Mines & Money: World Mining Congress Australia Day Presentation - December 2008 EXCO RESOURCES N.L.

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Mines & Money: World Mining Congress

Australia Day Presentation

EXCO RESOURCES N.L.

December 2008

Presented by Michael Anderson – Managing Director

DISCLAIMER

This presentation contains forward looking statements that are subject to risk factors associated

with resources businesses. It is believed that the expectations reflected in these statements are

reasonable but they may be affected by a variety of variables and changes in underlying

assumptions which could cause actual results or trends to differ materially, including but not

limited to: price fluctuations, actual demand, currency fluctuations, drilling and production

results, reserve estimates, loss of market, industry competition, environmental risks, physical

risks, legislative, fiscal and regulatory developments, economic and financial market conditions

in various countries and regions, political risks, project delay or advancement, approvals and

cost estimates.

All references to dollars, cents or $ in this presentation are to AUS$ currency, unless otherwise

stated.

Information in this presentation relating to mineral resources and exploration results is based on

data compiled by Exco’s Exploration Manager Stephen Konecny, BSc Hons Geo. (MAusIMM),

Mr Mike Dunbar, (who is a full time employee of the Mitchell River Group and a consultant to

Exco Resources Ltd), and who is a member of The Australasian Institute of Mining and

Metallurgy, and Mr Laurie Barnes (who is a full time employee of the Mitchell River Group and a

consultant to Exco Resources Ltd) and who is a member of the Australian Institute of

Geoscientists. Mr Konecny, Mr Dunbar and Mr Barnes have sufficient experience which is

relevant to the style of mineralisation and type of deposit under consideration and to the activity

which they are undertaking to qualify as Competent Persons under the 2004 Edition of the

Australasian Code for reporting of Exploration Results, Mineral Resources and Ore Reserves.

Mr Konecny, Mr Dunbar and Mr Barnes consent to the inclusion of the data in the form and

context in which it appears.

2

AGENDA

• Introduction to Exco

¾ Financial Summary

¾ Corporate Strengths

• Project Portfolio

¾ Queensland Copper Projects

¾ South Australia – White Dam

• Development Options

¾ Cloncurry Copper Project (CCP)

¾ Ore Supply scenario

¾ White Dam Joint Venture

¾ Ivanhoe Joint Venture

• Why invest in Exco?

3

SNAPSHOT OF EXCO (ASX:EXS)

EXS – Ordinary Shares 254,083,625

- Employee Options 14,500,000

Share Price (20/11/08) A$0.10

- 12-month range A$0.10 - A$0.43

Market Capitalisation (undiluted) A$25.4M

(fully diluted) A$26.8M

Current Cash (at end Q3/08) A$10.6M

Board of Directors

Major Shareholders

Barry Sullivan Chairman

Ivanhoe Australia Ltd 19.9 %

Michael Anderson Managing Director

Alasdair Cooke Executive Director Lion Selection Group Limited 10.4 %

Craig Burton Non-Exec Director Alasdair Cooke 6.4 %

Peter Reeve Non-Exec Director TOP 10 56 %

4

CORPORATE STRENGTHS

CASH POSITION The Company has a healthy cash position and

remains adequately funded to achieve immediate

objectives

MANAGEMENT Exco’s Board & Management team have a track

record of delivery, and a commitment to create long

term value for shareholders

QUALITY ASSETS Exco has large, strategic ground holdings in some

of Australia’s most prospective base metal terrains.

The established resources provide a critical mass

which underpins the Company’s development

strategies

OPPORTUNITY Exco’s project portfolio offers a number of near-

term opportunities to create cash flow and a

platform to grow a significant business

PROJECT

EXCO RESOURCES N.L.

PORTFOLIO

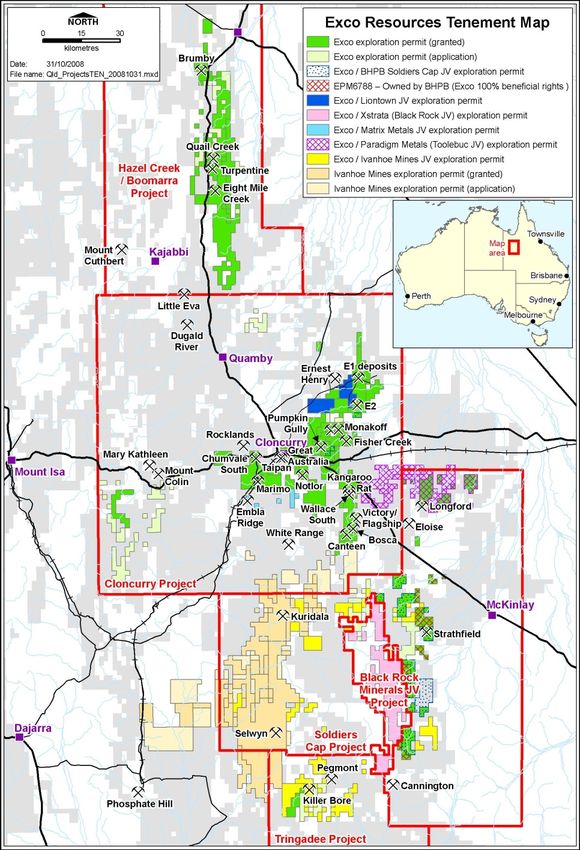

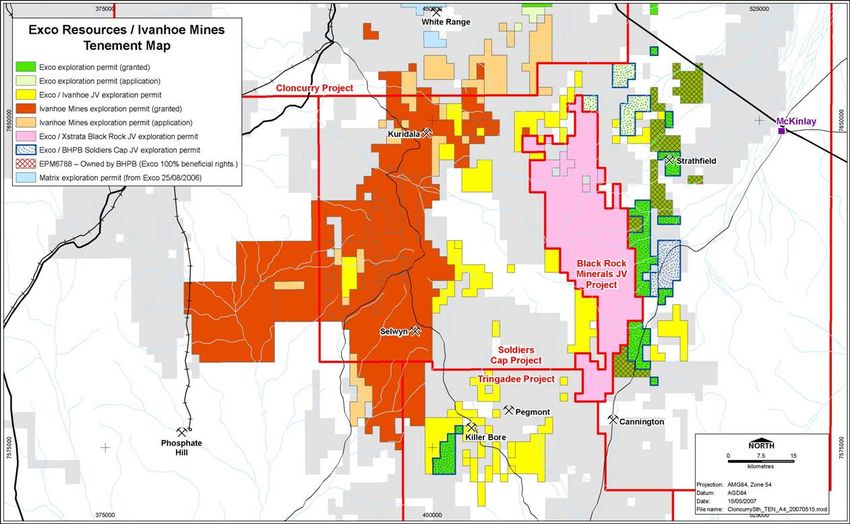

NW QUEENSLAND

Exco holds a strategic 4,100km2, land

position across 3 main centres in QLD:

- Cloncurry

- Hazel Creek / Boomarra

- Soldiers Cap / Tringadee

Geology highly prospective for Cu-Au-U

Key Activities:

(1) Resource Development

(2) Regional Exploration

(3) Joint Ventures

(4) Project Development

7

NW QLD - RESOURCE BASE

GRADE METAL

PROJECT DEPOSIT JORC TONNES

Cu % Au g/t Cu T Au Oz

E1 North * 63% Indicated 12,300,000 1.00 0.29 122,900 116,700

E1 South 40% Indicated 18,200,000 0.67 0.18 121,900 103,900

E1 East Inferred 8,000,000 0.83 0.26 66,000 65,500

CLONCURRY Monakoff * 49% Indicated 1,902,000 1.58 0.48 30,100 29,400

COPPER

PROJECT Monakoff East Inferred 700,000 1.25 0.36 8,700 8,000

Great Australia * 65% Indicated 2,134,000 1.54 0.13 32,900 8,900

SUB - TOTAL 43.2 Mt 0.88 0.24 382,400 332,500

Taipan Inferred 1,460,000 0.80 0.1 11,600 5,000

Kangaroo Rat * Inferred 875,000 1.65 1.0 14,400 28,000

Mt Colin * 64% Indicated 667,195 3.43 - 22,880 -

OTHER Turpentine 88% Indicated 1,841,000 1.03 0.2 19,000 11,800

Wallace South Inferred 1,000,000 - 1.6 - 53,000

Victory - Flagship Inferred 196,000 1.20 1.4 2,300 8,800

SUB - TOTAL 6.0 Mt 1.16 0.55 70,180 106,600

TOTAL 49.3 Mt 0.92 0.28 452,580 439,100

* Granted Mining Leases

8

NW QLD - RESOURCE GROWTH

60 Indicated >100% increase in Resource

“NEW”

Inferred INTERIM TARGET

Tonnage over last 2 years with

TOTAL further upside

50

R eso u rce T o n n ag e (M t)

Contained Cu up by 89% & contained

40 Au up by 128%

On track to exceed 50Mt of total

30 resource

New “Interim target” of 60Mt &

20 >500,000t of Cu by mid 2009

Current drilling will convert a total of

10

≥25Mt in-pit resources to Indicated

category

0

2006 2007 2008 2009 “Critical Mass” in place for the

Cloncurry Copper Project

YEAR

9

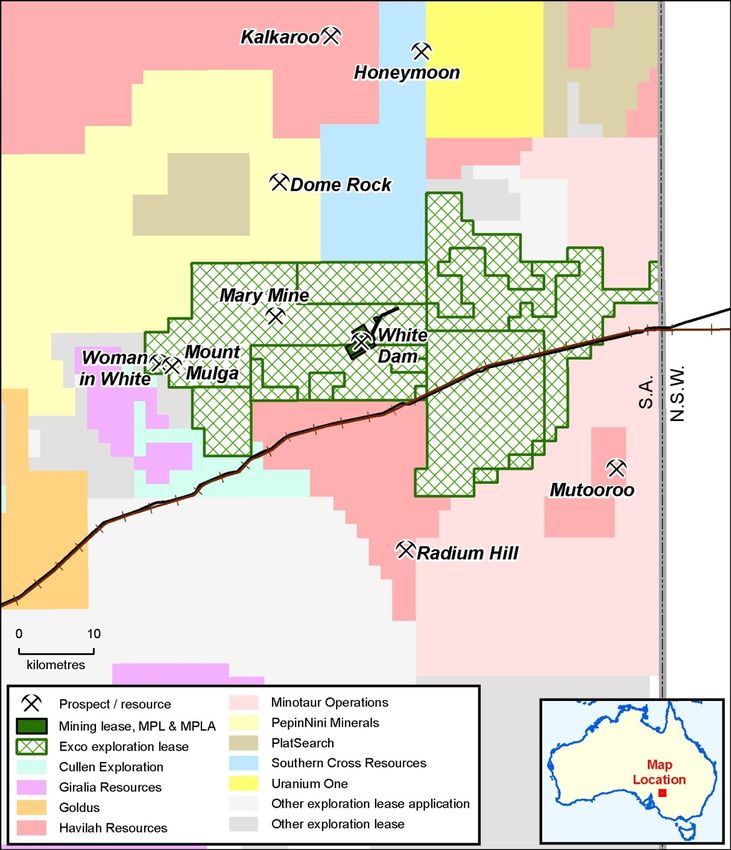

SOUTH AUSTRALIA

White Dam Gold Project

Final approval imminent

Proposed JV with Polymetals

Completing detailed project

implementation planning &

financial modeling

Regional Exploration

Highly prospective yet largely

untested area for:

• Gold

• Base Metals

• Uranium

Numerous geophysical

anomalies require follow-up

10WHITE DAM RESOURCE BASE

¾ Total Resource – 9.1 Mt @ 1.13 g/t Au for 330,400 ounces

¾ White Dam “in-pit” Oxide – 4.5 Mt @ 1.27 g/t Au

¾ Project upside from Vertigo – 1.78 Mt @ 1.28g/t Au

¾ Further potential at Vertigo, White Dam & White Dam North

White Dam Gold Project - Mineral Resource Estimate

(0.5g/t cut-off grade applied at White Dam; 0.7g/t cut-off grade applied at Vertigo)

Deposit Indicated Inferred Total

Tonnes g/t Tonnes g/t Tonnes g/t Ounces

White Dam Oxide 5,529,000 1.12 8,000 1.59 5,538,000 1.12 199,900

White Dam Fresh 493,000 1.13 1,288,000 0.96 1,781,000 1.01 57,600

Sub -Total 6, 022, 000 1.12 1,296,000 0.96 7,318,000 1.09 257,400

Vertigo 1,785,000 1.28 1,785,000 1.28 73,000

TOTAL 6, 022, 000 1.12 3,081,000 1.14 9,103,000 1.13 330,400

11DEVELOPMENT

EXCO RESOURCES N.L.

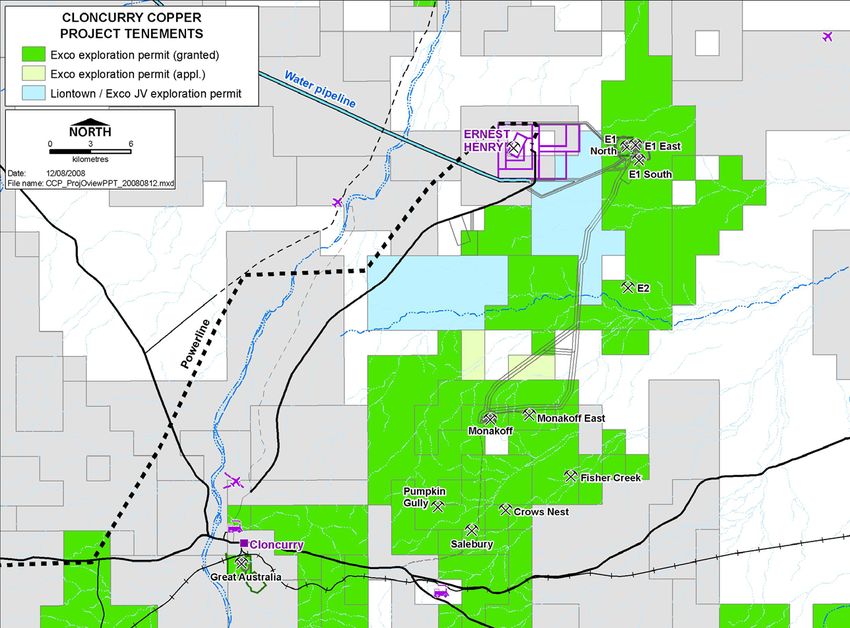

OPTIONSCLONCURRY COPPER PROJECT (CCP)

13RECENT KEY EVENTS - CCP

DEC 2007 Commenced PFS on Cloncurry Copper Project

FEB 2008 New resources at Monakoff East & Taipan

APR 2008 E1 South Resource increased by >50%

JUNE 2008 Successful completion of PFS demonstrates

credentials of ‘base case’ 2Mtpa project

JULY 2008 Commenced DFS on expanded (2.5-3Mtpa) project

AUG 2008 Discovery of new ore zone at E1 North

SEPT 2008 Major upgrade of E1 North & E1 South Resources

NOV 2008 Completion of drilling programs required to

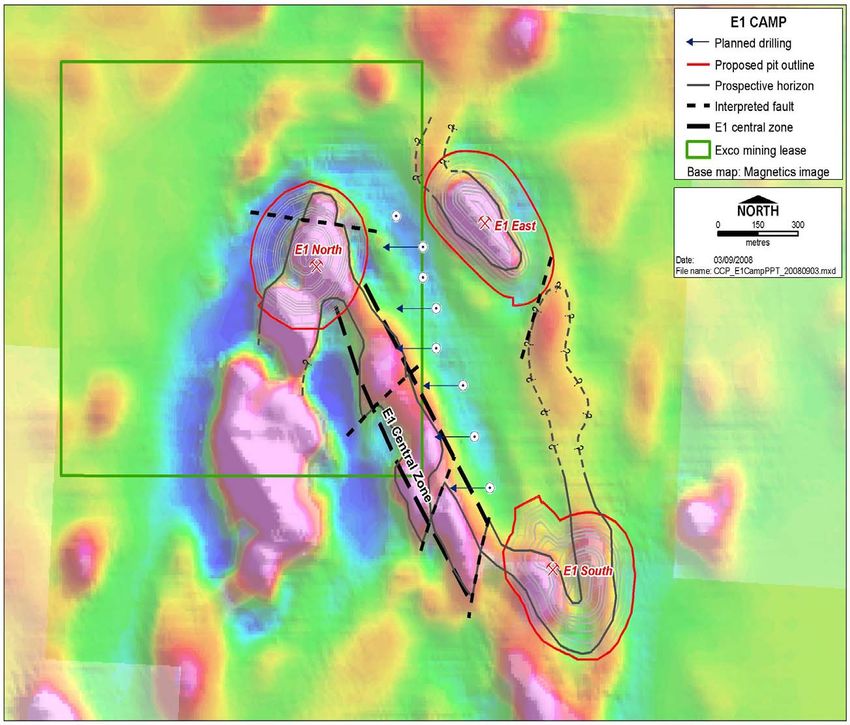

establish mineable reserveDRILLING SUCCESS - E1 CAMP

Infill drilling has confirmed grade and

continuity, plus depth & strike extensions

Recent upgrades of E1 North & E1 South:

significant increase in tonnage and

sizeable conversion to indicated category

NEW mineralised zone identified on

eastern limb of E1 North; further resource

upgrade due soon

E1 Camp now hosts 38.5Mt, 310,800t of

Cu & 286,100oz of Au, with further upside

Ongoing programs focused on resource

conversion and realising further potential

of “Central Zone”

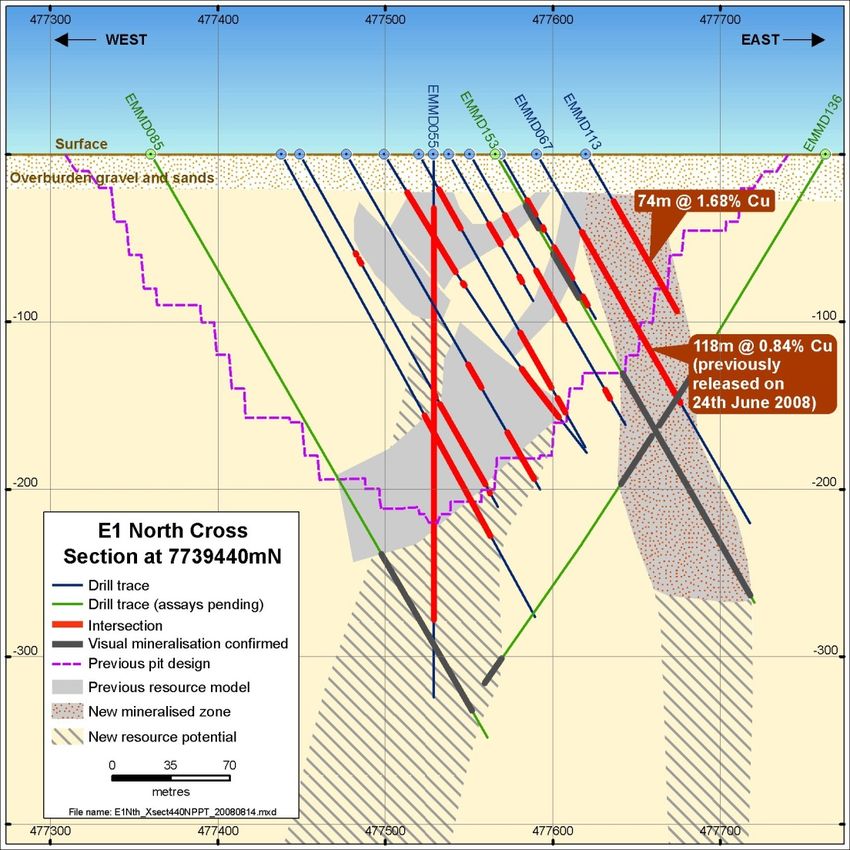

15FURTHER UPSIDE AT E1 CAMP

16CCP FUNDAMENTALS

– Stand-alone concentrator concept

– Key deposits: E1 Camp & Monakoff

– Initial 10-year open-pit mine life

– Throughput 2.5 to 3.0 Mtpa of ~1.0% Cu ore

– Production ~25ktpa Cu, ~17koz Au

– Straightforward process & metallurgy

– By-product potential: Co, Fe, Acid & U(?)

– Native title agreements in place

– EIS commenced Q4/2007

– Completed PFS in Q2/2008

– Full DFS now underway

17DFS - UPSIDE OPPORTUNITIES

Exploration & • Resource base can clearly deliver a mineable reserve of ≥ 25Mt

Resources

• Supports increase in throughput to ≥ 2.5Mtpa and improved economics

Mining & • Can achieve a 50% increase in throughput for only 25% increase in Capex

Processing

• Economies of scale lead to unit cost reductions in power and labour

Cobalt – Recovery to a bulk concentrate. Zero additional capex. Payability

subject to concentrate marketing

Magnetite – Potential to produce ≥ 500,000tpa; viability subject to transport

and marketing constraints. Additional process Capex only ~A$10M

By-Products

Pyrite / Acid – Roasting of pyrite concentrates to produce suphuric acid for

the local market. Potential to also generate power & increase Co recovery.

Conceptual scoping study completed; No value at present

Uranium – Available for tailings leach. Subject to politics could produce

>400,000lbs/annum; No value at present

N.B. By-product recovery has a positive impact on overall Cu-Au recoveries

18Building on the PFS Base Case

PFS DFS*

Throughput 2Mtpa 3Mtpa

Initial Project Life 11.5 years 8-10 years

Cu recovery 93% 93%

Au recovery 80% 80%

Estimated Capital Cost (±25%) ~A$209M ~A$250M

Operating Cost (including TC/RC & royalty) US$1.80/lb US$1.73/lb

Gold credit (US$0.34/lb) (US$0.34/lb)

Total Cash Cost US$1.46/lb US$1.39/lb

Base Case NPV @8.5% (Cu & Au only) A$126.7M A$256M

IRR (Cu & Au only) 28.6% 37%

Potential By-product NPV (Co & Magnetite) A$50-70M A$50-80M

Average Cu Price assumed US$2.68 US$2.50

A$ Exchange US$0.9 US$0.7

Payback period 2-3 years 2-3 years

* Indicative model 19CCP - FORWARD PROGRAM

DEFINITIVE FEASIBILITY STUDY (DFS)

• Seamless transition from PFS to DFS in July 2008

• Re-appointed GRD Minproc as Study Manager

• Current focus on unlocking upside: e.g.

¾ Increasing throughput ≥ 2.5Mtpa & production ≥25ktpa Cu

¾ Pit optimisations & mine scheduling

¾ Cost optimisation / reduction

¾ Metallurgy and By-product potential: Co, Fe, Acid & U(?)

• Ongoing resource upgrades (E1 North & Central Zone)

ENVIRONMENTAL IMPACT STATEMENT (EIS)

• Commenced baseline studies Q3/2007

• Application for voluntary EIS approved July 2008

• On track for completion Q1/2009, followed by approvals

20ORE SUPPLY OPTION

- E1 ores 8km from Ernest Henry Mine

- Existing 11Mtpa Concentrator at EHM

- Current open pit plan ends 2H/2010

- Evaluating U/G potential from 2011

- Potential for EXS to fill production gaps

- Significant tonnages at E1 with upside

- Compatible mineralogy / metallurgy

- Lower capital risk option for EXS

- Lower operating cost structure

- EXS seeking long-term arrangement

- No formal agreement yet in place

21WHITE DAM GOLD PROJECT

• Agreement with Polymetals to acquire

50% of project

• Polymetals to sole fund first A$9.6M

of capital development

• Polymetals will develop and manage

the project

• Grant of Mining Lease approved;

currently finalising MARP

• Plan to treat 2Mtpa (50,000oz pa)

commencing in late 2009

• A$ gold price offers attractive margins

• Exco remains exposed to project and

gold price upsideIVANHOE JOINT VENTURE

23EXCO’s KEY INGREDIENTS

MANAGEMENT: An experienced Board & Management Team with

a track record of disclosure & successful delivery

ASSET QUALITY: Strategic ground position in a highly prospective

belt, and a resource base which continues to grow

CASH: Well funded to complete drilling & resource development

programs, and to progress studies for the Cloncurry Copper Project

DEVELOPMENT OPTIONS: Three near-term opportunities for cash

flow for Exco:

1. Stand-alone development of the 100% owned Cloncurry Copper Project

2. Ore-Supply arrangements with Xstrata’s Ernest Henry Mine

3. Development of White Dam Gold Project in JV with Polymetals

COMMITMENT: Exco is committed to expediting the path to cash

flow, and to creating maximum value for shareholdersTHANK YOU

EXCO RESOURCES N.L.

ASX: EXS

www.excoresources.com.auYou can also read