Kingfisher Airlines Nosedives: Can It Soar Again or Will It Remain Grounded?

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Volume 11

Issue 4

December 2013

Kingfisher Airlines Nosedives: Can It Soar Again or Will It Remain

Grounded?

Case prepared by Professor Ritu NARANG, 1 Gaurav MAHAJAN 2 and Mohd. Hassan

KHAN 3

It was March 18, 2012. The scenes at the staggeringly high UB tower, the registered head office

of Kingfisher Airlines in the city of Bangalore, could be described as intense. The UB tower is an

imposing structure that epitomizes the strength of the UB 4 group headed by Dr. Vijay Mallya,

ubiquitously recognized for his flamboyance and style.

Sanjay Agarwal, the airline’s CEO, was facing an acute problem due to the declining fortunes of

Kingfisher Airlines, which was Dr. Mallya’s brainchild and which had, until very recently, been

considered a feather in the cap of the UB Group. Nothing seemed to be going right for the airline

as it struggled to escape from the clutches of debt and prospective closure. The airline’s bank

accounts had been frozen several times in the past few months, either by the Income Tax

Department or the Service Tax Department, because of defaults on tax payments. This, according

to Dr. Mallya, was the prime reason for all the disruptions in his airline’s cash management

function. The financial crisis plaguing Kingfisher Airlines had started in late 2011 and gradually

snowballed into human resource, services, safety and regulatory compliance issues.

The airline was now running up financial losses of almost Rs. 60 billion, 5 coupled with an

accumulated debt of Rs. 70.57 billion. 6 This, along with many other operational constraints, had

actually prompted the management to curtail its flight schedule to a mere 100 flights per day;

operating only 20 functional aircraft subject to the tight vigilance of the DGCA. 7 The cash-

1

Dr. Ritu Narang is a Professor at the University of Lucknow, India.

2

Gaurav Mahajan is a student in the Department of Business Administration, University of Lucknow, India.

3

Mohd. Hassan Khan is a student in the Department of Business Administration, University of Lucknow, India.

4

UB Group, or United Breweries Group, is an Indian conglomerate based in Bangalore, India. The company’s chairman is Vijay

Mallya and its core business includes beverages, aviation, chemicals, international trade and engineering.

5

1 U.S. dollar equals about Rs. 60.

6

htttp://alpha.newsx.com/story/mallya-meets-civil-aviation-minister, accessed August 2, 2012.

7

The Directorate General of Civil Aviation (DGCA) in India is the regulatory body in the field of civil aviation, primarily

dealing with safety issues; it is responsible for the regulation of air transport services to/from/within India. It is also responsible

for the enforcement of civil air safety, airworthiness standards and air regulations. Another major responsibility of the DGCA is

to coordinate all regulatory functions with the International Civil Aviation Organization (ICAO).

© HEC Montréal 2013

All rights reserved for all countries. Any translation or alteration in any form whatsoever is prohibited.

The International Journal of Case Studies in Management is published on-line (http://www.hec.ca/en/case_centre/ijcsm/), ISSN 1911-2599.

This case is intended to be used as the framework for an educational discussion and does not imply any judgement on the

administrative situation presented. Deposited under number 9 40 2013 035 with the HEC Montréal Case Centre, 3000, chemin de

la Côte-Sainte-Catherine, Montréal (Québec) Canada H3T 2A7.

Kingfisher Airlines Nosedives: Can It Soar Again or Will It Remain Grounded?

strapped carrier was compelled to take this decision after much deliberation and careful

consideration of various options before it. Investor confidence in the company had dwindled

along with the incremental drops in its share price, which fell by almost 70% in the last quarter of

FY 2011-12 in comparison to the same quarter in FY 2010-11. 1

By March 2012, most of its dry-leased 2 aircraft had been repossessed 3 by the lessors because of

non-payment of dues. The airline’s employees, including pilots, engineers and ground staff, were

seething with anger and frustration. Their morale had hit an abysmal low, primarily due to the

non-payment of their salaries and allowances since December 2011, which had cast a thick cloud

of uncertainty over their careers. These factors had prompted a large-scale exodus of the

company’s well-trained pilots to rival airlines, further compounding its problems.

There was widespread anger among the passengers as well owing to last-minute flight

cancellations that wreaked havoc with their well-planned vacations, important business meetings

or trips back home. An emotionally distraught Mr. Sharma, who was stranded at the Chattrapati

Shivaji International Airport in Mumbai, complained bitterly: “I was supposed to be flying out to

Lucknow on a Kingfisher Red flight to meet my ailing father, but unfortunately after reaching the

airport I learned my flight has been cancelled abruptly and there is virtually no way for me to get

to my destination now at this moment. They are not even accommodating me on another carrier

as that is not a privilege extended to the guests of their low-cost Red service. Damn!” There were

thousands of other passengers like him in different locations across the country and abroad who

were left clueless and disappointed by the sudden Kingfisher flight cancellations.

The customer support staff along with the striking ground staff of KFA had gone into hiding. The

customers’ frustration and complaints were aggravated by the fact that no company officials were

available to respond to their queries. The lack of communication by the company opened the way

for extensive criticism and misreporting in the media, which only served to fuel the annoyance of

its investors and all other stakeholders.

The Ministry of Aviation felt compelled to look into the matter, as there were widespread

concerns about passenger safety, though no major or minor accidents had occurred.

Dr. Mallya called for an urgent meeting with Sanjay Agarwal to pre-empt and plan for the

possible outcome of his impending meeting with the Union Civil Aviation Minister Chaudhary

Ajit Singh and the DGCA Chief Mr. Bharat Bhushan, which was scheduled for March 21, 2012. 4

He had been summoned primarily to explain the future course of action for the airline and to allay

the ministry’s fears regarding passenger flight safety.

1

www.moneycontrol.com, accessed February 25, 2012.

2

Dry lease refers to the simplest form of airline lease, whereby the lessor provides an aircraft without crew, ground staff,

maintenance staff, etc.

3

http://businesstoday.intoday.in/story/kingfisher-international-operations/1/23326.html, accessed May 15, 2012.

4

http://alpha.newsx.com/story/mallya-meets-civil-aviation-minister, accessed August 2, 2012.

© HEC Montréal 2

Kingfisher Airlines Nosedives: Can It Soar Again or Will It Remain Grounded?

Kingfisher Airlines Soars

Kingfisher Airlines (KFA) established representation of the UB Group in the Indian aviation

sector under the auspices of Dr. Vijay Mallya, the chairman of the UB Group. The airline was

launched in 2005 as a single-class, economy air carrier with food and in-flight entertainment.

Kingfisher Airlines made its grand entrance into the Indian skies with seven Airbus 320 aircraft. 1

It was India’s first airline to start its operations with a brand-new fleet of aircraft. In keeping with

the image of youthful exuberance and fun of the Kingfisher beer brand, Kingfisher Airlines

named its aircraft “Funliners” and positioned itself as a budget carrier. The airline captured

around 6% market share within its first six months of operations.

After having piloted the start-up airline for about a year, Mr. Nigel Harwood, an industry veteran,

made way for Dr. Mallya, who insisted on taking over command of the airline. The airline was

drawn to the larger-than-life style of its chairman, Dr. Mallya. He shifted the focus towards

making KFA a premium service operator offering high-class in-flight services and unrivalled

luxury. Kingfisher introduced its Kingfisher First premium service in April 2006 and redefined

business-class travel in the country by offering impeccable services such as extra-wide

personalized video screens, noise-cancelling stereo headphones, fully extendable footrests and

much more. 2 The airline offered Indian travellers an unmatched experience. For the first time in

the history of Indian aviation, world-class in-flight entertainment and comfort were provided. It

offered a top-notch cabin crew, comfortable seats with extra space and other ancillary services.

Quality service became the airline’s USP. Dr. Mallya left no stone unturned in ensuring the

recruitment, training and development of its employees, turning them into one of the most

admired staffs in India’s commercial civil aviation community. He handpicked the best talent to

pilot his aircraft and ensured that his ground staff was extremely courteous and well-behaved

while managing operations on the ground, which required them to be in close interaction with

passengers. Dr. Mallya’s largesse in terms of remuneration also kept the staff highly motivated

until the troubles and defaults on salaries and perks started. 3

In order to differentiate itself from other carriers, the airline made changes to the configuration of

its Airbus 320 aircraft by reducing the number of economy-class seats from 180 to 114 and

adding 20 business-class seats. KFA had around 14 aircraft when these alterations started. 4 With

its ambitious expansion plans, KFA had already placed orders for more A-320 aircraft 5 at the

Dubai Air Show in 2005, in a deal worth US$1.9 billion. At the same air show, the airline also

ordered ATR72-50 6 aircraft worth US$350 million. It became India’s fastest-growing airline,

recognized for the quality of its in-flight services. In December 2005, it was awarded “Best New

1

http://www.flykingfisher.com/media-center/in-the-news/kingfisher-airlines-orders-20-new-atr72-500-aircraft-worth-us$350-

million.aspx, accessed June 21, 2012.

2

http://www.flykingfisher.com/media-center/in-the-news, accessed June 21, 2012.

3

http://www.bbc.co.uk/news/world-asia-india-18882397, accessed March 25, 2012.

4

http://www.business-standard.com/taketwo/news/a-taletwo-airlines-kingfisher-vs-indigo/465252/, accessed February 25, 2012.

5

http://www.flykingfisher.com/media-center/in-the-news/kingfisher-airlines-orders-30-new-airbus-a320-family-jets-worth-

us$19-billion.aspx. accessed February 21, 2012.

6

http://www.flykingfisher.com/media-center/in-the-news/kingfisher-airlines-orders-20-new-atr72-500-aircraft-worth-us$350-

million.aspx, accessed February 23, 2012.

© HEC Montréal 3

Kingfisher Airlines Nosedives: Can It Soar Again or Will It Remain Grounded?

Airline of The Year” by the Centre for Asia Pacific Aviation (CAPA), and in 2006, KFA was

named the “Best New Domestic Airline for Excellent Services and Cuisine” by the Pacific Area

Travel Writers Association (PATWA). By November 2011, KFA had 64 aircraft in its fleet. 1

The airline had a mix of eight different kinds of aircraft, requiring pilots to obtain type ratings for

the aircraft they flew. This called for huge investments in training and development by the airline.

It also had to commission varied engineering support services for the different aircraft, which

also required a large financial commitment. All of this was necessary to ensure the safety of the

aircraft and, even more importantly, that of its passengers.

Growth amidst Struggles

The shift in the model by Dr. Mallya did not translate into sustainable profits for the airline, as a

large chunk of the market had already been deeply cornered by the low-cost, no-frill travel bug

who did not like the idea of paying more for frills on relatively short flights, particularly those

lasting no more than two or three hours. Even though the airline was operating on wafer-thin

margins, as had become the norm in those days due to cut-throat competition and price wars, it

did not compromise on its service quality at all and continued to offer its guests the best-in-class

hospitality and in-flight entertainment services. The airline started referring to its passengers as

“guests,” which was innovative and gave the airline a positive appeal. The marketing initiatives

positioned the airline as offering a “new flying experience” and the promotional campaigns used

top fashion models to give the carrier a chic, glamorous and up-market brand image.

The airline struggled hard to find its bearings in an extremely dynamic business environment and

continuously tried different strategies to boost growth. For instance, under pressure from the

rapidly changing business environment due to escalating jet fuel prices and the global recession,

in 2007, the airline made a move to acquire Air Deccan, the budget airline led by Capt. G. R.

Gopinath. Air Deccan was reeling under heavy losses of almost Rs. 5.50 billion. Ironically,

Kingfisher had to shell out another Rs. 5.50 billion for this acquisition. It was an eyebrow-raising

union, as the two airlines had different styles of operation. Kingfisher was known for its world-

class cuisine, comfort and luxury, whereas Air Deccan passengers had to pay for food and water.

The acquisition was touted as an aggressive move to expand and explore international markets in

the hope of encountering a relatively favourable business climate. The airline thus launched

operations on international routes, which it became eligible to fly due to its acquisition of

Deccan, which had operated in the domestic market for the mandatory period of five years

required by Indian aviation regulations to fly on international routes. While the soaring jet fuel

prices reached $150 per barrel and the recession in 2008 made the fundamentals in the airline

industry worse, Kingfisher launched its international operations in a big way. They included

long-haul as well as short-haul flights.

In 2008, the airline was granted a ‘5-Star Airline Status’ by Skytrax, the world’s leading

independent travel forum and air travel information organization, thus adding another feather to

its cap. By March 2008, the Kingfisher-Deccan Group had become India’s largest domestic

1

http://articles.economictimes.indiatimes.com/2013-02-15/news/37119333_1_lessors-kingfisher-airlines-ilfc, accessed

February 19, 2013.

© HEC Montréal 4

Kingfisher Airlines Nosedives: Can It Soar Again or Will It Remain Grounded?

airline group, connecting 71 cities. With a fleet of 80 aircraft, the group offered 540 flights daily

to almost every part of the nation. On September 3, 2008, 1 KFA commenced its international

operations with its first international flight between Bangalore and London-Heathrow Airport. In

the same year, Air Deccan was rebranded as “Deccan,” which was also phased out later in

September 2008. Effective September 5, 2008, Deccan Aviation Limited was renamed Kingfisher

Airlines Limited.

Kingfisher Airlines now offered three major classes of service: Kingfisher First, Kingfisher Class

and Kingfisher Red. The market for Kingfisher First was segmented around business travellers

who had a higher potential to pay for premium services. Kingfisher Class focused on the

country’s growing smart, elegant and ambitious middle class. Kingfisher Red mainly targeted the

price-conscious, middle-class passenger. The Kingfisher Red brand was positioned between a

low-cost and full-service carrier and was proudly referred to as the premium low-cost airline by

the company’s management. It was the only low-cost carrier that offered complimentary services

like food and in-flight entertainment and still managed to remain competitive with full-service

carriers in terms of pricing, which was the key differentiating factor in the aviation industry.

In 2011, Mr. Sanjay Agarwal assumed control as chief executive officer of Kingfisher Airlines.

The airline now contemplated discontinuing its Kingfisher Red service and again offering a dual-

class, full-service configuration, but before it could do so, problems emerged. With 75% of the

domestic capacity 2 being in the low-cost sector and international airlines competing hard for

short-haul flights to the West and South-East Asia, Kingfisher Airlines suddenly shifted back to a

full-service offering in a dual-class aircraft configuration.

Indian Civil Aviation Industry: An Overview

In 1912, Indian State Air Services along with the U.K.-based Imperial Airways established the

first flight between Karachi and Delhi and began an era of aviation industry in India. Tata

Airline, founded in 1932 by JRD Tata, was the first airline in India. Tata Airline went public in

1946 and became Air India Limited. Soon after, in 1948, Air India Limited formed a joint stock

company with the Government of India: Air India International Limited. 3

By the time India won independence from British rule, there were nine air transportation carriers

in the country. The Government of India nationalized the civil aviation industry with the Air

Corporations Act of 1953, 4 which dashed the hopes of private companies planning to enter the

industry. These national carriers continued to dominate the industry until the early 1990s, when

the government finally scrapped the Air Corporations Act of 1953 in order to enable and promote

the participation of private players in the industry. The Government of India adopted the open

sky policy and allowed air carriers to schedule their flights, passengers and cargo fares. The

monopoly enjoyed by Air India and Indian Airlines finally came to an end.

1

http://www.flykingfisher.com/media-center/in-the-news/debut-international-services.aspx, accessed March 1, 2012.

2

http://www.business-standard.com/taketwo/news/a-taletwo-airlines-kingfisher-vs-indigo/465252/, accessed February 25, 2012.

3

http://www.tata.com/aboutus/articles/inside.aspx?artid=0uT2PalyEbc=, accessed June 21, 2012.

4

http://www.civilaviation.gov.in, accessed March 10, 2012.

© HEC Montréal 5

Kingfisher Airlines Nosedives: Can It Soar Again or Will It Remain Grounded?

Economic liberalization in India, which started in 1991, opened the door to new avenues for

private players offering chartered and non-chartered services. Air Sahara and Jet Airways were

the major airlines that entered the industry in 1991 and 1993 respectively. By the mid-1990s, the

new private players accounted for more than 10% 1 of domestic market share. The move towards

privatization broke the monopoly and triggered competition in the industry. Airline customers

finally had options to choose from, and air transportation started to become affordable for the

middle class.

Aviation soon became a lucrative business option in India and continued to attract new entrants.

Air Deccan, widely known as the “common man’s” airline, commenced its operations on August

23, 2003. 2 With a completely different business strategy, Air Deccan entered the market as a low-

cost carrier and at one point offered tickets for as low as Re 1. 3 The airline soon gained

momentum because of its unique approach and made air travel affordable for a large segment of

the population that could not afford costly flights.

In 2005, Go Airlines (India) 4 Ltd. launched its GoAir brand, another low-fare carrier to enter the

market. In the same year, Kingfisher Airlines, the “King of Good Times,” commenced its

operations. In 2006, IndiGo airline began operating as a low-cost carrier. Competition was

heating up in the industry, with each airline trying hard to increase its market share. At the same

time, rising competition and the escalating cost of jet fuel due to an increase in the service tax

made it more and more difficult to generate profit. It was a paradoxical situation. Though

passenger traffic was growing at a rapid rate, airlines were struggling hard to break even due to

escalating fuel costs and their inability to charge high prices. Consequently, 2007 saw two major

mergers in the aviation industry. In an eyebrow-raising union, Kingfisher took control of Air

Deccan, while Jet Airways bought domestic carrier Air Sahara and rebranded it as JetLite. Jet

Airways became the market leader, with a market share of 27% in November 2009.

The private airline companies were not the only ones feeling the heat; the performance of

national carriers Air India and India Airlines had also become sub-optimal. Finally, in 2011,

these two national carriers were merged under Air India. But the merger did not prove to be a

boon for the national carrier, as the company continued to pile up debt and losses. As of February

7, 2012, Air India had debt worth Rs. 675.20 billion along with an accumulated loss of

Rs. 203.20 billion. 5

With IndiGo as the exception, five out of six of India’s major airlines were in the red, as per the

third-quarter reports for FY 2011-12.

The third-quarter financial report for FY 2011-12 6 revealed that Jet Airways along with JetLite

continued to be the market leader in domestic operations, with 26.5% of the market share.

1

Ibid.

2

http://www.deccanairlines.in/, accessed March 10, 2012.

3

Re 1=US$0.017

4

http://www.goair.in/aboutus.aspx, accessed March 12, 2012.

5

http://profit.ndtv.com/News/Article/government-approves-air-india-debt-recast-plan-297357, accessed February 27, 2012.

6

http://www.jetairways.com/doc/InvestorRelations/Q3_FY2012-Investors.pdf, accessed March 15, 2012.

© HEC Montréal 6Kingfisher Airlines Nosedives: Can It Soar Again or Will It Remain Grounded?

IndiGo, with its consistent performance, had toppled Kingfisher to gain second place, with 20%

of market share, followed by SpiceJet with a 16.1% market share. Kingfisher had slipped to fifth

place, with 14.2% of market share.

The aviation industry is one of the most complex sectors in which to conduct business. Airline

profitability is prominently driven by external forces, making the airline business vulnerable to

changing economic conditions, terrorism, customer preferences, etc. 1 However, despite the

ongoing predicament, the Indian civil aviation sector was ranked ninth largest in the world in

2011. The number of passengers increased to 150 million in 2011, an increase of 77 million from

73 million in 2005-06. Five out of six national carriers operated on international destinations.

Experts predicted that the Indian aviation sector would rank among the top three in the world by

2020, 2 said Mr. Ajit Singh, Union Minister for Civil Aviation at the India Aviation 2012

exhibition and conference. 3

Government Policy under Criticism

The Ministry of Civil Aviation is the governing body of the civil aviation sector in India. The

ministry holds power and responsibility for developing as well as regulating the civil aviation

sector in India. It is responsible for formulating various rules, policies, acts, agreements, etc.

related to the country’s civil aviation sector. This ministry oversees organizations such as the

Directorate General of Civil Aviation, the Bureau of Civil Aviation Security, the Indira Gandhi

Rashtriya Udan Akademi, and accredited public-sector undertakings like the National Aviation

Company of India Limited, Airports Authority of India and Pawan Hans Helicopters Limited.

“Every government has gone out of the way to support airlines connectivity. In India, airlines are

over taxed and over charged. Wonder why?” posted a defiant Dr. Vijay Mallya, promoter of

KFA, on a famous social networking website, blaming the government policies in India for the

problems ailing the aviation industry. A closer look at the government’s policies throws some

light on this issue. As per the policy of the Government of India, foreign direct investment was

not allowed in the industry, which restricted the source of funds for the struggling airlines. Other

airlines shared Dr. Mallya’s views and had called on the government to allow FDI in the aviation

sector. Aviation turbine fuel (ATF) accounted for more than 50% of the operating costs of the

airlines and was almost double the cost in India compared to countries like Singapore and Dubai.

As at March 2012, sales tax had soared to 30% in Gujarat and 29% in Madhya Pradesh. 4

Considering the bleak position of the aviation sector, the government decided to allow the direct

import of ATF to bring down airlines’ operating costs. 5 However, this modification in the policy

1

http://www.kpmg.com/IN/en/IssuesAndInsights/ArticlesPublications/Documents/Indian%20Aviation-

%20Flying%20Through%20Turbulence.pdf, accessed April 20, 2013.

2

http://www.thehindubusinessline.com/industry-and-economy/government-and-policy/article3223254.ec, accessed May 15,

2012.

3

http://www.thehindu.com/business/Industry/article2994435.ece, accessed June 21, 2012.

4

http://www.thehindubusinessline.com/industry-and-economy/logistics/article3314871.ece?css=print, accessed May 15, 2012.

5

Due to the enormously high rate of service tax on aviation turbine fuel (ATF), Indian carriers spend about 47% to 65% more for

ATF in domestic flights than carriers in other countries. For instance, ATF costs almost 50% more in India in comparison to

nearby hubs like Singapore and Sharjah. Moreover, international flights cost them 13% to 27% more in fuel than the other

© HEC Montréal 7Kingfisher Airlines Nosedives: Can It Soar Again or Will It Remain Grounded?

regarding ATF was again questionable. In a country that produces a surplus of ATF, as evidenced

by the fact that India exported 45% of its ATF production in 2010, was this move justified? This

leaves an ATF-surplus country importing ATF due to existing policies that give each state the

autonomy to decide its own applicable sales tax figures on ATF.

“The Ministry is working out on an economic policy framework for future airports to attract

investments as well as ensure their viability. This is in addition to allowing 100 per cent foreign

direct investments in the Greenfield airports under the automatic route and formulation of an Air

Cargo Promotion Policy which will soon be brought out for consultations,” said Mr. Ajit Singh,

Union Minister of Civil Aviation at the India Aviation 2012 exhibition and conference. 1

Later, the government announced that it was actively considering allowing 49% FDI in the

aviation sector. In view of the ongoing predicament in the industry, the airlines expected to get a

nod from the government.

The eligibility norms for Indian carriers to fly overseas had also been aggressively criticized by

Dr. Mallya in 2005. As per the norms mandated by the government, an Indian carrier must have

five years of domestic flying experience along with a fleet of 20 aircraft in order to qualify to fly

internationally. However, no such norms existed for foreign airlines flying to India. The Civil

Aviation Ministry at the time rejected calls to modify the norms by saying “the minimum

requirements were essential for safe and reliable operations on international routes.” Eligibility

norms for Indian carriers to fly overseas once again came into the spotlight in 2012, when

industry experts and the government were exploring possible measures aimed at reviving the

ailing industry.

“We are open to relaxing eligibility norms required for Indian carriers to fly international. No one

has approached us with a proposal to relax norms, but it can be looked at,” said Civil Aviation

Minister Ajit Singh.” 2

The Indian and U.S. Airline Industries: Striking Similarities

The U.S. and Indian airline industries have much in common in terms of their evolution and

growth. One of the most significant events to have kick-started rapid growth in the industry for

both countries was deregulation, which gave private players access to the domestic and

commercial aviation markets. This process started in America in the late 1970’s, while the ball

was set rolling in India in the early 1990’s. A dramatic decrease in air fares and an explosion in

demand had led to an incredible surge in the growth of U.S. airlines in the 1980’s. However,

intense competition, low differentiation, high costs, slow growth and excess capacity resulted in

low profit margins. Eventually, a lot of carriers folded and a round of consolidation in the

international airlines. Since ATF accounts for almost 50% of operating costs, this huge price difference makes it hard for Indian

carriers to compete with the foreign carriers. The government’s decision to allow the direct import of ATF can be seen as a

remedy to the problem of the huge price gap.

1

http://www.thehindu.com/business/Industry/article2994435.ece, accessed June 21, 2012.

2

http://www.business-standard.com/india/news/eligibility-for-carriers-flying-abroad-may-be-relaxed/472142/, accessed May12,

2012.

© HEC Montréal 8Kingfisher Airlines Nosedives: Can It Soar Again or Will It Remain Grounded?

industry left only four major carriers – American Airways, Delta Air Lines, United Continental

Airlines and South West Airlines – dominating 80% of U.S. skies. 1 Paul Stephen Dempsey, a

renowned aviation expert and professor in the faculty of law at Canada’s McGill University,

studied the effects of deregulation in the U.S. airline industry. His analysis shows that:

barely a decade after the Airline Deregulation Act of 1978 was implemented, the US airline industry

lost all of the money it made since the Wright Brothers’ inaugural flight in 1903. After

150 bankruptcies and 50 mergers, the US now flies the world’s oldest and most repainted fleet. Of the

176 airlines to which deregulation gave birth, only one remains and that too is bankrupt. Deregulation

has led to greater monopoly and concentration, with just four airlines controlling two-thirds of the US

market. Rather than leading to a reduction in fares, as laissez-faire economists had confidently

forecasted, deregulation actually led to a fare rise in real terms. The full fare has risen sharply, at

more than double the pace of inflation, costs have escalated, and service has declined. 2

Further, the willingness of the business traveller to pay more decreased with the economic

slowdown and the burst of the dot-com bubble in the 2000’s. The threat of terrorism posed an

additional challenge to the industry. The buying power of customers increased due to online

purchases, which facilitated access to detailed knowledge of pricing in the industry.

Telecommunications developments made it possible to hold many long-distance business

meetings through video-conferencing, reducing the need to travel for business purposes. Some

airlines, including American Airlines, cut their employees’ salaries to cope with the challenging

business environment following the terrorist attacks on the World Trade Center. Understanding

the difficulties faced by the airline, the employees cooperated. Further, in 2008, U.S. airlines

were allowed to unbundle services that they had formerly offered on a complimentary basis. This

paid rich dividends for the industry. The airlines were free to charge their passengers for services

such as checked-in baggage, use of lounges and carriage of equipment such as musical

instruments, sports gear and articles that placed a higher degree of responsibility and liability on

the airline.

The Indian aviation industry seems to have followed the U.S. pattern of growth and shrinking

profit margins. The deregulation in India that apparently aped the U.S. policy attracted a number

of new entrants to the airspace. The Indian aviation industry had earlier relied mostly on business

travel and very little on leisure travel, but the early 2000’s witnessed a heavy increase in leisure

travellers. This was made possible by the entry of several new players that seemed keen to try out

the South West’s hugely successful model of low-cost flying in India. Soon India’s low-cost

carriers such as Deccan, GoAir, IndiGo and SpiceJet started giving stiff competition to industry

doyens like Jet Airways, Air India and Indian Airlines by offering huge discounts designed to

attract rail travellers. While the Indian aviation industry was experiencing over-capacity, the U.S.

industry was undergoing tremendous turmoil. However, this phenomenon soon caught up with

India as well. The rivalry among air carriers, stiff price competition, lack of infrastructure,

burgeoning fuel prices, changing consumer preferences, stringent legislation 3 and operational

inefficiencies resulted in accumulated losses running into the millions of dollars for the aviation

1

http://www.transtats.bts.gov/, accessed March 8, 2013.

2

http://www.rediff.in/money/2008/oct/23air5.htm, accessed March 13, 2013.

3

The airlines were not allowed to unbundle their services, and a number of services like checked-in baggage up to a maximum

weight and lounge facilities were provided free of charge.

© HEC Montréal 9Kingfisher Airlines Nosedives: Can It Soar Again or Will It Remain Grounded?

industry. Many price-conscious customers went back to rail travel, as prices started to soar with

the reduction in over-capacity in the wake of Kingfisher Airlines’ exit from the scene.

The economic environment following the American subprime crisis of 2008 posed another

challenge to countries across the globe. Rising inflation and sluggish production and exports are

being experienced by most of the developing countries, including India. 1 It remains to be seen

how the Indian industry will weather these unfavourable storms and sail into calmer waters and a

friendlier business climate in the times to come.

Issues Faced by KFA

In the midst of its ambitious expansions, commencement of flights to international destinations

and unmatched luxury and comfort, KFA’s financial health was weakening. KFA had started its

operations with a strategic plan to produce profit right from year one, but this never really

happened. The company reported a loss at the end of every financial year, with a loss of

Rs. 1.88 billion on March 21, 2008. 2 The global economic slowdown during this period further

aggravated the situation and temporarily blocked the sources of funds. According to critics, the

multi-pronged crisis that plagued the airline could perhaps be attributed to certain strategic

blunders, inherent flaws in business plans, inept HR policies and, above all, operational

inefficiencies.

KFA ended March 31, 2009 with a loss of around Rs. 16.08 billion. 3 There were various reasons

for this. The recession that had hit the global economy had led to a sudden surge in oil prices.

The high tax rate on aviation turbine fuel (ATF) became another major problem as operating

costs began to skyrocket. 4 In order to contain its losses at the end of each financial year, KFA

shifted into cost-saving mode. The company decided to fly less in order to avoid losses on loss-

making routes and initiated what it called a route rationalization program. By the end of March

2010, the company had reduced its fleet size to 68 aircraft. Though KFA had become India’s

single largest domestic carrier (by passengers flown and cities served), with 22.9% of the

domestic market share, it nonetheless reported a loss of Rs. 16.472 billion. 5

In order to fight rising operating costs and continue its operations, KFA sought to raise funds

from different sources. However, KFA’s financial situation kept on deteriorating, and the

company ended the 2010-11 financial year with a loss of Rs. 10.24 billion. 6 The airline

encountered one problem after another, including a cash shortage making it impossible to make

salary payments. Oil companies stopped supplying fuel to the company due to overdue payments

1

http://www.thehindubusinessline.com/features/investment-world/market-strategy/opportunities-round-the-corner-for-india-

inc/article3509399.ece, accessed June 21, 2012.

2

Kingfisher Airline Limited Annual Report 2007-08, accessed May 15, 2012.

3

Kingfisher Airline Limited Annual Report 2008-09, accessed May 15, 2012.

4

Ibid.

5

Kingfisher Airline Limited Annual Report 2009-10, accessed May 15, 2012.

6

Kingfisher Airline Limited Annual Report 2010-11, accessed May 15, 2012.

© HEC Montréal 10Kingfisher Airlines Nosedives: Can It Soar Again or Will It Remain Grounded?

and the GMR Group 1 that operates the Delhi and Hyderabad airports adopted a cash-on-payment

policy at both airports. 2 The company’s bank accounts were frozen several times by the Income

Tax Department and the Service Tax Department because of defaults on tax payments, leaving

the company cash dry. The battered airline had to temporarily suspend its operations from several

cities due to lack of working capital and a staggering debt load that had reached Rs. 70 billion by

March 27, 2012. The banks refused to lend any more money to the airline.

The accounts were finally unfrozen upon payment of Rs. 440 million to the Income Tax

Department and another Rs. 200 million to the Service Tax Department on March 31, 2012. 3 By

then, Kingfisher Airlines had also started defaulting on its promise to release long-overdue

salaries and benefits. The worst hit were the highest-paid cabin crew members. Eventually, the

airline faced a spate of mass strikes and disruptions in operations. 4 In a bid to limit further

damage, Dr. Mallya travelled to many cities personally to address his staff’s qualms and other

serious issues, mainly the non-payment of overdue salaries and allowances.

In a letter to his employees on April 1, 2012, 5 Dr. Mallya promised to begin paying overdue

salaries in a staggered manner, which was later complied with. This last-ditch effort came as a

huge relief from the game of brinkmanship being played out by airline management and the

striking employees. It also cleared the way for co-ordinated efforts to salvage some lost ground.

Meanwhile, the chairman of the UB Group announced that KFA had ceased to be a subsidiary of

UB Holdings, though the latter had an exposure of around Rs. 120 billion in the airlines. 6

While the cash-strapped Kingfisher Airlines continued to slash its daily operating schedule due to

a lack of working capital, Civil Aviation Minister Ajit Singh was flooded with questions from the

media regarding the future of Kingfisher Airlines. The anxious question in the minds of the

stakeholders, media, and those following the Kingfisher story was: “Will the government offer a

bailout plan to Kingfisher or not?” Some of the honourable ministers in the present government

had already stated that the airline should not be allowed to fail. Ending the speculation regarding

a bailout option, Ajit Singh said, “Government is not going to give any bailout or ask the banks to

bail out any private airline or any private industry for that matter.”

This represented a striking difference in the government’s approach towards a national carrier

and a private carrier. In May 2012, the Government of India had proposed a Rs. 300-billion

1

Headquartered in Bangalore, India, GMR Group is one of the leading infrastructure enterprises in the country. The company has

operations spanning the airport, energy, highway, and urban infrastructure sectors. Presently, GMR has four major airport

projects, including Delhi International Airport (P) Limited, GMR Hyderabad International Airport Limited, Sabiha Gokcen

Airport Limited and Ibrahim Nasir International Airport Pvt. Ltd. Delhi International Airport (P) Limited is a joint venture of

GMR Group (54%), Airports Authority of India (26%), Fraport and Eraman Malaysia (10% each). GMR Hyderabad

International Airport Limited (GHIAL) is another major project in which GMR Group is the leading member of the joint

venture company with a 63% stake.

2

http://www.business-standard.com/india/news/after-air-india-kingfisher-delays-salary-payment/445794/, accessed June 21,

2012.

3

http://businesstoday.intoday.in/story/kingfisher-airlines-staff-vijay-mallya-pays-after-4-months/1/23836.html, accessed June 21,

2012.

4

http://www.myiris.com/newsCentre/storyShow.php?fileR=20121115115415102&dir=2012/11/15, accessed May 18, 2012.

5

http://indiatoday.intoday.in/story/vijay-mallya-kingfisher-airlines-employees/1/182646.html, accessed May 15, 2012.

6

“No Payment of Salary, KF Pilots Call in Sick,” The Times of India, Lucknow, May 11, 2012, p. 12.

© HEC Montréal 11Kingfisher Airlines Nosedives: Can It Soar Again or Will It Remain Grounded?

bailout plan for the ailing Air India, irrespective of the fact that the national carrier had been in

the red since the merger of Air India and Indian Airlines in 2007. 1 Air India had ended March

2011 with combined losses of Rs. 78.53 billion. 2

“Obviously the merger didn’t go as planned, and there was something that had seriously gone

wrong. My job is to see what is the current situation, learn from past mistakes and work to see

that Air India succeeds,” Singh had told a TV channel.

Despite continuously pumping huge amounts into the national carrier in order to keep it afloat,

the government’s efforts seemed to be in vain. Surging conflicts between management and

employees were quite evident, as pilots called in sick in huge numbers, 3 forcing Air India to

cancel many flights on a daily basis and leaving passengers irate and helpless.

The government’s decision not to offer a bailout to Kingfisher Airlines seemed to be justified

based on the current situation of Air India, but was the decision to invest taxpayers’ money on a

bleeding national carrier justified? This was another question drawing comments from various

stakeholders in the country.

Looking Forward

The challenge before Sanjay Agarwal was to make Kingfisher Airlines bounce back from its

precarious position as the smallest airline in the country. Daily flights had been drastically

trimmed to 110 from around 400. Ensuring the regular operation of these flights in the face of

frequent agitation by the pilots was another challenge that required deft handling.

Throughout this saga of unfortunate developments, management had unceasingly reiterated its

commitment to take on the challenge of restoring the airline to “fly the good times” and to

honour its responsibility towards its stakeholders. Even the chairman Dr. Mallya announced that

the UB Group had infused Rs. 15 billion 4 since February 2011.

As the hopes of a bailout from the government with taxpayers’ money were dashed, the airline

had no option but to manage its debt on its own. The first corrective measure entailed making a

concerted effort to raise cash for its day-to-day operations. It seemed that the time had come to

conduct a thorough review of its past policies and strategies and try to learn from the competitors

that had managed to weather the storm and still remain profitable in the most unfavourable of

business environments. Perhaps the company needed to completely re-invent itself in terms of its

operations and human resource management.

Kingfisher Airlines could attempt to pressure the government to introduce reforms in the policy

which could include 49% FDI in the aviation sector. This policy, if cleared by the cabinet, could

1

http://www.thehindu.com/opinion/op-ed/article3415784.ece, accessed August 2, 2012.

2

The Times of India, Lucknow, May 14, 2012.

3

http://articles.timesofindia.indiatimes.com/2012-05-11/india/31668687_1_absentee-pilots-rostered-kingfisher-airlines, accessed

June 21, 2012.

4

The Times of India, Lucknow, May 14, 2012.

© HEC Montréal 12Kingfisher Airlines Nosedives: Can It Soar Again or Will It Remain Grounded? prove to be a big boon for the cash-strapped carriers. The company was in dire need of cash, but because of the governmental policy was unable to attract foreign investors. Foreign airlines, especially the cash-rich ones from the Middle East, if allowed sizeable equity in the Indian carriers, would show interest in Kingfisher, mainly because of the growing consumer base in India and expected high growth in the industry. It would no doubt be a herculean task for the management to rescue the airline and move it back into the black. But this was exactly what was expected of a seasoned business tycoon like Dr. Mallya, who had a rich legacy of diverse cash-rich businesses and, more importantly, a never- say-die attitude towards tackling challenges head on and eventually succeeding. However, it was still very difficult to predict the outcome, as there were many factors at play. 2013-12-02 © HEC Montréal 13

Kingfisher Airlines Nosedives: Can It Soar Again or Will It Remain Grounded?

Appendix 1

Key Financial Metrics

Name Last Price Market Sales Net Profit Total Assets

Capitalization Turnover

(Rs. Billion)

Container Corp 9.08 118.02 38.27 8.30 49.78

Jet Airways 3.515 30.34 127.77 .097 160.85

Allcargo 1.25 16.31 8.26 1.52 12.27

Kingfisher Air .19 11.53 63.60 -10.27 41.06

Arshiya Intl 1.51 8.88 4.53 .252 11.95

Aegis Logistics 1.58 5.26 2.60 .31 3.28

Transport Corp .654 4.66 17.59 .51 6.16

Aqua Logistics .12 3.61 3.81 .22 5.94

Patel Integrate .26 .39 4.27 .035 1.28

Source: http://www.moneycontrol.com/competition/kingfisherairlines/comparison/KA02, accessed April 20, 2012.

© HEC Montréal 14Kingfisher Airlines Nosedives: Can It Soar Again or Will It Remain Grounded?

Appendix 2

Balance Sheet (in billions of Rs.)

Kingfisher AirContainer CorpJet AirwaysAllcargoSpiceJet

Mar ‘11 Mar ‘11 Mar ‘11 Dec ‘10 Mar ‘11

Sources of Funds

Total Share Capital 10.509 1.300 .863 .261 4.054

Equity Share Capital 4.978 1.300 .863 .261 4.054

Share Application Money .030 0.000 0.000 .012 .053

Preference Share Capital 5.531 0.000 0.000 0.000 0.000

Reserves -40.050 48.478 7.504 9.517 -.900

Revaluation Reserves 0.00 0.00 1,767.64 0.00 0.00

Networth -29.511 49.778 26.043 9.790 3.211

Secured Loans 51.845 0.00 45.105 2.473 .302

Unsecured Loans 18.726 0.00 89.699 0.00 .555

Total Debt 70.571 0.00 134.804 2.473 .858

Total Liabilities 41.059 49.778 160.847 12.263 4.069

Gross Block 22.543 32.661 179.405 7.761 1.138

Less:Accum. Depreciation 6.824 9.591 43.247 1.341 .287

Net Block 15.719 23.070 136.158 6.421 .850

Capital Work in Progress 6.734 3.392 3.489 .458 6.132

Investments .001 2.440 17.251 1.791 .000

Inventories 1.877 .063 7.112 .063 .204

Sundry Debtors 4.405 .173 9.658 .936 .172

© HEC Montréal 15Kingfisher Airlines Nosedives: Can It Soar Again or Will It Remain Grounded? Cash and Bank Balance .882 .563 1.412 .114 .123 Total Current Assets 7.164 .798 18.182 1.113 .498 Loans and Advances 53.802 5.618 36.886 4.637 1.817 Fixed Deposits 1.642 22.393 4.465 .021 1.800 Total CA, Loans & Advances 62.607 28.810 59.533 5.771 4.114 Deferred Credit 0.00 0.00 0.00 0.00 0.00 Current Liabilities 44.639 6.392 53.715 1.772 6.944 Provisions .621 1.541 1.869 .406 0.835 Total CL & Provisions 45.260 7.933 55.584 2.177 7.028 Net Current Assets 17.348 20.877 3.949 3.593 -2.913 Miscellaneous Expenses 1.258 0.00 0.00 0.00 0.00 Total Assets 41.059 49.778 160.847 12.263 4.069 Contingent Liabilities 229.202 14.404 139.284 .696 157.375 Book Value (Rs.) -70.46 382.96 96.91 74.92 7.79 Source: http://www.moneycontrol.com/competition/kingfisherairlines/comparison/KA02, accessed April 20, 2012. © HEC Montréal 16

Kingfisher Airlines Nosedives: Can It Soar Again or Will It Remain Grounded?

Appendix 3

Profit & Loss Account (in billions of Rs.)

Kingfisher Container Jet

Allcargo SpiceJet

Air Corp Airways

Mar ‘11 Mar ‘11 Mar ‘11 Dec ‘10 Mar ‘11

Income

Sales Turnover 62.334 38.281 127.825 6.998 28.795

Excise Duty 0.00 0.00 0.00 0.00 0.00

Net Sales 62.334 38.281 127.825 6.998 28.795

Other Income .816 1.735 2.506 .429 .713

Stock Adjustments 0.00 0.00 0.00 0.00 0.00

Total Income 63.150 40.016 130.331 7.428 29.508

Expenditure

Raw Materials .567 .027 0.00 .131 0.00

Power & Fuel Cost 22.740 .140 43.667 .239 12.262

Employee Cost 6.805 .869 13.422 .486 2.315

Other Manufacturing Expenses 11.928 25.983 23.759 3.526 5.998

Selling and Admin Expenses 9.973 .754 18.091 .640 2.589

Miscellaneous Expenses .879 .481 3.739 .153 .577

Preoperative Exp Capitalised 0.00 0.00 0.00 0.00 0.00

Total Expenses 52.893 28.254 102.677 5.174 23.741

Operating Profit 9.440 10.027 25.148 1.824 5.054

PBDIT 10.256 11.761 27.654 2.254 5.768

Interest 23.403 .003 18.727 .279 4.397

PBDT -13.147 11.758 8.926 1.975 1.371

Depreciation 2.030 1.452 9.106 .402 .089

Other Written Off .380 0.00 0.00 0.00 0.00

Profit Before Tax -15.557 10.306 -.180 1.573 1.282

Extra-ordinary items .730 .251 2.700 0.00 -.023

PBT (Post Extra-ord Items) -14.827 10.557 2.521 1.573 1.259

Tax -4.554 1.798 2.305 .237 .247

Reported Net Profit -10.274 8.760 .097 1.211 1.011

Total Value Addition 52.327 28.228 102.677 5.043 23.741

Preference Dividend 0.00 0.00 0.00 0.00 0.00

Equity Dividend 0.00 2.014 0.00 .394 0.00

Corporate Dividend Tax 0.00 .331 0.00 .064 0.00

Per share data (annualised)

Shares in issue (lakhs) 49.778 12.998 8.633 13.052 40.538

Earning Per Share (Rs) -.206 .674 .011 .093 .025

Equity Dividend (%) 0.00 1.550 0.00 1.500 0.00

Book Value (Rs.) -.705 3.830 .970 .749 .078

Source: http://www.moneycontrol.com/competition/kingfisherairlines/comparison/KA02, accessed April 20, 2012.

© HEC Montréal 17Kingfisher Airlines Nosedives: Can It Soar Again or Will It Remain Grounded?

Appendix 4

Cash Flow Statement (in billions of Rs.)

Kingfisher Jet Container

Allcargo SpiceJet

Air Airways Corp

Dec ‘10 Mar ‘11 Mar ‘11 Mar ‘11 Mar ‘11

12 mths 12 mths 12 mths 12 mths 12 mths

Net Profit Before Tax 1.449 -15.208 1.282 .466 10.583

Net Cash From Operating

1.219 -.022 -.455 12.273 8.083

Activities

Net Cash (used in)/from

-3.352 .381 -1.225 .138 -2.672

Investing Activities

Net Cash (used in)/from

2.063 -.817 .519 -12.061 -2.349

Financing Activities

Net (decrease)/increase In Cash

-.069 -.459 -1.161 .350 3.062

and Cash Equivalents

Opening Cash & Cash

.204 2.065 1.260 1.107 19.895

Equivalents

Closing Cash & Cash

.135 1.606 .100 1.457 22.957

Equivalents

Source: http://www.moneycontrol.com/competition/kingfisherairlines/comparison/KA02, accessed April 20, 2012.

© HEC Montréal 18Kingfisher Airlines Nosedives: Can It Soar Again or Will It Remain Grounded?

Appendix 5

Main Airline Players in India

Positioning of Various Airlines in India

Kingfisher Airlines:

KFA was launched as an all-economy carrier with in-flight entertainment and food facilities.

After nearly a year of operations, the airline shifted its focus towards the luxury market and

began to offer premium-class service and world-class facilities to its customers. Accordingly,

KFA was re-positioned as an airline that offered best-in-class service and unmatched luxury.

Later, KFA offered Indian travellers a mix of premium, less premium and economy-class travel.

The airline kept on changing its positioning as per the changing business models.

IndiGo Airlines:

IndiGo launched its operations as a low-cost carrier and has strictly followed the low-cost model

from the start. IndiGo has continuously focused on OTP (on-time performance), which is a major

concern for airline flyers, and has successfully positioned itself as a carrier that reaches its

destinations on time. Punctual performance at a relatively low cost has been the major

positioning strategy of IndiGo.

Jet Airways:

Jet Airways is positioned as a full-service airline that offers its customers premium-class service,

along with a large network of flights operating both within India and on international routes. Jet

Airways has a large network connecting 20 international destinations and flights to and from 51

destinations in India. 1

Air India:

Air India, the national carrier, operates as a full-service domestic and international airline. The

positioning of Air India has been as a premium-class service provider with its focus on the

quality of the travel experience.

GoAir:

Go Air is apparently the only low-cost carrier in India that has introduced significant product

differentiation by offering greater value for a marginally higher premium to its passengers. ‘Go

Business’ fares are available at a price differential of $20 over the normal discounted ‘Go Smart’

fares. For a $20 premium, customers get added benefits such as zero cancellation charges until

24 hrs from departure and a refund of taxes and fees even upon no-show, zero rescheduling

charges, baggage allowance of up to 77 pounds (the industry average being 44 pounds for the

other LCCs). Additional features include complimentary food and beverages along with a

1

http://www.jetairways.com/EN/IN/AboutUs/OurNetwork.aspx, accessed March 8, 2013.

© HEC Montréal 19Kingfisher Airlines Nosedives: Can It Soar Again or Will It Remain Grounded?

guaranteed seat with extra leg room in the first two rows. The middle seat is left vacant, with only

the aisle and window seats being occupied. Passengers can check in at a separate counter at the

Mumbai and Delhi airports to avoid the long queues.

Key Statistics on the Indian Aviation Industry

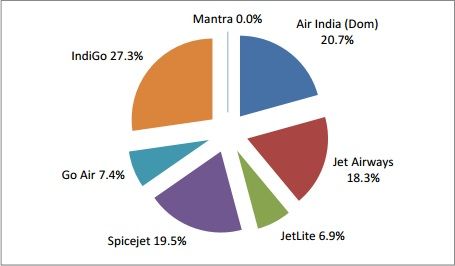

IndiGo Airlines was the market leader in November 2012, with a market share of 27.3%.

Market Shares of Scheduled Domestic Airlines

Source: http://dgca.nic.in/reports/stat-ind.htm, accessed on March 5, 2013

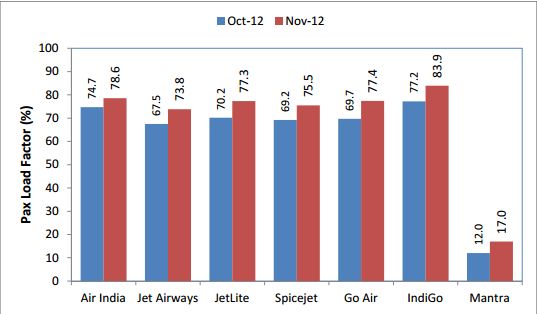

A marginal increase in the load factor for the month of November is due to increased travel

during the festive season. PSF (passenger load factor) here refers to the utilized capacity of the

total available capacity of an airline.

Passenger Load Factors of Scheduled Domestic Airlines as at November 2012

Source: http://dgca.nic.in/reports/stat-ind.htm, accessed on March 5, 2013

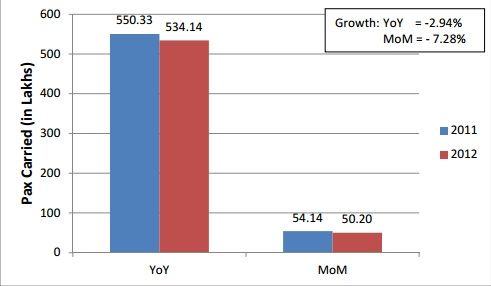

The number of passengers flown till November 2012 is marginally lower than the number of

passengers flown till November of the previous year 2011.

© HEC Montréal 20Kingfisher Airlines Nosedives: Can It Soar Again or Will It Remain Grounded?

Passengers Carried by Scheduled Domestic Airlines

Source: http://dgca.nic.in/reports/stat-ind.htm, accessed March 5, 2013

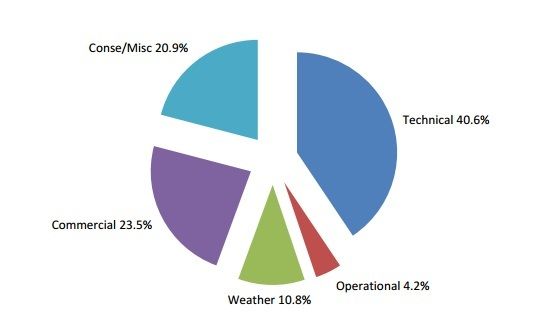

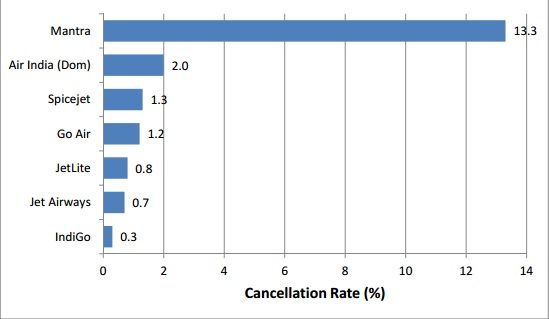

Cancellation Statistics of Scheduled Domestic Airlines

Source: http://dgca.nic.in/reports/stat-ind.htm, accessed March 5, 2013

The overall average cancellation rate for the six major airlines leaving out Mantra for the month

of November 2012 was 1.05%. The majority of the cancellations were due to technical problems.

© HEC Montréal 21Kingfisher Airlines Nosedives: Can It Soar Again or Will It Remain Grounded?

Reasons for Cancellation

Source: http://dgca.nic.in/reports/stat-ind.htm, accessed March 5, 2013

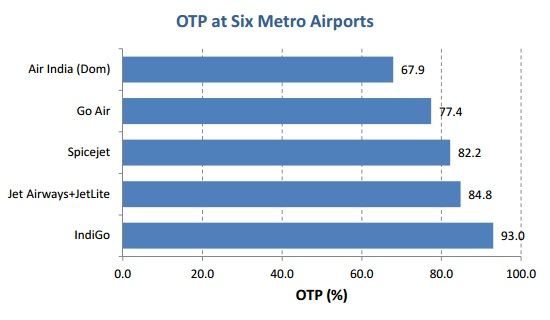

IndiGo Airlines is the industry leader in OTP, with a 93% success rate for on-time departures and

arrivals.

On-Time Performance (OTP) Statistics for Scheduled Domestic Airlines

Source: http://dgca.nic.in/reports/stat-ind.htm, accessed on March 5, 2013

© HEC Montréal 22Kingfisher Airlines Nosedives: Can It Soar Again or Will It Remain Grounded?

Fleet Statistics of Scheduled Domestic Airlines

Airlines No. of Aircraft (In Service )

Air India 106

Jet Airways 100

IndiGo 64

SpiceJet 51

GoAir 14

Source: http://dgca.nic.in/reports/stat-ind.htm, accessed on March 5, 2013

A Detailed Note on IndiGo Airlines: The Only Airline above the Red

IndiGo Airlines commenced operations in August 2006 and started off by positioning itself as a

“Not too expensive, not too cheap” airline. 1 It soon started making big strides in the domestic

aviation market, which was already cluttered with many strong competitors, and in March 2012,

it stood only second to Jet Airways in terms of market share. Today, it is the only profitable

airline operating in the Indian airspace. Industry experts attribute its phenomenal success and

growth to its efficient operational practices and systems.

The airline was co-owned by Rahul Bhatia and Sanjay Gangway, who was a former US Airways

chief executive. The airline also hired Bruce Ashby, a seasoned executive, as the CEO of the

airline and gave him sufficient autonomy and authority to guide the airline from the front. Bruce

Ashby took up his position a year ahead of the scheduled kick-off of the airline’s services in

2006. This gave him adequate time to familiarize himself with the business climate and to

strategize accordingly to ensure a smooth take-off for the airline.

IndiGo followed the low-cost model strictly and only operated a single type of aircraft, i.e., the

Airbus A-320 with single-class “economy” service. It pursued a strict policy of punctuality and

adopted the business model of a homogenous, low-cost, single-class, single aircraft, with no frills

and buy-on-board service. In 2005, it placed an order for 100 Airbus A-320 aircraft at the Paris

Air Show. It was the largest order in commercial aviation history. The big order made it possible

to negotiate favourable price terms and after-sale service agreements with Airbus in comparison

to its competitors. It was a master stroke. Apart from securing an excellent deal for the company,

it sent an extremely positive signal to passengers and the industry at large that the airline was in it

for the long haul.

The airline projected itself as an “on-time” operator and ceaselessly re-enforced its strict policy

of punctuality, which proved to be a brilliant selling proposition and increased corporate sales

quite handsomely.

The expansion plan adopted by the company was careful and measured. It ensured complete

understanding of the domestic air space before going international in January 2011. International

flights were launched in September 2011 between New Delhi and Dubai. In just over a week’s

1

http://articles.economictimes.indiatimes.com/2006-06-22/news/27439152_1_indigo-president-indigo-airlines-maiden-flight,

accessed June 21, 2012.

© HEC Montréal 23You can also read