THE DAILY BRIEF MARKETUPDATE WEDNESDAY,06JANUARY2021 GLOBAL MARKETS - CAPRICORN ASSET MANAGEMENT

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

The Daily Brief Market Update Wednesday, 06 January 2021 Global Markets Global stock prices slipped and U.S. bond yields rose on Wednesday as investors braced for the prospect that Democrats could win both races in a U.S. Senate run-off election in Georgia, handing them control of the crucial chamber. Along with their narrow majority in the House of Representatives, a 'blue sweep' of Congress could usher in larger fiscal stimulus and pave the way for President-elect Joe Biden to push through greater corporate regulation and higher taxes. Democrat candidates took early leads in the twin Georgia Senate races, though the outcome may remain in doubt for days if the margins are razor-thin. "Having control over both the legislative and executive branches could theoretically lead to sweeping changes to policy," said Vasu Menon, investment strategy executive director at OCBC Bank. "With Biden proposing to reverse President Donald Trump's tax cut, increase the minimum wage, and strengthen oversight on various industries, some might argue that his agenda is not particularly market-friendly." Futures for the S&P 500 fell 0.43%, while Nasdaq futures shed 0.7% on fears Democrats could pursue tighter regulations on big tech firms. Other industries, such as banks, oil and gas and healthcare, could come under heavier scrutiny, while infrastructure and alternative energy sectors

could benefit. Japan's Nikkei fell 0.4% while MSCI's index of Asian-Pacific excluding Japan erased earlier gains to stand almost flat. The 10-year U.S. Treasuries yield rose to as high as 0.987%, the highest level since March, on expectations of larger government borrowing. "A market pullback seems both reasonable and healthy. But stocks won't plunge to zero because there is a countervailing positive here," said Phil Orlando, Chief Equity Market Strategist, Federated Hermes of a potential Democratic sweep. "A Biden honeymoon with Democratic Congress helmed by Nancy Pelosi and Charles Schumer would likely lead to more fiscal stimulus and infrastructure spending. That would serve as a temporary sugar high for stocks in 2021 before the bill comes due in 2022." Adding to broader uncertainty in markets was the latest twist in a regulatory saga over whether the New York Stock Exchange would delist three Chinese telecom giants on security grounds. Shanghai stocks extended gains on Wednesday, with the CSI300 index rising 0.5% to reach its best levels since 2008. Oil prices held firm, maintaining their gains of nearly 5% made on Tuesday after Saudi Arabia offered to make voluntary cuts to its oil output. Tensions following OPEC member Iran's seizure of a South Korean vessel also frayed nerves, adding further support to the market. Tehran denied on Tuesday it was using the ship and its crew as hostages, a day after it seized the tanker in the Gulf while pressing a demand for Seoul to release $7 billion in funds frozen under U.S. sanctions. U.S. crude futures were almost flat at $49.95 a barrel after having climbed 4.9% on Tuesday. International benchmark Brent crude futures stood firm at $53.45 after a gain of 4.9% on Tuesday. In currencies, the U.S. dollar hit a new low before bouncing back on the prospects of the 'blue sweep' in Georgia. The euro rose to as high as $1.2328, a high last seen in April 2018, while the yen hit a 10-month high of 102.595 to the dollar. Spot gold held firm at $1,948.20 an ounce, having touched a two-month high earlier in the day. Bitcoin traded at $33,904, near record high of $34,800 set on Sunday. Domestic Markets Shares on the Johannesburg Stock Exchange (JSE) remained upbeat on Tuesday, driven by higher gold and platinum prices which pushed up shares in mining companies and posted a record closing for the main indices. However, the rand clawed back a substantial part of its gains seen in the last few weeks forcing it to cross the 15 rand per dollar mark on Tuesday. The FTSE/JSE all-share index ended up 0.73% to 60,921 points, hitting a two-year peak. The bluechip index FTSE/JSE top 40 companies closed up 0.97% to 55,976 points, racing past its all-time high number last seen in mid-December. The rally was mainly led by higher gold and platinum prices with the gold indices up almost 3% and the resources index crossing 1%. Safe-haven gold inched up on Tuesday to a two-month high on the back of a weak dollar which bore the brunt of uncertainty of the outcome of the U.S. senate runoffs in Georgia which will decide which party will control the Congress. Platinum was up 0.6% at $1,076.86, having hit a more than four-year high of $1,127.82 on Monday. However, the shares of banks, which are usually a reflection of the country's economic outlook, continued to decline with the index down 2.4% on Tuesday. However, the rand lost over 2% versus

the dollar, its biggest single day fall in over three months. At 1625 GMT, the rand was trading down

2.14% to 15.0425 rand against the dollar. It had opened the day at 14.7150.

Annabel Bishop of Investec Ltd said in a note that while globally news of more vaccine approvals and

more people being vaccinated could be boost for riskier currencies, locally, "patchy natures of

recoveries" could be a dampener. There is speculation that South Africa could announce a higher

level of lockdown as the country wrestles with an increasing number of coronavirus cases.

Bonds weakened, with the yield on the benchmark 2030 government issue up 2.5 basis points to

8.685%.

Corona Tracker

The number of new cases is distorted by cut-off times.

Source: Thomson ReutersMarket Overview

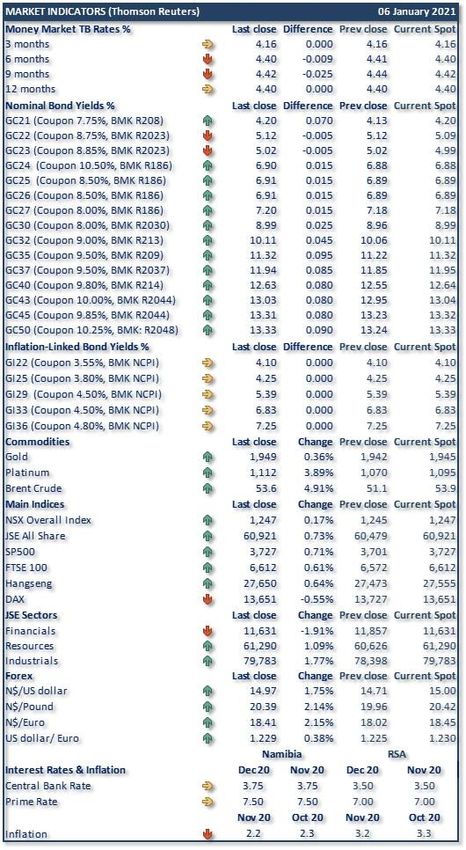

Notes to the table:

The money market rates are TB rates

“BMK” = Benchmark

“NCPI” = Namibian inflation rate

“Difference” = change in basis points

Current spot = value at the time of writing

NSX is a Bloomberg calculated Index

Important Note:

This is not a solicitation to trade and CAM will not necessarily trade at the yields and/or prices

quoted above. The information is sourced from the data vendor as indicated. The levels of and

changes in the yields need to be interpreted with caution due to the illiquid nature of the domestic

bond market.

Source: Bloomberg

For enquiries concerning the Daily Brief please contact us at

Daily.Brief@capricorn.com.na

Disclaimer

The information contained in this note is the property of Capricorn Asset Management (CAM). The

information contained herein has been obtained from sources which and persons whom the writer

believe to be reliable but is not guaranteed for accuracy, completeness or otherwise. Opinions and

estimates constitute the writer’s judgement as of the date of this material and are subject to change

without notice. This note is provided for informational purposes only and may not be reproduced in

any way without the explicit permission of CAM.You can also read