2014 Housing Giants Special Report

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

www.ProBuilder.com

May 2014 Powered by HousingZone.com

2014

Housing

Giants

Special Report:

• In pursuit of capital: the finance gap / 32

• The long road to energy efficiency / 38

• The resurrection of Orleans Homes / 46

• Ranking the nation’s largest builders / 50

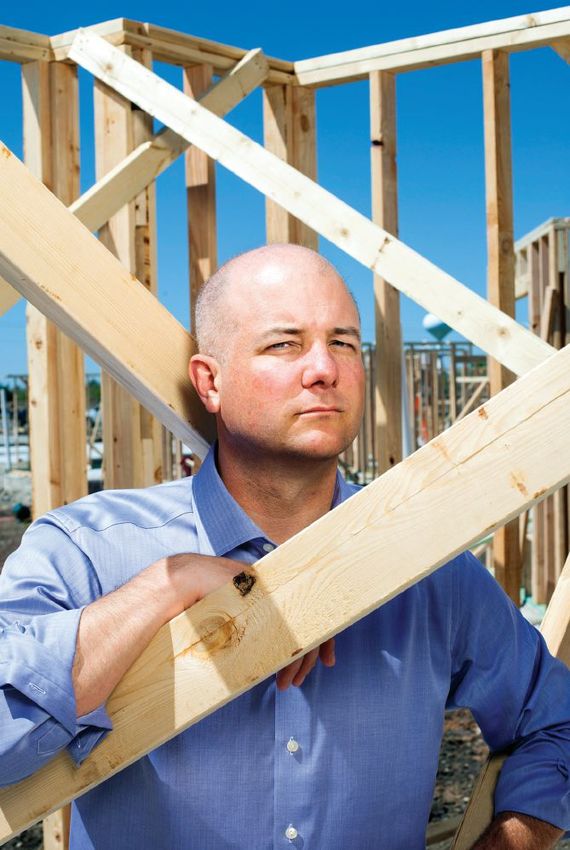

Eric Lipar

Chairman and CEO

LGI Homes

PHOTO: BEN SKLAR / DBPHOTOAGENCY

2012 JESSE H. NEAL

AWARD WINNER

special report:

Notching their best year since 2008, the nation’s biggest

builders took advantage of an improving economy and

a better housing market to find revenue in new places.

By Patrick O’Toole, Denise Dersin, Mike Beirne, Kyle Clapham, Scott Sedam

housing giants report contents n the more than 40 years this publication has com-

piled its annual list of the nation’s largest builders—

special pull-out giants map 28 the Housing Giants—seldom, if ever, have the results

over time reflected such a deep and prolonged decline

overview and analysis 29 in revenue and output as the one experienced by

builders over the past several years.

In 2008, as builders began reporting their initial de-

in pursuit of capital 32

scent, the largest 225 firms tallied $81.4 billion in rev-

enue on 317,361 closings. At the bottom, in 2011, those

the long road to energy efficiency 38 figures shrank by nearly half to $42.3 billion on 172,750 clos-

ings. The good news: The 2014 Housing Giants report clearly

resurrection: the saga of orleans homebuilders 46 shows that the downturn has been replaced by a housing

market filled with new opportunities and new challenges.

housing giants rankings 50 This past year, the largest 225 Housing Giants (of the 293

Giants reporting) made double-digit gains to get within ear-

shot of levels from five years ago and banked $75.4 billion in

methodology revenue on 254,218 closings. On the face of it, their recovery

seems nearly complete. But these gains hide the breadth of

Professional Builder has been compiling its list of Housing Giants for more than 40 changes underway at the nation’s biggest building firms. The

years. Firms that wish to submit their information for the list must complete a question-

naire. In addition, Professional Builder retains the services of researchers who contact

gains also obscure the diversity of approaches required by

large building firms that have not volunteered information in order to cast the widest most builders to succeed today. This Housing Giants report,

net for the biggest home building firms. The rankings are based on new-home revenue which includes the annual rankings and a heat-map poster of

only. Firms with fewer than 30 starts cannot be included in the rankings. To learn more

or to inquire about applying for next year’s list, please contact Professional Builder’s

the United States, as well as deeper discussions of financial

awards coordinator Heidi Riedl at hriedl@sgcmail.com or (847) 391-1000. and energy efficiency strides made by builders plus a profile

of a builder making a comeback, demonstrates that today’s

www.ProBuilder.com Professional Builder 29

housing giants market share

19% Giants 1 to 20

(14 4,225 CLOSINGS)

Giants 21 to 75

(58,228 CLOSINGS)

8%

Giants 76 to 150

(36,0 02 CLOSINGS)

5%

Giants 151 to 225

2% (15,763 CLOSINGS)

Non-Giants 1% Giants 226 to 293

total new residential revenue 65% (8,551 CLOSINGS)

(499,431 COmpLEtIONS) baSE: 293

$ b ILLIONS , CO mpaRES t Op 225 h O USING GIaN t S SOURCE: pROfESSIONaL bUILdER hOUSING GIaNtS REpORt 2014

$81.4

$75.4

317,361

$53.5

$48.9

$42.3 254,218

196,769 207,907

172,750

RE VENUE C LO S I N G S RE VENUE C LO S I N G S RE VENUE C LO S I N G S RE VENUE C LO S I N G S RE VENUE C LO S I N G S

2008 2010 2011 2012 2013

t hE hO U S I NG GI aNtS S UR V E y waS NOt CO NdUC tE d I N 2009 / baSE: 225 / SOU RCE: p ROfESSION aL bU IL d ER h OU SIN G G IaNt S REp OR t 2 0 1 4

housing market is grounded in new and sometimes unfamiliar job growth, and exhibited an entrepreneurial flair to make it

fundamentals. The new fundamentals have led big builders happen. This was true from the top of the list to the bottom.

to add new skills and new geographies and, in general, to be Once focused almost exclusively on starter homes, KB

more nimble and entrepreneurial. Home, No. 8 on this year’s list with $2.1 billion in revenue,

now builds 22 percent first move-up and 11 percent second

new fundamentals move-up. Likewise, Beazer Homes USA, No. 13 on the list

From the early 1990s until 2007, Housing Giants tended to with $1.27 billion in revenue, now builds only 50 percent

operate within clearly defined niches—single-family starter, starter homes, with the rest divided between first and sec-

single-family attached, first move-up, luxury, etc. That is no ond move-up and active adult. Ranked No. 39, DSLD, with

longer the case today. Due to myriad factors—the availabil- $300 million in revenue, is expanding its product offering

ity of finished lots to the relative buying strength of some to reach more move-up buyers. The fundamental reason is

demographic cohorts over others—big builders are working clear: The market for starter homes is weak. Millennials are

with what the market is giving them, even if it happens to simply not entering the market for new homes in the same

be very different from what they have done in the past. To numbers as their parents did.

achieve their gains in 2013, Housing Giants broadened their Consolidation continues to play a role as builders seek

product offerings, expanded into new markets with better new geographies and better markets. No. 15 builder David

30 Professional Builder May 2014

biggest challenges anticipated by giants in 2014 smaller houses, higher prices

36% Average

High material and labor costs Sq. Ft. for %

52%

Housing Type 2013 2012 Change

28%

Availability of land

N/A

Detached

27% Starter 1,781 1,763 1.02%

Scarcity of skilled labor

31%

14%

Government regulations Detached First

14% Move-Up 2,367 3,791 -37.56%

13%

Increased competition Detached

20%

Second

Move-Up 3,107 4,908 -36.70%

biggest opportunities anticipated by giants in 2014 Median Price

for Housing %

Type 2013 2012 Change

45%

Operational efficiencies

43%

Detached

32% Starter 185,000 175,000 5.71%

Economic recovery

59%

30%

Niche-market opportunities Detached First

41% Move-Up 270,000 250,000 8.00%

n 2014

28%

Market expansion n 2013 Detached

44%

Second

28% base: 293 Move-Up 388,975 375,000 3.73%

Move-up buyers source: professional

N/A builder housing

giants report 2014 b a se: 2 9 3 / sou rce: profession a l b u il de r hou s i n g g i a n t s r e p or t 2014

Weekley Homes in recent years expanded into Indianapolis communities. Shea Homes, ranked No. 16 with $1.1 billion

and Phoenix via acquisition. This is due, in part, to higher in revenue, opened 73 new communities. This proliferation

prices and higher demand for finished lots in A locations as of new communities translated directly to more new de-

builders stay away from riskier suburban edge communities. signs, more new model homes, and more new design cen-

The No. 5 builder, Toll Brothers, which billed $2.7 billion last ters. Cincinnati-based Drees Homes, No. 22 on the list with

year, acquired Shapell Homes for $1.6 billion last year. A driv- $568 million in revenue, said its “single biggest change” last

ing motivation for Toll in seeking that company was its 5,000- year was to build new models along with a new design cen-

plus entitled lots in coastal regions of California. Ranked No. ter. Many others did the same.

47 last year, TRI Pointe Homes acquired Weyerhaeuser Real This Housing Giants report offers a composite picture of

Estate, the No. 14 builder by revenue, at the very end of 2013 the largest builders—a landscape that is diversified, varied

in a deal valued at $2.7 billion (Weyerhaeuser Real Estate in- and, above all, growing. For 2014, Lennar is expecting 30

cludes Pardee Homes and Quadrant Homes, among others). percent growth; Toll Brothers, 42 percent; Weekley, 10 per-

Separately the company acquired 892 lots in California and cent; and Drees, 15 percent, just to name a few. Our sur-

Colorado via a flourish of fourth-quarter transactions. vey shows that many companies feel similarly optimistic.

In 2013, the name of the game also was to actively open A year from now, we expect to be reporting another good

new communities to meet pent-up demand. Toll opened 80 year for big builders. PB

www.ProBuilder.com Professional Builder 31

in pursuit of

By Mike Beirne, Editor

LGI

Homes would be ready to go public once it executed contracts, and the even-flow construction sched-

closed at least 2,000 houses a year, a bench- ule was managed to finish a house within 45 to 60 days from

mark that was probably a couple of years away, breaking ground.

or so Eric Lipar thought. But when Tri Pointe Homes, an Irvine, On the sales front, LGI blanketed Houston and San Antonio

Calif., builder with 144 closings in 2012, raised $156.3 million apartment complexes near its subdivisions every five weeks

in net proceeds from its IPO in January 2013, Lipar knew the with direct mail pieces announcing that it could turn renters

time was right to take his Houston-based company public. into homeowners through no frills, no down-payment mort-

“It really was a signal that the market was open to smaller gages—typically mortgages backed by the Federal Housing

companies because Tri Pointe was essentially a startup,” says Administration or the U.S. Agricultural Department’s rural

LGI’s chairman and chief executive officer. “Even though (Tri housing program—that cost less than or were on par with the

Pointe) had a very nice balance sheet with really good equi- target market’s current monthly rent. Those mailers gener-

ty, they were just starting to get closings into the company. ated as many as 100 leads a week.

When we saw that, we wanted to get out there before that “We have a very disciplined and systematic approach to our

window closed.” sales process, our direct mail, and with our construction staff.

Before LGI completed its $90-million offering last November, When you look at our growth strategy, we have the system,

Lipar and his team made several stops at various providers of we have the process, and all we’re doing is duplicating it and

capital along a journey that started when the company closed opening stores across the country similar to a franchise con-

its first house in 2003. That trek, in a sense, encapsulates the cept,” Lipar says.

varied sources of money that home builders are tapping—pri- The builder had designs in 2006 to grow to 1,000 closings

vate equity, public debt, and the common stock market—ever by 2012. Then the downturn hit. Banks stopped lending, and

since banks pulled back on credit after the start of the hous- LGI’s primary source of construction loans announced it was

ing market collapse in 2007. getting out of the Texas market. Without more capital, the

“Financing has changed in the sense that there is a more company’s growth plans were in jeopardy.

diverse range of sources available and needed,” says Dave So LGI’s management team sought friends and family fi-

Ledford, senior vice president of housing finance and regula- nancing. Lipar set up a private placement memorandum

tory affairs for the National Association of Home Builders. “I and raised $2.1 million from employees, trade contractors,

think that this will be more than just a temporary sign be- and friends—17 individual investors in all, kicking in at least

cause community banks are not going to be able to have 80 $100,000 each. They were told that in three-to-five years the

percent of their portfolios in construction and development return on their investment would be about 20 percent. With

loans going forward. The regulators made that very clear.” that capital, LGI entered the Dallas/Fort Worth market by

acquiring 210 foreclosed lots in the Deer Creek community

the go-go years and was building houses there by 2009. Still, LGI needed more

The stretch between 2003 and 2006 was a good one for LGI capital to reach its next growth phase, particularly since land

as it was for builders in general. Closings for the company was priced at a bargain thanks to the Great Recession.

steadily increased to 418, and bank credit lines were readily “In 2009 and going forward, that’s when we saw opportu-

available. LGI had aspirations to be a multiregional builder. nities to buy distressed finished lots with lower replacement

On the construction side, its business model focused on build- cost, and that’s when we got really excited about going down

ing entry-level homes with a yard, priced as low as $115,000. the road to raise private equity and raising friends and family

A steady inventory of move-in ready product was created capital to do whatever we needed to do to take advantage of

by setting building activity against projected closings, not those opportunities,” Lipar says.

32 Professional Builder May 2014

capital

IPO, bond, and private

equity money flocked to the

Housing Giants. Is there a

finance gap for everyone else?

In March 2010, the builder picked up a $50-million infu-

sion from Golden Tree Insite Partners, a New York-based real

estate investment firm now called GTIS Partners. With that

cash, LGI purchased 175 lots in the Chisholm Spring subdi-

vision in Fort Worth, and 393 lots across the street from its

Canyon Crossing community in San Antonio. The following

year, LGI planted a stake in Phoenix, buying 103 lots in San

Tan Heights, and then Austin, Texas, by purchasing 102 lots

in the Sonterra development. In 2012, LGI launched in Tampa,

and last year in Atlanta, Orlando, Albuquerque, and Tucson.

expansion barriers

The builder closed over 1,000 homes going into last year,

but pushing even higher created hurdles with private equity.

LGI needed even more upfront capital to develop land and

break into growth markets—an exercise that required more

time than the period private equity investors typically allot

before collecting their 20-plus-percent return on investment.

Banks were not an option, and LGI seemed to be another 1,000

closings and years away from being IPO ready. But after Tri

Pointe became the first home builder to go public since 2004,

LGI quickly followed suit.

“We went as fast as we could to prepare for it,” Lipar says.

“This was not an exit strategy. This was an event to help us

further grow in the future, so the multiple we went out at, and

the price to earnings ratio we went out at wasn’t important

to us. The important thing was getting out and getting the

capital raised so we could grow the company in the future.”

the public road

A total of six builders—Taylor Morrison, WCI Communities,

UCP, and William Lyon also completed IPOs—went public last

PHOTO: BEN SKLAR / DBPHOTOAGENCY

year. The New Home Company, Aliso Viejo, Calif., finished its

$86-million offering in January and Newport Beach, Calif.-

based City Ventures is scheduled to debut on the public mar-

ket this year. When it does, the industry will have 24 publicly

traded companies that predominantly build detached single-

family homes, the most since 2005. Eric Lipar, chairman and CEO

And why not? Wall Street had an appetite for new invest- LGI Homes, Houston

ment opportunities after sitting on the cash sidelines during

www.ProBuilder.com Professional Builder 33

the slow economic recovery. Last year, capital raised by IPOs in 6.75-percent senior unsecured

from U.S. issuers jumped 40.5 percent to $57.1 billion (201 notes due in 2021. He says that

deals) compared with $40.6 billion (126 deals) in 2012, accord- a downside with being public is

ing to Thompson Reuters. Top builders that were able to hold the headline noise that can affect

onto or get access to land and upscale move-up and move- share price regardless of the com-

down buyers rebounded early last year. When those builders pany’s performance.

sought to sell common stock in order to raise capital and buy “I was talking to one of the pub-

Doug Bauer

land, investors were eager to get in on the action. lic builder CEOs, and he said ‘I’m

Doug Bauer, Tri Pointe’s chief executive officer, jokes that growing by 10, 20, 30 percent, and

perhaps he should collect a “finders fee” or some sort of re- my stock gets dinged because the analysts think that it should

bate as a result of other builders going public after his com- be growing by 40 percent,’” Shine says. “‘They don’t understand

pany’s IPO. He admits that he would have doubted back in that growing that fast has a downside, but because they decid-

August 2012 whether there was an IPO market for his compa- ed that is how fast I should grow, they’re going to ding me for

ny. But $150-million financing from Starwood Capital, a clean it.’ There are some extremely savvy, smart analysts out there,

balance sheet, and quality management eventually added up the Ivy Zelmans of the world and a small handful of others.

to a compelling lure for investors. One negative since going Then there also are some guys out there who call me, they say

public is the company incurs more accounting and legal ex- stuff, and I scratch my head, and I just go, ‘Really?’”

penses related to compliance with the Sarbanes-Oxley Act—a

cost of equity that the builder didn’t have when it was private. public debt

But Bauer calls that more of a change than a negative. Builders were among the many private and public U.S. com-

“Frankly, I’d be a public company in any industry, especially panies that also took advantage of relatively cheap money by

home building,” Bauer says. “It imparts a certain amount of disci- issuing public debt in 2012 and 2013. Issues in the U.S. invest-

pline that I think makes a company a better operator and a bet- ment grade market reached $1.02 trillion last year, topping

ter steward of its capital so you can survive the ups and downs.” the previous all-time high of $1.01 trillion set during the pre-

After its January IPO, The New Home Company moved on vious year, per Thomson Reuters. That push was partially the

the $74-million purchase of Arantine Hills, a proposed mas- result of companies trying to beat rising interest rates during

ter plan development in Corona, Calif. The site is surrounded the second half of last year after the Federal Reserve Board

by established communities, already sits within a school dis- signaled that it was considering reducing its monthly bond

trict, and will have somewhere between 1,300 to 1,600 new- purchases, which had kept rates stable.

home sites. That deal would not have been possible without Well before that rush, David Weekley Homes, Houston, in

the builder raising money through its January IPO, says Larry February 2013 issued $200 million of senior unsecured debt due

Webb, chairman and chief executive officer. in 2023 at 6-percent interest, one of the more favorable terms

“I’ve been doing this for 30 years and during most of my ca- for a private builder. The money was raised through a 144A-for-

reer, during the good times and good market conditions, the life bond offering, which carries reporting requirements, but

capital was very plentiful for both the private and public build- the privately held builder only discloses its numbers to inves-

ers,” Webb says. “But coming out of this recession, private build- tors who are qualified to buy the bonds. That avenue was an

ers have a much more difficult time having access to capital.” attractive alternative to other forms of issuing debt or raising

money in the public market, particularly if shareholders and

the private side Wall Street analysts pushed for dividend payouts or buybacks

Perhaps the debate about the ad- at the expense of such Weekley practices as profit sharing with

vantages of public versus private is employees and donating 20 percent of pretax earnings to char-

not as salient as discussing wheth- ity. The builder used the bond money to pay down bank lines.

er a builder is large enough and “The cost of public debt was 1-to-1.5-percent higher (than

well-capitalized enough, which bank line rates available at that time), but what you’re paying

can be the case whether the com- for is the interest risk rate,” says Heather Humphrey, Weekley

pany sells stock or is privately held, Homes’ chief financial officer. “Revolving rates are not staying

says Joel Shine, chief executive offi- put, we’re locking in at 6 percent for 10 years. All other borrowing

cer of Woodside Homes, Salt Lake is variable. That’s about the lowest fixed rate we’ve ever seen.”

City. Last September, the privately William Lyon Homes, Newport Beach, Calif., also took

Joel Shine

held builder raised $220 million advantage of lower interest rates in 2012 by refinancing a

34 Professional Builder May 2014

Change from 2012

% Custom Homes

Adult/Retirement

% 2nd Move-Up

% 1st Move-Up

Custom Homes

2014 Forecast

2013 Closings

Previous Rank

Second Home

Year Founded

2013 Housing

% Production

and Beyond

% Vacation/

Total Other

% Revenue

2013 Rank

% Starter

Company

% Active

Revenue

Revenue

% Semi-

Homes

Types

D.R. HoRton Inc. — Fort Worth, TX SFD,

1 1 1978 $6,432,314,000 25,161 41.1% $222,534,000

Donald R. Horton / www.drhorton.com SFA

PulteGRouP Inc. — Bloomfield Hills, MI SFD,

2 2 1950 $5,424,309,000 17,766 19.2% $259,681,000 25 46 29 100

Richard J. Dugas Jr. / www.pultegroupinc.com SFA

lennaR coRP. — Miami, FL SFD,

3 3 1954 $5,292,072,000 18,290 51.5% $643,023,000 36 59 5 30%

Stuart Miller / www.lennar.com SFA

nVR Inc. — Reston, VA

4 4 1948 $4,134,481,000 11,834 32.5% $0 SFD

Paul Saville / www.nvrinc.com

toll BRotHeRs — Horsham, PA SFD,

5 5 1967 $2,711,838,000 4,235 44.0% $52,238,000 5 60 20 10 5 100 42%

Douglas Yearley / www.tollbrothers.com SFA

tayloR MoRRIson — Scottsdale, AZ

6 8 2007 $2,264,985,000 5,829 65.4% $30,371,000 SFD 23 31 31 15

Sheryl Palmer / www.taylormorrison.com

HoVnanIan enteRPRIses Inc. — Red Bank, NJ SFD,

7 6 1959 $2,089,729,000 5,927 21.1% $66,926,000 31 32 24 13

Ara K. Hovnanian / www.khov.com SFA

KB HoMe — Los Angeles, CA

8 7 1957 $2,084,978,000 7,145 34.7% $12,152,000 SFD 56 22 11 11 100

Jeffrey T. Mezger / www.kbhome.com

tHe RylanD GRouP — Westlake Village, CA SFD,

9 9 1967 $2,082,838,000 7,027 64.9% $57,917,000 23 42 34 1 100

Larry Nicholson / www.ryland.com SFA

stanDaRD PacIfIc HoMes — Irvine, CA SFD,

10 10 1965 $1,911,756,000 4,627 58.4% $40,530,000 26 47 26 1 100

Scott D. Stowell / www.standardpacifichomes.com SFA

MeRItaGe HoMes coRP. — Scottsdale, AZ

11 11 1985 $1,783,389,000 5,259 50.1% $31,270,000 SFD 24 49 24 3 100 -5%

Steven J. Hilton / www.meritagehomes.com

M.D.c. HolDInGs Inc. — Denver, CO SFD,

12 12 1972 $1,626,700,000 4,710 41.3% $80,665,000 47 53

Larry A. Mizel / www.richmondamerican.com SFA

BeazeR HoMes usa — Atlanta, GA

13 13 1994 $1,279,212,000 5,056 28.4% $8,365,000 SFD 50

Allan Merrill / www.beazer.com

WooD PaRtneRs — Atlanta, GA

14 41 1998 $1,249,800,000 4,275 447.9% $0 R

Ryan Dearborn / www.woodpartners.com

WeyeRHaeuseR Real estate co. — Federal Way, WA SFD,

15 14 1971 $1,218,430,000 2,939 40.0% $57,282,000

Peter Orser / www.weyerhaeuser.com/business/WRECO SFA

DaVID WeeKley HoMes — Houston, TX SFD,

16 15 1976 $1,124,000,000 2,899 30.5% $0 4 87 9 100 10%

David Weekley / www.davidweekleyhomes.com SFA

sHea HoMes — Walnut, CA SFD,

17 16 1968 $1,092,703,000 2,440 43.3% $51,926,000 31 11 20 38

Bert Selva / www.sheahomes.com SFA

M/I HoMes Inc. — Columbus, OH SFD,

18 17 1976 $993,000,000 3,472 33.1% $44,000,000 40 30 18 10 2 90 10

Robert H. Schottenstein / www.mihomes.com SFA

tHe VIllaGes of laKe suMteR — The Villages, FL

19 18 1959 $961,011,584 3,419 33.2% $0 SFD 100 100 0%

H. Gary Morse / www.thevillages.com

HIGHlanD HoMes llc — Plano, TX

20 20 1985 $760,600,000 1,915 21.5% $0 SFD 16 80 4 95 5

Rodger Sanders / www.highlandhomes.com

asHton WooDs usa llc — Roswell, GA SFD,

21 21 1989 $728,691,000 2,241 36.6% $5,427,000 28 39 33 100

Kenneth Balogh / www.ashtonwoods.com SFA

DRees HoMes — Ft. Mitchell, KY SFD,

22 22 1928 $568,009,000 1,512 8.8% $16,100,000 15 85 10 75 15 15%

David Drees / www.dreeshomes.com SFA

WIllIaM lyon HoMes — Newport Beach, CA SFD,

23 27 1956 $566,221,000 1,435 68.1% $18,692,000 40 32 28 100

William H. Lyon / www.lyonhomes.com SFA

PeRRy HoMes llc — Houston, TX

24 23 1967 $545,170,000 1,693 20.2% $8,200,000 SFD 25 50 25 100 9%

Kathy P. Britton / www.perryhomes.com

BRooKfIelD ResIDentIal PRoPeRtIes — Calgary,

25 NR 1956 $511,000,000 855 NA $74,000,000 SFD

Alberta, Canada; Alan Norris / www.brookfieldrp.com

claRK BuIlDeRs GRouP llc — Arlington, VA

26 28 2003 $505,785,040 1,598 51.3% $606,893 R

Keith Anderson / www.clarkbuildersgroup.com

MHI (McGuyeR HoMeBuIlDeRs Inc.) — Houston, TX SFD,

27 25 1988 $494,600,000 1,574 21.3% $7,400,000 10 25 65 20 80 5%

Frank B. McGuyer / www.mcguyerhomebuilders.com SFA

Gl HoMes of floRIDa — Sunrise, FL SFD,

28 29 1975 $491,335,000 1,020 55.0% $0 9 36 18 37 100

Itchko Ezratti / www.glhomes.com SFA

sIMPson HousInG llP — Denver, CO

29 NR 1948 $440,006,900 1,357 NA $0 R

J. Robert Love / www.simpsonhousing.com

WooDsIDe HoMes — North Salt Lake, UT SFD,

30 30 1977 $438,103,000 1,507 40.0% $3,076,591 14 42 44

Joel Shine / www.woodsidehomes.com SFA

N R = N OT RA N KE D

50 Professional Builder May 2014

Change from 2012

% Custom Homes

Adult/Retirement

% 2nd Move-Up

% 1st Move-Up

Custom Homes

2014 Forecast

2013 Closings

Previous Rank

Second Home

Year Founded

2013 Housing

% Production

and Beyond

% Vacation/

Total Other

% Revenue

2013 Rank

% Starter

Company

% Active

Revenue

Revenue

% Semi-

Homes

Types

Wermers Companies — San Diego, CA

31 NR 1957 $404,000,000 1,911 NA $0 R

Jeff Bunker / www.wermerscompanies.com

First texas Homes inC. — Dallas, TX

32 34 1986 $377,053,638 1,245 28.5% $2,250,463 SFD 60 40 80 20 2%

Keith Hardesty / www.firsttexashomes.com

polygon nortHWest Co. — Bellevue, WA SFD,

33 32 1991 $376,615,995 1,287 26.1% $4,000,500 45 45 10 100

Jeffery Gow / www.polygonhomes.com SFA, R

CroWn Communities inC. — Conyers, GA

34 36 1999 $375,205,186 1,540 34.1% $0 SFD 50 50 100

Francis J. Downey / www.crownus.com

Habitat For Humanity international — Atlanta, GA

35 26 1976 $364,000,000 3,367 -7.8% $0 SFD 100

Jonathan Reckford / www.habitat.org

stanley martin Homes — Reston, VA SFD,

36 42 1966 $323,831,770 588 42.5% $27,549,270 30 30 40 92 5 3 13%

Steven Alloy / www.stanleymartin.com SFA

mattamy Homes - us group — Winter Park, FL SFD,

37 45 1978 $320,464,000 1,224 56.1% $0 10 35 55 100 20%

Steve Parker / www.mattamyhomes.com SFA

a. g. spanos Companies — Stockton, CA

38 19 1960 $317,000,000 2,329 -53.3% $23,114,000 R

Dean A. Spanos / www.agspanos.com

DslD llC — Denham Springs, LA

39 46 2008 $299,679,299 1,597 51.3% $0 SFD 50 50 100 0%

Saun Sullivan / www.dsldhomes.com

FisCHer Homes — Erlanger, KY SFD,

40 43 1981 $296,780,000 1,008 35.8% $0 20 20 60 70 30

Henry Fischer / www.fischerhomes.com SFA

epCon Communities FranCHising inC. — Dublin, OH

41 40 1995 $290,715,049 1,072 23.3% $0 SFA 98 2 100 10%

Philip Fankhauser, Edward Bacome / www.epconcommunities.com

geHan Homes — Addison, TX

42 37 1994 $289,925,095 1,089 17.9% $0 SFD 50 50 100

Timothy Gehan / www.gehanhomes.com

sares-regis group — Irvine, CA SFD,

43 179 1993 $286,894,000 694 744.4% $198,474,000 100 100 0%

Geoffrey Stack / www.sares-regis.com SFA, R

tHe neW Home Co. — Aliso Viejo, CA SFD,

44 NR 2009 $266,266,753 424 145.4% $0

H. Lawrence Webb / www.nwhm.com SFA

stoCk Development — Naples, FL SFD,

45 NR 2001 $261,000,000 434 NA $175,869,080 100 35 65 20%

Brian K. Stock / www.stockdevelopment.com SFA

Century Communities inC. — Greenwood Village, CO SFD,

46 63 2002 $254,820,070 752 91.6% $784,750 20 35 40 5 100 100%

Robert Francescon / www.centurycommunities.com SFA, R

tri pointe Homes inC. — Irvine, CA

47 108 2009 $247,091,000 396 218.9% $10,864,000 SFD 25 50 25 100

Doug Bauer / www.tripointehomes.com

tHe bozzuto group — Greenbelt, MD SFD,

48 24 1988 $243,054,122 1,116 -46.0% $1,132,532,558 25 30 45 100

Thomas S. Bozzuto / www.bozzuto.com SFA, R

lgi Homes inC. — The Woodlands, TX

49 57 2003 $241,000,000 1,617 61.2% $0 SFD 95 5 100

Eric Lipar / www.lgihomes.com

ivory Homes ltD. — Murray, UT SFD,

50 49 1986 $240,810,000 714 41.1% $0 17 50 21 7 5 58 42 7%

Clark D. Ivory / www.ivoryhomes.com SFA

legenD ClassiC Homes ltD. — Houston, TX SFD,

51 66 1989 $239,294,597 1,357 83.1% $0 45 30 25 80 18 2 10%

Scott Bauer / www.legendhomeshouston.com SFA

neal Communities oF soutHWest FloriDa llC — SFD,

52 61 1970 $228,873,156 769 68.0% $7,754,636 16 73 11 89 11 30%

Sarasota, FL; Patrick K. Neal / www.nealcommunities.com SFA

mungo Homes inC. — Irmo, SC SFD,

53 52 1954 $227,977,000 1,082 37.6% $7,320,000 62 30 8 100 22%

Steven W. Mungo / www.mungo.com SFA, R

Dan ryan builDers — Frederick, MD SFD,

54 79 1990 $226,518,352 1,010 118.8% $1,612,419 50 40 10 100 22%

Dan Ryan / www.danryanbuilders.com SFA

albert D. seeno ConstruCtion Co. / DisCovery

55 35 1938 $225,017,000 491 -21.0% $145,340,452 SFD 20 58 22 94 6 3%

builDers — Concord, CA; Albert Seeno / www.seenohomes.com

tHe Community builDers inC. — Boston, MA

56 134 1964 $224,094,536 459 291.3% $0 R

Bart Mitchell / www.tcbinc.org

Fulton Homes Corp. — Tempe, AZ

57 55 1975 $223,766,400 696 45.8% $3,630,100 SFD 15 25 40 20 15 85 85%

Douglas S. Fulton / www.fultonhomes.com

van metre Companies — Fairfax, VA SFD,

58 53 1955 $221,020,000 476 40.3% $96,196,000 61 34 5 100 11%

Albert G. Van Metre Jr. / www.vanmetrecompanies.com SFA

ameriCan West Development inC. — Las Vegas, NV

59 106 1984 $220,888,128 730 180.1% $43,000,000 SFD 25 75 100

Lawrence D. Canarelli / www.americanwesthomes.com

JoHn WielanD Homes — Smyrna, GA SFD,

60 44 1970 $217,247,341 467 2.5% $2,696,500 6 60 31 3 80 19 1 31%

Greg Huff / www.jwhomes.com SFA

www.ProBuilder.com Professional Builder 51$235-million and 10.25-percent interest term loan due next the financing gap

year with a $325-million issue of senior notes with 8.5-per- Banks will still be the dominant

cent interest. Lyon raised another $150 million to buy 540 provider of credit but, like equity

infill lots in Orange, Los Angeles, and Santa Clara counties in investors, they will be very selec-

California with a 5.75-percent senior note issue completed tive and favor large companies

in March. Other builders that have dipped into the high- with stellar balance sheets.

yield market for capital recently include D.R. Horton, Fort Small- and medium-sized build-

Heather Humphrey

Worth, Texas; Beazer, Atlanta; Hovnanian, Red Bank, N.J.; ers are at a competitive disadvan-

Lennar, Miami, and Ashton Woods, Roswell, Ga. tage because even if the housing

But raising capital through bonds, obviously, is not available market returns to normal activity, there will be a gap that has

for smaller builders. Humphrey, Bauer, and Lipar agree that a to be filled with alternative capital sources since banks will

$200-million issue is the minimum buy-in for issuing public not be able to carry the load they carried before the crash.

debt. Anything less makes the bond too expensive for the issuer. “We’d like to see our smaller builder members have ac-

cess to credit and not be at a competitive disadvantage, but

private equity partner presently it’s hard to argue that they are not,” says Ledford

Some builders raised capital through partnerships with eq- of the NAHB. “That is why we are trying to level the field in

uity investors willing to take an ownership stake or set up a that regard.”

joint venture. Mountain Real Estate Capital LLC, with offices Details are in the works, but Ledford says that such a pro-

in Minneapolis, Charlotte, and San Diego, has committed $800 gram could launch this year. Unlike previous hodgepodge ef-

million through about 60 deals in the past four years. Many forts that tried to match builders with financing preferences

of the partners are builders that some Mountain employees until the program ran its course, the NAHB is developing a

worked with since their days with GMAC’s construction lend- plan to continuously provide capital on a regular basis.

ing group. Mountain’s investments range from $5 million to “(It’s) sort of like how the commercial paper market works

$75 million with the average deal size being about $12 mil- for you. You’re able to keep the money flowing from investors,

lion. Some deals are short two-to-three-year partnerships; and there’s an intermediary working for you servicing the

others are six-to-eight-year stretches, and some of its builder loans so the investors don’t have to be concerned about that,

partners have visions of going public in two-to-five years. and there’s confidence in the process,” Ledford says. “That’s

“We’ve found that if a builder is at 150 homes or more (a the key: to get confidence in the process so the investors don’t

year), we are a pretty good partner for them,” says Joel Kaul, have to look through every little detail in how the money is

Mountain’s managing director. “If they’re under 150 homes, applied and repaid. As long as that happens, they should be

it’s hard for us as institutional investors to figure out how satisfied and do it at a cost that is workable for the builders.”

we’re going to help them grow their business.” Credit watchers such as Experian Information Solutions,

He explains that a smaller builder with $5 million in capital Fitch, and the Federal Reserve note that banks are loosen-

doesn’t need an equity investor because he can just “recycle that ing lending standards and underwriting more mortgages and

capital through his home building company.” But a builder with business loans. Although banks will remain the main provid-

150 to 200 closings has outgrown his friends and family financ- er of capital, there is a financing gap that will have to be filled

ing. If that builder wants to double his production, his company by an alternative money source—or not. Nevertheless, the

probably needs another $5 million to $15 million to do so. industry will have to reckon with the notion that the Great

“We’re a really good resource Recession has fundamentally changed how builders acquire

for the builder to partner with. We financing.

move a lot of their new projects “For most of my career when looking at the home building

into a joint venture, and then we industry, I have felt that about 50 percent of new homes went

finance the land acquisitions, de- to private builders and the other 50 percent went to the pub-

velopment, and home building in lic builders,” says Webb of The New Home Company. “Moving

our partnership. We are more ex- forward I really believe that five years from now, you’re go-

pensive than debt, but it is a great ing to see that 75 percent of houses sold in America are from

structure for a conservative build- public builders. There will always be well-run private compa-

er who wants to grow, but doesn’t nies; but public builders, because of their access to equity, will

want to sign up for a bunch of have an incredible competitive advantage, and I don’t see that

Larry Webb

debt right now,” Kaul says. changing in the short term.” PB

36 Professional Builder May 2014executivecorner

Going from private to public, Larry Webb

talks about being a builder after the IPO

the best of being private and public. I’m still in charge, and I

H. Lawrence Webb

still have a major investment in my own company, but I have

Chairman and CEO

access to much cheaper capital and much more capital than

The New Home Company

I ever would have in the private sector.

Aliso Viejo, Calif.

Q Have any notions you had about being public changed?

A I knew the reporting was a lot more complicated and oner-

ous than what a private builder goes through. I probably

didn’t recognize how much time you have to spend on that.

That’s one, but it’s something we can deal with. On the other

side, prior to this I had three other customer groups besides

W henever Larry Webb participated in a home builder confer-

ence panel discussion about private versus public, he would

expound on the virtues of being privately held. After leaving

my partners, so those were the four ownership groups that I

reported to. Now we’ve sold more than 8 million shares of stock,

so more of my time is spent communicating with all different

John Laing Homes in 2008, Larry and three other former John kinds of investors, and I have to be more aware of everything

Laing executives started a new company during the depths of the I do. You know, I have to be quiet. I’m not allowed to speak to

housing crash in 2009. The New Home Company eventually at- people. I used to be able to say whatever I wanted whenever I

tracted capital from private equity investment firms and grew to felt like it. In today’s world, I probably wasn’t as cognizant or

build in 22 communities on its own and in joint ventures. Then the aware of the restrictions and the reasons for the restrictions,

builder completed an IPO in January 2014 and raised $86 million. and I’m learning that. I’m learning that if I predict something in

the future, and someone buys my stock because of me getting

Q Why did you go public?

on a panel somewhere, and it doesn’t happen, I could be liable

for that. So I’m a lot more aware and a lot less flip than I used to

A We just came to the conclusion within the last 18 months

that we had a lot of opportunities to continue to grow

be. I’m still flip, but not as much as I used to be.

the business. We have this great team of people, and what

we were constrained by was access to capital and access to Q What are your expansion plans?

well-priced capital, and that is what going public does for you.

It allows you to expand and grow your business, and you’re

only limited by the opportunities you can come up with. If

A When I look at our company and people, it seems to me

that our competitive advantage is in markets where land

is constrained, and where you get rewarded for thoughtful ar-

we were going to stay a relatively small company with two or chitecture and planning. Along with that is building in mar-

three housing programs in each area, then I would’ve stayed kets with job growth. That works very much for the Bay Area,

private. But we own or control over 6,000 lots now. In Califor- Southern California, and Sacramento. When I look beyond

nia that represents a significant amount of capital, and we that, to Phoenix, I don’t mean outside of Phoenix. I mean the

really could not take advantage of those lots unless we really inner loop of Phoenix, the Scottsdale area, and Paradise Val-

got a big influx of money, and there were only two ways to do ley. Along with that Seattle, Portland, and maybe Denver. So

that. One was to go public; the second was to attract a large it is clear that those are areas I am interested in. But with

private investor. I’m still an investor in this company, and I the proceeds from the IPO, maybe all the money we raised

didn’t want to be diluted. I also didn’t want a boss or a big will go to already identified projects in California. We are still

investment group that would basically tell me how to run the considering these other options. It may be 12 months away, it

company. By being public, I’m the chairman of the board. I may be sooner. We’re really not sure yet. But the majority of

have an independent board, and they understand what we do the money that we are focusing on raising was for California

and are very supportive. In a sense, this move kind of gave me projects that we already identified. PB

92 Professional Builder May 2014You can also read