50 WTI breakeven well

$60 WTI breakeven well

23

1) See “Expected well performance” in “Advisories”. Well economics at $80 & $100 WTI assume a total well cost of $6.5mm. Well economics at $60 WTI assume a total well cost of $6.0mm.BAKKEN EXTENDED CORE DRILLING INVENTORY

Murphy Creek

Expected average well performance (1) Inventory Distribution

Payout period at $60, $80, $100 per barrel WTI Net future drilling locations

Mountrail

300

WTI NPV10 $MM Williams

$100 $11 EXTENDED 670

250 $80 $6 CORE

$60 MURPHY

Cumulative oil production (mbbls)

$60 $2 WTI ~110

CREEK

locations

200 McKenzie

$80

WTI Murphy

Creek

150 $100

WTI Dunn

Billings

100 CORE

~560 Development plan

locations ~5-6 wells per 1,280 ft. spacing unit

50

Payout: 10 months

at $80 WTI MB

0

TF 1

0 2 4 6 8 10 12 14 16 18 20 22 24

Month TF 2

$50 WTI breakeven well Enerplus well

$60 WTI breakeven well

24

1) See “Expected well performance” in “Advisories”. Well economics at $80 & $100 WTI assume a total well cost of $6.5mm. Well economics at $60 WTI assume a total well cost of $6.0mm.MARCELLUS OVERVIEW

Core acreage position in the Marcellus dry gas window

MARCELLUS POSITION – NE PENNSYLVANIA

Non-operated position in Marcellus dry gas core

− 32,700 net acres Bradford Susquehanna

− 160-170 MMcf/d production(1)

High quality exposure to robust natural gas prices

− Low cost structures Wyoming

Sullivan

− Stable production, consistent free cash flow generation

Lycoming

Marcellus production & capital spending Marcellus pricing exposure (Apr-Dec) Marcellus unhedged annual net operating income

MMcf/d and $ millions Approx. % of natural gas sales Sensitivity to NYMEX ($ millions) $320

200 18% $260

$45

$50 Leidy $200

150 $31

$25 TZ6 Non-NY

100 $0.75/Mcf $140

$25 2022e portfolio

50 Gulf Coast $80

154 158 160-170 differential below 19%

0 $0 Other 60% NYMEX

2020 2021 2022e $3.00 $4.00 $5.00 $6.00 $7.00

Production Capital 3%

NYMEX Benchmark Price (US$/Mcf)

25

1) Enerplus production, net of royalties.CANADIAN OIL WATERFLOOD PORTFOLIO

Consistent, low decline production

Assets under water or polymer flooding CANADIAN WATERFLOODS

Portfolio optimized to focus on highest return, strong ANTE CREEK

free cash flow generating assets

Low decline production GILTEDGE

− Q1 2022 production was ~5,500 BOE/d (94% oil)(1) CADOGAN Saskatchewan

MEDICINE HAT

British Columbia Alberta FREDA LAKE

Enerplus has initiated a divestment process for its Canadian assets

26

1) Production is shown on a net after deduction of royalty basis.EMERGING OPPORTUNITY – DJ BASIN

Northern extension of Wattenberg field

DJ BASIN

~34,700 net acres in NW Weld County WYOMING

− Low entry price achieved through leasing and farm-in activity COLORADO 2017/2018 - 5 wells online

(4 Codell, 1 Niobrara)

− Significant oil in place through all Niobrara benches and Codell

2019 - 5 wells online

(4 Codell, 1 Niobrara)

Well results compare favorably to core DJ oil rates

2020 - 2 wells online

(2 Codell)

Focused on enhancing well economics through further drilling

2021 – 3 wells online

& completion optimization WELD

(3 Codell)

MORGAN

ADAMS

DENVER

27Board of Directors

Hilary A. Foulkes (Director since February 2014) Mark A. Houser (Director since March 2022)

Audit & Risk Management Committee

Board Chair Compensation & Human Resources Committee

Reserves, Safety & Social Responsibility Committee

Judith D. Buie (Director since January 2020)

Audit & Risk Management Committee Susan M. MacKenzie (Director since July 2011)

Corporate Governance & Nominating Committee Compensation & Human Resources Committee (Chair)

Reserves, Safety & Social Responsibility Committee Reserves, Safety & Social Responsibility Committee

Karen E. Clarke-Whistler (Director since December 2018)

Compensation & Human Resources Committee Jeffrey W. Sheets (Director since December 2017)

Corporate Governance & Nominating Committee Audit & Risk Management Committee (Chair)

Reserves, Safety & Social Responsibility Committee Compensation & Human Resources Committee

Ian C. Dundas Sheldon B. Steeves (Director since June 2012)

Audit & Risk Management Committee

President and CEO Reserves, Safety & Social Responsibility Committee (Chair)

Robert B. Hodgins (Director since November 2007)

Compensation & Human Resources Committee

Corporate Governance & Nominating Committee (Chair)

28Advisories Assumptions All amounts in this presentation are stated in U.S. dollars unless otherwise specified. All financial information in this presentation has been prepared and presented in accordance with U.S. GAAP, except as noted below under “Non-GAAP Measures”. Barrels of Oil Equivalent and Cubic Feet of Gas Equivalent This presentation contains references to "BOE" (barrels of oil equivalent), “MBOE” (one thousand barrels of oil equivalent), and “MMBOE” (one million barrels of oil equivalent). Enerplus has adopted the standard of six thousand cubic feet of gas to one barrel of oil (6 Mcf: 1 bbl) when converting natural gas to BOEs. BOE, MBOE and MMBOE may be misleading, particularly if used in isolation. The foregoing conversion ratios are based on an energy equivalency conversion method primarily applicable at the burner tip and do not represent a value equivalency at the wellhead. Given that the value ratio based on the current price of oil as compared to natural gas is significantly different from the energy equivalent of 6:1, utilizing a conversion on a 6:1 basis may be misleading. Non-GAAP & Other Financial Measures This presentation includes references to certain non-GAAP financial measures and non-GAAP ratios used by the Company to evaluate its financial performance, financial position or cash flow. Non-GAAP financial measures are financial measures disclosed by a company that (a) depict historical or expected future financial performance, financial position or cash flow of a company, (b) with respect to their composition, exclude amounts that are included in, or include amounts that are excluded from, the composition of the most directly comparable financial measure disclosed in the primary financial statements of the company, (c) are not disclosed in the financial statements of the company and (d) are not a ratio, fraction, percentage or similar representation. Non-GAAP ratios are financial measures disclosed by a company that are in the form of a ratio, fraction, percentage or similar representation that has a non-GAAP financial measure as one or more of its components, and that are not disclosed in the financial statements of the company. These non-GAAP financial measures and non-GAAP ratios do not have standardized meanings or definitions as prescribed by U.S. GAAP and may not be comparable with the calculation of similar financial measures by other entities. Please see Management’s Discussion & Analysis for the composition of each non-GAAP measure, the identified GAAP equivalency to the extent one exists, a reconciliation of the measure to the mostly directly comparable GAAP financial measure and details on the usefulness of the measure for the reader. These non-GAAP financial measures and non-GAAP ratios should not be considered as a substitute for, or superior to, measures of financial performance prepared in accordance with GAAP. Please see “Non-GAAP Measures” in the latest MD&A for more detail. Other financial measures include supplementary financial measures and capital management measures. Supplementary financial measures are disclosed by a company that (a) are, or are intended to be, disclosed on a periodic basis to depict the historical or expected future financial performance, financial position or cash flow of a company, (b) are not disclosed in the financial statements of the company, (c) are not non-GAAP financial measures, and (d) are not non-GAAP ratios. The following section provides an explanation of the composition of those supplementary financial measures if not previously provided: (a) “Capital spending” - Capital and office expenditures, excluding other capital assets/office capital and property and land acquisitions and divestments. (b) “Cash general and administrative expenses” or “Cash G&A expenses” - General and administrative expenses that are settled through cash payout, as opposed to expenses that relate to accretion or other non-cash allocations that are recorded as part of general and administrative expenses; and (c) “Cash share-based compensation” or “Cash SBC expenses” - share-based compensation that is settled by way of cash payout, as opposed to equity settled Capital management measures are financial measures disclosed by a company that (a) are intended to enable an individual to evaluate a company’s objectives, policies and processes for managing the company's capital, (b) are not a component of a line item disclosed in the primary financial statements of the company, (c) are disclosed in the notes to the financial statements of the company, and (d) are not disclosed in the primary financial statements of the company. The following section provides an explanation of the composition of those capital management measures if not previously provided: “Net Debt” - “Net Debt” is calculated as current and long-term debt associated with senior notes plus any outstanding Bank Credit Facilities balances, less cash and cash equivalents. For further details, see Note 15 to the Interim Financial Statements. Presentation of Production and Reserves Information All production volumes presented in this presentation are reported on a "net" basis (the Company's working interest share after deduction of royalty obligations, plus the Company's royalty interests), unless expressly indicated that it is being presented on a "gross" basis. Previously, the Company presented production volumes on a "company interest" basis, which was calculated as its working interest share before deduction of royalties plus the Company's royalty interests. With these changes, production volumes presented by the Company on a "net" basis are expected to be lower than those presented historically. All reserves information presented herein are reported in accordance with Canadian reserve evaluation standards under National Instrument 51-101 – Standards of Disclosure for Oil and Gas Activities (“Canadian NI 51-101 Standards”), except certain reserves information effective December 31, 2021 in accordance with the provisions of the Financial Accounting Standards Board’s ASC Topic 932 Extractive Activities – Oil and Gas, which generally utilize definitions and estimations of proved reserves that are consistent with Rule 4-10 of Regulation S-X promulgated by the U.S. Securities and Exchange Commission (collectively, the "U.S. Rules"), but does not necessarily include all of the disclosure required by the SEC disclosure standards set forth in Subpart 1200 of Regulation S-K (the "U.S. Standards"). The practice of preparing production and reserves data under the Canadian NI 51-101 Standards differs from the U.S. Rules and the presentation of production and reserves data under the Canadian Standards differs from presentation under the U.S. Standards. Please refer to our 2021 reserves news release for further information. All references to "liquids" in this presentation include light and medium crude oil, heavy oil and tight oil (all together referred to as "crude oil") and NGLs on a combined basis. All references to "natural gas" in this presentation include conventional natural gas and shale gas on a combined basis. Enerplus’ oil and gas reserves statement for the year ended December 31, 2021, which will include complete disclosure of our oil and gas reserves and other oil and gas information prepared under the Canadian NI 51-101 Standards and also certain information about our oil and gas reserves prepared in accordance with the U.S. Rules, is contained within our Annual Information Form (AIF) for the year ended December 31, 2021 which is available on our website at www.enerplus.com and under our SEDAR profile at www.sedar.com. Additionally, our AIF forms part of our Form 40-F that is filed with the U.S. Securities and Exchange Commission and is available on EDGAR at www.sec.gov. Readers are also urged to review the Management’s Discussion & Analysis and financial statements filed on SEDAR and as part of our Form 40-F on EDGAR concurrently with this presentation for more complete disclosure on our operations. Drilling Inventory and Expected Well Performance Drilling locations associated with proved plus probable undeveloped reserves have been evaluated or reviewed by Enerplus’ independent qualified reserves evaluators in accordance with the COGE Handbook. Drilling locations associated with unrisked “best estimate” economic contingent resources in “development pending” project maturity sub-class have been evaluated by Enerplus’ independent qualified reserves evaluators, McDaniel & Associates Ltd in the case of North Dakota in accordance with the COGE Handbook. Unbooked future drilling locations are not associated with any reserves or contingent resources of Enerplus and have been identified by Enerplus and have not been audited by Enerplus’ independent qualified reserves evaluators. Existing Enerplus net locations in North Dakota as at 1 Jan 2022 are 920 and comprise 316 2P undeveloped reserves locations, 284 best estimate contingent resources locations and 320 unbooked future locations. The Enerplus expected well performance comes from analyzing historical well productivity within the geographic area outlined in the locator box on the maps on the respective slides. The data set analyzed excludes wells completed before 2016 and the Enerplus expected well is an average of our future planned inventory. Payout times and NPVs are calculated assuming a $6.5MM capital well cost. 29

Contacts

Investor Relations Contacts

Drew Mair

Manager, Investor Relations & Corporate Planning

403-298-1707

Krista Norlin

Sr. Investor Relations Analyst

403-298-4304

Email: investorrelations@enerplus.com

30You can also read