RULE DETERMINATION National Energy Retail Amendment (Preventing discounts on inflated energy rates) Rule 2018 - AEMC

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

RULE DETERMINATION National Energy Retail Amendment (Preventing discounts on inflated energy rates) Rule 2018 Rule Proponent The Honourable Josh Frydenberg MP, Minister for the Environment and Energy on behalf of the Australian Government 15 May 2018

Inquiries Australian Energy Market Commission PO Box A2449 Sydney South NSW 1235 E: aemc@aemc.gov.au T: (02) 8296 7800 F: (02) 8296 7899 Reference: RRC0012 Citation AEMC, Preventing discounts on inflated energy rates, final rule determination, 15 May 2018. About the AEMC The AEMC reports to the Council of Australian Governments (COAG) through the COAG Energy Council. We have two functions. We make and amend the national electricity, gas and energy retail rules and conduct independent reviews for the COAG Energy Council. This work is copyright. The Copyright Act 1968 permits fair dealing for study, research, news reporting, criticism and review. Selected passages, tables or diagrams may be reproduced for such purposes provided acknowledgement of the source is included.

Summary

On 9 and 30 August 2017, the Prime Minister met with and announced agreement from

the seven largest Australian energy retailers on a range of measures to improve

outcomes for electricity consumers.

The Prime Minister’s meetings focused on the key issue of affordability, with a priority

being that consumers have increased transparency about their bills. A particular

concern raised was that percentage discounts contribute to consumer confusion and

that energy offers with large percentage discounts do not always lead to the lowest bills

for consumers.

Some of the agreements were addressed by the Australian Energy Regulator’s (AER)

recently revised Retail Pricing Information Guidelines (RPIG). The RPIG provides

guidance on how retailers should present pricing information, which could include

percentage discounting. For other matters it was concluded changes to the National

Energy Retail Rules (NERR) were required.

The rule change request

On 18 December 2017, the Honourable Josh Frydenberg MP, Minister for the

Environment and Energy on behalf of the Australian Government submitted a rule

change request to the Australian Energy Market Commission (Commission) under the

National Energy Retail Law (NERL). The rule change request states that:

“The rule is aimed at preventing a behaviour that is considered to be inherently

confusing for the average consumer – the practice of applying discounts to rates

that significantly exceed the base rate as represented by the retailer’s standing

offer. Because the base rate against which the discount applied is inflated, it can

lead the consumer to believe the discount is of relatively greater value than it is.”

The rule change request proposes to prohibit such behaviour by restricting retailers

from applying discounts to market retail contracts if any of the rates in the contract are

higher than the retailer’s equivalent standing offer rates.

Commission’s more preferable final rule and civil penalty provision

The Commission supports the intent of the rule change request and the final

determination achieves this intent through a targeted and integrated approach. It

strengthens the existing regulatory framework by changes to the NERR and the

addition of a civil penalty provision to the AER’s RPIG. These changes will work in

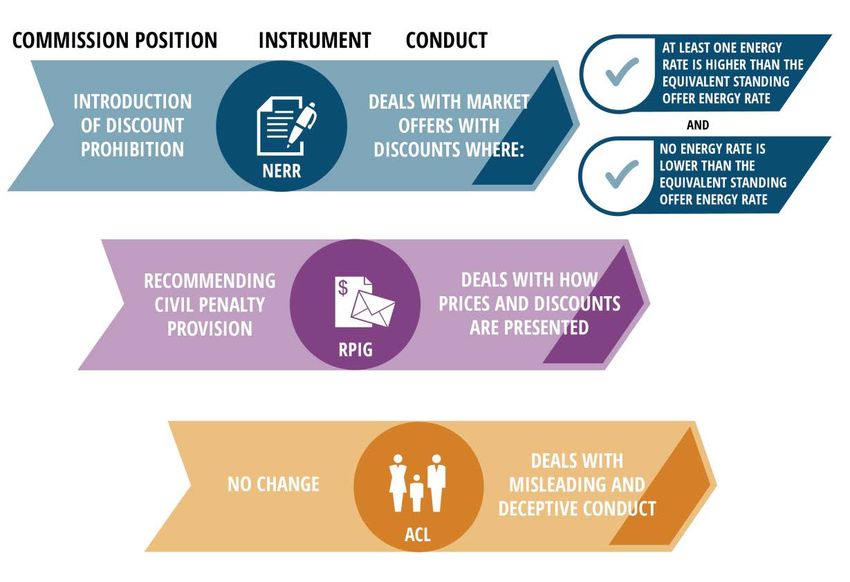

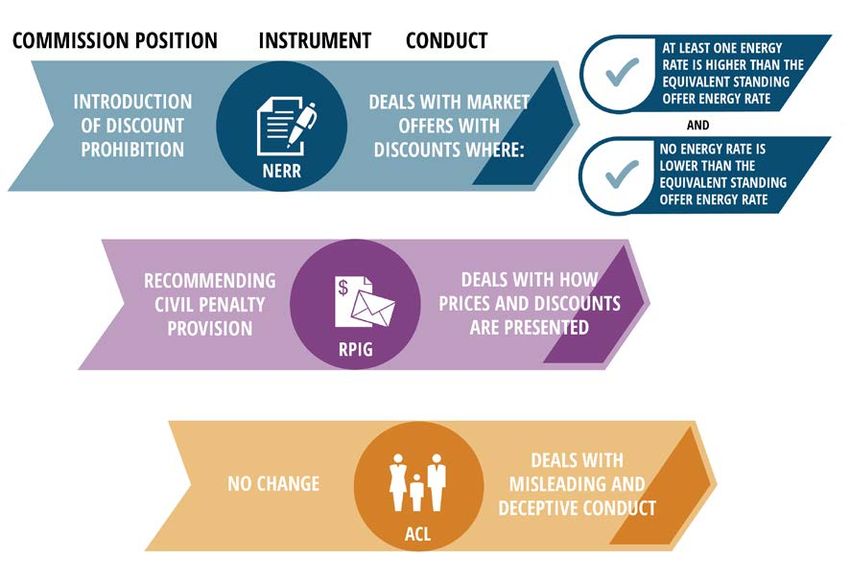

tandem with the existing Australian Consumer Law (ACL), as displayed in Figure 1.

Summary iFigure 1: Proposed package of regulatory arrangements

As displayed in Figure 1, the two changes are:

1. Introducing a rule in the NERR (not applicable in Victoria) restricting retailers

from including discounts in market retail contracts where customers would

definitely be worse off under the undiscounted market offer than under the

standing offer.

2. A joint Commission-AER recommendation to the COAG Energy Council to

make retailers’ non-compliance with the RPIG’s provisions on the presentation

of market and standing offer prices subject to a civil penalty under the NERL.

Having these provisions of the RPIG subject to a civil penalty would allow the

AER to issue infringement notices with penalties of up to $20,000 (for a body

corporate) per breach.

Commission’s analysis

A competitive retail energy market is generally better at producing energy offers that

meet consumers’ preferences at prices consumers are willing to pay than regulatory

measures which restrict the offers that retailers are able to make to consumers. The

primary means of addressing confusion should be through the existing regulatory

instruments governing the presentation and advertising of retail offers, that is, the RPIG

and ACL.

The ACL, enforced by the Australian Competition and Consumer Commission (ACCC),

and the AER’s RPIG together provide a framework for regulating how retailers present

and market offers in the competitive energy retail market. The ACL restricts misleading

or deceptive conduct and false or misleading representations. The RPIG contributes to

this framework by addressing the presentation of market offer prices and standing offer

ii Preventing discounts on inflated energy ratesprices. In this context it is important that the RPIG is enforceable and to achieve this the

Commission recommends a civil penalty provision for the RPIG.

The addition of civil penalties for the RPIG would provide the AER greater enforcement

options. The AER will be able to use these options to fit the circumstances when faced

with a contravention of the RPIG. The Commission considers civil penalties are an

effective tool for the AER in many of the circumstances where an RPIG provision

regarding the presentation of standing or market offer pricing has been breached.

In addition, where there are particular retail practices which cannot be in the interest of

consumers and are apparently designed purely to confuse consumers, a specific

restriction of such practices within the NERR is appropriate.

This is the case where retailers provide discounts in a market retail contract where at

least one rate is above the equivalent rate in a standing offer and no rates in the market

offer are below an equivalent rate in a standing offer. In this case, no consumer could be

better off under the undiscounted market retail contract than under the standing offer.

Therefore a key reason the market retail contract may be attractive is through confusing

consumers with inflated discounting rates. The Commission’s final rule prohibits this

practice under the NERR.

The rule change sought to prevent market offers with discounts where any rate is above

the equivalent rate in a standing offer, even if the other rates in the market offer are

below the standing offer rates. The final rule does not restrict such offers because that

would capture market offers that are beneficial to consumers. For example, high energy

consumption households may be better off on market offers with higher daily supply

charges but lower energy usage charges. The Commission also considers that the

proposed rule would be more likely to inadvertently cause increases in standing offers.

This would materially harm a significant number of consumers.

This new prohibition in the NERR will supplement the ACL. It does not narrow the

application of the ACL. If there are discounting practices that would constitute

misleading or deceptive conduct, or a false or misleading representation then these

practices can and should still be prosecuted by the ACCC under the ACL.

Broader issues relating to discounting

While this rule change relates specifically to the practice of discounting off rates above

the standing offer, the Commission is cognisant of issues with discounting more

broadly.

The Commission noted in the 2017 Retail Energy Competition Review that energy

retailers currently predominantly compete on price and do this through the use of

discounting. This typically involves providing market offers where there is a

conditional discount (e.g. a pay-on-time discount) on standing offer rates. While

discounts can be of benefit to consumers, the current presentation of discounts by

retailers contributes to consumer confusion. There is not a general recognition by

consumers that discounts typically reference a standing offer price that is not set

consistently across retailers. Each energy retailer can set its own standing offer and

change the standing offer price every six months. Other reviews, including the Thwaites

review in Victoria have also noted this issue.

Summary iiiThe result of this general discounting practice is that the value associated with different retail market offers becomes difficult for consumers to compare. Larger discounts have been shown often not to correlate with lower bills or the best deals for consumers. The Commission notes the AER’s recent revision of the RPIG has addressed this issue in part, and the ACCC’s ongoing Retail Electricity Pricing Inquiry is also investigating this issue. The Commission supports this work, is liaising with the AER and the ACCC on these issues and welcomes suggested reforms in this area. iv Preventing discounts on inflated energy rates

Contents

1 The rule change request ................................................................................................. 1

1.1 Introduction and outline .................................................................................................... 1

1.2 Rationale for the rule change request ............................................................................... 2

1.3 Solution proposed in the rule change request................................................................. 3

1.4 Relevant background .......................................................................................................... 6

1.5 The Commission’s rule making and consultation process ............................................ 9

2 Final rule determination .............................................................................................. 10

2.1 The Commission’s final rule ............................................................................................ 10

2.2 Rule making test ................................................................................................................ 13

2.3 Assessment framework .................................................................................................... 13

2.4 Summary of reasons ......................................................................................................... 14

3 The Commission's approach ....................................................................................... 17

3.1 The rule change request ................................................................................................... 17

3.2 Commission’s initial position .......................................................................................... 17

3.3 Stakeholder views ............................................................................................................. 19

3.4 Commission’s final position on the rule change ........................................................... 21

4 Final position on civil penalties for the RPIG......................................................... 23

4.1 Importance of improving enforcement tools for the RPIG.......................................... 23

4.2 Governance issues relating to civil penalties for the RPIG ......................................... 29

5 Final rule determination on the discount prohibition ........................................... 32

5.1 Summary of the discounting prohibition ...................................................................... 32

5.2 Energy rates test ................................................................................................................ 32

5.3 Energy payments test ....................................................................................................... 36

5.4 Exclusion of fees and penalties ....................................................................................... 37

5.5 Equivalency test ................................................................................................................ 38

5.6 Fixed price market retail contracts ................................................................................. 46

5.7 Commencement date of the rule ..................................................................................... 48

5.8 Standing offers under this rule change .......................................................................... 49

5.9 The rule’s coverage of gas contracts ............................................................................... 51

5.10 Discounts prohibition applies to energy rates at the date the contract is formed .... 52

5.11 Treatment of dual fuel contracts ..................................................................................... 53

Abbreviations........................................................................................................................... 61

A Summary of other issues raised in submissions ..................................................... 62

B Legal requirements under the NERL ........................................................................ 68

B.1 Final rule determination................................................................................................... 68

B.2 Power to make the rule .................................................................................................... 68B.3 Commission’s considerations .......................................................................................... 68

B.4 Civil penalties .................................................................................................................... 69

C Data analysis .................................................................................................................. 70

C.1 Methodology...................................................................................................................... 70

C.2 Analysis of energy offers.................................................................................................. 71

C.3 Bill analysis of energy offers ............................................................................................ 73

D Differences between proposed rule and more preferable final rule .................. 751 The rule change request

1.1 Introduction and outline

On 18 December 2017, the Honourable Josh Frydenberg MP, Minister for the

Environment and Energy on behalf of the Australian Government (proponent)

submitted a rule change request (rule change request) to the Australian Energy Market

Commission (Commission) under the National Energy Retail Law (NERL) that aimed to

address confusing retailer discounting practices. The rule change request proposed to

prohibit a retailer applying a discount to a rate under a market retail contract if any of

the rates in the contract are higher than the retailer’s equivalent standing offer rates.

The proponent also requested that the rule change request be considered a

non-controversial rule change request and, as a result, be progressed under an

expedited rule change process. This final rule determination:

• summarises the key elements of the rule change request

• sets out the background to the rule change request

• describes the rule change process

• describes the Commission’s more preferable final rule and how it meets the

national energy retail objective (NERO)

• provides the Commission’s approach in relation to its positions on the final rule

for this rule change request and civil penalties for the Retail Pricing Information

Guidelines (RPIG)

• summarises the issues the Commission considered in its position on civil

penalties for the RPIG, including stakeholder views, the Commission’s analysis

and its final position

• summarises the issues the Commission considered in assessing this rule change

request, including stakeholder views, the Commission’s analysis and its final

determination.

The rule change request 11.2 Rationale for the rule change request

1.2.1 Issues raised in the rule change request

The request raised a number of issues but sought to address one core issue. This core

issue is stated as follows:

“The rule is aimed at preventing a behaviour that is considered to be

inherently confusing for the average consumer – the practice of applying

discounts to rates that significantly exceed the base rate as represented by

the retailer’s standing offer. Because the base rate against which the

discount applied is inflated, it can lead the consumer to believe the discount

is of relatively greater value than it is.” 1

The issue raised in the rule change request is therefore a very specific framing of a

problem with discounting. The issue raised does not extend to broader problems

associated with discounting practices. These could include the presentation of discounts

generally or general consumer confusion created by other types of retailer discounting

practices, such as discounts off standing offers which are set in inconsistent ways by

energy retailers.

The rule change request further links its statement of the problem to be addressed to

two concepts: consumer detriment and the NERO. The rule change request specifically

mentions the complexity and variability of available offers means the discounting

practice it seeks to address has the potential to confuse a consumer and can easily result

in consumer detriment. 2

1.2.2 Arguments in the rule change request supporting the proposed rule

The rule change request provides two main arguments why a retail rule of the kind

proposed in the request would be a useful addition to the provisions already in place in

the Australian Energy Regulator’s (AER) RPIG and the Australian Consumer Law

(ACL): 3

1. A more effective deterrent than existing arrangements.

— Goes further than the RPIG. The RPIG only deals with the presentation of

discounting and pricing information, and contains requirements for

describing discounts in advertising and marketing. It does not extend to

what is permissible in the terms and conditions of contracts. 4

— A rule sends a strong signal to energy retailers as to what their

obligations are. A provision in the National Energy Retail Rules (NERR)

prohibiting discounting where charges in market offers are higher than in

1 Rule change request, p. 2.

2 Rule change request, p. 6.

3 These are discussed in section 1.4.1.

4 Rule change request, p. 3.

2 Preventing discounts on inflated energy ratesthe equivalent standing offer would send a strong signal to energy retailers

as to their obligations. 5

— Simpler and cheaper to enforce than the ACL. A rule preventing

discounting on offers above standing rates would operate in addition to the

ACL. The rule change request suggests a rule with such a prohibition would

prevent the relevant behaviour without the need for the costly and time

consuming process of prosecution under the ACL. 6

— A retail rule change allows the option to impose a civil penalty. A

financial penalty would be an effective deterrent to this discounting

behaviour and is appropriate given non-compliance could result in a retailer

receiving a financial benefit. 7

2. May capture behaviour that is not covered by the ACL. The rule change request

quotes the Australian Competition and Consumer Commission (ACCC) Retail

Electricity Pricing Inquiry’s preliminary report as support for addressing

behaviour that causes confusion (and potentially consumer detriment) not being

covered by provisions in the ACL:

“Even if a ‘discount’ does not meet the threshold to be considered

misleading or deceptive under the ACL, it could still be very

confusing for consumers. This is particularly the case when there is no

consistent form of presentation or application of discounts.” 8

1.3 Solution proposed in the rule change request

The proponent sought to resolve the issues discussed in section 1.2 by proposing a rule

(the proposed rule) that prohibits retailers from applying discounts to any amount in an

electricity market retail contract from a rate above a relevant standing offer with respect

to:

• daily supply charges

• usage charges

• demand charges.

These charges are not currently defined within the NERR and the proposed rule does

not seek to define them. They would therefore need to be defined in the NERR.

The rule change request states, however, that it relies on the term “standing offer

prices”, which is defined in the NERL as:

“…all of the tariffs and charges that a retailer charges a small customer for or in

connection with the sale and supply of energy to a small customer under a

standard retail contract.” 9

5 Ibid, p. 6.

6 Ibid, p. 6.

7 Ibid, pp. 3–4.

8 Ibid, p. 6.

9 NERL section 2.

The rule change request 3A standing offer would be relevant for the operation of the proposed rule if two

conditions are met:

• the market retail contract and the standing offer have the same tariff structure

• the standing offer is generally available to small customers in the region in which

the customer is to consume electricity under the market retail contract. 10

The proposed rule would apply only if there is a standing offer with a tariff structure

mirroring the tariff structure in the market retail contract (with discount provisions)

being formed with the small customer. Thus, the comparison of rates in a market retail

contract (to which a discount applies) with standing offer rates needs to resemble a “like

for like” comparison. If there is no standing offer with a directly comparable tariff

structure the proposed rule would have no effect. 11

The rule change request also suggested that comparisons of market offer rates to

standing offer rates for a retailer should be done within the region, and the standing

offer would be “generally available” to the customer in that region. 12 The Commission

has understood “region” to refer to the distribution network supply area in which the

consumer’s connection point is located. This interpretation makes the most sense in

terms of retail pricing in the national electricity market as distribution network pricing

covers groups of customers in the same geographical area. 13

The rule change request also notes that the intention is to prevent discounting on rates

that are in excess of the retailer’s standing offer available at the time the market retail

contract is entered into. It is not intended that the prohibition apply to a contract that

has already been entered into at the time the rule is made. 14

The rule change request suggested a civil penalty apply to the proposed rule. The

proponent argued a financial penalty would be an effective deterrent to the issue raised

in the rule change request given non-compliance could result in a retailer receiving a

financial benefit. 15

To illustrate how the proposed rule would apply, if it were made, the Commission has

developed examples of its likely operation. These examples are set out in Box 1.1 and

Box 1.2 below.

10 The term “generally available” has a meaning in the RPIG.

AER, AER Retail Pricing Information Guidelines: Version 4.0, Melbourne, 2015, p. 17. Version 5.0 of the

RPIG was released on 23 April 2018 but does not take effect until 31 August 2018; see p. 22 for its

definition of “generally available plan”.

11 To the extent that these comparisons cannot be made with respect to tariff structures, the rule

change request suggests the Commission consider a more preferable rule. The rule change request

(p. 5) considers the more preferable rule should not discourage tariff innovation or reform.

12 The rule change request (p. 4) suggests that the Commission could consider a more preferable rule

in this instance for an alternative construction such as “nearest region”. The intention behind this

suggestion is to not limit the application of the proposed rule where there is not an equivalent

standing offer tariff structure “generally available” to the consumer.

13 An alternative interpretation of region could be national electricity market region, along the lines of

the transmission pricing regions for the national electricity market.

See: AEMO, Fact Sheet: The National Electricity Market, AEMO, Melbourne, p. 1.

14 Rule change request, p. 4.

15 Rule change request, pp. 3–4.

4 Preventing discounts on inflated energy ratesBox 1.1 First example of how the proposed rule would operate

A retailer has a market offer and a generally available standing offer with an

equivalent tariff structure in the same distribution network supply area. The details

outlined in the table below:

Standing offer Market offer

Daily supply charge 122.80 c 132.624 c

Usage charge 35.90 c/kWh 38.77 c/kWh

Discounts (if applicable) N/A 15 per cent to all charges

The market offer rates are eight per cent higher than the standing offer rates. The

discount provision in a market retail contract based on the above market offer would

be in breach of the proposed rule.

Box 1.2 Second example of how the proposed rule would operate

A retailer has a market offer and a generally available standing offer with an equivalent

tariff structure in the same distribution network supply area. The details outlined in the

table below:

Standing offer Market offer

Daily supply charge 70.68 c 75.96 c

Usage charge 44.56 c/kWh 20 c/kWh

Discounts (if applicable) N/A 10 per cent to all charges

As the daily supply charge in the market offer on which the discount is being applied

exceeds the standing offer, the discount provision in a market retail contract based on

the above market offer would be in breach of the proposed rule. This is despite the

usage charge for the market offer being well below the standing offer usage charge.

The rule change request 51.4 Relevant background

On 9 and 30 August 2017 the Prime Minister announced agreement from the seven

largest retailers on a range of measures to improve outcomes for electricity

consumers. 16

The rule change proposal was developed following the Prime Minister’s meetings with

energy retailers last year. It was developed specifically through retailer roundtable

meetings which followed the Prime Minister’s meetings.

The Prime Minister’s meetings and the roundtables have looked at the key issue of

affordability, with a priority being that consumers have increased transparency about

their bills. In particular, there has been a concern that percentage discounts contribute to

consumer confusion. Part of the concern is that energy offers with large percentage

discounts do not always lead to the lowest bills for consumers.

1.4.1 Current arrangements

There are two existing regulatory frameworks that deal with discounting behaviour,

including the issue of discounting from rates above those in a standing offer which the

rule change request seeks to address. These are the ACL under the Competition and

Consumer Act 2010 (enforced by the Australian Competition and Consumer

Commission (ACCC)), and the AER’s RPIG.

The Australian Consumer Law

Among other things, the ACL protects consumers across Australia from:

• misleading or deceptive conduct, or conduct that is likely to mislead or deceive

(section 18)

• false or misleading representations about goods or services (section 29).

The ACCC has previously taken action against energy retailers for making false or

misleading representations about discounts under the ACL. In 2015, Origin was

required to pay penalties for making false or misleading representations about the level

of discount residential consumers in South Australia would receive. 17 This was in

respect of Origin’s DailySaver electricity, gas and dual fuel plans. 18

The energy usage rates (to which the discounts applied) were higher in the DailySaver

energy plans than in Origin’s standing offer generally available to residential

consumers. In the legal proceedings, Origin admitted that some consumers would have

understood that its discounts in the DailySaver plans would be applied to energy usage

rates available generally to consumers like themselves (i.e. the standing offer).

16 M Turnbull (Prime Minister), A better deal for Australian families, media release, Parliament House,

Canberra, 9 August 2017, https://www.pm.gov.au/media/better-deal-australian-families.

17 ACCC, Retail Electricity Pricing Inquiry: Preliminary report, ACCC, Canberra, 2017, pp. 128, 167–168,

viewed 19 March 2018,

https://www.accc.gov.au/system/files/Retail%20Electricity%20Inquiry%20-%20Indicative%20rep

ort%20-%2013%20November%202017.pdf.

18 Australian Competition and Consumer Commission v Origin Energy Limited [2015] FCA 55 (9 February

2015), Federal Court of Australia.

6 Preventing discounts on inflated energy ratesOrigin admitted that as the energy usage rates were not in accord with the reasonable

understanding that discounts would have reference to generally applicable rates

(standing offer rates), various advertisements of the DailySaver plan made false or

misleading representations. 19 Specifically, it admitted that it had contravened sections

29(1)(g) and (i) of the ACL: making false or misleading representations that goods or

services have certain characteristics or benefits, and making false or misleading

representations with respect to the price of goods or services. 20

The Retail Pricing Information Guidelines

Through its RPIG, the AER provides guidance on the presentation of pricing

information (including discounts). The NERL requires retailers to comply with the

RPIG in their presentation of standing and market offers (NERL sections 24 and 37).

The RPIG has been recently revised and the revised RPIG will come into effect in

August this year. 21 This revised RPIG had its genesis in a 2017 review conducted by the

AER. The Customer Price Information review, published in September 2017, focused on

the detailed implementation of the outcomes from the Prime Minister’s August 2017

roundtable meetings with energy retailers. 22

The issues paper for the review focused on how customers get the information they

need to prompt them to investigate the energy market, compare plans and providers,

and choose the best deal. 23 The Customer Price Information review informed a range of

the AER’s work in relation to its RPIG, including discounts.

Following the review and consultation on revisions to the RPIG, the AER published a

final revised RPIG on 23 April 2018 (version 5.0). It will take effect on 31 August 2018.

The final revised RPIG requirements on retailers regarding discounts have not changed

substantially from version 4.0. The most important change relevant to discounts is that

retailers will now be required to present a new Basic Product Information Document

(BPID; prepared by the AER) for all of their energy offers.

RPIG version 5.0 requires retailers to have two documents for each energy offer

available: the BPID and the Detailed Plan Information Document (DPID). 24

Importantly, the BPID includes two bill estimates for each of the following household

usage profiles:

• a one person household

• a two to three person household

• a four to five or more person household.

19 Ibid, paragraphs 25–27.

20 Relevant misleading or deceptive conduct was also alleged by the ACCC. The judgement indicated

that the ACCC did not, however, pursue this allegation. Ibid, paragraph 24.

21 AER, AER Retail Pricing Information Guidelines: Version 5.0, AER, Melbourne, 2018.

22 AER, Customer price information: issues paper, AER, Melbourne, 2017, pp. 6–7.

23 Ibid, p. 3.

24 AER, AER Retail Pricing Information Guidelines: Version 5.0, AER, Melbourne, 2018, p. 5.

The rule change request 7The two bill estimates for each of these usage profiles relate to when all available

discounts in the energy offer are obtained, and when conditional discounts are not

obtained under the energy offer. 25

Notably, the comparison pricing table will not be displayed on the BPID for:

• small business customer energy offers

• residential customer energy offers with demand charges

• plans where customer usage data is required to price the plan.26

In relation to discounts, the RPIG version 5.0 requires retailers to provide the following

information on Energy Made Easy (EME) for the purposes of the BPID and the DPID:

• the amount and/or percentage of the discount

• for percentage discounts, what component of the customer’s bill the discount

applies to (for example, whether the discount is off usage, the supply charge or

the whole bill) and if the discount is off the GST inclusive or exclusive charges

• the base level tariff and what the discount is off

• where information on the base level can be found (including the specific page

where it can be found on the retailer’s website)

• for dual fuel offers, which fuel(s) the discount applies to

• for solar plans, how any discounts are to be applied. For example, is the discount

off total usage, or the net bill amount after solar credits. 27

This information must also be included in retailers’ marketing or advertising about a

specific discount rate. There are some additional specific requirements for retailers in

describing discounts in their advertising and marketing. 28

1.4.2 Concurrent work on related issues: ACCC Retail Electricity Pricing

Inquiry

External to the Commission, the ACCC’s Retail Electricity Pricing Inquiry relates to

issues raised by this rule change request. This ACCC inquiry has the mandate and

scope to address broader issues to do with discounting.

On 27 March 2017 the Treasurer, the Hon Scott Morrison MP, directed the ACCC to

hold an inquiry into the supply of retail electricity and the competitiveness of retail

electricity prices. Relevant to discounts, the terms of reference state that the matters to

be considered for the inquiry include:

“any impediments to consumer choice, including transactions costs, a lack of

transparent information, or other factors.” 29

25 Ibid, p. 21.

26 Ibid, p. 21.

27 Ibid, pp. 9–10. These information requirements are similar to those in the RPIG version 4.0.

28 Ibid, p. 20.

29 S Morrison (Treasurer), Inquiry into Retail Electricity Supply, Parliament House, Canberra, 27 March

2017.

8 Preventing discounts on inflated energy ratesOn 16 October 2017 the ACCC published its preliminary report for the inquiry. The

preliminary report commented on discounting practices in the retail energy market. It

stated:

“Discounts are a common way for retailers in many sectors to advertise or signal

to consumers that the price being offered is lower than that which is generally

available. The retail electricity sector is no different and, while discounts are

attractive to consumers, the practice has been identified as a barrier to

consumers engaging with the market successfully. A number of parties also

consider that the practice of discounting has eroded trust in the retail electricity

market.” 30

The ACCC is still developing its final report for its Retail Electricity Pricing Inquiry, to

be provided to the Australian Government by 30 June 2018.

1.5 The Commission’s rule making and consultation process

On 20 March 2018, the Commission published a notice advising of its commencement of

the rule making process and consultation in respect of the rule change request. 31 A

consultation paper identifying specific issues for consultation was also published.

Submissions closed on 17 April 2018.

The Commission considered that the rule change request was a request for a

non-controversial rule as defined in section 252 in the NERL. Accordingly, the

Commission commenced an expedited rule change process, subject to any written

requests not to do so. The closing date for receipt of written requests was 3 April 2018.

No objections to the Commission carrying out an expedited rule change process were

received. Accordingly, the rule change request was considered under an expedited

process. 32

The Commission received 17 submissions. Issues that are not discussed in the body of

this document have been summarised and responded to in Appendix A.

The Commission also held stakeholder forums on 15 February 2018 and 5 April 2018 to

discuss the rule change request and the Commission’s initial and revised positions on

the issues raised in the rule change request. These were attended by a range of

stakeholders including representatives from energy retailers, ombudsmen, government,

market bodies and consumer representatives.

30 ACCC, Retail Electricity Pricing Inquiry: Preliminary report, ACCC, Canberra, 2017, p. 128, viewed 19

March 2018,

https://www.accc.gov.au/system/files/Retail%20Electricity%20Inquiry%20-%20Indicative%20rep

ort%20-%2013%20November%202017.pdf.

31 This notice was published under section 251 of the NERL.

32 Section 252 of the NERL.

The rule change request 92 Final rule determination

This chapter outlines: 33

• the Commission’s final rule determination

• the rule making test for changes to the NERR

• the assessment framework for considering the rule change request

• a summary of the Commission's consideration of the more preferable final rule

against the NERO.

2.1 The Commission’s final rule

The Commission's final rule determination is to make a more preferable final rule. The

more preferable final rule’s key features are summarised in Table 2.1 below.

At a high level, a retailer would be in breach of the final rule if all the following

conditions are satisfied:

(1) The retailer formed a market retail contract including provisions for discounts to

any energy rates

(2) The retailer has a standing offer that is equivalent to the market retail contract (an

“equivalent standing offer” — the conditions for equivalency are referred to as

the “equivalency test” in section 5.5)

(3) The retailer’s market retail contract both has:

(a) at least one energy rate that exceeds the equivalent energy rate component

under the equivalent standing offer (before the application of the discount)

(b) no energy rate that is lower than the equivalent energy rate component

under the equivalent standing offer (together with (3)(a) above, referred to

as the “energy rates test” in section 5.2).

(4) The retailer’s market retail contract has every single energy payment to a

consumer (for example, a feed-in tariff) equal to or lower than the equivalent

payments in the equivalent standing offer (referred to as the “energy payments

test” in section 5.3).

Table 2.1 Key features of the final rule

Key feature of the rule Operation of the feature

Prohibition on discounting in A retailer must not include a discount to an energy rate in a

certain circumstances market retail contract with a small customer if the conditions

outlined below are met.

33 Note that the proposal to attach civil penalties to the provisions in the NERL that require retailers to

comply with the RPIG in relation to the presentation of prices is discussed in chapter 4 rather than

this chapter, as that proposal will be a recommendation to the COAG Energy Council, not a rule

change.

10 Preventing discounts on inflated energy ratesKey feature of the rule Operation of the feature

Preventing confusing The discount prohibition will apply to all market retail contracts

discounts that cause where, before any discounts are applied:

consumer detriment: energy

• at least one energy rate exceeds the equivalent energy rate

rates test

component under the equivalent standing offer

• no energy rate under the market retail contract is lower than

the equivalent energy rate component under the equivalent

standing offer.

This condition is part of three conditions that must be satisfied for

the discount prohibition to apply. The other two conditions are the

energy payments test and conditions for equivalency.

Preventing confusing The discount prohibition will apply to all market retail contracts

discounts that cause where the level or rate of every energy payment to the customer

consumer detriment: energy under the market retail contract (if any), such as feed-in tariffs, is

payments test equal to or lower than the level or rate of the equivalent energy

payment under the equivalent standing offer.

This condition is part of three conditions that must be satisfied for

the discount prohibition to apply. The other two conditions are the

energy rates test and conditions for equivalency.

Conditions for equivalency The discounting prohibition applies only to a market retail

between a market retail contract that has an equivalent standing offer.

contract and standing offer

A standing offer is equivalent to a market retail contract if:

• they are provided by the same retailer (or by related bodies

corporate)

• their tariff structures are not materially different with respect to

energy rates and energy payments

• the market retail contract does not provide material additional

benefits or services to the customer compared to the standing

offer

• they are both available to the same customer, or would be, if

the retailer were the designated retailer for the customer’s

premises. 34

This condition is part of three conditions that must be satisfied for

the discount prohibition to apply. The other two conditions are the

energy rates test and energy payments test.

Materiality with respect to: • The references to “material” means trivial differences in tariff

structures or benefits and services between the market retail

• tariff structures of energy

contract and the standing offer will not prevent the discount

rates and energy

prohibition from applying to a retailer’s market retail contract.

payments

• The AER will need to judge what is “material” in enforcing the

• additional benefits and

final rule.

services.

Some guiding examples of materiality are provided in Boxes 5.2

to 5.6 in chapter 5.

34 This is included as only the designated retailer for a customer’s premises is obliged to offer a

standing offer to that customer. NERL Part 2, Division 3.

Final rule determination 11Key feature of the rule Operation of the feature

Explicit accounting for fixed Market contracts that have all energy rates fixed for 12 months or

price market retail contracts more will be exempt from the discount prohibition by way of not

being considered to have an “equivalent standing offer”. 35

Accounting for unique • A new definition of a dual fuel market contract has been

aspects of dual fuel contracts included in the NERR. 36 This covers:

in the operation of the

discount prohibition (a) one market retail contract between a small customer and a

retailer for the sale of both electricity and gas by the

retailer to the small customer

(b) two market retail contracts with the same small customer,

one for the sale of electricity and the other for the sale of

gas to the customer, where the prices or conditions of one

or both contracts are contingent on the customer entering

into both contracts.

• Dual fuel market contracts can have an equivalent standing

offer that is either:

— a dual fuel standing offer

— a combination of an electricity-only standing offer and a

gas-only standing offer.

• Single fuel market contracts will not match to one fuel in a dual

fuel standing offer.

Commencement date The final rule for the discount prohibition takes effect on 1 July

2018.

This date coincides with network pricing changes in all National

Energy Customer Framework adoptive jurisdictions.

The Commission's reasons for making this final rule determination are summarised in

section 2.4. Further information on the legal requirements for making this final rule

determination is set out in Appendix B.

The more preferable final rule made by the Commission is published with this final rule

determination.

The Commission has sought to enhance the proposed rule with its more preferable final

rule. The discount prohibition in the more preferable final rule targets instances where

consumers could enter into contracts where they would be (penalties and fees aside)

worse off on the undiscounted market retail contract compared to the standing offer.

We have also made sure the comparison of rates between the market retail contract and

standing offer is more of a “like for like” comparison. This way we can account for

additional benefits and services received by consumers.

A detailed comparison of the more preferable final rule and the proposed rule is

contained in Appendix D.

35 Other fixed price market contracts will be assessed by the AER under the conditions for an

“equivalent standing offer” in terms of the fixed price aspect being a “material additional benefit or

service”. This is covered in more detailed in section 5.6.4.

36 This impacts existing rules 48B and 117, as discussed in section 5.11.4 of this final determination.

12 Preventing discounts on inflated energy rates2.2 Rule making test

2.2.1 Achieving the national energy retail objective

The Commission may only make a rule if it is satisfied that the rule will, or is

likely to, contribute to the achievement of the NERO. 37 This is the decision

making framework that the Commission must apply.

The NERO is: 38

“to promote efficient investment in, and efficient operation and use of,

energy services for the long term interests of consumers of energy with

respect to price, quality, safety, reliability and security of supply of energy.”

The Commission must also, where relevant, satisfy itself that the rule is "compatible

with the development and application of consumer protections for small customers,

including (but not limited to) protections relating to hardship customers" (the

"consumer protections test"). 39 Where the consumer protections test is relevant in the

making of a rule, the Commission must be satisfied that both the NERO test and the

consumer protections test have been met. 40 If the Commission is satisfied that one test,

but not the other, has been met, the rule cannot be made.

There may be some overlap in the application of the two tests. For example, a rule that

provides a new protection for small customers may also, but will not necessarily,

promote the NERO.

2.2.2 Making a more preferable rule

Under section 244 of the NERL, the Commission may make a rule that is different

(including materially different) to a proposed rule (a more preferable rule) if it is

satisfied that, having regard to the issue or issues raised in the rule change request, the

more preferable rule will or is likely to better contribute to the achievement of the

NERO.

2.3 Assessment framework

In assessing the rule change request against the NERO the Commission has considered

the following principles:

• Transparency of information: Competition is most effective when consumers

have the information they need to allow them to compare and choose the

products and services that they value at prices they are willing to pay. The

Commission has assessed the extent to which the proposed rule and alternatives

are likely to promote information provision that facilitates informed consumer

choices.

37 Section 236(1) of the NERL.

38 Section 13 of the NERL.

39 Section 236(2)(b) of the NERL.

40 That is, the legal tests set out in sections 236(1) and (2)(b) of the NERL.

Final rule determination 13• Regulatory and administrative burden: The Commission has assessed the extent

to which proposed solutions impose costs on market participants. The

Commission has also assessed the extent to which any rule is likely to restrict

retail offers and potential side effects of such restrictions (e.g. increases in

standing offers).

• Facilitating service and tariff innovation: Competition will be most effective

where retailers are free to develop and offer services and tariffs that consumers

value. The Commission has assessed the extent to which any rule is likely to

restrict tariff and service innovation in the future.

The Commission’s assessment against these principles is set out in section 2.5.2.

2.4 Summary of reasons

2.4.1 Contributing to the achievement of the NERO

Having regard to the issues raised in the rule change request and during consultation,

the Commission is satisfied that the more preferable final rule will, or is likely to, better

contribute to the achievement of the NERO for the reasons set out below.

Transparency of information

The Commission considers that the more preferable final rule is likely to promote

greater transparency of information to consumers by restricting a practice that is

inherently confusing.

Standing offers generally correspond to the highest terms and conditions and consumer

protections afforded to consumers in jurisdictions applying the National Energy

Customer Framework (NECF), and thus generally are the most expensive energy offers

in the market. Therefore, the practice of discounting off market offers above the

standing offer (that will be prohibited by the Commission’s final rule) lacks

transparency as it obscures the market contract’s higher energy rates (relative to the

standing offer) through an inflated level of discount. A key reason the market retail

contract may be attractive is through confusing consumers with these inflated

discounting rates.

This kind of transparency of information is crucial to competition and consumer

engagement. This discounting prohibition in the final rule will assist consumers in

having the confidence to compare and choose energy products and services they value

at prices they are willing to pay.

Regulatory and administrative burden

The Commission’s final rule is unlikely to have a significant impact on regulatory

burden because the practice being restricted is not common within the industry. For

example, the Commission’s analysis (as set out in Appendix sections C.1 and C.2)

demonstrates that at 17 January 2018 0.9 per cent of all market offers would be restricted

under the more preferable final rule. More broadly, since the cases brought by the

ACCC under the ACL (described in section 1.4.1) the practice of discounting off market

offers above standing offers is rare.

14 Preventing discounts on inflated energy ratesFurthermore, the Commission’s final rule has the potential to reduce administrative

burden on the retail market’s compliance as a whole because it may avoid the legal costs

associated with action under the ACL by providing a clear and stronger deterrent on

the specific discounting practice.

Part of the burden identified for this rule change was the potential for retailers to

increase their standing offers to comply with the rule. The Commission considers there

is a low chance of any significant upward pressure on the standing offers across

jurisdictions that have adopted the NECF. This is due to the low prevalence of the

discounting practice the final rule will prohibit. Furthermore, the more preferable final

rule is likely to have less of an upward pressure on standing offer prices compared to

the proposed rule because under the proposed rule the discounting prohibition was

broader and likely to affect some offers that were in consumers’ interests.

Facilitating service and tariff innovation

Under the Commission’s more preferable final rule, retailers will be free to develop and

offer services and tariffs that consumers value without the risk of their discounting

provisions in market retail contracts being prohibited across the board.

The conditions for equivalence between a retailer’s market contract and standing offer

which are crucial to the operation of the final rule recognise that consumers value more

than just energy rates in market contracts for energy. There are often additional benefits

and services, and energy payments (such as feed-in tariffs), that motivate consumers to

adopt certain energy offers and take them up as market contracts. The operation of the

rule provides that retailers offering innovative extra services and innovating in their

market retail contract tariff structures beyond their basic standing offer tariff structures

will not have the risk of a discounting prohibition applying to these contracts.

Furthermore, the exclusion of fully fixed price contracts of greater than a year within

the final rule recognises these contracts do not have an equivalent standing offer and

that tariff innovation beyond standing offer tariff structures should not be restricted.

The final rule also accounts for and facilitates the potential for greater locationality of

pricing in the future, particularly as distribution network pricing evolves. An

equivalent standing offer, which forms the basis of the comparison of energy rates and

energy payments crucial to the discount prohibition for a market retail contract, must

also be available to the customer taking up the market retail contract (or would be

available if the retailer was the designated retailer for the customer’s premises). This

better facilitates locational pricing compared to the proposed rule, which referred to the

market retail contract and standing offer being available in the same region (such as a

distribution network supply area). This is because pricing signals at the postcode level,

for example, would be accounted for under the final rule, but not the proposed rule.

The Commission’s rule would only prohibit discounting provisions if one of the energy

rates in the market retail contract is higher than the same energy rate in an equivalent

standing offer, while all the other energy rates in the market retail contract are at least

equal to or higher than in the equivalent standing offer. This would allow retailers to

make offers (with discounts) to consumers where, for example, a daily supply charge is

lower but the usage charge is higher than the equivalent standing offer. This type of

pricing could be beneficial to lower usage households. In permitting this type of tariff

Final rule determination 15innovation, the Commission sees its final rule as a more preferable way to meet the NERO while maintaining the intent of the proponent to prevent confusing inflated discounts that cause consumer detriment. 2.4.2 Consumer protections test The Commission is satisfied that the more preferable final rule passes the consumer protections test as it is compatible with current consumer protections and is likely to be compatible with the future development of consumer protections for small customers. In particular, the final rule was designed to complement, and be compatible with, the consumer protections provided in the RPIG and through the ACL (as discussed in section 1.4.1). The restricted scope of the discounting prohibition also limits the potential for any future incompatibility with consumer protections as they are developed over time. 16 Preventing discounts on inflated energy rates

3 The Commission's approach

This chapter sets out the Commission’s overarching approach in relation to the issues

raised in the rule change request and broader discounting issues. It is broken down into:

• the rule change request

• the Commission’s initial position

• stakeholder views

• the Commission’s final position.

The details of the specific civil penalty recommendation and the NERR restriction are

set out in chapters 4 and 5.

3.1 The rule change request

On 9 and 30 August 2017, the Prime Minister met with and announced agreement from

the seven largest retailers on a range of measures to improve outcomes for electricity

consumers.

The Prime Minister’s meetings focused on the key issue of affordability, with a priority

being that consumers have increased transparency about their bills. A particular

concern raised was that percentage discounts contribute to consumer confusion and

that energy offers with large percentage discounts do not always lead to the lowest bills

for consumers.

Some of the agreements were addressed by the AER’s recently revised RPIG. The RPIG

provides guidance on how retailers should present pricing information, which could

include percentage discounting. For other issues it was concluded rule changes were

required.

On 18 December 2017, the Honourable Josh Frydenberg MP, Minister for the

Environment and Energy on behalf of the Australian Government submitted a rule

change request to the Commission under the NERL. The rule change request states that:

“The rule is aimed at preventing a behaviour that is considered to be inherently

confusing for the average consumer – the practice of applying discounts to rates

that significantly exceed the base rate as represented by the retailer’s standing

offer. Because the base rate against which the discount applied is inflated, it can

lead the consumer to believe the discount is of relatively greater value than it is.”

The rule change request proposes to prohibit such behaviour by restricting retailers

from applying discounts to market retail contracts if any of the rates in the contract are

higher than the retailer’s equivalent standing offer rates.

3.2 Commission’s initial position

3.2.1 Commission’s approach in relation to the rule change request

In the consultation paper the Commission considered that a competitive retail energy

market is generally better at producing energy offers that meet consumers’ preferences

at prices they are willing to pay than regulatory measures which restrict the offers that

The Commission's approach 17You can also read