OUTLOOK FOR MULTIEMPLOYER PENSION PLANS - ABA EMPLOYEEBENEFITSCOMMITTEEMIDWINTER MEETING2021

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

ABA EMPLOYEE BENEFITS COMMITTEE MIDWINTER MEETING 2021

OUTLOOK FOR MULTIEMPLOYER

PENSION PLANS

Deva A. Kyle

1

1. Multiemployer Funding Crisis: Understanding the

Problem

OVERVIEW 2. Legislative Solutions Past and Present

3. What’s Next: Budget Constraints and

Multiemployer Relief in 2021

2

“Retirement income is referred to by many as a

three-legged stool: Social Security, employer-

sponsored retirement plans and personal

MULTIEMPLOYER savings… Multiemployer pension plans are

contributing to the wobbly three-legged stools

FUNDING CRISIS for many retirees because these plans are in

crisis. About 10 million Americans participate in

multiemployer plans and about 1.5 million of

them are in plans that are quickly running out of

money…” – Ways and Means Chairman, Richard

Neal (Democrat, MA-1) (2018)

3

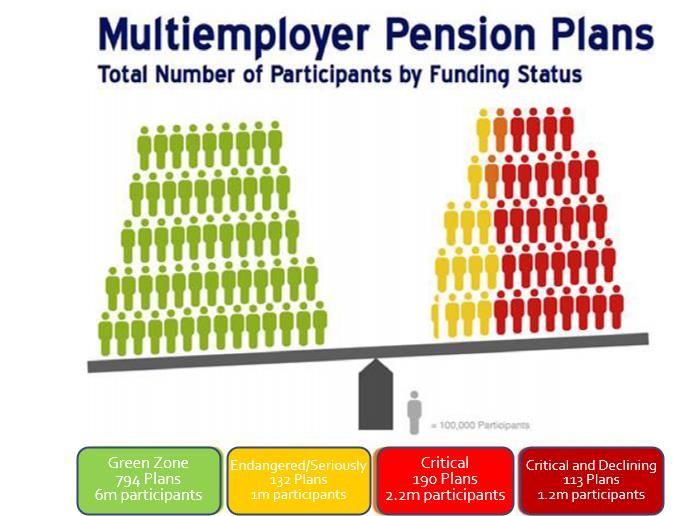

Most multiemployer plans– 60% –

are in plans that are generally

considered healthy (Green Zone)

A small number of plans are in

trouble but not yet critically

underfunded (yellow)

30% or so of plans are critically

underfunded (both the light red and

dark red together)

10-15% of the 10 million

participants in multiemployer pension

plans are in plans that are projected

to be insolvent in the next 20 years

(critical and declining– dark red only) Source: Congressional Research Service, “Data on Multiemployer Defined Benefit (DB) Pension Plans updated May 22, 2020

4

MULTIEMPLOYER FUNDING CRISIS:

UNDERSTANDING THE PROBLEM

Pension Benefit Guaranty Corporation (PBGC) is set

to go insolvent in 2026.

• Plans will continue to go insolvent and will

More than

require assistance from PBGC 50% chance

of insolvency in

• PBGC’s multiemployer guarantee is very low (at

2026

best under $14,000 a year with 30 years of

service).

• If PBGC goes insolvent, PBGC will pay about

1/10 of that amount.

Source: PBGC 2019 Projections Report

5

MULTIEMPLOYER FUNDING

CRISIS: NATIONAL IMPACT

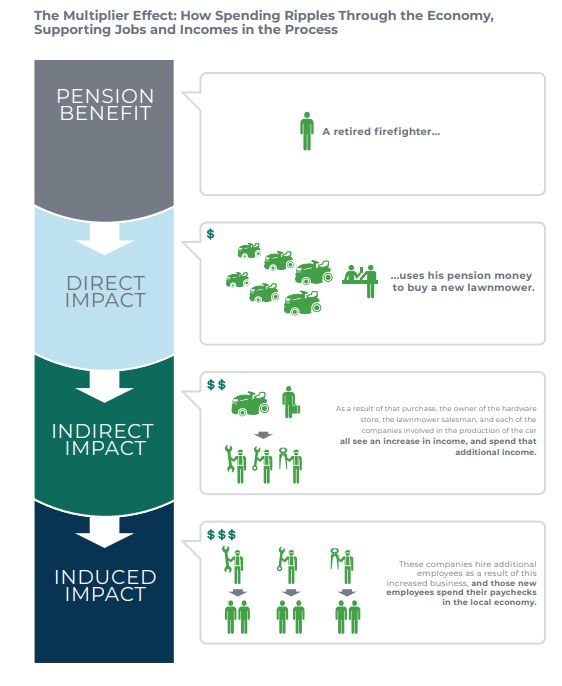

“Pension plans provide secure income in retirement and

through that income retirees contribute to the greater

economy as a whole contributing to the local, state, and

national economy through consumer spending.”

DB Pensions Support (Multiemployer only in

parenthesis)

-6.9 million American Jobs (523,000 jobs)

-$394.2 billion in Labor Income ($30b)

-$1.27 trillion in Total Economic Activity ($96.6b)

-$703.9 billion in GDP ($53.8b)

-$102 billion in Federal Tax Revenue ($7.8b)

-$89.8 billion in state/local tax revenue ($6.9b)

Source: Boivie, Ilana and Doonan, Dan, National Institute on Retirement Security, “Pensionomics 2021: Measuring the Economic Impact of DC

Pension Expenditures” (2021) https://www.nirsonline.org/wp-content/uploads/2020/12/Pensionomics-2021-Report-Final-V6.pdf 6

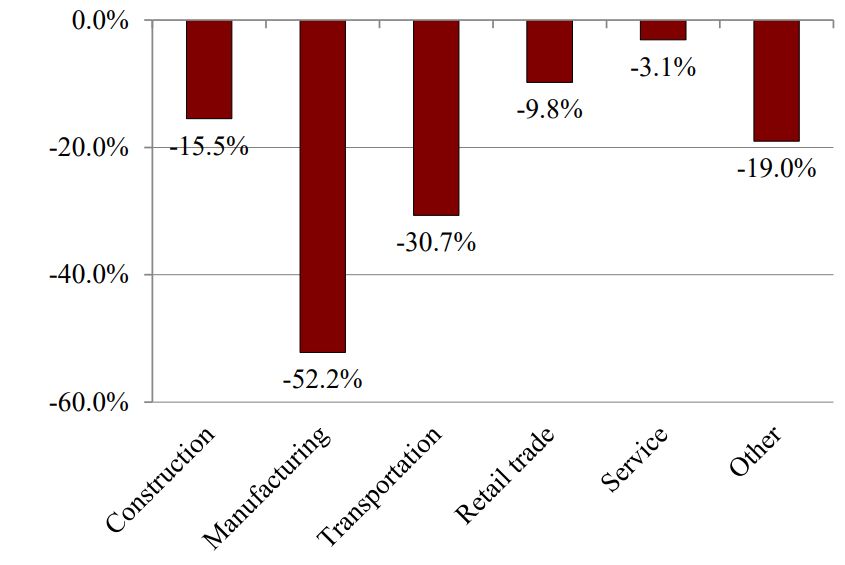

MULTIEMPLOYER FUNDING CRISIS

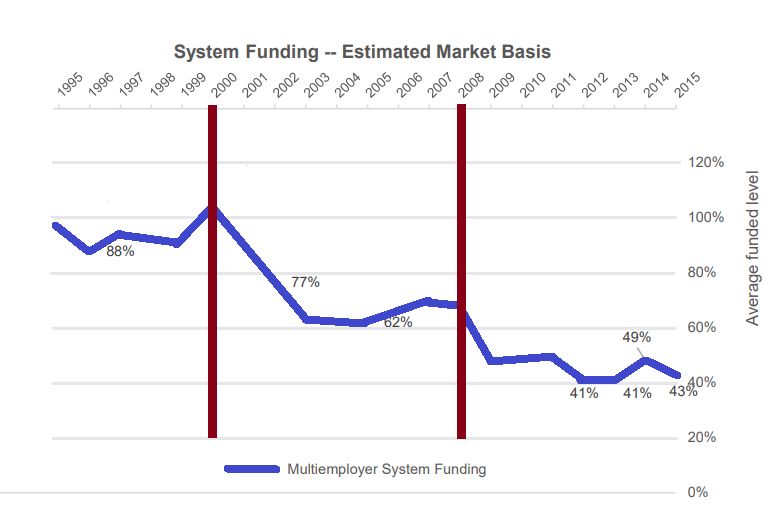

The number one factor in multiemployer pension plan funding losses was the dual financial crises of 2000

and 2008. Overall, the multiemployer system lost about 30% of its value from 2001-2003 and another

20% or so from 2008-2010.

The economic downturns in the 2000s had two crucial impacts on multiemployer pension plans separate

from the loss in assets all other market investments experienced: Insolvencies cut the number of contributing

employers and layoffs cut the number of active workers.

Financial

Crisis

Financial

Crisis

Source: Munnell et., al. IBID

Source: PBGC 2017 Projections Report 7

MULTIEMPLOYER FUNDING CRISIS

Deregulation, Automation, and maturing workers

Deregulation has led union employers out of business.

Automation led to layoffs and changes in industry

preferences led to insolvencies. For example, Central

States, the largest multiemployer pension plan facing

insolvency, has been public about the impact

deregulation has had on the financial outlook for their

fund. Central States has 380,000 participants in their

plan mostly within trucking. When the trucking industry

was deregulated in the 1980s, tens of thousands of

trucking companies went out of business. 70% of

Central States contributing employers were lost

between 1980 and 2003 and 47 of the top 50

employers who were in the plan in the 1980s have

since withdrawn.

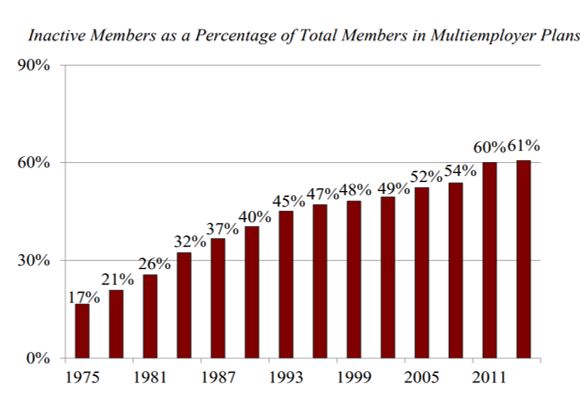

Many of the most troubled plans came to maturity

(i.e., plans with a large number of inactive

participants), at the same time, as the financial crises

hit. Mature plans have fewer resources to recover

from investment losses as the assets grow relative

to the contribution base supporting the plan.

8 Source: Munnell et., al. IBID

SELECT SOURCES

•Boivie, Ilana and Doonan, Dan, National Institute on Retirement Security, “Pensionomics 2021:

Measuring the Economic Impact of DC Pension Expenditures” (2021)

https://www.nirsonline.org/wp-content/uploads/2020/12/Pensionomics-2021-Report-Final-

V6.pdf

•Congressional Research Service, “Multiemployer Defined Benefit (DB) Pension Plans: A Primer

(updated April 3, 2020) https://crsreports.congress.gov/product/pdf/R/R43305

•PBGC, “FY2019 Projections Report” (2020) (https://www.pbgc.gov/sites/default/files/fy-2019-

projections-report.pdf)

•U.S. Chamber of Commerce, Employment Policy Division, “The Multiemployer Pension Plan Crisis:

Businesses and Jobs at Risk” (2018)

https://www.uschamber.com/sites/default/files/multiemployer_report_businesses_and_jobs_at_ris

k_final.pdf

•Munnell, Alicia, Aubry, Jean-Pierre, and Crawford, Caroline, “Multiemployer Pension Plans: Current

Status and Future Trends”, Center for Retirement Research at Boston College (2017)

https://crr.bc.edu/wp-content/uploads/2017/12/multiemployer_specialreport_1_4_2018.pdf

9“[T]he problem is not going away, and only grows worse with inaction... And

if we do not find a comprehensive solution, there will be a devastating

LEGISLATIVE

impact on the entire multiemployer system when the day of reckoning

arrives.

“…Within the multiemployer system, businesses are already being

SOLUTIONS PAST impacted by high contributions and potential withdrawal liability; active

workers are seeing fewer and fewer benefit accruals; and some retirees

AND PRESENT

are already experiencing reduced benefits. As the crisis grows, the impact

will be felt beyond the multiemployer system through a significant drag on

the economy, decreased tax revenues, and possible increased reliance on

social programs. A definitive solution is needed to address a looming crisis

that will affect us all.”

- Aliya Wong, Then Executive Director Of Retirement Policy, U.S. Chamber Of

Commerce, Hearing Before the Joint Select Committee on Solvency of Multiemployer Pension

Plans, United States Congress (June 13, 2018)

10LEGISLATIVE SOLUTIONS PAST AND PRESENT

Bills that • Pension Protection Act of 2006 (PPA)

became law • Multiemployer Pension Reform Act of 2014 (MPRA)

Bills/efforts • Rehabilitation for Multiemployer Pensions Act aka Butch Lewis

• Multiemployer Pension Recapitalization & Reform Plan or

that did not “Grassley/Alexander”

become law • Joint Select Committee on Solvency of Multiemployer Pension Plans

Bills currently • Chris Allen Multiemployer Pension Recapitalization and Reform

under Act of 2020 (CAMPRRA)

consideration • Emergency Pension Plan Relief Act of 2021 (EPPRA)

11PENSION PROTECTION ACT OF 2006

On August 17, 2006 H.R. 4, the Pension Protection Act was signed into law by the President.

The Pension Protection Act is often referred to as the most comprehensive reform of pension

laws since the passage of ERISA.

In response to the first market crash of the 2000’s Congress passed PPA with the following

changes to multiemployer law:

actuaries must certify the funding status of the plan in newly created statuses (green, endangered, or

critically under funded)

For underfunded plans, the plan must notify participants and create a schedule to improve the funding

of the plan within a funding improvement period.

For “critical status” plans, the plans may both increase contributions AND eliminate certain benefits for

participants not yet in pay status

New disclosure requirements for multiemployer plans to bring transparency to the funding of

multiemployer plans.

12MULTIEMPLOYER PENSION REFORM ACT OF 2014

On December 16, 2014, Congress passed, and the president signed, an end of year spending

bill titled the Consolidated and Further Continuing Appropriations Act. This spending bill

included The Multiemployer Pension Reform Act of 2014 (MPRA).

MPRA permitted critically underfunded plans facing insolvency in 20 years (also known as

critical and declining) to apply to:

the Treasury Department to approve a plan for long-term plan solvency achieved through a mix of

benefit cuts (up to 110% of the PBGC guarantee with additional protections for the elderly and

disabled) and increased contributions,

the Treasury Department for maximum benefit suspensions in conjunction with an application to the

PBGC to partition certain liabilities from the plan to further improve the plans’ financial outlook, or

the PBGC for a new facilitated merger between plans for which PBGC could, in theory, provide

funding.

13BUTCH LEWIS, GRASSLEY/ALEXANDER, AND THE

JOINT SELECT COMMITTEE

The Joint Select Committee on Solvency of Multiemployer Pension Plans co-chaired by Senator

Orin Hatch and Senator Sherrod Brown was a bi-partisan, bi-cameral committee established on

February 9, 2018 during the 115th United States Congress. (Section 30422 of H.R. 1892). The

two policy proposals put forward to solve the multiemployer crisis most under consideration

during the Joint committee were:

Rehabilitation for Multiemployer Pensions Act aka Butch Lewis – First introduced in 2017 (and reintroduced in 2019

where in passed in the House) in both the House of Representatives and the Senate, Butch Lewis allows underfunded

multiemployer pension plans to apply to the Treasury Department to get low interest 30-year loans and, if needed,

additional funds in the form of financial assistance from the PBGC to keep their plans solvent. Loan proceeds would be

invested conservatively and, generally, repayment would come via interest-only payments for the first 29 years

followed by a balloon payment in year 30 (other payment options were available).

Multiemployer Pension Recapitalization & Reform Plan or “Grassley/Alexander” – Grassley/Alexander is a white

paper put forward in 2017 by then Senate Chairman of the Finance Committee, Senator Grassley and then Senate

Chairman of the Health, Education, Labor, and Pension Committee, Senator Alexander. The plan called for

underfunded multiemployer pension plans to apply to the PBGC for a partition after receiving 10% benefit cuts and

other plan limitations including changes in governance. The plan also included sweeping changes for all multiemployer

plans including changes to funding rules, and new PBGC premiums.

14CAMPRRA AND EPPRA: NEW CONGRESS, NEW SOLUTIONS (SORT OF)

Chris Allen Multiemployer Pension Recapitalization and Reform Act of 2020 (CAMPRRA) – Introduced by Finance

Chairman Senator Grassley in December 2020, CAMPRRA has many of the same elements of Grassley/Alexander

Partition Amount: Amount needed to pay monthly benefits to participants and beneficiaries in the Successor Plan up to the PBGC

guarantee level

Changes for Partitioned Plans: Requires Restructuring, PBGC appointed as Independent trustee, and PBGC ability to remove trustees

Other Changes: New Increased PBGC Guarantee, New Premiums (flat rate, variable, union, and retiree), Caps discount Rate at 6.5%,

New Zone Statuses and Requirements, New Insurable event: PBGC guarantee when plan is projected to become insolvent in five years

Emergency Pension Plan Relief Act of 2021 (EPPRA) – Introduced separately by Ways and Means Chairman Richard

Neal and Education and Labor Chairman Bobby Scott, EPPRA is very similar to multiemployer provisions included in last

year’s Heroes Act:

Partition Amount: Amount necessary for the plan to remain solvent over 30 years and maintain a projected funded percentage of 80

percent at the end of the 30-year period. Note: PBGC can provide additional assistance to help plans satisfy their funding goals

Changes for Partitioned Plans: additional reporting, limits on plan improvements, and possibility for ongoing funding by the PBGC

Other Changes: New Increased PBGC Guarantee, Removes MPRA, Allows Extended Rehabilitation Period, single employer changes

15SELECT SOURCES

Pension Protection Act of 2006 https://www.congress.gov/bill/109th-congress/house-

bill/4?q=%7B%22search%22%3A%5B%22%5C%22Pension+protection+act%5C%22%22%5D%7D&s=6&

r=1

Multiemployer Pension Rehabilitation Act of 2014 https://www.congress.gov/bill/113th-congress/house-

bill/83/text

Rehabilitation for Multiemployer Pension Plans (also known as Butch Lewis)

https://www.congress.gov/bill/116th-congress/house-bill/397

Multiemployer Pension Recapitalization & Reform Plan or “Grassley/Alexander”

https://www.finance.senate.gov/download/white-paper_-multiemployer-pension-recapitalization-and-reform-

plan

Joint Select Committee on Solvency of Multiemployer Pension Plans https://www.pensions.senate.gov/

Emergency Pension Plan Relief Act of 2021 (EPPRA) https://edlabor.house.gov/imo/media/doc/2021-01-

20%20Emergency%20Pension%20Plan%20Relief%20Act%20Fact%20Sheet.pdf

Chris Allen Multiemployer Pension Recapitalization and Reform Act of 2020 (CAMPRRA)

https://www.congress.gov/bill/116th-congress/senate-bill/5045/titles?r=2&s=1

16"My Republican colleagues used reconciliation to give

WHAT’S NEXT: almost $2 trillion in tax breaks to the rich and large

corporations in the midst of massive income inequality

BUDGET … try to throw 32 million people off the health care

they had … [and] allow for drilling in the Arctic

RECONCILIATION wilderness… You know what? I think we can use

reconciliation to protect the needs of working families.“

-Senate Budget Committee Chairman, Bernie Sanders (I-

VT) (2021)

17WHY BUDGET RECONCILIATION?

Balance of Power: Previous multiemployer relief efforts assumed, in

order to pass (or even get a vote in the Senate), a multiemployer bill

would need strong support from both parties. This, in large part, had

to do with the make-up of Congress. Broadly speaking,

multiemployer relief has been a higher policy priority for Democrats

and, for the last decade, the Senate has been controlled by

Republicans. This changed this year with the Democrats taking

control of both the Congress and the White House.

While Democrats can now control what gets to a vote in the Senate,

they hold a slim 50/50 majority (with the Vice President bringing their

number to 51). Under this composition, Republicans can filibuster

any traditional bill the Democrats put forward in the Senate thwarting

their efforts to move forward with their agenda. One way around this

problem is through Budget Reconciliation.

18WHAT IS BUDGET

RECONCILIATION?

Budget Opportunity: Budget Reconciliation is a process created through the

Congressional Budget Act of 1974. Intended to rationalize the process by which Congress

sets the federal budget, Budget Reconciliation sets out instructions for the Budget

Committees to create a budget resolution by spending category. Once the budget

resolution is passed, the Appropriations Committees pass spending bills on specific topics

with the spending guidelines of the budget resolution.

The Appropriations Committees are charged with discretionary spending (including

defense, transportation, environmental laws, etc.). A much larger portion of the budget

deals with taxes and mandatory spending (including Social Security, Medicaid, Medicare,

etc.). Those programs are overseen by committees that are not the appropriations

committee.

The reconciliation process was created to reconcile the differences in the budget process

that get created in the discretionary, mandatory, and tax committees of Congress.

Source: Congressional Research Service, “The Budget Reconciliation Process: The Senate’s “Byrd Rule””, Updated December 1, 2020 https://crsreports.congress.gov/product/pdf/RL/RL30862 19BUDGET RECONCILIATION PROCESS

Budget Bill General Committees Budget Committees

• House and Senate each pass • Congressional committees in • The Budget Committee

an identical budget bill with the House and Senate bundles the committee

instructions for reconciling create reports on the budget reports together

the budget. in compliance with the

reconciliation instructions.

Full Chamber Conference Committees President

• The Full House and Full • To the extent that the House • The President either signs the

Senate separately consider and Senate versions of the bill into law or vetoes the

the reconciliation measure reconciliation measure are measure.

different, the differences

are ironed one in conference

20LEGISLATING THROUGH BUDGET RECONCILIATION

Because of the relative ease of passing sweeping changes with a simple majority,

Budget Reconciliation has also become an important vehicle for legislative change in

Washington. Since 1980, Budget Reconciliation has been used for:

Spending cuts in 1980

Deficit-reduction packages throughout the 80s and 90s

Welfare reform in 1996

Bush tax cuts in 2001 and 2003

Amend the Affordable Care Act in 2010

Tax cuts in 2017

21BUDGET RECONCILIATION LIMITS

Reconciliation can’t expand mandatory spending, even if The “Byrd rule,” named for late Senator

such spending is offset and can’t be used for provisions Robert Byrd and codified under the

“extraneous” to the federal budget. Congressional Budget Act, was put into place

to limit matters that are “extraneous” from the

Byrd Rule - Section 313(b)(1) of the Congressional Budget national budget for consideration under a

Act sets forth six ways a provision is extraneous under the reconciliation bill.

Byrd rule. Provisions are extraneous if they:

o Have no budgetary effect (do not produce a change in outlays or revenues);

o produce changes in outlays or revenue which are merely incidental to the non-budgetary

components of the provision;

o are outside the jurisdiction of the committee that submitted the title or provision for inclusion in

the reconciliation measure;

o increase outlays or decrease revenue if the provision's title, as a whole, fails to achieve the

Senate reporting committee's reconciliation instructions;

o increase net outlays or decrease revenue during a fiscal year after the years covered by the

reconciliation bill unless the provision's title, as a whole, remains budget neutral;

o contain recommendations regarding the OASDI (social security) trust funds.

Source: Congressional Research Service, “The Budget Reconciliation Process: The Senate’s “Byrd Rule””, Updated December 1, 2020 https://crsreports.congress.gov/product/pdf/RL/RL30862 22RECONCILIATION AND MULTIEMPLOYER RELIEF

Does multiemployer relief have a budgetary impact?

If a provision doesn’t affect outlays or revenues (or the terms and conditions for generating outlays or

revenues), it will not have a “budgetary impact”. Since both CAMPRRA and EPPRA require

governmental outlays through expanded PBGC partition assistance, it seems likely that this would not

be an issue. There is some precedence here. Congress passed two bills that expanded PBGC’s tools

(and increased PBGC’s premiums) through Budget Reconciliation in1985 and1987.

SEPPAA (title XI of P.L. 99-272 of the Consolidated Omnibus Budget Reconciliation Act of 1985) raised

the per-participant single employer premium and created new financial distress criteria for employers

to meet before they could terminate their single employer pension plans. It also expanded PBGC’s

employer liability claim and claim for nonguaranteed benefits.

The Omnibus Budget Reconciliation Act of 1987 (P.L. 100-203) increased PBGC’s single employer

premium again, created a variable rate premium, expanded PBGC’s employer liability claims and lien

authority, and changed some funding requirements.

23RECONCILIATION AND MULTIEMPLOYER RELIEF

Would multiemployer financial assistance be within the “budget window”?

Both CAMPRRA and EPPRA assume an applying plan would continue to get partition assistance throughout

a long-term solvency period (in practice, 30+ years). This would, of course, fall outside of the 10-year

budget window. In past budget reconciliations, the solution has been to end the outlays at the end of the

10-year window. For example, the 2001, 2003 (Bush tax cuts) and 2017 (Trump Tax cuts) all included

cuts that were intended to be permanent but instead sun-setted in 10 years with an expectation that the

bill would be extended at the end of the period. This seems more difficult to achieve for partition

assistance (would the plan merge at the end of the 10-year period? Would the original plan be on the

hook for the benefits of all participants even though they are now two plans?) but not impossible.

24SELECT SOURCES

Congressional Research Service, “The Budget Reconciliation Process: Stages of

Consideration,” Updated January 25, 2021

https://crsreports.congress.gov/product/pdf/R/R44058

Congressional Research Service, “The Budget Reconciliation Process: The Senate’s

“Byrd Rule””, Updated December 1, 2020

https://crsreports.congress.gov/product/pdf/RL/RL30862

U.S. House of Representatives Ways and Means Committee, Green Book Chapter 12:

Pension Benefit Guaranty Corporation Legislative History, https://greenbook-

waysandmeans.house.gov/book/export/html/306 (2008)

Joyce, Phillip G., “Congressional Budget Reform: The Unanticipated Implications for

Federal Policy Making” Public Administration Review, Vol. 56, No. 4 (Jul.0 Aug. 1996)

pp. 317-325 https://www.jstor.org/stable/976372?seq=1

25You can also read