Structural Changes in the Bio-Products Sector: An Investment Perspective - Don Roberts CEO, Nawitka Capital Advisors Ltd. November 27, 2017 New ...

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Structural Changes in the Bio-Products Sector:

An Investment Perspective

.

Don Roberts

CEO, Nawitka Capital Advisors Ltd.

November 27, 2017

New Value of Bioeconomy Seminar

Pellervo Economic Research PTT

Helsinki, Finland

..

Situation

Analysis

• The global bio-products sector is vertically integrated, and

comprised of multiple industries and market segments.

• It is undergoing transformational change related to a series of

demographic, technological, societal and environmental shocks.

ü Within the paper industry, communication papers are in secular

decline, while packaging & tissue papers are continuing to grow

• These shocks are affecting both the demand and supply-side of

the market, and creating winners and losers amongst traditional

players.

• How is Finland positioned to deal with this disruption?

|1

Outsiders’

View

of

Finland

National Innovation Report Card

Grade

A Grade

B Grade

C Grade

D

Finland U.S.A. Canada Ireland

Denmark Switzerland Germany

Sweden Netherlands Japan

Austria Australia

Norway Belgium

U.K.

France

• Overall, how innovative is Finland perceived to be by outsiders?

• According to the Conference Board of Canada (2015), Finland is one of only 3

countries to receive a Grade A in terms of national innovation – the top rank.

• According to Nawitka Capital (2017), the “continental leaders” in the forest products

industry regarding bio-products innovation are:

• UPM-Kymmene in Europe

• Fibria in Latin America

• Georgia Pacific in North America

|2

• Oji Paper in Asia

Finland’s

Response?

Nine major new and pending projects related to Bio-Products in Finland

In addition to

Investor Location Year Product/

Investment type pulp, this includes

bio-materials

Metsa-‐ Aanekoski 2017 -‐ NBSK &

NBHK

pulp (eg., MFC, MCC,

Fibre -‐ Micro

Fibrillated

intermediate for

Cellulose

(MFC)] viscose) and

biofuels.

UPM-‐ Kouvola 2017 -‐ NBSK/NBHK

pulp

Kymmene Pietarsaari 2019 -‐ NBSK/NBHK pulp Metsa’s EUR 1.2B

bioproduct mill is

Stora-‐ Imatra 2019

-‐ MFC the largest

Enso Uimaharju 2019 -‐ Dissolving

pulp investment in the

history of

Boreal

Kemijarvi 2020 -‐ NBSK

&

dissolving

pulp Finland’s forest

Bioref -‐ Micro

Crystalline products industry

Cellulose

If all the planned

KaiCell Paltamo 2021 -‐ Biorefinery with

NBSK

&

product is

Fibers intermediate

for

viscose exported, it

would likely

FinnPulp Kuopio 2021 -‐ NBSK

pulp boost Finland’s

bio-products

Kaidi Kemi 2021 -‐ Biodiesel &

bio-‐gasoline trade by more

than 2 billion

NEB Kajaani 2017 -‐ Bioethanol euros/year.

|3

SEB Kouvola 2019 -‐ Bioethanol Source: Prof. Olli Dahl

Three

Fundamental

Questions

This keynote presentation explores three fundamental questions

facing the Bio-Products sector.

1) Are key transformational technologies strengthening or weakening

the traditional competitive advantage of countries like Finland &

Canada?

2) Is renewable energy a meaningful opportunity for the bio-

products industry – or a potential threat?

3) Given demographic changes and low fossil fuel prices, can

governments afford to financially support the production of clean

bio-products?

|4

Question

#1

Are key transformational technologies strengthening or

weakening the traditional competitive advantage of

countries like Finland?

• Fiber strength resulting from slow growing trees has historically

been a key competitive advantage of both the pulp and solidwood

industries in northern countries.

|5

Value

of

Long

vs

Short

Fiber: Recent

Data

Point

Ø Consider an interesting data point generated in September

• A subsidiary of Asia Pulp & Paper paid a very high premium

for El Dorado’s pulp mill and expansion option in Brazil

• Reflected a particularly bullish view from Asia.

• Paid $2,810/tonne of pulp capacity

ü ~70% premium over average Brazilian peers (Fibria,

Suzano)

ü > 500% premium over the NBSK producer Canfor Pulp

• Interesting perspective on the future demand for pulp, and

relative attractiveness of southern hardwood and northern

softwood pulp.

Ø Does this suggest that northern countries like Canada and

Finland have a bad case of “pulp chauvinism”?

|6

Next-‐Generation

Genomics

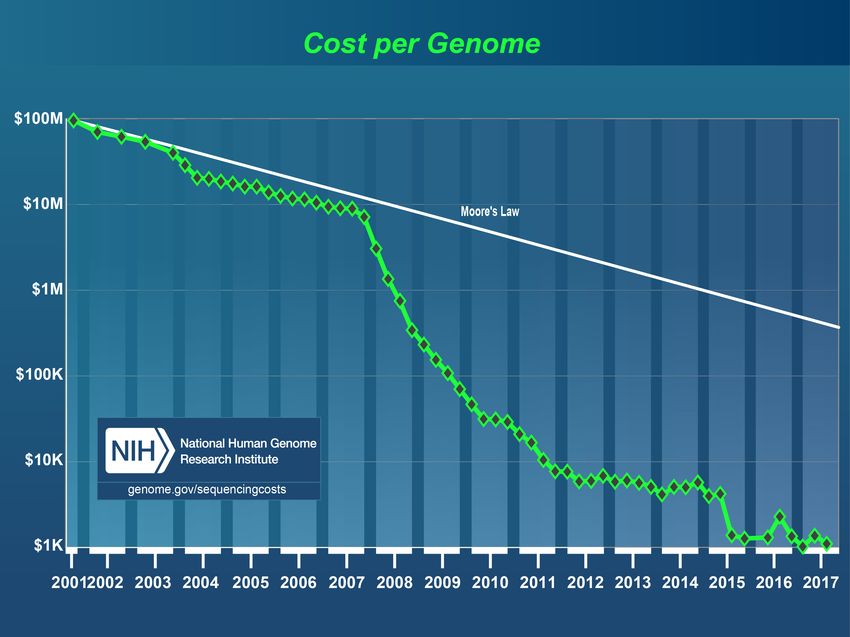

Ø Cost of DNA sequencing is falling even faster than that suggested by

Moore’s Law – from ~$100 million per genome in 2000 to ~$1,000 in

2017

Ø It is not “if” this dramatic cost reduction in DNA sequencing will have

a meaningful impact on the bio-products value chain, it is “how” &

“when”.

|7

Next-‐Generation

Genomics

Ø A technological “fix” can increasingly be used to enhance the

natural attributes of biomass.

Ø For example, Brazilian forest companies have already enhanced

genetics to produce energy oriented eucalyptus clones:

§ Have high lignin content/calorific value – superior for

generating energy, but cannot be used to produce pulp

§ Forest yield ~60-80 m3/ha/year (vs ~35-50 for pulp

oriented clones)

§ Harvest in 2-3 years (vs 7 years for pulp)

Ø Can the Brazilians also produce fast growing trees that can be

processed into stronger pulp? Likely.

|8

Biomaterials/Biochemicals

Wood is roughly 1/3 cellulose, 1/3 hemicellulose, and 1/3 lignin.

Focus on fractionating the biomass - extracting, separating and

processing each of the three components.

For example:

• Aside from being used to produce paper, cellulose can be used to

produce intermediates for things like films (eg., cellophane), and a

range of pharmaceutical applications.

• Use hemicellulose to produce xylose – an input into the sweetener

market.

• Use lignin to replace phenols in the wood adhesives market, or

processed into a substitute for carbon fibre composites.

|9Biomaterials/Biochemicals

Nanocellulose is nano-sized cellulose fibrils (eg. Micro-fibrillated

cellulose, Nano Crystalline Cellulose).

• Nanocellulose can enhance the performance of paper in terms of,

strength, stiffness, printability.

• If we want to produce Nanocellulose at scale, we don’t have to

constrain ourselves to the paper industry.

ü Schlumberger is finding the application of NCC and Cellulose

Filaments show positive results in the oil and gas industry, with

respect to cement well casing, drilling fluid and enhanced oil

recovery.

• The greatest financial returns will likely be applications outside the

paper industry. (eg., Personal & Health Care, Electronics)

| 10Solidwood

The solidwood industry has historically been the cornerstone of a

competitive forest sector in Scandinavia and Canada.

It’s use in the construction industry generates a high value per m3 of

roundwood, and helps pay for removing lower quality biomass from

the forest.

| 11Structural

Wood

Products

Opening

up

New

Markets

• Cross Laminated Timber is an engineered mass timber product that

utilizes smaller dimension lumber (2x4, 2x6, 2x8, etc.) to create large,

lightweight, made-to-order panels. CLT was first developed and used in

Austria in the early 1990s

• Glue Laminated Timber or Glulam is a product similar to CLT and is an

established product in the North American market. Like CLT it is made by

laminating smaller dimension lumber together, but in one direction as

opposed to alternating each layer.

CLT Glulam

CLT

panel.

Photo

Courtesy

of

Structurlam

Products,

Ltd. Glulam

beam.

Photo

courtesy

of

BMC

West

. 12UBC’s

Brock

Commons,

Vancouver

18-‐storey

student

residence,

primarily

made

of

wood

(CLT)

Mid

&

High

rise

buildings

open

up

a

whole

new

market

for

wood.

Constructed

in

9

½

weeks.

13 Source:

Naturally

WoodUBC’s Brock Commons • H=53.5m – the tallest wood- based building in the world. • Hybrid structure • Two-way point-supported CLT floor system • Gravity loads taken by glulam and PSL columns • Lateral system consists of floor panels and 2 concrete cores 14

UBC’s

Brock

Commons:

Environmental

Footprint

Source:

Naturally

Wood

15CLT

is

already

in

Scandinavia

• The

Treet Building

in

Bergen,

Norway

14-‐storeys

51m

– the

world’s

second

tallest

contemporary

wood

building

• Stora Enso

is

a

champion

of

CLT

in

Europe,

and

the

largest

producer.

16CLT

Wind

Turbines,

Germany

• H= 100 m with a ladder and lift system

• Turbine rotor diameter of 77 m weighs 100 tons 1,500 kW of electricity

17Implications

of

New

Markets

for

Structural

Wood

Products?

The good news?

• Potentially opening up the mid & high-rise market for wood,

with the associated economic and environmental benefits

The bad news?

• Given the newer panel technologies, we do not necessarily

need slow growing wood for structural applications (eg.,

Eucalyptus is also good for CLT).

. 183D

Printing

3D Printing has been called

“the source of the next industrial

revolution”.

• It allows for mass customization.

• It is a manufacturing process that builds layers to create a three

-dimensional solid object from a digital model on a computer.

• A range of alternative materials are being assessed for building

with 3D printers – including woody biomass.

• China and the Netherlands are the global leaders in exploring this

application.

ü Winsun, a Chinese construction company, has already built

flats using 3D printing.

| 193D

Printing

a

House

Using a 3D The team

printer in 2016 sprayed a

Apis Cor built polyurethane-

this 400 ft2 based mixture

structure for for insulation,

~$10,000. then installed

the house's

The walls, windows and

partitions and finishes, like

building envelope countertops and

were all printed. cabinets, and

painted it bright

yellow.

The workers

and the 3D

printer

finished

everything in

about 24

hours.

| 20Finished

3D

Printed

House

All the walls,

decorative

elements and

tower were printed

off-site, and then

assembled like a

Lego kit

It is estimated that

the use of 3D

printing technology

reduces the

construction

time by 8 to 12

times, which in

turn increases

efficiency and

reduces production

costs.

| 21Why

3D

Printing

for

Construction?

Ø Labor productivity in the Construction sector has been declining.

Ø Construction is the last remaining manufacturing sector to

not be automated. There is a large economic incentive to

change the way we build – and 3D Printing will become one

option.

Non-farm productivity index

Construction Productivity

indexImplications

of

3D

Printed

Structures?

The good news?

• Potential dramatic increase in labor productivity and reduced

time for construction and waste.

• Improved value proposition for wood in construction IF biomass

is the preferred substrate.

The bad news?

• Most of the substrate used for 3D printing is Polymers

(petrochemical plastics), metal alloys and modified cement.

• Biomaterials are currently less than 1% of the market.

| 23Answer

to

Question

#1?

Are key transformational technologies strengthening or

weakening the traditional competitive advantage of slow

growing temperate forests?

• It depends on the specific technology, but on balance they are

likely to decrease the traditional advantage of “strong-northern

fibers”

• Especially true with respect to

ü Next Generation Genomics

ü Tall-timber building

ü 3D Printing

• Less clear with respect to Biomaterials/Biochemicals, whose

applications may depend more on close co-operation & proximity

to major customers.

| 24Question

#2

Is renewable energy a meaningful opportunity for

the bio-products industry – or a potential threat?

| 25Isn’t

Bio-‐Energy

Unique?

Bio-energy is unique in that it:

• Creates base-load power which is dispatchable

• Generates relatively high employment compared to other

sources of renewable power.

ü ~5.5 permanent jobs per MW of capacity versus

0.7/MW for wind power and 0.2 for solar power.

• Can be converted into liquid fuels.

| 26Trend

in

Bio-‐Energy

Investment

Global Investment in Bio-energy ($US Billion),

2004-2016

Ø After peaking at over $US 50 billion in 2007, annual global investment

in bioenergy has trended down to ~$US 9 billion in 2016.

Ø An aggregate decline of ~80% over the last ten years, and the fall | 27

was even greater for liquid biofuels than power projects.Global

Investments

in

Bio-‐Power

Ø Investment down significantly from the recent peak in 2011 due to:

ü Low fossil fuel prices (natural gas & coal);

ü Uncertainty over feedstock supply & future price;

ü Falling prices of solar & wind energy; and,

ü Government efforts to rein in subsidies on renewable power.

Ø A few large coal-to-biomass conversions in Europe and Asia are still

being financed. Stand-alone plants are very challenging to finance.

Ø Smaller CHP plants are still being funded – especially where power

prices are relatively high.

Ø Some growth in wood pellet demand from Europe and Asia, but

forecasts have been revised downward.

Ø From a purely financial perspective, most bio-power

investments are not attractive.

. | 28Benchmark

Levelized Cost

of

Electricity:

H2 2016 ($/MWh)

Marine - wave

Marine - tidal

STEG - LFR

STEG - parabolic trough w/ storage

Nuclear (AMER)

STEG - tower & heliostat w/storage

Wind - offshore

Nuclear (EMEA)

Biomass - anaerobic digestion

Biomass - incineration

PV - c-Si tracking

Biomass - gasification

PV - thin film

PV - c-Si

Natural gas CCGT (EMEA)

CHP (AMER)

Coal fired (EMEA)

Municipal solid waste

Geothermal - binary plant

Natural gas CCGT (APAC)

CHP (EMEA)

Wind - onshore

Natural gas CCGT (AMER)

Small hydro

Large hydro

Coal fired (AMER)

Coal fired (APAC)

Geothermal - flash plant

Landfill gas

0 100 200 300 400 500 600

Source: Bloomberg New Energy Finance,

• There is a large variation in the cost of producing electricity across the

sources of electricity. (Also large variation within technologies)

• Bio-power is not the lowest cost source of electricity.

• This is a snap shot as of H2/2016, but what is the trend over time?Wind

and

Solar

Experience

Curves

SOLAR

PV

MODULE

COST

($/W) ONSHORE

WIND

LEVELISED

COST*

($/MWH)

100

1976 SOLAR

COSTS

HAVE

1,024

WIND

COSTS

HAVE

-0.30

y = 3,582.42x

FALLEN 1985

FALLEN

R² = 0.91

>99%

SINCE

1976 512 50%

SINCE

2009

1985

90%

since

2009

10 256

2003 2008

2009

128 1999

2025

1 2012 64

2016

2016 Learning rate = 19%

32

Learning

rate

24.3% 16

0.1

100 1,000 10,000 100,000 1,000,000

1 10 100 1,000 10,000 100,000 1,000,000

Cumulative capacity (MW)

Source: Bloomberg New Energy Finance, Maycock Source: Bloomberg New Energy Finance

• Dramatic cost reductions for solar and wind continue to be driven

by technological improvements and scaling of the supply chain.

• ….Largely due to the delivered cost of biomass, the cost of bio-

power has remained relatively flat over time.Unsubsidised

Clean

Energy

World

Records

Set

in

2016/17

Solar

PV Onshore

wind Offshore

wind

Country: Mexico Country: Morocco Country: Germany

Bidder: FRV Bidder: Enel

Green

Power Bidder: DONG/EnBW

Signed: September

2016 Signed: January

2016 Signed: April

2017

Construction:

2019 Construction: 2018 Construction: 2024

Price: US$

2.69

c/kWh Price: US$

3.0

c/kWh Merchant

Price: US$

4.9

c/kWh

• Note: The offshore wind merchant price is estimated based on project LCOE in real 2016 terms • Source: Bloomberg New Energy Finance; ImagesSiemens; Wikimedia Commons

By comparison, what is the typical cost of stand alone bio-

power plants? ~ US$ 10 c/kWh?Lithium-‐ion

Battery

Experience

Curve

($/kWh)

and

Cumulative

Capacity

2010-‐2030E

(GWh)

Lithium-‐ion

Battery

Price

Forecast .

• Source: Bloomberg New Energy Finance

• Cost of power storage fell by more than 70% from 2010-2016,

and is expected to drop by another 75% by 2030.

• Lower costs of storage are improving the value proposition for

| 32

intermittent sources of power like wind & solar PV vs biomassGlobal Investment in Biofuels, by Technology

Q1 2005–Q2 2015 ($m)

GLOBAL

INVESTMENT

IN

FIRST-‐GENERATION

35,000 GLOBAL

INVESTMENT

IN

NEXT-‐GENERATION

BIOFUELS, BIOFUELS,

30,000 3,000

25,000 2,500

20,000 2,000

15,000 1,500

10,000 1,000

5,000 500

0 0

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

• Investors are switching from First-Generation to Next-Generation Biofuels.

Large concern over ethanol’s blend wall constraint and food vs fuel debate.

• Almost $9 billion has been invested globally in developing Next

Generation biofuels over the past five years. The industry is emerging

beyond the initial stage.

Ø There are 12 small-scale next-generation commercial plants currently in

operationUS

Oil

Production

and

Rig

Efficiency

New-well Production per Rig US Monthly Oil Production (mbbl)

(bbl/day)

800 350

700 300 2007–17

2007–17

600 Up

83%

Up

1,300% 250

500

200

400

150

300

100

200

100 50

0

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

Source: EIA

• BUT - The technological revolution in fossil fuel extraction is still

under appreciated. It started in N. America, but has yet to be

meaningfully deployed around the world.

• True for oil……..US

Gas

Production

and

Rig

Efficiency

US monthly natural gas

New-well production per rig (‘000

production (bcf)

cf/day)

4,000 3,000

3,500 2007–17 2,500

3,000 Up

388%

2,000

2,500

2,000 1,500

1,500 2007–17

1,000

1,000

Up

35%

500

500

0 0

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

Source: EIA

• .....also true for natural gas

• Don’t bet that high fossil fuel prices will be what makes bio-

based fuels & chemicals more cost competitiveAnswer

to

Question

#2

Is renewable energy a meaningful opportunity for

the bio-products industry – or a potential threat?

• Combined Heat & Power (CHP) applications integrated into

bio-refineries continue to offer a compelling value proposition.

• Although there are local exceptions, bio-power is already

generally less competitive than other forms of renewable

power (eg., hydro, solar, wind).

• With improving battery storage technology, even liquid

biofuels will be threatened in the long-term.

| 36Question #3

Given demographic changes and low fossil fuel

prices, can governments afford to financially

support the production of clean bio-products?

| 37Is Carbon Pricing Enough?

Fundamental problem is that there is a disconnect between

the private and public value of bioenergy. Without some

form of gov’t intervention, we expect very few bioenergy

projects to be financially viable.

Carbon pricing? – right idea, but are levels high enough in

most countries to actually change behavior? No.

Ø In 2016, the three highest national carbon prices in the

world were $131 in Sweden, $86 in Switzerland and $65

in Finland.

Ø ….but only ~$25 in France, ~$23 in B.C., $13 in

California, $8 in China (Beijing Pilot), and $5 in EU ETS

| 38Options for Governments? Many countries still do not price carbon, and ~3/4 of the carbon emissions subject to carbon pricing in 2016 were priced below $10. UK Government estimates the Social Cost of Carbon to be in the range of $41-$124, with a central estimate of $83. If carbon pricing remains well below the Social Cost of Carbon, what are the best options? Most governments are under fiscal pressure, and the problem is likely to grow. • Rising cost of pensions, health care, etc. • The affordability of subsidies for the bio-economy will be a challenge. ”Smart Regulations” may be one option (eg., California’s | 39 Low Carbon Fuel Standard)

Focus on Fuel Standards

Renewable and Low Carbon Fuel Standards can play an

important role in stimulating investment in advanced biofuels

Fuel Standards can be viewed as a “Compliance Tool” as

opposed to an “Incentive Tool”.

• Anecdotal evidence suggests the former are more stable

than the latter, and thus tend to be more effective in

driving investment due to lower regulatory risk over time.

Globally, the U.S.’s Renewable Fuel Standard 2 and

California’s Low Carbon Fuel Standard are likely the most

important and effective Fuel Standards.

| 40U.S. Experience

40,000

RFS2 Blending Mandates 2016-2022

(millions of gallons)

35,000

30,000

25,000

20,000

15,000

10,000

5,000

0

2016 2017 2018 2019 2020 2021 2022

Corn

Ethanol Biodiesel

Advanced

Cellulosic

• RFS2 established mandates on the oil refining sector to integrate up to 36

billion gallons of specific types of renewable fuels by 2022.

• A plant-by-plant review suggests that over 80% of the global capacity in cellulosic

biofuels has been built in response to the RFS2 – including those plants in Canada

and Brazil.

• California has implemented a similar (but better) Low Carbon Fuel

Standard, which focuses on decreasing the Carbon Intensity of fuel in the State.| 41Value of the RFS2 and California LCFS to Investors:

Case Study of a Bio-Crude Oil Plant ($US)

• Given a $47/barrel market price of oil, prevailing C-RIN/ LCFS

Credit prices & an estimated Carbon Intensity of ~0.20 gCO2/MJ,

qualifying under the California/RFS2 regimes add an additional

$153/barrel in value – total comes to $200/barrel.

ü Fuel Value = $47 barrel;

ü RFS2 = $122/barrel;

ü California LCFS = $26/barrel;

ü California Cap & Trade Credit = $5/barrel

• The capital cost of a 75 million liter bio-crude plant is ~US$120

million, with an operating cost of ~$42/barrel – cash flow

positive, but not profitable without a subsidy.

ü BUT, it generates ~$80 million/year in regulatory savings (to be

shared between the bio-crude oil plant & oil refiner).

ü Significant incentive to produce bio-crude oil…..and it doesn’t

cost the public treasury.

| 42Answer to Question #3

Given demographic changes and low fossil fuel prices, can

governments financially support the production of clean bio-

products without over burdening the public treasury?

• It will be difficult. Production subsidies and tax breaks can be a

very significant tax burden.

• Meaningful carbon taxes are the best bet, but

ü Generally too low to change behavior (but not in Finland)

ü A competitive disadvantage for industry if not applied in other

countries.

• Targeted capital subsidies for R&D through to first commercial

plants can make sense. Gov’t procurement also has a role,

especially to establish an early market for emerging products.

• Explore “Smart regulations” which set Carbon Intensity targets,

are technology neutral, and create a ”credit market” involving

obligated parties so governments don’t have to pay. | 43Why

should

we

be

embracing

the

Bio-‐Economy?

Climate-related flood risk at Mar-a-Lago Club, Miami, Florida:

(i.e., President Trump’s ”Winter White House”)

Note: Blue areas

indicate risk of

flooding in 2045 2016

2030

Source: Coastal Risk Consulting © Mapbox, © OpenStreetMap Graphic: Jan Diehm/The Guardian

Don’t you want to save Donald’s golf course from flooding?

| 44.

APPENDIX:

U.S. INCENTIVES FOR LIQUID BIOFUEL

| 45U.S. Renewable Fuel Standard:

RIN Credit and Pricing Overview

Ø RFS2 credits are generated by displacing,

blending or processing fossil fuels with Historical

C-‐RIN

Pricing

(US$/C-‐RIN

Credit)

renewable fuel, yielding Renewable Identification

Numbers, or RIN Credits, which are used for

compliance

Ø Four types of RIN credits can be generated

based on the different types of biofuel that are

blended:

– Cellulosic Biofuel - C-RIN

– Biomass Based Biodiesel - B-RIN (Conventional Biodiesel)

– Advanced - A-RIN (Sugar cane ethanol, Renewable

Source:

OPIS

Diesel)

RFS2

Market

Value

per

Barrel

of

Biocrude

– Conventional - R-RIN (Corn Ethanol)

Ø C-RINS are the most valuable category of RINS, US$2.60

= US$122

and are primarily created when wood is used as Per

C-‐RIN Value

t

per

barrel

of

Biocrude

the feedstock. The price is strongly influenced by

a legislative formula that is inversely correlated to

oil prices – this provides a premium over other

RIN categories.

.

Ø Unlike the price of R-RINS (corn ethanol), that of

C-RINS did not drop in response to the U.S.

election….investors perceive less political risk.

54California Low Carbon Fuel Standard (LCFS):

Credit and Pricing Overview

Historical

LCFS

Credit

Pricing

(US$/MTCO2e)

• LCFS credits are measured in Metric Tonnes of

Carbon Dioxide Equivalent (MTCO2e) and priced

in US$

• LCFS credit trading is currently limited to

primary market trading between obligated

parties and producers of credits

• LCFS credit prices have averaged US$90 over

the last year, US$89 over the last two years and Source:

OPIS

are currently priced at US$70

LFCS

Value

per

Barrel

of

Biocrude

• LCFS credit prices are expected to rise further

due to the high marginal costs of compliance in US$90

= US$26

the transportation fuels sector Per

MTCO2e Value

Per

barrel

Biocrude

• LCFS credit prices are capped at a US$200

ceiling which is increased each year by a CPI

factor

.

56California Cap and Trade:

Allowance Credit and Pricing Overview

• The instrument used to measure emissions Historical

Cap

and

Trade

Credit

Pricing

(US$/MtCO2e)

reductions under the California Cap and Trade

program is referred to as Allowances. Allowances

are denominated in dollars per Metric Ton of

Carbon Dioxide Equivalent (US$/MTCO2e)

• The Quebec and California Cap and Trade

Programs are now linked, and Ontario’s will be

linked next year.

• California’s Cap and Trade system started with a Source:

California

Air

Resources

Board

price floor in 2012 of US$10.00, which is

escalated each year by 5% plus the CPI inflation C&T

Value

per

Barrel

of

Biocrude

to

Project

factor, ensuring a growing compliance cost

• Market prices for Allowances averaged

US$15 = US$5

Value

per

barrel

of

Biocrude

~US$15/MTCO2e in July/August 2017. Per

MTCO2e

• The carbon price will likely trend higher since:

– The transportation sector is now covered

under the California program and free

allocations of emissions credits are

mandated to decline .

– The Ontario market is expected to be short

of credits.

58You can also read