Residential Developer Market Intelligence

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Residential Developer

Market Intelligence

MAJOR RESEARCH PARTNER

Q1 –2019

Welcome to the Q1-2019 edition of the UDIA NSW Residential Developer Market Intelligence (RDMI)

report. The quarterly RDMI aims to provide a targeted residential market performance update across

the Greater Sydney, Lower Hunter, Central Coast, Illawarra and ACT housing markets.

This publication is prepared with the understanding that residential property market dynamics are

complex and nuanced, and thus quality, timely market intelligence is essential for market participants

supplying new products.

The publication draws upon a range of information sources including exclusive and bespoke data

provided by CoreLogic - our key research partner. A key feature of the RDMI report is the inclusion of

‘bottom-up’ insights provided by our leading developer members on the state-of-play in their regional

market of operational focus.

The RDMI reporting output and content inclusions continues to evolve, and in this edition we

are pleased to present a new dashboard headline indicators section - in the opposing page. This

dashboard highlights the continuation of challenging market conditions facing the development

sector as the property downturn continues to unfold across the State.

UDIA NSW expects the subdued demand profile for new residential products to persist for at least

the next six months and most likely into the 2020 calendar year. Underpinned by a ‘credit crunch’ for

both retail consumers and developers in the wake of the Banking Royal Commission, we expect the

soft market conditions to continue to put downward pressure on pricing and sales volumes over the

coming period.

I trust the data and insights in this RDMI are of value for you and your organisation, and would

welcome any feedback or thoughts about the publication emailed to tadams@udiansw.com.au

Toby Adams

General Manager – Strategy & Research

UDIA NSW

Cover Image: No. 1 Lacey by Cornerstone Property

Research Partners Gold Sponsors Silver Sponsors

Market Performance Headline Metrics

Median House Volume of House Median Unit Sale Volume of Unit Change in Approvals

Sale Price (set- Sales (settled) Price (settled) Sales (settled) (12 months to Feb 2018

tled) (3-month (3-month change) (3-month change) (3-month change) vs 12 months Feb 2019)

change)

Greater

Sydney -1.6% -6.3% -0.2% -1.4% -17%

Central -1.5% -7.6% -0.9% -4.2% 26%

Coast

Lower -0.3% -6.2% -1.1% -8.4% -15%

Hunter

Illawarra -1.3% -6.2% -0.5% -4.5% 12%

ACT 1.2% -3.2% -0.2% -1.4% 60%

Economic Cash Rate and Average Lending Rates

Snapshot

• The latest ABS statistics to Septmber 2018 show

a 34% drop in the natural population increase

from the previous quarter. The strong population

growth in NSW remains bolstered primarily by net

overseas migration. In Q3-2018, NSW experienced

a net increase of 35,500 people which was 39% of

the total net Australian population increase for the

quarter.

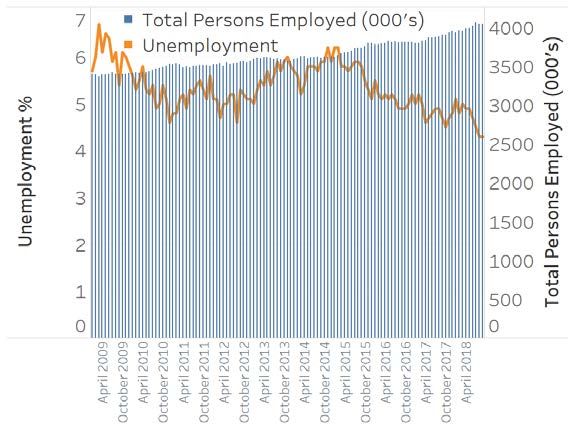

• In February 2019, NSW’s unemployment rate was

4.3% which is significantly lower than the national

average. This is below even the low national average

of 5%, with total employment growing in NSW by

2.3% over the preceding 12 months.

Source: RBA

• The official cash rate has remained steady at 1.5%

for 31 months now since August 2016.

• Consumer sentiment across the two major indices

fell slightly to start the year (4.4%, ANZ Roy-Morgan;

5.3% Westpac-Melbourne Institute)

Consumer Price Index (CPI)

Population Growth (NSW)

Source: ABS

Source: ABS

NSW Employment/Unemployment Consumer Sentiment

(Seasonally Adjusted)

Source: ABS

Source: Roy Morgan

National Housing Affordability Ratio (National)

Housing Snapshot 7.5

7.0

• The total volume of residential dwelling approvals

Dwelling Price to Income Ratio

continues to decline in most capital cities. In the year 6.5

to February 2019, the Sydney approval pipeline has

contracted by 17% and Melbourne’s by 13%. 6.0

• First home buyers accounted for 18% of national

house sales in January 2019, a proportion that has

been largely maintained since October 2017. 5.5

• The national housing affordability ratio for detached

dwellings (x7.8) and multi-units (x6.4) has improved 5.0

marginally in recent months on the back of falling Detached

pricing in Sydney and Melbourne. 4.5

Multi-unit

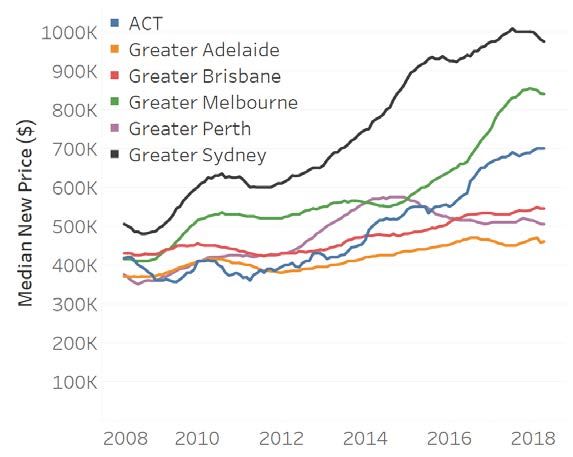

• The median sale price for new units in Sydney in

December 2018 was $735k, which was 24% higher

than Melbourne and 41% higher than Brisbane. 4.0

• The median sale price for new detached houses in

2

4

6

8

10

12

14

16

18

0

0

0

0

20

20

20

20

20

20

20

20

20

Sydney was $975k, down 3% from the March 2018

Source: CoreLogic

high.

First Home Buyers Australia, Proportion

and Loan Size Total Approvals 12 Months to Jan 2018

vs 12 Months to Jan 2019

Multi-unit

Detached

Dwellings

Source: ABS

Source: ABS

Median Unit Price (New): Capital Cities Median House Price (New): Capital Cities

Source: CoreLogic

Source: CoreLogic

Greater Residency Vacancy Rate (Sydney, Monthly)

Sydney

• Greater Sydney is continuing to feel the effects of the

current property downturn, with a decline in approvals,

the ongoing retraction of detached housing price, an

increase in the residential vacancy rate, and auction

stock and clearance levels falling short of early 2018

numbers.

• The approvals decline has been felt across the Greater

Sydney region, with every district experiencing

reduction in total approvals over the last year. The

Eastern City has recorded the greatest reduction with

total dwelling approvals contracting by 34%. This

was followed by the South District (which contracted Source: REINSW

by 30%) and the Western City (which contracted by

15%).

• Median whole-of-market house price in Greater Total Approvals (Sydney, Monthly)

Sydney has fallen by 1.6% in the last 3 months, and

the volume of house sales has fallen by 6.3%. New

detached house price has fallen by 1.5% in the last 3

months.

• Median whole-of-market unit price has contracted by

0.2%, with the volume of unit sales down 1.4% over the

last 3 months. New unit price has increased by 0.3%.

Change in New House and New Unit Price

(Rolling 3 month Average) (Sydney)

Source: ABS

Approvals by District 12 months to Jan 2018

vs 12 months to Jan 2019

Source: CoreLogic

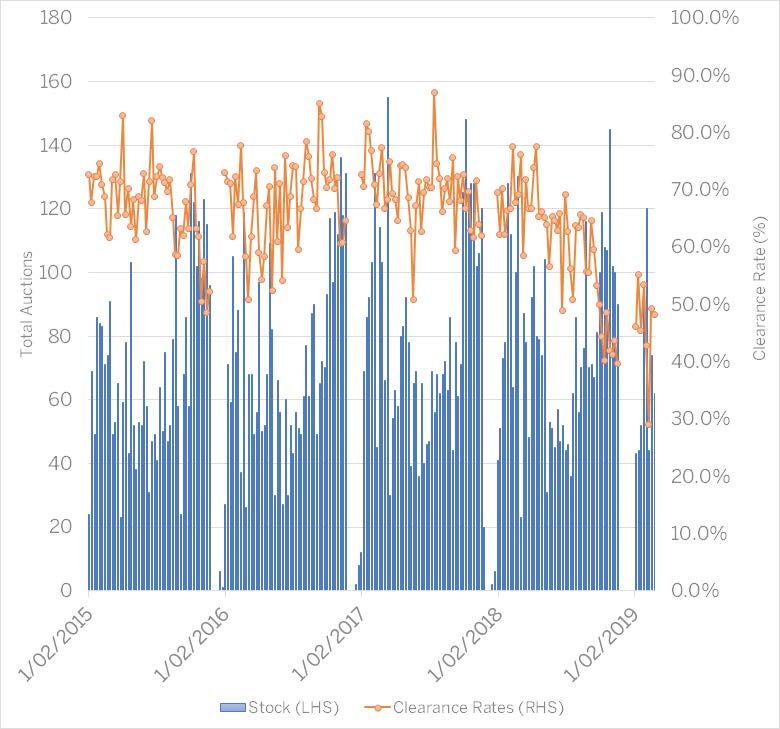

Weekly Auction Clearance Rates (Sydney)

Source: ABS

Source: CoreLogic

Greater Median Sale Price by Quartile, Houses,

Sydney Greater Sydney (12 months to Jan 2019)

Upper

Apartment Supply Snapshot Quartile:

$1,500,000

Current Twelve Month

Upper

Change

Quart

Median:

$950,9

Total Apartment Completions (Cal. Year) 33,270 16% $950,000

Media

Lower $720,0

Quartile: Lower

Total Apartment Yield Under Construction 41,975 55% $690,000 Quart

$572,0

Total Apartment Yields Approved 65,647 -26%

$0 $0

Median Sale Price of New Units $720,000 -1.3%

Jan 2019 Source: CoreLogic

Vacancy Rate (Residential) 3.2% 2.3%

(Feb 2019) (Feb 2018)

$540 -0.9%

Median Asking Rent (Residential)

Median Sale Price by Quartile, Units,

Upper Sydney (12 months to Jan 2019)

Greater

Median Rental Yield

3.9% N/A Quartile:

$1,500,000

Source: CoreLogic Upper

Quartile:

Median Days on Market, Selected LGAs (12 months to Jan 2019) Median:

$950,950

$950,000

Median:

Lower $720,000

Quartile: Lower

$690,000 Quartile:

$572,000

$0 $0

Source: CoreLogic

Source: CoreLogic

Developer Insight

“There is no doubt that negative sentiment combined with lending policies

is having a significant impact across Sydney’s market. Sales activity has

decreased with most buyers preferring to wait on the sidelines. There is some

settlement risk to work through in 2019, particularly in lower quality areas with

localised over-supply. On the positive side, we are seeing increased first home

buyer activity spurred by improved affordability while the fundamentals of

population growth and economic activity remain strong. The re-election of the

State Liberal government will provide policy continuity to underpin industry

investment, however housing approvals have fallen sharply suggesting that

Sydney’s housing supply targets will not be met in coming years. We expect to

see a period of undersupply that will coincide with an improvement in market

conditions. ”

Mike Williams – Head of Strategy & Acquisitions, Legacy Property

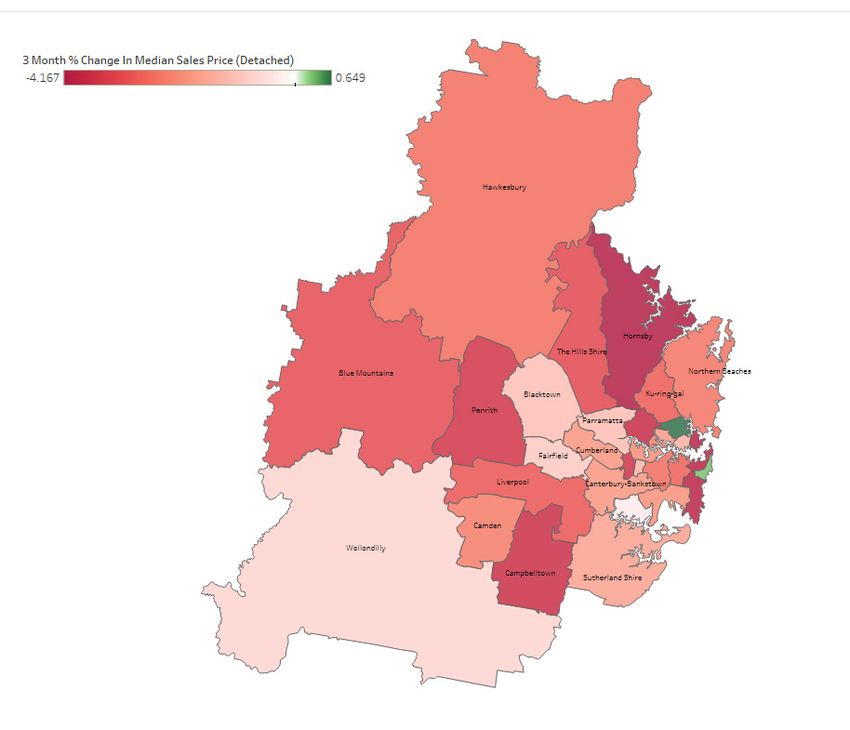

Greater Sydney (Detached)

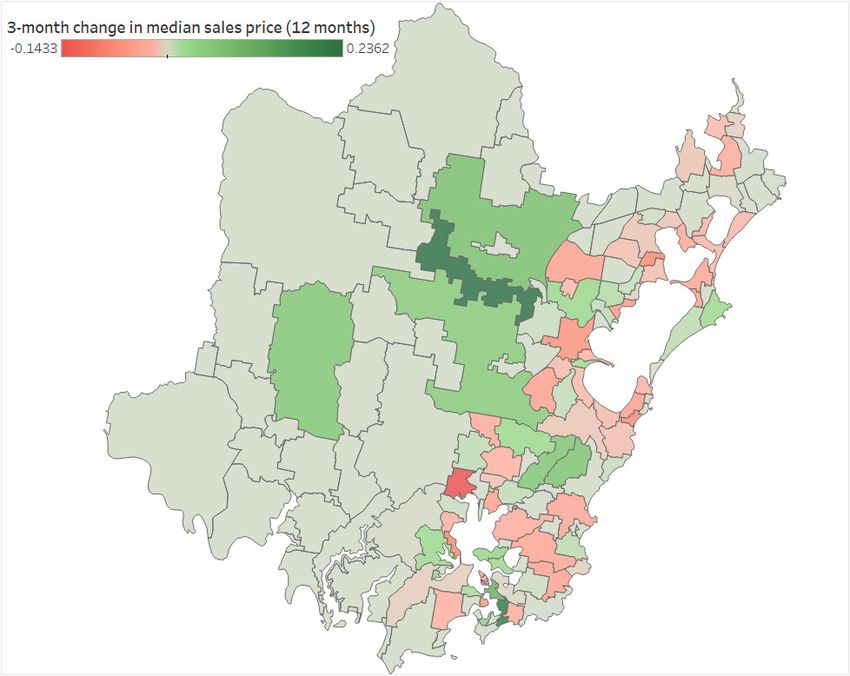

LGA 3 Month % Change in Median Sales Price

(Whole of Market, as at 31/01/2019)

% %

0%

1 14

15 1. Ryde

16 13 12

2 2. Canada Bay

3. Strathfield

3 4 11 4. Burwood

5 8 10 5. Inner West

9 6. Georges River

7 7. Bayside

6 8. Sydney

9. Randwick

10. Waverly

11. Woolhara

12. Mosman

13. North Sydney

14. Willoughby

15. Lane Cove

16. Hunters Hill

Source: CoreLogic

Spotlight on South District: LGA Market Update

Source: CoreLogic

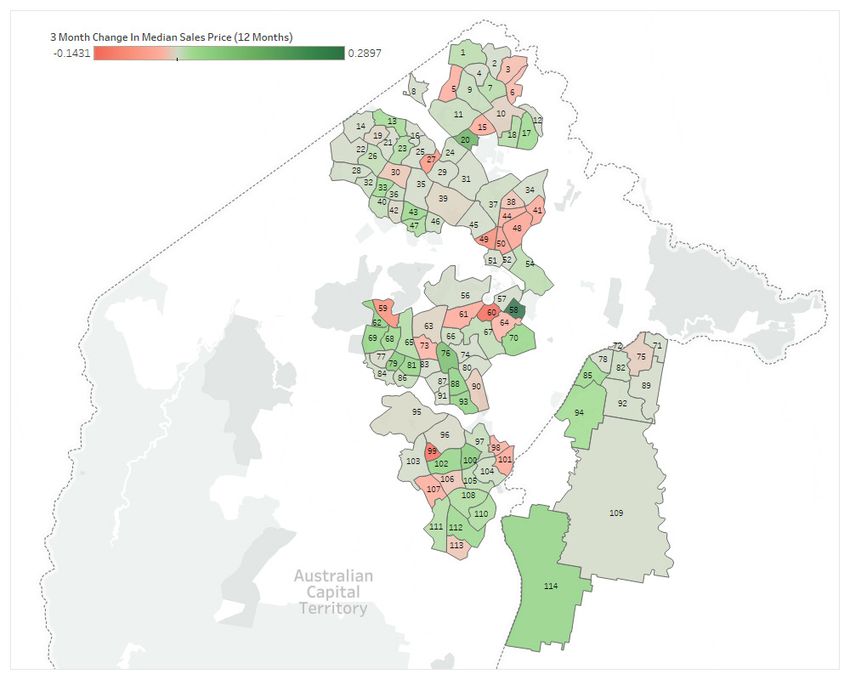

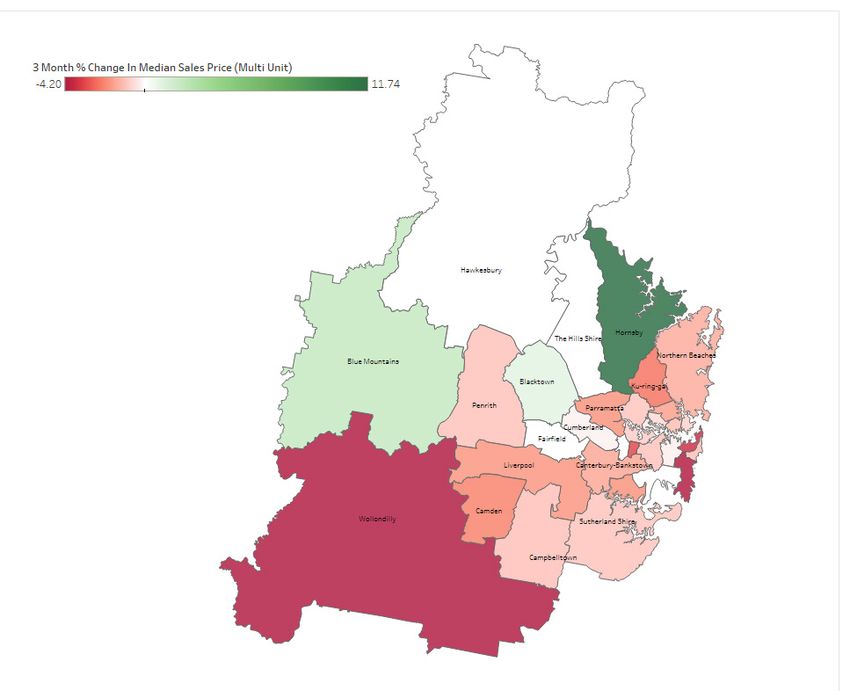

Greater Sydney (Multi Unit)

3 Month % Change in Median Sales Price

(Whole of Market, as at 31/01/2019)

% %

0%

1 14

15

16 13 12 1. Ryde

2 2. Canada Bay

3. Strathfield

3 4 11 4. Burwood

5 8 10

5. Inner West

9 6. Georges River

7 7. Bayside

6 8. Sydney

9. Randwick

10. Waverly

11. Woolhara

12. Mosman

13. North Sydney

14. Willoughby

15. Lane Cove

16. Hunters Hill

Source: CoreLogic

Spotlight on North District: LGA Market Update

Source: CoreLogic

Central Approvals (Central Coast, Monthly)

Coast

• Approvals in the Central Coast have dropped off in

recent months, with rolling annual dwelling approvals

falling 5% over the 3 months to February 2019.

• The price of new houses and units has remained

relatively flat in the 3 months to January 2019, with

the median new house price falling by 2% and the

median unit price remaining at $585k.

• Whole of market house and unit prices were similarly

stable, despite sales volumes beginning to decline.

The volume of house sales was down 7.6% in the

3 months to January 2019, while unit sale volumes Source: ABS

were down 4.2%. Approvals (Central Coast) by Dwelling Type,

• The suburbs with the greatest 3-month movement

in median house price were Wyong Creek (23.6% 12 Months to Feb 2018 vs 12 Months to Feb 2019

increase), Kilcare (21.4% increase) and West

Gosford (14.3% decrease). The greatest 3-month

movements in unit prices were in Wamberal (13.4%

increase), Booker Bay (13.3% decrease) and Toukley

(6% decrease).

Median New House and Unit Price

(Central Coast, Monthly)

Source: ABS

Completions (Central Coast, Monthly)

Source: CoreLogic

Vacancy Rates (Central Coast, Monthly) Source: NSW DPE

Weekly Rents (Central Coast, Jan 2019)

Median 12 Month Rental

Asking Change in Yield

Rent Asking Rent

Houses $450 0.0% 3.6%

Multi-Unit $390 2.6% 4.1%

Source: CoreLogic

Source: REINSWCentral Coast 3 Month % Change in Median Sales Price

(Whole of Market, as at 31/01/2019)

15%

% %

24%

0%

Source: CoreLogic

Central Coast Update as at 31/01/2019

Source: CoreLogicLower Approvals (Greater Newcastle, Monthly)

Hunter

• Lower Hunter approvals are also in decline, falling

16% in the 3 months to February 2019.

• New house and unit prices are starting to show signs

of contraction. House prices in Newcastle and Lake

Macquarie fell by 1%, while the rest of the Hunter

had no change. Unit prices across the Hunter fell

by 2%. Established house prices were stable, while

established unit prices dropped by 1%.

• Sales volumes have begun to decline in the Lower

Hunter, with house sales down 6.2% and unit sales

down 8.4%.

• The suburbs with the greatest 3-month movement Source: ABS

in median house price were Croudace Bay (20.9%

increase), Holmesville (13.7% increase) and Salt Ash Approvals by LGA Jan 2018 vs Jan 2019

(13.4% increase). Those with the greatest 3-month

movement in median unit price were Hamilton

(22.9% increase), the Junction (19.9% decrease)

and Edgeworth (14.7% decrease).

Median New House and Unit Price

(Hunter, Monthly)

Source: NSW DPE, ABS

Source: CoreLogic Weekly Rents (Newcastle LGAs, Jan 2019)

Median 12 Month Rental

Residency Vacancy Rates (Hunter, Monthly) Asking Change in Yield

Rent Asking Rent

$370 5.7% 4.8%

Cessnock $290 0.0% 5.6%

$430 2.4% 4.1%

Lake Macquarie $370 2.8% 4.6%

$410 2.5% 4.5%

Maitland $320 10.3% 5.3%

$450 4.7% 3.7%

Newcastle $405 2.5% 4.0%

$430 2.4% 4.2%

Port Stephens $350 6.1% 4.4%

Source: CoreLogic

Source: REINSWLower Hunter

Local Government Area (LGA) 3 Month Change in Median Sales Price

(Whole of Market, as at 31/01/2019)

Maitland City

↑ 0.0% Port Stephens

↓ 1.4% ↓ 0.9%

↓ 2.9%

Cessnock

↑ 0.1%

↑ 0.0%

Lake Macquarie Newcastle

0.0% ↓ 0.8%

0.0% ↓ 1.0%

Source: CoreLogic

LGA Market Update as at 31/01/2019

Source: CoreLogic

Developer Insight

“While demand for product in the Newcastle region has reduced slightly off a strong base

in line with the overall slowdown in investor lending, quality well-priced properties remain

attractive and Newcastle represents a value proposition within a dynamic labour market. The

overall Newcastle fundamentals remain sound.”

Suzanne Pitson – General Manager of Sales and Marketing, DHAApprovals (Illawarra, Quarterly)

Illawarra

• Dwelling approvals in the Illawarra have started

to slow, increasing by just 3% in the 3 months to

February 2019.

• New house and unit prices have remained flat over

the last 3 months, with the median new house

price falling just 0.5%. The established market

fared slightly less well, with the median house price

dropping 1.3% and the median unit price falling

0.5%.

• Sales volumes are starting to decline, with house

sales down 6% and unit sales down 4.5%.

• The suburbs that experienced the greatest

movement in median house price over the 3

months to January 2019 were Bawley Point (15.4%

increase), Minnamurra (15% decrease) and Dolphin Source: NSW DPE, ABS

Point (14.2% decrease). The suburbs with greatest

3-month movement in median unit price included

Coniston (15.1% increase), West Wollongong (11.7% Approvals by LGA, 12 Months to Feb 2018

increase) and Gerringong (7.8% decrease). vs 12 Months to Feb 2019

Median New House and Unit Price

(Illawarra, Monthly)

Source: CoreLogic Source: NSW DPE, ABS

Residency Vacancy Rates (Illawarra, Monthly)

Weekly Rents (Illawarra LGAs, Jan 2019)

Median 12 Month Rental

Asking Change in Yield

Rent Asking Rent

$580 3.6% 3.3%

Kiama $470 4.4% 4.0%

$500 0.0% 4.0%

Shellharbour $420 5.0% 4.2%

$395 3.9% 3.7%

Shoalhaven $330 0.0% 4.1%

$510 2.0% 3.5%

Wollongong $400 0.0% 3.5%

Source: REINSW

Source: CoreLogicIllawarra

Local Government Area (LGA) 3 Month Change in Median Sales Price

(Whole of Market, as at 31/01/2019)

Wollongong

Kiama

↓ 1.3%

↓ 3.2% ↓ 0.5%

↓ 0.4%

Shellharbour

0.0%

↓ 1.0%

Shoalhaven

↓ 0.7%

0.0%

Source: CoreLogic

LGA Market Update as at 31/01/2019

Source: CoreLogic

Developer Insight

“Sale prices have been flat or marginally lower over the last quarter, coming

off a high base. In general, prices in the region have fared slightly better than

Sydney, although there has been significant growth in listings for units over

the last year. Demand for greenfield and detached housing products remain

strong, buoyed by strong employment and population growth. However, we

continue to see some potential buyers struggling with financing as a result

of the changes at the major lenders. We need to continue releasing a steady

supply of serviced land in the urban release areas to keep prices affordable, as

well as pushing for caps on developer taxes and charges in the face of lower

sale prices.”

Alby Peros – Development Manager, StocklandACT & Approvals (New, ACT, by Dwelling Type) 12

Months to Feb 2018 vs 12 Months to Feb 2019

Queanbeyan

• Approvals in the ACT & Queanbeyan have also

slowed, increasing by just 1% in the 3 months to

February 2019.

• The median house price in the ACT has increased

by 1.2% to $658k, while unit prices remained flat at

$426k.

• Sales volumes have fallen slightly over the last 3

months, with house sales down 3.2% and unit sales

down 1.4%.

• The suburbs with the most significant 3-month

movement in median house price were Kingston

(29% increase), Forrest (14.3% decrease) and Oxley

(14% decrease). Those with the greatest 3-month

movement in median unit price were Chifley (26.2%

increase), Barton (23% increase) and Weston

(21.8% increase). Source: ABS

Weekly Auction Clearance Rates (ACT)

Approvals (New, Queanbeyan, by Dwelling

Type) 12 Months to Feb 2018

vs 12 Months to Feb 2019)

Source: ABS

Completions (ACT, Quarterly)

Source: CoreLogic

Approvals (ACT & Queanbeyan, Monthly)

Source: ABS

Source: ABSACT & Queanbeyan

3 Month Change in Median Sales Price (Houses), as at 31/01/2019

15%

% 29%%

0%

ACT

Queanbeyan Urban

(NSW)

Source: CoreLogic

LGA Market Update as at 31/01/2019

Source: CoreLogicNational Property Clock

Adapted from Herron Todd White, Month in Review

April 2019

Dubbo

Mid North Coast

HOUSES

Hobart Canberra

Sunshine Coast Central Coast

Illawarra

Adelaide

Melbourne

Albury

Newcastle

Launceston

Sydney

Brisbane Darwin

Cairns South West WA

Alice Springs

Perth

Rockhampton

Lismore

Mid North Coast

Hobart

Sunshine Coast

Central Coast

Coffs Harbour

Gold Coast

UNITS

Canberra Newcastle

Bathurst

Illawarra Perth

Dubbo

Melbourne Sydney

Brisbane

Adelaide

South West WA

Ipswich

Cairns Source: Herron Todd White,

Whitsunday Month in Review, April 2019ABOUT UDIA

THE URBAN DEVELOPMENT INSTITUTE

OF AUSTRALIA (UDIA) IS THE PEAK BODY

REPRESENTING THE URBAN DEVELOPMENT

INDUSTRY IN AUSTRALIA.

Officially established in 1963, UDIA NSW has grown to become the leading industry

body representing the interest of the NSW property development sector.

UDIA NSW aims to secure the viability and sustainability of the urban development

industry for the benefit of our members and the communities they create by

advocating for more liveable, affordable and connected cities.

We represent the leading participants in the industry and have more than 500

member companies across the entire spectrum of the industry including developers,

institutional investors, third party logistics providers, financiers, builders, suppliers,

architects, engineers, lawyers, town planners, academics and state and local

government bodies. A quarter of these members are based in regional NSW.

UDIA NSW members are represented by an elected council of 13 leading industry

practitioners who are responsible for the strategic direction of the Institute. UDIA

NSW also has an extensive committee and regional chapter structure that involves

more than 300 of the development industry’s key stakeholders in policy formulation.

UDIA NSW OFFICE

UDIA NEW SOUTH WALES

02 9262 1214

LEVEL 5, 56 CLARENCE ST.

SYDNEY, NSW 2000

www.udiansw.com.au

udia@udiansw.com.auImage: Wivenhoe Village by Mbark

Research Partners Gold Sponsors Silver SponsorsYou can also read