Smart finance for your business - Stefan Kempf CEO and founder - aifinyo

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

smart finance for your business Stefan Kempf CEO and founder

Mission

„We want to enable entrepreneurs to focus

on their business and be more successful by

supporting with fast, smooth and intelligent

financial solutions.”

aifinyo at a glance

digital finance plattform transaction volume in EUR m milestones

350

2012 starting with factoring for SME

300

2014 launch of factoring for freelancer

250 2015 initiating finetrading

200

2015 entering leasing market

2016 adding debt collection service

150

2017 small ticket finetrading (e-com)

100 2018 stock listing m:access

50 2019 rebranding to aifinyo

2020 merger with Decimo and Pagido

-

2012 2014 2016 2018 2020

market opportunity driven by megatrends

Technology

Retreat of banks

innovation

4m

Entrepreneurs prefer to

focus on business rather

than finance

Data, integration, Mindset and

AI expectation

revenue potential commercial retail clients Germany*

well positioned in a consolidating market

• currently high pressure on market consolidation

• aifinyo is well positioned, due to product range,

banks size and tech focus

multiple-product

saving banks • successful merger with Decimo + Pagido

provider

(~1.700)

• highly fragmented market, huge number of

competitors

alternative • banks lack technology and focus, regulatory

1-product fintechs

provider

financing burden

(~800)

(~1.000) • alternative financing competitors lack product

range and small ticket expertise

• fintechs are mainly too small for platform cost

and lack product range

low tech tech challenger

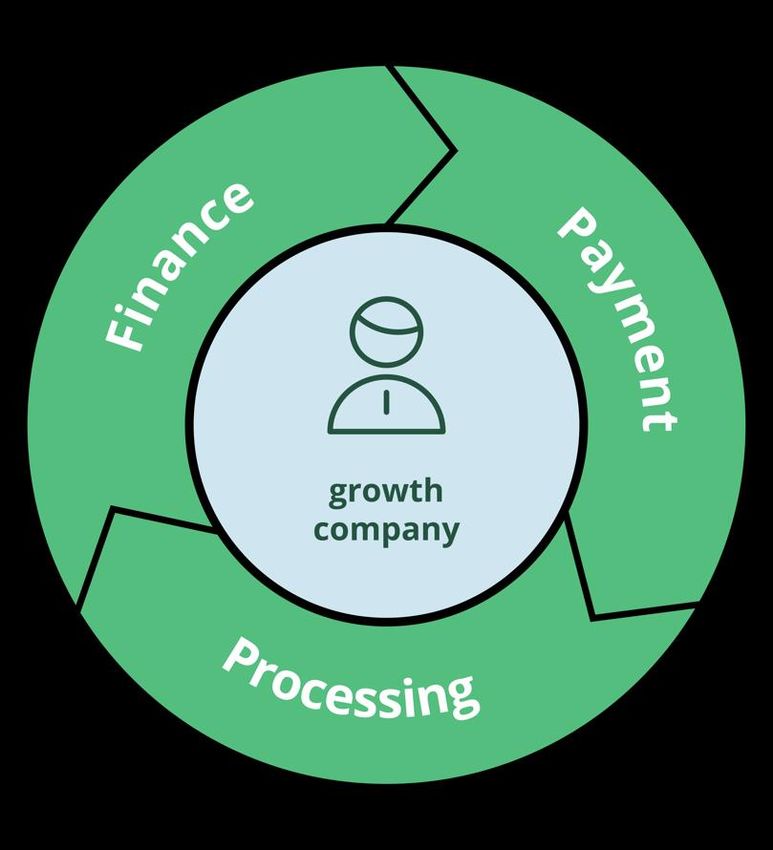

“aifinyo will define the new category smart finance

in B2B by combining finance, payment and processing

in a highly lucrative market.”value creation for growth companies

In finance, aifinyo creates value by matching the needs of its clients with the funding market.

funding: banks clients: growth companies

Slow decision processes Need small amounts

Ø funding cost ~2%

Ø return ~23%*

Prefer big companies due to rating Fast money preferred due to lack of planning

Focus on big tickets due to high processing cost Used to instant response from retail market

Low level of digitalization Open minded for digital solutions

aifinyo credit decision and processing platform

credit engine with ability

fast due to digital integration cost efficient for small tickets risk transformation

to rate small tickets

*as of 31.12.2020 preliminary / unauditedfocus on short term maturities

average duration - 5 10 15 20 25 30 35

in month

• aifinyo’ s portfolio consists largely of short term maturities

0,83 • 80% of the portfolio with remaining lifetime below 2 month

trade receivables

0,70

• aifinyo actively decreased long term exposure during 2020

• Essentially no interest rate risk

1,60

trade finance

2,03

due to short term portfolio duration aifinyo is able to

lease receivables 2019 32,40

quickly adopt to changing market environment

(covid-19 – one time risk expenses in Q2-20

Corona adjusted risk standards led to significant risk expense improvement in the last quarters.

risk expenses as % of adj. revenues risk expenses as % of adj. revenues

50% 140%

42% 116%

120%

40%

100%

30% 80%

20% covid-19 60%

40% 20% 26%

10% 5% 6% 11%

2% 3% 2% 20%

0% 0%

2015 2016 2017 2018 2019 2020 Q1-20 Q2-20 Q3-20 Q4-20

• Risk costs historically fluctuated due to lower diversification in • Due to short term adjustment in portfolio and credit selection

early years and increased mainly because of shift towards process risk levels came significantly down form Q2 to Q4.

finetrading and freelancer factoring, with higher provisions for

expected defaults. • Risk exposure has been significantly reduced by decrease of

portfolio duration, exit of corona affected industries and focus on

• Risk cost are historically a minor part of adj. revenues (~ 5%) but industries like e-commerce, technology and health care.

increased significantly during covid-19.“aifinyo has a rigorous risk management

with long term experience.”sound equity ratio

25%

20% • aifinyo managed to increase equity ratio over last years

20% to 13% tier 1 and 20% tier 2

17%

• Strong equity ratio provides for favourable debt funding

15% 14% 14%

13% and sufficient risk buffer

12%

10% 9% • Loss in 2020 was entirely offset by capital increases

8%

6% • Due to reduction in balance sheet total equity ratio even

5%

5% increased 2020

• aifinyo considers further capital increases to keep up the

0% equity ratio taking into account expected growth and

2016 2017 2018 2019 2020 software development expenses

tier 1 ratio tier 2 ratio

*based on unaudited, preliminary results for 2020quarterly financial figures 2020/21*

In quick response to corona impact led to rebound of turnover and revenues and significant improvement of EBT.

transaction volume turnover adj. revenues** EBT

in EUR m in EUR m in EUR m In K EUR

Q1/20 Q2/20 Q3/20 Q4/20 Q1/21

83

2,2

10 10

9 1,9 1,9

62 1,8 -304 -204

61 58

56 1,6 -422

-549

6 6

Q1/20 Q2/20 Q3/20 Q4/20 Q1/21 Q1/20 Q2/20 Q3/20 Q4/20 Q1/21 Q1/20 Q2/20 Q3/20 Q4/20 Q1/21 -2.187

• Due to corona less transaction • Loss in revenues mainly due • De-boarding of corona • EBT suffered especially due to

volume especially since Q2 to corona adjusted risk affected clients led to reduced corona related unexpected

measures adj. revenues in Q2 and Q3 losses in Q2 and one time

• Speed of slowdown merger integration cost of

significantly decreased and • Despite reduced transaction • Strong adj. revenues Decimo

rebound in Q4 with +11% volume turnover already back improvement in Q4 and Q1

on pre corona level • Significant EBT improvement

after Q2

*based on preliminary, unaudited results

*net of cost for purchased goods and depreciation for leased assets related to customer lending business5y-key (annual) financial figures

transaction volume turnover adj. revenues* EBT

in EUR m in EUR m in EUR m In K EUR

320 289

44 8,7 44

-208 -917

263 7,5

248 6,8 2016 2017 2018 2019 2020

32

29

185

4,8

124 3,4

14

-3.461

7

2016 2017 2018 2019 2020 2016 2017 2018 2019 2020 2016 2017 2018 2019 2020

aifinyo Decimo total aifinyo Decimo total aifinyo Decimo total aifinyo Decimo total

• Strong growth in transaction • Strong growth as well in • Adj. revenues is most • Despite high IT/R&D

(financing) volume turnover important internal financial spending's aifinyo was always

KPI profitable

• Dominated by factoring, • Dominated by finetrading

followed by finetrading and (gross accounted for in • Revenues are adjusted for • Unexpected losses (~2.5m)

leasing turnover, vs. e.g. factoring cost for purchased goods and and Decimo integration cost

only accounts for the fee) leasing depreciation (~1m) main driver of negative

EBT 2020“aifinyo achieved strong long-term (profitable) growth,

which was recently affected by corona.”covid-19 – long term benefits expected

decrease in competition due to reduction in number of alternative financing will profit

banks expected (German factoring market)

50.000 300

120

45.000 number of clients

100 250

40.000

transaction volume in bn €

80 35.000

200

last 30.000

60 last

recession 25.000 150

40 20.000

recession

100

15.000

20

10.000

50

0 5.000

0 0

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019

2000 2002 2004 2006 2008 2010 2012 2014 2016 2018

expected, that banks will restrict lending

(change in size of corporate credit portfolio)

competition

8%

6%

4% need for consolidation

2%

last

0%

recession demand for alternative financing

-2%

-4%

-6%

-8%

need for unique digital solutions

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019“Post corona will lead to less active players in the market while demand for smart finance solutions will increase.”

share price with upside potential

share price in EUR key facts conferences

number of shares: 3,446,819 MKK/München 03.-04.05.2021

40

market cap: ~ EUR 80 m Börse München 13.10.2021

35

ISIN: DE000A2G8XP9 Eigenkapitalforum 22.-24.11.2021

30

ticker: ebe MKK/München 07.-08.12.2021

25

20 segment: m:access

research

15 indices: m:access All-Share

10 Listing: Frankfurt, Munich, Warburg (08/2020) buy 36.00 EUR

5 Xetra SMC (04/2021) buy 45.80 EUR

0

Dez. 18 Jun. 19 Dez. 19 Jun. 20 Dez. 20 designated sponsor

Warburgstable shareholder structure

shareholder structure shows

trading volume intended to be increased

strong management commitment

Employees

1% Stefan Kempf • Management and founding partners are highly

(Management) committed with a high stake in ownership

Other

24% structure

Investors

(complimentary management team

Finance Tech Sales

Stefan Kempf Prof. Dr. Roland Fassauer Matthias Bommer

Co-partner and founder of aifinyo. Joining aifinyo from Decimo Co-partner and founder of aifinyo.

M.Sc. in Banking and Finance Serial Entrepreneur (INTERSHOP, Masters degree in finance and

as well as a Law Master LL.M. from Pixaco, Mobizcorp), Institute for controlling from the University of

Frankfurt School of Finance. Applied Informatics (InfAI) at the Applied Sciences in Mainz.

University of Leipzig.

Before founding aifinyo, working in Before founding aifinyo, managing

capital markets for a major bank and Expert in machine Learning and director and executive board member

in the German leasing and trade decision Systems. for several German factoring companies.

receivables industry.steps for further growth

building the leading B2B

ecosystem for finance,

payment and processing teaming with

partners

expand product

portfolio

consolidation

brand

opportunitykey takeaways

aifinyo…

• is a fintech pure play on a profitable growth track.

• operates in an billion euro market (only in

Germany).

• is well positioned – due to product range, size and

tech focus – in a consolidating market.

• has sharpened the business model during

corona.

• sees significant revenues and earnings growths in

the coming years with existing and new products.

• works to increase the attractiveness of its share

for investors.disclaimer This presentation contains forward-looking statements. Forward-looking statements are statements that are neither facts nor a description of past events; they comprise statements relating to our assumptions and expectations. Each statement made in this presentation that reflects our intentions, assumptions, expectations or forecasts as well as the underlying presumptions is a forward- looking statement. These statements are based on planning figures, estimates and forecasts currently available to the Board of Directors of aifinyo AG. Accordingly, forward-looking statements refer exclusively to planning data, estimates and forecasts at the time at which they are made. We assume no responsibility to further develop or modify such statements in the event of fresh information being available or future events occurring. By their very nature, forward-looking statements imply risks and uncertainty factors. A large number of key factors can contribute towards actual events varying quite substantially from forward-looking statements. Such factors include the condition of the financial markets and the regional focal points of our investment activities.

contact

aifinyo AG

Tiergartenstraße 8

01219 Dresden

T: 0351 8969 3310

F: 0351 8969 3315

E-Mail: ir@aifinyo.de

Web: www.aifinyo.deYou can also read