State of the Markets 2017 - The Early Harvest Second Quarter 2017 - Deloitte UK

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

State of the Markets 2017 The Early Harvest Second Quarter 2017

State of the Markets: Second Quarter 2017

Four months in, 2017 is shaping up to be a year of harvesting and replanting for the innovation economy.

The SVB team examined the private-company growth propelled by the large capital raises of 2014-15 and the

subsequent plunge in large investments and exits in 2016. Given the activity we’ve seen in the first quarter

of 2017, we are forecasting significant harvesting of returns resulting from the last decade of sweeping

innovations.

We predict many private companies will find numerous avenues open in 2017 for raising cash. For those

companies with the strongest growth stories ― those who are reaching their previously frothy valuations ― the

public equity market, sparingly available in 2016, is opening to new issuances. For companies still growing into

their private valuations, yet in need of capital, there are exceedingly well-capitalized private equity firms

seeking buyout opportunities.

Further, as technology accelerates disruption of incumbent business models, we expect an increase in strategic

corporate acquisitions — designed in many cases to help the corporates stay relevant in the 21st century.

But 2017 isn’t only about harvesting returns. Venture capitalists, flush with cash after raising $42 billion in

2016, will have many opportunities to fund the next crop of innovative companies that are poised to drive

disruption for the next decade.

State of the Markets 2

State of the Markets: Second Quarter 2017

1 Predictions: Year to Date

2 Market Dynamics

3 Decisions Ahead for Late Stage

4 The Early Harvest: IPO Conditions

5 Encouraging Outlook for UK

6 Closing Thoughts

State of the Markets 3

Preliminary Grades on 2017 Predictions

The themes of 2016 have provided reliable insight into what 2017 holds for the venture landscape.

But risks remain: Unexpected economic or geopolitical events could shock the innovation economy.

Q1 Predictions Q2 Updates

With plenty of capital in VC war chests, valuations Early indications for 2017 point toward a

remain stable across early stages but fall in later Valuations plateau in valuations, as comparable capital

stages without crossover participation. levels flow to fewer deals.

With public company valuation confidence After a slow start to 2017 following the U.S.

restored and a stable of maturing unicorns, 2017 IPOs presidential election, IPOs have picked up steam.

sees 2 to 3 times the number of IPOs as 2016. Bellwether Snap Inc. successfully listed in March.

Tech giants’ spending spree reaches the Two unicorns were acquired in Q1’17 — as many as

VC-backed ecosystem but with mixed success M&A went public. Expect future deals both explosive

compared to the most recent private valuation. (AppDynamics, $3.6B) and tame (SimpliVity,

Market

Dynamics

State of the Markets 5Post-Election Rally Reaches New Peaks

The bull run in U.S equities showed no signs of slowing post-election, touching all-time highs even in the

face of fiscal policy stumbles and geopolitical uncertainty.

Nasdaq Composite Index: Q2’16–Q1’17

7000

Post 2016 Election: • U.S. investment

+14% incentives

6500

• Tax reform

6000

5500 • Geopolitical

concerns

Year 2000 Peak • Reduced trade

5000

and/or immigration

• Rising rates

4500

4000

April May June July Aug. Sept. Oct. Nov. Dec. Jan. Feb. Mar.

2016 2017

Source: S&P Capital IQ. State of the Markets 6The Federal Reserve Tightens Monetary Policy

Strong economic growth indicators in the United States have led the Fed to hike rates three times since

October 2015, departing from a decade of dovish interest rates. The market believes there are more to come.

Fed Funds Effective Overnight Rate: Q2’07–Q1’17 Probability of a Rate Hike based on Fed Funds Futures:

As of 3/31/2017

6%

80.0%

5%

63.0%

4% 56.7%

3%

2%

Three rate hikes

in the last 18 months 13.3%

1%

0%

April Jan. Jan. Jan. Jan. Jan.

May June July Sept.

2007 2009 2011 2013 2015 2017

Sources: S&P Capital IQ and Bloomberg. State of the Markets 7Rising Rates Lead to Real Capital Movement

As the sun sets on an era of historically low rates, fund managers are once again able to find yields in

debt instruments. Investors in Q1’17 clamored for floating-rate corporate loans, which perform well in

rising interest rate environments, with outsized demand actually reducing the cost of borrowing for

firms. This led to the highest quarterly volume of repricings in the last 15 years.

Quarterly Volume of Corporate Leveraged-Loan Repricing: Q1’02–Q1’17

$250B

$200B

$150B

$100B

$50B

$0B

Adopted from: Wirz, Matt. “U.S. Firms Slash Interest Tab in $100 Billion Refinancing Blitz.” The Wall Street Journal. Feb. 8, 2017.

https://www.wsj.com/articles/u-s-firms-slash-interest-tab-in-100-billion-refinancing-blitz-1486549801

Data source: Leveraged Commentary and Data, an offering of S&P Global Market Intelligence. State of the Markets 8Decisions Ahead

for Late Stage

State of the Markets 9Froth Subsides from an Otherwise Healthy Ecosystem

As crossover investors chase returns elsewhere, $100M-plus rounds are again something of a rarity.

Late-stage companies, which may have otherwise continued to rely on growth capital, will face

decisions as to how to adapt to a shifted landscape.

Venture Capital Invested in Information Technology by Round Size: 2012–Q1’17

$20B

Split by Round Size:

$100–999M $1B+

$18B

$25–50M $50–100M

$0–9M $10–24M

$16B

$14B

$12B

$100M+ Rounds $10B

$8B

$6B

$4B

$2B

$0B

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1

2012 2013 2014 2015 2016 2017

Source: PitchBook. State of the Markets 10Options Available to the Late Stage

Lacking the crossover mega-rounds of 2014 and 2015, which extended private runway, today’s late-stage

ventures face a familiar assortment of possibilities worth exploring ― some more lucrative than others.

$100M+ Financial Strategic

Rounds Buyers IPO

Buyers

State of the Markets 11Turning to Strategic Investors ― Sell or Raise?

Consolidation continues as tech giants look for inorganic growth and accelerated access to hot

markets — particularly autotech and developer tools. Many of these acquisitions were of publicly

traded companies, including the four largest: NXP, LinkedIn, Mobileye and NetSuite.1

Notable Strategics’ $200M+ Acquisitions: 2016–Q1’17 Most Active CVC’s Deal Participation: 2016–Q1’17

90

Apple Alphabet Microsoft Split by Total Round Size:

Deals $50M+ DealsNames to Know in Private Equity

Private equity took notice of steep declines in tech valuations in mid-2016, prompting a string of

acquisitions. Be on the lookout for more investment following new fundraising in 2016 and 2017.

Notable Private Equity Firms: Technology

Vista KKR Insight Thoma Bravo Silver Lake

Equity Partners Venture Partners

Austin, TX New York, NY New York, NY Chicago, IL Menlo Park, CA

HQ

Fundraise

$10.5B $13.9B $6.0B $7.6B $15.0B

March 2017 March 2017 In Process1 Sept. 2016 April 2017

$1.8B Acquisition Series G2 Series F Minority Investment $24B MBO2 / $67B Acq.2

Notable Investments

May 2016 Apr. 2017 Jun. 2014 Apr. 2017 Feb. 2013 / Oct. 2015

$1.6B Acquisition Series C2 Series D $3.0B Acquisition Series G

April 2016 Feb. 2016 Oct. 2015 June 2016 March 2017

$1.5B Acquisition Series D2 Series C $2.4B Acquisition Growth Financing

Sept. 2016 June 2016 April 2017 Dec. 2014 Aug. 2015

1. According to The PE Hub; March 7, 2017.

2. Denotes participation.

Sources: Company websites, Crunchbase, Bloomberg, The PE Hub, S&P Capital IQ and PitchBook. State of the Markets 13What Does It Take to Go Public Today?

Despite investor sentiment shifting away from “growth at all costs,” all 11 of the most recently

announced cloud software offerings were unprofitable as of their S-1 filing. In fact, just two exceeded

the “Rule of 40”* guideline for measuring software-as-a-service company growth vs. profitability.

Selected Metrics from Last 11 SaaS S-1 Filings: 2016–Q1’17

100%

Listed

Filed Okta3 90%

Twilio5

Acquired

80%

Coupa4

MuleSoft2 70%

Revenue Growth

Cloudera1 Alteryx2 60%

AppDynamics3

BlackLine4 50%

Yext3 40%

Everbridge4 30%

Notes: Apptio4 20%

1. Growth: Fiscal Year 2017 vs. Fiscal Year 2016; Margin: Fiscal Year 2017

2. Growth: Full Year 2016 vs. Full Year 2015; Margin: Full Year 2016

3. Growth: 9 months ended Oct. 31, 2016 vs. 9 months ended Oct. 31, 2015; Margin: 9 months ended Oct. 31, 2016 10%

4. Growth: 6 months ended June 30, 2016 vs. 6 months ended June 30, 2015; Margin: 6 months ended June 30, 2016

5. Growth: Full Year 2015 vs. Full Year 2016; Margin: Full Year 2015

0%

-80% -70% -60% -50% -40% -30% -20% -10% 0%

Operating Margin

*The “Rule of 40” is a guideline for software-as-a-service companies to manage growth (approximated by revenue) in

sacrifice of profitability (approximated by operating margin). Growth rate + profitability should exceed 40%.

For further reading: http://feld.com/archives/2015/02/rule-40-healthy-saas-company.html

Source: Company SEC filings. State of the Markets 14The Early Harvest:

IPO Conditions

State of the Markets 15Multiples Climb Following 2016 M&A Blitz

Cloud software companies continue to ride a wave of restored confidence in valuation metrics as they

enter the public market. After a post-election pause at the start of the year, as of March 31, 2017 two

cloud software companies had successfully listed and three more had filed: Okta, Yext and Cloudera.

NTM Revenue Multiples1

10.0x Shopify: 11x Atlassian: 12x Twilio: 10x Coupa: 12x MuleSoft: 12x

Box

Q2-Q3 Cloud M&A

Cloud IPOs2

8.0x

BVP Cloud Index Demandware Alteryx

Constituents (Median)

6.0x

Instructure LinkedIn Apptio

4.0x

Xactly

Opower

2.0x

6-Month Gap Restored

“Good Times”

Between IPOs Confidence

0.0x

Jan. ’15 April ’15 July ’15 Oct. ’15 Jan. ’16 April ’16 July ’16 Oct. ’16 Jan. ’17

1. NTM revenue multiples for IPOs based on earliest estimates, adjusted to IPO date.

2. Multiples above 10x at IPO are represented with an arrow.

Sources: S&P Capital IQ and Bessemer Venture Partners. State of the Markets 16Recent Listings Exceed Their Private Values

The success of recent IPOs serves as an indication of public market confidence. These companies

represent a diverse range of sectors ― from social media and adtech to communications hardware.

Market Cap Relative to Last Private Round for Venture-Backed Tech Companies Listing in 2016–Q1’17:

As of 3/31/2017

+1061% +423%

200%

IPO Date: 2016

2017

150%

100%

50%

0%

-50%

Acacia Impinj Twilio MuleSoft The Trade Quantenna Coupa Nutanix Snap Everspin Alteryx Apptio

.Comm. Desk .Comm. .Tech.

Includes venture-backed technology companies with available private valuation data within five years of IPO.

Sources: PitchBook and S&P Capital IQ. State of the Markets 17Markets’ Calm Waters Ideal for IPO Plunges

After the 2016 U.S. election, the VIX experienced its longest streak of sub-15 closes since 2007.

Despite this period of calm, just two technology companies priced in the three months following the

election. Snap broke that streak with its $3.4 billion capital raise in early March.

90

VIX Volatility Index (Daily) vs. U.S. Tech IPO Count (Semiannual): 2007–Q1’17

80

70

60

50

2016

Election

40

30

20

10

IPO

23 25 2 1 4 2 13 11 16 10 20 10 16 16 23 9 10 7 3 13 4 Count

0

Jan/07 2007 Jan/08 2008 Jan/09 2009 Jan/10 2010 Jan/11 2011 Jan/12 2012 Jan/13 2013 Jan/14 2014 Jan/15 2015 Jan/16 2016 Jan/17Q1’17

Sources: S&P Capital IQ and Yahoo! Finance. State of the Markets 18Field of $1B+ IPO Candidates Remains Crowded

Snap’s IPO was just the third U.S. tech debut greater than $10 billion since Facebook’s 2012 offering.

Seven others have attained that lofty valuation through private funding, with another 82 above $1 billion.

U.S. Tech IPOs with Market Caps $1B+ Sized by First-Day Market Cap or Last Private Valuation: 2012–Q1’17

2012 2013 2014 2015 2016 2017 …and Beyond1

Q1

Q3

Q4 x13

x30

x35

1. For illustrative purposes only.

Sources: S&P Capital IQ and The Wall Street Journal. State of the Markets 19Encouraging

Outlook for UK

State of the Markets 20UK Shows Vitality in European Venture Landscape

While the long-term impacts of the decision to leave the EU are yet to be seen, the period following last

summer’s referendum saw no significant drop in deal numbers. 1 In fact, recent figures revealed UK tech

firms received more venture capital investment than any other European country post-referendum.2

European Venture Activity by Region: Q1’17 European Venture Activity by Metro (Top 5): Q1’17

Deal Value Deal Count

100% Metro Area Deal Count Deal Value

90%

UK/Ireland

London 118 €635.4M

80% 37.5% 41.6%

70% Southern Europe

Paris 41 €235.4M

60% Nordics

50%

DACH Berlin 39 €209.8M

40%

France/Benelux

30%

Central &

Stockholm 16 €239.8M

20%

Eastern Europe

10%

Barcelona 11 €29.0M

0%

1. The Deal: Equity Investment in the UK 2016. Beauhurst (February 2017).

2. PitchBook data sourced by London & Partners (January 2017).

Sources: PitchBook and Beauhurst. State of the Markets 21Strong Fundraising Leads to Full Coffers

Global venture capital and private equity firms have $121 billion and $754 billion, respectively, to invest

after raising new funds in recent years. 1 We therefore expect to see funds continue investing in the best

high-growth UK technology companies through 2017 and beyond.

Global Venture Capital Overhang: 2007–20161 European Venture Fund Size: 2007–2016

$140B €200M €187

2016

Overhang by Average

Fund Size1

$120B Median

€160M

$1B+

$100B €132

$500M-

€120M

$80B $1B

$60B $250M-

€80M

$499M- €66

€60 €55

$40B

$100M-

€40M

$249M- €24

$20B €20 €17Closing Thoughts

State of the Markets 23Tech Drives Overall Economic Growth

Since the hype and collapse of the dot-com era almost two decades ago, technology has steadily

increased in importance (and value) for the U.S. economy. Tech companies comprise nearly one-quarter

of the S&P 500 index value. As a consequence, all industries face disruption from tech-native companies.

S&P 500 Technology Sector1 Weighting: 1995–2016 Largest U.S. Companies by Market Cap as of 3/31/2017

with Value Change Since 3/31/2015

35%

Autos Lodging

30% +17%2

-13%

25%

23%

20% +210%

3

-28%

15%

-34%

10%

+91% -19%

5%

Technology Peak of Trough of Slope of

Trigger Inflated Disillusionment Enlightenment

Expectations -19%

0%

1995 1998 2001 2004 2007 2010 2013 2016

Tech-Native Other

1. Amazon.com has been included in the technology sector.

2. Value change for Marriott is based on stock price. Marriott acquired Starwood for $13B in cash and stock in September 2016.

3. Airbnb value is based on most recent private valuation (March 2017).

Sources: Company websites, PitchBook, Siblis Research, CNBC and S&P Capital IQ. State of the Markets 24Corporates Take up the Innovation Imperative

Old-guard companies have recognized and embraced the need to innovate — from soup to nuts and

bolts, no sphere of the global economy has been unaffected by this next generation of technology.

Number of New Corporate Venture Capital Groups: 2011–2016 Deals with CVC Participation: 2011–2016

120 1600

1400

100

1

1200

80 2 2

1000

2

1

60 800

2

1 2

1 1

2 600

40

2

1 1 1

1 2 400

20 1

1

1 1 1 1 200

1

0 0

2011 2012 2013 2014 2015 2016 2017

1. Denotes launch of CVC and/or first investment.

2. Denotes announcement of corporate initiative (accelerator, research facility, etc.)

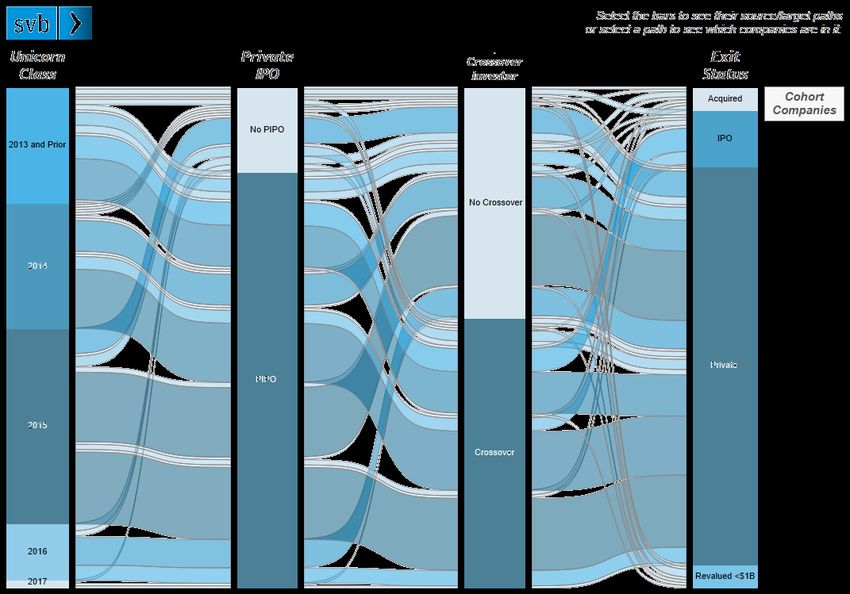

Sources: Company websites, Crunchbase, Fortune, Bloomberg, The Wall Street Journal, Star Tribune, Xconomy, Skift and CB Insights. State of the Markets 25Updated: SVB’s Interactive Unicorn Navigator

Use our Unicorn Navigator to follow the journeys of the billion-dollar club as they traverse the venture

landscape toward an eventual exit – now updated with 2017 entrants: C3 IoT, View and Zoom Video.

https://www.svb.com/state-of-the-markets-report/

Sources: The Wall Street Journal, PitchBook and S&P Capital IQ. State of the Markets 26About Silicon Valley Bank About SVB’s UK Branch

For more than 30 years, Silicon Valley Bank has helped SVB provides a range of targeted financial services and expertise

innovative companies and their investors move bold ideas through its office in the UK. With commercial and international

forward, fast. SVB provides targeted financial services and banking services, SVB helps address the unique needs of

expertise through its offices in innovation centers around the innovators. The UK's leading technology and life science

world. With commercial, international and private banking businesses, in all stages of development, look to SVB’s niche

services, SVB helps address the unique needs of innovators. expertise, experience and unparalleled network, as they grow at

home and tackle new markets abroad.

This material, including without limitation to the statistical information herein, is provided for informational purposes only. The material is based in part on information from third-party

sources that we believe to be reliable, but which have not been independently verified by us and for this reason we do not represent that the information is accurate or complete. The

information should not be viewed as tax, investment, legal or other advice nor is it to be relied on in making an investment or other decision. You should obtain relevant and specific

professional advice before making any investment decision. Nothing relating to the material should be construed as a solicitation, offer or recommendation to acquire or dispose of any

investment or to engage in any other transaction.

Silicon Valley Bank is registered in England and Wales at Alphabeta, 14-18 Finsbury Square, London EC2A 1BR, UK under No. FC029579. Silicon Valley Bank is authorised and regulated by the

California Department of Business Oversight and the United States Federal Reserve Bank; authorised by the Prudential Regulation Authority with number 577295; and subject to regulation by

the Financial Conduct Authority and limited regulation by the Prudential Regulation Authority. Details about the extent of our regulation by the Prudential Regulation Authority are available

from us on request. Silicon Valley Bank is a subsidiary of SVB Financial Group, a Delaware corporation and is an affiliate of SVB Financial Group UK Limited. SVB Financial Group UK Ltd is

registered in England and Wales at Alphabeta, 14-18 Finsbury Square, London EC2A 1BR, UK under No. 5572575 and is authorised and regulated by the Financial Conduct Authority, with

reference number 446159. SVB Financial Group and its subsidiary Silicon Valley Bank are members of the Federal Reserve System and Silicon Valley Bank is a member of the FDIC.

©2017 SVB Financial Group. All rights reserved. Silicon Valley Bank is a member of FDIC and Federal Reserve System. SVB>, SVB Financial Group, and Silicon Valley Bank are registered

trademarks.

State of the Markets 27You can also read