THOUGHTS ON THE 2020 LME MARKETS - OCTOBER 2019- PREPARED BY: EDWARD MEIR, INDEPENDENT COMMODITY CONSULTANT FOR ED&F MAN CAPITAL MARKETS INC ...

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

THOUGHTS ON THE 2020 LME MARKETS

-- OCTOBER 2019--

PREPARED BY: EDWARD MEIR, INDEPENDENT COMMODITY CONSULTANT

FOR ED&F MAN CAPITAL MARKETS INC.

1

Disclaimer:

Edward Meir/Commodity Research Group (“CRG) is an independent consultant to E D & F Man

Capital Markets Inc. (“MCM ”) focusing on metals commentary. Neither Ed Meir or CRG have a

personal futures trading accounts. The information contained in this material should be

construed as market commentary, merely observing economic, political and/or market

conditions, and not intended to refer to any particular trading strategy, or specific trade

recommendation, promotional element or quality of services provided by MCM Inc. Trading

ranges given are not a reason to buy, sell or hold any commodity mentioned. MCM is not

responsible for any redistribution of this material by third parties, or any trading decisions taken

by persons not intended to view this material. Information contained herein was obtained from

sources believed to be reliable but is not guaranteed as to its accuracy. These materials represent

the opinions and viewpoints of the author, and do not necessarily reflect the viewpoints and any

trading strategy employed by MCM. This is not an offer to buy or sell any derivative. The

information and data provided is not tradable and is for indication-only purposes. The trading of

derivatives such as futures, options and OTC products or swaps may not be suitable for all

investors. Derivative trading involves substantial risk of loss, and you should fully understand

those risks prior to trading.

2

Y-T-D performance (through mid-Oct; lackluster apart from nickel)

Copper: -19%

Aluminum: -2%

Zinc: -3%

Lead: +4.2%

Nickel: +60%

Tin: -15%

CRB Index: Flat

Source for data: E-Signal/Futuresource.com

3

But supply-side fundamentals are not that bearish!

--Stock levels down across most metals markets

--All metals are in projected deficit this year.

--Mine expansion restrained on account of...

Declining ore grades

Production disruptions

More aggressive unions and governments

Natural disasters

Source: Reuters

4

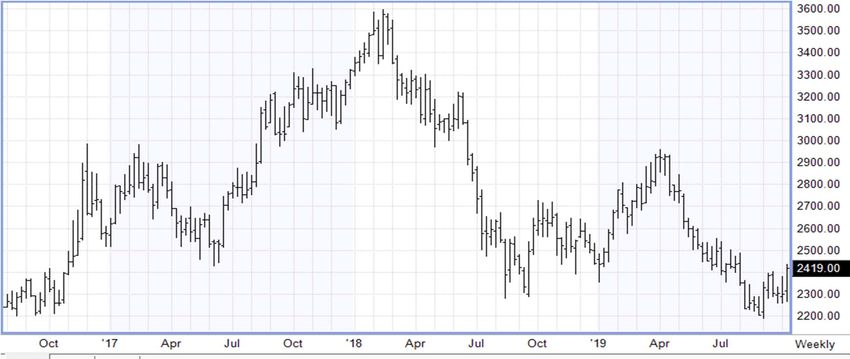

COPPER – 3 Month

Source: E-Signal

5

Copper supply struggling this year - weather issues in Chile, strikes in Peru and lower

African output. Also, Grasberg transitioning between open-pit to underground mining.

ICSG has world mine production -1.4% in the first half of 2019, refined and concentrate

output -1%, while SX-EW output -3.5%

But prices hardly reacting as demand is more in focus. The ICSG saw a 2% increase in

global apparent usage in May, but now sees a decline of 1%. China demand up .5%-

1.5% for 2019; Ex-China, demand off 3% (first half).

One positive: Global exchange stocks are low and market is in a deficit of around

220,000 tons in the first half of the year.

6

ALUMINUM– 3 months

Source: E-Signal

7

CRU –ali demand falling by 0.3% y/y in 2019 –the first decline since 2009. Demand outside China is down by 1.1%; Chines demand is up only .5%-1.5% (from 4% last year). Supply also falling – globally by -0.6% in the first 8 months of 2019. Down .4% ex-China, down .7%% in China -- but these could be due to one-off production setbacks i China. Chinese exports still rising (up 4% y-o-y) and more production on the way– up 5% next year in China (CRU). Ali scrap is playing an increasing larger supply role, esp in rolled/extrusions. US tariffs no longer supportive. Contangos keeping stocks “hidden” and incentivizing more output. SOURCE: MISC. SOURCES 8

Source: CRU

9

Source: CRU

10Source: CRU

11Source: CRU 12

Zinc – 3 months

13

Source: E-SignalZinc fundamentals got bearish in mid- 2019 as deficit projections gave way to expectations for

big surplus in the second half of the year.

But the surplus has not materialized, allowing prices to stabilize:

--Slower ramp-ups at New Century Tailings, Gamsberg

-- Lower output from South Korea, Europe and India

-- Teck/Trail equipment failure in NA will sideline 20-30k

Going forward, new Chinese supply should come on due to high treatment charges and easier

smelting.

Chinese refined output already up by 8.2% y/y in Jan-August; August output alone by 18.9% y/y

--highest in two years.

Deficit for zinc this year, but focus remains on demand.

Source: Bloomberg/Reuters

14Lead – 3 months

Source: E-Signal

15• Supply conditions remain tight –projected deficit this year 40k-80k

• Korea Zinc’s Onsan lead smelter closed for a 40-day maintenance

• Production at Port Pirie is still down.

• Workers at San Cristobal in Bolivia on strike

• Newmont Goldcorp’s Peñasquito zinc–lead mine on/off

• But….Battery demand fairly weak; Car sales are all off...

• -------------------------

• CRU: Chinese demand down by 1% y/y in 2019, 2nd yearly decline.

• US demand soft, although improving over the summer, US y-t-d replacement demand is off

3.9% (J), while new battery is flat y-t-d.

• Similar trends in Europe.

Source:

Bloomberg/Reuters/CRU

16Source: CRU

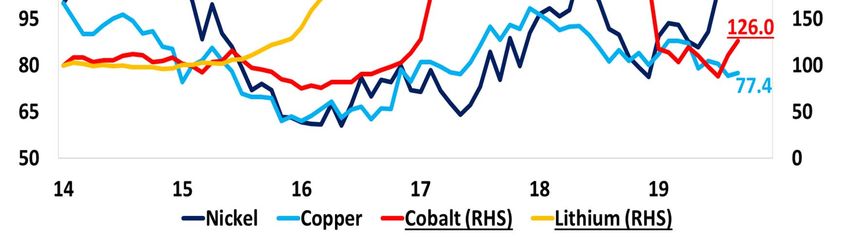

17Nickel Prices - 3 months

Source for data: E-Signal/Futuresource.com

3Reasons behind the recent rally….

--Indonesian ore ban moved up to Jan 2020

-- Reports of Tsingshan buying LME metal

-- Flooding in Indonesia

-- Substantial fund buying

-- LME/Chinese stocks falling/ deficits

4Source for data: International Nickel Study Group (INSG)

5Source for chart: Bloomberg

6Source for chart: Bloomberg

7Global BEV sales set to exceed ICE sales by 2036 (million units)

Source for data: Morgan Stanley (MS)

8Source for data: INSG, WBMS, Wood Mackenzie

9Some caution is in order for the EV price impact on nickel and other metals....

“Cure for high prices is high prices” –

Recycling a new supply source?

Battery technology will change

EV's need to make stand on their own feet without subsidies.

Government policies/targets could change in light of economics and changing

assumptions.

Source for information: Miscellaneous

10Trade uncertainty is biggest common denominator across markets in 2019 and will remain so for

2020. The fallout so far has been serious....

-- Global investment down 19% this past year; FDI into China rose 3% last year, down from

7.9%. FDI in the US fell 19% last year; Chinese investment into the US has collapsed, off some

84% y-o-y in 2018.

-- Growth continuing to slow despite falling rates – manuf. in recession.

-- There has been practically been no “re-shoring” of manufacturing back to the US; 70% of US

operators in China say they would move to other Asian Rim countries.

-- Companies see rising supply chain costs and difficulty in investment planning.

Source: Bloomberg/Reuters

20• Recent US/China agreement still problematic–

• US tariffs suspended for October, not December

• -- Currency Pact? China cannot afford to let the currency “float”?

• Chinese ag purchases $40-$50 billion – no time frame specified; if spread out

over 2 years, this is same as before.

• Concession on financial service activity -- too late in our view.

• Huawei, all other major issues to be discussed later. (Ph 2)

• Enforcement still to be agreed.

• US/China continuing “stop-start” tariffs into next year.

• Hong Kong is an ongoing wild card.

Source: Bloomberg/Reuters

21• How to forecast amid a trade war and slowing growth?

• Very difficult, but our assumption is that metals should start to do

better during the 2nd half of 2020 in expectation that Mr. Trump could

lose.

• Democrats could be less hostile on tariffs and more open to

protracted negotiations ; confidence could return and be positive for

metals going into 2020 amid low-rate environment.

Source: Bloomberg/Reuters

22LME 2020 Ranges*

High Low Average

Copper $6,600 $5,450 $6,090

Aluminum $2,120 $1600 $1,810

Zinc $2,800 $2,180 $2,500

Lead $2,350 $1,820 $2,090

Nickel $19,000 $13,500 $14,500

Tin $19,500 $15,200 $17,500

* These opinions are that of the author. All ranges are inherently subjective and speculative no assurance or guarantee is made that these forecasts will be

achieved. ED&F Capital Markets assumes no liability for the use of this information and expresses no solicitation to buy or sell any investment products

23THANK YOU!

13You can also read