Multi Asset Allocation Views - June 2020 - AXA IM Luxembourg

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

This promotion document is intended for Professional Clients under MIFID ( 2014/65/EU)

only and can not be rely upon by retail clients. Circulation must be restricted accordingly.

Multi Asset Allocation

Views

June 2020

Multi-Asset Investment views

Our key messages and convictions

#1

Neutral on equites Global economy has near Positive on

collapsed in 1H20, but the

foundation for a 2H20

#2 Investment Grade

Unprecedented Credit

growth bounce is being laid support from both

fiscal and monetary

authorities should

help to ease

#3 valuation and

liquidity concerns

Fiscal policy on

one hand,

monetary policy

Neutral Sovereign

Bonds on the other hand #4

should contain Concerns over depth and

bond yields in the length of impact of COVID- Long Volatility

current range 19 virus on global growth

generates higher volatility

Source: AXA IM as at 20/05/2020

1

Asset allocation stance

Positioning across and within asset classes

Asset Allocation Equities Fixed Income

Key asset classes Govies

Developed

Equities Euro core

Euro area

Bonds Euro periph

UK

Commodities UK

Switzerland

Cash US

US

Inflation Break-even

Japan

US

Emerging & Equity Sectors

Euro

Emerging Markets

Credit

Europe Oil & Gas

Euro IG

Europe Telecoms

US IG

US Industrials Euro HY

US Cons. Discretionary US HY

EM Debt

EM Bonds HC

Legend Negative Neutral Positive Change ▲ Upgrade ▼ Downgrade

Source: AXA IM as at 20/05/2020

2

Central & alternative scenarios

Deep recession with little

ammunition 35%* Central scenario 55%* V-shape recovery 10%*

• Virus-shock fractures key labour markets • Coronavirus sparks severe recession in • Virus is contained quickly and growth sees

leading to significant global job losses most economies. Global growth forecasted “V-shaped” rebound

dampening demand even as virus fades. to fall to -2.8% in 2020. • Easier financial conditions (diminished

• Coronavirus outbreak more persistent • Central banks globally pushed beyond the trade, Brexit and political uncertainties)

• Scale of shock results in isolationist policies: envelope of their 2008 toolkits. Fed prove to be a tailwind for growth

trade wars and other geo-political tensions, backstopping most markets, ECB steps • Productivity growth accelerates,

echoing 1930s beyond limits dampening inflation pressures and

• Growth/inflation expectations weaken • Large fiscal easing in most economies. allowing central banks to maintain easy

further, a new depression threatens, Stimulus has focused on filling “the drop”. policy

corporates’ earnings under more pressure More likely necessary to build recovery • Global/US/EMU growth surprises to the

• Further monetary policy where space permits • Monetary and fiscal stimulus are sufficient. upside in a stronger and more persistent

(including China). Government’s continue Economic rebound depends on policy, rebound from Q2 dip

with fiscal stimulus and divide between labour market reaction and indebtedness. • ECB ends latest QE in 2020; Fed reverts to

monetary financing blurs further. As well as the virus itself. a patient upside bias beyond 2020

• Equities: Risk appetite continues to • Equities: earnings contraction priced so • Equities: equities rebound strongly,

deteriorates with equities continuing to far may be optimistic. Containment of mimicking the “V-shaped” rebound in

sell off pandemic a necessary condition for economic activity

• Safe haven government bonds rally rebound to be sustained • Government Bonds: US and EUR break-

resumes • Government bonds: in a range as central even rates rise

• Credit spreads to widen bank purchases offset massive fiscal policy • Credit: Spreads to rally

• EM debt to come under pressure • Credit: fundamentals at odd with recent

sharp reduction in spreads

*Probability for each scenario according to AXA IM as of 20/05/2020. Those expectations are provided for illustration purposes only. They are hypothesis based on data made public by official providers of

economic and market statistics. AXA Investment Managers Paris disclaims any and all liability relating to a decision based on or for reliance on this document

Change of the month: Upgrade Downgrade

3

Setting the scene: our global economic outlook

Economic contraction in 2020 with downside risk, AXA IM Research & Investment Strategy economic forecasts*

Unprecedented accommodative measures from Central Banks

Real GDP growth (%) 2018 2019* 2020* 2021*

• The US sets its own path with an easing of restrictions relatively sooner World 3.6 2.9 -2.8 6.3

than other countries. This should minimize the economic cost but carries

Advanced economies 2.3 1.7 -5.7 5.9

a relatively higher risk of a second wave of the virus. With the economy

US 2.9 2.3 -3.8 5.3

already re-opening, activity should rise sharply from a low base. We

Euro area 1.9 1.2 -7.0 6.2

forecast a contraction of -3.8% in 2020 and tentatively suggest +5.3% for

next year whilst stressing the uncertainty around specific forecasts UK 1.4 1.3 -8.7 8.0

Switzerland 2.5 0.9 -4.9 3.5

• Eurozone economic indicators have unsurprisingly shown a massive effect

from Covid-19 albeit with persistent and strong divergences between Japan 0.7 0.8 -5.8 3.3

countries, reflecting different economic structures, severity of lockdowns Emerging economies 4.4 3.7 -1.1 6.5

and implementation of exit strategies. The limited scope of the EU’s China 6.6 6.1 2.3 8.0

Pandemic Crisis support leads us to cut our forecast for 2020 to -7%

• China’s recovery continues thanks to supply normalization with a V-

shaped recovery in industrial production. However, sustainability of the

industrial recovery is questionable. More forceful policy easing is required

to offset growth headwinds. We maintain our 2.3% growth forecast for

2020, but acknowledge risks to the downside

• Emerging economic activity will suffer from the sharp falls in industrial

production and retail sales in the 1st quarter with deeper falls expected in

the 2nd quarter given the stringency of the lockdown measures. Central

banks have been very reactive with accommodative measures, but this will

not be sufficient to compensate for the contraction

• Major central banks implemented unprecedented accommodative policy

measures to counter virus related weakness and improve market

liquidity. The US Fed* keeps its rates to zero and continues to expand QE.

The ECB** also pursues its large QE programme. BoE*** also pursues a

large package of measures. The BoJ**** maintains its expanded QE

Source: AXA IM, Consensus Economics, IMF and Datastream as at 20/05/2020

*Federal Reserve ** European Central Bank, ****Bank of England, ****Bank of Japan

4

Overview of asset allocation stance

Our views: Investors remain cautious as interest rates stay low and

• As many parts of the world slowly deconfine investors are focused on the value stocks crushed

speed and pace of the recovery. It will have a profound impact on the way

various asset classes behave over the next couple of months. There is much

talk of a U shaped or a V shaped recovery. Despite the bounce in equities,

investors seem more positioned for the U as interest rates stay low, value

and cyclical stocks crushed and sentiment and positioning is bearish. There is

a good investment opportunity but timing is crucial.

• We maintain our medium-term constructive view on risky assets and credit

as the policy response to the pandemic is aggressive, but at this stage the

shape of the recovery is uncertain.

• The Covid 19 crisis has also put Governments under pressure and

accelerated to the surface any of the underlying global tensions. In an

election year, US-China recent truce could be seriously tested and Brexit was

on the sidelines but progress on negotiations is poor to say the least. The

resurgence of these various pressure points could again lead to bouts of

market volatility. However, we had constructive news in the Eurozone with

France and Germany’s 500 Bln Eurozone recovery fund proposal. Key asset classes

Our key convictions: Equities

• Positive on Credit –Unprecedented support from both fiscal and monetary Bonds

authorities should help to ease valuation and liquidity concerns

Commodities

• Neutral on equities - Global economy is set to collapse in 1H20, with massive

negative impact on earnings, but the foundation for a growth bounce in the Cash

2nd half is being laid

• Neutral duration on government bonds - monetary arsenal is a clear support Change ▲ Upgrade Downgrade

for bonds, but unparalleled fiscal stimulus and eventually unprecedented

supply should maintain government bond yields in the current range

Source: AXA IM, Bloomberg, 20/05/2020

5

Equity markets outlook and convictions

Our views: This is getting very extreme

• Equities range traded over the last month. Dire economic data no longer

seems to shock and investors focus is on the pace and strength of the

recovery. Is it U shaped, V shaped or L shaped ?

• Within our process we are now focusing on our high frequency indicators to

get insight on the timing and pace of the recovery. As the chart on the right

illustrates – shell shocked investors prefer to pay for quality visible growth

stocks (often found in the Technology sector) whilst value stocks (often found

in financial and cyclical sectors) are now trading at a huge discount. The

catalyst for a reduction in this spread would be a sign of improvement in our

indicators or even just less negative relative to expectations

• In terms of valuations – 2020 earnings are a write off and we look forward to

2021. Consensus expects anything between +15%/25% growth but until we

get a clearer idea of where 2020 growth settles it is still early days

• Sentiment and positioning are cautious. Cash levels are high and so good

news could see markets move fast Developed Emerging & sector diversification

• Our key convictions: Eurozone Emerging Markets

• We prefer a more neutral positioning. We are keeping a close eye on the UK EMU Banks

underperformance of value stocks as better news could trigger a partial Europe Oil & Gas

Switzerland

rerating here and investors are not positioned for that.

• US – Continues to benefit from higher weighting in Technology and Sweden Europe Telecom

Healthcare both winners from the COVID 19. US Industrial

US

• Eurozone – Inexpensive but high % of financials and energy both suffering

• Emerging Market Equities – Getting cheaper but hit by strong $ and for Japan US Cons. Discr.

many collapse in commodity prices.

• Switzerland – Benefits from higher exposure to staples and pharmaceuticals. Change ▲ Upgrade ▼ Downgrade

Source: AXA IM, Datastream as at 20/05/2020

6

Government and inflation-linked bonds outlook and convictions

Our views: UST’s show the depth of March panic not divesting per se

• Government bond markets have remained in a tight range for another

month despite concern that supply would pose a problem for valuations

and investor appetite with the Fed, in particular, having materially reduced

the rate of Treasury purchases of late. The chart to the right shows the huge

liquidation of UST’s in the panic part of the market sell off in risk assets. Yet

Japan in that month bought more UST’s than ever before. Long end UST’s are

now available at a currency hedged pick up to Japan and Euro Core long end

bonds which will attract further flow and continue to anchor long rates whilst

Central Banks will continue underpin demand this year. Neutral on duration

but appetite remains to buy on weakness as risks remain asymmetric for

yields in the coming months.

• Emerging markets bonds continue to suffer from perceived risk amongst

investors and are the only major fixed income asset class that is failing to

attract inflows. USD weakness would be a welcome support. Meanwhile the

asset class is probably unduly impacted and offers relatively attractive yields Govies Inflation Break-even

for those less impacted by mark-to-market considerations.

Euro core US

• Inflation breakeven pricing remain morose, close to levels seen with the

Euro periph Euro

initial recovery in risk assets at end of March. Currently no impending

catalyst for a sustained rebound. UK

Emerging

US

Our key convictions: Emerging Markets

• Government Bonds: Neutral whilst range set to be contained Japan

▼

• Inflation Breakevens: Positive on depressed valuations

Change ▲ Upgrade Downgrade

Source: AXA IM, Bloomberg as at 20/05/2020

7

Credit bonds outlook and convictions

Our views: Central Banks Drive Recovery in Returns

• Credit spreads have seen a further progress in their return recovery, chart

to the right, with the support of major Central Banks now extending to

‘Fallen Angels’, i.e. Investment Grade companies that were downgraded

to High Yield since the crisis. This trend of Central Bank intervention is

likely to continue further afield with notably the Bank Of England now

looking to extend its policy beyond the status quo in line with the ECB and

Fed. Credit markets are now an explicit rather than implicit tool of Central

Bank monetary policy.

• Credit markets have continued this month to benefit from large investor

inflows that have been met with unprecedented levels of issuer supply as

corporates bolster their liquidity levels. Whilst issuance has permitted a

higher degree of price discovery as new issues are priced and distributed,

the underlying secondary market is still suffering from poor liquidity in

general amidst limited risk appetite from financial intermediaries.

• Whilst valuations might be hard to justify with fundamentals so unclear and

default expectations below those in the Great Financial Crisis, the technical

support from CB’s and the improved sentiment that this affords investors

do, in our opinion, justify a positive appetite for IG credit risk. Credit

Euro IG

Our key convictions:

US IG

• Investment Grade: Overweight

• High Yield: Neutral Euro HY

US HY

Change ▲ Upgrade ▼ Downgrade

Source: AXA IM, Bloomberg as at 20/05/2020

8

Currency market outlook and convictions

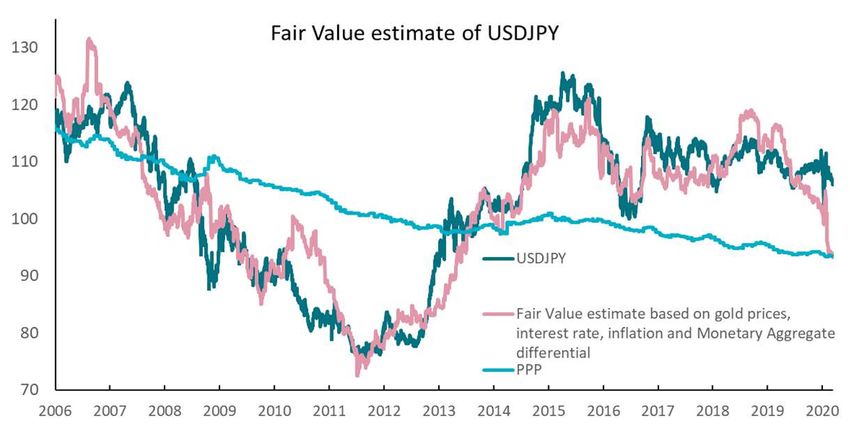

Our views: USDJPY doomed to depreciate after FED massive easing

• USD: US economy is currently equally threatened by the impact of

lockdowns, putting an end to US growth exceptionalism. Massive FED

intervention brought liquidity back to normal. USD has lost all key supports,

including carry advantage. US administration is pushing to shorten the

lockdown period, leading to a higher risk of a second wave.

• EUR: German court decision on PSPP highlights the difficulty of delivering

fiscal union, questioning EUR viability. In the short term, this should not derail

ECB QE and EUR is holding up well, leaving timid chances for a comeback.

• JPY: Undervaluation even more acute as Central Banks ease against an

already constrained BoJ. The uncertain outlook and the lower foreign rates

differential should depress Japanese unhedged investment outflows, while

the stock is compelling to re-hedge in downturns, justifying safe haven status.

• GBP: UK government looks serious about not wanting to extend Brexit

transition. Market should reprice further the probability that UK exits with a Currencies

narrow or no deal as we approach June extension deadline.

USDEUR

• CAD : Double whammy of lockdown recession and damaged Oil Industry is a

serious threat for highly leveraged Canadian households. Production cuts and USDJPY ▼

restarting economies could continue to support the oil price rebound.

• AUD : Australia deployed a massive fiscal stimulus, against more limited EURGBP

monetary easing and more advanced pandemic recovery. Australia exports USDCAD

could benefit from further infrastructure spending from China.

Our key convictions: USDNOK

USDCHF

• We are positive on JPY versus USD with a constructive bias on EUR also ▼

against USD and on AUD versus CAD.

Change ▲ Upgrade ▼Downgrade

Source: AXA IM, Bloomberg as at 20/05/2020

9Commodity market outlook and convictions

Our views: Oil price rebound amidst supply cuts despite lower demand

• The impact of COVID-19 related containment measures on global

commodity demand is a major headwind for cyclical commodities.

Sentiment improved for oil and industrial metals and remained positive

for gold whist technical remain more neutral for gold, less negative for

industrial metals and Oil.

• The oil price rebounded from last month’s low following OPEC+

decision to cut production as well as the announcement of oil field

shut-ins as demand is expected to pick-up as lockdown restrictions

despite social distancing measures across the globe. Given the

production cuts are offset by the ongoing negative supply/demand

balance, we expect the oil price to remain at its current level until the

market shows sign of normalising.

• Industrials metals should benefit from the muted recovery in Chinese Commodities

demand which is likely to be offset by recovering production, following

Oil

the easing of labour restrictions at major mines.

Industrial Metals

• The gold price should continue to be anchored by low rates at fairly high

levels at $1700. In addition, gold continues to benefit from its safe haven Gold

status as investors pushed ETF holdings to record levels.

Our key convictions:

• We adopt a more neutral view on the commodity complex despite the Change ▲ Upgrade ▼ Downgrade

unprecedented negative demand/supply balance given the prospect of

reduced supply amidst an expected rebound in demand following the

easing of Covid-19 containment measures.

Source: Bloomberg , AXA IM 20/05/2020

10Volatility outlook and convictions

Our views:

Observed versus predicted equity volatility (US market)

• Houston, do we still have a problem? While the US Treasuries volatility curve

has normalised to pre-COVID-19 level and the FX market is stabilising in the

normal valuation range, equity volatility remains high with a VIX in the 30%

range. Our Equity Volatility Fair Value is close to current market level (cf. chart

on the right), mainly driven by the high level of stocks pairwise correlation. In

this context we should focus our attention on the US elections and the US China

relationship, a key element that might be a new catalyst.

• Regarding equity volatility, all major indices remain expensive with an inverted

term structure and a rather steep skew slope. Only Asian Markets exhibit

relatively interesting skew both on an absolute and relative basis.

• The FX market has normalised except for the GBP and the commodity

currencies. The Risk reversal are very heterogenous across currencies in terms

of valuation. However, the kurtosis pricing while decreasing remains high and

suggest FX market fragility.

Our key convictions:

• Begin the hedging of US election with mid-term maturity to benefit from

inverted volatility curve

• Rebuild volatility carry strategy with some beta protection overlay

• Relative Value has re-emerged with new entry point

Source: AXA IM, Bloomberg, as at 20/05/20

(1) Vo-Vol stands for implied volatility on VIX option contracts

11Important disclaimer This promotional document is designed for informational purposes. It does not constitute a contractual element, or investment advice. Due to its simplification, the information contained in this document is incomplete. It can be subjective and could change without notice. It is based on market information available at the time of preparing this document, market information that have not been verified or audited by AXA Investment Managers Paris or its affiliates (AXA IM). AXA IM is not required to update the information contained in this document, and do will not update it. This document is intended for institutional investors with a thorough knowledge of financial markets and investment techniques described in this document. The information contained in this document is based on elements of information, assumptions, projections, estimates, scenarios resulting from judgments and analytics which are by nature subjective. Therefore, given the subjective nature and purely indicative information contained in this document, AXA IM draws attention of this document’s recipient to the fact that the assumptions, projections, estimates and scenarios used by AXA IM to produce the information contained herein may be inaccurate and / or incomplete and AXA IM makes no warranty as to their future or as to their accuracy and relevance to the date of this document. AXA IM is not responsible for any omission in the information contained in this document. This document does not in any way constitute any commitment of AXA Investment Managers Paris to create, manage or distribute, or otherwise participate in the management or implementation of any financial instrument, portfolio investment whose performance is linked to the investment strategy described in this document. The recipient of this document remains the sole judge of whether an investment or divestment in financial instruments, funds or other investment vehicle whose performance is linked to the implementation of investment strategies described in this document. AXA Investment Managers Paris not grant any legal, tax or accounting and in no way will responsible for the legal, tax and accounting-related investment decisions implemented by the recipient of this document. The responsibility of AXA Investment Managers Paris, its employees, officers, representatives and advisers shall not be incurred by making investment decisions based on only the information contained in this document. An investment in any financial instrument must be based on a prospectus or any other legal document specifically describing the characteristics and risk factors, what does not provide this document. The recipient of this document will keep the information contained in it strictly confidential, so that information given and available to it, directly or indirectly, by AXA Investment Managers Paris. The recipient of this document shall use the information contained in this document only to determine its interest in the investment strategy described herein. Any reproduction, even partial, of this document is strictly prohibited. AXA Investment Managers Paris - “Coeur Defense" Tour B - La Défense 4 - 100, Esplanade du General de Gaulle - 92400 Courbevoie. Portfolio management company, holder of AMF approval n° GP 92008 dated April 7, 1992. Limited company with a capital of 1,384,380 euros registered in the Register of Commerce and Companies of Nanterre under number 353 534 506. 12

Important disclaimer For Japanese investors: AXA Investment Managers Japan Ltd., whose registered office and principal place of business is at NBF Platinum Tower 14F 1-17-3 Shirokane, Minato-ku, Tokyo 108-0072, Japan, which is registered with the Financial Services Agency of Japan under the number KANTOZAIMUKYOKUCHO (KINSHO) 16, and is a member of Japan Securities Dealers Association, Type II Financial Instrument Firms Association, Investment Trust Association of japan and Japan Investment Managers Association to carry out the regulated activity of Financial Instrument Business t under the Financial Instrument Exchange Law of Japan. In Japan, none of the funds mentioned in this document are registered under the Financial Instrument Exchange Law of Japan or Act on Investment Trusts and Investment Corporations. This document is purely for the information purpose for use by Qualified Institutional Investors defined by the Financial Instrument Exchange Law of Japan. For UK investors : Issued in the UK by AXA Investment Managers UK Limited, which is authorised and regulated by the Financial Conduct Authority in the UK. Registered in England and Wales No: 01431068. Registered Office: 7 Newgate Street, London EC1A 7NX. For Hong Kong investors: The authorisation of any fund by the Securities and Futures Commission in Hong Kong (“SFC”) does not imply official approval or recommendation. SFC authorization of a fund is not a recommendation or endorsement of a fund nor does it guarantee the commercial merits of a fund or its performance. It does not mean the fund is suitable for all investors nor is it an endorsement of its suitability for any particular investor or class of investors. Where any of the Funds is not authorized by the SFC, the information contained herein in connection with such unauthorized Fund is solely for the use of professional investors in Hong Kong. Materials exempted from authorization by the SFC have not been reviewed by the SFC. For Malaysian investors: As the recognition by the Malaysian Securities Commission pursuant to Section 212 of the Malaysian Capital Markets and Services Act 2007 has not been / will not be obtained nor will this document be lodged or registered with the Malaysian Securities Commission, the shares referred to hereunder (if any) are not being and will not be deemed to be issued, made available, offered for subscription or purchase in Malaysia and neither this document nor any other document or other material in connection therewith should be distributed, caused to be distributed or circulated in Malaysia. For Taiwan investors: The offer, distribution, sale or re-sale of fund units/shares in Taiwan requires approval from and/or registration with Taiwanese regulatory authorities. To the extent that any units/shares of the Funds are not so licensed or registered, such units/shares are made available in Taiwan on a private placement basis only to banks, bills houses, trust enterprises, financial holding companies and other qualified entities or institutions (collectively, “Qualified Institutions”) and other entities and individuals meeting specific criteria (“Other Qualified Investors”) pursuant to the private placement provisions of the Rules Governing Offshore Funds. No other offer or sale of such units/shares in Taiwan is permitted. Taiwanese purchasers of such units/shares may not sell or otherwise dispose of their holdings except by redemption, transfer to a Qualified Institution or Other Qualified Investor, transfer by operation of law or other means approved by the Taiwan Financial Supervisory Commission. For Qatar investors: This document has been prepared and issued by AXA Investment Managers LLC, Qatar Financial Centre, Office 703, 7th Floor, QFC Tower, Diplomatic Area, West Bay, PO Box 22415, Doha, Qatar. It is not for use by retail customers under any circumstances. AXA Investment Managers LLC is authorised by the Qatar Financial Centre Regulatory Authority. This presentation has been issued on [16-11-15] 13

You can also read