Starbucks TATA Alliance Marketing Strategy - By Martina Kancheva University of Bath

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Starbucks‐TATA Alliance Marketing Strategy

By Martina Kancheva

University of Bath

According to the Harvard Business School, after Starbucks first entered one of the most tea

loving countries (England) in 1998, tea sales fell even as coffee sales rose rapidly. By 2008,

annual sales of coffee in Britain had exceeded sales of tea. India, where Starbucks plans to

penetrate this year, is also not a habitual coffee drinking nation. The current paper aims to

propose a strategy for entering the Indian market while the taking into account local tastes

and lifestyle.

The analysis begin with an overview of the Indian Coffee Retail Market; continues with

examining the strengths of the Starbucks brand and the benefits of a joint venture with the

India's largest coffee producer and exporter. The report will finally propose the most

effective marketing strategy for Starbucks to enter the Indian coffee industry and get a piece

of the 'market pie'.

1. Situation Analysis of the Indian Coffee Retail Market

As coffee shops may be nearing saturation point in the US and Europe, Starbucks has

identified the potential to expand in emerging markets like China and India. The coffee

industry is expected to continue growing through at least the year 2015 and even longer in

emerging markets (Lingle 2007).

As there no framework that provides a full

picture of the dynamics within a particular

market, a more holistic approach will be

adopted. Economic, Legal and Socio‐cultural

factors will be examined from a PESTEL analysis

and the Power of Suppliers, the Threat of

Competitors and the Threat of Substitutes from

the Porter Five Model.

Picture 1: Porter’s Five Forces Model

1.1. Economic Factors

2

The Indian economy will expand an estimated 6.5 percent this year, the fastest pace among

developing Asian economies excluding China, according to January estimates from the World

Bank (Agrawal and Sharma, Bloomberg 2012). The Reserve Bank of India projects seven

percent growth for the twelve months ending March. As sales contribution in the US has

declined in the past decade to less than 70% in the last fiscal year, Starbucks is expanding in

fast developing markets like China and India.

India is one of the emerging markets throughout the world that is becoming a spending

oriented country. The personal disposable income per capita in India has doubled between

2000‐01 and 2009‐10 resulting in improved purchasing power (Deloitte 2011). Thus, its

upper and middle classes are more able to spend money on coffee, beverages and food in

coffee houses that might not have been though of as a necessity in the past.

1.2. Legal Factors

India’s government on January the 10th raised the ownership limit to 100% for foreign

retailers selling a single brand, a decision benefiting companies including Starbucks

(Passport, Euromonitor 2011). However, Starbucks and TATA will possess equal shares in the

venture as both companies will both benefit from such an alliance.

1.3. Socio‐Cultural Factors

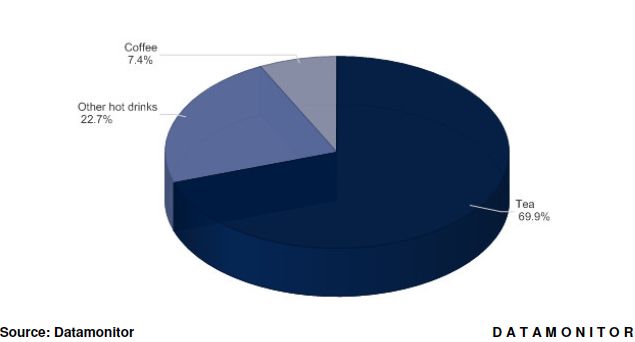

India is a “traditional tea drinking nation” (Vasudha 2011, pp. 2) which is proven by the fact

that 69.9% of the hot drinks market is dominated by the tea industry (Figure 1).

3Figure 1. India Hot Drinks Market Segmentation

Even though in India tea was the common beverage for the upper and middle classes, now

coffee is becoming a statement of wealth and prosperity among the traditional sector of the

Indian population, i.e. people more resistant to changes (aged above 30) (Bose, Reuters

2012). This phenomenon might be explained by the fact that as more and more economies

head towards industrialization, those economies also begin to be influenced by

westernization.

Westernization is also easily adopted by the younger generation in India (18‐25 years).

Research shows that 72% of coffee shops customers are students and young professionals

(Euromonitor 2011). The popularity of specialist coffee shops among youths as a place to

socialise registered 18% growth in 2010; with average time spent on a table higher that in

other countries. Spending capacity of youth of India is increasing, as well as their brand

consciousness. 60% of India’s population is below the age of 30 leading to popularization of

brands and products (Deloitte 2011).

As illustrated above, there is a market potential subject to ‘dual economies’, i.e. targeting

both the modern sector (youths) and the traditional sector (nationalistic individuals resistant

to changes) (Nuttall 2011).

4In the process assessing the growth opportunities in the specialty coffee industry, one must

also examine the competitive landscape.

1.4. Bargaining Power of Suppliers

The major threat in the specialty coffee industry is the power that suppliers have over the

price of coffee. Arabica coffee prices soared 77% in 2010 which caused concerns to coffee

retailers (Murphy 2011). Arabica coffee is one of the most sold brands of coffee in the

specialty coffee industry. With prices for that type of coffee sky rocketing, it hurt the bottom

line of competitors, especially those that thrive on a low cost strategy. However, Starbucks

strategy can be regarded as ‘charging premium price for premium product’; and it is

supplying coffee form their partner, so the power of suppliers can be regarded as weak.

1.5. Competitive Rivalry within the Industry

The second threat is from specialty coffee competitors that Starbucks will face when it

enters the Indian market. Well‐established coffee shops chains, such as Café Coffee Day

(CCD) and Barista, enhanced their pan‐India presence in 2011. In 2010, CCD and Barista had

970 and 200 stores, respectively, and they aim to continue expanding in the next few years

(Datamonitor 2010). Meanwhile, several relatively new players, such as Costa Coffee, Coffee

Bean, Gloria Jean’s and Java Coffee, are trying to ‘get a piece of the pie’ in Indian coffee

retailing. Both these factors drove on‐trade consumption of fresh coffee beans in 2010, with

volumes growing by 12% (Datamonitor 2010). On‐trade sales have emerged as the primary

sales channel for fresh coffee beans, in the absence of any substantial off‐trade

consumption. However, “the popular opinion was that with only about 1 500 cafes the INR

20 billion market provided enough room for growth and could accommodate more players.”

(Vasudha 2011) Even that major players started expanding, there is potential for further

growth in the Indian Coffee Retail Market.

51.6. Threat of Substitute Products

A third relevant threat in the case of Starbucks entering India is the threat of substitute

goods. For instance, consumers may opt to reduce their caffeine intake due to health

concerns, which will influence coffee consumption somewhat. In such case, herbal tea and

functional drinks can be potential substitutes. However, considering the increased

consumption of coffee in recent years, it is unlikely that such substitution would

substantially impact upon sales. Overall, the threat of substitutes in the Indian coffee market

might be considered as moderate.

2. Starbucks

This section aims to examine the strengths of the Starbucks brand and critically evaluate the

rationale behind their alliance with TATA.

2.1. SWOT Analysis

SWOT analysis will be used to evaluate Starbucks’s Strengths, Weaknesses, Opportunities

and Threats.

Strengths Weaknesses

‐ Leading retailer and roaster for brand ‐ High pricing which not everyone can

specialty coffee in the world; afford;

‐ Brand image with the motto ‘The ‐ Starbucks refuses to guarantee that milk,

Starbucks Experience’; beverages, chocolate, ice cream, and

‐ 17 000 stores across 57 countries; 1 500 baked goods sold in the company’s stores

in China alone; are free of genetically‐modified

‐ Strong balance sheet; ingredients;

‐ One of the strongest franchises in the ‐ Focused more on US domestic market;

world with more than 6 500 licenses ‐ Starbucks Workers Union was made

6shops in the world; because some employees complain

‐ Starbucks is known for providing superior about the management style within the

products and services; company;

‐ Have loyal customers in every country ‐ No experience in countries like India.

that has entered;

‐ Sophisticated atmosphere, music,

interior design and artwork;

‐ Have a lot of flavours variation;

‐ Limited number of strong competitors;

‐ High market share and market growth.

Opportunities Threats

‐ High consumerism in emerging markets; ‐ Global financial crisis made people spend

‐ Easier to penetrate market because less on good that are not regarded as

Starbucks is selling as experience, not necessities;

just a simple product; ‐ Increasing health concern of the negative

‐ Many of Starbucks coffee are using effect of coffee;

organic beans; ‐ Starbucks domination is driving small

‐ Some of Starbucks’s beans are harvested cafes out of the business;

in Indonesia island of Sumatra and ‐ Threat of substitute products in cultures

Sulawesi. Starbucks are purchasing at where there is a strong preference for

premium prices to support local tea, like China, India and UK.

community and sustainable production.

Starbucks pays an average price of $1.20

per pound against the commodity

average price of $0.40 – 0.50 per pound;

‐ Fair Trade Products can be offered.

Table 1: Starbuck’s SWOT Analysis

After examining the strength of the Starbucks company, one should examine the strengths

of the joint venture that Starbucks will enter with TATA Global Beverages Group.

72.2. The Joint Venture with Tata

Starbucks entering into the Indian market will be in the form of 50/50 joint venture with the

TATA Global Beverages Group. “Share prices of both companies soared following the

announcement of the pact.” (Vasudha 2011, pp. 10) This is the first time Starbucks is

entering the market with a local partner and will be co‐branding their stores and products

with their counterpart. The Indian outlets will be called Starbucks TATA Alliance. The

partnership will enable an expanded range of beverage offerings for Indian consumers. One

of these being the Starbucks’s premium tea product Tazo that will be available in Indian

outlets renamed as TATA Tazo Tea.

The major advantage of the alliance will be that “the knowledge and understanding of the

Indian market can be brought by TATA Global Beverages.” (Vasudha 2011, pp.10) Entering

into a strategic pact with “the world’s largest integrated coffee plantation company” should

enable Starbucks to ensure sustainable profit growth in India. Also, TATA Tea is the tea

market leader with 18.4% share. Starbucks will also benefit from TATA’s experience in the

Indian market regarding different tastes in different regions; thus making sure it offers the

most preferable blend of both tea and coffee to customers.

Apart from product and local preferences knowledge, Starbucks will benefit from TATA

Global’s infrastructure. In India, there is the challenge of balancing higher rentals and

profitability given the lack of infrastructure in India along with inflating real estate prices.

Starbucks is a step ahead of competitors due to their alliance with TATA Global Group. TATA

has a local knowledge on the real estate market and they have opportunities to leverage

their capabilities in this area. Starbucks will be able to use TATA’s current infrastructure to

effectively grow the business.

TATA Group will also benefit from the pact. TATA’s experience in retailing is not sufficient to

open a coffee retail shop on their own; so, by entering in such alliance they will gain a vast

amount of knowledge. Also, TATA Global Beverages produces bottled Himalayan water

which might be offered in Starbucks stores around the world.

8Starbucks should also consider the possible disadvantages of such joint venture. After

gaining enough knowledge in retailing industry and knowing the Indian market better, TATA

might decide to compete with Starbucks instead of working with them. In addition, potential

conflict might occur regarding the strategy of the alliance and how it should be managed.

Such joint ventures might also accrue significant costs of control and coordination; and on

top of that, profit is shared with a partner.

3. Marketing Strategy

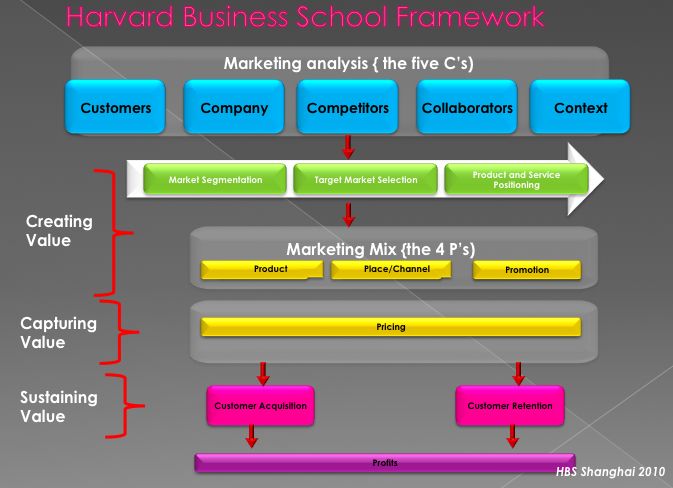

The Harvard Business School Framework (Figure 2) (Comrie 2012) will be used as a model to

explain the marketing strategy in the current proposal.

Figure 2. Harvard Business School Framework

The marketing analysis was conducted in Section 1.

93.1. Capture Value

In this section, tools and techniques will be used to explain how Starbucks can create and

capture value for their products.

3.1.1. Market Segmentation

Apart from the demographic characteristics presented in part one of the analysis, marketers

should also consider psychographic variables such as interests and lifestyles. In general,

India’s coffee culture has changed the way young Indians socialise. In a country where there

is a limited bar culture, and where drinking alcohol is still not allowed in many circles, it has

provided an acceptable and safe outlet for people, particularly young Indians, to share a

drink (Vaidyananthan, BBC 2012).

As mentioned earlier, coffee is becoming a statement of wealth and prosperity among

people with high disposal income, i.e. individuals in employment.

3.1.2. Target Market Selection

The marketing strategy will focus on targeting both groups – college and university students

(aged 18‐25) in the short term and working professionals (25‐40) in the medium to long run.

Also, tourist and frequent flyers will be a target audience in the long‐run.

3.1.3. Product and Service Positioning

It is essential to have a unique selling point to position Starbucks above competitors

(Pickton 2005). In TATA‐Starbucks customers will be able to rely on genuine service, an

inviting atmosphere and a superb cup of premium coffee or tea every time.

103.2. Set Marketing Objectives

In order to make the marketing communications objectives as comprehensive as possible,

the SMART approach has been used, to ensure the objectives are specific, measurable,

achievable, realistic, timed and targeted:

The proposed strategy provides a plan for TATA‐Starbucks to open 50 stores by the end of

2012 in major metro cities and second‐tier towns offering premium coffee experience to the

primary target group of students (aged 18‐25) and working professionals (aged 25‐40).

3.3. Marketing Mix (4 Ps)

The marketing mix will be examined to determine Starbucks‐TATA unique selling points, i.e.

the unique qualities that will differentiate their products and services from those of

competitors.

3.3.1. Product

Anil Dharker (2012), a Mumbian columnist and social commentator in India, points out that

when a foreign player sees a commercial opportunity and enters the new market; and then

it adapts giving McDonalds as an example (Vaidyanathan, BBC 2012). However, this should

not be the case and Starbucks should have a clear strategy about their product range (both

drinks and food) it is going to offer prior entering the Indian market. Costa Coffee Shops in

India, for instance, offers products like Apple Pie Latte, Latte Caramellato, Coconut Hot

Chocolate, etc. suited for Indian taste (Costa Coffee India online 2012). Therefore, Starbucks

should adapt their drinks in order to cater local preferences. Ice coffees should also be

included in Starbucks’s menu as Indians have a strong preference for them because of high

temperatures during summer.

However, one should not ignore the fact that India is a tea loving country even though

people “prefer to consume tea at home because finding a perfect cup of chai outside is

11really tough," said Smiti Singh, a Bangalore‐based software engineer, who drinks at least

four cups of tea a day (Madhok, Reuters 2012). TATA Tea (a unit of the software‐to‐steel

TATA conglomerate) is the world’s second‐largest branded tea company, so their premium

tea products should be also offered to customers apart form the Tazo Tea.

The biggest distinction is north India's preference for bread, meat, and chai (tea), compared

to the south's preference for rice, pulses, and coffee. Food‐wise, paninis, sandwiches and

wraps with meat but not with beef. The cow is considered sacred by most Hindus and hence

beef is considered taboo in the majority of Indian states. Predominant food option in the

south should be the bistro boxes with rice and pulses.

3.3.2. Place

The first Starbucks locations are scheduled to open in August in New Delhi and Mumbai.

TATA Starbucks might consider the option of opening on the 15th of August, India’s

Independence Day. Starbucks‐TATA partnership is expected to open 50 stores in the country

by the end of 2012. Starbucks also plan to explore the retail properties of Croma, Star

Bazaar, Trent and Indian Hotels belonging to the TATA Group to open stores and also to

“rope in another franchisee for standalone cafes in the future.” (Vasudha 2011) This is an

efficient way of targeting individuals on business trips in New Delhi, for instance, who prefer

to go to a place which is familiar for a cup of coffee; or tourists, who do not want to

experience the local culture. As an international brand, Starbucks should also open kiosks at

airports; thus, not depending solely on Indian tastes and preferences as airports are

occupied with people from all over the world, who will recognise the Starbucks logo.

In Mumbai (most populous city in India) Starbucks should position the stores mainly in

shopping centres, cinemas, near universities or cultural venues as it is commercial and

entertainment capital of India.

Coffee shops normally close around eleven o’clock at night, so Starbucks should consider the

option of closing at midnight or even one o’clock in the morning; thus, becoming the

12preferred venue for young people. Also, providing some guitar for jam sessions or karaoke

nights on Friday or Saturday may attract even more people.

As coffee chains are seen as places to socialise and people aged 25‐40 will be also a target

group of the Indian population, Starbucks may consider opening a new type of Starbucks

coffee called Starbucks Lounge, for example. The atmosphere in the lounges will be more

relaxed and the interior more expensive; thus wealthy individuals will be able to show their

class.

In general, experts felt that largest café chains in India like CCD, Barista Coffee and Qwiky’s

are targeting the same locations, mainly the large cities. Geographical expansion has huge

possibilities as cities are not saturated and the market is not limiting at all. Therefore,

Starbucks‐TATA should aim to gain competitive advantage in smaller cities as well in the

medium to long rum as people there are more likely to be brand‐loyal as opposed to

customers in cosmopolitan cities.

3.3.3. Promotion

Promotional activities will not be analysed in details as they should be in line with Starbucks

promotions worldwide. Besides, retailers in India rely heavily on word‐of‐mouth (personal

communication). The Starbucks Card will be introduced – a convenient way to pay for your

drinks and earn rewards for your purchase. Furthermore, “in‐store promotions accompanied

by new products such as drinks and accessories sourced from the regions” should be present

in India as well (Vasudha 2011).

Even though it is highly unlikely for a coffee chain in India to advertise on TV, Starbucks

might consider that idea. In the US, there are three places that the average American spend

his time during weekdays ‐ at home, in the work place and in Starbucks. So, they should

somehow show the western lifestyle to the Indian and a TV advertisement at the day of the

launch should do the job.

13Furthermore, it is the first 50/50 joint venture for Starbucks; so, both Starbucks and TATA

Group will benefit from co‐marketing activities.

3.3.4. Price

Historically Starbucks has retained it US pricing model in almost every market they have

entered, but should they follow the same pattern in India? Starbucks should adopt their

pricing based on the demand form the Indian consumer. After analysing analysed the Indian

market for hot drinks and the price elasticity of products, probably the prices of products

should be at least 30% lower than in the US.

Conclusion

If Starbucks can adapt to the peculiarities of the Indian market, coffee may soon become

many Indians’ cup of tea.

Based on the analysis presented above, the current proposal contradicts Levitt’s

globalisation theory suggesting that “companies must learn to operate as if the world were

one large market – ignoring superficial regional and national differences.” (Levitt 1983, pp.

92) In India “F&B and retail typically is very close to local culture and taste” (Vasudha 2011);

thus, the so adaptation or ‘glocalisation’ strategy should be adopted (Robertson 1994).

Glocalisation will serve as a mean of combining the successful Starbucks strategy in

“providing the emotional needs around the world” (Vasudha 2011) while taking into account

local tastes.

14Bibliography

Agrawal A. and Sharma M. (2012). Starbucks, Tata Venture to Open First India Store

by August. Bloomberg, January 31, 2012.

Bose N. (2012). Starbucks to enter India, targets 50 oulets by year‐end. Reuters,

Junuary 30, 2012.

Cormie C. (2012). Tales from the frontline. Getting tactical (Lecture). University of

Bath.

Costa Coffee India online. Available at:

www.costacoffee.co.in [Accessed on: 12 April 2012].

Datamonitor (2010). Hot Drinks in India (0102‐0803).

Deloitte (2011). Indian Retail Market. Embracing a new trajectory. UK.

Euromonitor International (2011). Coffee – India.

Levitt T. (1983). The globalization of markets. Harvard Business Review, pp. 92 ‐102.

Lingle R. (2007). State of the specialty coffee industry: Small Business Advice, July 1,

2007.

Madhok D. (2012). Chai cafes woo coffee fans in urban India. Reuters, February 8,

2012.

Murphy P. (2011). Brazil could be world number one coffee drinker by 2012. Reuters

Business & Financial News, Breaking US & International News, January 26, 2011.

Nuttall P. (2012). Emerging Markets (Lecture). University of Bath.

15Pickton, D. (2005). Integrated marketing communications. 2nd ed. New York: Prentice

Hall/Financial Times.

Robertson (1994). Globalisation or glocalisation? Journal of International

Communication, 1 (1).

Vaidyanathan R. (2012). Coffee v tea: Is India falling for the cappuccino? BBC,

February 9, 2012.

Vasudha M. (2011). Starbucks Alliance: Brewing a Fresh Strategy for India. Bangalore:

AMITY Research Centers (115879).

16You can also read