Swedbank Economic Outlook - January 2018 - "Swedbank" Žinių terasa

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Swedbank Economic

Outlook

January 2018

Completed: January 23, 2018, 17:00 CET

Disseminated: January 24, 2018, 08:00 CET

Welcome to Swedbank

Economic Outlook!

Swedbank Economic Outlook presents the latest economic forecasts for

Sweden, the Baltics and the major global economies. In a series of in-

depths, current issues that have a bearing on the economic developments

are analysed.

Swedbank Economic Outlook is a product made by Swedbank Macro Research.

Swedbank Research

Olof Manner

olof.manner@swedbank.se

Head of Research

+46 8 700 91 34

Macro Research

Sweden Maija Kaartinen Lija Strasuna

maija.kaartinen@swedbank.se lija.strasuna@swedbank.lv

Anna Breman

Research Assistant Senior Economist

anna.breman@swedbank.se

+358 50 4688 759 +371 6744 5844

Group Chief Economist

+46 70 314 95 87

Jörgen Kennemar Linda Vildava

jorgen.kennemar@swedbank.se linda.vildava@swedbank.lv

Oscar Andersson

Senior Economist Junior Economist

oscar.andersson@swedbank.se

+46 8 700 98 04 +371 6744 42 13

Junior Economist

+46 8 700 92 85

Ingrid Wallin Johansson Lithuania

ingrid.wallin-johansson@swedbank.se Nerijus Mačiulis

Martin Bolander

Economist nerijus.maciulis@swedbank.lt

martin.bolander@swedbank.se

+46 8 700 92 95 Chief Economist Lithuania

Senior Economist

+46 8 700 92 99 +370 5258 22 37

Estonia

Cathrine Danin Tõnu Mertsina Laura Galdikiené

cathrine.danin@swedbank.se tonu.mertsina@swedbank.ee laura.galdikiene@swedbank.lt

Economist Chief Economist Estonia Senior Economist

+46 8 700 92 97 +372 888 75 89 +370 5258 22 75

Liis Elmik Vytenis Šimkus

Jana Eklund

vytenis.simkus@swedbank.lt

jana.eklund@swedbank.se liis.elmik@swedbank.ee

Economist

Senior Econometrician Senior Economist

+370 6945 71 95

+46 8 5859 46 04 +372 888 72 06

Norway

Marianna Rõbinskaja

Josefin Fransson Øystein Børsum

marianna.robinskaja@swedbank.ee

josefin.fransson@swedbank.se ob@swedbank.no

Economist

Assistant Chief Economist Norway

+372 888 79 25

+46 8 5859 03 05 +47 99 50 03 92

Åke Gustafsson Latvia

Ingvild Almestad Aasen

ake.gustafsson@swedbank.se Mārtiņš Kazāks ingvild.aasen@swedbank.no

Senior Economist martins.kazaks@swedbank.lv Economist

+46 8 700 91 45 Deputy Group Chief Economist/Chief Economist +47 48 12 63 30

Latvia

Knut Hallberg +371 6744 58 59 Kjetil Martinsen

knut.hallberg@swedbank.se kjetil.martinsen@swedbank.no

Senior Economist Agnese Buceniece Senior Economist

+46 8 700 93 17 agnese.buceniece@swedbank.lv +47 92 44 72 09

Economist

Alexandra Igel +371 6744 58 75

alexandra.ext.igel@swedbank.se

Research Assistant

+46 73 999 42 15

Table of content

Summary____________________________________________________________________________ 4

Regions

United States_________________________________________________________________________ 6

Europe ______________________________________________________________________________ 7

Asia/Emerging markets_________________________________________________________________ 9

Sweden _____________________________________________________________________________ 11

Nordics ______________________________________________________________________________ 14

Baltics_______________________________________________________________________________ 17

Interest and exchange rate forecasts______________________________________________________ 20

In-depths

Sustainability Indicators________________________________________________________________ 22

Sweden vs. Norway housing – similar yet different___________________________________________ 24

Demographics and the reversal of falling interest rates________________________________________ 26

Appendices: Forecast tables _____________________________________________________________ 28

Information to client ___________________________________________________________________ 30

Recording date of price data 2018-01-18

The Swedbank Economic Outlook is available at: www.swedbank.com/seo.

Cover image: Getty Images

LEADER AND SUMMARY

Global growth – impressive so far, pitfalls ahead

As we enter 2018, the outlook for global growth is on a stronger footing. Euro

area growth keeps improving, while the US has kept up speed. Emerging mar-

kets are enjoying a positive momentum. The global cyclical upswing benefits the

Nordic and Baltic economies. Political risks have abated somewhat, in particular

in Europe. The rise of populism, however, still warrants concern as increased

protectionism and geopolitical instability pose a risk to the short-run outlook.

In the long run, populist policies could undermine political and economic

institutions that are crucial for long-run growth prospects.

Euro area coming out of a 10-year The euro area recovery is gaining speed. Households have deleveraged

slump after the financial crisis and the euro crisis. They are enjoying a firming

labour market. Employment is growing at 1.7% in annual terms, which helps

boost disposable incomes and household consumption. Firms are investing,

and exports have picked up markedly. France, Spain, and Germany are all

expected to deliver growth at 2% or above in 2018. The firming labour

market has been slow to deliver higher wages, and core inflation remains

low. Still, the ECB is sending increasingly upbeat signals, and asset purchases

have been scaled back. Towards the end of the year, we expect QE to stop,

and rate hikes to start in the second quarter of 2019.

Federal Reserve raises rates as US The US labor market remains robust, and the temporary factors that pushed

business cycle is maturing down inflation in 2017 will be reversed in 2018. This year, Jerome Powell,

nominated to replace Yellen as Chair of the Federal Reserve, is expected

to stay on course and deliver three rate hikes. The US midterm elections

towards the end of the year ensure that politics will remain in focus. The US

administration’s attacks on the judicial system, the democratic process, and

the free press in the United States risk harming the political and economic

institutions important to growth.

Emerging markets show better Growth is rebounding in several of the larger emerging economies. In Brazil,

growth prospects the economic recovery, supported by higher global commodity prices, is

expected to continue in 2018-2019. The Russian economy stalled in the

second half of 2017, mostly due to weak manufacturing. The upward trend

in the oil price, however, is benefitting Russia, and we expect growth to

reach about 2% in 2018-2019. In India, the temporary negative effects of

reforms in 2017 have seemingly begun to wear off, and growth is set to

rebound in 2018-2019. In China, growth is stabilising around 6.5% as the

country benefits from stronger export growth; meanwhile, the transition

towards a more services- oriented economy is progressing.

Nordics and Baltics enjoy strong The Nordics are all benefitting from stronger growth in the euro area. In

export demand, but domestic fac- addition, trade flows among the Nordic and Baltic countries are strong,

tors pose a risk

reinforcing a positive feedback loop. Notably, Finland is growing at a ro-

bust 3%. Denmark is still lagging somewhat, with growth expected to be

4

LEADER AND SUMMARY

about at 2% in 2018-2019. Sweden and Norway are enjoying high levels

of growth, but both countries face risks in terms of the cooling down of

the housing market. The Baltics are benefitting from high productivity

growth, strong exports, and high domestic demand. This bodes well for

these countries, which are progressing well to catch up with the Nordics

in terms of GDP per capita. For the Baltics and Sweden, Swedbank’s new

Sustainability Indicators (see p.22) provide a comprehensive review of

structural preconditions for medium-term growth and progress towards the

UN Sustainable Development Goals.

Risks to global outlook still stem The risks to the economic outlook stem predominantly from political fac-

from political factors and high tors. High indebtedness and asset price correction, e.g., in the US, follow-

indebtedness

ing years of low interest rates, also pose a risk. Many European countries

remain heavily indebted. In China, it is the corporate sector that needs to

deleverage, whereas in Sweden and Norway household debt has risen, a risk

to growth if the labour market were to unexpectedly weaken and the fall

in housing to accelerate. We expect, however, the current downturn in the

housing market to stay contained to the larger cities in both Norway and

Sweden and have limited effects on overall growth (see p.24).

In terms of political uncertainties, heightened geopolitical tensions, such

as an escalation of the US-North Korea tensions, or in the Middle East,

pose a risk. Turkey is in a geographically sensitive area, and an escalation

of conflicts in this region could affect stability in Europe. The Italian elec-

tion in March could cause market turmoil, but, overall, we judge that the

risks related to the election have diminished. Another risk is populism and

potentially weaker institutions in the US and parts of Europe; this could shift

global power towards less democratic nations. This will not slow near-term

growth, but it remains a threat to long-run prospects for well-being.

Swedbank’s global GDP forecast1/ (percentage change)

2016 2017F 2018F 2019F

US 1.5 2.3 (2.2) 2.6 (2.2) 2.0 (1.7)

EMU countries2/ 1.8 2.5 (2.3) 2.3 (2.1) 1.9 (1.8)

Germany 1.9 2.5 (2.3) 2.4 (2.2) 2.0 (1.8)

France 1.1 1.9 (1.8) 2.1 (1.8) 1.9 (1.9)

Italy 1.1 1.5 (1.5) 1.4 (1.3) 1.2 (1.1)

Spain 3.3 3.1 (3.1) 2.7 (2.6) 2.2 (2.3)

Finland 1.9 3.1 (2.8) 2.5 (2.2) 1.9 (1.8)

UK 1.9 1.8 (1.6) 1.6 (1.5) 1.6 (1.6)

Denmark 2.0 2.0 (2.4) 2.0 (2.2) 2.0 (2.0)

Norway (mainland) 0.9 1.9 (1.8) 2.1 (1.8) 1.5 (1.4)

Japan 0.9 1.8 (1.6) 1.4 (1.3) 0.9 (0.8)

China 6.7 6.9 (6.7) 6.6 (6.6) 6.3 (6.3)

India 7.9 6.5 (6.3) 7.3 (7.3) 7.6 (7.9)

Brazil -3.5 1.1 (0.9) 2.5 (2.7) 2.4 (2.4)

Russia -0.2 1.6 (2.0) 2.3 (2.3) 2.0 (2.0)

Global GDP in PPP 3/ 3.3 3.7 (3.6) 3.9 (3.8) 3.7 (3.7)

1/

Previous forecast in parentheses.

2/

Calendar adjusted.

3/

IMF PPP weights (revised Oct 2017)

Sources: IMF and Swedbank

5

UNITED STATES

US – Tax reform gives short-term boost

The economy is enjoying a strong momentum with cheerful consumers and

investment plans suggesting that growth will turn higher. Tax reform provides a

further stimulus. The Fed will be raising its policy rate at a slightly quicker pace.

Political uncertainty remains, especially leading up to the midterm election.

Growth forecast revised higher, As expected, US growth turned higher in 2017 after a weak start. For 2017

but tax reform will produce only a as a whole it is expected to reach a healthy 2.3%. We have revised our

short-term stimulus growth forecast notably higher in coming years, partly because 2018 has

begun with a tailwind. The tax reform that Congress passed just before the

holidays should, moreover, provide a fiscal stimulus in 2018. The tax cuts

boost our 2019 GDP forecast as well. On the other hand, the medium-term

impact of the reforms is likely to be negative, partly because the reforms

exacerbate the already large fiscal challenges.

Consumption and investment are Consumer spending, which represents about two-thirds of US GDP, has

jointly driving the US economy continued to grow at a good speed, and consumer confidence remains high.

Growth will probably hold steady in the light of wage increases and tax

cuts, although rising inflation and interest rates will be mitigating factors.

Changes to social programmes (“entitlements reform” in US parlance) are

a risk factor. Business investment picked up in 2017, and investment plans

remain expansive. The tax reform, which includes lower corporate tax

rates, is likely to provide further support. We see investment contributing

more to GDP growth going forward.

A tight job market and rising Full employment has essentially been reached in the US. According to many

inflation will encourage the Fed to indicators, one would have to go back to the early 2000sto find a similar

continue with policy tightening situation in the labour market. Unemployment has hit a 17-year low, while

the job vacancy rate remains at levels also not seen since 2001. Companies

are having a hard time recruiting at the same time even though they

want to hire. While it is true that jobs are still being created at a high pace,

labour shortages will become a more pronounced concern in the not too

distant future. The missing link is low wage inflation. While there are signs

of acceleration, this is from a low rate. Inflation was also low throughout

2017, though it, too, seems to be gradually rising. We believe that the

PCE (personal consumption expenditure) deflator, the Federal Reserve’s

preferred measure of inflation, will clearly rise, starting this spring. Growth

is also expected to speed up. Against this backdrop, we now expect the

Federal Reserve to raise the target interval for the federal funds rate three

times in 2018.

Political uncertainty remains as Uncertainty revolving around US politics, including economic policy,

attention turns to the midterm remains high. Controversy continues over the possible collusion of the

election this autumn President and his close associates with Russia, and over how business is

being handled at the White House. The recent government shutdown is

a further symptom of the political polarisation. On top of this, a midterm

election will be held in November. The entire House of Representatives and

one- third of the Senate are up for re-election. While indications are that

the Democrats will see gains, this does not necessarily mean there will be a

power shift on Capitol Hill.

6

EUROPE

Euro area glitters while UK sputters and stutters

Strong and broad-based expansion in the euro area (EA) was a welcome

surprise last year. The economy is expected to sustain the momentum this

year, before decelerating in 2019. The ECB will end its asset purchases in

September and will start hiking rates gradually in 2019. Brexit uncertainties

continue to loom over the UK economy, but the Bank of England (BoE) will

again react to the persistently overshooting inflation and hike rates.

Euro area

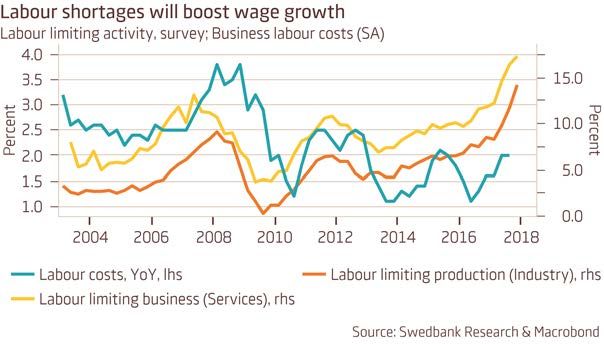

EA economy – firing on all cylin- The economy is firing on all cylinders and continues to surprise positively.

ders Annual GDP growth accelerated to 2.6% (seasonally and calendar adjust-

ed) in the third quarter of 2017 – the fastest growth rate in more than 6

years. Leading indicators are pointing towards continued strong growth

momentum this year. The composite PMI increased to 58.1 in December–

the highest level in almost 7years, while the economic sentiment indicator

reached its highest level in 17 years.

Export growth will ease Growth last year was supported by recovering global demand and, thus,

somewhat on the back of appre- strong export growth. Rising trade volumes boosted industrial confidence

ciating euro and serious capacity to all-time highs in December. Export order-book levels continued rising

constraints despite the recent euro appreciation; however, “Ifo” export expectations

moderated somewhat towards the end of last year. We expect export

growth to ease somewhat this year, not least due to deteriorating price

competitiveness, but also due to looming capacity constraints and, especi-

ally, large labour shortages in numerous EA countries.

Picking up investment growth After a temporary setback, growth in investment picked up in the third

– additional pillar to economic quarter. Productive investments, like those in machinery and equipment,

growth exhibited the fastest growth. Supported by improved corporate balance

sheets, still-cheap credit, high global demand, and high capacity utilisa-

tion rates, growth in business investments is expected to accelerate this

year. However, unexpected turns in political events remain the main risk to

higher investment growth.

7

EUROPE

Households are ripe for a splurge; Household consumption picked up as well, supported by an improving la-

wage growth to pick up bour market and rising consumer sentiment. Growth in private expenditure

is expected to rise further this year - the lack of labour will finally translate

into higher wage growth, while the continued economic recovery will boost

employment growth. Meanwhile, reduced leverage and increased housing

wealth will limit consumers’ caution when opening their wallets.

No asset purchases beyond Considering all the aforementioned factors, core inflation is expected to

September; expect first hikes next pick up to 1.2% this year, while higher oil and other commodity prices will

year help push headline inflation to 1.6%. Inflation will be much closer to the

ECB’s target; thus, the governing council will not have enough arguments

to extend asset purchases beyond this September. This intention can

already be witnessed in comments by some high ECB officials. The ECB

may formally drop a pledge to keep QE open-ended as early as the March

meeting. We forecast that core inflation will increase to 1.6% in 2019 and

the ECB will gradually start raising its main refinancing rate in the second

quarter of 2019.

United Kingdom

BoE responds to overshooting After an initial setback in 2017, growth regained strength but is still below

inflation and will hike rates again previous years’. Private consumption rebounded in the third quarter, but

despite Brexit worry the data probably are erratic, and the underlying pattern of a slowdown,

given weak real income, persists. Despite moving forward in Brexit nego-

tiations companies’ expectations have fallen, and business investments

may be modest due to remaining uncertainties. Stronger global demand

and a weak sterling; however, support export growth and dampen the

investment downturn. At present, Brexit negotiations are protracted, and

it seems that some former supporters have doubts and regrets. The best

and most likely outcome for the UK is a transition period during which it

will stay an EU member. However, we expect the deals to be agreed upon

in the last minute, and the UK will probably have to give in to EU demands.

Assuming an orderly Brexit and persistently overshooting inflation, the BoE

will hike the Bank rate again this year.

8

ASIA AND EMERGING MARKETS

Asia/Emerging Markets – Stabilisation in China

Growth is returning in several of the larger emerging economies. In China,

growth is stabilising near the new, more sustainable growth target. Economic

recovery continues in Brazil and Russia. In Japan, growth will continue above

potential, though at a slower rate in 2019 as compared with 2017. In India, the

temporary negative effects of reforms in 2017 have seemingly begun to wear

off. The possibility of renewed US-China trade frictions and the situation with

North Korea pose a risk, along with the outlook for Chinese financial stability.

Japan

Growth in Japan will slow in 2019 Economic growth will remain above potential in 2018-2019, supported

as compared with 2017 by healthy global growth and an expansive monetary policy. Exports and

investment will remain supportive and consumption should strengthen,

once real wages start growing. Economic growth is expected to slow as

compared with 2017 due to capacity constraints. In 2019, retail sales will

be affected by a planned sales tax hike. Inflation is slowly accelerating but

is not even half way towards the central bank’s target; therefore, a hike in

interest rates remains distant.

China

Growth stabilising in China Growth stabilised in 2017, and it is expected to gradually fall going into

with new sustainable focus, but 2018-2019. We also expect that the renminbi will stabilise in 2018 and app-

financial stability still a risk reciate in 2019. As exports turned higher in 2017, China’s need for a weaker

renminbi decreased. In the longer term, China aims to increase the global

use of its currency, as well as its capital inflows. The Chinese leadership is

therefore pleased with the stabilised renminbi.

Supply-side reforms that resulted in increased industrial profits translated

into a stabilisation of total credit growth in 2017. The Financial Stability

and Development Committee held its first meeting in November, addressing

the priority task of risk prevention. Total debt stabilised during 2017 and

deleveraging is progressing, though this remains at an early stage. The new

aim is to direct credit towards more productive sectors. The formerly over-

heated housing market has cooled. Growth rate targets are now slightly

compromised in favour of more sustainable growth.

With the trade surplus against the US once again trending upwards, the risk

for renewed trade frictions has returned in 2018, especially given the app-

roaching midterm elections in the US, where this development may serve as

an electoral issue. Currently, this issue, as well as the situation with North

Korea, poses a risk, in addition to the evolving outlook on financial stability

in the Chinese economy. President Xi Jinping further consolidated his power

at the 19th National Congress of the Communist Party of China in October

2017.

India

Growth returning in India after ne- We expect that the growth dampening in 2017 will be reversed in 2018-

gative effects of reforms in 2017, 2019. Third-quarter data showed that growth had returned, suggesting

but credit growth is still weak that, the temporary negative effects of tax and demonetisation reforms

in the beginning of 2017 have begun to wear off. Inflation seems to have

9

ASIA AND EMERGING MARKETS

bottomed out. The Reserve Bank of India, therefore, kept its policy rate

unchanged at the latest meeting in December. On the positive side, the

government proposed a plan in October to recapitalise the fundamentally

weak banking sector, aimed at addressing the limited lending capacity and

weak credit growth. Furthermore, the credit rating institute Moody’s un-

expectedly increased its rating for India in November. On the negative side,

the recovering oil price is weakening India’s terms of trade.

Brazil

Recovery on the way in Brazil, but The recovery that began in 2017 was supported by higher global commo-

the general election in October dity prices, and we expect that it continues in 2018-2019. In 2017, exports

poses a risk to growth turned up, which supported industrial production and growth. At the same

time, fiscal cuts addressing the growing public debt have further weakened

households in an economy with high unemployment and falling wages. Low

inflation has raised real wages, though, offering households and private

consumption some support. However, with an overall lower domestic de-

mand, investments have declined. To address the low inflation and further

boost a weak but recovering economy, the Central Bank of Brazil lowered

its policy rate by 6.75 percentage points in 2017. Political turbulence stem-

ming from political leaders’ involvement in corruption scandals remains; this

continues to halt the reforms, e.g., the budget-heavy pension reform, requi-

red to meet the budget deficit target. With the general election coming in

October, the challenge of passing necessary and efficient reforms will likely

increase, presenting a risk to growth.

Russia

Russian recovery stalled in second The recovery stalled in the second half of 2017, mostly due to weak manu-

half of 2017, but to resume in facturing. Hence, we cut the 2017 real GDP growth estimate to 1.6% (from

2018 2%) but retain 2-2.3% growth for 2018-2019. Other sectors are slowly im-

proving: construction is bottoming out, the investment rebound continues,

and the tighter labour market supports retail. With inflation at a historic

low of 2.5%, the Central Bank of Russia will continue to ease, cutting its

policy rate from the current 7.75% to 6.5% by end-2018. The banking

troubles have so far had a minor impact on other sectors. Watch out for the

risk of new, individually targeted sanctions after the US Treasury report in

February. Putin will be re-elected President - no change in foreign policy

expected.

10SWEDEN

Sweden – Soft landing due to strong exports

Last year ended with positive economic signals from outside the country and

rising global growth - both of which are benefitting Sweden. The industrial pro-

duction has accelerated at the same time as the services sector is staying strong.

Yet, 2018 contains several domestic uncertainties. Will the Riksbank raise the repo

rate this year? What will happen to the housing market? 2018 is also an election

year – how will that affect financial markets and the economy?

The Swedish economy stands Prospects for Swedish growth are good in the short term. Employment con-

strong, and a notable slowdown in tinues to rise, fiscal policy is expansionary, with hefty spending on families

housing investment is not antici- with children and pensioners, and the global economy continues to make

pated to have a significant effect progress. This suggests that the Swedish growth rate will stay high this

this year year, even as housing investment declines.

Lower house prices of late and general uncertainty about the housing mar-

ket are expected to continue. A large supply of new housing in 2018 and the

stricter amortisation requirements mainly affect metropolitan areas, whe-

re prices could fall further, mainly for tenant-owned flats. But with a solid

increase in disposable incomes and a strong job market, we see house prices

stabilising for Sweden as a whole in 2018. For single-family homes outside

metropolitan areas, we expect a slight price increase this year.

Lower housing investment is com- A subdued housing market is affecting GDP growth through fewer housing

pensated for by robust business starts. The decline in housing investment is cushioned, however, by in-

and public investment vestments in renovations and the completion of building projects begun in

2016-2017, which are generating investment throughout the construction

process. It is not until 2019, therefore, that we will see the impact of lower

construction, when we estimate housing investment will drop by nearly

2% on an annual basis. The Swedish economy has thus timed the global

economic turnaround well, especially since it supports business invest-

ment, which had already turned higher last year – a trend we anticipate will

continue.

11SWEDEN

Exports turn higher thanks to Stronger global economic conditions and a favorable mix of investment and

improved global demand and intermediate goods will pave the way for higher export growth in 2018.

favourable mix of goods In 2018 and 2019, foreign trade is expected to positively contribute to

GDP, as exports grow for more sectors, while domestic demand slows. The

challenge for exporters will be to address likely higher unit labour costs and

a slightly stronger krona in 2019, which will make them less competitive.

The heyday for consumers is not In the annual budget, spending increases were targeted at, among oth-

over yet – good disposable income, ers, pensioners and families with children – i.e., households with a high

partly thanks to strong labour propensity to consume. In combination with a strong labour market and

market inflation that is staying just above target, we expect a generally strong

trend in disposable incomes this year. We see good consumer spending

growth, which shifts over to housing and “necessities”; at the same time,

service consumption will stay robust. Instead, it is spending on durables

that will lose ground, with car sales leading the way. Another reason for

the slowdown is the very high savings rate. An increase in amortisations,

high contractual savings, given the labour market’s strength, and an aging

population will support savings in the near term.

Internal and external security, Despite the expansionary fiscal policy this year, Sweden has a large budget

education, and health care will surplus. We expect public investment to stay at high levels as defense

top the agenda in this year’s spending grows. In addition, demographic factors and a population increase

parliamentary election are contributing to continued high investment in municipalities and county

councils. These entities are also expected to continue raising their spen-

ding, since most new immigrants who arrived in 2015 have by now been

placed in municipalities. Public services catering to this group will therefore

count as municipal consumption rather than central government consump-

tion.

A fragmented parliament and dif- A parliamentary election will be held in September. Recent polls indicate

ficulty forming a strong govern- that voters are split. A complicated outcome is likely. In light of the govern-

ment are a likely outcome after ment’s strong finances, this could mean more expansionary fiscal policy

the election than usual after an election.

To achieve sustainable develop- The turmoil around the world in recent years has proved that political

ment, Sweden has to speed up its events can be just as important to the financial markets as statistics and

reform process rate decisions. The Swedish election is not expected, however, to provi-

de the same drama as those in the UK and the US. In the short term, it is

12SWEDEN

unlikely that the Swedish election will affect economic development or the

financial markets at all. Instead, the risk is that a divided parliament will

not be able to get the needed reforms done. A poorly functioning housing

market, slow integration of immigrants, and an education system that does

not match the needs of a competitive economy are all major challenges.

Swedbank’s new “Sustainability Indicators” (see page 22) clearly show that

Sweden has to speed up the reform process to achieve sustainable develop-

ment.

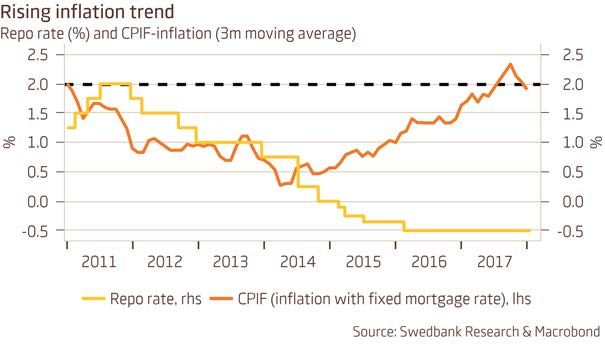

Repo rate hike in sight

The Riksbank is likely to announce The rest of the world is firing on more cylinders, at the same time that do-

its first rate hike in July mestic resources are being stretched. Compared with the picture the Riks-

bank painted a year ago, when risks were mainly negative, this is entirely

different. Wage increases picked up slightly last year and will continue to

rise in 2018 and 2019. The combination of an increase in other labour costs

with a labour force that is getting only marginally more productive means

that unit costs will rise in coming years. This increase, combined with higher

oil prices, will contribute to rising price pressure in 2019. We estimate that

inflation will reach 2% at the end of next year after falling in 2018 due the

comparatively high inflation during the same months in 2017.

We think the Riksbank is ready to raise the repo rate even if inflation this

spring temporarily stays a bit below the 2% target. An upward inflation

trend, coupled with cautious tightening by global central banks, supports

this course of action. Taken together, we therefore see the repo rate being

raised in July to -0.40%. In October, the rate is expected to be raised again,

to -0.25%, to be followed with three hikes of 25 basis points each in 2019.

13NORDIC S

Nordic countries – Continue to improve

The economies of the Nordic countries continue to improve. Growth in the

Norwegian economy has strengthened even as house prices fall. Household

demand and a tightening labour market are bolstering the Danish economy.

Improved price competitiveness is contributing to Finland’s export growth,

while robust private consumption comes in support of a diminishing saving rate.

The Nordic economies continue to gain from stronger growth in the euro area.

Norway

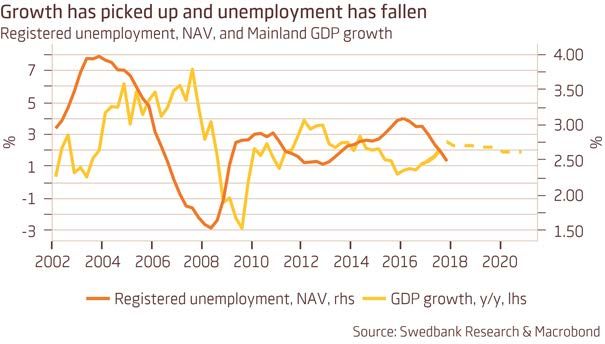

Growth has strengthened even as Growth in the Norwegian economy has picked up significantly as the down-

house prices fall turn in the oil sector has ended. Oil investments and manufacturing produc-

tion stabilised last year, and surveys now indicate growth. This outlook is

supported by rising oil prices in recent months. With strong global demand

and a weak Norwegian krone, tourism and other export-related businesses

will continue to grow. Unemployment is falling, consumer confidence is

rising, and household demand has gained in strength even as house prices

fall.

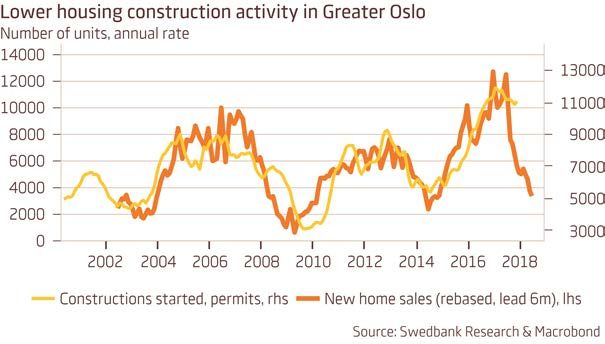

House prices fell through most of last year, but mostly for apartments in

the three largest cities; meanwhile, prices in areas outside the cities are

actually rising. This suggests developments are not the start of a broad

downturn in the housing market, but rather a function of high construction

activity, as well as tighter credit constraints. Recent data show that both

existing home sales and credit growth are keeping robust, indicating strong

demand.

14NORDICS

Lower housing construction acti- We judge the longer-term fundamental factors as sound and supported by

vity will dampen growth improving macroeconomic developments; however, we expect apartment

prices to decline further in the short term in the major cities as many units

under construction will be completed. New home sales will take time to pick

up, and, as a consequence, construction activity will peak and likely dampen

GDP growth going forward. But we expect other parts of the economy to

remain strong, such that overall GDP growth will keep up quite well.

Denmark

Growth outlook is good The Danish economy has enjoyed robust growth in recent years on ac-

count of household spending, business investments and growing exports.

The expansion looks set to continue, due to high consumer confidence

and improving business barometers. The export outlook remains good as

growth has strengthened further in the euro area. Employment continues

to expand. We see the reported fall in GDP in the third quarter of last year

as transitory and expect growth to remain at 2% in the years ahead.

Capacity utilisation is rising but no Falling underlying unemployment is evidence of higher capacity utilisa-

signs of overheating tion. Signs of a shortage of labour have become more widespread but are

not acute. Wage growth remains modest, just as in many other countries.

Although total consumer price inflation has been below 1% most of the

time since 2013, it rose over the past year towards 1.5% on account of

higher energy prices. We expect inflation to be sustained by gradually

tighter conditions in both product and labour markets as resources become

increasingly scarce.

Several policy issues must be To ensure continued growth and stability in the coming years, the govern-

addressed to ensure continued ment must address several policy issues. It is critical to stimulate labour

growth and stability supply, otherwise fiscal policy will have to be tightened more to keep the

economy from overheating. The continuing house price growth and high

household indebtedness raise concerns for financial stability. The govern-

ment has enacted several measures to dampen house price growth and

reduce vulnerabilities, but more can be done with respect to taxation,

valuation schemes, and macroprudential policies.

15NORDICS

Finland

Export outlook for Finland rema- In 2017, economic growth in Finland accelerated to 3.1%, the fastest pace

ins favourable in 2018 of the last nine years. Production capacity and the turnover of Finland’s

business sector have expanded, whereas improved price competitiveness

and stronger foreign demand are contributing to export growth. Although

demand from Finland’s trade partners peaked last year, it is expected to

remain relatively strong in 2018 and offer good growth opportunities for

exporting sectors. Increased new orders in manufacturing confirm the

continuation of export growth momentum, at least in the short term.

Private consumption maintains Investment growth in construction is decelerating, while foreign demand,

good growth in 2018 the expanded production, and several major industrial projects will maintain

robust growth in private investments. Private consumption has increased

at the expense of households’ diminishing saving rate. Increased consumer

confidence, gradually rising employment, and decreasing unemployment

rates are expected to keep household consumption strong this year, but

wage moderation and gradually accelerating inflation will slow it down in

2019.

Longer-term perspective of Fin- According to our forecast, Finland’s GDP growth decelerates to 2.5% in

land’s public finances is challen- 2018 and to 1.9% in 2019. The strong economic growth and comprehen-

ging sive reforms will help to reduce Finland’s government debt and budget

deficit in the coming few years, but the increased expenditures related to

the ageing population will be a major challenge for public finances from the

longer-term perspective.

16BALTICS

Baltic countries – peaking growth, but balanced

and resilient

Growth has peaked for this cycle, but it will remain above potential this year

before slowing to more sustainable rates in 2019. Exports and investment

will continue to benefit from global tailwinds. Domestic demand will

increasingly contribute to growth. Labour markets will keep tightening, but

rising productivity partly helps to outweigh strong wage growth. Inflation has

accelerated due to global commodity price growth, local tax hikes, and wage

growth.

Estonia

In 2017, economic growth in Esto- Economic growth in Estonia accelerated to 4.4% in 2017, the fastest pace

nia accelerated to the fastest pace since 2011. The growth was broad based and supported both by foreign

of the last five years demand and economic activity on the domestic market. Stronger economic

activity has increased the demand for labour. At the same time, the number

of job vacancies has risen, and the shortage of labour has become an increa-

singly serious problem.

We expect that GDP growth will We expect that GDP growth will remain strong in 2018, increasing to close

remain strong in 2018 to 4% in real terms. Robust foreign demand and rising export prices are

allowing Estonian enterprises to increase their export turnover. The govern-

ment sector will continue to raise its investments with the support of the EU

structural funds. However, at this point in the growth cycle, such a strong

fiscal stimulus to the Estonian economy is wrongly timed.

Robust demand and increased in- Robust demand and increased investments contribute to productivity

vestments contribute to produc- growth. Although the tight labour market will maintain fast wage growth,

tivity growth the changes in income taxation could lower wage growth expectations.

We expect that productivity growth will exceed wage growth in 2018 and

2019. This will help to improve Estonian enterprises’ profitability and slow

the deterioration of their price competitiveness against trade partners. The

households’ financial situation is expected to remain strong. Average pur-

chasing power of households will improve with the support of the increase

in their nontaxable income, and this should give stronger momentum to the

growth of private consumption in 2018.

17BALTIICS

We forecast that GDP growth will decelerate to 3% in 2019, primarily due to

cyclical factors. Because of the openness of the Estonian economy, the main

downward risks to the current baseline scenario are related to the external

environment.

Latvia

Broad upswing continues; do- The strong cyclical upswing continued in Latvia throughout 2017 and

mestic demand takes over as key into 2018. Real GDP growth of 5.8% in the third quarter was the peak of

driver of growth the cycle. Confidence is robust across the board. With the business cycle

maturing, growth will go downhill but in 2018-2019 will still remain strong

and above its medium-term potential of 2.5-3%.

All sectors are expanding, except for financial intermediation (transitory

fall caused by offboarding of nonresidents due to tighter know-your-client

and anti-money-laundering regulations) and agriculture (hurt by rainfall).

Heavy rainfall hampered log supplies to the wood processing industry in

2017, which may weaken exports in early 2018, but, with strong global

demand continuing, the general outlook for exports of goods and services is

good, and we forecast solid 4-4.5% volume growth in 2018 and 2019.

Strong investment activity to Gross fixed capital formation has shot up by 20%. About 40% of the rise is

continue to limit labour market likely due to Air Baltic’s renewing its fleet; thus, the investment recovery

pressures and cover for past for the overall economy is less spectacular. High capacity utilisation, inflows

underinvestment of EU funds, and an upturn in the mortgage credit cycle will yield double-di-

git investment growth also this year and the next. Construction, which was

the fastest-growing sector in 2017, will remain such in 2018.

Tight labour market and pro-cycli- The labour market remains the hotspot of this business cycle. In 2017, the

cal fiscal policy to boost consumer growth in wages was matched with a rise in productivity, but productivity

spending is unlikely to keep up the pace, and risks to competitiveness will build up.

Tighter labour market supports consumer spending, which in 2018 will be

additionally boosted by a rise in the minimum wage (up 13%) and labour tax

cuts. Fiscal policy is mildly pro-cyclical as politicians gear up for the October

2018 general election. We do not foresee major U-turns in economic policy

post-election, but with the election approaching, the reform agenda is likely

to suffer. No major imbalances are present, and strong growth is set to

continue. Hence, do not worry, be happy… for now.

18BALTICS

Lithuania

Growth peaked at 3.8% last The Lithuanian economy remained on strong footing at the end of 2017

year and is set to ease towards and probably expanded for the year at a rate of 3.8%. The main source of

potential output growth last year and in the final quarter was an impressive expansion of

foreign trade – estimated real annual growth of exports of goods and servi-

ces was 12%. Even more impressive was the growth of exports of services

last year, when its value increased more than 20%.

Investments grew slightly more slowly last year – at an estimated 7% - but

this was still a nice recovery after the contraction in the previous year.

During the past two years, investments were dragged down by the public

sector, but it seems the trend has been broken – nominal public sector

investments increased by 25% in the third quarter of last year. Investments

are likely to continue boosting overall GDP growth in 2018, as the pace of

distribution of the EU structural funds finally picks up.

Household consumption growth is Household consumption increased by an estimated 4% last year. Although

being dragged down by demo- consumption growth somewhat eased in the second half of last year, it is

graphics, but the worst of emigra- expected to continue growing at a similar pace in 2018. Overall household

tion is in the past consumption is dampened by negative demographic trends, but, on an

individual level, most households are doing fine – average wage growth

was close to 8% last year. Emigration seems to be easing, while immigration

continues picking up. In December 2017, for the first time in this century,

immigration was higher than emigration. Even though this may have been a

blip, the worst of net emigration is in the past.

The overall economy remains very well balanced and resilient. Foreign trade

was close to a record surplus last year – at 1.9% of GDP – while the current

account was in balance. The general government budget was in surplus

for the second year in a row and is planned to remain in surplus again in

2018. The private sector has very low debt-to-income ratio, while housing

affordability and other indicators show that there are no bubbles in the

residential real estate market. Unlike in 2008, the private and public sectors

are very well positioned to withstand even large external shocks.

19EXCHANGE AND INTEREST RATES

Exchange and Interest Rates

The policy direction of central banks is clear: a gradual removal of policy stimu-

lus has begun. This normalisation is expected to continue and will affect market

interest rates, as well as exchange rates. Interest rates are rising, and we see a

progressively stronger krona, as well as euro, during the forecast period.

Central banks’ cautious normalisation of policy continues

The Riksbank will start hiking The US central bank, the Fed, has begun normalising monetary policy by

rates very cautiously raising the federal funds target 125 basis points (bp) since its post-crisis

low. The central bank has also started reducing its bond holdings. We expect

this to continue in the near term, and, with a slightly more ”hawkish” FOMC

committee, we foresee that the Fed will increase its policy rate three times

in 2018. This is a slight upward revision compared to our previous forecast.

A somewhat higher inflation rate, combined with the tight labour market,

will be a central focal point for the Fed. A pickup in economic growth within

the euro zone will also make the ECB slightly more hawkish, and we expect

the ECB to end net asset purchases by September. The ECB will continue to

focus on inflation developments and the strength of the recovery, as well as

the euro exchange rate. The Riksbank will maintain an eye on the krona ex-

change rate and imported inflation. However, we expect that the Riksbank

will begin lifting the repo rate in mid-2018. It will start cautiously, with a

hike of 10 bp, followed by a further hike in October of 15 bp, thereby ending

the year with a repo rate of -0.25 percent. In 2019, we foresee three hikes

of 25 bp each.

Monetary policy sets tone in fixed-income markets

Raising long-term rates, but The central banks’ varying pace in normalising monetary policy will be the

rates will stay low by historical key factor affecting long-term interest rates. In the short term, we expect

standards yield curves to steepen as short-term rates are anchored by policy rates.

Thereafter, as policy rates are raised, we expect yield curves to flatten aga-

in. The differences in timing of the central banks’ actions will be important

to determine interest rate spreads and curvature developments. Throug-

hout the forecasting horizon, long-term interest rates will, however, remain

low by historical standards. Swedish government bond yields will also be

held down by a limited free float of bonds. In terms of peripheral spreads,

the political risks in Europe have diminished, and the cyclical upswing in the

euro area has gained momentum. Nonetheless, one should not completely

rule out the political risk, which could widen peripheral spreads.

Policy rate differentials and short-term market rates affect ex-

changes rates

Gradual strengthening of the Central bank policy also continues to be the major driving force in the cur-

krona and euro rency markets. In the short term, interest rate differentials will support the

US dollar, although recent strong developments in euro area and a slightly

more hawkish ECB will limit the downside in the euro-dollar movements. In

the longer term, we foresee a gradually strengthening of the euro. As the

Riksbank will begin to raise the repo rate, we also expect the Swedish krona

to strengthen. The Norwegian krone will stabilise in the near term, suppor-

ted by a higher oil price and stabilising house prices. Uncertainty surroun-

20EXCHANGE AND INTEREST RATES

ding Brexit will cloud the outlook for the UK pound. We moreover expect

emerging market currencies to strengthen gradually, supported by brisker

global growth and higher commodity prices.

Commodity markets

Oil prices have risen as demand The oil market returned to balance last year, and stock levels continue to

strengthens decline. Stronger global demand and continued production restraint in

OPEC and Russia have driven up the Brent oil price to almost 70 USD/barrel.

Increased tensions in the Middle East have also contributed to push up pri-

ces. We have revised up our estimates for the oil price to 64 USD per barrel

in 2018 and 59 in 2019, as US shale oil is now growing at a high rate again

and US petroleum exports are booming. At the same time, investments in

conventional production have been severely reduced, and the production

shortfall could turn out to be larger than expected.

Interest and exchange rate forecasts

Outcome Forecast

2018 2018 2018 2019 2019

18.JAN 30.JUN 31.DEC 30.JUN 31.DEC

Policy rates (%)

Federal Reserve, USA 1/ 1.50 1.75 2.25 2.50 2.50

European Central Bank 2/ 0.00 0.00 0.00 0.25 0.50

Bank of England 0.50 0.50 0.75 1.00 1.25

Riksbank -0.50 -0.50 -0.25 0.00 0.50

Norges Bank 0.50 0.50 0.50 0.75 1.00

Bank of Japan -0.10 -0.10 -0.10 -0.10 -0.10

Government bond rates (%)

Sweden 2y -0.34 -0.10 0.35 0.70 0.90

Sweden 5y 0.26 0.65 1.25 1.45 1.55

Sweden 10y 0.86 1.15 1.60 1.90 2.00

Germany 2y -0.59 -0.45 -0.10 0.35 0.65

Germany 5y -0.12 0.10 0.60 1.05 1.35

Germany 10y 0.52 0.80 1.20 1.65 1.85

US 2y 2.05 2.20 2.60 2.65 2.65

US 5y 2.43 2.75 3.00 3.10 3.10

US 10y 2.62 3.00 3.20 3.30 3.30

Exchange rates

EUR/USD 1.22 1.20 1.22 1.24 1.25

EUR/SEK 9.81 9.50 9.35 9.25 9.10

USD/SEK 8.03 7.92 7.66 7.46 7.28

KIX (SEK) 3/ 112.8 109.6 107.4 106.1 105.7

EUR/NOK 9.60 9.41 9.17 9.07 9.01

NOK/SEK 1.02 1.01 1.02 1.02 1.01

EUR/GBP 0.88 0.92 0.94 0.94 0.92

USD/CNY 6.44 6.60 6.55 6.60 6.50

USD/JPY 110.3 115.0 115.0 120.0 115.0

USD/RUB 56.8 55.0 53.0 51.0 50.0

1/

Upper Bound

2/

Refi Rate

3/

Trade-weighted exchange rate index for SEK. A higher value of the index means that SEK

has depreciated.

Sources: IMF and Swedbank

21IN-DEPTHS

Sustainability indicators

Swedbank has developed a new methodology, Sustainability Indicators, to monitor

the progress towards the 2030 Agenda. There is much unused business potential

in Sweden and the Baltics in advancing sustainability, e.g., in making the transition

to cleaner and more energy-efficient economies. The aim is to support business

looking at ESG (environmental, social, governance) criteria and help to identify

weaknesses and strengths in Sweden and the Baltics. We find that Sweden has to

speed up to remain among the leaders in Europe, while the Baltics have a lot of

catching up to do.

Progress towards UN SDGs, % of benchmark*

Estonia Latvia Lithuania Sweden

Preconditions for sustainable medium-term growth1/ 71 61 64 90

Social inclusion2/ 56 55 55 89

Environmental protection3/ 58 72 70 82

Governance and institutions 4/

70 51 62 97

Downward/stable trend during last 5 years (4 years for governance) – ↓

* Benchmark is 90/10th percentile of EU28 in 2015. In total 40 indicators covering 14 from 17 SDGs, aggregated to four pillars.

Cut-off points for traffic lights - Sweden: >90% for green, 70-90% for yellow, Baltics: >80% for green, 60-80% for yellow

1/

SDGs #4, 8, and 9: education, labour force participation, employment, and innovations

2/

SDGs # 1, 3, 5, and 10: income and gender inequality, poverty, and health

3/

SDGs # 6, 7, 11, 12, 13: water supply, energy intensity, renewable energy, sustainable cities, waste generation, and GHG emissions

4/

SDGs # 16, 17: government effectiveness, rule of law, corruption perception, regulatory quality, AML, and official development assistance

Focus on sustainable development Sustainable business is going mainstream worldwide. Demand for en-

creates many business opportu- vironmentally friendly products and services is growing, as well as socially

nities responsible investments, especially among millennials. There is also a push

from new regulations and global arrangements (e.g., the Paris climate

agreement). New business/investment opportunities in many sectors are

being created as a result – renewable energy capacity is expanding, electric

cars are soon to be the norm, big data are used for sustainability ratings of

companies, and new finance instruments are being developed.

UN SDGs as a point of departure to To assess long-run sustainability in Sweden and the Baltics and to see

assess sustainable development where the biggest potential for improvement is, we take the 17 UN Sus-

tainable Development Goals (SDGs), a part of the 2030 Agenda, as a point

of departure. We have selected 40 indicators, covering 14 out of 17 SDGs,

and grouped them into four sustainability pillars: sustainable medium-term

growth, social inclusion, environmental protection, and governance. To

assess and compare progress in these areas, we use EU28 90th or 10th per-

centiles (depending on whether a maximum or minimum is relevant) in 2015

as a benchmark and calculate how far the countries have come towards the

benchmark. We calculate the average for each of the four pillars. We assign

a traffic light colour, depending on how likely countries are to reach these

benchmarks by 2030. This shows which areas require the biggest action and

simultaneously provide the largest opportunities. A more detailed methodo-

logy/analysis can be found in our Macro Focus here.

22IN DEPTH

Peer pressure (sustainability as a part of a competitive offer) and policy

pressure (sustainability disclosure) for the companies are growing. Among

the potential benefits of integrating sustainability into business (including

measuring sustainability-related performance) are the following:

• cost efficiencies (e.g., energy) and better risk management (legal

claims and reputational risks);

• innovation and productivity growth, leading both to cost savings

and better revenue streams (access to new markets, new product deve-

lopment); and

• talent development and retainment (employee satisfaction and

engagement, equal opportunities).

Opportunities, though, do not present themselves without risks. The ne-

cessary shift to a low-carbon economy results in a reallocation of resources

and a revaluation of assets, which can pose risks to financial stability and

present challenges for regulators and central banks in safeguarding the resi-

lience of the financial system and developing a proper framework to finance

the transition. The shift itself does not come for granted – emission targets

to moderate climate change are ambitious, and there are already backslas-

hes in commitment from some politicians (read: Trump).

Largest potential in environmen- The Sustainability Indicators show that Sweden has to speed up to remain

tal protection in Sweden among the leaders in Europe. Three out of the four traffic lights are yellow,

and the only green one, governance, shows a negative trend. Sweden enjoys

high scores for social inclusion, but the situation with respect to income

inequality and poverty has been worsening in the last few years. As for the

growth pillar, education is a challenge – for some indicators, Sweden even

lags some of the Baltic countries. For the environmental protection pillar, the

largest improvements are necessary in the areas of resource productivity

and waste generation.

Largest potential in social inclu- The Baltic countries have a longer way to go. Still, the improvements, partly

sion in Lithuania, environmental driven by economic recoveries, during the last five years in all pillars, except

protection in Estonia, and gover- social inclusion, have been remarkable. The largest differences between

nance in Latvia countries are for the governance pillar, while the smallest differences and

lowest scores are for the social inclusion pillar. Gender inequality seems to be

a larger challenge for Estonia, while Latvia and Lithuania struggle more with

income inequality, poverty risk, and maternal mortality. As for the growth

pillar, innovations and lifelong learning for adults constitute the most

pressing problems for both Latvia and Lithuania; meanwhile, in Estonia, the

number of patents is very small despite higher R&D expenditure. For the

environmental protection pillar, Estonia scores the worst on many indicators

due to its polluting shale oil industry.

Overall, Swedbank’s Sustainability Indicators show that the state, civil socie-

ty and business sector must work together for strengthened environmental

protection and social cohesion in order to attain Agenda 2030. Long-term

sustainable economic development goes hand in hand with better pre-con-

ditions for a sound environment, social cohesion and strong democratic

institutions.

23IN-DEPTHS

Sweden vs. Norway housing – similar yet different

After years of strong growth, Norway and Sweden both saw a downturn in house

prices in 2017. We expect that a large supply of new homes and tighter mortgage

credit regulations will continue to dampen house prices this year. But the overall

economic situation is good, and spillover effects to the real economy will be

limited in both Norway and Sweden. However, favourable external factors can

shift. Therefore, in terms of risks, differences in the housing markets suggest that

the Norwegian economy is more vulnerable than its neighbour.

The overall macroeconomic environment is favourable in Sweden and

Norway. The global economy is enjoying a synchronised cyclical upswing,

benefitting the Scandinavian economies. Strong labour markets and expan-

sionary fiscal and monetary policy imply high growth in disposable income.

Household confidence and consumption growth remain strong. The interest

burden is a historically small share of income; it will remain small despite hou-

seholds’ strong preference for floating mortgage rates and the anticipation

of slowly rising interest rates. Banking systems in both countries are well

capitalised and well supervised, with generally sound lending practices. In

addition, strong public finances in both Sweden and Norway can be mobili-

sed if push comes to shove.

A shift in the market balance, with The cooler housing markets in Sweden and Norway are thus not a consequ-

large supply of housing in both ence of changes in fundamental demand. Instead, the downturn is primarily

countries driven by the increase in supply and tightened macroprudential policies,

limiting mortgage credit. As a result, the downturn is mainly concentrated in

metropolitan areas, where new construction of, especially, flats is high, and

debt-to-income ratios are the highest. For example, prices are down more

than 11% from the peak in Oslo, while Stockholm flat prices have fallen 10

% from their seasonally-adjusted peak . Swedbank’s forecast for the year

ahead remains that a stabilisation of housing prices is likely for the two

countries as a whole. However, favourable external factors can shift. It is,

therefore, important to assess risks in the Scandinavian markets.

Severe macroeconomic effects from the housing market downturns can

generally be seen as emanating from three channels: (1) the impact on the

banking sector from falling collateral values, resulting in a credit crunch;

(2) the direct and indirect impact of a reduction in residential investment in

the wake of uncertainty regarding prices; and (3) the impact of households

reducing consumption as their preferences for savings increase.

Strong banking systems in both First, although the conventional banking channel of transmission from

countries works as a buffer, but the housing market to the real economy appears limited for both Sweden

macroprudential tools may backfi- and Norway, authorities in both countries have in recent years tightened

re in short run regulations on the banking sector. These include macroprudential policies

that directly target mortgage lending. Most recently, Norway tightened

limitations on mortgage lending in early 2017, while in Sweden higher

amortisation requirements based on debt-to-income ratios will soon enter

into force. These restrictions can, in a qualitative sense, be compared with a

24You can also read