Looking Ahead 2020 PROPERTY & CASUALTY CONSIDERATIONS FOR THE COMING YEAR - Woodruff Sawyer

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Looking Ahead 2020 PROPERTY & CASUALTY CONSIDERATIONS FOR THE COMING YEAR

TABLE OF CONTENTS

4 Introduction: Challenging Market Conditions Ahead

6 US Insurance Market Update: What Happened?

11 Property Update: Industry Losses Are Not Driving Your Premium

19 Casualty Market Update: Managing Risk Creatively

26 Am I Good Candidate for a Loss-Sensitive Program?

31 Cyber and Errors & Omissions: Do I Need to Cover Both?

36 Environmental Liability: A Dynamic Marketplace in 2020

41 Real Estate Development Trends: Tread Cautiously in 2020

47 US Healthcare Professional Liability Update—A Market Finally in Transition?

LOOKING AHEAD 2020 | WOODRUFF-SAWYER & CO. 3

INTRODUCTION:

CHALLENGING MARKET

CONDITIONS AHEAD

Carolyn Polikoff

Senior Vice President,

National Commercial Lines Practice Leader

415.402.6513 | cpolikoff@woodruffsawyer.com

View Bio

Most companies did not escape the tide insurance partners can create a sustainable

of rising premiums in 2019, leaving many insurance program that is relevant, no

executive teams and risk managers matter what the insurance pricing cycle may

wondering how to budget insurance costs be. In our Casualty Market Update we offer

for 2020. The common statement we hear alternative ideas to consider as you plan for

from our clients is: "Please tell me it's over." your 2020 insurance renewal. We also provide

specific advice around migrating to a loss

We have good news and bad news. The bad sensitive program.

news is that we do not expect rate relief in

the near future; but the good news is that Healthcare is one of the fastest growing

there are proactive measures insurance segments of our economy, so we've provided

buyers can take to lessen the impact of this some specific guidance to companies in

increasing rate environment. This Property & this sector. Furthermore, the construction

Casualty Looking Ahead Guide is full of tips to boom over the last several years has led to

help you plan for what lies ahead in 2020. increased insurance costs for developers,

so we've included advice on preparing for a

Starting early is a common theme you'll development project.

encounter in these pages. We know that

preparing for an insurance renewal does not Although we can't tell you the pain of

bring a lot of joy to the average insurance increasing rates will end in 2020, we assure

buyer and that can lead to procrastination. you that this is a cycle and it will pass. An

In decreasing rate environments, the experienced insurance broker will help

procrastinator can still get a good result you navigate all insurance cycles. Good

because underwriters are hungry for new preparation, effective loss control, and creative

business and eager to keep their renewals. In solutions are the elements of success in risk

increasing rate environments, underwriters management and insurance program design.

are more cautious. They focus on good loss We at Woodruff Sawyer look forward to being

control and submissions with inadequate a partner in your growth in 2020 and beyond.

information are often declined immediately.

Challenging market conditions also bring

an opportunity to control costs through

creativity. Insurance buyers who are open

to a collaborative conversation with their TABLE OF CONTENTS

LOOKING AHEAD 2020 | WOODRUFF-SAWYER & CO. 5

US INSURANCE MARKET UPDATE:

WHAT HAPPENED?

Carolyn Polikoff

Senior Vice President,

National Commercial Lines Practice Leader

415.402.6513 | cpolikoff@woodruffsawyer.com

View Bio

The increase in rates that started slowly

in 2018 and gained momentum in 2019 Average Commercial Pricing Increased

Every Quarter in Past Year

is expected to continue into 2020. The

5.2%

question on everyone's mind is: "When will

this end?"

3.5%

In our 2019 Property & Casualty Looking

Ahead Guide for commercial lines, published 2.4%

in November 2018, we predicted that

1.5% 1.6%

overcapitalization in the insurance sector

would likely result in soft market conditions

in most parts of the industry, except for

property, auto, and cyber. Q2 2018 Q3 2018 Q4 2018 Q1 2019 Q2 2019

Policyholder surplus—which is the capital Source: The Council of Insurance Agents & Brokers. Chart prepared by

Barclays Research.

buffer an insurance company has after it puts

aside money to pay claims—is an indicator

of insurance market capitalization, and it

continues to increase this year as it has

A Culmination of

the past several years. According to Verisk,

Costly Dynamics

policyholder surplus increased by $37.4 billion

in the first quarter of 2019. The year 2019 will likely be remembered

in the insurance industry as the year that

The following chart shows a decidedly

premiums caught up with reality. In the

upward movement in commercial lines' rates

property market, both 2017 and 2018 were

across all account sizes over the past five

two of the costliest years in terms of natural

quarters. The industry appears relatively

catastrophes, and by the end of 2018, many

healthy as measured by policyholder surplus,

were surprised that property premiums were

but rate increases seem to be accelerating

not increasing at a faster rate.

and are expected to continue doing so.

The casualty market experienced its own

reckoning in 2019 as loss trends across

multiple casualty sectors deteriorated.

Commercial auto has been problematic for

LOOKING AHEAD 2020 | WOODRUFF-SAWYER & CO. 7

the industry for years. According to a Fitch Impact on the Insurance

Ratings report, commercial auto premiums

Buyer—Is This a Hard Market?

have increased over 31 consecutive quarters,

but insurers still face underwriting losses. The CIAB chart provided confirms what most

insurance buyers already know: Premiums

The general liability/excess casualty space is are increasing at an accelerating rate.

best characterized by the phrase "frequency However, there are additional factors other

of severity." Historically, mega verdicts would than rate increases driving up premiums.

catch the public's attention, mainly because

they did not occur often. First, reinsurance premiums are up. Most

insurers use their balance sheet to pay a

This year alone, Johnson & Johnson was certain portion of a loss; the remainder

hit with a $572 million verdict in Oklahoma of the loss is passed to the reinsurance

related to its marketing of opioids, and the market. After the 2017 natural catastrophes,

manufacturer of Roundup weed killer (now reinsurance premiums rose slightly, but most

owned by Bayer) initially faced a $2 billion insurance companies absorbed the increase.

As reinsurance premiums continued to rise in

verdict involving allegations that the product

2019, insurers began to pass these increases

causes cancer. The verdict has since been

on to buyers.

reduced to $86.7 million, but other cases

against Roundup with the same allegations Second, capacity has decreased in certain

are ongoing. sectors. Capacity is the supply of capital that

an insurer will deploy to a given product or

Finally, the combination of an increasing

sector. Several Lloyd's of London syndicates

number of securities class actions and exited the property market in early 2019.

the Cyan, Inc. v. Beaver County Employees Furthermore, several US insurers drastically

Retirement Fund decision in 2018 have pushed cut limits in property and excess casualty

directors & officers liability premiums placements. Simple economics is in play—

upward. For a more detailed discussion of decreased supply of capital leads to

the D&O market, see our 2020 D&O Looking increased prices.

Ahead Guide.

ADDITIONAL FACTORS CONTRIBUTING

TO HIGHER PREMIUMS

Rising Decreasing

Reinsurance Capacity

Premiums (supply of capital)

8

We would be remiss if we did not attempt to Our opinion is that this is an optimistic view

address the initial question we posed: Why do (from the insurers' standpoint) that ignores

premiums continue to increase if the industry basic economic principles. That's true for a

appears relatively healthy as measured by number of reasons.

policyholder surplus?

First, the insurers we spoke with believe that

To answer this question, we spoke to many rates will continue to increase in the three-to-

of our top insurer partners and read their five year time period they cite. If that occurs,

comments in their public financial filings. We it will surely attract additional capital to the

discovered that there is uniform consensus industry because a capital provider will be

among US insurers: If the trends of costly paid more for the risk they take. Insurers

catastrophes and frequent and severe casualty sometimes forget that pesky economic

losses continue, insurer balance sheets will principle of supply and demand. More supply

weaken and thus jeopardize the industry's of capital will drive down premiums.

ability to pay large losses over time.

The impact on the buyer could be insolvency Although we differ with insurers on

of weaker insurers and/or a "hard market." the prediction that this environment

Technically, one cannot consider the will continue for another three to

insurance market of 2019 "hard" because five years, 2020 is not likely to bring

the vast majority of buyers can still get the premium decreases. In fact, the two

coverage they want, albeit more expensively. remaining sectors of the commercial

In a hard market, coverage is not available. market that seemed immune to

premium increases in 2019—workers’

compensation and cyber—may be

When Will This End?

joining the increasing-rates club.

Again, we regularly ask our insurance

company partners for their opinions on when

they expect this rising premium environment Furthermore, there is already a healthy

to end. Their responses range from three to supply of capital on the balance sheets of

five years, which is likely to cause many an most US insurers. A year or two of low natural

insurance buyer to gasp. catastrophes could lead to complacency,

which is likely to lead to loosened underwriting

standards and lower premiums.

LOOKING AHEAD 2020 | WOODRUFF-SAWYER & CO. 9

Workers' compensation premiums have been In 2020, expect to see premiums increasing

decreasing steadily over the past several across most commercial lines sectors.

years because the combined ratio—the The level of increases will be based on the

amount of losses an insurer pays out per quality of risk, i.e., good loss history and

premium dollar collected—has steadily risk management procedures will mitigate

decreased every year since 2011. Most increases. Be prepared to start your renewal

insurers have reported increased workers' process early to allow adequate time to fully

comp losses and many are forecasting the market your risk.

combined ratio to hit 100% in 2020.

Cyber is another area where trouble is

brewing. Most insurers have viewed this as

a growth product and therefore have

allocated big chunks of capital here. The

supply of capital has kept premiums down,

even in the wake of highly public breaches like

that of Equifax.

What changed in 2019 was the proliferation

of ransomware attacks, where a bad actor

threatens to release a company's information

or blocks access until a ransom is paid. That

ransom is insurable under most cyber

policies and insurers report increasing losses

in this area.

TABLE OF CONTENTS

10PROPERTY UPDATE:

INDUSTRY LOSSES ARE NOT

DRIVING YOUR PREMIUM

Casey Soares

Senior Vice President, Property Specialist

415.399.6458 | csoares@woodruffsawyer.com

View BioYes, the past two years saw the highest Hurricane Andrew in 1992, the World Trade

insured catastrophe losses on record and Center attacks in 2001, and Hurricanes

an ongoing stream of single-risk large Katrina, Rita, and Wilma in 2005 rendered

losses. And yes, carriers are increasing rates many companies insolvent or devoid of

and reducing coverage. But this is not your capital on which to write future business.

grandma's hard market.

This gave rise to the discrete "classes"

Perhaps this firming market is more akin to of companies providing much of today's

your grandma's tough love—the correction is traditional reinsurance, originally formed to

purportedly for your long-term benefit, but it provide much-needed capacity at high returns

still hurts. in those hard markets.

Until now, the cyclical nature of property Then followed a decade of below-average

pricing has been the result of market-changing catastrophe losses and steady influx of non-

events draining industry capital. It began in traditional (or "alternative") capital (see more

the reinsurance and retrocession markets and on this in our blog post).

trickled down to primary carriers.

Historical cycles of Rate-on-Line (pricing for reinsurance, premium/limit)

have been driven by market-turning loss events draining industry capital.

Source: Data from Guy Carpenter, presented by Artemis.bm

12Alternative capital drastically changed market dynamics by flooding

the industry with capacity over the last decade

Source: Aon Securities Inc.

And so it seemed the wheel had been broken, In 2017, global reinsurance capital (traditional

that the volume of capacity in the market and alternative) reached $605 billion. The

could never allow for a market-turning event. consensus among industry pundits pre-2017

was that a market-turning event would have

to be $200 billion. Then 2017–2018 losses

2017 was the highest insured catastrophe surpassed that on a combined basis, without

loss year on record, mostly due to Hurricanes

affecting the capitalization of the market.

Harvey, Irma, and Maria, and California wildfires

Despite record losses, rates remained stable

through YE 2018—confounding many of us

in the industry. For five years we reported

on unsustainable insurer practices of chasing

Source: Munich Re, III

business with double-digit rate decreases,

expanding terms, and reserve harvesting

(when insurers release funds they had set

aside to pay future losses).

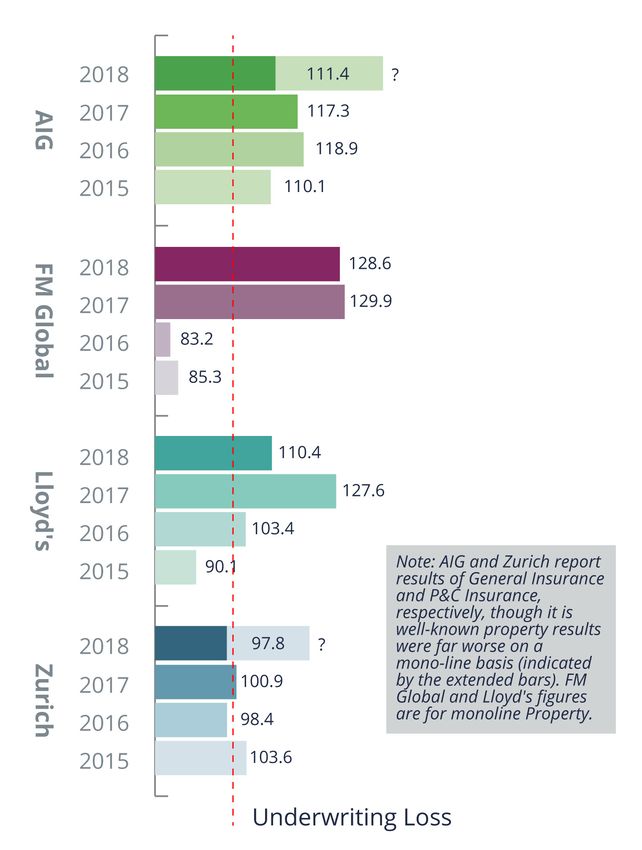

LOOKING AHEAD 2020 | WOODRUFF-SAWYER & CO. 13At the lowest point of the soft market,

Morgan Stanley estimated 30% of insurer Property results are driving carrier

earnings over the prior five years were from combined ratios well north of 100, producing

multiple years of underwriting losses

reserve harvesting alone. Still we pushed, and

the market continued to give way.

Until it didn′t.

Starting in 2017 and continuing today were

a remarkable number of severe single-risk

losses, each in the hundreds of millions, in

addition to the published natural catastrophe

industry loss figures. Each loss draws the

attention of management to see what was

being offered versus what was being charged,

shedding light on the Maserati-for-the-price-

of-a-minivan that had become commonplace

in the industry. (You're welcome.)

For property carriers across the board,

the catastrophe losses may have been the

weakening force, but the single-risk losses

delivered the knockout punch.

Source: Individual Company Results

With no foreseeable boost from investment

portfolios (mostly bonds, by regulation) and

worries of more reserve harvesting leading to This graph shows the combined ratio (loss

famine, insurers had to take the performance ratio + expense ratio) of some top property

of their businesses at face value. insurers and 100% is break-even. Some

carriers were collecting $1 and outlaying $1.30

for multiple years. When the ultimate goal for

all of us is a fulfillment of promises, insurer

solvency has to be a priority.

14A Market of Mass Disruption

In the ultra-competitive soft market,

Q1 2019 brought sweeping changes.

underwriters had to relax standards

At YE 2018, Lloyd's of London led the charge to keep and grow their books. No

by mandating syndicate plans to return sprinklers? "We can live with that."

More contingent time element?

to profitability, limiting stamp capacity for

"Ok, just show us some resiliency

some and prompting complete exits for

planning." HPR buildings in high-

others. Lloyd's controls the stock throughput

hazard cat zones? "Please, sir, I want

market, which is digging itself out of a worse

some more."

financial position than standard property, and

renewals reflect this with increases from 20%

up to 200%.

As carriers execute plans to ensure solvency,

AIG replaced its global property leadership and they willingly lose business that would

implemented a 40% RIF (reduction in force) threaten it. Carriers are reducing participation

of engineering staff. FM Global/AFM began across their books—single-carrier placements

an overhaul of its book of business to meet may need two to three participants to renew

strict underwriting standards. Zurich, AXA/XL, the same program, and long-standing shared-

Swiss RE Group, and others made the harsh and-layered placements may need additional

adjustments on price and coverage needed to or replacement markets.

reflect true exposures across their books and

Even so, carriers are beating budget with the

ensure preparedness for future losses.

increases achieved on the fewer accounts

Adding to the disruption is discontinuity that did renew at their terms. Many hit their

among client-broker-underwriter teams, budgeted written premium figures in the first

due to significant personnel turnover from part of 2019, leaving little incentive to write

broker consolidation and underwriters anything else unless it promises some serious

disenfranchised by new corporate mandates. return on capital.

Further, the industry's aging workforce has

positioned less experienced professionals at

BOTTOM LINE

Your account will be underwritten

the helm in this perfect storm. We felt those

anew and the market will support

effects managing through the catastrophe corrections towards actuarially

losses of 2017, and they're even more sound rates and coverage.

pronounced now.

LOOKING AHEAD 2020 | WOODRUFF-SAWYER & CO. 15Every Rose Has Its Thorn others. Canvassing the market for alternatives

is a must, though working with incumbents

When industry losses are behind market usually produces the most palatable result.

turns, rate increases feel arbitrarily punitive.

Thankfully, this is a horse of a different And yes, those improvements garnered

color. Renewal outcomes are extremely over years of positive renewals are toggles

individualized from insured to insured. Every that could offset an increasing premium.

account has its challenges, and the degrees But making those decisions only reinforces

of difficulty will determine approach and the need to truly know your risk and risk

outcome. By knowing your risk, you take tolerances, which goes far beyond output

control of your renewal. from computer models.

Each challenge has a commensurate course

of action, but some are more immediate than

Renewal outcomes are extremely individualized, depending

Renewal on

outcomes are extremely individualized, depending on the specific challenges of the account.

the specific challenges of the account

Renewal outcomes are extremely individualized, depending

on the specific challenges of the account

Rate Increases

Coverage Reductions: Limits,

Deductibles, Breadth

0 20 40 60 80 100 Low Coverage Reductions: Limits,High

Rate Increases Deductibles, Breadth

1

0 20 40 60 80 100 Low High

2

1

3

2

4

3

5

4

6

5

7

6

7 Note: For accounts with

1 Underreporting: ValuesExamples

to reflect current replacement costs 5

of Specific Challenges

have not increased No demonstrated commitment to carrier

recommendations for risk improvement

multiple challenges,

rate increases

Note: and with

For accounts

21 65

coverage

multiplereductions

challenges,

Underreporting:

Unconvincing Values

or lack have not increased

of Business No demonstrated commitment to carrier

to reflect current replacement costs Loss ratios over 100%for

recommendations in risk

last improvement

3 years are additive

rate increases and

Interruption modeling

but not necessarily

coverage 1:1

reductions

32 76

Unconvincing or lack of Business Difficult class:over

Loss ratios Ex. hazardous

100% in last 3 years are additive

High Maximummodeling

Interruption Foreseeable Loss (MFLs): manufacturing operations or frame

Inadequate protections for key locations construction real estate

but not necessarily 1:1

43 7

Difficult class: Ex. hazardous

High Maximum Foreseeable Loss (MFLs): manufacturing operations or frame Note: For accounts with

Inadequatecatastrophe

High-hazard protectionsexposure

for key locations construction real estate multiple challenges, rate

4

increases and coverage

High-hazard catastrophe exposure reductions are additive

but not necessarily 1:1

16So, What Did You Do on Your Looking Ahead

Soft Market Break?

We expect disciplined risk selection to

Some light-hearted commiserating with continue and prolong the sellers' market

underwriters one evening led to the characterized by increasing rates and

question, "For whom is this market most contracting coverage.

difficult, underwriter or broker?" to which all

the underwriters answered, "Definitely the Carriers will continue to refine appetites

broker!" We've since seen enough renewals and underwriting guidelines as leadership

in this environment to know it's actually evaluates the changes achieved by YE 2019.

answer C: client.

If your renewal is underway, this is the first

What did we do with the savings in both you're experiencing this market and results

money and time garnered over a decade will follow those outlined earlier. The million-

of soft market renewals? Did we address dollar question is whether accounts gearing

existing challenges via risk engineering, up for their second renewal, in March or later,

employee training, supply chain resiliency, will receive increases of similar magnitude a

business continuity plans, data capture, second time.

submission quality, and incumbent and

prospective carrier meetings? We predict the answer lies within measures

you've taken since that first wake-up call.

Clients ultimately make the tough calls on Renewals to date have focused on corrections

where to spend those premium dollars. Let's for pre-existing rate and coverage, but going

not forget the simultaneous hard market in forward there will be a more pronounced

directors and officers insurance, the growing flight to quality.

need for cyber, and other lines with their own

challenges requiring attention and premium. Accounts able to show efforts made to

address underwriter concerns will face

additional increases, but roughly 50% of the

Clients are making enterprise first, with a floor of 10% increase overall.

decisions and property is one piece Accounts showing up unprepared for their

of that puzzle. It may be the most second renewal will face another round of

labor-intensive line, but it is the harsh outcomes, and worse if they need to

most controllable. replace carriers.

LOOKING AHEAD 2020 | WOODRUFF-SAWYER & CO. 17Fallout from broker consolidation and

restructuring at key carriers will prompt

personnel movement across the industry

for the foreseeable future, prolonging the

disruption and adding to challenging renewals.

Specific trends in coverage changes include

increasing deductibles for accounts with

heavy Tier 1 wind, tornado/hail, and wildfire,

and reduced limits for flood and contingent

time element.

"It's a Relationship Business."

A closing thought on our industry adage: It is

truest in difficult losses and difficult markets.

Some lost sight of this in the soft market,

and it quickly went from cliché to karma

catalyst. Insurer capacity is not the limiting

commodity, but insurer attention is. With

submission flows up 50%-plus, underwriters

and management devote their efforts to

respected, collaborative partners—brokers

and clients alike.

We wish you the hard-fought satisfaction of

weathering this "hard" market in 2020.

TABLE OF CONTENTS

18CASUALTY MARKET UPDATE:

MANAGING RISK

CREATIVELY

Evan Hessel

Casualty Practice Leader, Property & Casualty

949.435.7387 | ehessel@woodruffsawyer.com

View BioWith great challenges come great policies every year since 2010, estimates SNL

opportunities. The broad hardening of the Financial. Insurers are forecast to pay out

market that casualty insurance experienced $1.12 in claims for every $1.00 of premium

over 2019 has stressed corporate insurance collected in the 2018 policy year.

budgets and jeopardized renewal outcomes

It is difficult to pinpoint the factors behind

for even the most prepared policyholders.

the rise in the number of auto liability claims,

The market shift also presents an

but analysts cite the increased number of

unprecedented opportunity for creative risk

highway miles logged by US commercial and

managers in 2020. The time to reimagine

personal drivers (as a result of a generally

insurance and risk financing programs for the

strong economy) as well as distracted driving

future is now.

behaviors as key factors in boosting the

In this article, I will detail the economic frequency of auto accidents.

forces driving current casualty underwriting

While the increased number of auto accidents

dynamics and dig into key strategies for

is concerning, it is the recent boom in claims

building a sustainable, cost-efficient

severity that has shaken underwriters and

insurance program.

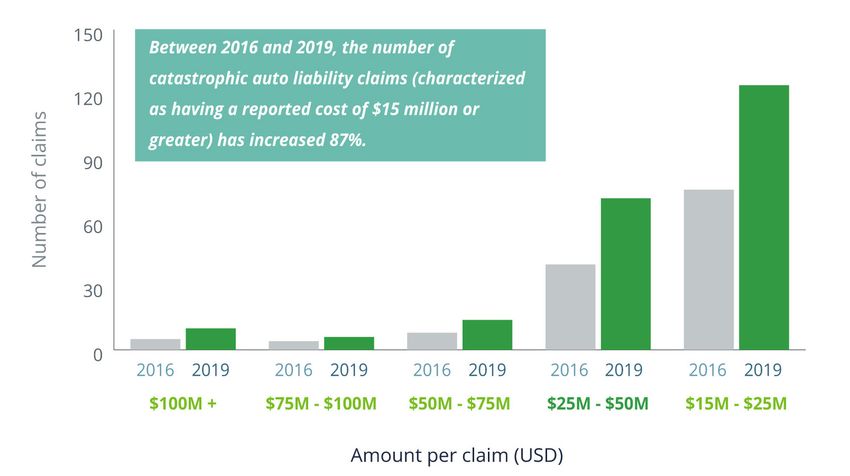

policyholders. Between 2016 and 2019, the

number of catastrophic auto liability claims

Casualty Market Loss Trends (characterized as having a reported cost of

$15 million or greater) has increased 87%,

"Frequency of severity" is the term

according to data collected by Advisen.

underwriters and brokers use to describe

the casualty insurance industry's recent

loss experience. Rather than an increase

in the number of claims or an increase

in the average size of claims, the current

environment is marked by an unprecedented

number of massive claims.

Auto liability is the line of coverage (rather

than general/products liability or workers'

compensation) that has predominantly cut

into insurers' profitability. The US insurance

industry has lost money on commercial auto

20Catastrophic Auto Liability Claim Counts & Settlements

“Catastrophic” equates to a cost of $15 million or greater

The number of catastrophic auto liability claims has

increased 87% since 2016.

Source: Advisen

Due to the confidential nature of settlements, Finally, while auto liability claims have garnered

it is difficult to obtain facts and circumstances an outsized portion of headlines lately, general

for claims and ascertain a pattern across cases. liability loss results have also deteriorated.

Still, underwriting executives and insurance The industry combined ratio has run over

industry analysts point to two recurring 100% since 2014, according to the Conning

themes in liability litigation: an empowered, Insurance Segment Report. Medical cost

well-financed plaintiff's bar and juries that are inflation, an increase in allegations of traumatic

increasingly willing to punish corporations with brain injuries, investor litigation funding, and

huge punitive damages judgments. In 2020, increased trial verdicts have dragged down

look for the insurance industry to intensify insurer profitability for general liability, explains

lobbying efforts in support of tort liability caps Liberty Mutual.

for personal injury cases (along the lines of the

non-economic damage caps that many states

have for medical malpractice claims).

LOOKING AHEAD 2020 | WOODRUFF-SAWYER & CO. 21Market Response: Decreased Making the hunt for aggressively priced

excess insurance capacity even tougher is

Capacity and Increased Rates

the wave of insurer consolidation over the

The casualty market's response to the past several years (for example, AXA and XL,

explosion of huge liability claims has been Liberty Mutual and Ironshore, Hartford and

a new focus on underwriting discipline and Navigators, among others).

rate adequacy.

With fewer insurers competing for

Whereas non-auto liability insurance lines business and a terrifying loss trend forcing

(such as umbrella/excess liability and general/ underwriters to strengthen their pricing

products liability) have experienced single- discipline, the job of a corporate insurance

digit average rate reductions over the past few manager building a cost-effective liability

years, insurers are seeking to hold rates flat program has become incredibly stressful.

for general liability (GL) coverage and obtain

modest rate increases for excess placements.

Creative Insurance Program

Underwriters have generally succeeded Design in a Hardening Liability

in their efforts to bump up rates. Among Market

participants in the Council of Insurance

Agents & Brokers' Commercial Property/ The current underwriting environment is

Casualty Market Report Q2 2019, 73% dangerous for insurance buyers who want

of policyholders experienced umbrella to maintain the status quo and rollover

rate increases, with 20% of respondents liability renewals using the same terms and

experiencing rate increases of 10%. conditions as in prior years. For creative

risk managers, the current market presents

Another challenging dynamic is that

a great opportunity for building insurance

underwriters are almost universally seeking

programs that can withstand large losses and

to reduce their capacity for umbrella policies.

insurance market gyrations.

(According to the CIAB study, some 53% of

policyholders had their umbrella limits cut at

their last renewal.)

Insurers’ newfound discipline in reducing their exposure to severe liability claims can best

be summed up in a cliché uttered by brokers and clients when discussing their lead umbrella

policies in 2019: “$10 million is the new $25 million.”

22Comprehensive Actuarial Increase Primary Retentions,

Evaluation: Initiate Renewal Primary Limits, and Umbrella

Planning Early Attachments

The first step towards building a For many corporations, liability program

new insurance program is to have a structures have remained the same for

comprehensive understanding of your own decades: Typically a $1 million or $2 million

loss experience, your peer group's loss primary liability (auto liability and general

histories, and underwriting performance for liability) limit with the umbrella attaching

the insurance industry in general. above that primary layer.

It is critical to conduct a detailed actuarial Given the increasing average severity

analysis forecasting losses at various of liability claims, particularly for auto

retention levels and back-test the costs and accidents, few insurers are willing to provide

benefits of different program structures. This aggressively priced umbrella policies at the

analysis should also quantify your firm's total historical attachments.

exposure to potential claims cost volatility

(as in, the total potential claims cost at worse A sensible alternative structure would involve

than expected outcomes for the entire increasing the deductible or self-insured

insurance program). retentions on the primary liability policies

to achieve premium savings on the primary

Additionally, insurance program managers

program. The savings could be deployed

should collaborate with their corporate

to fund the purchase of increased primary

finance team colleagues to evaluate different

general liability and auto liability limits. The

retention and limit structures alongside the

increased primary limits allow for a higher

corporation's capital structure, operational

umbrella attachment, which will increase

strategy, and tax structure.

insurer competition for the lead umbrella and

minimize premiums.

Understand your company’s loss experience

By absorbing more of the "working" layers of

Understand your peer group’s loss histories risk and relying less on the external insurance

Understand the current state of the general market, clients can make their programs

insurance market more sustainable and capable of weathering

market pricing fluctuations and large claims.

LOOKING AHEAD 2020 | WOODRUFF-SAWYER & CO. 23Of course, clients deploying this strategy Review Unconventional

must be confident they have the safety and

Insurance Arrangements

claims management controls in place to take

on additional retained risk. Several global insurers have created divisions

focused on "alternative risk" or "integrated

risk" underwriting. Among the products

Slice the Umbrella/Excess

offered by these groups are excess insurance

Layers programs that combine uncorrelated

As previously discussed, insurers are risks (such as excess auto/general liability,

increasingly uncomfortable providing a full property, management liability, and cyber)

$25 million umbrella liability policy. Embrace into single blocks of coverage with annual or

this market reality and break the first $25 multi-year aggregate limits.

million into different layer configurations

By combining multiple unrelated coverages

(such as five layers of $5 million each) as a

into a single contract over three years, clients

means for attracting the most aggressive

can achieve reduced overall pricing as well

insurers to the best layer for their

as cost certainty beyond a single policy

underwriting model.

year. A cautionary word, however: These

program structures often incorporate some

Consider Captives additional element of loss sensitivity and

require considerable underwriting and pricing

Captives are insurance company subsidiaries

efforts. It is recommended that clients begin

formed to underwrite the risks of their

designing and vetting these arrangements

parent company (and in some cases, the

earlier in the renewal cycle than with

risks of third parties). While a captive is not

conventional programs.

required to increase retained risk—and to

reduce a client's reliance on the commercial

insurance market—they can facilitate certain

useful underwriting strategies otherwise A CAUTIONARY WORD ON

unavailable. Examples of potentially useful ALTERNATIVE PROGRAM

captive strategies include using the captive STRUCTURES:

These structures may have

to take on risk in non-traditional structures

additional loss sensitivities. Begin

(such as quota sharing with an external

your design and evaluation of

insurer) and engaging reinsurers unwilling to

them earlier than you would with

write direct insurance policies to obtain hard- conventional programs.

to-place coverage.

24A Final Word on Punitive Damages Only 23 states allow for punitive damages claims to be legally covered by an insurance policy. The other states, including California, New York, and Florida, have statutes preventing insurers from covering punitive damages judgments assessed by courts against policyholders, regardless of policy language. These jurisdictional variances have the potential to create unexpected coverage gaps. Given the massive increases in the number of claims involving punitive damages awards, clients should review affirmative punitive damages coverage options with their broker. Many insurers' Bermuda subsidiaries can provide punitive wrap policies that provide for affirmative punitive coverage. While punitive wraps do add new cost items to insurance programs, they are increasingly valuable. In short, today's market is one that begs for a reimagining of insurance and risk financing programs. Risk managers need to be comfortable looking at alternative program structures that will be capable of withstanding whatever instability 2020 may bring. TABLE OF CONTENTS LOOKING AHEAD 2020 | WOODRUFF-SAWYER & CO. 25

AM I GOOD CANDIDATE

FOR A LOSS-SENSITIVE

PROGRAM?

Matthew Parsons

Account Executive, Construction

415.399.6348 | mparsons@woodruffsawyer.com

View BioAs we look ahead to 2020, insurance retention amount. The carrier will then pay

buyers may want to consider alternatives for all loss amounts that exceed the

to their insurance financing and risk retention amount.

management approach by making use

of loss sensitive programs. For the right

The insuring agreements, coverage

customer, these programs can help mitigate

terms, and exclusions typically

rate fluctuations, improve risk management

remain the same, regardless of

culture, and reduce costs. whether you choose a guaranteed

cost or loss sensitive program.

As your business grows, a risk

What is a Loss-Sensitive

versus reward analysis should be

Program? conducted to determine which

program is right for your firm.

Traditional or guaranteed-cost insurance is

"first dollar" insurance, where the insured

pays a fixed cost in the form of a premium

and the insurance carrier pays for all What Are My Options? Four

claims and administrative costs thereafter Types of Loss Sensitive

(beginning at "first" dollar). A loss sensitive Programs

insurance program is a plan where the

insurance cost will vary based upon the

1. Large Deductible Plans

insured's own loss experience.

These are most commonly used for a loss

For organizations with favorable loss sensitive plan where the insured pays

experiences, a loss sensitive program a reduced premium in exchange for a

provides an opportunity for significant large deductible. The insurer pays for all

premium savings and lower total cost of risk. claims within the deductible and seeks

But with that comes a risk of higher costs if reimbursement from the insured for losses

the experience is worse than expected. within the deductible plus claims-handling

fees. Collateral is used by the insurer as

In a loss sensitive program, the insured will

security for the unpaid losses.

pay a discounted fixed premium amount

in exchange for a higher retention, and will

be responsible for all losses up to a certain

LOOKING AHEAD 2020 | WOODRUFF-SAWYER & CO. 272. Retrospective Rating Plans insured retention. If the insured cannot or will

This is a formulaic approach to loss sensitive not meet their financial responsibility to pay

programs, similar to a large deductible the claim, the excess carrier is not expected

program, except in addition to the premium to pay the claims on a primary or first dollar

payment at inception, the insured will also basis. The insurer has no responsibility to pay

pay the insurer for the expected loss amount any claims until the SIR has been satisfied by

within the retention. the insured.

After the policy term, usually six months In an excess over SIR plan, there is no

after expiration, the premium and losses are collateral requirement. For workers’

adjusted based on actual experience, with compensations, because of the significant

excess loss funding returned to the insured. financial responsibility for all claims,

Adjustments then take place every 12 months companies are required to be approved by

until a "close out date." Some programs can the state as a "qualified self insurer." General

be closed as early as five years but the insurer liability is not a state-required coverage,

may leave a retro program open longer if so there isn't formal qualification for this

there are open claims. coverage. Carriers are reluctant to offer

excess over SIR plans and reserve these for

the most financially stable companies with

3. Excess Over Self-Insured Retention Plans

sophisticated claims-handling practices.

Sophisticated risk management and

insurance buyers are potential candidates

4. Captives

for excess over self-insured retentions (SIR).

Excess over SIR plans are very similar to In its simplest form, a captive is an insurance

large deductible plans given that the insurer company set up by the insureds themselves

provides coverage over the selected loss level for financing the risks of its owners and

of retention by the insured. participants. For more information on

captives, please see the Woodruff Sawyer

However, contrary to a deductible plan, where 2019 P&C Looking Ahead Guide for an article

the insurer pays for the claims and seeks on captives by Chris Kakel.

reimbursement within the retention, an excess

over SIR plan means the insured must fully pay

for the claims and seek reimbursement from

the carrier for the amount above the self-

28Factors That Determine a characteristics are imperative for loss

sensitive candidates since your company now

Good Loss Sensitive Candidate

has "skin in the game" and is paying part or

Before graduating your insurance program all of a claim (up to the retention).

from guaranteed cost to loss sensitive, assess

the following four areas: Predictable Loss History

Losses are not predictable, hence the reason

Premium Size for insurance. However, if your company

Loss sensitive programs are predicated on tracks claim frequency and severity, past

saving insureds the fixed dollar costs of claims history can be an excellent predictor of

guaranteed-cost programs in exchange for future loss exposure.

larger retentions. In order to be a candidate

for a loss sensitive program, a prerequisite is

to have enough guaranteed-cost premium to By working with your broker to

make a loss sensitive program feasible. understand trends and volatility,

you may discover that you can

Many insurance carriers have specific predict an annual average range

minimum premiums in order to be for expected losses with a relative

considered, but as a general rule, $350,000 degree of certainty.

of premium or more per line of business

(guaranteed-cost basis) could make a loss

sensitive option feasible from the carrier's This is extremely important in evaluating

perspective. A solid premium base allows the the expected total cost of risk (discounted

carrier to offer a material premium discount premiums for taking large retentions plus

to offset the retention of the insured. expected losses) and comparing them to your

guaranteed cost premium.

Company Culture and Sophistication of

Risk Management

Loss sensitive programs are built on the

concept of incentivizing good behavior, safe

work practices, and a proactive approach

to risk management and claims. These

LOOKING AHEAD 2020 | WOODRUFF-SAWYER & CO. 29Financial Stability • Taxes: There are tax implications to

If you are entering into a loss-sensitive participating in a loss-sensitive plan. Under

agreement with a carrier, this can have a long- both guaranteed-cost plans and loss

term impact on your company's financials. sensitive plans, premiums are deductible

It is important to understand the financial in the year they are paid. So, with a loss

position of your company and the impact a sensitive program you will pay less in

loss sensitive program can have on cash flow, premium due to the retention credit. Losses

credit lines, and taxes. paid within the retention are only tax

deductible when paid.

• Cash flow: Loss sensitive programs can

Determining whether your company is a good

offer a cash flow advantage because your

candidate for a loss sensitive option requires

initial premium is lower due to the retention

working with your broker to honestly evaluate

credit and the losses are paid out slowly

your firm's approach to risk management,

over time.

your appetite for risk, and your financial

• Credit risk: In large deductible programs, stability. Many insureds graduate from

the carrier will pay all losses and then guaranteed-cost options to loss sensitive

seek reimbursement for losses within options with the mindset of retaining risk

the retention, therefore creating a credit and reducing insurance costs through a

risk for the carriers. Due to this credit performance-driven risk management

risk, carriers will require some form of culture, all the while staying within a

security or collateral for the risk of not comfortable range of risk tolerance.

being reimbursed. As you renew your loss

sensitive program, the collateral position

will grow, but some credit may be applied

to the previous years' collateral position.

Carriers base their collateral decision on the

financial stability of your company and your

loss history.

TABLE OF CONTENTS

30CYBER AND ERRORS & OMISSIONS:

DO I NEED TO COVER BOTH?

Matthew Gauen

Senior Vice President, Property & Casualty

949.435.7357 | mgauen@woodruffsawyer.com

View BioThe terms "cyber" and "errors and security failure (virus/malware) and system

omissions" (E&O) are frequently used, failure (failed upgrade/patch or human error).

but often conflated. Going into 2020, it's

Cyber Liability: Media (third party) protects

more important than ever to understand the

difference between cyber liability and E&O, you from claims that you infringed someone

the intent of each coverage, and the circular else’s intellectual property (other than patent)

nature that can occur in an actual claim, not and advertising and personal injury (commonly

only for your own understanding, but to be excluded under a general liability policy for

able to explain these nuances to the board. companies that have an online presence).

The C-Suite has taken notice of the Errors and Omissions (third party) is

inescapable cyber threats companies face. separate from cyber liability coverage, and

Hearing about massive breaches or extortion protects from financial loss due to failure of

attacks will often draw their immediate your product/service to perform as designed.

attention. It is essential to know how to

address these concerns and make sure your Think of the above as broad coverage grants.

organization is prepared. It is equally, if not more, important to capture

what these policies don't cover. Typically,

there is no coverage for:

Cyber and E&O Coverage

Terms Defined • False/deceptive advertising

Let's make things clear by defining the terms • Antitrust/unfair trade

and understanding the intent of each coverage.

• Trade secrets

Cyber Liability: Network Security &

• Patent infringement

Privacy (first and third party) protects

against unauthorized access, transmission of • Product recall

a virus or malicious code, theft/destruction of

• License fees/royalties

data, cyber extortion, or exposing Personally

Identifiable Information (PII) or Personal • Lost value of own IP

Health Information (PHI).

• Loss of future profits

Cyber Liability: Network Business

• Business interruption caused by a

Interruption (first party) protects your

utility/ISP failure

company from an income loss due to a

32Although not all companies have an E&O as awareness of cyber risk increases. It is

exposure, all companies do have cyber recommended that organizations utilize both

liability exposure. There's an adage to internal and external information technology

describe the pervasiveness of cyber threats: services to manage a network.

companies fall into two categories: those that

have had a security breach and those that Cyber threats that are gaining momentum

don't know they've had a security breach.

Are your employees trained on cyber

security issues? Does it include:

Password management?

STILL HAVE QUESTIONS? Public wifi use?

Check out our post, Cyber Social engineering?

Insurance 101: What Does

Cyber Insurance Cover?

include cryptomining (hijacking computing

processing power) and ransomware attacks

And if you want to know how Woodruff Sawyer (targeted attacks seeking high ransom sums

can help you manage your cyber liability, in exchange for unlocking computer systems).

explore our cyber services, beyond insurance.

The message is clear: Place a higher value

on security over convenience and on "doing

Cyber Crimes Trends to Watch things safely" versus doing them quickly.

for 2020

Reports from various watchdogs indicate Common Board-Level Cyber

financial loss to organizations is on the

Do you have an incident response plan?

rise due to cyber crime. According to IBM's

Has it been tested?

Ponemon Institute's 2018 Cost of a Data Have you identified vendors to assist with

Breach study, the cost of the average data cyber security incident?

breach to a US company is a whopping $7.91

million, and the average time it takes to

identify a data breach is 196 days.

The combined impact of human error and

targeted phishing campaigns mean that

more organizations are being affected even

LOOKING AHEAD 2020 | WOODRUFF-SAWYER & CO. 33Questions the financial loss to your customer, i.e., their

cyber policy would seek reimbursement for

In the spirit of being prepared, the following their expenses from your E&O.

are six areas of concern we see most often:

Which Would Respond—Cyber or E&O?

States require employers to comply

There is nothing like a claim to prompt an

with notification laws whenever

understanding of how the coverage(s) work.

there has been a cyber security

The following scenarios are designed to breach. Clients can manage that on

identify what coverage would respond and their own or, if they have a cyber

illustrate what types of organizations might policy, the carrier will do it for them

need coverage for similar risks. once they learn which state(s) the

client had customers or employees.

In the following examples, we'll use a fictional

This is a major benefit of having

software company whose software product cyber coverage.

is a platform for doctors' offices, hospitals,

and clinics. They employ 1,000 employees

and often source hardware as part of the

software sale. Scenario 2: The software company's

systems are compromised and employee

Scenario 1: A customer's systems are

and customer data is exposed.

compromised and their employee and

customer data is exposed. Claim: Again, the owner of the data (in

this scenario, the software company) is

Claim: The owner of the data (in this case,

legally responsible for notifying all exposed

the software company's customer) is legally

employees and customers, which is covered

obligated to notify all exposed employees and

by their cyber liability policy. However, if it is

customers. They would need cyber liability

discovered that a third-party's product was

coverage to cover the expense of notification

the cause, then the company's cyber liability

and to comply with state notification

carrier would seek reimbursement from

requirements. However, if the software is

their E&O.

deemed the "weak link" and the cause of

the breach, you would need E&O to cover

34Scenario 3: The software company Together, this data allows brokers to develop

sourced hardware for a customer. The an incident cost estimate. The last step is

company modified that hardware to work to determine your company and board's

with its software and there was a glitch tolerance for risk. These all factor into the

limit you choose and the retention/co-

(the software company's fault), causing

insurance you are willing to accept.

a clinic to shut down and forcing all

potential patients to visit other clinics or a

nearby hospital. A Board-Level Concern

Claim: The software company would need Cyber liability for security and errors and

E&O for the financial loss to its customer omissions has grown to be a board-level

(lost revenue due to patients having to be concern. While it is the board's job to ask

redirected) as a result of the product's failure about cyber coverage, it's management's

to perform. job to know. To be sure, a good defense is

the best offense when it comes to security.

Understanding the circular nature of a claim

BE PREPARED determines who is legally responsible for

with the Woodruff Sawyer Cyber

notification, and is critical to determining

Liability Insurance Buying Guide

which coverage(s) are necessary. Know your

business, model your exposures, understand

contractual obligations, and determine an

How Much Limit Do You Need for appropriate limit based on risk tolerance.

Cyber Coverage? Now that you're prepared, put this topic on

There are several tools available to model the agenda as a discussion point at your next

a cyber event and they all require data. board meeting.

Modeling a limit involves translating the

number and type of individual customer

records at risk, location of the data,

protection, use of outside vendors (payment

processors, cloud providers, and the

contractual limits of liability with each), and

lost profit estimates, should your organization

be associated with a security incident or an TABLE OF CONTENTS

error or omission.

LOOKING AHEAD 2020 | WOODRUFF-SAWYER & CO. 35ENVIRONMENTAL LIABILITY:

A DYNAMIC MARKETPLACE

IN 2020

Parker Bunbury

Vice President, Construction

206.876.5383 | pbunbury@woodruffsawyer.com

View BioLooking ahead to 2020, there are a where we have seen a significant reduction

number of trends to keep an eye on in of market appetite and the addition of higher

the environmental liability sector. The deductibles, or "per door" deductibles.

environmental liability marketplace remains

Quite the opposite is true for properties with

dynamic with the vast majority of coverage

complex life histories or businesses looking

still being written on surplus lines paper.

for longer policy terms (seven to 10-years),

This allows for a tremendous amount of

which are common in transactional deals.

product customization, but also confuses

The appetite remains extremely small, but

clients with the lack of standardized forms

meaningful coverage is still available.

and endorsements.

We cannot stress enough that meaningful

It is common for businesses to obtain the

coverage is available. Many businesses fail

wrong coverage, so it's prudent to work with

to obtain environmental coverage for their

a knowledgeable insurance broker when

unique exposures and liabilities. It requires

purchasing environmental coverage. Each

intensive underwriting, recent data, and

market has its own unique coverage forms

property information (Phase 1, Phase 2,

and all coverage terms are fully negotiable.

testing and/or monitoring results, no further

It's important to know that subtle differences

action letters, remedial action plans, etc.)

in policy term language such as "sudden and

and working with an environmental specialist

accidental" rather than "sudden and gradual"

to obtain meaningful coverage terms and

significantly impact coverage terms. With that

reasonable pricing.

in mind, let's discuss what we are seeing with

some of the environmental products.

Contractors' Pollution Liability

Pollution Legal Liability (PLL) (CPL)

Market capacity and appetite remain strong The marketplace for contractors' pollution

for premises pollution legal liability (PLL) liability (CPL) coverage remains strong with

insurance, specifically for new conditions coverage terms continuing to broaden;

coverage on one to five-year policy terms for most markets are now offering incidental

properties with clean life histories. For now at professional coverage on all of their CPL

least, mold coverage is still widely available, policies. The market capacity is large and

with the exception of hospitality/hotel risks pricing is extremely competitive. It is worth

considering whether a practice policy or a

LOOKING AHEAD 2020 | WOODRUFF-SAWYER & CO. 37project policy make the most sense, and also If you are a tenant or lessee, the important

worth noting that many carriers will offer a thing is to avoid purchasing coverage that

per project aggregate on practice policies. only protects your landlord or lender. There

is meaningful coverage that will also comply

with your contractual obligation. We would

UNDERGROUND STORAGE typically recommend a PLL product to our

TANKS (UST) clients versus a secured creditor/lender

We continue to see businesses liability policy that only protects the lender,

have compliance issues with their for example.

underground storage tanks (UST) and

recommend reading, "The Problem On the flip side, if you are a lender or a

with Storage Tanks: What you Need landlord, in a perfect world you would have

to Know to Own or Operate."

a PLL or secured creditor policy for your

liability, and your tenant or lessee would have

a PLL policy for their operations.

Environmental Liability For quick clarification: A secured creditor

Coverage for Lessees and policy does one of two things in the event of a

Lenders default resulting from an environmental loss.

It will either pay off the remaining balance or

Lease and lender requirements for

pay to clean up the property, whichever costs

environmental liability coverage are

less. We all know that perfect world scenarios

continuing to trend and the frequency has

don't occur frequently and there are other

increased significantly. We believe this is due

options to consider.

to the nature of environmental claims, which

are typically very severe and costly when Require your tenant or lessee to carry PLL

they occur. coverage with a limit and deductible that

you feel adequately protects the asset in the

Lenders and landlords are ultimately looking event of an environmental claim. One million

to protect themselves and their assets dollars does not go very far with a significant

through the policies that tenants and lessees environmental claim given that legal

are required to carry. If your organization has expenses can typically run high, so you might

not come across this yet, you likely will in the consider $2 million or more depending on the

near future. unique circumstances of the property and

lessee. You should also require to be listed as

an additional insured.

38You can also read