Taming a Minsky Cycle - with Emmanuel Farhi

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Webinar Hosted from PRINCETON For EVERYONE, WORLDWIDE Taming a Minsky Cycle Iván Werning with Emmanuel Farhi MIT 11. March 2021 Markus Brunnermeier

Extrapolative Expectations & Bubbles Extrapolative expectations (adapted expectations in growth) E.g. Gennaioli & Shleifer book (distorted beliefs) Potential Momentum Price path Bubbles Bubble starts Fundamental innovation Fundamental value 2

Good vs. bad bubbles New technologies and R&D investments (1998-2000) Overcoming QWERTY (chicken-egg) problems Safe Asset as a bubble (government debt < ) Serves as precautionary savings tool Asset Price = E[PV(cash flows)] + E[PV(service flows)] dividends/interest insurance via re-trading 2 s > 0 < 0 Debt as Safe Asset Brunnermeier-Merkel-Sannikov 2020 Real estate bubbles (2006) Financial innovation/liberalization bubbles BITCOIN 3

Harmless vs. Dangerous Bubbles – how to fight? Equity financed bubbles (1998-2000) Credit financed bubbles (2005-2006) Minsky’s financing classification Hedge borrowing: can pay off whole debt Speculative borrowing: can pay off interest due Ponzi financing 1. Policy makers should “fight” bubbles by a. Leaning against during build-up b. Clean afterwards only 2. Policy makers should “fight” bubbles a. with monetary policy b. primarily with macro-prudential tools c. both 4

Minsky’s bubble phases Potential Price path Bubble Fundamental starts innovation Fundamental value Displacement Boom Euphoria Profit-taking Panic phase phase phase phase 5

Why do rational investor ride rather than attack bubbles? Co-opetition among rational investors Sequential awareness/learning + critical mass Competition: exit bubble before it bursts Kills backwards induction argument Cooperation: ride as long as other ride it common knowledge of bubble Potential Price path Bubble Fundamental starts innovation Fundamental value Mutual knowledge 1. order 2. order 3. order …. 6

Poll Questions 1. Policy makers should “fight” bubbles by a. Leaning against during build-up b. Clean afterwards only 2. Policy makers should “fight” bubbles a. with monetary policy b. primarily with macro-prudential tools c. both 3. Policy makers’ belief distortions and exuberance are a. smaller than the markets’ b. about the same c. Larger than the markets’ 7

Taming a Minsky Cycle Emmanuel Farh Iván Werning March 202 Markus Academy, Princeton 0 i

Macroprudential Policy Macroprudential policies motivation nancial fragilit aggregate demand stabilizatio monetary policy constraints or dilemma Open economy: capital ows, dilemma Farhi-Werning (2013, 2014, 2016) Applications: capital controls, scal unions, deleveragin General model: pecuniary + demand externalitie Formula: MPCs + Wedges (Econometrica 2016 New Today… “Taming a Minsky Cycle” (2020 Minsky Boom Bust Cycle Boom: compolacency, rising asset prices and leverag Bust: “Minsky moment”, risk repricing, deleveragin Non-rational expectations, extrapolation fi y fl s n fi … … s ) ) s g e g

Macroprudential nancial macro decisions impact e.g. credit boom e.g. low return shock high leverage and risk taking lower future loans fi

Macroprudential macropru regulation nancial macro decisions impact e.g. credit boom e.g. low return shock high leverage and risk taking lower future loans fi

Macroprudential macropru regulation nancial macro decisions impact e.g. credit boom e.g. low return shock high leverage and risk taking lower future loans Is there a market failure? Not necessarily. Externality needed. fi

Macroprudential monetary policy? macropru regulation nancial macro decisions impact e.g. credit boom e.g. low return shock high leverage and risk taking lower future loans Is there a market failure? Not necessarily. Externality needed. fi

Macroprudential monetary policy? monetary policy? macropru regulation nancial macro decisions impact e.g. credit boom e.g. low return shock high leverage and risk taking lower future loans Is there a market failure? Not necessarily. Externality needed. fi

Macroprudential nancial macro decisions impact Macropru formula: linked to MPCs and wedge General model: incomplete markets, nancial constraints with prices etc. (pecuniary externalities) fi fi s

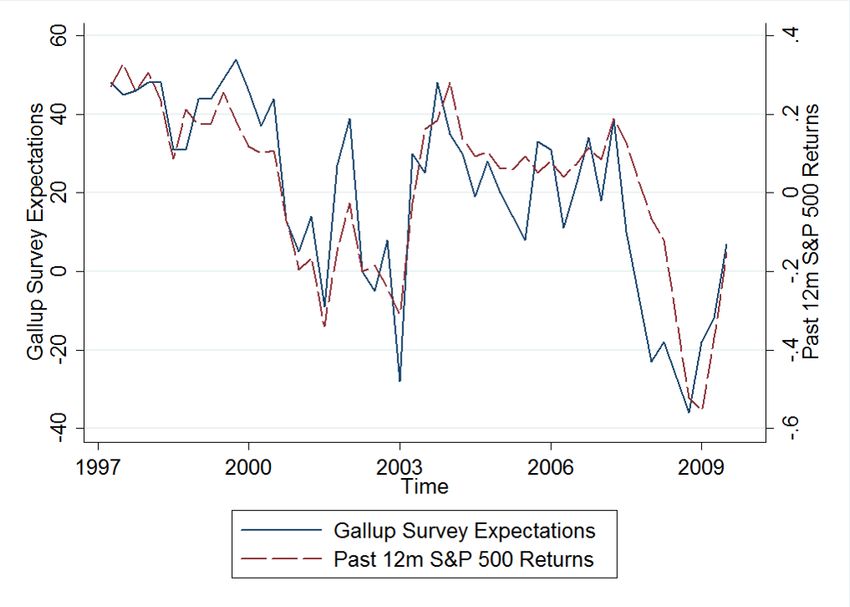

Extrapolative Expectations Greenwood-Sheifer (2014): survey of investor expectations Extrapolation of future stock is Common: Bothreturns Boom correlate & Bust with past returns and level of stock market

Policies to Tame a Minsky Cycle Elements today Monetary with and without macro-pr Macroeconomic vs. nancial stability Targets and instruments a la Tinberge trading off targets with given instrument assignment of targets to instrument Key role of endogeneity of beliefs … fi s s n u s

Minsky Unhappy with neoclassical synthesis; important aspects of Keynes but missing nancial/investmen too rosy on stability prospect Ideas system is endogenously unstable… … perfect stabilization with money and scal policy: impossibl tranquility, seeds the risk taking, that creates boom/ bus nancial markets different than real economy; debt nancing during expansion, turns more speculative fi fi t … e fi s t fi

Minsky in “Stabilizing an Unstable Economy” Boom and role of expectation feedback “Instability emerges as a “unless the past is being “A rise in the price of period of relative tranquil validated […] none but nancial instruments or growth is transformed into a pathological optimists will capital assets may very well speculative boom […] invest.” increase the quantity middlemen in nance demanded […] thus breed change in response to the conditions conductive to success of the economy.” another such rise.” Policy implications for nancial controls… “We need a Theory that “External controls and “It is possible that with other coordinating mechanisms institutional organizations makes instability a may be needed in a and policy systems the normal result in our capitalist economy. Indeed, susceptibility of our economy economy and gives us central banking and other to nancial crises can be handles to control it.” nancial control devices lower than at present” arose as a response to the embarrassing incoherence of nancial markets.” fi fi fi fi fi fi …

Related Literature Monetary Policy: Woodford, Gali, Werning, Eggertson- Krugman, McKay-Nakamura-Steinsson, Auclert; Monetary Policy and Expectations: Farhi-Werning; Angeletos-Lian; Gabaix Macroprudential Policy: Farhi-Werning, Korinek- Simsek, Caballero-Simsek, Bianchi-Mendoza Extrapolative/Diagnostic Expectations: Bordalo- Gennaioli-Shleifer, Maxted … … … …

Monetary Monetary Macropr Rational Expectation + u

Monetary Monetary Macropr Rational IT Expectation + u

Monetary Monetary Macropr IT Rational IT + Expectation Macropru + u

Monetary Monetary Macropr IT Rational IT + Expectation Macropru Extrapolativ Expectations + u e

Monetary Monetary Macropr IT Rational IT + Expectation Macropru Extrapolativ Lean Against Expectations Boom + u e

Monetary Monetary Macropr IT Rational IT + Expectation Macropru I Extrapolativ Lean Against Expectations Boom Macropru + + T u e

Model Ingredients He-Krishnamurthy (2013) (Brunnermeier-Sannikov, 2014 asset pricing model adds nominal rigidities + optimal polic Incomplete markets risky asset (Lucas tree risk-free short-term bon Two agents savers: save risk-fre borrowers invest in risky asse borrow risk-fre Three periods t=0,1, Consumption good produced 1-to-1 with labor Rigid wages, no in ation : … e fl t e … 2 ) d y )

Demand Determined Outpu Endowment (rigid wage) t=0 t=1 t=2 borrowin risky retur ZLB binds realize & investing d g n t

Periods, States and Demographics

Three periods t ∈ {0,1,2}

Aggregate state ω ∈ {H, L}

Determines dividend D2,ω of Lucas tree with

D2,H > D2,L

Agents i ∈ {S, B} share ϕ iPreferences and Technology Technolog t = 0,1 t=2 Preference Borrower Savers s y s

Nominal Rigidities Sticky wages normalized to on Zero Lower Bound (ZLB) binds at t=1, not at t=0 e

Budget Constraints Savers Borrowers

Labor Wedges and Output Gaps Labor Wedge Positive wedges iff negative output ga “Macroeconomic Stability” s p

Debt as a State Variable Savings of savers b1S (debt of borrowers) state variable at t= Asset price and output… 1

Debt as a State Variable Savings of savers b1S (debt of borrowers) state variable at t= Asset price and output… Financial Fragility: two intuitions higher debt lower risk-taking capacity higher risk premia lower asset price lower consumptio higher debt higher precautionary motive lower natural rate lower consumptio Risk always key here; without it, no effect. 1 n … n

Value Functions and AD Externality S Allocation pinned down by b1 S S B S Value functions V (b1 ) and V (b1 ) Aggregate demand externality if recession at t=1 (compare MRS of planner to agents’) Externality Social Marginal Utilities ≠ Private Marginal Utilities

Monetary Policy Focus on Pareto weights that neutralize distributive objectives (λ S /λ B = c0S /c0B) Optimal monetary policy targeting rul Lean against boom (μ0 < 0) iff borrowers initially S levered (b0 > 0 S Benchmark with b0 = 0 gives standard “in ation targeting” (IT) ) e fl

Monetary Monetary Macropr Rational IT Expectation Extrapolativ Expectations + u e

Monetary Policy an Macropru Optimal monetary policy targeting rul Macroprudential tax on borrower leverag Assignment of targets to instruments: macro stability to monetary polic nancial stability to macroprudential policy fi y e e

Monetary Monetary Macropr IT Rational IT + Expectation Macropru Extrapolativ Expectations + u e

Extrapolative Expectations Introduce extrapolative expectations by borrower Modeled by either wedge in investor Euler equation o subjective probabilities s … r

AD and Belief Externality AD and Belief Externalit Belief externality reinforces AD externality as B,e B long as borrowers optimistic (c1 > c1 ) in equilibriu This will be the case. m y

Monetary Policy Optimal Monetary Policy targeting rul Lean against boom (μ0 < 0) if extrapolative expectations e

Intuition “Take the punch bowl away when the party is still going” Contractionary Monetary Policy cools economy during boo cools expectations of return cools borrowin low borrowing bene cial in future Extrapolative expectations important g fi m s …

Monetary Monetary Macropr IT Rational IT + Expectation Macropru Extrapolativ Lean against Expectations Boom ? + u e

Monetary+Macropru Optimal monetary policy again Macropru tax borrower leverag Assignment of targets to instrument monetary: macro stability nancial stability: macropru fi e … s

Monetary Monetary Macropr IT Rational IT + Expectation Macropru I Extrapolativ Lean Against Expectations Boom Macropru + + T u e

Extrapolative Expectations During Bust Before: only extrapolative during t = 0; rationality kicks in at t = 1 (“Minsky moment” Now: extrapolative also during bus Two state variables leverage (as before beliefs affected by past asset prices (new Two-dimensional nancial stabilit monetary policy alone: additional reason to lean against the wind at t = 0… …remains true with macropru policy fi ) … y t ) )

Monetary Monetary Macropr IT Rational IT + Expectation Macropru I Extrapolation Extrapolativ Lean Against during Bust Expectations Boom Macropru Lean Against Boom + + T u : e

Conclusion General theory of macropru + monetary polic workhorse for many applications general formula: MPCs and wedge Minksy Cycles with non-Rational Expectations expectation management: interventions attempt to mitigate nancial crashes in price dilemma: may affect monetary polic modi es optimal policy responses (targets and instruments) fi fi s s y y

You can also read