Zur Lage der Weltwirtschaft - VDF/BVDF Jahrestagung 2016 | Hamburg, 29. April 2016 - Stefan Kooths

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

VDF/BVDF Jahrestagung 2016 | Hamburg, 29. April 2016 Zur Lage der Weltwirtschaft Prof. Dr. Stefan Kooths Institut für Weltwirtschaft an der Universität Kiel, Prognosezentrum

Agenda

Weltwirtschaft

» Entgleiste Geldpolitik (I)

» Rohstoffpreisverfall

» Schwellenländerschwäche

Europäische Union/Euroraum

» Entgleiste Geldpolitik (II)

» Quo-vadis European Governance?

Deutschland

» Gefahr der konjunkturellen Überhitzung/Blasenbildung

» Politik der Gegenwartsgeschenke (Infrastrukturerosion)

» Trügerisches demografisches Zwischenhoch

» Flüchtlingsmigration und Arbeitsmarktregulierung

2 | KOOTHS: Zur Lage der Weltwirtschaft

Agenda

Weltwirtschaft

» Entgleiste Geldpolitik (I)

» Rohstoffpreisverfall

» Schwellenländerschwäche

Europäische Union/Euroraum

» Entgleiste Geldpolitik (II)

» Quo-vadis European Governance?

Deutschland

» Gefahr der konjunkturellen Überhitzung/Blasenbildung

» Politik der Gegenwartsgeschenke (Infrastrukturerosion)

» Trügerisches demografisches Zwischenhoch

» Flüchtlingsmigration und Arbeitsmarktregulierung

3 | KOOTHS: Zur Lage der Weltwirtschaft

Global economic activity and business climate

World Economic Activity Business expectations by groups of countries

World output IfW-Indicator World Advanced economies Emerging economies

Percent Index Index

2 2 2

1 1

1

0 0

0 -1 -1

-2 -2

-1

-3 -3

-2 -4 -4

1997 2000 2003 2006 2009 2012 2015 1997 2000 2003 2006 2009 2012 2015

Quarterly data, seasonally adjusted.

Monthly data, seasonally adjusted.

IfW-Indicator: based on business expectations in 42 economies. Based on business expectations in 34 (8) advanced (emerging) economies.

GDP: price adjusted, change over previous quarter.

4 | KOOTHS: Zur Lage der Weltwirtschaft

Typical post-crisis patterns (the not so new “new normal”)

Recovery following an ordinary recession and a severe crisis

Growth path Ordinary recession Severe crisis

„Ordinary“ recessions

120

Index » Induced by preceding booms

» Correction of mismatches

115

» Boom-bust cycles are costly

110

105

Severe crises

» Heavily distorted capital

100

stock/production structures

(obsolete capacities)

95

» Flipside: Financial crisis

90

Quarter

(over-indebtedness) following

0 1 2 3 4 5

excessive credit expansion in

Annual data, volume; GDP as index (year0=100); recovery following a

decline of GDP of 5 percent in year 1; according to Boysen-Hogrefe et al.

(forthcoming)

preceding boom

5 | KOOTHS: Zur Lage der WeltwirtschaftWeltproduktion und Welthandel 2014-2020 6 | KOOTHS: Zur Lage der Weltwirtschaft

TurmOil: Three (interwoven) troublemakers

Commodity prices

Slump in raw material HWWI-Index ex energy Brent oil (rhs)

prices 300

2010=100 US-$

140

» Global income redirection 120

250

2.6 percent (2015)

100

0.8 percent (2016) 200

80

150

(Other) structural problems 60

in emerging economies 100

40

50

20

Derailed monetary policy in 0 0

2000 2002 2004 2006 2008 2010 2012 2014 2016

the Western world

Monthly data.

Commodities prices without energy: HWWA-index based on US-Dollar.

7 | KOOTHS: Zur Lage der WeltwirtschaftGlobal oil market and implications for net oil exporters

GDP of the 15 biggest Net-Oil Exporters and Oil price Global oil market

GDP Oil price Inventory change (rhs) Oil consumption Oil production

Percent Percent Mn. Mn.

10 80 98 5

4

8 60 96

3

94

6 40 2

92

1

4 20

90 0

2 0

-1

88

0 -20 -2

86

-3

-2 -40 84

-4

-4 -60 82 -5

1991 1995 1999 2003 2007 2011 2015 2008 2009 2010 2011 2012 2013 2014 2015 2016

Yearly data; percentage change; Oil price: Brent in US-Dollar; Quarterly data; barrel per day.

GDP: percentage change weigthed by nominal GDP in US-Dollar.

8 | KOOTHS: Zur Lage der WeltwirtschaftSlumping Western stock markets (1/2)

Stock prices

Eurostoxx 50 Nikkei 225 S&P 500

Recent peak-to-trough

150 Index (2006=100 )

» US: - 13 percent

140 » JP: - 23 percent

130 » EU: -27 percent

120

110

100

90

80

70

60

50

40

Weekly data; last Value: March 03, 2016.

9 | KOOTHS: Zur Lage der WeltwirtschaftSlumping Western stock markets (2/2)

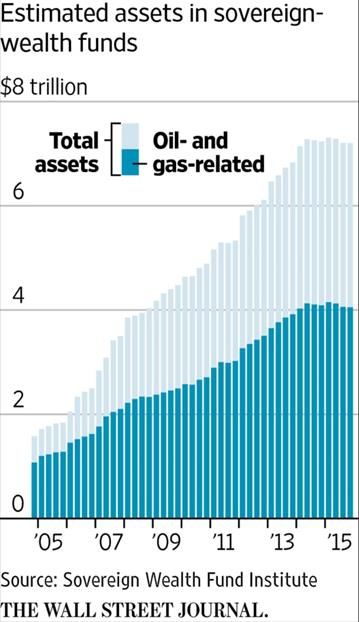

Sovereign wealth funds:

Not so wealthy anymore

» Approx. 5 percent of all stocks

» Estimated/expected net sales

USD 200 bn (2015)

USD 400 bn (2016)

Low interest rate environment:

Feeding market volatility

» Sensitive discount factors (DF)

» 50 bp increase

DF(5%) = 20 DF(5.5%) = 18.2

DF(1%) = 100 DF(1.5%) = 66.7

10 | KOOTHS: Zur Lage der WeltwirtschaftGlobal QE

Data source: Thomson Reuters Datastream, IfW calculations

Monetary Base Nominal effective exchange rates

Fed BoE BoJ ECB USD GBP JPY EUR CNY

Index (2005=100)

1000 160 Index (2005=100)

900 150

800 140

700 130

600 120

500 110

400 100

300 90

200 80

100 70

0 60

2005 2007 2009 2011 2013 2015 2017

Quarterly data. Monthly data.

11 | KOOTHS: Zur Lage der WeltwirtschaftMoney matters

More money cannot cure what too much money created.

(Patrick Barron)

Capital gives money the time to cause trouble.

(Roger Garrison)

We are destined to spend decades

paying for the easy money orgy of a few years.

(Ludwig von Mises)

12 | KOOTHS: Zur Lage der WeltwirtschaftMonetary Policy: Overloaded

Source: FAZ, 26 October 2011, p. 11

13 | KOOTHS: Zur Lage der WeltwirtschaftStimulus policies: Riding a dead horse?

Fiscal policy record high public debt levels

Monetary policy zero interest rates

» Private sector over-indebtedness, but: more money = more debt

» Rational uncertainty

Negative interest rates, central bank money explosion

CBs fight for inflation (and weaker currencies?)

Debate on helicopter money, ban on cash, …

Investors realize that they are not operating in normal times

Capital stock crisis

» Severe distortion of price and production structures

» The problem is in the composition, not in the levels of aggregates

Crisis of interventionism/short-termism

14 | KOOTHS: Zur Lage der WeltwirtschaftThree options of coping with debt-crises

Public bail-outs

» Shifts private debt to public sector

» Private debt crisis sovereign debt crisis Anti-capitalist

approach

» No solution for fiscally distressed countries (harms principle of

Inflating the debt away accountability,

creates moral

» Takes a long time, promotes zombification hazard risks)

» Puts the currency at risk

» Not targeted towards non-performing loans

Liquidation

Capitalist

» Tough (cold turkey) in the short-run … approach

» … but targeted (and root cause oriented) (in line with free

» Puts capital at second (now first) best use market principles)

15 | KOOTHS: Zur Lage der WeltwirtschaftSome thoughts on the cashless society

Focus

» Supervision of transactions (crime control)

» Room for negative interest rate polices (secular stagnation thesis)

So far: Cash (banknotes) as exclusive legal tender

Ersatz

» Declaring commercial bank money as legal tender

Ultimate privilege, totally at odds with a market economy

» Central banks offers electronic high powered money to anyone

Dramatic pull effect, transition to 100-percent-money

Chicago plan 2.0 (one-off anti-market socialization of risks)

Eliminating elastic credit creation

Last way out of current monetary systemic dead-end?

(private money emission to safeguard monetary discipline)

16 | KOOTHS: Zur Lage der WeltwirtschaftAgenda

Weltwirtschaft

» Entgleiste Geldpolitik (I)

» Rohstoffpreisverfall

» Schwellenländerschwäche

Europäische Union/Euroraum

» Entgleiste Geldpolitik (II)

» Quo-vadis European Governance?

Deutschland

» Gefahr der konjunkturellen Überhitzung/Blasenbildung

» Politik der Gegenwartsgeschenke (Infrastrukturerosion)

» Trügerisches demografisches Zwischenhoch

» Flüchtlingsmigration und Arbeitsmarktregulierung

17 | KOOTHS: Zur Lage der WeltwirtschaftEuro area: Debt overhang hampering credit channel

Data source: Bank for International Settlements, World Bank

Gross Private Sector Debt Non-Performing Loans

Protugal Italy Spain Greece Ireland Portugal Italy Spain Greece Ireland

Percent

Percent 40

350

35 34,4

300

30

250

25

200

20

18,9

17,3

150

15

12,3

100 10

7,0

50 5

0

0 2000 2002 2004 2006 2008 2010 2012 2014

2000 2002 2004 2006 2008 2010 2012 2014

Annual Data. In relation to nominal GDP. Annual data. Share of total loans.

18 | KOOTHS: Zur Lage der WeltwirtschaftEuro area: Monetary financing of governments

Data source: Eurostat, European Commission

Gross Government Debt Government Bond Yields (10-year)

Germany France Italy Spain EMU Germany France Italy Spain EMU

Percent 8 Percent

140

7

120

6

100

5

80

4

60 3

40 2

1

20

0

0

2005 2007 2009 2011 2013 2015 2005 06 07 08 09 10 11 12 13 14 15 16

Annual Data. In relation to nominal GDP; EMU: Average. Monthly data. EMU: Averrage.

19 | KOOTHS: Zur Lage der WeltwirtschaftTarget-2 imbalances:

Intra-euro area liquidity and capital flight are back

TARGET balances

Bank Recovery and billion euro

1200

Resolution Directive (BRRD) 1000

FIN

» Passed in March 2014 800

NED

LUX

» Bail-in elements 600

Liquidity flight 400 GER

200

Greek crisis 2015 0 AUT

BEL

» Capital flow and cash controls -200 ESP

-400 ITA

» ELA

-600 GRE

Liquidity and capital flight -800

POR

IRE

FRA

QE-programs -1000

» Starting in March 2015 -1200

20 20 20 20 20 20 20 20 20

08 09 10 11 12 13 14 15 16

» 60 (now 80) bn Euro/month

Monthly data. Sorce: ECB.

Capital flight

20 | KOOTHS: Zur Lage der WeltwirtschaftQE-related policy risks

Inflation targeting and policy communication

» (Necessarily) disappointing expectations

» Central bank reputation (overall monetary policy approach)

Central bank independence and monetary financing

» Pending loss risks on Eurosystem‘s balance sheets

» Eurosystem becomes largest single creditor of European governments

Systemic financial risks and misallocation of resources

» Asset price bubbles and systemic financial instability

» Misallocation of resources and zombification

Disincentives for governments

» Structural reform policies

» Fiscal consolidation

Distortions in foreign exchange markets (“currency wars”)

21 | KOOTHS: Zur Lage der WeltwirtschaftKrise als Beschleuniger der europäischen Integration?

Maastricht-Vertrag (Februar 1992)

Stabilitäts- und Wachstumspakt (Juli 1997), Reform (März 2005)

Wachstumsstrategie „Europa 2020“ (Juni 2010)

EFSF (Juni 2010)

Europäisches Semester (September 2010)

Euro-Plus-Pakt (März 2011)

Six-Pack (Dezember 2011) MIP

Fiskalpakt (März 2012)

ESM (Oktober 2012)

Two-Pack (Mai 2013)

22 | KOOTHS: Zur Lage der WeltwirtschaftMakroökonomisches Ungleichgewichteverfahren (MIP)

Fokussierung

» Krisenprävention (vs. Europa 2020)

» Gemeinschaftsinteressen (vs. „gute“ Wirtschaftspolitik)

Spannungsfelder

» Koordinierung vs. Subsidiarität

» Strukturprobleme vs. Makroindikatoren

Konzeptionelle Unschärfe (eklektischer Ansatz)

» Makroökonomischer Ungleichgewichtsbegriff

» Wettbewerbsfähigkeit von Wirtschaftsräumen

Ökonomische Systeme als soziokybernetische Regelkreise

» Binnenmarkt: Pekuniäre „externe“ Effekte als Normalfall

» Instrumenteneinsatz: Primat der Primärwirkung über Nebeneffekte

23 | KOOTHS: Zur Lage der WeltwirtschaftKrisenerklärung und -interpretation

MIP: Reaktion auf europäische Schuldenkrise

Finanzkrisen Kapitalstockverzerrung

» Monetäre Konjunktur- und Krisentheorie

» Zinsniveau, Fristentransformation und Produktionsstruktur

(realwirtschaftliche Verwurzelung einer Finanzkrise)

» Krise als Korrektur nicht-nachhaltiger Forderungspositionen

(Liquidationskrise zur Bereinigung von „Zombie-Strukturen“)

» Neubewertung des marktfähigen Kapitalstocks

Krisendiagnose in EUV 1176/2011

» Unzureichende wirtschaftspolitische Koordination

» Mangelnde ökonomische Konvergenz (Leistungsfähigkeit)

24 | KOOTHS: Zur Lage der WeltwirtschaftOrdnungsökonomisches Spannungsfeld

Subsidiaritätsprinzip gemäß EU-Vertrag

(Wettbewerb und wirtschaftspolitische Selbstverantwortung)

Abwehr von Fehlentwicklungen in einzelnen Mitgliedsländern,

die das Gemeinschaftsinteresse berühren

(Koordinierung und wirtschaftspolitische Überwachung)

Hohe Hürden für die Legitimation von Eingriffen

» Nachweis systemischer externer Effekte erforderlich

» Recht auf „falsche“ nationale Wirtschaftspolitik liegt im

Gemeinschaftsinteresse (Raum für institutionelle Experimente)

25 | KOOTHS: Zur Lage der WeltwirtschaftMakroökonomische Koordinationsdefekte

Ökonomische Diskrepanzen zwischen einzelwirtschaftlichen Plänen

Ungleichgewichte Dynamische Koordinationseffizienz

(Abbau von Angebots- und Nachfrageüberhängen)

Pervasive Koordinationsdefekte

Verfügungsrechte (Ordnungsrahmen)

Makroökonomische Geld (allgemeines Tauschmittel)

Ungleichgewichte Kapital/Zins (intertemporale Koordination)

Arbeit/Lohn (quasi-universeller Produktionsfaktor)

Grenzüberschreitende Koordinationsdefekte

MIP-relevante Geld- und Kreditwesen, Schuldentragfähigkeit

Ungleichgewichte

≠ Konjunkturglättung (Globalsteuerung)

≠ Pekuniäre Wettbewerbseffekte im Binnenmarkt

Dysfunktionale Koordinationsmechanismen Symptomatische Makroentwicklung

26 | KOOTHS: Zur Lage der WeltwirtschaftSystemische externe Effekte und Stabilitätskultur

Finanzsystem: Geld- und Kreditwesen

» Kreditdeckung des Geldes

(simultane Geld- und Kreditschöpfung aus dem Nichts)

» Implizite Gesamthaftung für Kollateral des Eurosystems

» Regulierungsarbitrage

Hartwährungsverbund erfordert Stabilitätskultur

» Variante 1:

Haftungsprinzip, Anreiz zur Vorsicht („No-bail-out“)

» Variante 2:

Überwachung, Hilfen unter Auflagen („No-bank-left-behind“)

Funktionsfähigkeit von Institutionen beruht auf Einsicht und

gemeinsamem Regelverständnis (Ownership)

27 | KOOTHS: Zur Lage der Weltwirtschaft„Nationale Wettbewerbsfähigkeit“

WF kein makroökonomisch bedeutungsvolles Konzept

» Anpassung der Faktorpreise

» Internationaler Handel kein Nullsummenspiel

» Konsummöglichkeiten sind relevant (Volkswirtschaft ≠ Exportsektor)

Leistungsfähigkeit = Produktivität

» Produktivität entscheidet über Einkommen/Terms-of-Trade,

nicht über Vorteilhaftigkeit des Außenhandels

» Funktionsfähiger Binnenmarkt setzt weder hohe, noch konvergierende

Produktivität voraus (sondern hat sie zur Folge)

» Produktivitätsschwäche: Kein Problem der Außenbeziehungen

Politikkoordinierung?

» Best-practice und peer-review

» Keine Interessenkonflikte, Recht auf „schlechte“ Wirtschaftspolitik

28 | KOOTHS: Zur Lage der WeltwirtschaftPrimat des Subsidiaritätsprinzips

Subsidiaritätsprinzip

» Anreizkonstellation

» Informationsstand

» Instrumentenzugriff

» Demokratische Legitimierung

Vertikaler Aufgabenzuschnitt

» Theorie des Fiskalföderalismus (Exkludierbarkeit, Rivalität)

» Genuine europäische Gemeinschaftsgüter statt „politische Projekte“

Subsidiarität macht Europa stark, nicht schwach

29 | KOOTHS: Zur Lage der WeltwirtschaftAgenda

Weltwirtschaft

» Entgleiste Geldpolitik (I)

» Rohstoffpreisverfall

» Schwellenländerschwäche

Europäische Union/Euroraum

» Entgleiste Geldpolitik (II)

» Quo-vadis European Governance?

Deutschland

» Gefahr der konjunkturellen Überhitzung/Blasenbildung

» Politik der Gegenwartsgeschenke (Infrastrukturerosion)

» Trügerisches demografisches Zwischenhoch

» Flüchtlingsmigration und Arbeitsmarktregulierung

30 | KOOTHS: Zur Lage der WeltwirtschaftBruttoinlandsprodukt und Komponenten 2014-2020 31 | KOOTHS: Zur Lage der Weltwirtschaft

Arbeitsmarkt und Preisentwicklung 2014-2020 32 | KOOTHS: Zur Lage der Weltwirtschaft

Drohende Überhitzung (stilisierter Konjunkturzyklus)

Kapazitätsauslastung Kapazitätsauslastung

(Abschwung/Kontraktion) (Aufschwung/Expansion)

Produktion tatsächlich

Erholung

Rezession

Abkühlung

Boom

Überauslastung Unterauslastung

Zeit

33 | KOOTHS: Zur Lage der WeltwirtschaftMittelfristprojektion für Deutschland

Potential und Produktion

Produktionslücke (rechte Skala) Bruttoinlandsprodukt Potenzial

Mrd. Euro Prozent

3200 5

4

3000

3

2800 2

1

2600

0

2400

-1

2200 -2

-3

2000

-4

Projektion

1800 -5

1991 1993 1995 1997 1999 2001 2003 2005 2007 2009 2011 2013 2015 2017 2019

Jahresdaten; Bruttoinlandsprodukt, Potential: preisbereinigt (verkettete Volumenwerte, Referenzjahr 2010).

Quelle: Statistisches Bundesamt, Fachserie 18, Reihe 1.2; Berechnungen und Projektion des IfW.

34 | KOOTHS: Zur Lage der WeltwirtschaftWachstumspotenzial und -faktoren 2001-2020

Produktionspotenzial und Wachstumsfaktoren

Prozent(punkte)

2,0

TFP Kapital Arbeit Potenzial

1,5

1,0

0,5

0,0

Projektion

-0,5

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

Jahresdaten. Produktionspotenzial: Veränderung gegenüber Vorjahr in Prozent; Faktoren: Wachstumsbeitrag in Prozentpunkten.

Quelle: Statistisches Bundesamt, Fachserie 18, Reihe 1.2; Berechnungen und Projektion des IfW;

35 | KOOTHS: Zur Lage der WeltwirtschaftPotenzielles Arbeitsvolumen 2001-2020

Potenzielles Arbeitsvolumen und Komponenten

Prozent(punkte)

0,8

0,6

0,4

0,2

0,0

-0,2

-0,4

Projektion

-0,6

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

Erwerbsbevölkerung Parizipation NAIRU Arbeitszeit Arbeitsvolumen

Jahresdaten, Vorjahresveränderung (Arbeitsvolumen) und Wachstumsbeiträge (Komponenten).

Quelle: Statistisches Bundesamt, Fachserie 18, Reihe 1.2; Berechnungen und Projektion des IfW.

36 | KOOTHS: Zur Lage der WeltwirtschaftDemografisches Zwischenhoch bis 2020 37 | KOOTHS: Zur Lage der Weltwirtschaft

IfW-Szenario zur Flüchtlingsmigration 38 | KOOTHS: Zur Lage der Weltwirtschaft

Flüchtlingsmigration: Kein makroökonomischer Gamechanger

Makro-Effekte

» Kurzfristig stimulierend via

Staatsausgaben (25 Mrd. p.a.)

» Potenzialeffekte mit

Verzögerung

Zugang zum Arbeitsmarkt ist

entscheidend

» Mindestlohnhürde

» Qualifizierung „on the job“

39 | KOOTHS: Zur Lage der WeltwirtschaftÖffentliche Infrastruktur 1991-2020

Öffentliche Nichtwohnbauten

Mrd. Euro Mrd. Euro

30 1100

Kapitalstock (rechte Skala) Nettoinvestitionen Projektion

1080

20

1060

10

1040

0 1020

1000

-10

980

-20

960

-30 940

1991 1993 1995 1997 1999 2001 2003 2005 2007 2009 2011 2013 2015 2017 2019

Jahresdaten.

Kapitalstock: Nettoanlagevermögen des Staates, preisbereinigt (Referenzjahr 2010); Nettoinvestitionen: in jeweiligen Preisen.

Quelle: Statistisches Bundesamt, Fachserie 18, Reihe 1.4 und Anlagevermögen nach Sektoren (Arbeitsunterlage); Berechnungen und Projektion des IfW.

40 | KOOTHS: Zur Lage der WeltwirtschaftAusgabenanteile der Gebietskörperschaften 1991-2015

Prozent Prozent

25 25

Differenz Investive Ausgaben Sozialausgaben

20 20

15 15

10 10

5 5

0 0

1991 1993 1995 1997 1999 2001 2003 2005 2007 2009 2011 2013 2015

Jahresdaten, Anteil an den Gesamtausgaben der Gebietskörperschaften.

Investiv: Bruttoinvestitionen und Investitionszuschüsse; Sozial: Monetäre Leistungen und Sachleistungen.

Quelle: Statistisches Bundesamt, Fachserie 18, Reihe 1.4; Berechnungen des IfW.

41 | KOOTHS: Zur Lage der WeltwirtschaftInfrastrukturbereitstellung

Tonnendenken vermeiden (mehr ≠ besser)

Privatisierung und Bereitstellungsagenturen

» Finanzierung über Nutzungsentgelte (Gebühren, Beiträge)

» Investitionssignale via Zahlungsbereitschaft

» Keine Haftungsübernahme durch den Staat

Niedrigzinsen keine Begründung für öffentliche Investitionen

» Massiver Einfluss der Geldpolitik

» Nullzinsen ≠ Nullkosten (Abschreibungen!)

» Verstetigung der Investitionstätigkeit

» Finanzierungslast vs. Finanzierungskonflikt:

„Generationenausgleich“ via Staatsverschuldung läuft ins Leere

42 | KOOTHS: Zur Lage der WeltwirtschaftYou can also read