IPO First North Master Class 2021 - Webinar 3 - Nasdaq First North Premier - Deloitte

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

IPO First North Master Class 2021

Webinar 3 – Nasdaq First North Premier

Tip: Aktiver side-til-side tilstand og få en

forbedret seeroplevelse:

Aktiver side-til-side tilstand

• Gå til 'vis muligheder' øverst på din skærm

• Vælg tilstanden "side til side"

• Du skulle nu se både indhold (venstre) og

videogalleri (højre)

• Der er en glidestang i midten - du kan styre

skærmstørrelsen under sessionen

IPO First North Master Class 2021

Velkomst af Bjørn Winkler Jakobsen

Bjørn Winkler Jakobsen +45 22 20 21 06

Revisionspartner bjakobsen@deloitte.dk

Webinar 3

Bjørn er partner i vores revisionspraksis i Danmark. Bjørn har været partner

siden 2008 og har mere end 20 års erfaring som leder af danske og

Nasdaq First North Premier internationale revisions- og rådgivningsopgaver. Bjørn har over de seneste

par år været revisor og rådgiver for en række selskaber, der er blevet noteret

Dagens emner på tredje webinar: på First North i Danmark og Sverige.

• Introduktion til Nasdaq First North Premier

• Aflæggelse af regnskaber efter IFRS Bjørn er medlem af den danske ledelse af Deloitte.

• Erfaring – Rejsen mod en børsnotering på (Premier)

IPO First North Master Class 2021

Nasdaq First North Premier

Agenda

Carsten Borring +45 40 70 71 94

• Introduktion til Premier carsten.borring@nasdaq.com

Noteringschef Nasdaq

• Hvad er forskellene til First North

Carsten er ansvarlig for alle børsnoterede selskaber og investeringsfonde i

• Optagelseskrav Danmark samt børsnoteringer og har mere end 15 års erfaring med

• Opgradering fra First North til Premier børsnoterede selskaber og indgående kendskab til kapitalmarkederne.

Market setup mechanisms (Europe)

Regulated markets Main market

Operated by a market operator

Directives from EU applicable

• Prospectus directive

• Transparency directive

• Market abuse directive

MTF* markets First North

Operated by a market operator or financial

institution

No EU requirements for traded companies

*Multilateral Trading Facility

3

First North Capital raised/secondary offerings

2018 – 2021 June

2020: Sec off = 2,1 billion Euro. Capital raised in IPO = 0,9 billion Euro

2.500

2.000

1.500

EUR Millions

1.000

500

0

June 2021 stands out in a record month in Capital Raised and second best month in Secondary offerings.

Source: Economic & Statistical Research, Nasdaq Nordic

First North Growth Market 25 Leading Development Since Start

680

580

480

380

280

180

80

FN25 Index First North Index AIM100 Index OMXS Index

Source: Economic & Statistical Research

5

Benefits of a Nasdaq First North Listing

ACTIVE MARKET NORDIC ECO SYSTEM

Strong investor demand for growth companies, both among retail and Financial advisors exclusively working with smaller growth companies.

institutional investors.

CERTIFIED ADVISERS GLOBAL BRAND

Collaborates with both issuers and Nasdaq and ensures a high market quality. The Nasdaq brand brings visibility and credibility, and can potentially help listed

companies as they expand internationally.

GROWTH PARTNER ADDITIONAL SERVICES

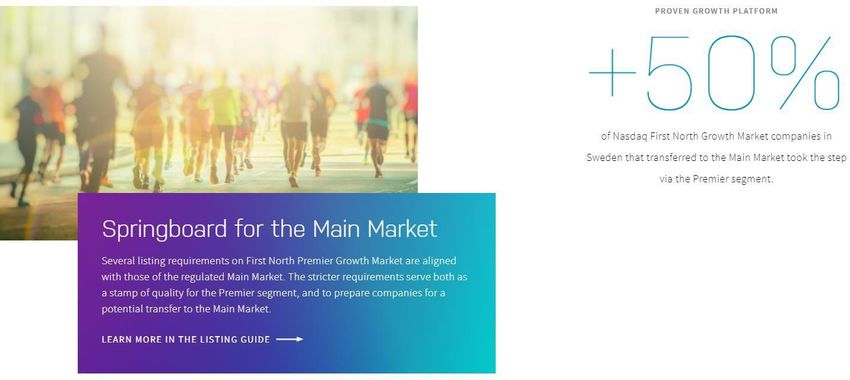

Over 100 FN companies have grown and migrated to the Main Market since 2006, Listed companies get access to our GRC solutions and Corporate Solutions suite,

most of which have taken the step via the Premier segment. including Director’s Desk and Globe Newswire.

6

7

Nasdaq Markets

Many requirements are the same on the different markets, such as competence in exchange rules,

application of MAR (Market Abuse Regulation), 12 months working capital, but there are some key differences.

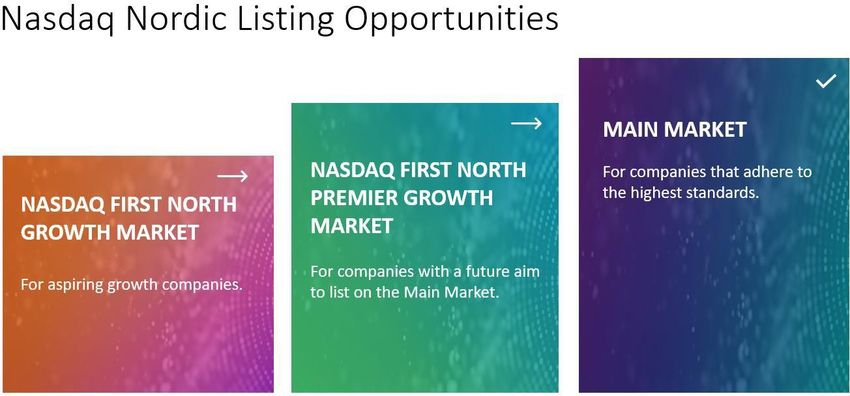

NASDAQ FIRST NORTH NASDAQ FIRST NORTH PREMIER NASDAQ

GROWTH MARKET GROWTH MARKET MAIN MARKET

FREE FLOAT 10% 25% 25%

MARKET VALUE n/a > 10 MEuro > 1 MEuro

LISTING DOCUMENT Prospectus or Company Description1) Prospectus or Company Description1) Prospectus

FINANCIAL REPORTING Local accounting standard IFRS IFRS

DISCLOSURE AND INFORMATION MAR and First North rules MAR and Main Market rules2) MAR and Main Market rules

CORPORATE GOVERNANCE CODE n/a Yes Yes

CERTIFIED ADVISER Yes Yes n/a

1) A prospectus may, however, be required according to the EU Prospectus Regulation and a company may also voluntary chose to issue a prospectus.

8 2) Premier segment issuers follow the information disclosure rules of the Main Market, and a few sections of the Nasdaq First North Growth Market Nordic

Rulebook. For comparison, see the Main Market rulebook and the First North rulebook.First North & First North Premier fast facts 2021 Q2

First North total from which

First North Premier

Market capitalization EUR 61.2 billion EUR 12.9 billion

Turnover/business day EUR 214 million EUR 42 million

Trades/business day 133 822 28 034

Average trade size EUR 1 599 EUR 1 493

Listed companies 487 71

Trading started June 2006 February 2009

80%

70% Turnover in First North Premier and

FN 25 companies of total turnover on

60% First North (%)

50%

Turnover in FN 25 companies of total

40% turnover on First North (%)

30%

20% Turnover in First North Premier

companies of total turnover on First

10% North (%)

0%

maj-17

nov-15

jan-16

mar-16

maj-16

jul-16

sep-16

nov-16

jan-17

mar-17

jul-17

sep-17

nov-17

jan-18

mar-18

maj-18

jul-18

sep-18

nov-18

jan-19

mar-19

maj-19

jul-19

sep-19

jul-20

jul-21

jan-20

sep-20

jan-21

mar-21

nov-19

mar-20

maj-20

nov-20

maj-21

Source: Economic & Statistical Research, Nasdaq Nordic 9Why First North Premier 10

Nasdaq First North Premier

12

13

Nasdaq First North Premier 14

Listing Timeline*

1 2 3 4

Company Exchange Advisor FSA

Meet your Nasdaq relation 1 3 Start-up meeting at 1 Define transaction

1

and learn about listing Exchange structure and offer

2 2 1 1st Day of Trading:

opportunities details

- Welcome Bell Ceremony at

2 the Exchange

1 Internal preparations for 1 Submit timetable 3 - Share trading starts

becoming a listed company - Press release & marketing

4 Approval of

1 Choose advisors prospectus

(legal and financial)

Preparation phase Formal listing process (3-6 months)

1 Draft prospectus + 1 Preparations:

1 Book start-up Approval of

Description of - IR website

3 meeting at the 3 how issuer meets 2 application for - Distribution setup for

exchange admission to trading

each listing Company notices and press

1 Decision to list on requirement releases

Exchange 1 Filing of prospectus and - Pre-marketing of offering

1 preliminary listing

3 application - Analyst meetings

3 Pre-Audit 3 Due Diligence - Roadshow

to FSA and Exchange

15 15

*Scenario subject to variationWE ARE IN – ARE YOU?

JOIN US!

CARSTEN BORRING

CARSTEN.BORRING@NASDAQ.COMIPO First North Master Class 2021

Aflæggelse af regnskaber efter IFRS

Agenda

Bjarne Iver Jørgensen +45 22 20 23 56

• Hvad er en IFRS Implementering? bjoergensen@deloitte.dk

IFRS Partner og specialist

• Typiske forskelle mellem IFRS og ÅRL

• Processen for en IFRS Implementering Bjarne er partner og leder vores regnskabsrådgivning i Danmark. Bjarne har over

15 års erfaring med danske og internationale revisions- og rådgivningsopgaver.

Bjarne har over de seneste år bistået en række danske vækstvirksomheder med

rådgivning om og konvertering til de internationale regnskabsregler (IFRS) i

forbindelse med notering på First North Premier i Danmark og Sverige.IPO First North Master Class 2021

Initial GAAP Analysis

20IPO First North Master Class 2021

Conversion from Danish GAAP to IFRS – Overview of the four phases of the GAAP convertion

GAAP Analysis IFRS 1

In many instances assets and IFRS 1 determines how an entity for the

liabilities are recognised and first time adopts IFRS.

measured according to the

same principles. The standard contains a main rule,

from which there are certain optional and

However, within some areas mandatory exceptions.

IFRS has detailed and specific

requirements to the accounting

treatment and in other areas

different recognition criteria.

Accounting model

Opening IFRS balances IFRS has less strict presentation requirements

Any monetary effects derived compared to the Danish Financial Statements Act

from the transition is which gives the opportunity to prepare a more

recognised in equity on theme based annual report.

transition date. This date

should be determined early in On the other hand, IFRS contains

the process. Comprehensive disclosure requirements that may

be time consuming to prepare.

21IPO First North Master Class 2021

IFRS adoption timeline – First-time adopters are required to comply with all IFRSs effective at the reporting date

2020 2021 2022

1 January 2020 31 December 2020 31 December 2021

Transition date Danish GAAP reporting First IFRS financial

period ends statements with comparatives for 2020

IFRSs effective at 31 December 2021

are applied retrospectively

22IPO First North Master Class 2021

Key differences

RECOGNITION AND MEASUREMENT

IFRS

• According to IFRS, revenue must be recognised under different criteria than DK GAAP – that is why an analysis of the following must be made:

• How are the contracts organised? Are there any long-term contracts with many different services? Are variable items included in the consideration etc.?

REVENUE RECOGNITION • IFRS requires the use of a five-step model where recognition of revenue is based on the transfer of control of the goods or services transferred to the customer.

• IFRS requires capitalization of sales provision etc. if it is directly attributable to the sales contract.

• According to IFRS 16 all leases must as a main rule be recognised in the balance sheet

• Right-of-use assets are required to be recognised in the balance sheet and amortised over the shortest of the economical life time or the contractual lifetime.

LEASING • Lease liabilities are required to be recognised in the balance sheet at the net present value of the liability.

• Short-term leases under 12 months and low-value leases (IPO First North Master Class 2021

Key differences – continued

RECOGNITION AND MEASUREMENT

IFRS

• Any identifiable asset or liability meeting the definition of an asset or a liability must be recognized as separate assets and liabilities in the pre-acquisition balance sheet.

• Separate recognition of identifiable acquired intangible assets and contingent liabilities

BUSINESS COMBINATIONS • Contingent consideration, such as earn-out agreements, is required recognised at the acquisition-date measured at fair value (contingent liabilities?)

• IFRS allows a first-time adopter to not apply IFRS to business combinations occurred before the date of transition I.e. Goodwill is recognized at carrying amount on transition

date adjusted for impairment.

• In accordance with IFRS, amortisation of goodwill is not allowed and, therefore, amortisation should be reversed at transition.

GOODWILL

• Impairment test is to be prepared at least annually.

• Under IFRS, financial liabilities are derecognised if the derecognition criteria are met (e.g. extinguishment).

• IFRS requires derecognition of a loan, if the NPV of the cash flows under the new liability is at least 10 % different from the NPV of the remaining cash flows of the existing liability.

FINANCING • Every adjustment to the loan conditions will have an impact on P&L.

• Some compound instruments have both a liability and an equity component. In that case, IFRS requires that the component parts be accounted for and presented separately

according to their substance based on the definitions of liability and equity.

24IPO First North Master Class 2021

Key differences – continued

PRESENTATION AND DISCLOSURE REQUIREMENTS

IN GENERAL, IFRS IS MUCH MORE DETAILED THAN DK GAAP (SEE THE INCOMPLETE LIST BELOW)

IFRS

• Requirement of disclosure of right-of-use assets separately.

LEASING • Requirement of disclosure of lease liabilities.

• Comprehensive requirements of note disclosures of first-time application of IFRS 16. e.g. weighted average incremental borrowing rate used, applied exemptions etc.

• Comprehensive note disclosure requirements regarding all related party transactions.

RELATED PARTY

• IFRS requires, as a minimum, disclosure of the amount, the amount outstanding including commitments, provisions for doubtful debts and expense recognised.

TRANSACTIONS

• Disclosure requirements regarding compensation of key management personnel.

FINANCIAL • Comprehensive note disclosure requirements regarding credit risk, fair value, market risks, sensitivity analysis etc.

INSTRUMENTS • Disclosure requirements regarding risk management policies and potential hedging activities.

CASHFLOW • IFRS requires disclosure of changes in liabilities arising from financing activities, which include IFRS 16 effects

STATEMENT • Non-cash items may not affect the cash-flow statement

• Comprehensive disclosure requirements of at least:

• three statements of financial position

• two statements of profit or loss and other comprehensive income

FIRST TIME

• two statements of cash flows

ADOPTION • two statements of changes in equity and related notes

• comparative information for all statements

• Reconciliation of IFRS and applied GAAP

Share based • Detailed description of the programme, cost recognised during the year, recognised liabilities, methods applied for fair valuation 25

paymentIPO First North Master Class 2021

Indicative Plan

26IPO First North Master Class 2021

IFRS Conversion – Conversion and implementation phases

STEPS SUBPHASES

1 Planning

Initial

scoping

Initial identification

of GAAP differences

Materiality

Scoping of

entities

Insignificant GAAP

2 Detailed analysis Significant GAAP differences

differences

Data collection and preliminary

3 Revenue analyses

Data validation Compliance

Data collection and Estimation of effect on

4 Leases preliminary analyses the financial statements

Data collection and

5 Share based payment preliminary analyses

Accounting impact

Conversion of opening balance Conversion of balance

6 Conversion

1 Jan 2020 31 Dec 2020

2021 IFRS figures

Preparation of financial Model financial Preparation of annual

7 statements Statement and checklists report 2021

Annual report &

8 audit

documentation

Audit documentation Signing

Project stream initiation

27IPO First North Master Class 2021

Interim Reporting

28IPO First North Master Class 2021

Requirements to financial reporting when listed on First North Premier Growth

IAS 34 | Interim Financial Reporting

• According to ‘Delårsrapportbekendtgørelsen’, listed entities are required to prepare an interim financial report for the first 6 months of each financial year according to IFRS. It is optional for

Accounting regulation

the executive management to prepare quarterly reports.

Complete or condensed • It is optional for the executive management whether they want to prepare a complete or condensed set of financial statements.

• IAS 34 describes the minimum content of an interim financial report and the recognition and measurement principles for an interim financial report:

a) Balance sheet as of the end of the current interim period and a comparative balance sheet as of the end of the immediately preceding financial year.

Content of the Interim Financial b) Statement of comprehensive income or a condensed statement of comprehensive income and a condensed income statement for the immediately preceding financial year.

Report c) Statement of changes in equity year to date with comparison figures for the same period last year.

d) Statement of cash flows cumulatively for the current financial year to date, with a comparative statement for the comparable year-to-date period of the immediately preceding financial year.

e) Selected explanatory notes, not excepting required is segment information, revenue from specified categories as required in IFRS 15 and disclosure of mergers and discontinued operations.

Significant events and • The explanatory notes required are designed to provide an explanation of events and transactions that are significant to an understanding of the changes in financial position and performance

transactions of the entity since the last annual reporting date.

• The management report must comment on all of the interim report, regardless of the company publishing an optional statement for the first quarter.

Management report

• The management report must comment on the development of the Group’s activities, results, equity and stress specific circumstances.

Adjustment of fair value • The management must evaluate if the fair value of assets and liabilities is unchanged compared to the latest financial report. If there are changes, this are to be included in the interim report.

Performance of impairment test • The management must evaluate if there are indications as to whether an impairment need exists.IPO First North Master Class 2021

Erfaring – Rejsen mod en børsnotering på Premier

Agenda

Michael Gram Hansen +45 53 74 09 00

• Valg af børsnotering på Nasdaq Premier mg@mapspeople.com

CEO & Founder MapsPeople

• Processen/erfaringer MapsPeople har gjort sig på noteringsrejsen

• Perspektiver på livet som en børsnoteret virksomhed på First North Premier Michael Gram er CEO og medejer af virksomheden MapsPeople.

Han har været hos MapsPeople siden 1997 og har været i spidsen for hvor

• Læringspunkter for børsnoteringsrejsen (dos and donts) børsnoteret MapsPeople er i dag. MapsPeople er Google partner, og en SaaS-

virksomhed som vækster flot og ambitionen er at blive markedsleder indenfor

´Indoor mapping´.IPO

Nasdaq First North Premier Growth Market

1MapsPeople’s revenue streams – MapsIndoors is the future

M apsIndoors Platform Google M aps Other subscriptions

67% 22% 11%

IPO ARR split IPO ARR split IPO ARR splitStatus Pre IPO

Business

Tech // BtB // SaaS

Performance

ARR 30m DKK ($5m)

120% average Y-on-Y growth (2018-2020)

370 customers in 40 countries

6% churn

Ambition

Indoor mapping market leader

+85% Y-on-Y growth (2021-2023)

Challenge

Funding of growth journey 300m DKK

Valuation

85m DKK

OfferFirst North Premier Growth Market

Venture Capital vs Stock Market

● Structured funding

● Control

● Visibility

● BrandingFirst North Premier Growth Market

Venture Capital vs Stock Market

● Structured funding

● Control

● Visibility

● Branding

Denmark vs alternatives

● Company registration address

● Level of knowledge

● Advisor experience

● Networking and communicationFirst North Premier Growth Market

Venture Capital vs Stock Market

● Structured funding

● Control

● Visibility

● Branding

Denmark vs alternatives

● Company registration address

● Level of knowledge

● Advisor experience

● Networking and communication

Nasdaq First North - Premier or not

● Display maturity

● Transparency

● Ambition for main marketFirst North Premier Growth Market

First North Premier Growth Market

IPO process

Marketplace (Nasdaq)

Auditor (Deloitte) Supervisory authority (Finanstilsynet)

PR Agency (MindShare)

Lawyer (Elmann)

Certified Advisor (Grant Thornton)

Trading platform (Nordnet) Media distribution (Cision)

Issuing bank (Danske Bank) IR Tools & Services (Q4)

Financial infrastructure (VP Securities) Cornerstone Investors (BankInvest)IPO process

Financials IFRS

Corp. finance Preparations - data collection, business plan

Prospectus

4 round of approval - Nasdaq // Finanstilsynet

Investor Presentation

Pre subscription // cornerstone investors

Subscription period // Investor Presentations

Legal Due diligence

Warrants

Corporate Governance Code

Issuing Bank Booking ressources

Communication Investor Relation

Internal knowledgeGoing forward

Investments Market expansion Partners, customer success, Asia

Marketing Direct, partners

Platform development Automation, AI, Live data

Guidance ARR

IR Investor communication

Staff 2020 65

2021 100

2022 135Learnings

● Solid traction

● High quality data is crucial

● Reserve a minimum of 6-7 months for the process

● Consider the necessity of Premier (IFRS)

● Clarify warrants well in advance

● The choice of Certified Advisor is crucial

● Run processes in parallel

● Prepare aftermarket activities well in advanceThanks

13You can also read