"SUBSCRIBE" Our Recommendation - IRCON INTERNATIONAL LTD IPO Price Band : ' 470 -' 475

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

IRCON INTERNATIONAL LTD

IPO

Price Band : ` 470 –` 475

Our Recommendation

“SUBSCRIBE”

THE OFFER Issue Open : 17 Sep 2018 to 19 Sep 2018 »» Issue Type: Book Built Issue IPO »» Issue Size: › 9,905,157 Equity Shares @ 10 aggregating up to ` 470.49 cr »» Face Value: ` 10 Per Equity Share »» Issue Price: ` 470 - ` 475 Per Equity Share »» Market Lot: 30 Shares »» Minimum Order Quantity: 30 Shares »» Listing At: NSE, BSE A Discount of ` 10 per equity share is offered in Retail and employee quota.

CAPITAL STRUCTURE

The share capital of Company, is set forth below:-

(Amount in ` except share data)

Authorized Share Capital :-

400,000,000 Equity Shares @10 Aggregate value 400 cr

Issued, subscribed and paid up capital before the Issue :-

94,051,574 Equity Shares @10 Aggregate value 94.05 cr

Present Issue:-

9,905,157 Equity Shares @ 10 aggregating up to ` 470.49 crOBJECT OF THE OFFER The objects of the Offer are To carry out the disinvestment of upto 9,905,157 Equity Shares, including Employee Reservation Portion, by the Selling Shareholder constituting 10.53% of Company’s pre- Offer paid up Equity Share capital of the Company. To achieve the benefits of listing the Equity Shares on the Stock Exchanges. Company will not receive any proceeds from the Offer and all proceeds shall go to the Selling Shareholder.

COMPANY OVERVIEW Ircon International is a Mini-Ratna public sector undertaking. It is an integrated engineering and construction company specializing in major infrastructure projects, including railways, highways, bridges, flyovers, tunnels, aircraft maintenance hangars, commercial and residential properties, development of industrial areas, and other infrastructure activities. It is headquartered in Saket, New Delhi and has overseas office in Malaysia. It has 26 project offices in India and overseas, including Sri Lanka, Bangladesh, South Africa and Algeria. The company’s primary focus stays rooted in the railway sector. The total order book of the company as on March 31, 2018 stood at Rs 22,406.79 crore

IRCON’S CORE BUSINESS Companies core operations are Construction :- As on March 31, 2018, it undertook a total of 33 railway projects in two countries internationally and in 13 states in India, with an aggregate length of 1,664.74 km. The order book for these ongoing projects amounted to Rs 19,425.77 crore as on March 31, 2018, accounting for 86.70% of its total order book. Under the electrical business, it undertook eight electrification projects in India and abroad and the order book amounted to Rs 1208.39 crores as on March 31, 2018, accounting for 5.39% of the total order book. Under the building and other business, it undertook three building and other projects in India and abroad. The order book amounted to Rs 494.61 crore as on March 31, 2018, accounting for 2.21% of the total order book. Infrastructure development :- As on March 31, 2018, it had completed one road project of 115 km in India. It intends to complete two more BOT toll projects by the end of 2018 and start realizing toll revenues.

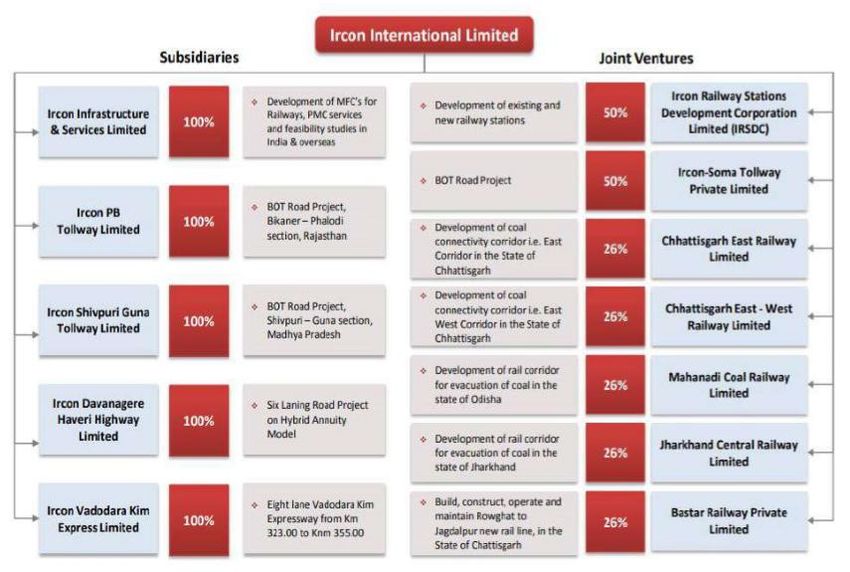

CORPORATE STRUCTURE

INDUSTRY OVERVIEW Over the years 2019-2022, CRISIL Research expects the construction sector to increase 54% to Rs 22.2 trillion. Of this, about 93% would be contributed by infrastructure investments, while the rest would be from industrial sector. During 2015-18, railways accounted for 11% of the construction sector at Rs 1.6 trillion. Over the next four years, the construction opportunity in railways is expected to double to Rs 3.1 trillion, driven by investments by public as well as the private sector.. CRISIL Research also expects the investments in railway sector to increase by about 77% from Rs 3.9 trillion in fiscals 2015-2018 to Rs 6.8 trillion in fiscals 2019-2022.

ROAD MAP AHEAD Company objectives are to expand their market share and aim to accomplish this through the following strategies: Continue expanding geographical footprint within and beyond India. Paradigm shift in revenue generation. Focus on high value projects in the construction business to benefit from economies of scale. Actively bid for new projects . Maintain favorable financial risk profile. Explore different models of project execution to optimize project portfolio . Explore potential ways to capture sectorial initiatives undertaken by the Government to improve economic growth.

STRENGTHS Construction business operates in diverse sectors covering many countries. Excellent execution track record through strong operating systems and controls. Strong financial performance and credit profile. Visible growth through robust order book and steady execution.

FINANCIAL HIGHLIGHTS Total Revenues stood `2908.63cr, ` 3301.34cr and `4212.40cr, in Fiscal 2016, Fiscal 2017 and Fiscal 2018 respectively. Aggregate revenue from construction business amounted to `2418.51cr, ` 2994.79cr and `3896.39cr accounting for 97.48%, 98.58% and 96.75%, for Fiscal Year 2016, Fiscal Year 2017 and Fiscal Year 2018, respectively, of total operating revenue for these periods. Revenue from railway projects accounted for 77.12%, 68.26% and 68.95% of total revenue from operation for Fiscal Year 2016, Fiscal Year 2017 and Fiscal Year 2018, respectively. PBT was `611.60cr, ` 555.52cr and ` 558.35cr, in Fiscal 2016, Fiscal 2017 and Fiscal 2018 respectively. PAT was ` 393.10cr, ` 383.97cr and ` 411.58cr, in Fiscal 2016, Fiscal 2017 and Fiscal 2018 respectively.

SNAPSHOT

RISK FOR THE BUSINESS Business is substantially dependent on construction and infrastructure projects undertaken any change in government policies, may adversely affect business. Railway sector projects contribute approximately 86.70% of Order Book as of March 31, 2018. Any change in the sector may adversely affect revenues and profitability. Projects sub-contracted or undertaken through a joint venture may be delayed on account of the performance of the joint venture partner, could lead to material adverse effect on business.

CONTINUE Projects are exposed to various implementation and other risks and uncertainties which could lead to material adverse effect on business. Statutory Auditors, in the past, have raised a vigilance related issue in their audit report. Materialization of contingent liabilities may impact financials. As of March 31, 2018, contingent liabilities appearing in consolidated financial statements aggregated to 10,86.77 cr.

VALUATION IRCON being majorly under railways has managed to perform well over the years. Companies reputation for quality, commitment and consistency in terms of performance, as well as local, regional and international presence, have allowed to service the growing infrastructure needs throughout India. Further, Foreseeing at the strong order book (`22,406.79 crore as on March 31, 2018) and steady execution, strong financials, proven track record of various domestic and foreign project executions, will help IRCON to grow at a robust pace. On the upper price band of `475 with EPS of `43.78 for FY18, P/E works out at 10.84x, which appears to be low on valuations, but with no direct peer comparison and being Government entity with stable business outlook, we recommend to “SUBSCRIBE” the issue for listing gains.

DISCLAIMERS This Research Report (hereinafter called report) has been prepared and presented by RUDRA SHARES & STOCK BROKERS LIMITED, which does not constitute any offer or advice to sell or does solicitation to buy any securities. The information presented in this report, are for the intended recipients only. Further, the intended recipients are advised to exercise restraint in placing any dependence on this report, as the sender, Rudra Shares & Stock Brokers Limited, neither guarantees the accuracy of any information contained herein nor assumes any responsibility in relation to losses arising from the errors of fact, opinion or the dependence placed on the same. Despite the information in this document has been previewed on the basis of publicly available information, internal data , personal views of the research analyst(s)and other reliable sources, believed to be true, we do not represent it as accurate, complete or exhaustive. It should not be relied on as such, as this document is for general guidance only. Besides this, the research analyst(s) are bound by stringent internal regulations and legal and statutory requirements of the Securities and Exchange Board of India( SEBI) and the analysts' compensation was, is, or will be not directly or indirectly related with the other companies and/or entities of Rudra Shares & Stock Brokers Ltd and have no bearing whatsoever on any recommendation, that they have given in the research report Rudra Shares & Stock Brokers Ltd or any of its affiliates/group companies shall not be in any way responsible for any such loss or damage that may arise to any person from any inadvertent error in the information contained in this report. Rudra Shares & Stock Brokers Ltd has not independently verified all the information, which has been obtained by the company for analysis purpose, from publicly available media or other sources believed to be reliable. Accordingly, we neither testify nor make any representation or warranty, express or implied, of the accuracy, contents or data contained within this document. Rudra Share & Stock Brokers Ltd and its affiliates are engaged in investment advisory, stock broking, retail & HNI and other financial services. Details of affiliates are available on our website i.e. www.rudrashares.com. We hereby declare, that the information herein may change any time due to the volatile market conditions, therefore, it is advised to use own discretion and judgment while entering into any transactions, whatsoever. Individuals employed as research analyst by Rudra Shares & Stock Brokers Ltd or their associates are not allowed to deal or trade in securities, within thirty days before and five days after the publication of a research report as prescribed under SEBI Research Analyst Regulations. Subject to the restrictions mentioned in above paragraph, we and our affiliates, officers, directors, employees and their relative may: (a) from time to time, have long or short positions acting as a principal in, and buy or sell the securities or derivatives thereof, of Company mentioned herein or (b) be engaged in any other transaction involving such securities and earn brokerage or profits.

FOR MORE DETAILS LOG ON TO www.rudrashares.com

You can also read