US Rates Strategy US Rates Outlook: Insurance or More? - Ian Lyngen, CFA Head of US Rates Strategy 212-702-1703 - Oregon.gov

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

US Rates Strategy

US Rates Outlook: Insurance or More?

Ian Lyngen, CFA

Head of US Rates Strategy

Ian.Lyngen@bmo.com

212-702-1703

0

Our Call: Late-Cycle Inflection

Q3 '19 Q4 '19 Q1 '20

2s 1.65 1.55 1.15

2s/10s 0.10 0.45 0.45

5s 1.45 1.40 1.20

10s 1.75 2.00 1.60

30s 1.95 2.15 1.80

5s/30s 0.50 0.75 0.60

2s/10s/30s -0.10 0.30 0.25

2s/5s/10s -0.50 -0.75 -0.35

1 Source: BMO CMFed’s Dimming Economic Outlook

FOMC 2019 2020 2021 Long-Run

GDP 2.10 2.00 1.80 1.90

Mar Est. 2.10 1.90 1.80 1.90

Core-PCE 1.80 1.90 2.00

Mar Est. 2.00 2.00 2.00

UNR 3.60 3.70 3.80 4.30

Mar Est. 3.70 3.80 3.90 4.30

Fed Funds 2.40 2.10 2.40 2.50

Mar Est. 2.40 2.60 2.60 2.80

Source: FOMC, BMO CM

2Third Quarter 2019:

Monetary policy uncertainty will be particularly high during the

third-quarter following the Fed’s preemptive easing plan. The

debate is how far (no longer ‘if’) Powell will need to go –

particularly if any additional correction in risk assets has

occurred.

The trade war continues to drag out with no end in sight. The

prospects for further escalation linger as hopes for a near-term

deal with China dim.

Traditional economic theory holds that the 12- to 18-month

lagged impact of monetary policy will begin to flow through to the

real economy in H2 2019.

Source: BMO CM

3Fourth Quarter 2019:

As the year winds down and the combination of mixed economic

optimism and an even more cautious Fed becomes a reality,

questions about what will cause the next recession will dominate

the market discussion.

A lower forward path of policy rates will be priced in as investors

begin to more convincingly look beyond the ‘insurance cut’

narrative to whatever may be lurking on the horizon.

Solidifying concerns about a global slowdown will serve to

contain rates and the shift in monetary policy will lead the belly to

outperform. Any steepening of the curve will be offset by

investors’ belief that the Fed will employ the balance sheet (i.e. a

fresh round of QE) if the next economic downturn becomes

severe enough. This is a new dynamic in the Treasury market

based on the experience of the Fed’s response to the crisis.

Source: BMO CM

4Seasonals are a Key Factor in Our Near-term Bias 5

Rolling Fed Expectations Will Imply Deeper Cuts 6

Financial Conditions Much Easier in 2019 7

Neutral: We’ve Passed It (Funds vs. Core-PCE) 8

Volatility Drives Financial Conditions 9

Front-end Inversion is Very Typical 10

Fed’s Curve Preference 11

Cleveland Fed’s Recession Odds Climbing 12

Under-Confidence Risk 13

Falling Confidence Lowers Spending 14

5s/30s Cyclical Flattening Completed 15

Above Average Growth Sustainable? 16

Trade Remains a Wildcard due to Tariffs 17

Is the CapEx Boom Over? 18

Inventory Drag – Big Bet on Consumption 19

Inventories Building Faster than New Orders 20

Housing Continues Weighs on Domestic Growth 21

Global Business Sentiment Declining 22

Europe Still Leading Race Lower 23

European External Export Growth Stalls 24

Global Manufacturing PMIs Dismal 25

Global Trade Declining Sharply 26

Disappointing 2019 for US and World Economies 27

European Economy Turning? Trade Concerns Linger 28

Italy’s Recession Triggers European Banking Concerns 29

Every Significant Recession Preceded by an Energy Spike 30

Different This Time? US Oil Production Soars 31

Different This Time? Concentration in Lower-end IG 32

Non-Mortgage Interest Payments Spike Ahead of Recessions 33

Savings Rate Falls as Interest Payments Increase 34

Importance of Student Debt and Auto Loans 35

Student Debt Delinquencies Remain Elevated 36

Education Loans Undermining Household Formation 38

Real Wage Gains 39

AHE Don’t Guarantee Accelerating Core-CPI 40

Home Buying Conditions Lowest Since 2009 41

Consumer Confidence and Housing Diverge 42

Home Buying Conditions more than just Mortgage Rates 43

Downward Pressure on Prices in 2018 44

Real Net Worth Negative (YoY) 45

Risk to Corporate Profit 46

Corporate Receipts Drop on Tax Reforms 47

Year-over-Year Core Peaked 48

Rent and OER Remain Strong 49

Downward Pressure on OER 50

Shelter a Key Positive Contributor to Inflation 51

Ex-Shelter CPI Under Pressure 52

Tariffs, Soy (11.2%), and Commodity Pressure 53

Autos: Driving Modest CPI Volatility 54

Apparel: Transitory or Just Volatile? 55

SMRA Shows Investors No Longer Short 56

Sentiment Remains Overbought 57

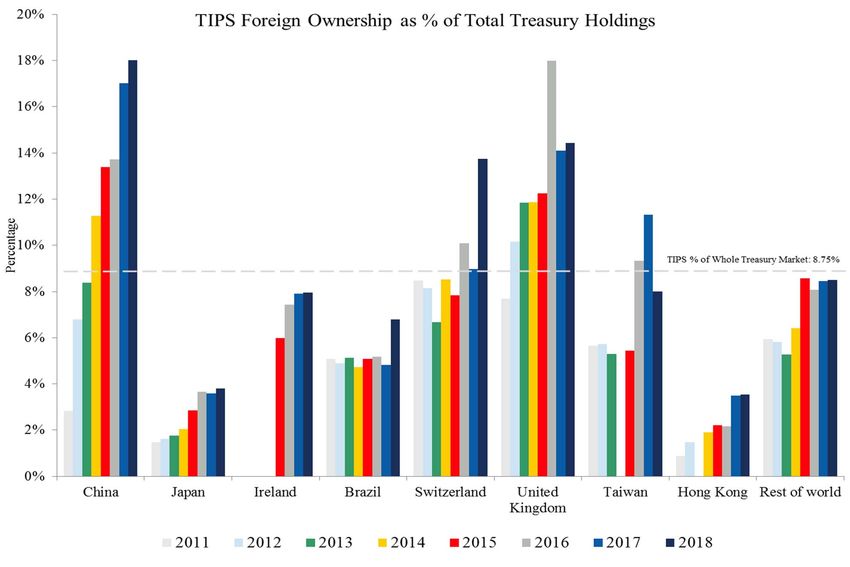

Overseas Interest in TIPS Plummets 58

TIPS Ownership High in China and UK 59

Hedge Adjusted 10-year Yields Range-Bound 60

Japanese Investors Back in Treasuries? 61

When does China Return to Treasuries? 62

Foreign Official Flows Show Significant Selling 63

DISCLAIMER

Disclaimer

These materials are confidential and proprietary to, and may not be reproduced, disseminated or referred to, in whole or in part without the prior consent of BMO CM

(“BMO”). These materials have been prepared exclusively for the BMO client or potential client to which such materials are delivered and may not be used for any

purpose other than as authorized in writing by BMO. BMO assumes no responsibility for verification of the information in these materials, and no representation or

warranty is made as to the accuracy or completeness of such information. BMO assumes no obligation to correct or update these materials. These materials do not

contain all information that may be required to evaluate, and do not constitute a recommendation with respect to, any transaction or matter. Any recipient of these

materials should conduct its own independent analysis of the matters referred to herein.

“BMO CM” is a trade name used by BMO Financial Group for the wholesale banking businesses of Bank of Montreal, BMO Harris Bank N.A. (formerly Harris N.A.) and

Bank of Montreal Ireland p.l.c, and the institutional broker dealer businesses of BMO CM Corp. and BMO CM GKST Inc. in the U.S., BMO Nesbitt Burns Inc. (Member –

Canadian Investor Protection Fund) in Canada, Europe and Asia, BMO Nesbitt Burns Securities Limited (registered in the United States and a member of FINRA), BMO

CM Limited in Europe, Asia and Australia and BMO Advisors Private Limited in India.

BMO does not provide tax or legal advice. Any discussion of tax matters in these materials (i) is not intended to be used, and cannot be used or relied upon, for the

purposes of avoiding any tax penalties and (ii) may have been written in connection with the “promotion or marketing” of the transaction or matter described herein.

Accordingly, the recipient should seek advice based on its particular circumstances from an independent tax advisor.

This document is issued and distributed in Hong Kong by Bank of Montreal (“BMO”). Bank of Montreal is a registered institution licensed and regulated by the Securities

and Futures Commission pursuant to the Securities and Futures Ordinance (Chapter 571 of the Laws of Hong Kong). BMO does not represent that this document may

be lawfully distributed, or that any financial products may be lawfully offered or dealt with, in compliance with any regulatory requirements in other jurisdictions, or

pursuant to an exemption available thereunder. This document is directed only at entities or persons in jurisdictions or countries where access to and use of the

information is not contrary to local laws or regulations. Their contents have not been reviewed by any regulatory authority. This document is provided for general

information only and does not take into account any investor’s particular needs, financial status or investment objectives. This document is not to be construed as an

offer to sell, a solicitation for or an offer to buy, any products or services referenced herein (including, without limitation, any commodities, securities or other financial

instruments), nor shall such Information be considered as investment advice or as a recommendation to enter into any transaction. Each investor should consider

obtaining independent advice before making any financial decisions.

All values in this document are in C$ / US$ / A$ / € / £ / ¥ / ₹ unless otherwise specified

64You can also read