MIDDLE EAST & NORTH AFRICA INVESTMENT OPPORTUNITIES IN FOOD & DRINK: RISK/REWARD ANALYSIS

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

MIDDLE EAST & NORTH AFRICA INVESTMENT OPPORTUNITIES IN FOOD & DRINK: RISK/REWARD ANALYSIS

MENA Investment Opportunities In

Food & Drink: Risk/Reward Analysis

Published by: BMI Research

BMI Research © 2018 Business Monitor International Ltd

30 North Colonnade, All rights reserved.

London

E14 5GN, UK All information contained in this publication is

Tel: +44 (0)207 248 0468 copyrighted in the name of Business Monitor

Fax: +44 (0)20 7248 0467 International Ltd, and as such no part of this

Email: subs@bmiresearch.com publication may be reproduced, repackaged,

Web: http://www. bmiresearch.com redistributed, resold in whole or in any part, or used in

any form or by any means graphic, electronic or

mechanical, including photocopying, recording, taping,

or by information storage or retrieval, or by any other

means, without the express written consent of the

publisher.

DISCLAIMER

All information contained in this publication has been researched and compiled from sources believed to be accurate and reliable at the time of

publishing. However, in view of the natural scope for human and/or mechanical error, either at source or during production, Business Monitor

International Ltd accepts no liability whatsoever for any loss or damage resulting from errors, inaccuracies or omissions affecting any part of the

publication. All information is provided without warranty, and Business Monitor International Ltd makes no representation of warranty of any

kind as to the accuracy or completeness of any information hereto contained.MENA Investment Opportunities in Food & Drink: Risk/Reward Analysis

CONTENTS

MENA Food & Non-Alcoholic Drinks: Sin Tax Won't Impede Top Ranked UAE ....................................... 3

Sin Tax: Not A Major Threat To Consumption ........................................................................................................................................................... 4

UAE Still An Outperformer ......................................................................................................................................................................................... 6

Morocco Outperforms North Africa And Two GCC Markets ...................................................................................................................................... 7

Saudi Arabia - Q1 2018 .................................................................................................................................. 12

Egypt - Q1 2018 .............................................................................................................................................. 14

Iran - Q1 2018 ................................................................................................................................................. 16

United Arab Emirates - Q1 2018 ................................................................................................................... 17

Methodology .................................................................................................................................................. 19

Food & Drink (Non-Alcoholic Drinks) Risk/Reward Index ....................................................................................................................................... 20

Food & Drink (Alcoholic Drinks) Risk/Reward Index, Indicators ....................................................................................................................... 23

Food & Drink (Alcoholic Drinks) Risk/Reward Index............................................................................................................................................... 24

Food & Drink (Alcoholic Drinks) Risk/Reward Index, Indicators ....................................................................................................................... 27

© Business Monitor International Ltd Page 2MENA Investment Opportunities in Food & Drink: Risk/Reward Analysis

MENA Food & Non-Alcoholic Drinks: Sin Tax Won't

Impede Top Ranked UAE

BMI View: MENA ranks fourth out of six regions globally in our Food and Non-Alcoholic Drinks

Risk/Reward Index. The Middle Eastern sub-region remains the outperformer, occupying the top five

MENA spots. We highlight Morocco as a North Africa bright spot, placing in sixth position in the region

and first in North Africa, outperforming two of the GCC markets.

Middle East Remains Top Pick To North Africa

MENA - Food & Non-Alcoholic Drinks Risk/Reward Heat Map

Note: Scores out of 100; higher score= more attractive market. Source: BMI

Important Note: Our entire Food & Drink Risk/Reward Index (RRI) includes two Food & Drink

Risk/Reward indices: our Food & Non-Alcoholic Drinks RRI and our Alcoholic Drinks RRI. The first

quantifies the risks and rewards associated with food and non-alcoholic drink sales in each country, while

the other quantifies the risks and rewards associated with the alcoholic drinks sector.

Main Regional Features And Latest Updates

The Middle East and North Africa (MENA) region is ranked fourth in BMI's Food & Non-

Alcoholic Drinks RRI. The regional average RRI score is 47.0, compared to the global average

of 50.0.

The UAE remains the most attractive market in the region for food and non-alcoholic drinks in

MENA and is the region's only country to score within the global top 10.

Our top five countries in our MENA RRI score above the global average of 50.0.

Morocco slips out of the top five, ranking sixth. Its sixth position is worth highlighting, as it far

exceeds it North African regional peers as well as two Gulf Cooperation Council (GCC)

markets.

© Business Monitor International Ltd Page 3MENA Investment Opportunities in Food & Drink: Risk/Reward Analysis

Strong Rewards Balanced With Risks

MENA - Food & Non-Alcoholic Drinks Risk/Reward Index

Note: Scores out of 100; higher score = more attractive market. Source: BMI

Sin Tax: Not A Major Threat To Consumption

The UAE has introduced excise tariffs at a rate of 100% on tobacco and energy drinks, and 50% on

sugary drinks, with the law coming into effect on October 1 2017. Following in the footsteps of Saudi

Arabia, which implemented a similar levy in June 2017, the move towards so-called 'sin taxes' by GCC

states aims to discourage consumption of unhealthy products, while also providing a welcome boost to

fiscal revenues amid the low oil price environment.

© Business Monitor International Ltd Page 4MENA Investment Opportunities in Food & Drink: Risk/Reward Analysis

Affluent Consumer Able To Absorb Added Cost

UAE - Household Disposable Income Breakdown

f = BMI forecast. Source: BMI, UAE National Bureau of Statistics

In terms of sales and consumption of carbonates, we believe the overall impact of the excise duty in the

UAE will be limited. We have only slightly adjusted our forecasts for consumption of carbonated drinks

in response to the tax, with the five-year (2017-2021) compound annual growth rate (CAGR) projected to

be 4.9%, compared to 5.2% CAGR previously.

Below we outline the key factors behind this modest revision:

We were already forecasting slower growth in carbonates relative to other soft drinks categories,

such as mineral water and fruit and vegetable juices, as we were already anticipating health

consciousness trends to prevail in consumption patterns.

The tax will have minimal impact on our carbonates forecasts for 2017 given that it does not

come into effect until Q417. We forecast 5.1% y-o-y growth in 2017, down from 5.35% y-o-y

previously. We expect to see a more marked slowdown in growth in 2018, with sales growth

slowing by one percentage point to 4.7% y-o-y.

The majority of consumers in the UAE are high earners, with our forecasts showing over three

quarters of the population having disposable incomes of USD25,000-plus in 2017, and 44% with

a disposable income of USD50,000-plus. Given that retail prices of carbonated drinks in the

UAE range between AED1.5 (USD0.40) and AED3 (USD0.80), this level of disposable income

is more than sufficient to absorb a 50% to 100% price increase.

© Business Monitor International Ltd Page 5MENA Investment Opportunities in Food & Drink: Risk/Reward Analysis

The regressive nature of the tax means lower-income consumers will be hardest hit, particularly

as these consumers tend to purchase carbonated drinks on a frequent basis, often due to a lack of

awareness of health concerns such as obesity.

Energy drinks such as Red Bull are most exposed. We expect consumers to switch to other

beverages for sources of caffeine, such as coffee or carbonates - which have a lower price point

to begin with and are subject to a 50% rather than 100% tax rate.

UAE Still An Outperformer

The UAE is the MENA region's outperformer in our Food & Non-Alcoholic Drinks RRI, with the country

obtaining a score of 74.0 out of 100. This score places the country in the top 10 globally, finishing in third

position. The UAE is, however, the only MENA state to place within the global top 10, with the region's

second-placed state, Saudi Arabia, trailing the UAE by some distance with a score of 61.7, which equates

to 29th place out of 107 states measured worldwide in our RRI.

The UAE's top regional position is earned through high scores for both industry rewards and industry

risks, scoring highly for per capita food and drink spending. While the country and the population might

be relatively small and so the volume of food and drink consumption is lower, the comparative wealth of

the population ensures high spending levels on food and drink. The country also offers growth potential

for the sector, with the household spending real growth outlook over the next five years (2017-2021)

projected by BMI to average an annual increase of 4.1%. The UAE's strong food and drink spending

growth outlook ensures the country's industry reward score of 79.6, which is the highest industry reward

score in the region.

© Business Monitor International Ltd Page 6MENA Investment Opportunities in Food & Drink: Risk/Reward Analysis

UAE Top Market

UAE And MENA RRI Breakdown

Note: Scores out of 100, higher score = more attractive market. Source: BMI

From an industry risks perspective, the UAE benefits from its position as a regional business and logistics

hub. This has meant that the country has developed a robust regulatory framework for international

companies to operate in and a strong infrastructure network, with its airports and ports functioning as

transhipment points, offering companies plenty of supply chain options at competitive rates. The

country's industry risk score of 79.9 is also a high score for the country by comparison to the region.

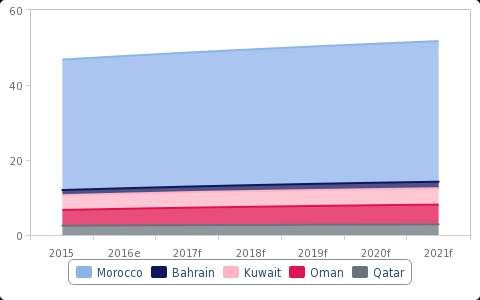

Morocco Outperforms North Africa And Two GCC Markets

Morocco stands out in our MENA Food and Non-Alcoholic Drinks RRI owing to it high score for North

Africa of 50.5. This places Morocco in sixth place out of 14 MENA markets, far higher than other North

African peers. Morocco ranks first in the sub-region (North Africa) and we also highlight that the country

outperforms two of the GCC countries - Bahrain and Oman. Bahrain scores 44.2 and Oman scores 45.5,

ranking ninth and eighth respectively.

© Business Monitor International Ltd Page 7MENA Investment Opportunities in Food & Drink: Risk/Reward Analysis

Morocco Offers Large Consumer Base

Selected Countries - Population (mn)

f = BMI forecast. Source: National sources, BMI

Morocco benefits from a large population of over 35mn and an urban population of close to 60%, leading

to a rewards score of 52.8. Although Bahrain and Oman have high urbanisation rates of nearly 90% and

80% respectively, they each are home to a consumer base of less than 5mn. However, we caution that

Morocco's risks scores reflect the key downside risks to operating in a North African market. Its risks

score of 44.9 is below the two aforementioned GCC countries, due to higher logistics risks and much

weaker retail formalisation.

© Business Monitor International Ltd Page 8MENA Investment Opportunities in Food & Drink: Risk/Reward Analysis

MENA Food & Non-Alcoholic Drinks Risk/ Reward Index

Rewards & Risks Scores

Note: Scores out of 100, higher score = more attractive market. Source: BMI

© Business Monitor International Ltd Page 9MENA Investment Opportunities in Food & Drink: Risk/Reward Analysis

MENA Food & Non-Alcoholic Drinks Rewards

Industry Rewards & Country Rewards Scores

Note: Scores out of 100, higher score = more attractive market. Source: BMI

© Business Monitor International Ltd Page 10MENA Investment Opportunities in Food & Drink: Risk/Reward Analysis

MENA Food & Non-Alcoholic Drinks Risks

Industry Risks & Country Risks Scores

Note: Scores out of 100, higher score= more attractive market. Source: BMI

Please Note: Our Risk/Reward Indices are updated frequently and, as a result, scores in this section may

not match scores in the rest of the report.

© Business Monitor International Ltd Page 11MENA Investment Opportunities in Food & Drink: Risk/Reward Analysis

Saudi Arabia - Q1 2018

BMI View: Saudi Arabia's food and drink sector faces a number of challenges which will dampen

growth prospects for investors over the short term. Anaemic economic growth, combined with new

regulations such as the selective tax on sugary drinks and tobacco and restrictions on non-Saudi

employees in the grocery retail sector, raise the risks for companies operating in the market. We maintain

a more optimistic outlook over the back end of our 2017-2021 forecast period as the economy picks up in

line with oil prices, with Saudi Arabia offering one of the largest and most youthful consumer bases in the

MENA region.

Food And Drink Spending

(2014-2021)

e/f = BMI estimate/forecast. Source: BMI, national statistics

Latest Updates And Industry Developments

The Saudi Arabian economy will fall into recession in 2017 before returning to modest growth in

2018. With our expectations for oil sector growth to remain in negative territory in the second

half of 2017, and for the government's paring back of fiscal consolidation measures to only

slowly feed through to stronger consumer spending, we are now forecasting a recession of 0.5%

in 2017, before gradually picking up to 1.3% in 2018.

Saudi Arabia's Ministry of Labour and Social Development has confirmed plans to ban foreign

workers from jobs in grocery stores by 2020. The move is part of the kingdom's wider

'Saudisation' agenda which aims to reduce unemployment among Saudi nationals. We believe

© Business Monitor International Ltd Page 12MENA Investment Opportunities in Food & Drink: Risk/Reward Analysis

this poses a downside risk to investment by grocery retailers as it will increase operating costs

and drive up wage pressures.

Soft drink companies operating in Saudi Arabia are lowering prices and rolling out smaller can

sizes in an effort to mitigate against weaker demand following the introduction of 100%

selective tax on sugary and energy drinks in June 2017.

As part of Vision 2030 and the Kingdom's wider economic diversification efforts, Saudi Arabia's

food processing sector will continue to attract considerable investment, particularly in key

segments such as dairy and halal.

Looking beyond the short-term economic slowdown, premiumisation and rising health

awareness will fuel dynamism in Saudi Arabia's food and drink market over our five-year

forecast period, as consumers increasingly adopt Western-influenced consumption patterns.

© Business Monitor International Ltd Page 13MENA Investment Opportunities in Food & Drink: Risk/Reward Analysis

Egypt - Q1 2018

BMI View: While high inflation remains a major issue for Egypt's food and drink industry, we expect the

pressures on consumer purchasing power and profit margins to gradually ease from 2018 onwards.

However, prices of imported products will remain elevated over the near term, and the majority of

consumers will prioritise the purchasing of staple food and drink items, while switching to discounters,

private labels and local produce wherever possible.

Food And Drink Spending

2014-2021

e/f = BMI estimate/forecast. Source: BMI, national statistics

Latest Updates And Industry Developments

Surging prices have hurt the food sector as Egyptians choose to downgrade to cheaper

alternatives or go without discretionary products.

In US dollar terms, BMI forecasts a 26% contraction in headline food sales over 2017. However,

a recovery is expected in 2018, following sharp devaluation in the Egyptian currency.

Egypt's rising interest rates and soaring inflation have hit second quarter profits at the country's

largest food companies, providing evidence that consumers' purchasing power is being squeezed.

Knockmart Food Industries and Jumia Egypt announced in a joint statement in November 2017

that they have entered into a strategic partnership to launch online grocery platform Jumia Fresh.

© Business Monitor International Ltd Page 14MENA Investment Opportunities in Food & Drink: Risk/Reward Analysis

Because of their early-mover advantage and Jumia's expertise in e-commerce in Egypt, we

believe the new platform will become a major force in the country's nascent online grocery

market.

Edita Food Industries launched a new product, Todo Donuts, in October 2017, further

consolidating its position as the leader in Egypt's packaged snack food market. This follows the

opening of a new production facility in July 2017. The company now has five facilities in Egypt,

encompassing 28 production lines and a nationwide distribution network. The firm's customer

base includes more than 67,000 wholesale and retail customers, while it exports to more than 16

markets in the region.

© Business Monitor International Ltd Page 15MENA Investment Opportunities in Food & Drink: Risk/Reward Analysis

Iran - Q1 2018

BMI View: Rising urbanisation and a large youth population will bolster Iran's consumer market. Over

our forecast period to 2021, we expect Iran to present increasingly attractive opportunities for food and

drink companies, further supported by rising income levels.

Food And Drink Spending

(2014-2021)

e/f = BMI estimate/forecast. Source: BMI, national statistics

Latest Updates And Industry Developments

Although we expect diversification in consumer tastes and preferences, spending on staple foods

such as rice and bread will still form an important part of local diets and remain dominant.

We forecast strong growth for Iran's non-alcoholic drinks sector, growing at a compound annual

growth rate of 12.2% over 2017-2021, in local currency terms.

Iran's food retail market is dominated by small independent retailers and open air markets.

Organised food retail accounts only for around 10% of the total sales, a figure which we expect

to increase gradually over the next five years. Considering their local knowledge, regional

companies hold a distinct advantage entering Iran's highly prospective mass grocery retail

market, while other investments are likely to come in a form of joint ventures with local

partners.

© Business Monitor International Ltd Page 16MENA Investment Opportunities in Food & Drink: Risk/Reward Analysis

United Arab Emirates - Q1 2018

BMI View: In line with consumer spending more broadly, our outlook for the UAE food and drink

market remains positive over our 2017-2021 forecast period. Ongoing rises in disposable incomes

combined with increasing adoption of Westernised consumption patterns will drive industry growth,

particularly for premium food and drink products. While we note downside risks posed by regulatory

changes such as the imposition of a tax on tobacco and sugary drinks in late 2017, and VAT in 2018, we

believe the overall impact will be limited due to the affluence of the consumer base and relatively low

retail prices to begin with.

Food And Drink Spending

(2014-2021)

e/f = BMI estimate/forecast. Source: BMI, National statistics

Latest Updates And Industry Developments

Health consciousness trends are starting to prevail in the consumption patterns, with slower

growth in carbonated soft drinks.

Fast-evolving e-commerce sector will present new growth opportunities for retailers to penetrate

the market.

The UAE will introduce excise tariffs at a rate of 100% on tobacco and energy drinks and 50%

on sugary drinks from October 2017. The UAE will be the second country in the Arabian Gulf to

© Business Monitor International Ltd Page 17MENA Investment Opportunities in Food & Drink: Risk/Reward Analysis

introduce excise taxes after Saudi Arabia began implementing the tax at the same rate in June

2017.

In terms of sales and consumption of carbonates, we believe the overall impact of the excise duty

in the UAE will be limited. We have only slightly adjusted our forecasts for consumption of

carbonated drinks in response to the tax, with the five-year compound annual growth rate

(CAGR) projected to be 5.0%, compared to 5.2% CAGR previously.

India's Hielo Beverages, maker of premium healthy soft drinks, will enter the UAE market at the

end of 2017 under its flagship brand name PEAUR. The initial roll out will see the company

promoting their PEAUR Natural Mineral Water sourced in the Himalayas and PEAUR nectar

based fruit juices. Initially the company has tied up with exclusive retail outlets in Dubai, but

plans to expand more widely.

Majid Al Futtaim, which owns the franchise rights for Carrefour in MENA, acquired Retail

Arabia in July 2017, the franchise owner of Geant hypermarkets in UAE, Bahrain and Kuwait,

and will rebrand its 29 stores under the Carrefour brand before the end of 2017.

© Business Monitor International Ltd Page 18MENA Investment Opportunities in Food & Drink: Risk/Reward Analysis

Methodology

BMI Food & Drink Forecasting & Sourcing

How We Generate Our Industry Forecasts

BMI's industry forecasts are generated using the best-practice techniques of time-series modelling and

causal/econometric modelling. The precise form of model we use varies from industry to industry, in each

case being determined, as per standard practice, by the prevailing features of the industry data being

examined. BMI mainly uses OLS estimators and in order to avoid relying on subjective views and

encourage the use of objective views, BMI uses a 'general-to-specific' method. BMI mainly uses a linear

model, but simple non-linear models, such as the log-linear model, are used when necessary. During

periods of 'industry shock', for example a deep industry recession, dummy variables are used to determine

the level of impact.

Effective forecasting depends on appropriately-selected regression models. BMI selects the best model

according to various different criteria and tests, including, but not exclusive to:

R2 tests explanatory power; Adjusted R2 takes degree of freedom into account

Testing the directional movement and magnitude of coefficients

Hypothesis testing to ensure co-efficients are significant (normally t-test and/or P-value)

All results are assessed to alleviate issues related to auto-correlation and multi-co-linearity

BMI uses the selected best model to perform forecasting.

It must be remembered that human intervention plays a necessary and desirable role in all of BMI's

industry forecasting. Experience, expertise and knowledge of industry data and trends ensures that

analysts spot structural breaks, anomalous data, turning points and seasonal features where a purely

mechanical forecasting process would not.

Within the Food & Drink industry, this intervention might include, but is not exclusive to: significant

company expansion plans; new product development that might influence pricing levels; dramatic

changes in local production levels; product taxation; the regulatory environment and specific areas of

legislation; changes in lifestyles and general societal trends; the formation of bilateral and multilateral

trading agreements and negotiations; political factors influencing trade; and the development of the

industry in neighbouring markets that are potential competitors for foreign direct investment.

© Business Monitor International Ltd Page 19MENA Investment Opportunities in Food & Drink: Risk/Reward Analysis

Example of Food Consumption Model:

(Food Consumption)t = β0 + β1*(GDP)t + β2*(Inflation)t + β3*(Lending Rate)t + β4* (Foreign

Exchange Rate)t + β5*(Government Expenditure)t + β6*(Food Consumption)t-1 + εt

Sourcing

BMI uses the following sources in the compilation of data, developments and analysis for its range of

Food & Drink reports: national statistics offices; local industry governing-bodies and associations; local

trade associations; central banks; government departments, particularly trade, agricultural and commerce

ministries; officially-released information and financial results from local and multinational companies;

cross-referenced information from local and international news agencies and trade press outlets; figures

from global organisations, such as the World Trade Organization (WTO), the World Health Organization

(WHO), the United Nations Food and Agricultural Organization (FAO) and the Organisation for

Economic Co-operation and Development (OECD).

Food & Drink (Non-Alcoholic Drinks) Risk/Reward Index

Our Food & Drink (Non-Alcoholic Drinks) Risk/Reward Index (RRI) quantifies and ranks a country's

attractiveness within the context of the Food & Drink (Non-Alcoholic Drinks) industry, based on the

balance between the Risks and Rewards of entering and operating in different countries.

We combine industry-specific characteristics with broader economic, political and operational market

characteristics. We weight these inputs in terms of their importance to investor decision making in a given

industry. The result is a nuanced and accurate reflection of the realities facing investors in terms of:

1) the balance between opportunities and risk; and

2) between sector-specific and broader market traits.

This enables users of the index to assess a market's attractiveness in a regional and global context.

The index uses a combination of our proprietary forecasts and analyst assessments of the regulatory

climate. As regulations evolve and forecasts change, so the index scores change providing a highly

dynamic and forward-looking result.

The Food & Drink (Non-Alcoholic Drinks) Risk/Reward Index universe comprises 107 countries.

© Business Monitor International Ltd Page 20MENA Investment Opportunities in Food & Drink: Risk/Reward Analysis

Benefits of using BMI's Food & Drink (Non-Alcoholic Drinks) RRI

Global Rankings: One global table, ranking all the countries in BMI's universe for Food & Drink

(Non-Alcoholic Drinks) from least (closest to zero) to most attractive (closest to 100).

Accessibility: Easily accessible, top down view of the global, regional or sub-regional

Risk/Reward profiles.

Comparability: Identical methodology across 107 countries for Food & Drink (Non-Alcoholic

Drinks) allows users to build lists of countries they wish to compare, beyond the confines of a

global or regional grouping.

Scoring: Scores out of 100 with a wide distribution, provide nuanced investment comparisons.

The higher the score, the more favourable the country profile.

Quantifiable: Quantifies the rewards and risks of doing business in the Food & Drink (Non-

Alcoholic Drinks) sector in different countries around the world and helps identify specific

flashpoints in the overall business environment.

Comprehensive: Comprehensive set of indicators, assessing industry-specific risks and rewards

alongside political, economic and operating risks.

Entry Point: A starting point to assess the outlook for the Food & Drink (Non-Alcoholic Drinks)

sector, from which users can dive into more granular forecasts and analyses to gain a deeper

understanding of the market.

Balanced: Multi-indicator structure prevents outliers and extremes from distorting final scores

and rankings.

Methodology is a combination of proprietary BMI forecasts, analyst insights and globally

acceptable benchmark indicators (for example, World Bank's Doing Business Scores,

Transparency International's Corruption Perceptions Index).

© Business Monitor International Ltd Page 21MENA Investment Opportunities in Food & Drink: Risk/Reward Analysis

Weightings Of Categories And Indicators

Food & Drink (Non-Alcoholic Drinks) Risk/Reward Index

Source: BMI

The RRI matrix is divided into two distinct categories:

Rewards

Evaluation of an industry's size and growth potential (Industry Rewards), and also macro industry and/or

country characteristics that directly impact the size of business opportunities in a specific sector (Country

Rewards).

Risks

Evaluation of micro, industry-specific characteristics, crucial for an industry to develop to its

potential (Industry Risks) and a quantifiable assessment of the country's political, economic and

operational profile (Country Risks).

Assessing Our Weightings

Our matrix is deliberately overweight on Rewards (60% of the final RRI score for a market) and within

that, the Industry Rewards segment (60% of the final Rewards score). This is to reflect the fact that when

it comes to long-term investment potential, industry size and growth potential carry the most weight in

indicating opportunities, with other structural factors (demographic, labour statistics and infrastructure

availability) weighing in, but to a slightly lesser extent. In addition, our focus and expertise in emerging

and frontier markets has dictated this bias towards industry size and growth to ensure we are able to

identify opportunities in countries where regulatory frameworks are not as developed and industry sizes

© Business Monitor International Ltd Page 22MENA Investment Opportunities in Food & Drink: Risk/Reward Analysis

are not as big (in USD terms) as in developed markets, but where we know there is a strong desire to

invest.

Indicators - Explanation And Sources

Food & Drink (Alcoholic Drinks) Risk/Reward Index, Indicators

Indicator Source Rationale

Rewards

Industry Rewards

Denotes per capita spending on food & non-alcoholic drinks in

F&D Spending Per Capita BMI Forecast USD. Wealthier populations spend more on F&D products.

Denotes food & non-alcoholic drinks sector dynamism as a %.

Scores based on annual average growth over our five-year

F&D Five-Year Growth Rate BMI Forecast forecast period.

Denotes total household spending on food & non-alcoholic

drinks in USDbn. Large markets score higher than smaller

Total F&D Expenditure BMI Forecast ones.

Country Rewards

Size of the population in millions as a measure for the total

Population BMI Forecast addressable market.

Proportion of households with an income that exceeds

USD10,000. Excludes those in poverty but demonstrates

Mass Affluent Class BMI Forecast potential demand for branded products.

Size of the urban population in millions. Higher urban

population size is a positive for distribution, higher economic

development and accessing products through a network of

Urban Population BMI Forecast retailers.

Proportion of the population between 20-39 years old as a %.

This is typically the range that companies target as a high

Spending Population BMI Forecast spending/trendsetting generation.

Risks

Industry Risks

Uses Operational Risk's Economic Openness as a proxy for

BMI Operational determining the ease of entering and doing business in a

Regulatory Environment Risk Index market.

Uses our urban/rural split (%) data as a proxy for determining

the level of retail/hospitality formalisation in the market. Highly

urbanised markets allow companies to easily serve more

F&D Formalisation BMI Forecast consumers.

Uses Operational Risk's Logistics Risk to determine the risks

and costs associated with moving products around a market.

BMI Operational Higher scores indicate quality transport, cheap fuel/electricity

Logistics Risk Risk Index and high levels of tech adoption

Country Risks

© Business Monitor International Ltd Page 23MENA Investment Opportunities in Food & Drink: Risk/Reward Analysis

The Long-Term Economic Risk Index takes into account the

structural characteristics of economic growth, the labour

market, price stability, exchange rate stability and the

Long-Term Economic Risk BMI Country Risk sustainability of the balance of payments, as well as fiscal and

Index Index external debt outlooks for the coming decade.

The Short-Term Economic Risk Index seeks to define current

vulnerabilities and assess real GDP growth, inflation,

unemployment, exchange rate fluctuation, balance of payments

Short-Term Economic Risk BMI Country Risk dynamics, as well as fiscal and external debt credentials over

Index Index the coming two years

The Long-term Political Risk Index assesses a country's

structural political characteristics based on our assumption that

liberal, democratic states with no sectarian tensions and broad-

BMI Country Risk based income equality exhibit the strongest characteristics in

Long-Term Political Risk Index Index favour of political stability, over a multiyear timeframe.

The Short-Term Political Risk Index assesses pertinent political

BMI Country Risk risks to investment climate stability over a shorter time frame,

Short-Term Political Risk Index Index up to 24 months forward.

The Operation Risk Index focuses on existing conditions

BMI Operational relating to four main risk areas: Labour Market, Trade and

Operational Risk Index Risk Index Investment, Logistics, and Crime and Security.

Source: BMI

Food & Drink (Alcoholic Drinks) Risk/Reward Index

Our Food & Drink (Alcoholic Drinks) Risk/Reward Index (RRI) quantifies and ranks a country's

attractiveness within the context of the Food & Drink (Alcoholic Drinks) industry, based on the balance

between the Risks and Rewards of entering and operating in different countries.

We combine industry-specific characteristics with broader economic, political and operational market

characteristics. We weight these inputs in terms of their importance to investor decision making in a given

industry. The result is a nuanced and accurate reflection of the realities facing investors in terms of:

1) the balance between opportunities and risk; and

2) between sector-specific and broader market traits.

This enables users of the index to assess a market's attractiveness in a regional and global context.

The index uses a combination of our proprietary forecasts and analyst assessments of the regulatory

climate. As regulations evolve and forecasts change, so the index scores change providing a highly

dynamic and forward-looking result.

The Food & Drink (Alcoholic Drinks) Risk/Reward Index universe comprises 90 countries.

© Business Monitor International Ltd Page 24MENA Investment Opportunities in Food & Drink: Risk/Reward Analysis

Benefits of using BMI's Food & Drink (Alcoholic Drinks) RRI

Global Rankings: One global table, ranking all the countries in BMI's universe for Food & Drink

(Alcoholic Drinks) from least (closest to zero) to most attractive (closest to 100).

Accessibility: Easily accessible, top down view of the global, regional or sub-regional

risk/reward profiles.

Comparability: Identical methodology across 90 countries for Food & Drink (Alcoholic Drinks)

allows users to build lists of countries they wish to compare, beyond the confines of a global or

regional grouping.

Scoring: Scores out of 100 with a wide distribution, provide nuanced investment comparisons.

The higher the score, the more favourable the country profile.

Quantifiable: Quantifies the rewards and risks of doing business in the Food & Drink (Alcoholic

Drinks) sector in different countries around the world and helps identify specific flashpoints in

the overall business environment.

Comprehensive: Comprehensive set of indicators, assessing industry-specific risks and rewards

alongside political, economic and operating risks.

Entry Point: A starting point to assess the outlook for the Food & Drink (Alcoholic Drinks)

sector, from which users can dive into more granular forecasts and analysis to gain a deeper

understanding of the market.

Balanced: Multi-indicator structure prevents outliers and extremes from distorting final scores

and rankings.

Methodology is a combination of proprietary BMI forecasts, analyst insights and globally

acceptable benchmark indicators (for example, World Bank's Doing Business Scores,

Transparency International's Corruption Perceptions Index).

© Business Monitor International Ltd Page 25MENA Investment Opportunities in Food & Drink: Risk/Reward Analysis

Weightings Of Categories And Indicators

Food & Drink (Alcoholic Drinks) Risk/Reward Index

Source: BMI

The RRI matrix is divided into two distinct categories:

Rewards

Evaluation of an industry's size and growth potential (Industry Rewards), and also macro industry and/or

country characteristics that directly impact the size of business opportunities in a specific sector (Country

Rewards).

Risks

Evaluation of micro, industry-specific characteristics, crucial for an industry to develop to its

potential (Industry Risks) and a quantifiable assessment of the country's political, economic and

operational profile (Country Risks).

Assessing our Weightings

Our matrix is deliberately overweight on Rewards (60% of the final RRI score for a market) and within

that, the Industry Rewards segment (60% of the final Rewards score). This is to reflect the fact that when

it comes to long-term investment potential, industry size and growth potential carry the most weight in

indicating opportunities, with other structural factors (demographic, labour statistics and infrastructure

availability) weighing in, but to a slightly lesser extent. In addition, our focus and expertise in emerging

and frontier markets has dictated this bias towards industry size and growth to ensure we are able to

identify opportunities in countries where regulatory frameworks are not as developed and industry sizes

are not as big (in USD terms) as in developed markets, but where we know there is a strong desire to

invest.

© Business Monitor International Ltd Page 26MENA Investment Opportunities in Food & Drink: Risk/Reward Analysis

Indicators - Explanation And Sources

Food & Drink (Alcoholic Drinks) Risk/Reward Index, Indicators

Indicator Source Rationale

Rewards

Industry Rewards

Denotes per capita consumption of Alcoholic Drinks in litres.

Measures which populations consume more on alcohol

Alcohol Consumption Per Capita BMI Forecast products at the individual level rather than total size.

Denotes Alcoholic Drinks sector dynamism as a %. Scores

based on annual average growth over our five-year forecast

Alcohol 5-Year Growth Rate BMI Forecast period.

Denotes total consumption of Alcoholic Drinks in millions of

Total Alcohol Consumption BMI Forecast litres. Large markets score higher than smaller ones.

Country Rewards

Size of the population in millions as a measure for the total

Population BMI Forecast addressable market.

Proportion of households with an income that exceeds

USD10,000. Excludes those in poverty but demonstrates

Mass Affluent Class BMI Forecast potential demand for branded alcohol products.

Size of the urban population in millions. Higher urban

population size is a positive for distribution, higher economic

development and accessing products through a network of

Urban Population BMI Forecast retailers.

Proportion of the population between 20-39 years old as a %.

This is typically the range that companies target as a high

spending/trendsetting generation and are generally over the

Spending Population BMI Forecast legal drinking age.

Risks

Industry Risks

Uses Operational Risk's Economic Openness as a proxy for

BMI Operational determining the ease of entering and doing business in a

Regulatory Environment Risk Index market.

Uses our Urban/Rural Split (%) data as a proxy for determining

the level of retail/hospitality formalisation in the market. Highly

urbanised markets allow companies to easily serve more

F&D Formalisation BMI Forecast consumers.

Uses Operational Risk's Logistics Risk to determine the risks

and costs associated with moving products around a market.

BMI Operational Higher scores indicate quality transport, cheap fuel/electricity

Logistics Risk Risk Index and high levels of tech adoption

Country Risks

The LT ERI takes into account the structural characteristics of

economic growth, the labour market, price stability, exchange

rate stability and the sustainability of the balance of payments,

BMI Country as well as fiscal and external debt outlooks for the coming

Long Term Economic Risk Index Risk Index decade.

© Business Monitor International Ltd Page 27MENA Investment Opportunities in Food & Drink: Risk/Reward Analysis

The ST ERI seeks to define current vulnerabilities and assess

real GDP growth, inflation, unemployment, exchange rate

BMI Country fluctuation, balance of payments dynamics, as well as fiscal

Short Term Economic Risk Index Risk Index and external debt credentials over the coming two years

The LT PRI assesses a country's structural political

characteristics based on our assumption that liberal,

democratic states with no sectarian tensions and broad-based

BMI Country income equality exhibit the strongest characteristics in favour

Long Term Political Risk Index Risk Index of political stability, over a multiyear timeframe.

The ST PRI assesses pertinent political risks to investment

BMI Country climate stability over a shorter time frame, up to 24 months

Short Term Political Risk Index Risk Index forward.

The ORI focuses on existing conditions relating to four main

BMI Operational risk areas: Labour Market, Trade and Investment, Logistics,

Op Risk Index Risk Index and Crime and Security.

Source: BMI

© Business Monitor International Ltd Page 28You can also read