Key events & developments in 2018 - CommSec

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Economics | January 2 2019

Year in Review 2018; Year in Preview 2019

Key events & developments in 2018

The US-China trade dispute dominated investor attention over 2018. Other issues in focus over the

year included: Brexit; the US-Canada-Mexico trade negotiations and eventual deal; debate over

“neutral” interest rates in the US; rising, and then falling oil prices; personnel changes in the US White

House; US Mid-term elections; the shape of the US yield curve and implications for the economy;

Australian political instability; falls in Sydney and Melbourne home prices.

The global economy likely grew by 3.7 per cent in 2018, just above longer-term averages.

The Chinese economy softened under the weight of the tariff war with the US.

The US unemployment rate fell to a 49-year low of 3.7 per cent.

The US Federal Reserve lifted the federal funds rate from a range of 1.25-1.50 per cent to 2.25-2.50

per cent - the ninth increase in interest rates of the current monetary policy tightening cycle.

The Australian economy likely grew by 2.8 per cent over 2018, above the 2.6 per cent decade average.

National home prices fell by 4.8 per cent in 2018 after rising by 4.5 per cent in 2017. The decline in

national home prices has been driven by lower Sydney and Melbourne prices.

The Reserve Bank left the cash rate at 1.50 per cent over 2018.

The budget deficit continued to improve with the rolling annual deficit at $1,816 million in the year to

November (less than 0.2 per cent of GDP).

The Australian dollar eased from highs of US81.35 cents in January to US70.18 cents in October and

ended the year at 70.58 cents, down by 9.5 per cent.

The CRB futures commodity index declined by 12.4 per cent in 2018.

The Nymex oil price began the year at US$60.42 a barrel, hit highs of US76.90/barrel in October and hit

lows of US$42.53/barrel in December. The Nymex finished the year at US$45.41/barrel, down by

almost 25 per cent.

The Australian ASX 200 began the year at 6065.1 points; hit highs of 6373.5 in August; and bottomed

at 5467.6 in December. The ASX 200 was down 6.9 per cent over 2018 - its worst year since 2011.

The US Dow Jones index fell by 5.6 per cent over 2018 – its worst yearly performance since the Global

Financial Crisis. It was last at record highs on October 3.

Returns on Australian 10-year government bonds rose by 3.3 per cent in 2018.

Craig James – Chief Economist

(02) 9118 1806 (work); 0419 695 082 (mobile), | craig.james@cba.com.au; Twitter: @CommSec

Ryan Felsman – Senior Economist

(02) 9118 1805 (work); 0457 524 482 (mobile), | ryan.felsman@cba.com.au; Twitter: @CommSec

Produced by Commonwealth Research based on information available at the time of publishing. We believe that the information in this report is correct and any opinions, conclusions or

recommendations are reasonably held or made as at the time of its compilation, but no warranty is made as to accuracy, reliability or completeness. To the extent permitted by law, neither

Commonwealth Bank of Australia ABN 48 123 123 124 nor any of its subsidiaries accept liability to any person for loss or damage arising from the use of this report.

The report has been prepared without taking account of the objectives, financial situation or needs of any particular individual. For this reason, any individual should, before acting on the information

in this report, consider the appropriateness of the information, having regard to the individual’s objectives, financial situation and needs and, if necessary, seek appropriate professional advice. In the

case of certain securities Commonwealth Bank of Australia is or may be the only market maker.

This report is approved and distributed in Australia by Commonwealth Securities Limited ABN 60 067 254 399 a wholly owned but not guaranteed subsidiary of Commonwealth Bank of Australia.

This report is approved and distributed in the UK by Commonwealth Bank of Australia incorporated in Australia with limited liability. Registered in England No. BR250 and regulated in the UK by the

Financial Services Authority (FSA). This report does not purport to be a complete statement or summary. For the purpose of the FSA rules, this report and related services are not intended for

private customers and are not available to them.

Commonwealth Bank of Australia and its subsidiaries have effected or may effect transactions for their own account in any investments or related investments referred to in this report.

Economic Insights: Year in Review 2018; Year in Preview 2019

International

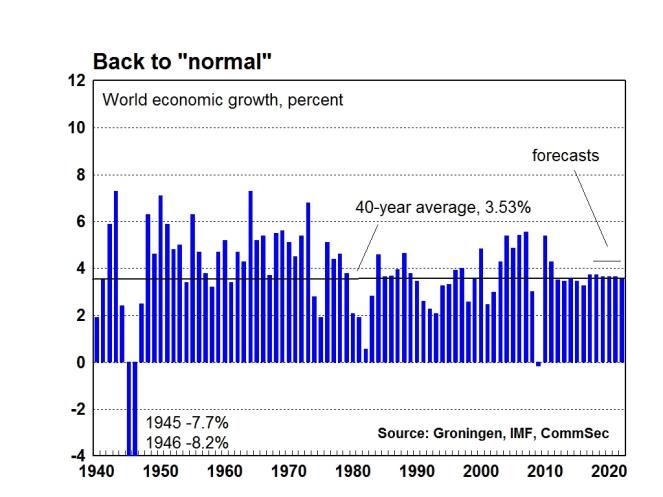

The International Monetary Fund currently expects the global economy to grow by 3.7 per cent in both

2018 and 2019, a similar outcome to 2017. The 30-year average is 3.6 per cent while the 50-year

average is around 3.7 per cent. The growth rates for 2018 and 2019 were both revised lower by 0.2

percentage points in October from the projections made in April 2018.

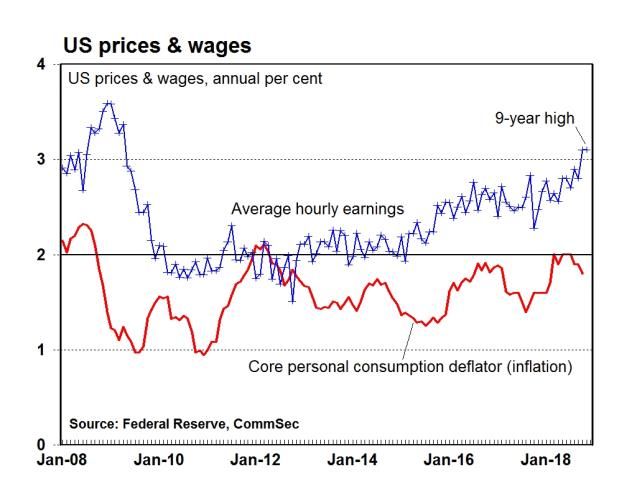

The IMF expects the US economy to slow from a three-year high of 2.9 per cent in 2018 to 2.5 per cent

in 2019. The US unemployment rate remains at a 49-year low of 3.7 per cent. But inflation remains low,

near 2 per cent, while wages were up by just 3.1 per cent over the year – the highest in 9 years.

Euro area growth is tipped at 2 per cent in 2018 and 1.9 per cent in 2019 although the European

Central Bank now tips 1.7 per cent growth. The IMF expects Japanese growth of 1.1 per cent in 2018

and 0.9 per cent in 2019.

The Chinese economy grew at a 6.5 per cent annual rate in the September quarter, down from 6.7 per

cent in the June quarter. It was the slowest annual growth rate in 9½ years.

The IMF expects that the Chinese economy grew by 6.6 per cent over the full 2018 year. And growth is

tipped to slow further to 6.2 per cent in 2019. In part the slowdown in growth reflects the maturation of

the economy and its transition from an “emerging” nation to an “advanced” economy. Chinese

economic growth still contributes accounts for around a third of total global growth.

Resolution of the US-China trade dispute is the key factor likely to influence global economic growth

over 2019. The other key issue is US monetary policy. A number of US recessions in recent decades

have occurred due to policy ‘mistakes’ – lifting interest rates too quickly or leaving rates too high in the

face of a weakening economy.

January 2 2019 2

Economic Insights: Year in Review 2018; Year in Preview 2019

Australian economy

The Australian economy grew by 2.8 per cent for the year to September. Over 2018 as a whole, growth

is likely to be around 2.8 per cent, up from 2.4 per cent in 2017. Growth has averaged 2.6 per cent over

the decade and averaged 2.9 per cent over the last 15 years.

While employment has been strong, productivity growth is soft with a key measure up by just 0.4 per

cent over the year.

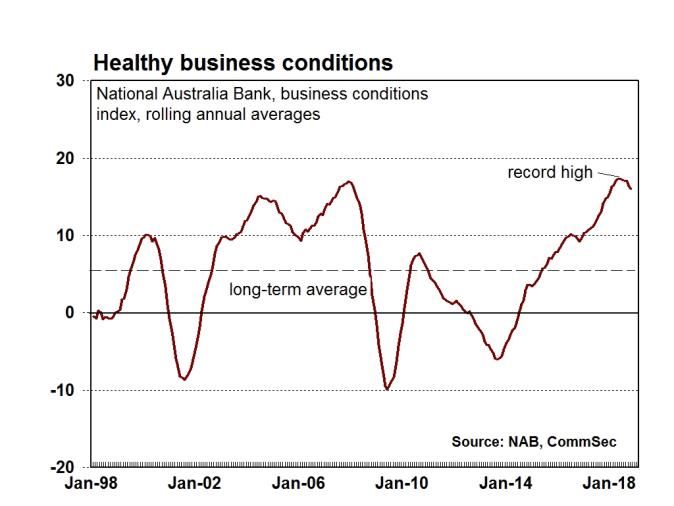

Business conditions remain good. The NAB business conditions index stood at +12.7 points in

November. The long-term average is +6.0 points. The rolling annual average business conditions index

was +16.1 points in November, modestly below the record high of +17.3 points in June. Profits are at

record highs. And the upgrade in investment plans in the September quarter was the biggest in 19

years.

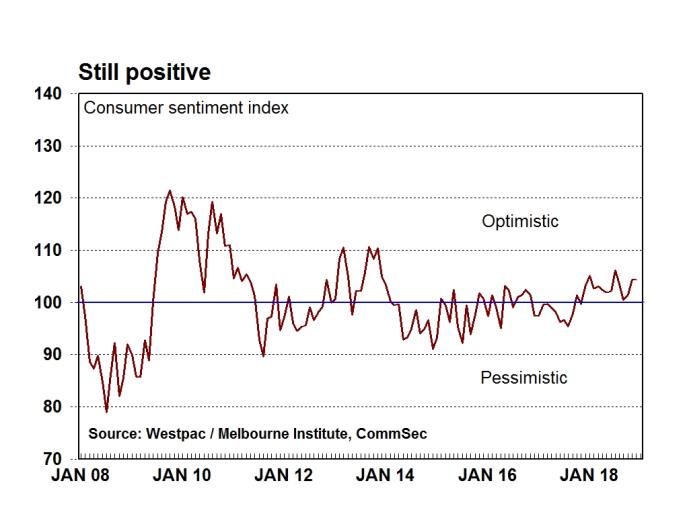

Consumers remain positive. The Westpac/Melbourne Institute survey of consumer sentiment index

stood at 104.4 in December. The sentiment index is above its long-term average of 101.3. A reading

above 100 denotes optimism.

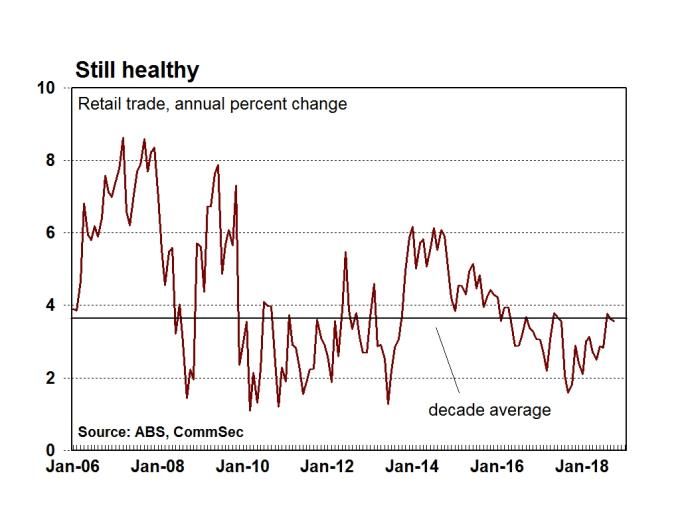

Consumers continue to spend. Retail trade rose by 3.6 per cent in the year to October, close to the 10-

year average of 3.7 per cent. In real terms, broader household consumption was up by 2.5 per cent in

real terms to the September quarter (decade average 2.6 per cent.)

The trade accounts are in surplus. In October the trade surplus was $2,316 million and the rolling

annual surplus rose from $13.69 billion to $15.29 billion – the highest level in 11 months. Annual

exports to China hit record highs of $112.2 billion in October, up 10.3 per cent over the year.

In the twelve months to November 2018, the Budget deficit stood at $1,816 million (less than 0.2 per

cent of GDP) and down from the $2,345 million deficit in the year to October. The rolling annual deficit

is the lowest for over 9½ years. Over the same 12-month period to November, the fiscal balance was in

surplus by $5.124 billion.

January 2 2019 3

Economic Insights: Year in Review 2018; Year in Preview 2019

Inflation, jobs and wages

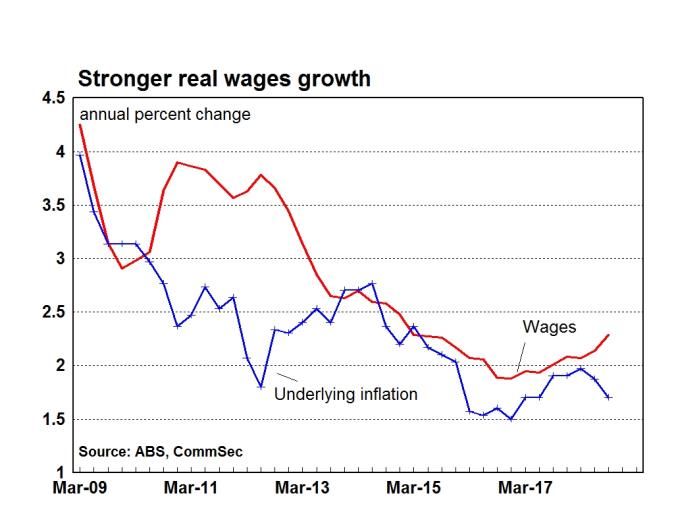

Inflation remains low. In the September quarter the annual rate of headline inflation eased from 2.1 per

cent to 1.9 per cent. Over the past decade inflation has averaged 2.18 per cent – the lowest decade-

average inflation result since September quarter 1967.

“Underlying” inflation is also low on an annual basis. The average of the weighted median and trimmed

mean measures stands at 1.75 per cent.

Wage growth is slowly lifting. The wage price index rose by 0.6 per cent in the September quarter.

Annual wage growth lifted from 2.1 per cent to a 3½-year high of 2.3 per cent. Including bonuses,

wages were up by 2.7 per cent on a year ago. But employers are preferring to modestly increase their

labour costs via alternatives to base pay, such as gym memberships and flexible working

arrangements.

The job market improved over the year. In trend terms the jobless rate fell to a 6½-year low of 5.1 per

cent in November.

Annual job growth currently stands at 2.3 per cent (decade average 1.6 per cent) with 285,800 jobs

created over the year to November. Hours worked lifted by 1.1 per cent. The monthly trend

underemployment rate fell to 3½-year lows of 8.4 per cent. The monthly trend underutilisation rate fell to

4½-year lows of 13.5 per cent. While an improvement, still-high underemployment (people wanting to

work more hours) and strong population growth suggest that there is still some spare capacity in the

labour market.

The NSW unemployment rate stood at 4.4 per cent in November while the Victorian jobless rate stood

at 4.6 per cent. Both jobless rates were near the lowest in a decade.

January 2 2019 4

Economic Insights: Year in Review 2018; Year in Preview 2019

Housing

Home prices are easing, especially in Sydney and Melbourne, as the supply of homes lifts to meet the

level of demand. The CoreLogic Home Value Index of capital city home prices fell by 1.3 per cent in

December to stand 6.1 per cent lower over the year. The national home price index fell by 1.1 per cent

in the month to be down 4.8 per cent over the year – the worst annual decline in a decade.

In capital cities, house prices fell by 1.4 per cent in December and apartment prices fell by 1.1 per cent.

House prices were down 6.7 per cent on a year ago and apartments were down by 4.3 per cent.

Home prices were higher than a year ago in four of the eight capital cities in December. Prices

rose most in Hobart (up 8.7 per cent), followed by Canberra (up 3.3 per cent), Adelaide (up 1.3 per

cent) and Brisbane (up 0.2 per cent). But prices fell in Sydney (down by 8.9 per cent); Melbourne (down

7.0 per cent); Perth (down 4.7 per cent) and Darwin (down by 1.5 per cent).

Total returns on national dwellings fell by 1.2 per cent in the year to December with houses down by 1.8

per cent on a year earlier, but units were up 0.4 per cent.

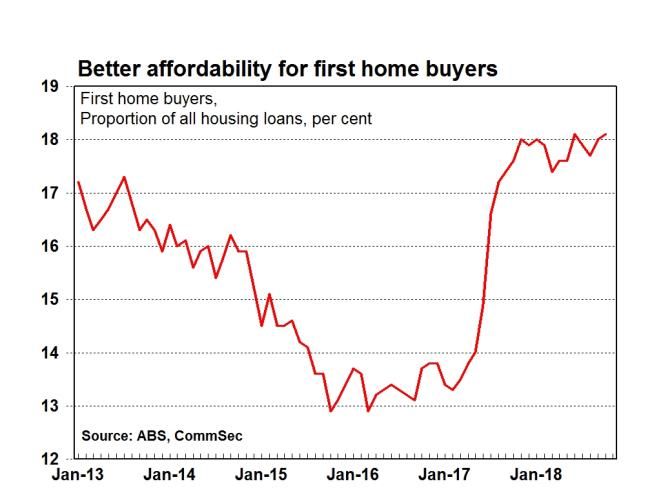

In response to lower prices, demand for properties is rising, especially from first home buyers. The

number of loans (commitments) by home owners (owner-occupiers) rose by 2.2 per cent in October -

the largest gain in 15 months. And the proportion of first-time buyers in the home loan market rose from

18.0 per cent in September to 6-year highs of 18.1 per cent in October (decade-average 17.7 per cent).

Construction activity remains solid. In the year to September, construction work done was at record

highs in NSW, Victoria and South Australia. While engineering continues to ease with the easing in

mining work, Non-residential was up by 2.3 per cent on the year. Residential building was up by 5.4 per

cent over the year.

There is a record amount of private sector infrastructure projects under construction, a key factor that

will support economic activity over 2019.

January 2 2019 5

Economic Insights: Year in Review 2018; Year in Preview 2019

International financial markets

Over 2018, the US Federal Reserve lifted the federal funds rate from a range of 1.25-1.50 per cent to

2.25-2.50 per cent – the ninth increase in interest rates of the current monetary policy tightening cycle.

The gap between US 10-year yields and US 2-year yields (measure of the yield curve) was the flattest

since 2007, closing the year at 19 points. US 10-year yields stood at 2.69 per cent (up by 28 points)

with US 2-year yields up by 61 points to near US 2.50 per cent in 2018. The flat yield curve has caused

some investors to fret that a slowdown of the US economy may lie ahead or even a recession. But if

history is any guide, it takes on average 21 months for the economy to slow down significantly after the

curve inverts and 14 months for the US sharemarket to go into reverse.

But while short-term interest rates have lifted over time, it has to be remembered that they have lifted

from essentially zero. Longer-term bonds have been supported by global uncertainties such as the US-

China trade dispute as well as the low level of inflation. Inflation has remained remarkably contained

despite solid economic growth and tight job markets.

Global sharemarkets. The world index (MSCI – Morgan Stanley Capital International index) hit a

record high of 2,248.9 in late January. But by late December 2018 the world MSCI fell to 1,835.7. The

world index fell by 10.3 per cent over 2018.

Only 15 of 73 major sharemarkets posted gains over 2018 (Australia was 42nd). Amongst the best

was Ukraine (up 77.5 per cent). Among the worst was China (down 24.6 per cent).

In 2018, global sharemarkets recorded their worst annual performance since the Global Financial

Crisis. The US Dow Jones (down 5.6 per cent), S&P500 (down 6.5 per cent) and Nasdaq (down 3.9 per

cent) indexes all fell. In Europe, Germany’s Dax (down 18.3 per cent) and the UK FTSE (down 12.5 per

cent) bourses tumbled. In Asia, Japan’s Nikkei fell by 12.1 per cent and the Australian ASX200 index

was down 6.9 per cent – its worst year since 2011 – and the All Ordinaries fell by 7.4 per cent.

Global currencies weakened against the US dollar over 2018. Only nine of 120 currencies rose against

the greenback over the year (Australia 104th or 17th biggest decline.) Strongest was the Japanese yen

(up 3.3 per cent). The US dollar index ended 2018 near a 19-month high.

January 2 2019 6

Economic Insights: Year in Review 2018; Year in Preview 2019

Commodity prices

The CRB futures commodity index declined by 12.4 per cent in 2018, more than the 9.5 per cent

decline in the Aussie dollar.

Commodities have been caught in the Sino-US trade crossfire, despite supply-demand fundamentals

remaining bright for late-cycle commodities like copper. While weakening global trade flows and

demand are headwinds, likely Chinese infrastructure stimulus could propel metals higher. US shale

remains the ‘wildcard’ for oil markets, despite OPEC attempts to stabilise the crude price.

Base metal prices eased over 2018 with the London Metal Exchange index down by 18 per cent – its

first annual decline in three years. Copper, aluminium, zinc and nickel fell between 16 and 26 percent.

Iron ore hit the year’s highs of US$79.95 a tonne in late February but softened with equities market

volatility over March and April. After again rallying to around US$77 a tonne in late October/ early

November, iron ore eased again late in the year. Iron ore finished 2018 at US$72.70 a tonne, down just

0.3 per cent on the year.

US Nymex crude began the year around US$60 a barrel. Over the first quarter, crude prices were

relatively settled, broadly holding US$60-65 a barrel. But prices motored to US$74 in the second

quarter and to near 4-year highs in early October. But since early October, crude oil prices slumped by

more than 40 per cent. Nymex ended the year at US$45.41 a barrel, down by almost 25 per cent.

Thermal coal prices remained firm over 2018 and were up 0.8 per cent. And the gold price held

between US$1,184-1,363 an ounce over 2018, although finishing the year down 1.8 per cent at

US$1281.30 an ounce.

Across rural commodities, wheat recorded one of the strongest gains in 2018, up by 19.8 per cent over

the year. Wool lifted 5.8 per cent over the year while cotton fell 9.8 per cent with the beef price down

3.7 per cent and sugar down 20.6 per cent.

January 2 2019 7

Economic Insights: Year in Review 2018; Year in Preview 2019

Interest rates & exchange rates

The Reserve Bank left the cash rate at 1.50 per cent over 2018. In fact the Reserve Bank hasn’t

changed the cash rate for 28 consecutive months. The last move was a rate cut in August 2016, with

the Reserve Bank cutting the cash rate from 1.75 per cent to a record low – an emergency level – of

1.50 per cent.

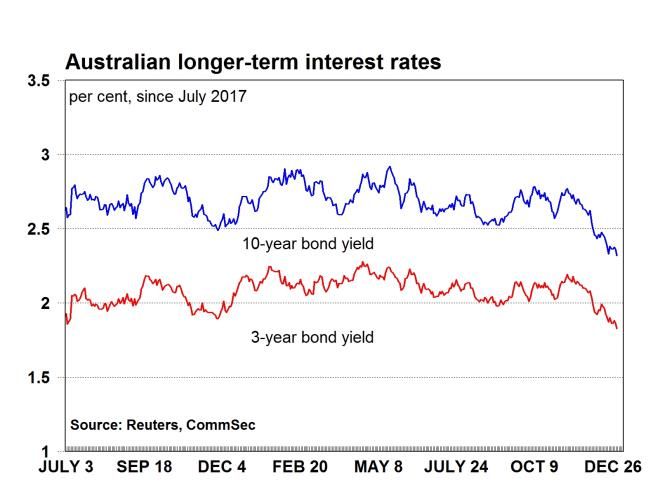

Ninety-day bank bill yields continue to hold above the 1.5 per cent cash rate. Ninety-day bills held

between 1.76-2.12 per cent over 2018 and yields are currently near 2.08 per cent – not far below 2-year

highs. Rising international interest rates have increased bank borrowing costs, pressuring margins and

resulting in out-of-cycle variable mortgage rate increases.

At the other end of the yield curve, 10-year bond yields held between 2.32-2.92 per cent over 2018.

Yields peaked in mid-May but eased in the latter months of 2018. Low inflation, weaker global equities

markets and on-going global uncertainties such as the US-China trade dispute have provided support

for safe-haven government bonds. Yields on 10-year bonds ended 2018 at the year’s lows, down 35

points or up 3.3 per cent.

The Australian dollar eased from highs of US81.35 cents in January to US70.18 cents in October and

ended the year at 70.58 cents, down by 9.5 per cent.

Over the year the Aussie tracked a range of just over 11 cents. While up from the 11-year low of 9.64

cents in 2017, it remained below the 30-year average of 13.7 cents.

While commodity prices eased over 2018, the major factor driving the Aussie dollar lower over the year

was rising US interest rates.

January 2 2019 8

Economic Insights: Year in Review 2018; Year in Preview 2019

Australian shares, bonds, cash

The Australian ASX 200 began the year at 6065.1 points; hit highs of 6373.5 in August; and bottomed

at 5467.6 in December. The ASX 200 was down 6.9 per cent over 2018 - its worst year since 2011. The

broader All Ordinaries index fell by 7.4 per cent.

Total returns on Australian shares as judged by the All Ordinaries Accumulation index hit record highs

in late August but eased to 15-month lows in December. The accumulation index fell by 3.5 per cent

over 2018.

Returns on Australian government bonds rose by 3.3 per cent over 2008 while cash was 1.5 per cent

(with bank term deposits slightly higher).

The MSCI (Morgan Stanley Capital International index) for Australia in US dollar terms fell by 15.8 per

cent in 2018.

Only four of the 22 industry groups lifted over 2018: Pharmaceuticals, Biotech & Life Sciences (up 31.4

per cent); Software & services (up 5.5 per cent); Food, Beverages & tobacco (up 2.0 per cent) and

Food & staples retailing (up 1.1 per cent). The biggest fall was recorded by Household & Personal

Products (down 26.7 per cent); from Telecom (down 17.4 per cent); and Banks (down 15.5 per cent).

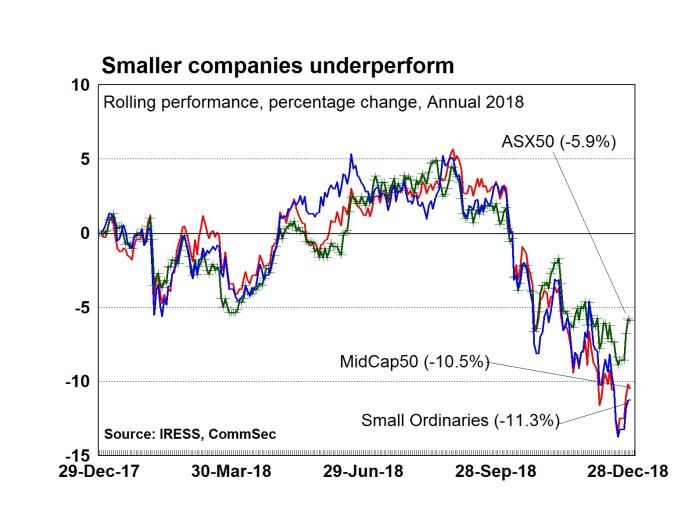

Larger companies out-performed. The ASX 50 index fell 5.9 per cent in 2018; from ASX 100 (down

6.5 percent); ASX 200 (down 6.9 per cent); MidCap 50 (down 10.5 per cent) and Small Ordinaries

(down 11.3 per cent).

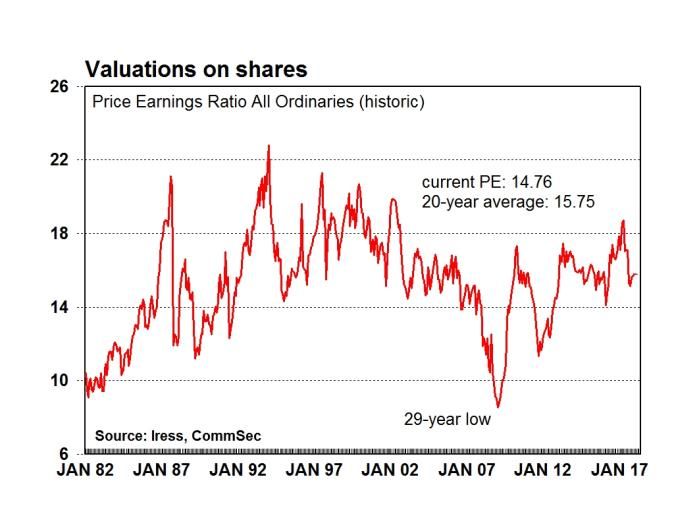

Valuations. The historic price-earnings ratio stands at a 32-month low of 14.76, well down on the 5-

year average of 16.1 and decade average of 15.1. The average dividend yield stands at a 29-month

high of 4.31 per cent.

January 2 2019 9

Economic Insights: Year in Review 2018; Year in Preview 2019

Outlook for 2019

Much is riding on the resolution of the US-China

trade dispute. Hopes are increasing after China

FORECASTS

2017/18 2018/19

removed its “Made in China 2025” technology-

Economic Growth 2.8% 3.00-3.50%

focused industrial policy from its local

Underlying inflation 1.9% 2.00-2.50%

government priority list for 2019. And China has Unemployment 5.3% 4.75-5.25%

reportedly proposed to reduce US auto tariffs mid 2019 end 2019

from 40 per cent to 15 per cent in 2019. Cash rate 1.50% 1.50-1.75%

Any forecasts for 2019 are contingent on the Sharemarket (All Ords ) 6,200-6,500 6,450-6,750

assumptions made for resolution of the dispute. Aust ralian dollar US73-80c US73-80c

We take the view that it is very much in the

interests for both countries to have the dispute resolved. And while it may take a little longer than the

March 1 data set for resolution, we believe enough progress will be made to provide optimism for

investors.

So sharemarkets are expected to be on the path of repair in 2019, especially in the second half of the

year. Firm economic growth rates will provide fundamental support. But slower earnings growth will

keep a focus on margins. Companies with pricing power will be tempted to lift prices while at the same

time seeking to constrain growth of expenses.

The Australian ASX 200 share index is expected to rebound by 10-12 per cent in 2019 after a decline

of around 6-8 per cent in 2018. Including dividends, total returns are tipped to lift by 14-17 per cent in

2019. While above-normal growth of total return on equities is expected, this must be seen in the

context of the below-normal performance in the latter part of 2018.

In addition, valuations on Aussie shares are well below historic averages while dividend yields are

above longer-term averages. Fear has been a key driver on global sharemarkets over 2018, especially

the last three months of the year. The hope is that investors return to focussing on ‘fundamentals’ or

earnings and economies in 2019.

The US Federal Reserve is expected to tread more

warily in lifting interest rates in 2019. While there may

still be 1-2 rate hikes over the year, they may be

focussed later in 2019 and dependent on a tighter job

market forcing up wages and prices. The European

Central Bank should start withdrawing stimulus as it

has previously indicated. But rate hikes are still some

way off.

The Chinese economy should grow by between 6.0-

6.5 per cent over 2019 with increased spending on

infrastructure to be a key driver of growth. Success in

supporting economic growth at the upper end of the

range will be pivotal in ensuring firm demand and

prices for industrial economies.

Technology and Globalisation will remain active

themes serving to constrain wage and price growth

across developed economies.

The OPEC+ nations (OPEC and its allies) will

continue to face challenges in trying to engineer an oil

price near US$55-60 a barrel. Output of North

American shale oil and oil sands will ensure that

global supplies remain healthy. Then there is the

competitive threat to gasoline from electric and

hydrogen-powered vehicles. And then there are the

vagaries of global economic growth, especially noting

the over-riding issue of the US-China trade dispute.

The Australian economy is in solid shape. While the

mountain of residential and commercial building

January 2 2019 10Economic Insights: Year in Review 2018; Year in Preview 2019

projects will be reduced over the year, there is a bevy

of infrastructure projects to underpin construction

activity and overall economic growth. Businesses are

also keen to invest. And rural and mining commodities

are expected to remain in strong demand, especially

through Asia.

Economic growth near 3 per cent, inflation near 2 per

cent, wage growth near 2.6 per cent and

unemployment near 4.75 per cent would be solid

outcomes for an economy well into its 28th consecutive

year of growth.

With the US Federal Reserve becoming more ‘data

dependent’ on lifting interest rates, the greenback may

ease against major currencies. And that is especially

the case if there are more compelling local

requirements to lift rates in other nations. We expect

the Aussie dollar to drift higher to the mid-70s against

the greenback over 2019.

Australian interest rates are tipped to remain on hold

over most of 2019. We agree with the Reserve Bank

that the next move in rates is more likely to be up. The

job market is tightening and wages are lifting.

As we noted above, infrastructure building, exports

and business investment are tipped to support growth

in 2019.

Fiscal stimulus is also possible over 2019 with the

Budget in good shape and an election likely to be held

by May.

But inflation is still contained. And wages can only sustainably lift if supported by firmer productivity

growth.

We currently expect the Reserve Bank to begin a “normalisation” task for interest rates in November.

Craig James, Chief Economist, CommSec: (02) 9118 1806; Mobile: 0419 695 082;

Ryan Felsman, Senior Economist, CommSec: (02) 9118 1805; Mobile: 0457 524 482

January 2 2019 11You can also read