SURVEY GERMANY CITY OFFICE AND INVESTMENT MARKETS - AN OVERVIEW - Colliers

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

GERMANY CITY SURVEY OFFICE AND INVESTMENT MARKETS – AN OVERVIEW 2020 / 2021

ACCELERATION

INSTEAD OF

STANDSTILL

At the last publication of our City Survey, Digitalization, which has now also made a

no one could even guess at the challenges breakthrough in the real estate sector,

the economy and the real estate markets has been acting as a pioneer in all of this

would face in 2020. Although the impact and setting the pace for market activity.

of the economic downturn and challeng- By making it possible to finalize deals and

ing global environment on the German sign leases online in light of the contact

leasing and investment markets were a restrictions in place, offering many em-

topic of discussion a year ago, no one ployees the option to work from home and

doubted that the unusually long, robust further spurring the e-commerce sector,

Matthias Leube MRICS boom would continue. The prospect of digitalization has brought with it transfor-

CHIEF EXECUTIVE OFFICER ongoing, strong market performance now mational changes to the office, retail,

matthias.leube@colliers.com appears obsolete, however, in view of a logistics and hotel sectors.

pandemic that temporarily eclipses all

previous risks of a downturn and is diffi- However, the Covid-19 crisis has also

cult to get a handle on because of its com- increased risk awareness and brought

plexity. But is this actually the case? with it the tendency to place greater

importance on the quality and future-

At no time did activity on the German real resilience of an asset. Being able to

estate market come to a full standstill. identify and realize sustainable concepts

Following a brief orientation phase on the that fit the demands of market players in

investment and leasing markets in Q2 that location, like Forum Steglitz featured

2020, activity began to pick up in the on our cover page, is key to crisis-resil-

second half of the year and again tangibly ient investment.

accelerated in Q4 despite a second lock-

down in early November. This momentum I look forward to exploring these new

is an impressive indication of the robust opportunities with you.

nature of the German real estate market

and the capacity of market players to

adapt to an environment that is new to all

of us.

3

CONTENTS

City Survey Germany | Colliers International

CONTENTS | 2020 / 2021

Market Data 4

Commercial Real Estate Market Germany

Office Leasing 6

Investment 9

Retail Investment 12

Industrial and Logistics Investment 15

Hotel Investment 18

City Reports

Berlin

Office Leasing 23

Investment 25

Düsseldorf

Office Leasing 29

Investment 31

Frankfurt

Office Leasing 35

Investment 37

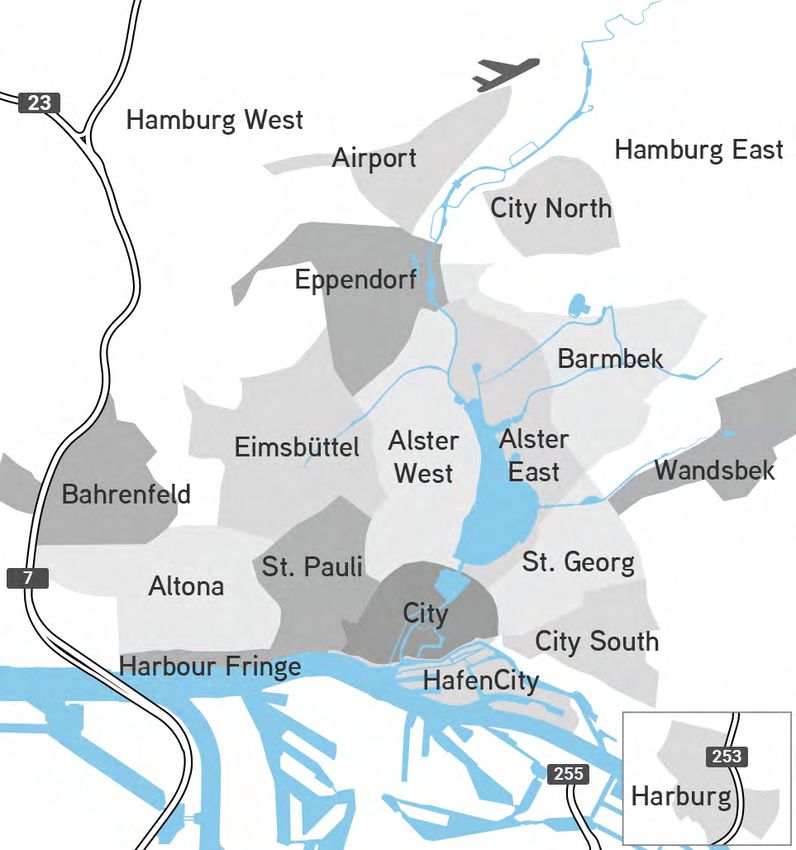

Hamburg

Office Leasing 41

Investment 43

Cologne

Office Leasing 47

Investment 49

Munich

Office Leasing 53

Investment 55

Stuttgart

Office Leasing 59

Investment 61

Research Services 64

Glossary 66

Contacts /Locations 67

4

MARKET DATA

Office Leasing

Market Data | 2020 / 2021

City Survey Germany | Colliers International

TOP 7 Berlin Düsseldorf Frankfurt Hamburg Cologne Munich Stuttgart

Stock of Office Space in million sqm 92.83 20.90 7.86 11.49 13.99 7.92 22.50 8.17

Office Space Take-up 2020 in sqm 2,555,100 734,000 248,000 329,500 334,300 202,000 567,800 139,500

Change year-on-year in % – 35.3 – 28.7 – 47.8 – 40.1 – 37.6 – 26.5 – 26.3 – 55.3

Forecast for 2021

Office Space Take-up in sqm 3,457,000 750,580 344,500 505,300 525,000 296,600 762,600 272,500

Average 2010 –2019

Prime Rent in € / sqm 41.10 28.50 45.00 30.00 25.75 39.50 25.50

Forecast for 2021

Average Rent in € / sqm 28.70 16.30 23.00 17.10 15.90 21.50 16.60

Forecast for 2021

Vacant Office Space in sqm 3,269,900 354,000 436,500 810,200 413,300 219,300 787,900 248,700

Vacancy Rate in % 3.5 1.7 5.5 7.1 3.0 2.8 3.5 3.0

Change year-on-year in bp* 60 50 – 40 20 50 60 130 110

Forecast for 2021

The data for Berlin, Düsseldorf, Hamburg and Cologne are related to the respective city area. The data for Frankfurt, Munich and Stuttgart are related to each of the

respective markets on the whole.

* basis points

Investment

Germany TOP 7 Berlin Düsseldorf Frankfurt HamburgCologne Munich Stuttgart

Transaction Volume 2020 in million € 59,247 30,576 8,549 3,220 6,335 5,008 1,450 4,969 1,045

Change year-on-year in % – 17.3 – 30.6 – 29.8 – 16.1 – 19.2 16.7 – 55.2 – 54.4 – 40.5

Forecast for 2021

Transaction Volume in million € 43,599 24,702 5,658 2,127 5,220 3,473 1,501 5,459 1,264

Average 2010 – 2019

Prime Yield Offices in % 2.80 3.20 3.00 3.00 3.30 2.70 3.10

Prime Yield High Street Retail in % 3.20 3.40 2.80 3.30 3.40 2.80 3.30

Prime Yield Logistics in % 3.70 **

** Refers to the defined logistics market areas

5

City Survey Germany | Colliers International

Commercial Real Estate Market Germany | 2020 / 2021

COMMERCIAL

REAL ESTATE

MARKET

GERMANY

OFFICE LEASING

6

INVESTMENT

9

RETAIL INVESTMENT

12

INDUSTRIAL AND

LOGISTICS INVESTMENT

15

HOTEL INVESTMENT

18

6

OFFICE LEASING

Commercial Real Estate Market Germany | 2020 / 2021

City Survey Germany | Colliers International

Take-up Following a slow start to the year, the

German office leasing market hit its

The German office leasing market was hit

trough in Q3 with take-up at just under

hard by the Covid-19 pandemic. In early

600,000 sqm. Sentiment improved at

2020, the global economic downturn

year-end and Q4 2020 posted the year’s

mainly impacted manufacturing and ex-

highest quarterly take-up of 712,300 sqm.

port-oriented sectors. At the latest by

spring, however, almost all sectors have

Activity proved livelier in Berlin than in

found themselves in a recession. As ex-

Germany’s other top 7 cities. The German

pected, the office leasing market is being

capital recorded 734,000 sqm in take-up

affected by the economic crisis as well.

in 2020, only slightly below the ten-year

Expansion plans have been postponed or

average of 750,000 sqm. Annual take-up

are simply not being implemented as the

in the other cities came in 25% to 50%

result of the pandemic. Roughly 2.6 mil-

below the long-time average. Most loca-

lion sqm in take-up was posted in Germa-

tions only saw a handful of large-scale

ny’s 7 top office hubs in 2020, down

leases signed for over 10,000 sqm.

roughly 35% compared to the previous

Leases targeting over 5,000 sqm were

year’s exceptional results and around

also scarcer than in the previous year.

25% below the ten-year average. Never-

Take-up of small and medium-scale units

theless, 2020 take-up results are still

was not as heavily impacted by the

higher than they were during the 2009

pandemic with some locations posting

financial crisis, in which only 2.3 million

relatively substantial results.

sqm of office space was taken up.

Fast Facts Figure 1: Office Space Take-up in the TOP 7

in million sqm

Office Leasing TOP 7 2020 Change

year-on-year

4,5 4.2

Office Space Take-up 2,555,100 sqm – 35.3% 3.9 3.8 3.9

3,5

Vacant Floor Space 3,269,900 sqm 22.9%

4,0

Vacancy Rate 3.5% 60 bp* 3.0

3,0 2.6

Office Space Stock 92.83 million sqm 0.2%

2,5

* basis points

2,0

1,5

1,0

0,5

0,0

2016 2017 2018 2019 2020 2021

Whole year Forecast

Average 2016 – 2020

7

Rents landlords in the form of rent-free periods

began to play an increasingly important

City Survey Germany | Colliers International

Commercial Real Estate Market Germany | 2020 / 2021

The increase in prime rents over the past

role towards the end of the year.

several years, sometimes in the double

digits, stopped short in early 2020, and

prime rents have been trending sideways Supply and Vacancy

ever since. The only exception is Stutt-

Unlike 2019, vacancy increased across

gart, where prime rents rose more than

the board with the exception of Düssel-

6% to a current €25.50 per sqm. Prime

dorf. However, the wave of vacancies

rents in Frankfurt fell slightly by 50 cents

feared by some market participants did

to €45.00 per sqm, allowing the city to

not materialize. Vacancies were only up

keep its status as having the highest

moderately with the vacancy rate still

prime rents in Germany. Frankfurt pri-

below the 5% threshold in all cities except

marily has this reputation due to the

for Düsseldorf and Frankfurt, indicating

unique office space offered by the city’s

a tense market situation.

CBD combined with the presence of

solvent tenants from the consulting, com-

Although the practice of subletting

munication and finance sectors.

increased in significance in H2, offers

remained scattered and subletting has

The situation around average rents paint-

yet to become a widespread phenomenon.

ed a diverse picture. Average rents in

The average share of vacancies in the

Berlin, Frankfurt and Munich continued to

TOP 7 is less than 10%.

rise considerably by 9%, 8% and 7%, re-

spectively. Tenants in Berlin could expect

Only a few new-build developments saw

to pay an average of €28.70 per sqm with

their completion delayed and around

€21.50 per sqm the standard in Munich

1.7 million sqm of new office space hit the

and €23.00 per sqm in Frankfurt. Düssel-

market in 2020. Almost 80% of that space

dorf experienced a very different trend

had been taken up by year-end. A similar

with average rents down almost 6% to

amount of office space is scheduled for

€16.30 per sqm. Incentives granted by

Figure 2: Completions of Office Properties in the Figure 3: Vacancy Rate in the TOP 7 in %

TOP 7 in total in 1,000 sqm and Vacancy in million sqm

2,000 1,888 6

1,739 1,697 4.9 %

5

1,500 4.1 %

1,226 4 4.4

3.5 %

1,070 3.1 %

3.7 2.9 %

939

1,000 843 3 3.3

770 774 2.9

2.7

2

500

1

0 0

2016 2017 2018 2019 2020 2021 2022 2016 2017 2018 2019 2020

Completions Pre-let Vacancy Vacancy Rate

Average 2016 – 2020

8

completion in the next two years as well. The start of vaccinations and general up-

Around 63% of the space scheduled for swing in the economy give cause for hope.

Commercial Real Estate Market Germany | 2020 / 2021

City Survey Germany | Colliers International

completion in 2021 has been preleased According to the ifo Business Climate

along with 40% of the space scheduled Index, company business sentiment for

for completion in 2022. Despite the spike 2021 was up in December and a number

in remote working since the spring, com- of economic forecasts are predicting GDP

panies do not appear to be turning their growth of over 4%. This positive outlook

backs on the office despite the fact that will trigger a boost in demand on the of-

working from home is gaining increasing fice markets, albeit somewhat delayed.

acceptance with employers and their Due to the second wave of the pandemic,

employees. Offices will continue to be the we do not expect the markets to return

main hub for communication and innova- to pre-crisis levels in the near future.

tion going forward. However, a result of 3.0 million sqm take-

up is feasible.

Summary and Outlook

2020 was a challenging year for the office

leasing market. Many companies were

Philipp Allroggen more reserved in their leasing activity

Junior Consultant I Research than in past years because of the Covid-19

+49 211 862062-40 crisis and the uncertainties it has brought

philipp.allroggen@colliers.com with it.

Figure 4: Vacancy Rate in the TOP 7 in % Figure 5: Average Rents in the TOP 7 in €/sqm

15 30

28

26

24

10

22

20

18

5

16

14

12

0 10

Q4 16 Q4 17 Q4 18 Q4 19 Q4 20 Q4 16 Q4 17 Q4 18 Q4 19 Q4 20

Berlin Düsseldorf Frankfurt Hamburg Berlin Düsseldorf Frankfurt Hamburg

Cologne Munich Stuttgart Cologne Munich Stuttgart

9

INVESTMENT

City Survey Germany | Colliers International

Commercial Real Estate Market Germany | 2020 / 2021

Transaction Volume Supply and Demand

German commercial real estate assets Investor confidence in the German real

posted a transaction volume of €59.2bn in estate market was quick to rebound fol-

2020, reflecting the third-best result in lowing a brief orientation phase in Q2.

the past decade while significantly ex- With ten large-scale transactions chang-

ceeding the €50bn mark for the sixth year ing hands for over €250m in Q1, this num-

in a row despite the Covid-19 pandemic. ber halfed to five in Q2, bounced back to

Q4 contributed €18.2bn, or 31%, to the ten in Q3 and increased to thirteen in Q4.

annual result, slightly exceeding the re-

cord start to the year of €17.7bn. This indi- The year’s highest-volume deal by far was

cates a return to the upward trend that the TLG portfolio acquisition for around

characterized the investment market in €4bn in Q1 within the scope of the

H2 2020 following the relatively moderate Aroundtown merger. This noteworthy

impact of the first lockdown, with market deal alone accounts for one-fifth of the

activity even gaining additional momen- annual total volume generated by portfolio

tum in the last three months of the year. acquisitions, reflecting €20.9bn, or a 35%

market share. The largest single-asset

Investors continue to focus on Germany’s deal of the year was Silberturm in Frank-

top 7 investment hubs, pouring roughly furt, which was sold on behalf of Sam-

€30.6bn, or 52% of transaction volume, sung Life Insurance and asset manager

into these markets in 2020. However, de- Hines to Austrian Imfarr Beteiligungs AG

spite the fact that there were high-volume and Swiss SN Beteiligungen Holding AG.

deals signed in H2, none of the country’s The deal marks an important milestone

top 7 investment locations were able to for the overall market in terms of the re-

exceed the €10bn mark in 2020 as Berlin turn of foreign investors, particularly

and Munich managed in 2019. from Asia, after the lockdown in March.

Fast Facts Figure 1: Total and Office Transaction Volume in

Germany in billion €

Transaction Volume in million € 2020 2019 Change

Commercial Properties total 59,247 71,630 – 17.3% 80

71.6

Total Top 7 30,576 44,047 – 30.6% 70

60.6 59.2

57.3 57.5

Type of transaction 60

52.6

Individual Transactions 38,341 50,576 – 24.2% 50

40.5

Share in the TOP 7 23,324 34,908 – 33.2% 40

Portfolio Transactions 20,906 21,053 – 0.7% 30.9

30 24.9 26.7

Share in the TOP 7 7,252 9,140 – 20.7% 20.4

20

Source of capital

10

Share by International Buyers 25,344 30,436 – 16.7%

0

Share in the TOP 7 13,151 19,841 – 33.7%

2016 2017 2018 2019 2020 2021

Share by International Sellers 17,900 30,526 – 41.4% Transaction Volume in Germany Forecast

Share in the TOP 7 9,126 20,356 – 55.2% thereof Office Properties Average 2016 – 2020

10

Foreign investors accounted for an overall particularly in Q4. As a result, prime

market share of 43% and a transaction vol- yields are currently posting anywhere

Commercial Real Estate Market Germany | 2020 / 2021

City Survey Germany | Colliers International

ume of €25.3bn. Domestic investors with from 2.70% in Munich to 3.30% in

their strong equity base, however, acted as Cologne. However, building quality and

a particularly stabilizing factor in the face length of lease term are playing an in-

of the crisis over the course of the year. creasingly important role in determining

German institutional investors proved the purchase price and marketability of

quite active in the small-to-medium market a property. Highly sought-after logistics

segment of under €100m, particularly in properties that meet current market

Q2 and Q3 when foreign investors tended standards recorded the most substantial

to prefer a wait-and-see stance. Through- price increases throughout 2020. Aver-

out all of 2020, German institutional inves- age prime yields in Germany’s top

tors dominated this size segment with a locations came to 3.70% in December.

market share of 75% and a 57% market However, we expect to see considerable

share across all size segments. price reductions outside the premium

segment. Office/retail mix buildings in

Open-ended real estate funds and special prime locations were only sporadically

funds took the lead buy-side with €13.2bn, involved in deals in 2020, with yields ris-

or 22%, ahead of asset and fund manag- ing in many markets.

ers with €11.6bn, or 20%, and listed prop-

erty companies with €7.1bn, or 12%.

Office Investment

Office assets were able to strengthen

Yields

their lead and increase their market share

Gross prime yields experienced further to 46% in the past three months. Discus-

compression ranging between 5 bps and sions surrounding the topic of the office

20 bps in Germany’s office hubs of Mu- of the future in light of the current trend

nich, Düsseldorf, Hamburg and Stuttgart towards remote and flexible working

due to excess demand for core assets, arrangements as well as the pandemic’s

Figure 2: Transaction Volume Figure 3: Buyer and Seller Groups in Germany

by Size Category 2020 share in % in billion €

upupto to € 10

€ 10 m m5%5% 00 5 5 1010 1515 20

20

€ 10

€ 10 mmto to € 25

€ 25 m m10%10% Open-ended

Open-ended Real

Real Estate

Estate Funds/Special

Funds/Special Funds

Funds

€ 25

€ 25 mmto to € 50

€ 50 13%

m m13% Asset

Asset Managers/Fund

Managers/Fund Managers

Managers

Listed

Listed Property

Property Companies

Companies

Property

Property Developers

Developers

€ 50

€ 50 mmto to € 100

€ 100 15%

m m15%

Insurance

Insurance Companies

Companies

Other

Other Investors

Investors

€ 100

€ 100 mmto to € 250

€ 250 26%

m m26% Property

Property Developers

Developers

above € 250

above € 250 m 31% m 31% Listed

Listed Property

Property Companies

Companies

Asset

Asset Managers/Fund

Managers/Fund Managers

Managers

Open-ended

Open-ended Real

Real Estate

Estate Funds/Special

Funds/Special Funds

Funds

Corporates/Owner-occupiers

Corporates/Owner-occupiers

Other

Other Investors

Investors

Buyers

Buyers Sellers

Sellers11

overall economic impact on the leasing break of the pandemic. In the current

markets do not fundamentally call into market environment, off-market options

City Survey Germany | Colliers International

Commercial Real Estate Market Germany | 2020 / 2021

question the segment’s significance as an should prove more popular than struc-

asset class. Compared to the exceptional tured sales processes. With pressure to

€40.5bn recorded in the office segment invest high, we expect transaction volume

in 2019, transaction volume was down to come in between €55bn and €60bn in

one-third to €27.1bn. At the start of the 2021 despite the many uncertainties still

pandemic, investors tended to shy away impacting the markets.

from investments in high-volume proper-

ties, which had fueled previous-year

results. This particularly affected the of-

fice segment.

Summary and Outlook

Unlike the first lockdown, the underlying

sentiment among investors following the

announcement of a second lockdown was

positive to optimistic. Market players have

learned that it is possible to conduct most

steps in a transaction digitally, even if the

process may take somewhat longer.

The crisis has brought with it opportuni-

ties in certain asset and risk classes. In

terms of the dip seen on the rental mar-

Susanne Kiese kets, however, which were hit harder by

Head of Research the crisis than the investment markets,

+49 211 862062-47 financial reviews of tenants and proper-

susanne.kiese@colliers.com ties will take longer than before the out-

Figure 4: Transaction Volume by Type of Property Figure 5: Office Prime Yield in the TOP 7 in %

in billion €

0 5 10 15 20 25 30 5.0

5.0

Office

Office

4.5

4.5

Retail

Retail

Industrial 4.0

4.0

Industrial

&& Logistics

Logistics

Building

Building Site

Site 3.5

3.5

Commerical

Commerical

Mixed

Mixed use

use 3.0

3.0

Hotel

Hotel

2.5

2.5

Other

Other properties

properties Q4 16 Q4 17 Q4 18 Q4 19 Q4 20

Berlin

Berlin Düsseldorf

Düsseldorf Frankfurt

Frankfurt Hamburg

Hamburg

Transaction

Transaction Volume

Volume Germany

Germany thereof

thereof TOP

TOP 77

Cologne

Cologne Munich

Munich Stuttgart

Stuttgart12

RETAIL INVESTMENT

Commercial Real Estate Market Germany | 2020 / 2021

City Survey Germany | Colliers International

Transaction Volume comprising 33 Metro wholesale stores,

which was sold by Aroundtown to P3, the

German retail assets changed hands in

European logistics platform of Singa-

2020 for roughly €11.4bn in total. Transac-

pore-based sovereign wealth fund GIC,

tion volume was up 12% yoy, with 2020

for around €800m.

replacing 2019 as the third-best year of

the decade. The trend reversal we saw at

These megadeals contributed considera-

the end of the year, with transaction

bly to the high market share claimed by

volume up 42% qoq, was particularly key

portfolio deals, which accounted for

in guaranteeing a positive end to a year

roughly two-thirds of total transaction

marked by the Covid-19 pandemic.

volume, or €7.7bn.

Supply and Demand Quantum’s sale of the Karstadt depart-

ment store on Mönkebergstraße in

The highest-volume retail deals in 2020,

Hamburg to Signa in Q3 for roughly

however, were signed in Q1, including

€250m was the largest single-asset deal

the sale of more than 30 retail assets

in 2020. A total of five single assets were

within the scope of the TLG acquisition

sold in 2020 in the 9-figure range, two

by Aroundtown. In terms of transaction

of which changed hands in Q4. Even after

volume, the retail portion of the mixed

the second lockdown was imposed,

portfolio accounted for around 25% of

market activity remained intact.

the deal’s total volume of €4bn. Of similar

scope was the deal involving a portfolio

Pure-play food retail has become the

comprised of 80 Real hypermarkets,

major driver behind investment activity in

which was acquired by Russian SCP

terms of use type. Between 2016 and

Group from Metro for around €900m.

2020, transaction volume involving this

Q4 saw the sale of the Matrix portfolio

Fast Facts Figure 1: Transaction Volume Retail

in billion €

Investment 2020 2019

Transaction Volume in million € 11,365 10,122 16

Portfolio Transactions 67% 57% 14

TOP 7 21% 33% 11.9

12 11.4

Share by International Buyers 52% 39% 9.8 10.1

10 9.2

Share by International Sellers 42% 53%

8

Prime Yield High Street Retail 2.80% 2.75%

6

4

2

0

2016 2017 2018 2019 2020

Whole year Average 2016 – 202013

retail segment more than tripled to a re- ed by office-retail mix assets and shop-

cord €2.0bn from a previous €0.6bn. ping centers correlates with the low rate

City Survey Germany | Colliers International

Commercial Real Estate Market Germany | 2020 / 2021

Discounters, supermarkets and hyper- of transactions recorded in Germany’s

markets experienced a boom in 2020 due top 7 investment hubs, with market share

to the Covid-19 pandemic with volumes down to 21% yoy from 33% in 2019.

increasing 30% in 2020 alone. The share

in total retail investment claimed by this Foreign investors accounted for a 52%

sector has risen steadily over the past five market share and German investors for

years from 6% to 18%. 48%. In light of the major deals outlined

above, the dominant investor groups rank

Retail warehouses and retail parks ac- as follows: Open-ended real estate funds

counted for €5.7bn this past year, reflect- and special funds (€2.2bn, or 19%) led the

ing half of total retail transaction volume pack buy-side followed by listed property

and an increase of 13 percentage points companies and asset and fund managers

yoy. Downtown office-retail mix proper- (both with €2.0bn, or 18%). Listed proper-

ties in prime locations, which also include ty companies dominated sell-side with

department stores, came in second place €4.5bn, or 39%, ahead of asset and fund

with €4.0bn, or 35%, down 10 percentage managers (15%) and open-ended real

points yoy. Deals like the one in Hamburg estate funds and special funds (13%).

also show that investors are becoming

increasingly aware of opportunities to

Yields

reposition downtown assets with high

footfall as mixed-use properties. Al- The yield trend of different usage types

though this trend is still in its infancy, it continued to diverge, reflecting differenc-

continues to grow in significance because es in investor demand. Highstreet assets

of the pandemic. Shopping centers regis- in Germany’s 7 major investment hubs

tered a d

ecrease in market share from have departed from their historically low

18% to 15% and generated a transaction yield levels and currently range between

volume of €1.7bn. The low share generat- 2.80% in Munich and Frankfurt and 3.40%

Figure 2: Transaction Volume by Type of Figure 3: Transaction Volume by Buyer and

Building 2020 share in % Seller Groups in billion €

RetailWarehouses/Retail

Warehouses/RetailParks 50%

Parks 50%

Retail 00 11 22 33 44 55

Open-endedReal

Open-ended RealEstate

EstateFunds/Special

Funds/SpecialFunds

Funds

ListedProperty

PropertyCompanies

Companies

HighStreet

High 35%%

Street 35 Listed

AssetManagers/Fund

Asset Managers/FundManagers

Managers

OpportunityFunds/Private

Opportunity Funds/PrivateEquity

EquityFunds

Funds

PensionFunds

Pension Funds

OtherInvestors

Other Investors

ListedProperty

Listed PropertyCompanies

Companies

Asset Managers/Fund Managers

Asset Managers/Fund Managers

ShoppingCenters

Shopping 15%

Centers 15%

Open-ended Real Estate Funds/Special Funds

Open-ended Real Estate Funds/Special Funds

PropertyDevelopers

Property Developers

Closed-ended Real Estate Funds

Closed-ended Real Estate Funds

OtherInvestors

Other Investors

Buyers

Buyers Sellers

Sellers14

in Düsseldorf and Cologne, while shop- Summary and Outlook

ping centers in high-footfall locations are

Commercial Real Estate Market Germany | 2020 / 2021

City Survey Germany | Colliers International

The Covid-19 pandemic shows how im-

posting yields at 4.80%. Prime yields for

portant it is to evaluate retail assets

retail parks continue moving toward

particularly in terms of their resilience

4.00%, which is lower than those record-

based on their heterogeneous composi-

ed for shopping centers in prime loca-

tion. While downtown brick-and-mortar

tions. Some stand-alone retail warehous-

fashion retailers took a heavy hit, other

es are posting yields well below the

sectors are benefiting from a selective

5.00% mark, while food retail is trading at

boom including grocery as well as

a significant premium.

non-food sectors such as recreation,

sporting goods and DIY. Even in this

challenging environment and thanks to

the comparatively small-volume retail

Susanne Kiese warehouse and retail park segments

Head of Research as the main driver, annual transaction

+49 211 862062-47 volume came in at well over €10bn, which

susanne.kiese@colliers.com we expect will set the bar for next year.

Figure 4: Prime Yield High Street Retail in %

4.5

4.0

3.5

3.0

2.5

2.0

Q4 16 Q4 17 Q4 18 Q4 19 Q4 20

Berlin Düsseldorf Frankfurt Hamburg

Cologne Munich Stuttgart15

INDUSTRIAL AND LOGISTICS INVESTMENT

City Survey Germany | Colliers International

Commercial Real Estate Market Germany | 2020 / 2021

Transaction Volume tition and 2020 saw multiples in a range

that you would typically only expect for

The German industrial and logistics in-

office assets.

vestment market finished out 2020 with

an exceptional transaction volume total-

ing at roughly €7.5bn. Topping previ- Supply and Demand

ous-year results by 14%, this strong annu-

An above-average number of sale-and-

al result is second only to record year

leaseback transactions generated some

2017 (€8.7bn). Although the logistics

additional supply throughout the year.

asset class continued to rank third on the

This increase in sale-and-leaseback

overall commercial real estate market, it

transactions can primarily be attributed to

did manage to up its market share to 13%

economic fallout from the Covid-19 pan-

compared to the previous year’s 9%. 2020

demic, as some companies are seeking

was marked by remarkable deals that

liquidity by selling their own properties in

highlighted the strength and attractive-

this attractive market environment, in

ness of this asset class more than ever

part to bolster their operative growth and

before. The global Covid-19 pandemic

competitive position through corporate

created additional impetus for investment

acquisitions. This trend has meant a slight

in logistics assets and put the logistics

boost in investment opportunities and

asset class on the radar of many investors

has proven particularly beneficial to in-

for the first time. An increasing number of

vestors looking for new, sometimes

investors with very little or even no prior

riskier and more profitable opportunities

exposure to logistics were involved in

in a logistics investment market with very

bids for this asset class. Ongoing limited

little supply on offer.

supply, particularly in the core segment,

also served to intensify the fierce compe-

Fast Facts Figure 1: Transaction Volume Industrial

and Logistics in billion €

Investment 2020 2019

Transaction Volume in million € 7,478 6,566 8 7.6

Portfolio Transactions 35% 40% 7

TOP 7 33% 35% 5.8

6

Share by International Buyers 43% 60% 4.8

5

Share by International Sellers 28% 30% 3.9

4

Prime Yield Logistics in the TOP 7 (average in %) 3.70% 4.20% 3.2

2.9

3

1.8 1.7

2 1.4

1.1

1

4.6 8.7 6.8 6.6 7.5

0

2016 2017 2018 2019 2020

Logistics Industrial TAV in total

Average 2016 – 202016

German investors generated the majority sale of the Roots portfolio featuring 14 as-

of annual transaction volume, pouring sets, which was bought by AEW Europe

Commercial Real Estate Market Germany | 2020 / 2021

City Survey Germany | Colliers International

roughly €4.2bn into industrial and logis- for over €500m in Q4, and Union Invest-

tics assets and increasing their market ment’s acquisition of the Rocket portfolio.

share by another 18 percentage points yoy

to 57%. Because of travel restrictions,

Yields

foreign investors had very limited oppor-

tunities to schedule property viewings The boom in investor demand for logistics

or on-site visits. This situation caused and the resulting fierce competition for

their market share to drop significantly these assets led to significant yield com-

over the course of the year. Remarkably, pression in Germany this past year. While

the logistics investment market was able the average gross prime yields for state-

to achieve such strong annual results of-the-art logistics assets in Germany’s

without the help of major portfolio deals top logistics regions came to roughly

in the multi-billion-euro range. Transac- 4.20% in 2019, they fell a further 50 bps to

tion volume for logistics assets even below 3.70% over the course of 2020 (re-

managed to come in just behind the ex- flecting a net yield of around 3.30%).

ceptional record-breaking year of 2017. Some of the deals finalized in 2020 were

Portfolio deals accounted for around absolute outperformers in terms of the

€2.6bn, reflecting a 35% share in total total package they offered. These proper-

transaction volume. One of the largest ties saw purchase price multiples in ex-

portfolio deals to change hands in 2020 cess of 28x based on annual net rent. Mul-

was Union Investment’s acquisition of the tiples in this range are typically more

European Logistrial portfolio early in the common in the office and residential mar-

year. The deal posted a volume of roughly kets. As a result, the purchase prices

€800m with more than half of total value achieved per square meter in some cases

generated by the portfolio’s assets in exceeded the €2,000 mark, setting the

Germany. Other portfolio deals to change tone for future transactions with similar

hands in the mid-9-figure range were the features.

Figure 2: Transaction Volume Figure 3: Transaction Volume by Buyer and

by Size Category 2020 share in % Seller Groups in billion €

upup

to to € 10 6%

m m6%

€ 10

00 1 1 22 3 3 44

Asset

Asset Managers/Fund

Managers/Fund Managers

Managers

€ 10

€ 10 mmto to € 30

€ 30 19%

m m19% Open-ended

Open-ended Real

Real Estate

Estate Funds/Special

Funds/Special Funds

Funds

Corporates/Owner-occupiers

Corporates/Owner-occupiers

Insurance

Insurance Companies

Companies

Property

Property Developers

Developers

€ 30 11% Other Investors

€ 30 mmto to € 50

€ 50 m m11% Other Investors

Property

Property Developers

Developers

€ 50

€ 50 mmto to € 100

€ 100 14%

m m14% Asset Managers/Fund Managers

Asset Managers/Fund Managers

above € 100 m

above € 100 m 50% 50% Open-ended Real Estate Funds/Special Funds

Open-ended Real Estate Funds/Special Funds

Corporates/Owner-occupiers

Corporates/Owner-occupiers

Pension

Pension Funds

Funds

Other

Other Investors

Investors

Buyers

Buyers Sellers

Sellers17

Outlook

City Survey Germany | Colliers International

Commercial Real Estate Market Germany | 2020 / 2021

The growth trend in e-commerce speaks

to the increasing attractiveness and im-

portance of logistics assets in Germany.

Due to the spread of the Covid-19 pan-

demic in 2020 and the resulting restric-

tions on everyday life, more and more

people are choosing to order online and

have groceries delivered to their homes.

This has considerably increased parcel

delivery volumes in Germany and trig-

gered greater demand for warehouse and

logistics space. We also expect growing

pressure to optimize and innovate in some

areas of traditional industry in the

post-Covid-19 era to lead to calls for lean-

er operations in modern logistics assets.

Because the logistics sector has once

Nicole Kinne again proven resilient in times of crisis,

Associate Director I we anticipate that the run on industrial

Research Industrial & Logistics and logistics assets will continue,

+49 89 624294-792 possibly causing further yield compres-

nicole.kinne@colliers.com sion in 2021.

Figure 4: Prime Yield Logistics in the TOP 7

Average in %

6.0

5.5

5.0

4.5

4.0

3.5

Q4 16 Q4 17 Q4 18 Q4 19 Q4 2018

HOTEL INVESTMENT

Commercial Real Estate Market Germany | 2020 / 2021

City Survey Germany | Colliers International

Transaction Volume Supply and Demand

Hotel assets changed hands for a total of Similar to 2019, an increasing number of

€2.0bn in 2020. The hotel investment hotels changed hands within the scope of

market almost came to a standstill due to portfolio deals, which generated a market

the Covid-19 pandemic following a solid share of roughly 38%. Aroundtown’s take-

start to the year, in which Q1 brought in over of TLG in Q1 2020 was the primary

roughly €1.0bn in transaction volume. driver behind this high market share along

The unsteady recovery in Q3 was unable with several smaller portfolios that

to put down roots before the second changed hands over the course of the

wave of the pandemic and the restrictions year. The sale of nhow in Berlin was the

it brought with it again hit the hotel busi- largest single-asset deal of the year.

ness in general, and along with it, the Although a dozen additional assets broke

investment market for hotel assets. through the €50m barrier, most of the

Transaction volume fell almost 60% assets sold went for below €30m. Core

compared to strong previous-year results assets in good locations remained attrac-

and came up almost one-third short of tive and competitive despite the challeng-

the ten-year average. As overall commer- ing market environment. Conversions

cial transaction volume in Germany was have been gaining in significance as well

not nearly hit as hard by the Covid-19 with a growing number of hotel assets

crisis as the hotel segment, hotel assets sold for conversion projects in 2020,

saw their market share fall to 3%. particularly towards the end of the year.

Hotel assets are currently being convert-

ed into office and residential properties

as well as healthcare and mixed-use.

Fast Facts Figure 1: Transaction Volume Hotel

in billion €

Investment 2020 2019

Transaction Volume in million € 2,035 5,033 6

5.2

5.0

Portfolio Transactions 38% 27%

5

TOP 7 53% 60% 4.2

4.0

Share by International Buyers 41% 41% 4

Share by International Sellers 18% 30%

3

Prime Yield Hotel 4.01% 3.70% 2.0

2

1

0

2016 2017 2018 2019 2020

Whole year Average 2015 – 201919

One favorable development is the fact that Hotels in the 4-star segment remained the

foreign investors maintained their 41% most popular investment, pulling in a

City Survey Germany | Colliers International

Commercial Real Estate Market Germany | 2020 / 2021

market share buy-side despite the pan- market share of 56%. Second place went

demic. That means German hotel assets to 3-star hotels with a one-third share of

continue to attract foreign capital. Listed the market. Investment in budget and

property companies were the most active luxury hotels almost came to a complete

buy-side in 2020 with a market share of standstill with only a few deals registered.

just over 23%. Asset and fund managers Serviced apartments were the only hotel

followed in the ranks with 18% in the wake category to experience a favorable trend

of a considerably more active 2019 where with their share in total hotel transaction

they generated a share of 27%. While volume up five percentage points to 8%,

open-ended real estate funds and special or €166m. Serviced apartments have

funds were the most active buy-side into navigated the crisis well to date thanks to

2019, they slid to third place in 2020 with strong occupancy rates and are becoming

13%. increasingly popular with investors.

German investors dominated market Core assets are currently the most

activity sell-side and accounted for 82% popular among the risk classes. Supply,

of total transaction volume. As in previous however, is limited. Many investors are

years, property developers proved the avoiding core+ assets in the current

most active, selling assets valued at more market environment, particularly due to

than €724m, which reflects a market the tense situation currently being faced

share of almost 36%. Listed property by hotel operators. Value-add assets are

companies ranked second with 18%, rarely being sold as such but are rather

largely due to the TLG takeover. Family being further developed into core or core+

offices and private investors claimed assets before being listed on the market.

third place with 14%.

Figure 2: Transaction Volume by Star Segment 2020 Figure 3: Transaction Volume by Buyer and

share in % Seller Groups in billion €

0.0

0.0 0.5

0.5 1.0

1.0

4 Stars55%

4 Stars 55% Listed Property

Listed Companies

Property Companies

Asset

AssetManagers/Fund

Managers/Fund Managers

Managers

3 Stars33%

3 Stars 33% Open-ended Real Estate Funds/Special Funds

Open-ended Real Estate Funds/Special Funds

Property Developers

Property Developers

Private Investors/Family Offices

Private Investors/Family Offices

Other Investors

Other Investors

Property Developers

Property Developers

Boarding

Boarding House8%

House 8%

Listed Property Companies

Listed Property Companies

Private Investors/Family Offices

2 Stars2%

2 Stars 2% Private Investors/Family Offices

5 Stars1%1%

5 Stars Corporates/Owner-occupiers

Corporates/Owner-occupiers

1 Star1%1%

1 Star Asset Managers/Fund

Asset Managers

Managers/Fund Managers

Other Investors

Other Investors

Buyers

Buyers Sellers

Sellers20

As a result of these activities, the core Summary and Outlook

segment posted €1.1bn in transaction

Commercial Real Estate Market Germany | 2020 / 2021

City Survey Germany | Colliers International

The hotel segment is likely to face another

volume in 2020, reflecting a market share

difficult year in 2021. Convention hotels

of 59%. Core+ and value-add followed in

will particularly continue to suffer under

the ranks with 32% and 6%, respectively.

the ongoing restrictions. Operators are

expected to continue to pursue market

Yields consolidation. Hotel chains, particularly

those in the budget segment, appear to be

Yields for hotel investments remained

navigating the crisis more successfully.

stable over the course of the year. Munich

Major operators in the lower price seg-

continued to post the lowest gross prime

ment are even continuing with their ex-

yields at a flat 3.70% with yields in Berlin

pansion strategies. Core assets in top

at the other end of the spectrum at 4.40%.

locations remain an attractive investment

Gross prime yields nationwide are post-

and the same applies to properties boast-

ing at an average of roughly 4.00%. Be-

ing conversion potential, which offer

cause so few deals were transacted in

opportunity as well. We expect the market

2020, these numbers are based on limited

to return to pre-crisis levels no earlier

data.

than 2023. Look for market recovery to

move from the inside out and from bottom

to top. That means that hotels in down-

town locations will likely recover more

Philipp Allroggen swiftly than those located in city outskirts

Junior Consultant I Research and that demand for budget accommoda-

+49 211 862062-40 tion will pick up earlier than demand for

philipp.allroggen@colliers.com higher priced accommodation.

Figure 4: Prime Yield Hotel in %

6.0

5.5

5.0

4.5

4.0

3.5

Q4 16 Q4 17 Q4 18 Q4 19 Q4 20

Berlin Düsseldorf Frankfurt Hamburg

Cologne Munich Stuttgart21

City Survey Germany | Colliers International

City reports | 2020 / 2021

CITY

REPORTS

BERLIN

22

DÜSSELDORF

28

FRANKFURT

34

HAMBURG

40

COLOGNE

46

MUNICH

52

STUTTGART

5822 Berlin | 2020 / 2021

City Survey Germany | Colliers International BERLIN

CITY FACTS Berlin Fast Facts

Population in 1,000 3,669 Office Leasing Berlin 2020 Change year-on-year

Employees Paying Social Security Contributions 1,539 Office Space Take-up 734,000 sqm – 28.7%

in 1,000

Leasing Take-up 668,600 sqm – 32.4%

Unemployment Rate in % 10.1 Prime Rent 41.10 € / sqm 3.0%

Per Capita Disposable Income in € 22,294 Average Rent 28.70 € / sqm 9.1%

Vacancy Rate 1.7% 50 bp

Office Space Stock 20.90 million sqm 2.0%

Rents in € / sqm

Submarket Range of Rents

CBD City West 20.75 - 42.50

CBD City East 20.00 - 39.80

CBD Potsdamer Platz / Leipziger Platz 20.85 - 38.00

Central Station 28.00 - 35.00

Mediaspree 24.00 - 36.15

City West 17.00 - 32.00

City East 18.45 - 42.30

City Margins North 19.40 - 38.25

City Margins South 18.00 - 34.00

Periphery North 13.50 - 27.50

Periphery West 21.00 - 28.50

Periphery South 14.00 - 30.00

Periphery East 14.45 - 26.00

Adlershof 15.00 - 20.00

Schönefeld 14.45 - 16.2523

OFFICE LEASING

City Survey Germany | Colliers International

Berlin | 2020 / 2021

Take-up Market activity once again revolved

around the CBD City Ost and City Ost sub-

The Berlin office leasing market posted

markets, which contributed around

around 734,000 sqm in take-up in 2020,

253,000 sqm to total take-up. The largest

a good result in line with the ten-year

lease of 2020, which was signed by

average of roughly 750,000 sqm despite

insurer Deutsche Rentenversicherung for

the impact of the Covid-19 pandemic.

more than 84,000 sqm at the An den

The final quarter of the year proved par-

Treptowers property, was a major driver

ticularly robust with take-up coming in at

behind the above-average result posted

231,000 sqm. A number of large-scale

in the Mediaspree submarket of

leases signed for over 10,000 sqm played

113,000 sqm. Neighboring locations are

a significant role, accounting for more

also attracting increasing demand due to

than 300,000 sqm in take-up.

the ongoing supply bottleneck in central

locations. The City Periphery North and

Public administration was responsible for

City Periphery South submarkets both

roughly 270,000 sqm in take-up, generat-

benefited from current market conditions

ing a market share of almost 40%. With

and also ranked high among the city’s

this result, the public sector solidified its

most popular office locations. Take-up in

dominant position on the Berlin office

the City Periphery South submarket was

market. Companies from the ICT, banking

particularly impacted by the lease signed

and finance sectors trailed in the ranks at

by Deutsche Bahn for roughly 30,000 sqm

some distance, each falling just shy of

at EUREF-Campus on Torgauer Straße.

double-digit results.

Figure 1: Office Space Take-up in 1,000 sqm Figure 2: Completion Volume in 1,000 sqm

1,200 1,200

989

1,000 1,000

837

800 740 752 800

669

602

600 600 551

457

400 400 309

341

203 185

200 123 200

100

39 41 65

0 0

2016 2017 2018 2019 2020 2018 2019 2020 2021 2022

Leasing Owner-occupiers Completions thereof Pre-let/Owner-occupied24

Rents Key Developments

Berlin | 2020 / 2021

City Survey Germany | Colliers International

Office rents have been showing very little A total of 551,000 sqm are currently in the

change in the wake of the pandemic and development pipeline for 2021 with

remained high at year-end 2020. Prime around two-thirds of this space already

rents come to a current €41.10 per sqm taken up as at the start of the year. These

with average rents at €28.70 per sqm, developments are primarily targeting CBD

reflecting a yoy increase of 3% and 9%, locations in the City Ost and West submar-

respectively. Tenants were willing to pay kets and around the Berlin central station.

more than €35.00 per sqm for roughly

106,000 sqm of new office space.

Summary and Outlook

We can look for rents to continue to rise

Supply and Vacancy

slightly in 2021, albeit with significantly

Berlin’s extremely low vacancy rate of less momentum than in past years. Nu-

1.2% increased slightly over the course of merous businesses are on the lookout for

2020 to 1.7% at the end of December. large-scale units in 2021 as well, guaran-

The amount of space available for imme- teeing the Berlin market a solid founda-

diate tenancy rose yoy to around tion going forward despite the impact of

354,000 sqm. The situation in submar- the pandemic. We have yet to see a

kets outside Berlin’s suburban train ring dramatic drop in vacancy. Office proper-

remains particularly tense at below 1.0%. ties will continue to play an important

role for companies. In light of the above,

2021 is set to post another increase in an-

nual take-up to over 800,000 sqm.

Figure 3: Vacancy Rate in % and Vacancy Figure 4: Prime and Average Rents in ¤/sqm

in 1,000 sqm

600 567 45

41.10

39.90

500 40

35.10

390 35

400 31.30

354

28.50 28.70

3.0% 304 30

26.30

300

246

25

2.0% 21.70

200 1.7%

1.5% 19.15

1.2% 20

16.30

100 15

0 10

2016 2017 2018 2019 2020 2016 2017 2018 2019 2020

Vacancy Vacancy Rate Prime Rent Average Rent25

INVESTMENT

City Survey Germany | Colliers International

Berlin | 2020 / 2021

Transaction Volume The second wave of the pandemic in Q4

2020 was unable to stop the end-of-year

2020 was an unusual year that started off

rally on the Berlin market. The dip in

on Berlin’s commercial real estate invest-

market activity due to high uncertainty at

ment market as strong as record-year

the start of the pandemic created excess

2019 ended, which was with €12.2bn in

demand that hit the market in H2 and

transaction volume. Then market activity

boosted deal activity. Commercial trans-

came to an abrupt halt. Investors, howev-

action volume came in 50% above the ten-

er, quickly regained confidence in the

year average despite the crisis.

market, pouring €8.5bn into the city’s

commercial assets by year end, putting

2020’s strong transaction results in sec-

ond place after 2019.

Fast Facts

Investment Berlin 2020 2019

Transaction Volume 8,549 million € 12,172 million €

Portfolio Transactions 38% 17%

Share by International Buyers 52% 59%

Share by International Sellers 29% 46%

Most Important Property Type Office 64% Office 79%

Prime Yield Office 2.80% 2.90%

Figure 5: Transaction Volume in million € Figure 6: Transaction Volume by Type of

Property 2020 share in %

14,000

14,000 12,172 Office 64%

12,000 12,172 Office 64%

12,000

10,000 Retail 16%

10,000 8,549

Retail 16%

7,522 8,549

8,000 6,959

8,000 7,522

6,959

6,000 4,900 Building Site 6%

6,000 4,900 Building Site 6%

4,000 Hotel 4%

4,000 Hotel 4%

Industrial &

2,000 Industrial

Logistics 3%&

2,000 Logistics 3%

Other 7%

0 Other 7%

0

2016 2017 2018 2019 2020

2016 2017 2018 2019 202026

Supply and Demand Aroundtown’s takeover of TLG was the

largest portfolio deal in 2020. Listed

Berlin | 2020 / 2021

City Survey Germany | Colliers International

Office assets accounted for two-thirds of

property companies ranked most active

total transaction volume in 2020 with

buy-side (€2.4bn) and sell-side (€2.5bn)

€5.5bn. Retail assets ranked second with

as a result. Property developers came in

€1.4bn, or a 16% market share. Commer-

second sell-side with €1.6bn, followed

cial land sites posted above-average

closely by asset and fund managers,

transaction volume at over €500m, se-

which posted just under €1.6bn. Asset

curing third place.

and fund managers purchased assets in

the same volume and ranked third buy-

Large landmark deals such as those in the

side just behind open-ended real estate

record year 2019 with more than half a

funds and special funds with €1.8bn.

billion euros were absent in 2020. How-

ever, three single-asset deals were

Property developers in Berlin particularly

signed for over €250m. One of the year’s

benefited from the fact that demand for

most pricey deals was the sale of the

large-scale adjoining office space, some-

western section of the office complex at

thing that is hard to come by in stock prop-

Humboldthain. A section of the Focus

erties, remained quite high among tenants

Teleport office center in Moabit and the

from the public sector despite the pan-

Südkreuz Offices in Schöneberg joined

demic. Interest in assets guaranteeing

the ranks towards the end of the year.

long-term secure cashflow is on the rise.

The sale of Spreeturm at Postbahnhof in

the Mediaspree submarket was another

high-volume deal that changed hands for

just shy of €200m.

Figure 7: Transaction Volume by Buyer Groups Figure 8: Transaction Volume by Seller Groups

in million €, share in % in million €, share in %

Listed

Listed

Property

Property 28%

28% Listed

Listed

Property

Property 29%

29%

Companies

Companies Companies

Companies

Open-ended

Open-endedReal

Real

Estate

Estate 20%

20% Property

Property

Developers

Developers 19%

19%

Funds/Special

Funds/Special

Funds

Funds

Asset

Asset

Managers/

Managers/ 19%

19% Asset

Asset

Managers/

Managers/ 18%

18%

Fund

FundManagers

Managers Fund

FundManagers

Managers

Property

Property

Developers

Developers 7%7% Open-ended

Open-endedReal

Real

Estate

Estate 9%9%

Funds/Special

Funds/Special

Funds

Funds

Insurance

Insurance

Companies

Companies 6%6% Private

Private

Investors/

Investors/ 5%5%

Family

Family

Offices

Offices

Other

Other

Investors

Investors 20%

20% Other

Other

Investors

Investors 20%

20%

00 1,000

1,000 2,000

2,000 3,000

3,000 00 1,000

1,000 2,000

2,000 3,000

3,00027

Yields Summary and Outlook

City Survey Germany | Colliers International

Berlin | 2020 / 2021

Gross initial yields for core office assets Activity in 2020 has shown investor

dropped a further 10 bps yoy to 2.80%. confidence in the Berlin market remains

Increased demand for industrial and logis- strong, also and especially in times of

tics assets because of the pandemic trig- great uncertainty. Because we are still

gered strong yield compression of 50 bps. unable to predict the course of a pandem-

Retail assets in high-street locations saw ic that is still waging, we cannot realisti-

an increase of 10 bps in contrast. cally forecast transaction volume for 2021

with the necessary degree of precision.

The two property developments, IMPULS However, the development of promising

on Stresemannstraße and NEO on Knese- vaccines has been a major victory in the

beckstraße, both of which are under long- fight against Covid-19. As such, we have

term lease and were transacted within the reasonable cause to hope that life will

scope of forward deals, are representative soon be getting closer to normal and that

of the current trend in office yields. Fi- uncertainties around the market will

nancing for office investments with val- begin to fade. The development pipeline is

ue-add or opportunistic risk files, on the well-stocked at the moment and, com-

other hand, has become more expensive, bined with the benefits of the recent grand

leading to owners having to accept con- opening of Berlin’s BER airport, should

siderable price reductions of 10% to 15%. create the perfect conditions for even

While the parties involve were able to livelier market activity in 2021 with the

notarize the sale of the Goldstück office current year possibly even taking over

building in the Moabit district in 2020 at 2020's second-place ranking.

roughly €5,000 per sqm and an expected

yield of 5.60%, the sale of The Heinrich of-

fice complex in Schöneberg, which would

have likely been the largest single-asset

deal of the year, fell through as the parties

were unable to agree on the price.

The Berlin office leasing market remains robust despite

the impact of the pandemic. Rents continue to rise

and the boom on the investment market remains intact.

CONTACT

Margit Lippold Director | Research

+49 30 202993-43, margit.lippold@colliers.com28 Düsseldorf | 2020 / 2021

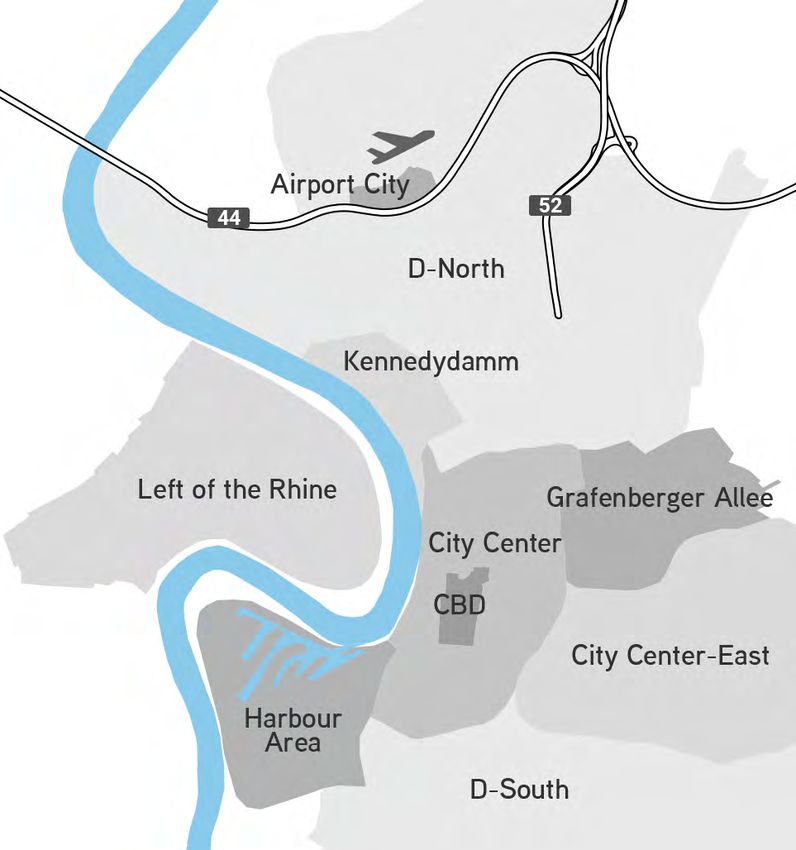

City Survey Germany | Colliers International DÜSSELDORF

CITY FACTS Düsseldorf Fast Facts

Population in 1,000 622 Office Leasing Düsseldorf 2020 Change year-on-year

Employees Paying Social Security Contributions 430 Office Space Take-up 248,000 sqm – 47.8%

in 1,000

Leasing Take-up 234,500 sqm – 50.2%

Unemployment Rate in % 8.0 Prime Rent 28.50 € / sqm 0.0%

Per Capita Disposable Income in € 28,528 Average Rent 16.30 € / sqm – 5.8%

Vacancy Rate 5.5% – 40 bp

Office Space Stock 7.86 million sqm 1.4%

Rents in € / sqm

Submarket Range of Rents

CBD 18.50 - 28.50

City Center 13.00 - 26.00

Harbour Area 16.50 - 25.00

Kennedydamm 16.50 - 25.00

Left of the Rhine 11.00 - 22.00

Düsseldorf-North 11.00 - 18.00

Airport City 14.50 - 17.50

Grafenberger Allee 12.00 - 14.50

City Center-East 10.00 - 16.00

Düsseldorf-South 9.00 - 12.0029

OFFICE LEASING

City Survey Germany | Colliers International

Düsseldorf | 2020 / 2021

Take-up Most space segments recorded signifi-

cant decreases in take-up compared

The Düsseldorf office leasing market

to the previous year, the sole exception

(municipal area only) recorded

being the segment of between 500 sqm

248,000 sqm in take-up in 2020, down

and 1,000 sqm, which posted an increase

48% as anticipated compared to the previ-

of roughly 5% yoy. The medium and

ous year’s all-time high of 475,000 sqm.

large-sized space segments saw take-up

These results can be attributed to to the

drop significantly compared to the previ-

restrictions imposed due to the pandemic.

ous year’s excellent result, as considera-

Looking at performance over the course

bly fewer leases were signed in 2020.

of the year, take-up was noticeably up in

Q3 compared to a very weak Q2 at around

In terms of location, the majority of

60,000 sqm. Activity dropped again

take-up tended to revolve around three

slightly in Q4 due to the stricter Covid-19

different submarkets. The City Center

restrictions implemented around that

East submarket led the pack with

time. Around 25% of 2020 annual take-up

41,000 sqm thanks a large-scale lease

can be attributed to the public sector.

signed by the financial administration

Consulting firms, which typically com-

office, closely followed by the Düsseldorf

prise one of the city’s strongest tenant

North and Linksrheinisch submarkets

groups, increased their activity noticeably

with roughly 39,000 sqm each.

in H2, putting them in second place with

an overall market share of 14%.

Figure 1: Office Space Take-up in 1,000 sqm Figure 2: Completion Volume in 1,000 sqm

500

500 471

471 150

150

400

400 120

120 111

111 114

114

359

359

322

322 323

323

92

92

86

86

300

300 90

90

235

235 73

73 70

70 69

69

200

200 60

60

100

100 30

30

77 1111 15

15 44 13

13

00 00

2016

2016 2017

2017 2018

2018 2019

2019 2020

2020 2018

2018 2019

2019 2020

2020 2021

2021 2022

2022

Leasing

Leasing Owner-occupiers

Owner-occupiers Completions

Completions thereof

thereofPre-let/Owner-occupied

Pre-let/Owner-occupiedYou can also read