Why mobile social media money transfers are going to be huge - WHITE PAPER - By Robin Arnfield | Contributing writer, Digital Signage Today ...

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

WHITE PAPER

Why mobile

social media money

transfers are going

to be huge

By Robin Arnfield | Contributing writer,

Digital Signage Today

SPONSORED BY:

WHITE PAPER

Why mobile

social media money

transfers are going

to be huge

By Richard Slawsky | Contributing writer,

Digital Signage Today

SPONSORED BY:

FIs and payment processors have a major opportunity to collaborate with FinTech pioneers

such as Moneymailme to serve the growing market for mobile social media money transfers.

Mobile person-to-person (P2P) transfers are increasingly replacing cash and checks for

informal transactions, particularly among millennials. Convenient, easy-to-use mobile P2P

apps such as Venmo and Google Wallet have been enabling users to send money to each

other without visiting ATMs to get cash, or banks to cash checks. Improved newcomers are

coming to market as the economic scale rises to meet the trend and emerging need. Mon-

eymailme, the United Kingdom start-up app that fuses chat into its transfer function, has

caught the attention of FinTech investors.

What will really drive the mobile P2P market will be the ability for consumers to chat via

social media apps and at the same time embed mobile money transfers in their messages.

Venture capital investments

The FinTech sector is attracting considerable interest from venture capitalist firms. Global

investment in fintech ventures in the first quarter of 2016 reached $5.3 billion, a 67 percent

increase over the same period last year, with Europe being the fastest growing region in

© 2016 Networld Media Group | Sponsored by Moneymailme

2

the world, according to an Accenture report. Investments going to fintech companies in

Europe and Asia-Pacific nearly doubled to 62 percent, Accenture says.

The P2P money transfer market has proved a key target for investors. In July 2015, Sin-

gapore-based social media money transfer firm Fastacash raised $15 million in Series B

funding from international investors, taking its total funding to $23.5 million.

Other digital money transfer firms which have raised significant amount of investments

include London-based WorldRemit which as of February 2016 had so far received nearly

$200 million, U.K.-based Azimo which raised $20 million in June 2015 and integrates with

Facebook for money transfers, and London-based TransferWise which raised $58 million

in January 2015.

Mobile banking

Because of its ubiquitous nature, the smartphone is expected to become the primary

digital banking channel, especially among Millennials. This consumer segment takes their

smartphones everywhere, and use them for all aspects of their life, including purchases

and banking transactions.

The 2015 Bank of America Trends in Consumer Mobility Report found that 38 percent of

U.S. adult consumers never disconnect from their smartphones. Bank of America (BofA)

says 89 percent of U.S. adults check their smartphones at least several times daily, and 36

percent report they constantly check their devices.

This growing dependency is visible in managing finances. BofA found that, of those con-

sumers who use a mobile banking app, 62 percent access it at least a few times a week,

Potential nontraditional providers for personal banking

and financial needs

Amazon 40%

Google 37%

PayPal 34%

Apple 31%

Walmart 26%

AT&T 24%

Verizon 24%

Facebook 24%

Starbucks 22%

Twitter 19%

Square 16% Source: Synergistics Research

© 2016 Networld Media Group | Sponsored by Moneymailme

3

while 20 percent check at least once a day. It found that 51 percent of respondents use

mobile or online banking as their preferred method of banking. Less than a quarter (23

percent), including six percent of younger millennials aged 18–24, complete the majority of

their transactions at branches.

According to BI Intelligence’s “The Digital Disruption of Retail Banking” report, U.S. mil-

lennials increasingly use digital banking channels for banking tasks, and visit their banks’

branches less often than ever before.

The BI Intelligence report says the smartphone will become the foundational banking

channel. “Banks that don’t act fast are going to lose relationships with customers,” it

warns. “Consumers are increasingly opting for digital banking services provided by third-

party tech firms. This is disrupting the relationships between banks and their customers,

and banks are losing out on branding and cross-selling opportunities.”

A survey by Norcross, Georgia-based Synergistics Research for its “Millennials: Financial

Insights” report found that millennials are open to using a wide variety of non-traditional

organizations for banking services.

“Millennials aren’t going to abandon tra-

ditional financial providers,” says Syn-

ergistics COO Genie Driskill. “However,

they will look at all types of organiza-

tions including non-traditional providers

to meet their financial needs. Traditional

providers are faced with a challenge to

show how their products and services

have value and utility in this increasingly

competitive environment.”

Rapid growth

According to a U.S. consumer survey by San Francisco, California-based Javelin Strategy

& Research for its Mobile P2P Payments in 2015: The Growth and Adoption of Mobile

Money Transfers report, the number of U.S. mobile P2P users will grow from 69 million in

2015 to 126 million by 2020. By 2019, Javelin expects over half of all U.S. mobile device

owners to use mobile P2P.

Globally, the number of mobile P2P transfers was forecast by Hampshire, U.K-based

Juniper Research to have risen by nearly 150 percent in 2015 to more than 13 billion, with

several social media firms experiencing significant growth in service usage.

Juniper Research’s Mobile Money Transfer & Remittances: Domestic & International Mar-

kets 2015-2020 report predicts that social media will play a major role in driving the global

mobile money transfer market. During 2015, PayPal subsidiary Venmo was handling $1 bil-

lion in social media transfers per quarter.

© 2016 Networld Media Group | Sponsored by Moneymailme

4Javelin says the influx of new mobile P2P users is

attracting new non-bank competitors such as Face-

book and Snapchat, which are keen to enhance their

social media apps’ functionality to include everyday

occurrences such as P2P transfers.

A social media user can send money to a friend sitting

opposite them at dinner to pay for their share of the

meal. A friend can send funds as a birthday or Christ-

mas gift to someone via social media, embedding the

transfer in a message containing photos or videos.

International transfers

The social media P2P transfer services offered by Facebook, Venmo and SnapChat (its

SnapCash partnership with Square) are currently restricted to the U.S.

With the global adoption of social media and particularly with the growing use of P2P for

international remittances to emerging markets, there is a need to be able to embed inter-

national money transfers within social media communications.

London, U.K.-based Moneymailme has developed the Moneymailme app which can be

downloaded from the Google Play Store and the Apple iPhone App Store. The app lets

consumers chat with each other, receive news feeds and send free money transfers across

the world, including 33 African nations where the historically lucrative remittance flow is

larger than foreign aid packages. Moneymailme’s business model offers free sending and

receiving of funds, in US dollars, British pounds, or EU euros with minimal charges (2.4

percent) for topping up and withdrawing into bank accounts and onto credit cards from

Moneymailme accounts.

Highest known industry standards for security and financial safely are ensured by Money-

mailme’s use of PINs/passwords for each transaction and the fact that its app can only be

used on one smartphone, not multiple devices. The company has employed some of the

most advanced security programmers.

Opportunity for FIs

FIs and payment companies have an opportunity to collaborate with FinTech start-ups

such as Moneymailme to capitalize on the fast-growing market for domestic and interna-

tional social media money transfers. Millennial consumers, in particular, want to be able to

carry out free or very low-cost money transfers while engaging in social communications.

According to “Innovation in Retail Banking,” a November 2015 report by financial IT firm

Infosys Finacle, a subsidiary of India-based Infosys and Paris, France-based banking in-

dustry association EFMA, 72 percent of banks surveyed perceive that the threat of indus-

try disruption in retail banking is high or very high.

© 2016 Networld Media Group | Sponsored by Moneymailme

5“Several new technologies have emerged in recent years which are starting to have a

dramatic impact on the banking industry,” the EFMA/Infosys Finacle report says. “The

most important of these according to banks is mobility, where 59 percent of banks expect

the impact to be high or very high. The most notable disruptive business model which

has impacted banking is Peer-to-Peer (P2P), already affecting product areas like personal

and small business lending, and money transfers. 40 percent of respondents in our survey

believed that P2P will have a high or very high impact on the industry.”

The EFMA/Infosys Finacle report says banks expect that start-ups will have the most im-

pact in the payments industry in the P2P payments space. Unlike incumbent banks, which

are often hampered by legacy IT systems, FinTech start-ups have greenfield technology

which enables them to be very innovative and fast-moving.

“Banks’ systems are so complex and clunky that it takes a bank two years to do any-

thing,” a FinTech executive whose firm provides payment services to banks was quoted as

saying in the Economist Intelligence Unit report “The Disruption of Banking.”

Rather than leave Millennials to migrate from bank accounts at traditional banks to ac-

counts with disruptive new digital-only financial services providers, FIs can partner with

social media money transfer leaders such as Moneymailme to target this demographic.

Moneymailme is currently in discussion with its A List of global banks in countries it deems

strategic in its first tier marketing to acquire hundreds of thousands of users with each

institutional partner.

FIs can enjoy branding and cross-selling opportunities by partnering with Moneymailme

and also share in the revenue stream these firms generate from charges for topping up or

withdrawing from social media money transfer accounts.

Provided customers opt in to let Moneymailme collect data on their Moneymailme trans-

actions, the company’s bank partners can leverage and analyse this transaction informa-

tion and offer their customers targeted financial management services.

Remittances

There is a major opportunity to use social media

for remittances to emerging markets, since many

people in these countries are using social media.

As a use case example, a migrant worker takes a

short break from work, switches on their Money-

mailme app, chats with a relative back home and

sends them some money from within the app. This

is far easier and cheaper than having to go to a

money transfer service agent’s office.

“Progress in the remittances sector is crucial to aid

global development, as it enables migrant workers

© 2016 Networld Media Group | Sponsored by Moneymailme

6to send money home more effectively than traditional FIs allow,” Rajesh Agrawal, founder

and CEO of London, U.K.-based international money transfer firm Xendpay, wrote in a Mo-

bile Payments Today blog. “Mobile wallets, for example, continue to gain popularity across

the world, especially in areas where access to bank accounts is limited, enabling users to

pay for specific goods and services, such as groceries and bills straight from their device.

It can be expected that instant mobile-to-mobile transfers will become the standard for

individuals sending money across borders, replacing remittances sent in cash in the post

or via risky high-street outlets. Not only will this make transfers more secure, but it will also

help drive down the cost of transfer fees.”

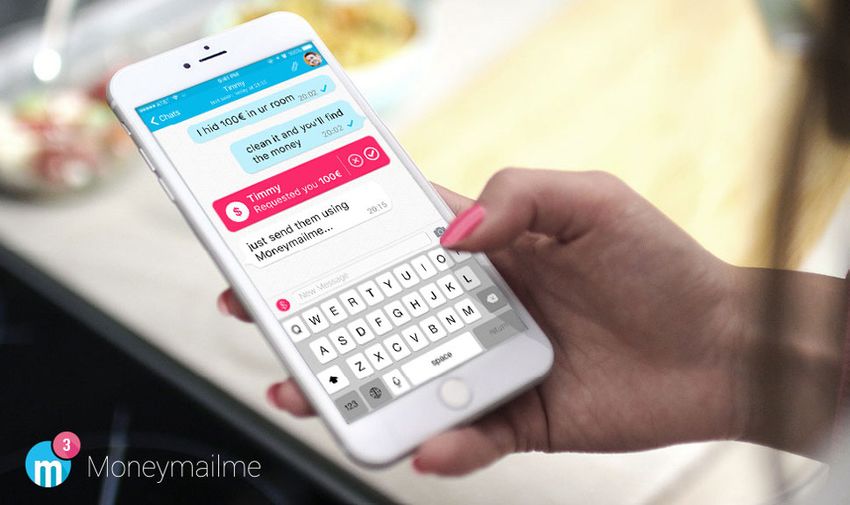

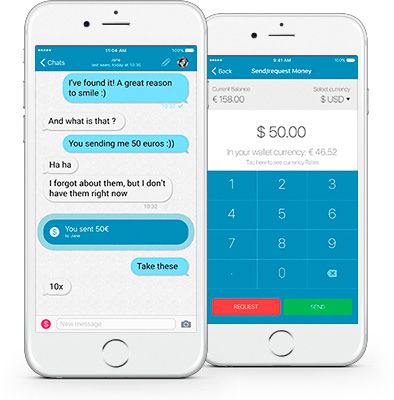

Moneymailme’s M3 app

M3 meets the Millennial consumer’s requirement to have an All remittance transactions within the app are free, although

app which brings everything together, making chat, reading there is a charge to add or withdraw money from a Money-

news, sending money to friends or making charitable dona- mailme account.

tions fast and easy. Moneymailme enables the use of three different currencies

Features offered by the app include chat; picture- and video- (EURO, USD and GBP) in its network and foreign exchange

sharing; instant worldwide money transfers; personalized capability, to help make transferring money abroad easier for

news feeds from the most important international publications users worldwide. Due to the product’s highly advantageous

which users can share with their contacts; sending the user’s fees and global reach of its services, Moneymailme is on target

GPS locations to friends; and donations to charitable causes, to reach 50,000 users by the end of the Q3 2016.

humanitarian projects and advocacy campaigns. Additional services and features are in beta phase now, in-

Users import their contacts from their phone by clicking the cluding a synergy with publishers including Washington and

invite button on the people they want to connect with. They Dakar-based Kiwai Media to enable readers in developing

receive a message with a link to download the app, and, after countries the ease of access to new content as e-books and

doing so, appear in the user’s contact list. print on demand titles.

About the sponsor:

London, U.K.-based Moneymailme was founded to develop a millennial-oriented social media app that responds to an unmet need

in the market by incorporating global social money transfers with instant conversation.

For more information, visit www.moneymail.me

© 2016 Networld Media Group | Sponsored by Moneymailme

7You can also read