QUARTERLY PROPERTY MARKET & ECONOMIC UPDATE - NEW ZEALAND QUARTER 4, 2020 - CORELOGIC

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Quarterly Property Market & Economic Update New Zealand Quarter 4, 2020

Table of Contents

About CoreLogic. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 3

Executive Summary. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 4

Macro Economic and Demographic Indicators. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 5

New Zealand Asset Classes . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 6

New Zealand and Australia GDP Growth. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 7

New Zealand Population. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 8

Migration . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 9

Regional Building Consents . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 10

Consumer Confidence. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 10

Employment . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 11

Interest Rates . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 12

Housing Overview . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 14

Early Property Market Indicators . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 15

Listings. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 15

Lending Conditions . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 16

Sales Volumes. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 18

Values. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 19

Rent. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 20

House Price Index . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 23

Buyer Classification . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 24

Main Cities Housing Market Indicators. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 25

Auckland Market Activity. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 26

Auckland Values . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 27

Current Auckland Suburb Values . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 28

Hamilton Market Activity. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 30

Hamilton Values . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 31

Tauranga Market Activity. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 32

Tauranga Values . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 33

Wellington Market Activity . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 34

Wellington Values. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 35

Christchurch Market Activity. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 36

Christchurch Values. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 37

Dunedin Market Activity. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 38

Dunedin Values. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 39

CoreLogic Data and Analytics . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 40

Legal Disclaimer . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 41

2

About CoreLogic

CoreLogic is a leading property information, analytics and Contact

services provider in the United States, Australia and New Zealand.

Call us 0800 355 355

CoreLogic helps clients identify and manage growth opportunities,

improve performance and mitigate risk, by providing clients with Wellington office

innovative, technology-based services and access to rich data Level 2, 275 Cuba Street

and analytics. PO Box 4072

Wellington 6140

Whilst all reasonable effort is made to ensure the information in this

publication is current, CoreLogic does not warrant the accuracy, Auckland office

currency or completeness of the data and commentary contained in Level 5

this publication and to the full extent not prohibited by law excludes 41 Shortland Street

all loss or damage arising in connection with the data and Auckland 1010

commentary contained in this publication. Email: reports@corelogic.co.nz

corelogic.co.nz 3

Executive Summary

The upturn for the property market that started in Q3 Classification series shows that the key buyer groups

last year gathered considerable momentum in Q4, of interest are still first home buyers (23% of

with buyer demand (especially from investors), purchases in Q4) and mortgaged investors, who

mortgage lending activity, property sales volumes, surged up to a 27% market share in the final three

and property values all showing strength in the final months of 2020. Given that FHBs don’t have anything

three months of 2020. However, the (un-)affordability to list/sell before they buy and that very few investors

problem has come to the fore again, and both the are selling much at present either, their continued

Government and Reserve Bank have the property buying presence will keep the pressure on the supply/

market firmly in their sights. demand balance in the market.

A key support for the recent strength in the property Looking at movers, their share of purchases dipped to

market has been the decent performance of the just 26% in Q4, an historically low level. In some cases,

economy, especially with unemployment not rising as existing owner-occupiers are choosing to stay where

far as had been anticipated. Indeed, from its current they are due to already high debt levels and the extra

level of 5.3% (up from the recent low of 4.0%), the costs of moving house (such as legal, estate agent etc).

unemployment rate may only rise by another 1% or But in other cases, people aren’t moving because they

so. Meanwhile, timely indicators such as the NZ simply can’t find the ideal next property, given the

Activity Index show that the wider economy continues tight supply of available listings. In turn, that is feeding

to recover, and sectors such as construction are still back into an even tighter listings picture.

growing steadily (despite previous fears of a collapse).

With the property politics having heated up and

In the property market itself, mortgage credit has affordability pressures re-emerging, it looks likely that

continued to flow in the past few months. Indeed, regulation will be a key feature of the market in 2021.

after the slump in activity in April and May, new We’ve already seen the Reserve Bank move to

lending flows quickly recovered. Indeed, the rise in reinstate the LVR speed limits from 1st March, and

activity over the second half of 2020 was so strong there is surely a growing chance that a 40% deposit

that it far outweighed the lockdown-related hiatus, requirement for investors could be officially mandated

and left the value of mortgage lending by the banks later in the year (ANZ has already done so). Indeed,

up by almost 10% for the calendar year. the last time that mortgaged investors had a market

share as high as they do now – which was back in Q3

Consistent with that, property sales volumes also 2016 – was also when the RBNZ previously imposed a

picked up strongly in the final few months of 2020 and 40% deposit requirement. Meanwhile, an extension to

in fact could have been even higher still were it not for the current five-year hold period for the Brightline

the lack of listings on the market – you can’t buy Test could be on the cards too, while the Reserve

what’s not for sale. Combined with low mortgage Bank has also requested the ability to use debt to

rates, that lack of choice for buyers has been a key income ratio caps if and when they deem it necessary.

contributor to the sharp growth in property values

lately. So overall, there are many moving parts and a COVID

relapse could of course change everything. But for

Indeed, the CoreLogic House Price index showed that now, it would seem that property sales volumes will

average property values across NZ as whole rose by be solid again in 2021, and that property values will

6.1% in Q4 – a figure not seen since 6.6% in the three continue to rise. However, after an 11% gain in values

months to February 2004. Tauranga (10.2%), in 2020, growth in 2021 could be a little slower, as

Wellington (8.1%), and Dunedin (6.4%) were all above those potential regulatory changes in the property

that national average, with smaller areas such as market start to take effect.

Masterton and Whanganui also recording strong

growth. Hamilton (4.1%) and Christchurch (3.4%) were As always, we keep a running monitor on the property

slightly more subdued in Q4, but those growth figures market every week via our NZ Property Market Pulse

were still fairly solid, especially for Christchurch (which articles, so be sure to check these out on our website

has seen little change at all in property values for a http://www.corelogic.co.nz/news-research/

number of years now). all-news/. Our podcast is also a great source of data

and commentary: https://

What’s more, it may be that listings remain fairly low corelogicnzpropertymarket.buzzsprout.com/.

4 for a while yet. After all, the CoreLogic Buyer 4

Macro Economic and

Demographic Indicators

5

New Zealand Asset Classes

RESIDENTIAL REAL ESTATE

$1.35 trillion

$298 billion in home loans

COMMERCIAL/INDUSTRIAL REAL ESTATE

$229 billion

NZ LISTED STOCKS

$197 billion

NZ SUPER & KIWISAVER

$126 billion

The value of residential property across the country as at Q4 2020 was $1.35T. Mortgages are secured against

22% of this value, or in other words, 78% of the value of the property market is household equity. However,

it’s also important to note that household debt is high relative to income, and to some extent the debt has

only been sustainable in recent years because of low mortgage rates.

Ever since lockdown the NZX has been on a reasonably steady upwards trend, and indeed after reaching a

trough of less than 8,500 in late March, it has since rebounded to sit at around 13,400 in early January (a rise

of more than 55%). The rise in the sharemarket has been replicated for pooled investment funds, with the

values of KiwiSaver pots and the NZ Super Fund also continuing to improve.

6 Sources: CoreLogic NZ, Reserve Bank of NZ, NZX, NZ Super Fund 6

New Zealand and Australia GDP growth

After dropping by 11% during Annual Average GDP Growth (%)

April-June (obviously with a

large COVID effect from 8

lockdown and subsequent

social restrictions), NZ’s GDP 7

surged back by 14% over 6

July-September. The net

result is that the economy is 5

estimated to actually be a bit

4

bigger now than it was a year

ago, even though we haven’t 3

had any international tourists

2

for the past 6-9 months.

Clearly, this is an impressive 1

result, although it does reflect

the influence of social 0

support packages such as the

-1

wage subsidy, which have

now ended. -2

Even so, the timelier -3

indications from the NZ 1990 1994 1998 2002 2006 2010 2014 2018

Activity Index show that

activity continued to expand Australia NZ

in October and November, so

that bodes well for the official

Q4 GDP release (18th March). Annual Change in New Zealand Activity Index and GDP (%)

Over the coming months and

quarters, economic data has 10%

the potential to remain a little

‘jumpy’, although the overall 5%

prospects for GDP growth

look brighter this year,

especially if the COVID 0%

vaccine can be rolled out

successfully and we can -5%

regain some of the lost

international tourism.

-10%

-15%

-20%

-25%

2004 2008 2012 2016 2020

GDP NZ Activity Index

Source: Reserve Bank of New Zealand, Stats NZ 7

New Zealand Population and Migration

Quarterly Change in National Population Change Composition

Population (persons per quarter) (persons per quarter)

40000

50000

35000

45000

30000

40000

25000

35000

30000 20000

25000 15000

20000 10000

15000 5000

10000 0

5000 -5000

0 -10000

1992 1996 2000 2004 2008 2012 2016 2020 1996 2000 2004 2008 2012 2016 2020

4 quarter moving average Natural increase

Quarterly population change Net migration

Annual Change in Population (persons)

105000

37000

4200 5100 7000

3100 1800

There’s been a dramatic slowdown in the rate of population growth in the past two quarters, from an annual

pace of 2.4% in Q1 to 1.9% in Q3. Natural growth (i.e. births minus deaths) has of course been pretty steady,

so the overall slowdown reflects the migration component – which is no surprise, given the closed border.

Indeed, after averaging about 18,500 per quarter throughout 2019, the net migration figure was just 900

people in Q2 2020 and 1,600 in Q3. These are the weakest migration figures for 6-7 years.

Both arrivals and departures of migrants have fallen in recent months, with the (low) arrivals mostly made up

of returning NZ citizens, and the departures mostly being non-citizens. Although the so-called ‘flood’ of

returning kiwis post-COVID has probably been exaggerated a bit, it’s still true that the net balance for kiwi

migration is much stronger than it was in the 2000s and early 2010s, when the so-called brain drain was in full

swing. Indeed, in 2011-12, we lost more than 40,000 NZ citizens in net terms, whereas over the past 12

months we’ve gained more than 20,000.

8 Source: Statistics New ZealandLong term migration (12-month rolling totals)

250,000 Net

Arrivals

Departures

200,000

150,000

100,000

50,000

0

-50,000

2002 2006 2010 2014 2018

Migration flows for NZ citizens (12-month rolling totals)

80,000 Departures

Arrivals

Net

60,000

40,000

20,000

0

-20,000

-40,000

-60,000

2002 2006 2010 2014 2018

Source: Statistics New Zealand 9Building Consents

New dwelling consents trend (consents per month)

1,800 Auckland region

Waikato region

1,600

Wellington region

Canterbury region

1,400

Rest of NI

Rest of SI

1,200

1,000

800

600

400

200

0

1995 1999 2003 2007 2011 2015 2019

Residential construction activity continues to hold up better than many would have thought, with the

shortage of available property on the market probably pushing some buyers towards a self-build or off-the-

plans purchase. Indeed, the number of new dwelling consents was more than 38,000 in the 12 months to

November 2020, higher than the pre-COVID peak back in February, and again the strongest levels since the

mid-1970s.

Much of the strength in nationwide construction activity reflects the growing role for smaller dwellings such

as townhouses, while regionally the key market remains Auckland. This all seems pretty logical, as we face the

need to accommodate an ever-growing population in a more intensified dwelling stock. Of course, at the same

time, consents issued for alterations to existing properties are also running at high levels, with more people

choosing to renovate rather than relocate. This is also a useful trend in terms of improving the quality of

housing.

However, although dwelling consents are running at high levels in their own right, they’re not quite as

impressive when you look relative to our population. Indeed, we’ve recently been consenting about 7.5 new

dwellings per year for every 1,000 people in the country, which is the highest for about 15 years, but still well

below the figures of 13 in 1973 and 12 in 1974. In other words, we need to keep dwelling consents going at

current levels for a number of years yet, or perhaps even raise them further.

Unfortunately though there are already signs emerging of cost pressures in the construction industry,

reflecting rising land prices and also labour shortages. This could restrain our ability to keep dwelling

consents high over a series of years. In addition, restrictions on development finance are always a lingering

risk.

Overall, the high number of dwellings already consented suggests that builders will be busy well into 2021.

The hope thereafter is that consents will stay high and help to alleviate the supply pressures that we face, and

in turn help to improve housing affordability. Encouragingly, the Government has indicated that they will

continue with a strong state house construction programme.

10 Source: Statistics New ZealandConsumer Confidence

ANZ-Roy Morgan Consumer Confidence (index, monthly)

160

140

120

Average

100

80

60

40

20

0

2004 2006 2008 2010 2012 2014 2016 2018 2020

The recent trend for the ANZ Roy Morgan consumer confidence measure has been positive, with the index rising from

100 in September to 112 in December – the highest reading since February. December’s figure was still below the long

term average of around 119, but even so the recent rises have still been encouraging.

In other words, confidence amongst households has rebounded from the worst point of alert level four lockdown, and

although there were fears that the end of the wage subsidy may reverse the stronger trend, confidence has proved to

be pretty resilient in the past few months. No doubt low mortgage rates and steadily rising house prices are playing a

role in supporting consumer confidence, while the smaller-than-expected rise in unemployment (so far) is also likely to

have been a factor.

Meanwhile, a similar message applies for business confidence – it has been rising in recent months and suggests that

the economy should start off fairly well in 2021.

Sources: ANZ, Roy Morgan 11Employment

Annual change in employment, Labour force

full time and part time participation rate (%)

10% 72

8%

70

6%

68

4%

66

2%

0% 64

-2%

62

-4%

Full time 60

-6%

Part time

-8% 58

1987 1998 2009 2020 1987 1999 2011

Number of Jobseeker

Unemployment rate (%) Support claimants

12

240,000

10

220,000

8

200,000

6 180,000

160,000

4

140,000

2

120,000

0 100,000

1986 1998 2010 Jan-20 Mar-20 May-20 Jul-20 Sep-20 Nov-20

The latest labour market figures were clearly weaker than the recent past, with overall employment growth

slowing to 0.4% year on year in Q3, the lowest since 0.2% in Q1 2013. Part-time employment growth

accelerated to 3.4% in Q3, but this probably isn’t as encouraging as it looks – given that it may reflect a shift of

workers from full-time jobs into a reduced hours situation. Indeed, the full-time employment figure actually

dropped by 0.3% in Q3 2020, the first fall since 2012.

Meanwhile, after a drop in Q2 from 70.7% to 69.9%, the labour force participation rate (people employed or

looking for work as a percentage of the working age population) rose back slightly in Q3 to 70.1%. This

explains part of the sharp rise in the unemployment rate in Q3, from 4.0% to 5.3%, but the most significant

factor there was simply people losing their jobs – especially in tourism related sectors of the economy.

Looking ahead, the unemployment rate is unfortunately expected to rise further in the coming months.

However, the end of the wage subsidy doesn’t appear to have triggered the sharp job cuts that some were

fearing, and unemployment rate projections are being slowly improved. Indeed, whereas a few months ago

the Reserve Bank was predicting a peak unemployment rate of more than 9%, that forecast has now been

reduced to around 6.5%.

All else equal, higher unemployment will tend to be a restraint for the housing market, although to the extent

that it’s younger/lower-paid workers who feel more of the brunt, it may be the tenant/rental sector that gets

more affected than owner-occupation.

12 Source: Stats NZ, Ministry of Social DevelopmentInterest Rates

The outlook for interest rates looks a little more mixed Mortgage Interest Rates (%)

than it done for a while now. On one hand, the Reserve 25

Bank’s (RBNZ) asset purchase programme is still in action, 2 year fixed rate

and their cap remains at $100bn of purchases out to June Floating mortgage interest rates

20

2022. Meanwhile, the Funding for Lending Programme is

also underway, which means banks can access cheap loans

directly from the RBNZ, which in turn allows them to 15

continue lending to business and households at low

interest rates. In short, these measures point to further

10

low rates for borrowers.

On the other hand, however, the bounce-back in the 5

economy in Q3 (and the continued strength of other

economic indicators for October through to December) as

0

well as the resilience of the property market suggest that 1965 1971 1977 1983 1989 1995 2001 2007 2013 2019

the chances of a negative official cash rate have receded –

which in turn would indicate that mortgage rates might

have already reached a floor. Official Cash Rate and Mortgage Rates (%)

12

Overall, a typical new mortgage (with a 20% deposit) on a OCR history

OCR projection

one year fixed term currently carries a rate of around 2.5%,

10 2-yr fixed mortgage

and while further falls in interest rates couldn’t be ruled

out (especially if the banks enter a new ‘rate war’), previous

8

expectations that they could fall below 2% are now looking

less likely. Of course, significant rises in interest rates aren’t

6

especially likely for the next year or two either.

4

2

0

2000 2009 2018

Average Two Year Fixed Mortgage Rates (%)

5 .2%

4 .7%

4 .2%

3 .7%

3 .2%

2018 2019 2020

Source: Reserve Bank of NZ, interest.co.nz 13Housing Overview 14

Early Property Market Indicators

During alert level four lockdown, measures relating to the early stages of a sale process – i.e. pre-listing (such as appraisals

generated by real estate agents) and pre-mortgage (valuations ordered by banks) – fell away sharply, which was no surprise.

However, as our Early Market Indicators Report shows, they then bounced back steadily, and have recently been running at

around normal levels: https://www.corelogic.co.nz/early-market-indicators

In other words, the early stages of both the supply (appraisals, which lead to listings) and demand (borrowers requesting a

mortgage, hence the bank ordering a valuation) pipelines are holding up well, which points to further resilience for property

sales volumes in the coming months. If anything, demand has been running ahead of supply, which suggests continued

upwards pressure on property values too.

Listings

Weekly flow of new for-sale listings Weekly flow of new for-rent listings

3,500

2020 4,000

2020

2019 3,500

2019

3,000

3,000

2,500

2,500

2,000

2,000

1,500

1,500

1,000

1,000

500

500

0 0

Jan-20 Feb-20 Apr-20 Jun-20 Aug-20 Oct-20 Dec-20 Jan-20 Feb-20 Apr-20 Jun-20 Aug-20 Oct-20 Dec-20

A key and ongoing feature of the NZ property market in recent times has been the low supply of listings available on the

market, which has been bolstering property values as buyers continue to face limited choice. There has been no material

change in the tight listings situation in the past three months either, with the total stock of existing properties available for

sale running at multi-year lows.

In turn, that has reflected both a continued stream of achieved sales (which removes listings at the end of pipeline) but also

only a ‘normal’ flow of new listings coming onto the market at the start of the pipeline. Indeed, after the listings lull of April/

May, it was possible that we’d subsequently see new listings running above previous levels – but this hasn’t happened.

In some ways, there is a vicious circle going on for listings, with some existing owner-occupiers not moving house because

they don’t have much choice about their next property. And of course, those owners are then not listing their own house,

which feeds back into even tighter supply conditions. Similarly, other active buyer groups at present – namely first home

buyers (FHBs) and mortgaged investors – aren’t generally selling any property before they purchase either (certainly FHBs

are not selling anything, by definition).

A similar message applies for new rental listings. In recent weeks, they’ve only been running at ‘normal’ levels, despite the

lack of activity in April/May.

Source: CoreLogic 15Lending conditions

Annual Change in Gross New Lending Flows ($m per month)

3,000

2,000

1,000

0

-1,000

-2,000

-3,000

2016 2017 2018 2019 2020

Investor Owner-occupier

In the past three months, mortgage lending activity has continued to surge higher and the new flows hit

$9.3bn in November, having topped $7bn in each of September and October. In each case, this equated to an

annual increase of at least $1.7bn. Indeed, after April’s lockdown disrupted the market, the bounce-back has

been so strong that total lending flows for 2020 so far have returned to being much higher than for 2019.

First home buyers have been active borrowers this year, but perhaps the most important driver has been

demand from mortgaged investors. The reduction in term deposit rates has diverted some of their money

into the property market, while of course low mortgage rates have been a factor as well. But on top of that,

the temporary removal of the loan to value ratio rules (LVRs) has been another important driver – many

investors who may previously have struggled to raise the 30% deposit have been able to purchase property

with a 20% deposit instead.

That said, this doesn’t mean that general credit standards have dropped. In fact, banks are still scrutinising a

borrower’s income and expenses very closely, and also applying their serviceability tests at (hypothetical)

interest rates of more than 6%. Generally speaking, all borrowers are still requiring at least a 20% deposit too.

However, the surge in activity amongst higher LVR investors has prompted the age-old debate about what’s

‘good’ for the property market, and the RBNZ of course is consulting on the reinstatement of the previous LVR

regime – i.e. 20% deposit for owner occupiers with a 20% allowance outside the threshold (speed limit), and a

30% deposit requirement for investors with a 5% speed limit. This looks likely to become the official

requirement again from 1st March, while of course the ANZ bank has gone even further, requiring investors to

put in 40%.

16 Sources: Reserve Bank of New ZealandWith all this in mind, then, it’s High LVR Lending to Owners and Investors (% of new lending)

likely that securing a mortgage

may be a little tougher this year 25%

than it was for most of the

second half of 2020. In turn,

this could take a little heat out 20%

of sales activity and property

prices as we move through the

next few months – especially if

15%

the Government also gives the

RBNZ the ability to impose debt

to income ratios (DTIs) on

lending at some stage. 10%

Finally, it needs to be noted that

the mortgage payment deferral 5%

scheme will end on 31st March.

However, about 90% of these

deferrals have already ended

0%

without too much trouble, so it

2014 2015 2016 2017 2018 2019 2020

seems unlikely that the passing

of the late March deadline will

have too much impact on the

general lending environment or Refinancing Profile for Mortgages (% of stock)

the wider property market.

50%

44.57%

45%

40%

35%

30%

25%

20% 18.09% 17.71%

15%

10.48%

10%

5.62%

5% 3.52%

0%

Floating Fixed < 1 year Fixed > 1 year

Investor Owner-occupier

Sources: Reserve Bank of New Zealand 17Sales Volumes

The first few months of strengthening property Nationwide Sales Volumes

sales activity post-lockdown could be mostly (monthly total)

explained by ‘catch up’ demand after the pause

during April/May, but that’s no longer the case – we 14,000

now have genuine new and extra demand in the 13,000

12,000

market. Indeed, the monthly sales total (across 11,000

private and agent sales) for October topped 10,000, 10,000

9,000

then climbed even higher to 11,112 in November, and

8,000

stayed above 10,000 in December too. 7,000

6,000

The rebound in activity has been seen in almost all 5,000

4,000

parts of the country – and it’s worth noting that 3,000

sales activity may have been even higher still, were it 2,000

not for the low supply of property listed and actually 1,000

available to buy. Indeed, areas that perhaps haven’t 1996 1999 2002 2005 2008 2011 2014 2017 2020

seen such a strong rebound in sales are more likely

to have restrained by lack of supply rather than

sluggish demand. Nationwide Annual Change

The rise in demand has reflected continued interest in Sales Volumes (%)

from first home buyers, who in many cases are

tapping their KiwiSaver funds for the deposit (or at 40%

least part of it), but also mortgaged investors – in

20%

particular, those who were previously struggling to

find the 30% deposit, but thanks to the temporary 0%

removal of the LVR speed limits have recently been -20%

able to purchase with 20%.

-40%

Looking ahead, the environment is favourable for

-60%

more solid levels of property market activity in the

coming months, especially given continued low -80%

mortgage rates and the fact that unemployment 1996 1999 2002 2005 2008 2011 2014 2017 2020

isn’t expected to peak as high as was previously

thought. We’d anticipate sales activity in 2021 being

around the 90,000 mark, similar to the past few

years, and in line with long term averages (albeit

Regional Sales Volumes

below past peaks in 2015-16 and the mid-2000s). (year-on-year % change)

55%

50%

45%

40%

35%

30%

25%

20%

15%

10%

5%

30.5% 54.4% 36.5% 32.4% 7.4% 32.4% 10.8%

NZ AUK HAM TAU WEL CHC DUN

18 Source: CoreLogicValues

Reflecting the tight supply/ Average Value of Housing Stock - New Zealand ($)

demand balance and low

mortgage rates, property

$788,967

$800,000

values have well and truly

spiked higher in the past few

$700,000

months. In addition, the upturn

has been broad-based across

the country, including $600,000

previously more subdued areas

such as Christchurch and $500,000

Selwyn.

In December, national average $400,000

property values rose by 2.6%,

taking the three month change $300,000

to 6.1%, and the annual growth $788,967

rate to 11.1%. That equates to a

$200,000

value of $788,967, up by almost

$79,000 from a year ago. This is

obviously a drastically different $100,000

level for house prices than

would have prevailed if those $0

pessimistic forecasts during 2005 2008 2011 2014 2017 2020

lockdown of a 15-20% fall in

prices had become reality. Annual and Quarterly Change in Value (%)

In addition, the momentum 20.0% Quarterly Change $45,289 6.1%

looks to be upwards for at least Annual Change $78,838 11.1%

the first few months of 2021 5 Year Change $229,919 41%

too. The end of the mortgage 15.0%

deferral scheme on 31st March

shouldn’t be too much of an

10.0%

issue, but the reinstatement of

LVRs on 1st March (especially if

investors were to eventually

5.0%

require a 40% deposit) and

ever-increasing affordability

pressures could start to bite 0.0%

thereafter and mean a slower

end to 2021 for property

values. -5.0% Quarterly Change $45,289 6.1%

Annual Change $78,828 11.1%

Annual Change %

5 Year Change $229,919

Quarterly Change % 41%

-10.0%

2005 2008 2011 2014 2017 2020

Quarterly Change % Annual Change %

19House Price Index

The upswing in property values has been seen Average Dwelling Value ($)

right across the country, and although the

‘provincial’ markets are still seeing the largest $1,200,000

New Zealand

gains, the main centres have accelerated too. Auckland

Hamilton

$1,000,000 Tauranga

Wellington

Areas such as Gisborne (30.4%), Masterton Christchurch

Dunedin

(29.6%), and Rangitikei (27.6%) have all seen $800,000

average property values rise by more than 25%

$600,000

over the past 12 months. But larger areas such as

Palmerston North and New Plymouth have also $400,000

seen pretty strong gains in values, at 20.3% and

11.8% respectively. $200,000

In Auckland, average values have risen 6.0% over $0

2008 2011 2014 2017 2020

the past three months (to December), and by 9.1%

over the past year. Manukau and Waitakere have

seen the fastest upturns within Auckland, while the more expensive North Shore and Auckland City (old

territorial authority) markets have lagged behind slightly.

Tauranga’s average values have surged by 10.2% in the past three months and by 14.8% over the past year, to

now stand at $876,122. Hamilton has seen an increase of close to 12% since December last year, while

Dunedin’s average values are up by 13.1%, and the wider Wellington area (City, Porirua, Upper Hutt, Lower

Hutt) by 15.4%.

Meanwhile, even the previously lagging markets around Canterbury have shown signs of life. Selwyn and

Christchurch have both seen average values rise by about 3.5% in the past three months (and by roughly 6%

over the past 12 months), while Waimakariri’s figures have been 5.4% and 8.5% respectively.

December 2020

Current value 1 month 3 months 12 months 5 years

New Zealand $788,967 2.6% 6.1% 11.1% 41%

Auckland $1,142,700 2.4% 6.0% 9.1% 23%

Hamilton $674,562 2.3% 4.1% 11.7% 52%

Tauranga $876,122 6.8% 10.2% 14.8% 62%

Wellington $861,794 3.2% 8.1% 15.4% 81%

Christchurch $539,561 1.6% 3.4% 6.2% 12%

Dunedin $582,269 1.9% 6.4% 13.1% 88%

20Annual Value Change (%)

-4% 36%

© 2021 Mapbox © OpenStreetMap

Over a 12 month horizon, average property values have risen in almost all parts of the country, with the most

strength evident in the central and lower North Island. Queenstown’s values have ‘only’ been flat over the

past 12 months, but this is actually a pretty good result, given the sharp falls seen in the first few months

after lockdown.

21Three Month Value Change (%)

-1% 9%

© 2021 Mapbox © OpenStreetMap

Over the shorter three-month period since September, the acceleration in the property market is clear

to see pretty much right across the country – including almost all of the North Island, and large parts of

Canterbury and Otago. Parts of Southland, by contrast, have looked a little softer.

22Rent

National Annual Change Gross Rental Yield – National (%)

in Value and Rent (%)

20% Annual change in rent

4 .5%

Annual change in value

15% 4 .0%

3 .5%

10%

3 .0%

5%

2 .5%

0% 2 .0%

1 .5%

-5%

1 .0%

-10%

0 .5%

-15% 0 .0%

2005 2008 2011 2014 2017 2020 2005 2008 2011 2014 2017 2020

National rents averaged $480 in the three months to December, up by 8.0% from the same period a year earlier. Rental

growth has accelerated quite strongly since it dipped to about 3% in July/August, and there are certainly few signs of much

rental weakness, which might have been anticipated given the unemployment problems being experienced by younger

workers at present (who are more likely to be renting than in owner-occupation).

Auckland’s rents in the three months to November averaged $566 per week, up by 6.8% from a year earlier, while

Wellington’s market has been a little softer lately, with rents ‘only’ up by 4.7% annually. By contrast, Dunedin has seen

average rents rise by 10.5% over the past year, Tauranga by 10.6%, and Hamilton and Christchurch both at 8-9%.

Meanwhile, outside the main centres, areas such as Gisborne, Whanganui, and Invercargill have all seen average weekly

rents rise by about 15% or more over the past year. It’s only really Queenstown that continues to see much downwards

rental pressure, with a drop of almost 17% over the past year.

Rental yields around the main centres range from 2.6% in Auckland up to 3.8% in Christchurch. With term deposit rates

falling (and borrowing getting cheaper too), the rising presence of investors in the market shows that those property yields

are starting to look increasingly attractive.

Med Weekly Rent Ann chg rent Gross yield

Auckland $566 6.8% 2.6%

Hamilton $433 7.5% 3.3%

Tauranga $523 10.6% 3.1%

Wellington $566 4.7% 3.0%

Christchurch $399 9.4% 3.8%

Dunedin $393 10.5% 3.5%

23Buyer Classification

Buyer Classification – NZ Property Transfers by Non-Citizens

New Zealand (% of sales) or no Resident Visa (% of total transfers)

3 .5%

Mover

30% 30% First Home Buyer

27% Multiple Property Owner Mortgage

3 .0%

Multiple Property Owner Cash

30% 30% 26% New to Market

26%

ReEntry

26% Other

26% 23% 2 .5%

21% 25%

20% 21% 25%

2 .0%

20%

1 .5%

12%

10% 10% 12% 1 .0%

10% 10%

5%

5%

4%

5%5%

5%

0 .5%

4% 5%

4%

4% 2%1%

0%

0% 0 .0%

2005

2005 2008

2008 2011

2011 2014

2014 2017

2017 2020

2020 2017 2018 2019 2020

Mover Multiple property owner mortgage Buying Selling

First home buyer Multiple property owner cash

New to market ReEntry Other

The past few months have seen a continuation of recent buyer trends, with first home buyers (FHBs)

managing to sustain a market share in the mid-20%’s, while mortgaged investors have continued to rise, with

movers (i.e. existing owner-occupiers) tending to be relatively quiet.

The key trend in recent months has really been the continued growth in market share for mortgaged

investors. Indeed, after troughing at just 22% in Q4 2017, their share of purchases has steadily risen and in Q3

2020 was 26%. It has pushed even higher in Q4, reaching 27% – that is the highest figure seen since 28% in Q3

2016, which was just prior to the Reserve Bank (RBNZ) imposing the 40% deposit requirement on investors

nationwide.

The low interest rate environment is having a two-way effect on investors – it’s cheap to borrow, so they’re

actively seeking property because of that. But at the same time, low rates on term deposits are also creating

an incentive to take money out of the bank and look for alternative asset choices, such as property. Indeed,

the stock of money held in bank term deposits has actually fallen in recent months. Meanwhile, investor

demand for property has also been stimulated by the temporary removal of the LVR speed limits, which has

allowed more buyers to get in with a 20% deposit rather than the previous 30%.

Of course, the Reserve Bank has consulted on reinstating a 30% deposit for investors, which looks likely to

commence from 1st March. Meanwhile, ANZ for example has already gone further, requiring a 40% deposit

from investors. These restrictions are likely to take some heat out of investor demand, but not remove it

altogether – there’ll still be buyers who can find the required 30-40% deposit.

Meanwhile, the share of property purchases in Q4 made by FHBs was 23%, down from Q3’s figure of 25%, but

still a very strong share by historical standards. FHBs are still using their KiwiSaver funds for the deposit (or at

least part of it), while a compromise on location and/or property type is also helping them into the market.

Looking at movers, their share of purchases dipped to just 26% in Q4, an historically low level (indeed the

lowest since Q4 2010). In some cases, existing owner occupiers aren’t moving because they simply can’t find

the ideal next property, given the tight supply of available listings. In turn, that is feeding back into an even

tighter listings picture – i.e. it’s a vicious circle.

24 Source: Statistics New ZealandMain Cities Housing

Market Indicators

25Auckland Market Activity

Buyer Classification – Auckland Buyer Classification – Northland

(% of purchases) region (% of purchases)

40%

Mover First Home Buyer

Multiple Property

30% Multiple Property Owner Mortgage

Multiple Property

Multiple Property34%

Owner Cash

New to Market

30% 30% First Home Buyer 32%

Mover

28%

28% 29% New to Market32%

30% ReEntry

27%

27% 28% Other

30%

ReEntry

Other

27% 26%

27% 23% 27%

20%

20% 20% 22% 21%

20%

21% 21%

20% 20%

19% 18%

15%

15%

12% 15% 15%

10%

10% 11% 12%

10%

10%

7%

7% 8% 7%

6%

5% 7% 7%

7%

4%

4% 5%

4% 4% 5%

4%

0% 1%

1% 4%

4% 2%

2%

0% 2005 2008 2011 2014 2017 2020 0%

0%

2005 2008 2011 2014 2017 2020 2004

2003 2006

2006 20082009 2010 2012

2012 2014

2015 2016 2018

2018 2020

2021

Mover Multiple property owner mortgage Mover Multiple property owner mortgage

First home buyer Multiple property owner cash First home buyer Multiple property owner cash

New to market ReEntry Other New to market ReEntry Other

The national Buyer Classification trends over recent months have also been seen in Auckland, but perhaps to

an even stronger extent.

Indeed, the share of purchases going to mortgaged investors has spiked up to 30% in Q4, up from 26% back

in the middle of 2020 and also above the national share (27%). Gross rental yields are relatively low in

Auckland, so it’s possible that some of these investors have found what they perceive to be ‘bargains’,

potentially timing the market right at the start of another upswing phase.

The rise in market share for mortgaged investors has come alongside a continued low presence for movers,

with their share at just 23% in Q4 2020, roughly the lowest levels since 2009. Again, in some cases this is likely

to reflect the shortage of listings and their inability to find the ideal next property.

Meanwhile, the market share for first home buyers in Auckland has dipped in the past few months, now

standing at 26%, down from 29% in Q3. Given the renewed upswing in property values (from an already high

level of >$1m) in our biggest city, this could be the first signs of ‘fatigue’ from FHBs.

Around Auckland’s neighbouring areas, the mix of buyers is quite different in Northland, with movers

accounting for the highest share of activity, at 30% in Q4 2020. First home buyers have a much lower

presence in this market, at just 16% in Q4, while mortgaged investors have also been quieter, at 19%.

26Auckland Values

Average value of housing stock Annual and quarterly value change

Auckland ($) Auckland (%)

$1,142,700

$1,200,000 $64,374 6.0%

25.0% Quarterly Change

$1,100,000 Annual Change $95,590 9.1%

5 Year Change $210,000 23%

$1,000,000 20.0%

$900,000

15.0%

$800,000

$700,000 10.0%

$600,000

5.0%

$500,000

$400,000

$1,142,700 0.0%

$300,000

-5.0%

$200,000 Annual Change %

-10.0% Quarterly Change %

$100,000

$0 2005 2008 2011 2014 2017 2020

2005 2008 2011 2014 2017 2020

Quarterly Change % Annual Change %

The upturn in average property values for Auckland as a whole in the past few months has reflected rising markets across

each sub-area. Indeed, over the past three months, the changes in average values have ranged from around 4% to 6%

everywhere, with Franklin at the bottom of the range (4.1%) and the Auckland and Manukau City areas equal top (6.3%).

On an annual basis, the wider Auckland market has seen average values rise by 9.1%, to now stand at $1,142,700. In the

sub-markets, those annual growth rates have ranged from 7.8% in Papakura and Auckland City (old council area), up to

11.5% in Manukau.

In broad terms, first home buyers and mortgaged investors tend to be more active in cheaper areas, while movers are

more important in more expensive areas (where a higher amount of equity is required). This pattern for buyer types – with

FHBs and investors generally busy at present; but movers quieter – would help to explain continued rapid value gains in

cheaper parts of Auckland, but a (slightly) more subdued picture elsewhere.

DECEMBER 2020

Current value 1 month 3 month 12 months 5 years

Rodney $1,040,323 2.1% 5.6% 10.2% 28%

North Shore $1,311,259 2.7% 6.1% 9.1% 20%

Waitakere $912,136 2.2% 5.6% 11.1% 22%

Auckland City $1,342,162 2.3% 6.3% 7.8% 22%

Manukau $1,005,432 2.8% 6.3% 11.5% 26%

Papakura $771,697 1.3% 4.3% 7.8% 28%

Franklin $740,042 1.9% 4.1% 9.3% 28%

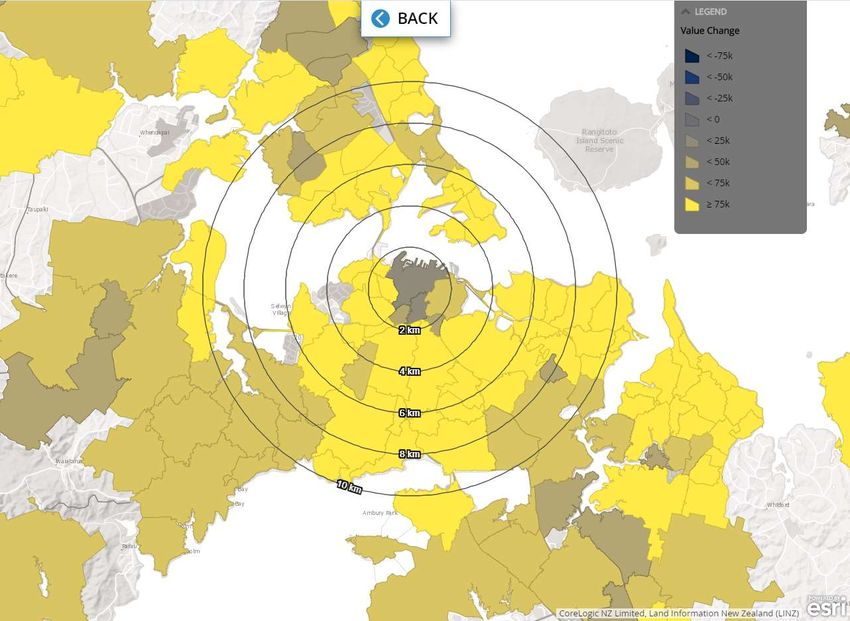

27Current Suburb Values:

‘Mapping the Market’

Auckland suburb value change 2020 ($)

Generally speaking, property values around the country have bounced back strongly since lockdown, and

even Queenstown (where there were initially sharp falls) now seems to be past the worst too. CoreLogic’s

interactive ‘Mapping the Market’ product shows the changes over the past 12 months (covering a pre- and

post-COVID phase), it’s freely available and updated quarterly. The heatmaps in ‘Mapping the Market’ are

point-in-time snapshots of median values from 2019 and 2020, and show the % and $ change over that period

too. See www.corelogic.co.nz/mapping-market

Auckland is illustrated in the heatmap here. Herne Bay remains the highest priced suburb in Auckland (and

the entire country), with a median property value of $2.68m. Auckland Central has the lowest median value

(reflecting its concentration of apartments), at about $548,000. Only three suburbs have a median value29

Hamilton Market Activity

Buyer Classification – Hamilton Buyer Classification – Waikato region

(% of purchases) (% of purchases)

40% First Home Buye

40% Mover Multiple Property

40% First Home Buyer Multiple Property

37% Multiple Property Owner Cash New to Market

Multiple Property Owner Mortgage 32% Mover

35% Market 31%

New to30% 32% ReEntry

ReEntry Other

30% 31% Other

30% 31%

30%31% 28% 25%

27%

27% 26%

24%

25%

25% 25%

20%

22%

20% 20%

20% 20% 19%

19% 17%

17% 18%

14%

14% 15%

14%

12%

10%

10% 10%

10%

7%7% 6%

8%

4% 4%

6% 5%5%

4%4% 5%5%

3%3% 3%

4% 3%

4%

2%

1% 3% 2%

0%0% 1% 0%

0%

2%

2004 2006

2006 2008

2008 2010

2010 2012

2012 2014

2014 2016

2016 2018

2018 2020

2020 2004 2006 200820092010 2012 2014 2015

2016 2018 2020 2021

2003 2006 2012 2018

Mover Multiple property owner mortgage Mover Multiple property owner mortgage

First home buyer Multiple property owner cash First home buyer Multiple property owner cash

New to market ReEntry Other New to market ReEntry Other

Hamilton’s Buyer Classification trends have also mirrored the national picture lately, but with the upswing in

market share for mortgaged investors even more pronounced.

Indeed, in the fourth quarter of 2020, mortgaged investors accounted for 37% of property purchases in

Hamilton, well above the national figure of 27% (which itself was pretty high). Again, low term deposit rates are

likely to be diverting funds towards property in Hamilton, alongside cheap mortgage rates that are

encouraging borrowing.

Meanwhile, first home buyers had a 28% share of purchases in Hamilton in Q4 2020, more or less the highest

on record. Cheaper property than in surrounding main centres (such as Auckland and Tauranga) could be

attracting some FHBs into the Hamilton market. Finally, the share in Hamilton going to movers remains low, at

just 20% in the fourth quarter of 2020.

Around the wider Waikato region (excluding Hamilton), buyer classification patterns in Q4 saw movers’ share

hold relatively steady (at about 32%), and FHBs also hold their ground at around 18%. However, mortgaged

investors’ market share continued to rise, reaching 24% in Q4.

30Hamilton Values

Average value of housing stock Annual and quarterly value change

Hamilton ($) Hamilton (%)

$700,000 $674,562 Quarterly Change $26,785 4.1%

30.0% Annual Change $70,528 11.7%

5 Year Change $230,351 52%

$600,000

25.0%

20.0%

$500,000

15.0%

$400,000

10.0%

$300,000 5.0%

$200,000

$674,562 0.0%

-5.0%

Annual Change %

$100,000 Quarterly Change %

-10.0%

$0 2005 2008 2011 2014 2017 2020

2005 2008 2011 2014 2017 2020

Quarterly Change % Annual Change %

Hamilton’s average property values have also been strong in the past few months, up by 2.3% in December alone and by

4.1% since September. The level is now just short of $675,000.

The growth in December was pretty broad-based across Hamilton, ranging from about 2% in Central & North West and

South East, up to almost 3% in North East. On a three-month change, Central & North West has lagged a little, but North

East (6.2%) and South West (5.6%) have risen sharply. Across the board for Hamilton’s sub-areas, annual changes in average

property values are now in the double-digits.

DECEMBER 2020

Current value 1 month 3 month 12 months 5 years

Hamilton Central &

$617,999 1.8% 1.5% 10.4% 48%

North West

Hamilton North East $835,599 2.8% 6.2% 11.7% 49%

Hamilton South East $622,686 1.8% 3.6% 11.2% 53%

Hamilton South West $613,105 2.4% 5.6% 13.8% 56%

31Tauranga Market Activity

Buyer Classification – Tauranga Buyer Classification – Bay of Plenty

(% of purchases) region (% of purchases)

40% 40%

40%

40% First Home Buye

First Home Buyer Multiple Property

Multiple Property Owner Mortgage Multiple Property

Multiple Property Owner Cash

New to Market

Mover

New to Market Mover

33%

33% 31% ReEntry ReEntry

30% 30% Other

31% 30% 30%

Other 30%

30%

30%

28%

27% 27% 27%

27%

25% 25%

23%

23%

22%

20% 20%

20%

19% 20%

16% 18%

18%

16% 17%

15% 16% 13%

14%

15% 15% 13%

13%

13%

10%

10% 10%

10%

6%

6%

4% 5% 5% 6%

6% 6%

5%

3%

4% 5% 4% 4%

4% 5%

5%

3% 2% 3%

3% 1%

0%0% 2% 0%

2%

0%

2004 2006

2006 2008

2008 2010

2010 2012

2012 2014

2014 2016

2016 2018

2018 2020

2020 2003 2006 2009 2012 2015 2018 2021

2003 2006 2009 2012 2015 2018 2021

Mover Multiple property owner mortgage Mover Multiple property owner mortgage

First home buyer Multiple property owner cash First home buyer Multiple property owner cash

New to market ReEntry Other New to market ReEntry Other

From October to December, movers remained the key buyer group in Tauranga, accounting for 31% of

purchases. The high market share for movers contrasts with all of the other main centres, and potentially

illustrates how a solid base of equity/wealth (which movers have, either from having lived locally or bringing in

equity from other parts of the country) is important in Tauranga, rather than necessarily local wages being a

key driver for a property purchase.

Meanwhile, first home buyers’ market share dipped in Tauranga in Q4, from 19% in Q3 to 16% - still broadly in

line with past norms. By contrast, mortgaged investors’ market share continued to creep higher, from 24% in

Q3 2020 to 27%. That was the highest share for investors in Tauranga since Q1 2018, and is a consistent trend

with many other parts of the country. Around the wider Bay of Plenty region (excluding Tauranga), mortgaged

investors are also seeing a solid market share at present, with movers a little quieter than normal.

32Tauranga Values

Average value of housing stock Annual and quarterly value change

Tauranga ($) Tauranga (%)

$900,000

$876,122

30.0% Quarterly Change $80,940 10.2%

Annual Change $112,700 14.8%

$800,000

25.0% 5 Year Change $334,241 62%

$700,000

20.0%

$600,000

15.0%

$500,000

10.0%

$400,000

5.0%

$300,000 $876,122 0.0%

$200,000

-5.0%

$100,000 Annual Change %

-10.0% Quarterly Change %

$0

2005 2008 2011 2014 2017 2020 2005 2008 2011 2014 2017 2020

Quarterly Change % Annual Change %

Tauranga’s average property values have soared in the past few months, rising 10.2% from September to December.

They’re also up by 14.8% over the past 12 months, which equates to almost $113,000. The level of values in Tauranga now

stands at more than $876,000. In surrounding areas such as Rotorua and Whakatane, the picture is a little mixed.

Whakatane’s values have been flat since September, and up by ‘only’ 6.4% in the past 12 months. However, in Rotorua,

momentum is much stronger, with the three-month gain at 8.8% and annual gain at 19.2%.

33Wellington Market Activity

Buyer Classification – Wellington Buyer Classification – Lower Hutt

(% of purchases) region (% of purchases)

40% First Home Buyer

40%

Mover

Multiple Property Owner Cash

First Home Buye

30% 30% Multiple Property Owner Mortgage

40% Multiple Propert

29% New to Market

27% Multiple Propert

ReEntry

27% New to Market

33% Other 33% ReEntry

30%

31% 30% 30%

30% 32% Mover

Other

30% 30%

27%

27%

20% 21%

25% 25%

23% 25%

22%

20%

19% 20%

20%

16% 18%

15% 17%

14%

10% 9% 15% 13%

10% 8% 10%

10%

6%

4%

4%

5%

4% 5% 6%

5% 6%

7%

5%

3%

3% 4% 4%

4%

4%

5%

2%

3%

2% 2% 0% 3%

0%0% 2004 2008 2012 2016

1%

2020

2005 2008 0%

2006 2008 201020112012 2014

2014 2017 2018 2020

2016 2020

2003 2006 2009 2012 2015 2018 2021

Mover Multiple property owner mortgage Mover Multiple property owner mortgage

First home buyer Multiple property owner cash First home buyer Multiple property owner cash

New to market ReEntry Other New to market ReEntry Other

Across the four main territorial authorities in Wellington (City, Lower Hutt, Upper Hutt, Porirua), first home

buyers remained the largest buyer group in Q4, accounting for 30% of property purchases. That was down a

touch from the figure of 31% in Q3, but still a very high level. Porirua remains a hotspot for first home buyers,

where they accounted for 32% of property purchases in Q4, with Lower Hutt seeing a figure of 33%.

Tucked just in behind first home buyers were mortgaged investors, with their rising market share a similar

trend to many other parts of the country. Lower Hutt has seen a surge of investor activity lately, with their

share rising from 22% in the second quarter of 2020 to 32% in Q4. Wellington City also has a relatively high

presence for mortgaged investors, at 29% (on a par with first home buyers).

Meanwhile, existing owner occupiers are very quiet around Wellington at present, accounting for just 21% of

purchases in Q4, basically a record low for the 15 year history of this series. As with other parts of the country,

the tight supply of available listings is meaning that many would-be movers are instead just staying where

they are, and potentially renovating (rather than run the risk of selling and not being able to find their ideal

next home).

Elsewhere around the Wellington region, mortgaged investors have also been a rising presence on the Kapiti

Coast in particular, with their share of property purchases rising from less than 20% a couple of years ago to

27% in the final quarter of 2020.

34Wellington Values

Average value of housing stock Annual and quarterly value change

Wellington ($) Wellington (%)

$900,000 $861,794

Quarterly Change $64,598 8.1%

$800,000

Annual Change $114,839 15.4%

20.0% 5 Year Change $385,173 81%

$700,000

15.0%

$600,000

10.0%

$500,000

5.0%

$400,000

0.0%

$300,000

$861,794

-5.0%

$200,000 Annual Change %

Quarterly Change %

-10.0%

$100,000 2005 2008 2011 2014 2017 2020

$0

2005 2008 2011 2014 2017 2020 Quarterly Change % Annual Change %

The wider Wellington property market has been part of the boom in the past few months, with growth in average values

since September ranging from 7-8% in Upper Hutt, Carterton, Lower Hutt, Wellington City, and Kapiti Coast, up to a

rampant 14.2% in South Wairarapa and 17.4% in Masterton.

On an annual basis, growth has been at least 20% in Masterton, South Wairarapa, and Porirua, but also in double digits in

every other area of the region too. Wellington City has the highest level for property values, with the higher starting point

potentially contributing to slightly lower growth (but still strong at 13.4% annually).

DECEMBER 2020

Current value 1 month 3 month 12 months 5 years

Porirua $788,104 4.6% 10.9% 20.8% 98%

Upper Hutt $707,138 2.3% 6.9% 17.2% 104%

Lower Hutt $750,542 3.8% 7.7% 17.2% 93%

Wellington City $970,669 2.8% 7.9% 13.4% 70%

Carterton $533,796 3.2% 7.4% 18.0% 101%

Masterton $519,437 6.8% 17.4% 29.6% 113%

South Wairarapa $694,312 4.3% 14.2% 26.7% 119%

Kapiti Coast $746,081 4.7% 8.4% 18.3% 91%

35Christchurch Market Activity

Buyer Classification – Christchurch Buyer Classification – Canterbury

(% of purchases) region (% of purchases)

40%40% First Home Buyer

New40%to Market First Home Buye

Multiple Property Owner Cash Multiple Property

Multiple Property Owner Mortgage Multiple Property

New to Market

33% Mover 40%

Mover

33% ReEntry 37% ReEntry

30%30% Other

28% 31% 30% 30%

Other

35%

27% 27%

24% 30% 27%

25% 25%

23%

23%

22%

22%

20%20%

19% 20% 22% 22%

16% 20% 18% 19%

15% 14%

13% 15% 13%

16%

10% 13%

10% 10%

6%

8% 10% 10%

4% 5% 6% 6%

4%

3%

5% 4% 6%

4%

5%

5%

5%

5% 5%

4% 2% 3% 1%

0% 0% 1% 3% 1%

0%

0%

2005

2006 2008

2008

20102011 2012 2014

2014

2016

2017

2018 20202020 2003 2006 2009 2012 2015 2018 2021

2003 2006 2009 2012 2015 2018 2021

Mover Multiple property owner mortgage Mover Multiple property owner mortgage

First home buyer Multiple property owner cash First home buyer Multiple property owner cash

New to market ReEntry Other New to market ReEntry Other

Christchurch is seeing very similar Buyer Classification trends to the other main centres, with first home

buyers and mortgaged investors active (and rising), but movers quiet.

Indeed, the market share for FHBs was pretty steady at 28% in Q4 2020, in line with past highs. Meanwhile,

the share of purchases going to mortgaged investors continued to rise in Q4, and now stands at 27% – up

from 21% a couple of years ago and the highest figure since Q3 2016. Movers’ market share in Christchurch

was just 22% in Q4, a low only matched once before (in Q4 2013).

Around the wider Canterbury region, movers play a bigger role than in Christchurch itself, such as in

Ashburton where movers were 34% of activity in 2020 (albeit down from 38% in 2019). In Waimakariri, movers’

share was even higher last year, at 44% (up from 41% in 2019), while Selwyn’s figure was 40% (up from 35% in

2019). To some degree, the high share for movers in Selwyn will reflect existing owners (either from Selwyn or

other parts of Canterbury) seeking out a new-build.

36You can also read