RETAILER DISTRIBUTION IN SOUTHERN COUNTRIES AND IN MOROCCO - 1st REGIONAL TRAINING LACTIMED - ANIMA Investment Network

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

RETAILER DISTRIBUTION IN SOUTHERN

COUNTRIES AND IN MOROCCO

Prof. Abdelaziz SBAÏ,

Institut Agronomique et Vétérinaire Hassan II,

Morocco

1st REGIONAL TRAINING LACTIMED

BIZERTA, TUNISIA, 2-3 APRIL 2014

Brainstrorming exercise

Considering you own experiences in your country, discuss the following subjects:

1-) Does the implementation of the supermarkets have an impact on the traditional

systems? If so, in which sense?

2-) What are in your opinion the factors that have contributed to the acceleration of

the retailers phenomenon?

3-) In your own experience of small and medium producer, do you think that the large

distribution is inclusive of your category of producer?

If not, why?

If so, what is your real degree of negotiation with them?

4-) If you are a retailer provider, do you think that the specifications between retailers

and providers are equitable?

5-) Does the retail sector have an impact on the value and promotion of the local

products?

6-) In what sense traditional channels and informal distribution are not fully adapted to

your products?

7-) As a consumer, how do you rate the retailers implementation (hyper and

supermarkets) on your way of life?

8-) Do you think that the convenience stores will disappear in the long term?

9-) Are you aware of successful results between the benefits of the hyper and

supermarkets and the benefits of the convenience stores?

10-) Do you agree that retailers must stay in the medium-sized cities? Or only in big

metropolis?

Overview of the situation of retailer distribution in Morocco

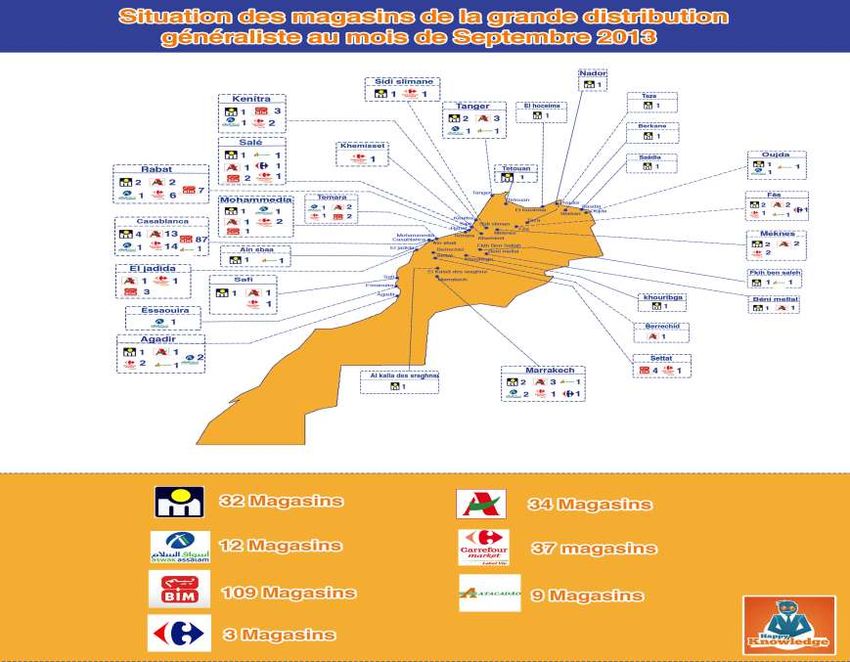

the market sector reprensents 13 % of GDP, about 3 % of volume des IDE and the income of 13% of the working population (1,5 Milllions of people) The modern distribution realizes in terms of turnover 16 Billions of Dirhams it is 1,4 bilions of euros, what represents 13 % of retail market, croit de 9 % par an 106 stores in 2010 and an objectif of 600 for 2020 Industry concentration (oligopoly position) with the predominance of Marjane and important imbalance in terms of territorial coverage: 43% of the total area of the retailers distribution is focused on the Atlantic axis: Casablanca / Mohammedia / Rabat / Kenitra

Geographical distribution of the Hyper&Super

Markets, by number (2010)

Competition Council 2011

Distribution of the stores by brands and city (2010) Competition Council 2011

Competition Council 2011

Competition Council 2011

Banned in France and in

some countries

Competition Council 2011Evolution of the hyper and supermarkets

creation

Evolution of hyper and supermarket openings

Competition Council 20113 main growth phases in the development of the retailer distribution. Before 2002: with an average of less than 3 stores / year created. Between 2002 and 2006 : between 7 and 10 new stores / year. After 2007: with an average of 12 openings /year. Consumption pattern drawn by the wealthy class and followed by the middle class.

2 main groups share 92 % of the market (4 brands: Metro, Label Vie,

Marjane and Acima). Asswaq Salam is an outsider with 8 % of the

market. BIM is new arrived and announced in 2012 the opening of

50 news points of sales, to be added to the 76 that already has.

Competition Council 2011Evolution of the implementation strategies of the

brands

Competition Council 2011- In emerging countries, the modernisation of the distribution system is launched by the wealthy calsses and disseminate by middle classes. - Massive establishment of new foreign distribution formats that are added grafted to the national commercial context. - Risks and limitations of the establishment in the SD countries: country risk, significance of local purchasing power, degree of urbanization and development perspective … - Strategies of the major groups in different regions (PVD): privilégient les pays émergents à forte population urbaine, ayant une faible densité du commerce moderne et avec une classe moyenne importante

Global Index Retail Development (GRDI), an study of the AT Kearney counsulting firm in order to help companies to prioritize their international expansion strategy. ranking of countries according to their market potential (market attractiveness), the levels of economic and political risks, the level of commercial equipment and competitive intensity (saturation of the market) and the speed in which the economy grows (time pressure) The top ten countries in 2012 are: Brazil, Chilli, china, Uruguay, Inde, Georgia, United Arab Emirates, Oman, lMongolia and Peru «Concerning Middle East and North Africa, il faut remarquer la récupération face à la récession et une plus grande confiance des consommateurs dans la plupart des pays avec une croissance du PIB entre 3% et 5%, avec un niveau de revenu relativement élevé, une population jeune et une classe moyenne qui n’arrête pas de grandir. The regional potential is shown on its ranking: Koweit (5), Saudi Arabia (7), United Arab Emirates (9), and not to forget Turkey (10), Lebanon (12) and Morocco (17). Concerning these ones, Turkey is the country with the higest evolution, 6 places won thanks to its strong sconomic growth.».

The internationalization of the retailer distribution face to crisis, by the A.T.Kearney firm (2012) « economic stagnation of the markets in developed countries, combined with the attractiveness of emerging economies, makes that the internationalization be essential in the maintain of the growth levels. On the other hand, he also stressed the need to analyse the international expansion from a multichannel perspective (physical store, e-commerce and m-commerce), even in less developed markets, as well as the importance of attracting local talent to organizations » «Economic and political tensions can speed up or slow down some decisions, but the general trend is that globalization will continue. In any case, more than focus attention on particular regions or countries, what is need is to build a portfolio of markets in order to establish a balance between short-term risk and long-term growth aspirations»

Driven by the rise of Brazil, Chile (2nd) and Uruguay (3rd) confirm their attraction for the third consecutive year thanks to strong growth (around 10%) of disposable income and low inflation. More generally, Latin America continued its extraordinary dynamism, with seven countries represented in the Top 30. The shopping centers play a key role in the structuring of these markets like the new Village Mall in Rio de Janeiro and JK Iguatemi Sao Paulo, or the Costanera Chile. In particular, they attract large luxury industry players such as Valentino, Miuccia Prada, Sephora, Gucci, Lanvin or Van Cleef & Arples. Political instability in the Maghreb countries continue to have different consequences in the countries of the MENA region. If the Arab revolutions have impacted negatively many countries such as Tunisia, which comes out of the rankings this year, after Egypt in 2012, other countries are doing better (Morocco, Saudi Arabia, Oman, Jordania) and have increase their attractiveness like the United Arab Emirates (+2 places) and Koweit (+3 places).

Reasons Markets with needs to be cover, attractive economic and fiscal policies (lower toll fees, implementation assistance) Investment in transport infrastructure, etc. Saturation (near) of the European or North American domestic markets with a low development potential Specific legal constraints in some developed countries restricting new store openings Absence of a regulatory framework laying down the rules of business activity (delimitation of retail space, schedules, etc.)

Lack of access to other developed markets due to the presence of strong local competitors and a strong commercial density, Potentiel de développement qu’offrent les pays émergents en tant que levier de croissance externe Adhesion and permeability of a growing portion of consumers in emerging countries to these new distribution concepts

- However, these countries cover a variety of realities, from rapid and large opening to the modernization of distribution and private investments (Brazil) to a slow and measured opening (India)

Anticipatory Policies EX. Fragmented market Ex Emerging market Ex Mature market Consolidated market Pakistan Vietnam South Africa W. Europe Key factors: Key factors: Supermarkets Supermarkets dominant dominant sales > 45%; few sales > 65%; few traditional traditional traditional wet traditional wet markets, markets, markets market markets, high markets modernisation level of markets modernisation degree > 10% modernisation degree > 5% •“Politiques institutionnelles peu averties sur le LT” •“Or si on comprend cette évolution, on peut choisir les mesures appropriées pour guider les orientations futures

Development and specificities of modern distribution

in Southern countries- Fragmented traditional distribution system - Opacity of its structure and legal vacuum in terms of distribution law, competition or planning - Socio-cultural changes in household lifestyles: time constraints, seeking comfort, well-being and quality of products, media and communication development, improving education and cultural, women’s employment, knowing the modern distribution system thanks to travels and satellite channels, etc.

- macroeconomic and tax measures facilitating the implementation of modern distribution - Overlapping distribution formats rather than sequential development of the classic life cycle distribution formats - In emerging countries, local consumers are joining quickly the modern distribution system - Strongher local and international competition, meaning quickly saturation for modern commerce - Coexistence of multiple retail systems (duality)

The conditions of the evolution: does all depend on the evolution of the GDP?

Evolution du PIB par tête et de la distribution au M aroc

20

15

10

5

0

1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

GDP / capita (MAD)

Retail sales / capita (MAD)

Grocery retail sales / capita ( MAD)

Modern grocery distribution, total sales / capita (MAD)Effect of the traditional distribution in southern

countries- Two functions (distribution and social) integrated into each other - The convenience store was able to resist the development of modern commerce (which, in fact, was not able to attract the great mass of low income consumers) compared to its European counterpart or French - Le commerce moderne bute sur cette contrainte malgré son développement dans les quartiers urbains (ex Acima in Morocco, Label Vie, etc.)

Developement perspectives of the hyper and

supermarkets in southern countriesComparing the contexts and distribution systems in

mature and emerging marketsSource : Amine, Dupuis, Obadia and Prime (2005)

Expansion and braking factors of the modern

distribution in transition marketsFacteurs de développement de la GD Facteurs freinant le développement de la

dans les pays du Sud GD dans les pays du Sud

- Accroissement de la densité de la population et - Difficultés d’adaptation de la distribution moderne à certaines

développement de la classe moyenne habitudes culturelles de consommation : vente à crédit,

- CM répond à un volume croissant de la demande et permet de horaires d’ouverture et de fermeture, faible prise en charge de

faire face aux problèmes de faiblesse de la taille des points de la clientèle peu instruite ou analphabète dans le magasin

vente du commerce traditionnel, d’incapacité à gérer livrée à elle même

rapidement de grands flux de consommateurs, du coût - concurrence du secteur informel

croissant du travail et du manque de contrôle de la fidélité des - faible croissance de la classe moyenne cantonnant la

employés localisation de la GD dans les grands centres urbains

- Existence d’attentes non comblées par l’offre traditionnelle - Commerce traditionnel de proximité répond à des attentes et

locale (diversité en quantité et qualité/hygiène…) facilitant des demandes sociales et culturelles que la distribution

l’adhésion d’une partie des consommateurs aux formats de la moderne ne réussit pas encore à combler

distribution moderne - faible pouvoir d’achat d’une part significative des ménages ;

- Besoins et comportements de consommation en évolution en - Insuffisance des moyens de transport individuels et/ou

raison de l'accès quasi-généralisé de la population aux chaînes collectifs pour accéder sans contraintes aux nouveaux temples

satellitaires et à la diffusion des médias internationaux de la consommation à la périphérie des villes ;

diffusant les valeurs du modèle culturel occidental de - forte concurrence sur certaines catégories de produits sur

consommation lesquelles les GMS ne sont pas compétitives par rapport au

- Faible densité de l’appareil de distribution marché parallèle (habillement, produits d’hygiène et

- Apparition d’une classe moyenne significative cosmétique, produits électroniques), aux marchés de plein air

- Main-d’œuvre bon marché (propice aux groupes de ou couverts (légumes et fruits frais), etc. ;

distribution étrangers) - cherté du foncier pour l’achat de terrains ou la location de

- Multiplication des filiales de sociétés multinationales surfaces en centre ville qui constitue un grand handicap à

installées dans les grandes villes des pays émergents et le l’extension de la grande distribution dans les pays émergents ;

gonflement du personnel expatrié - problèmes de risque de change (pénalisation en cas de

- Augmentation de la proportion des femmes actives dévaluation de la monnaie, augmentation brusque des taxes

douanières) pour les importations de produits, de denrées et

de matériels.The impact of modern distribution on market

system- Job creation – direct and indirect (subcontrators, suppliers) in a context of an important unemployment rate. - Restructuring the industrial sector offer, mainly composed by SMEs /SMIs, by respecting high quality standards; more rigor in the delivery and cost rationalization - Total revision of the supply chain to optimize transport, open platform for storage and distribution, ensuring non-breaking cold chain, increase inventory turns and improve product packaging - Large producers are avantaged because retailer distribution allows them greater regularity incomes and a higher sales rate as of network expansion. - Small producers harmed or excluded, can not work permanently with retailer distribution because of their lack of tecnical and monetary capacities.

- rebalancing of power in the channel for distributors profit - The rise of hyper and supermarkets began to question the hegemony of convenience stores in emerging countries because of its purchase and negotiation power and their capacity to attract customers. - Nevertheless, convenience stores are still an important actor on the distribution level. - At the international distribution level, this implementation comes with transfert of knowledge but also by adapting mais par touches et paliers d’adaptation au contact de la réalité du pays d’accueil (example Auchan/Marjane)

- Placing hypermarkets not only on the outskirts of the cities but also at the city centrum - This emplacement is competing with the convenience stores but changes are done in order to adapt the format and become more like a discount stablishment. - A readjustment of merchandising and improving the store atmosphere allowing low prices all the time («soft discount») = in order to adapt itselfs to the population expectations (including lower income classes) : ex. Russia and Morocco (see picture on next slide: Carrefour Maxi in Casablanca)

The new concept of warehouse – store of Carrefour Maxi

Relations between Retailers and suppliers in Morocco,

by the competition council (2011)- « it appears that the production of some essential food products (sugar, oil and dairy products) - highly concentrated in the domestic market – are responsible of critical situations in terms of competition. Indeed, some retailers, such as Marjane and Acima, may be tempted to gain a competitive advantage because of the fact of belonging to groups with major suppliers of these basic foods products». - « Unbalanced relationships between retailers and suppliers, as is known abroad. Indeed, it is often criticized to the supermarkets are often criticized because of their abusing position in front of their suppliers. Thus, the use of restrictive clauses for suppliers in commercial contracts is often criticized, especially in terms of prices, supply and logistic conditions. This imbalance affects particularly affects domestic firms, which are depending on the hyper and supermarket conditions to develop their business ».

- « the annual commercial contracts between suppliers and distributors may contain highly demanding clauses vis-à-vis suppliers, particularly in terms of performance conditions (retroactive application of the current fiscal year, settlement between 30 and 90 days) price practiced (guarantee of the lowest prices), back margins (invoicing of sales efforts provider), end-year rebates (unconditional discounts) and logistics and supply conditions (management of risk taken by the supplier) ». - « Suppliers highlight the severity of certain clauses and the difficulty of the negotiations. This position is more serious when the supplier’s turnover depends on the Supermarkets - even when this figure does not exceed 15% of its total revenue - to ensure the development of its brands».

Commercial contracts with hyper and

supermarkets

The access to retail distribution

- the regulation of the entrance fee is based on a percentage of the

turnover of the first year.

- With every new opening, extention or renovation of a store, a fee is

charged to the supplier.

- Tout référencement d’un article d’un fournisseur fait également

l’objet de droit de référencement.

- « The degree of these fees depend on the bargaining power of the

actors».Guarantee the lowest prices - Some clauses stipulate that if the distributor shows that price discrimination comming from a supplier does not allow him to offer a similar price than his direct competitors, the supplier must offer a lowest price, and this retroactively to the date on which the price discrimination was done. - Any increase in prices done by the supplier has to be justify, which if accepted will be effective after a period (usually one month) after the reception of the new price. - In terms of price reductions, financial compensation on the retailers stocks is made by providers

Logistic conditions - Retailers charge suppliers for logistics - Beyond a rate of non-delivery which depends on distributors and on products, usually between 8% and 15%, the entire revenue excluding taxes lost by the distributor will be reintegrated into the calculation of the trade agreements due by the supplier.

Suppliers are in charge of the promotion and communication tools - Suppliers undertake to pay distributors partially or totally of all the actions and efforts made by the distributors to accelerate sales. - Internal campaigns in store: competitive prices for customers, communication activities through flyers and poster campaigns, highlighting products on gondolas or through gifts to customers - Suppliers agree to grant to the distributor with a additional discount for all the promoting products during the promotion campaign - Agreements do not need a prealable acceptation by supplier of the terms and implementation of promotions times.

The rebates in commercial contracts - At the end of the year unconditionals (calculated on a basis of a percentage of the sales charged by the supplier to the distributor) - conditional (calculated on a basis of a percentage of the sales charged by the supplier to the distributor per completion). - The rebates degree depend on the product and on the bargain power of suppliers.

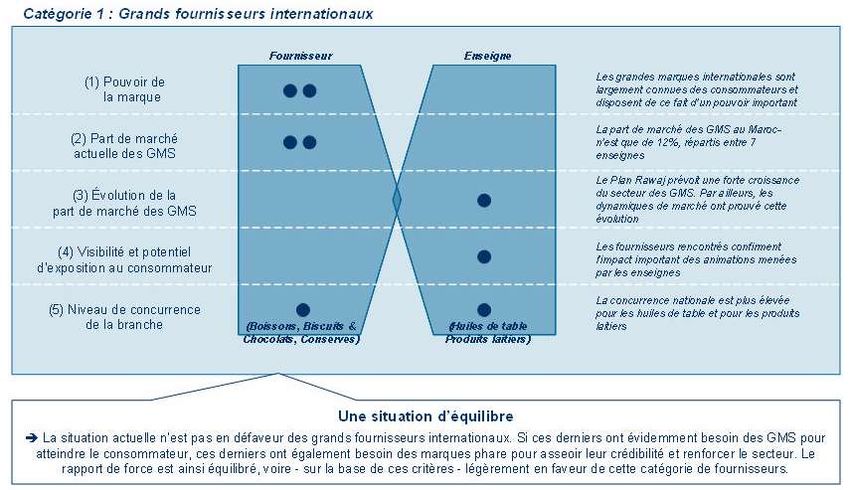

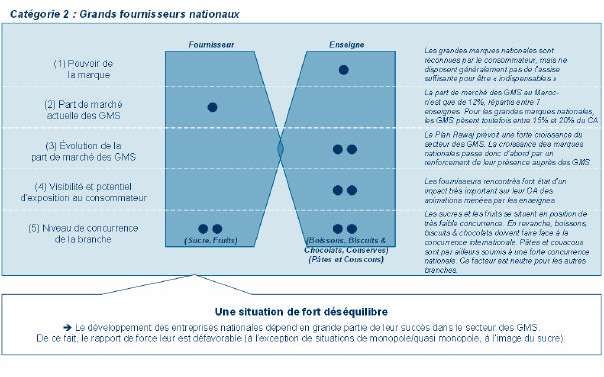

The bargaing power of the large international suppliers Balanced situation. The current situation is not unfavorable for large international suppliers. They need obviously the Hyper and Supermarkets to arrive to the consumer, but also, the large retailers need these brands to stablish their credibility and to strengthen the sector. The balance of power is well balanced, even on the basis of these criteria, slightly in favor of this category of suppliers.

The bargaing power of the small national suppliers

High unbalanced situation. The development of national companies depends

largely on their success in retailers sector. Thus the balance of power is

unfavorable except for monopoly / near-monopoly situation (ex. Sugar)

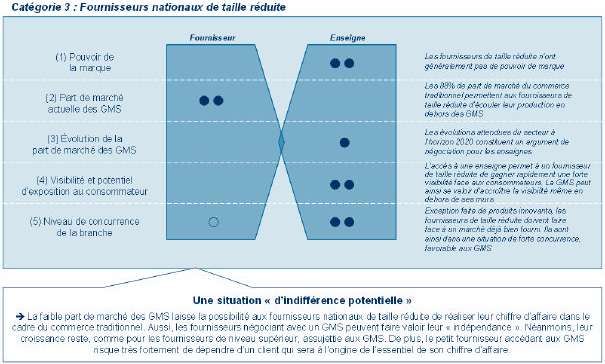

Conseil de la concurrence 2011The bargaing power of the small national suppliers Potential indifference situation. The low share of the market of the retail distribution gives the opportunity to small domestic suppliers to achieve their sales in the traditional trade. Thus, those suppliers who can negotiate with retailers can assert their independence. However, their growth still stays, as for top-level providers, subject to the supermarkets rules. In addition, the small supplier accessing to large retailers has the risk of depending on a single client that will be the main source of its turnover.

The impact of modern distribution on buyer’s

habits- changing the importance of the different criteria to choose stores and products - Confiance dans le format de vente et dans l’enseigne qui véhiculent une image moderne et dynamique valorisée par les clients/confiance dans le vendeur de proximité. - By sensorial dimensions (mixing lights, sounds, spaces and coulours) the fact of buying become an entertainment for families - Buying at hyper and supermarkets has become a social status reference - Socialisation by the consomption / strategies on wealthy classes

Competition Council 2011

You can also read