A MULTI-SPEED HOUSING MARKET

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

A MULTI-SPEED

HOUSING MARKET

Niels Arne Dam, Tina Saaby Hvolbøl and Morten

Hedegaard Rasmussen, Economics

INTRODUCTION AND SUMMARY being accompanied by a faster pace of income

growth, the higher level of house prices could be

At the national level, Danish house prices are in- temporary, resulting in substantial capital losses

creasing, but the housing market as a whole is still for households and higher loan-to-value, LTV, rati-

struggling with low turnover, a substantial hou- os. This places demands on homeowners’ financial

sing supply and a long time on the market. Howe- robustness. Against this backdrop, it is important

ver, there are considerable regional differences. for homeowners to build up home equity over

Large Danish towns and cities, especially time, thus moving away from the maximum LTV

Copenhagen, are experiencing a surge in house ratio.

prices, reasonable turnover and limited supply. In A reduction of the maximum LTV ratio for defer-

recent years, population numbers in large Danish red amortisation loans could increase the financial

towns and cities have been growing faster than robustness of homeowners, while at the same

the housing supply, indicating pressure on the time preserving the security of mortgage bonds.

housing market. This will ensure that the system is robust – even in

At the same time, prices in most of Denmark periods of falling house prices. Calculations in this

are unchanged or slightly higher, implying that article show that reducing the maximum LTV ratio

the market is sluggish with slow trading activity for deferred amortisation loans from 80 to, say,

and many homes on the market. In some areas, 60 per cent would cause house prices to increase

house prices are falling, and sales are few and far less than would otherwise be the case.

between. These areas also have an overrepresen- Housing market stability is also challenged by

tation of enforced sales. Moreover, population economic policy framework conditions for the

numbers are declining, and there are no immedi- housing market, which are, in some respects, pre-

ate indications that this will change. If the balance venting the free formation of prices and leading

between supply and demand is to be restored, to randomness and inefficiency in the housing

permanent changes in the housing supply are market. The freeze on property value tax means

required. This will take many years to accomplish. that this tax is the cause of greater housing price

The housing market is of great significance fluctuations. Restoring the link between property

to both financial and macroeconomic stability. value tax and house prices would help to stabilise

Looking forward, a more stable housing market prices, and thus the business cycle, for the benefit

would contribute to smoother economic develop- of financial stability. Rent regulation in the rental

ment. housing market is also likely to amplify cyclical

House prices are highly dependent on interest fluctuations in owner-occupied house prices. That

rates, and if interest rates remain low, this may being the case, deregulation could contribute to

provide a boost to prices – at least in certain are- smoother price developments for owner-occupied

as. If interest rates subsequently increase without housing.

DANMARKS NATIONALBANK MONETARY REVIEW, 3RD QUARTER, 2014 43

Simulations in the article show that changes in ner-occupied flats were about 20 per cent lower

capital gains taxation through a reduction of the than their peaks, but in line with prices in early

tax value of interest-rate deductibility would have 2005, cf. Chart 1 (right).

a relatively modest effect on house prices, espe- The reason why prices of owner-occupied flats

cially in the current very low interest-rate environ- rise faster than house prices is that most ow-

ment, as such changes would have only a modest ner-occupied flats are located in large towns and

effect on household interest payments after tax. cities, which are seeing the strongest growth. In

A lower value of interest-rate deductibility could individual parts of Denmark, price increases of

lead to improved household capitalisation for the houses and owner-occupied flats are somewhat

benefit of financial stability. more homogeneous than at the national level.

Owner-occupied flats account for only about

11.5 per cent of all owner-occupied homes for

DEVELOPMENTS IN THE DANISH year-round occupation, cf. Table 1, and are of

HOUSING MARKET limited significance to the overall Danish housing

market. Below, the primary focus is therefore

Danish house prices have been on the rise since on houses. However, in some parts of Denmark,

the spring of 2012, cf. Chart 1 (left). In June 2014, owner-occupied flats are quite significant. Just

nominal prices of houses and owner-occupied under 45 per cent of all owner-occupied homes in

flats were up by 1.6 and 10.4 per cent year-on- Copenhagen and environs1 are owner-occupied

year. These increases follow a sharp price corre- flats, accounting for close to two-thirds of the

ction after the housing bubble of the mid-2000s, total value of owner-occupied flats in Denmark in

with prices peaking in 2006-07. In June 2014, 2011.

nominal prices of houses and owner-occupied In Denmark, about half of all owner-occupied

floats were 14 and 8 per cent, respectively, below homes for year-round occupation are houses

their peak levels. In real terms, house prices were owned by private individuals. But developments

approximately 25 per cent lower and prices of ow- in this market also depend on other types of

House prices in Denmark Chart 1

Nominal Real

Index, 2000 = 100 Index, 2000 = 100

225 225

200 200

175 175

150 150

125 125

100 100

75 75

00 01 02 03 04 05 06 07 08 09 10 11 12 13 14 00 01 02 03 04 05 06 07 08 09 10 11 12 13 14

Houses Owner-occupied flats Houses Owner-occupied flats

Note: The 2nd quarter of 2014 is a simple average of monthly observations. In the right-hand chart, nominal prices are deflated by the defla-

tor for private consumption.

Source: Statistics Denmark and own seasonal adjustment.

1 Copenhagen City comprises the Cities of Copenhagen and Frederiks-

berg and the municipalities of Tårnby and Dragør, while Copenhagen

environs comprise the municipalities of Albertslund, Ballerup, Brønd-

by, Gentofte, Gladsaxe, Glostrup, Herlev, Hvidovre, Høje-Taastrup,

Ishøj, Lyngby-Taarbæk, Rødovre and Vallensbæk.

44 DANMARKS NATIONALBANK MONETARY REVIEW, 3RD QUARTER, 2014

Number of homes for year-round occupation and value of owner-occupied homes, Table 1

broken down by areas

Share of value for all of

Number in thousands

Denmark, per cent

Homes

owned by Owner- Owner-

private occupied Cooperative Rental flats, Homes, Single-family occupied

individuals flats housing etc. other homes flats

Copenhagen City 33 63 115 137 3 5.3 49.7

Copenhagen environs 84 26 16 93 21 13.8 13.5

Northern Zealand 112 14 7 39 18 14.8 8.1

Bornholm 16 0 1 2 2 0.6 0.0

Eastern Zealand 60 5 6 23 10 6.2 2.5

Western and southern

Zealand 177 8 12 60 26 9.9 2.8

Funen 138 7 8 57 28 8.2 2.3

Southern Jutland 200 9 12 88 37 10.3 3.4

Eastern Jutland 202 25 17 117 32 16.0 11.6

Western Jutland 132 5 5 44 17 6.7 2.0

Northern Jutland 174 11 10 68 26 8.2 4.0

Entire country 1,327 173 209 729 220 100.0 100.0

Note: The number is calculated as at 1 January 2014. Homes include detached single-family homes, farmhouses, terraced homes, linked

homes and semi-detached homes, and owner-occupied flats include owner-occupied flats in multi-storey buildings owned by private

individuals. In the article, owner-occupied flats and homes owned by private individuals are referred to as owner-occupied homes. The

category of ”Rental flats, etc.” includes rental flats given as multi-storey housing less owner-occupied flats, and student homes in halls of

residence and residential institutions not owned by a private cooperative housing association. ”Homes, other” include homes owned by

others than private individuals and private cooperative housing associations. Homes classified under the ownership category of ”Other

or undisclosed” are homes, multi-storey housing, halls of residence and residential institutions, a total of 80,123, which are not included

in the table. Values have been calculated based on the Danish Customs and Tax Administration’s property valuation from 2011 and

comply with the Administration’s property definitions. The total value for the entire country is kr. 2,559 billion for single-family homes

and kr. 273 billion for owner-occupied flats.

Source: Statistics Denmark and Danish Customs and Tax Administration.

housing and ownership, since they are, to some segments of the housing market with free price

extent, substitutes. Especially in towns and cities, formation, including the market for owner-occu-

rental and cooperative housing makes up a high pied housing. Hence, rent regulation presumably

percentage of the total housing stock. If housing contributes to reinforcing cyclical fluctuations in

demand increases, rental and cooperative hou- the prices of owner-occupied homes, cf. Ministry

sing will be able to absorb some of the demand of Economic and Business Affairs et al. (2003)

and the price impact on owner-occupied homes Only a limited segment of the rental housing

will be smaller. However, vacant housing must be market is subject to free price formation. Thus,

available for this to occur. Social housing is publi- seven out of eight privately rented homes in 2011

cly subsidised, entailing that practically all ten- were subject to rent regulation, cf. Danish Tenants

ants of social housing pay a lower rent than they Association (2011). Rents in the social housing

would pay for a similar owner-occupied home. sector are not determined by supply and demand

The same applies to most rental housing subject either. Moreover, cooperative housing is subject to

to rent regulation. Thus, this housing will not be maximum prices, capping the price at which they

vacant, and increased demand must be met by can be sold. If the maximum prices are binding,

DANMARKS NATIONALBANK MONETARY REVIEW, 3RD QUARTER, 2014 45

House prices and house sales for selected areas Chart 2

House prices House sales

Index, 2000 = 100 Index, 2000 = 100

225 170

200

175 120

150

125 70

100

75 20

00 01 02 03 04 05 06 07 08 09 10 11 12 13 14 00 01 02 03 04 05 06 07 08 09 10 11 12 13 14

Denmark Copenhagen environs Denmark Copenhagen environs

W and S Zealand Nothern Jutland W and S Zealand Nothern Jutland

Note: Seasonally adjusted series. Right-hand chart: number of registered sales on the free market.

Source: Statistics Denmark and own seasonal adjustment.

this is another segment of the housing market that sale, totalling about 300 days since early 2012.

is not subject to free price formation. These factors That is a long time, emphasising that most of the

seem to indicate a potential for more stable prices housing market is struggling. Regional differences

in the market for owner-occupied housing if the are also reflected here, since the time on the mar-

overall housing market were deregulated. ket was 345 days in western and southern Zealand

The housing market is exhibiting different pat- in July 2014, or more than twice as long as the

terns across the country. House prices are surging time on the market in Copenhagen environs, cf.

in large towns and cities, particularly Copenha- Chart 3 (left).

gen, while they are falling in other parts of the There is a marked tendency for the largest

country, cf. Chart 2 (left). In Copenhagen City, the price reductions to be given in areas with weak

annual rate of price increase in the 1st quarter housing markets, cf. Chart 3 (right). Large price

of 2014 was 12 per cent for owner-occupied flats reductions indicate that the seller and buyer ge-

and 9.3 per cent for houses, while house prices nerally do not agree on the price. This also makes

in western and southern Zealand declined by 0.7 the sale less feasible.

pct. In northern Jutland, house prices have remai- The seasonally adjusted number of enforced

ned largely unchanged since early 2009, albeit sales has stabilised at around 300 per month,

with a slightly decreasing trend. albeit with some variation from one month to the

The differences in the housing market are also next. The number of enforced sales has declined

reflected in trading activity, cf. Chart 2 (right). Sin- over the last two and a half years from just over

ce 2011, annual house sales have been totalling 450 per month. During the same period, mortga-

approximately 32,500 houses, equivalent to just ge arrears have fallen, dropping to approximately

two-thirds of the average since 1995. However, in 0.25 per cent in the last few quarters. The arrears

Copenhagen environs house sales are up, in 2013 rate indicates the proportion of total payments

almost reaching the average since 1995. In we- that had not been made 105 days after the due

stern and southern Zealand, sales in 2013 remai- date. The decline in the number of enforced sales

ned roughly unchanged from the previous couple has been distributed evenly across regions, alt-

of years, the level slightly over half of average hough there are still considerable regional diffe-

sales since 1995. rences, cf. Chart 4. Municipalities in western and

During the last few years, the supply of houses southern Zealand have a particularly high number

on the market has amounted to just over 40,000. of enforced sales relative to the number of ow-

High supply and low turnover have an impact on ner-occupied homes.

the average time on the market for a house for In summary, house prices are increasing at the

46 DANMARKS NATIONALBANK MONETARY REVIEW, 3RD QUARTER, 2014

Time on the market and price reductions on house sales, selected areas Chart 3

Time on the market Price reductions

Number of days Per cent

450 25

375

20

300

15

225

10

150

75 5

0 0

04 05 06 07 08 09 10 11 12 13 14 04 05 06 07 08 09 10 11 12 13 14

Denmark Copenhagen environs Denmark Copenhagen environs

W and S Zealand Nothern Jutland W and S Zealand Nothern Jutland

Note: Seasonally adjusted series. Right-hand chart: price reductions are given as the spread between the initial asking price and the sales

price relative to the initial asking price.

Source: Housing Market Statistics.

However, this masks substantial regional differen-

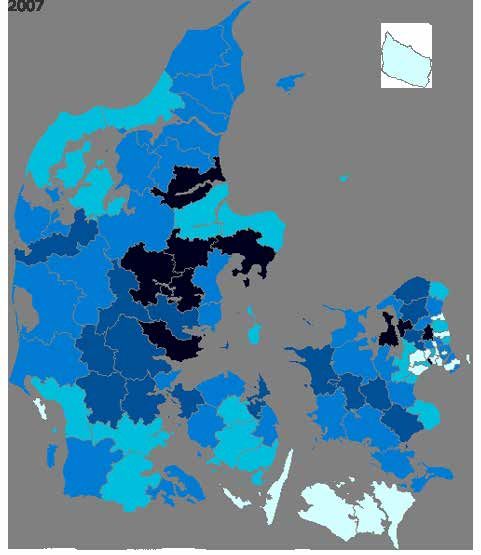

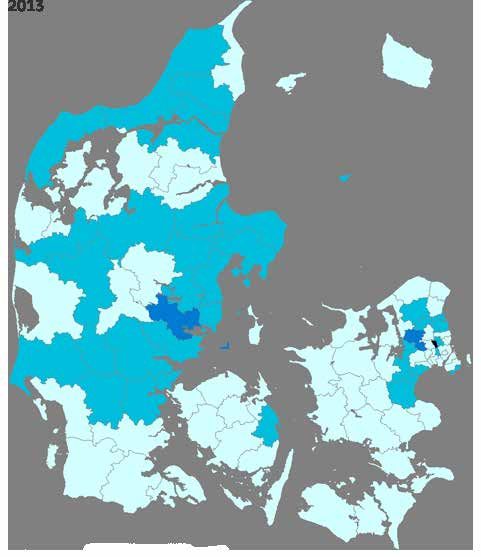

Enforced sales as a percentage of the Chart 4

ces; prices, turnover and supply, etc. are showing

stock of owner-occupied housing

different patterns with considerable variation in

levels.

The diverging trends also reflect the self-re-

inforcing mechanisms in the housing market.

Increasing prices could encourage households to

buy a home, expecting that its price will continue

to rise, so that they will make a capital gain from

homeownership. This will boost demand for hou-

sing and could cause prices to escalate further.

Conversely, households could be hesitant to buy

a home if prices are falling or they expect them to

fall. The delay in demand could reinforce a dow-

nward trend in house prices.

Moreover, since homes sold through enforced

sale tend to be sold at a substantial discount to

the market value, a large number of enforced

sales in a given area could have a negative effect

on house prices. This also reduces the probability

of selling a home on the market. If the owner is

0.00-0.09 0.10-0.19 0.20-0.29

having trouble meeting his mortgage payments,

0.30-0.39 0.40-1.00

longer time on the market increases the risk of en-

forced sale. Moreover, in itself, low turnover adds

Note: Number of enforced sales from July 2013 to June 2014.

Enforced sales and housing stock are calculated for all to the risk that a home cannot be sold on the

owner-occupied homes, including leisure homes. market and has to be sold through enforced sale.

Source: Association of Danish Mortgage Banks.

At the same time, uncertainty as to the proper

price of a home increases with few recent sales for

comparison.

national level, but the housing market as a whole To identify the causes of the regional differen-

is still struggling with low turnover, a substantial ces, the factors determining housing supply and

housing supply and a long time on the market. demand are examined below.

DANMARKS NATIONALBANK MONETARY REVIEW, 3RD QUARTER, 2014 47

HOUSING DEMAND in a large disposable amount for other expenses.

Part of the disposable amount is probably saved

House prices, like prices of any other commodi- to allow homeowners to pay future interest costs

ty, are determined by supply and demand. But, when interest rates are likely to be higher. Thus,

unlike most other markets, prices in the housing the current low interest rates are hardly fully re-

market do not adjust instantaneously to match flected in housing demand and house prices. This

supply to demand. This is due to the housing mar- relationship is in line with the high current level of

ket’s special characteristics – for example indivi- household savings.

dual homes vary substantially, much time is spent

searching for a home and the costs of changing DEMOGRAPHICS

homes are high. Housing demand is also determined by demo-

Demand for housing is usually assumed to be graphics. Population growth fuels demand, and

determined by household disposable income the age composition has a bearing on the types

and the user cost, i.e. the cost of owning a home. of homes in demand. At present, Denmark is

The user cost includes real interest rates after tax, experiencing population growth in the order of

housing-related taxes, depreciation and mainten- 30,000 people a year due mainly to net immigrati-

ance and the expected real capital gain or loss in on, which increases total housing demand.

the form of changed house prices, which ex ante Recent years have seen substantial migrati-

are subject to great uncertainty. on from rural to urban areas. For instance, the

Moreover, first-year payments may be signifi- combined population of the Cities of Copenhagen

cant to households. The reasons are that, in addi- and Frederiksberg has grown by a total of 60,000

tion to the financial user cost, some families also inhabitants since early 2009, equivalent to 10 per

attach importance to their liquidity position, have cent, while the number of inhabitants in the mu-

limited access to loans or find it easier to relate to

the payment to be made now than to the calcula-

tion underlying a residential investment over its

entire lifetime, cf. the discussion in Dam et al. Percentage change in the number Chart 5

of inhabitants from 1 January 2009 to

(2011a). Badarinza et al. (2014) analyse the choice 1 July 2014

between short-term and long-term interest rates

on household mortgage loans across nine coun-

tries (including Denmark), finding that, in their

choice of financing, households tend to focus on

short-term costs and liquidity.

Based on the Danish figures, it cannot be de-

termined whether the first-year payments have a

separate impact on Danish house prices. Statisti-

cally, the relation obtained by including the lowest

possible first-year payments is neither better nor

worse than a relation based solely on the pure user

cost.2 However, the economic arguments mentio-

ned are deemed to be strong enough for first-year

payments to be included in the demand relation

for housing used in this article, cf. the Appendix,

which describes the model used in the article.

The current extraordinarily low interest rates

mean very low borrowing costs, especially for

homeowners with loans based on short-term in- [-9.3]-[-4.1] [-4.0]-[-2.1] [-2.0]-[-0.1] 0.0-1.9

terest rates. Other things being equal, this results 2.0-3.9 4.0-5.9 6.0-13.0

2 This requires that inflation expectations are down-weighted in the Source: Statistics Denmark.

real interest rate expression.

48 DANMARKS NATIONALBANK MONETARY REVIEW, 3RD QUARTER, 2014

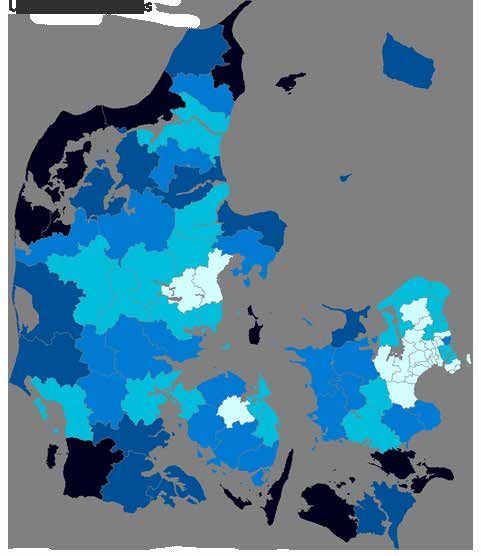

nicipality of Lolland has been reduced by 4,400, Consequently, the future demand for urban hou-

corresponding to a decline of more than 9 per sing will increase, while the demand for housing

cent, cf. Chart 5. in peripheral areas will decrease. This is especial-

According to Statistics Denmark’s most recent ly true when demographic factors such as age,

population projection, urban population growth education and cohabitation patterns are taken

is set to continue at the expense of rural areas. into account, cf. Hansen et al. (2013).

Interaction between regional housing markets Box 1

A ripple effect exists between regional housing markets, pulation of Copenhagen remained largely unchanged, while

cf. Meen (1999 and 2001). This effect is created through it increased in the surrounding areas. When prices subse-

multiple channels, the most import channel seeming to be quently fell in Copenhagen, narrowing the price difference,

the price. A growing price spread between two areas implies the population of Copenhagen started growing rapidly.

that more of the demand will be aimed at the area with the In recent years, prices have been escalating in Copenha-

lowest price, contributing to some geographical equalisati- gen, thereby increasing price differences, and at the same

on – both in terms of price and activity. But price differences time, the population of Copenhagen continues to grow, for

should be seen in the context of distances. The closer two instance because people are not moving out to the same

areas are, the closer substitutes the general location of extent as seen in the first half of the 2000s.

housing will be. Accordingly, in general, Danish house prices However, in 2012 and 2013, slighly more people in the

are lower, the further the distance to the nearest urban area 25-39-year age group moved out of Copenhagen than in the

with high prices, cf. the chart below (left). Heebøll (2014) preceding years, most of them moving to municipalities in

finds indications that price developments in Copenhagen eastern and northern Zealand. At the same time, higher pri-

seem to lead prices in the rest of the country. ces in Copenhagen once again seem to be rippling through

In the mid-2000s, surging prices in Copenhagen caused to eastern Zealand, but this time the effect starts at a higher

the price difference between Copenhagen and other areas price difference per square metre of home than in the 2000s,

of Zealand to increase, having a ripple effect from Copenha- cf. the chart below (right).

gen to the surrounding areas. During that period, the po-

Average price in kr. 1,000 per square metre of home 2013/14 (left) and additional price per square me-

tre of home in Copenhagen environs relative to the closest surrounding areas (right)

1,000 kr. 1,000 kr.

18 28

16 26

14 24

12 22

10 20

8 18

6 16

4 14

2 12

0 10

00 01 02 03 04 05 06 07 08 09 10 11 12 13

Northern Zealand

Eastern Zealand

Western and Sourthern Zealand

Level for Copenhagen environs (right axis)

0.0-5.9 6.0-7.9 8.0-9.9

10.0-14.9 15.0-19.9 20.0-34.9

Note: Left-hand chart: average sales price in the period from the 2nd quarter of 2013 to the 1st quarter of 2014. Prices have not been adju-

sted for potential quality differences between the homes sold. Right-hand chart: Seasonally adjusted data. 3-quarter moving averages.

Source: Housing Market Statistics.

DANMARKS NATIONALBANK MONETARY REVIEW, 3RD QUARTER, 2014 49

Interaction between regional housing markets Box 1 continued

The reason why higher prices in Copenhagen are rippling ced using a fixed rate loan with amortisation, the differences

through later this time could be that – due to the decline in the 1st quarter of 2014 were in line with those in 2006, at

in interest rates – the difference between financing costs at their peak, cf. the chart below (right).

and housing taxes in Copenhagen and environs relative Expectations in terms of the future user cost could also

to other Danish areas has not increased similarly. This is help explain growing price differences. This is the case if

particularly true for homes financed with variable rate and people base their expectations of price patterns on histori-

deferred amortisation loans. With this type of financing, the cal performance. If prices have been appreciating for some

difference between financing costs and tax payments on a time, as seen in Copenhagen, people may expect to make a

home in Copenhagen environs and other Zealand areas was capital gain from homeownership. This will reduce the expe-

generally smaller in the 1st quarter of 2014 than during the cted user cost and boost housing demand. Conversely, fal-

period from the 2nd half of 2005 to 2008, cf. the chart below ling prices, as seen in western and southern Zealand, could

(left), although the difference in price per square metre was cause them to anticipate a capital loss. This will increase the

smaller at the time. If, instead, the home purchase is finan- user cost and reduce housing demand.

Savings in annual financing costs and tax payments related to homeownership in selected areas rather

than in Copenhagen environs

Kr. 1,000 Variable-rate loan without amortisation Kr. 1,000 Kr. 1,000 Fixed-rate loan with amortisation Kr. 1,000

100 180 150 250

80 160

100 200

60 140

40 120

50 150

20 100

0 80 0 100

04 05 06 07 08 09 10 11 12 13 14 02 03 04 05 06 07 08 09 10 11 12 13 14

Northern Zealand Northern Zealand

Eastern Zealand Eastern Zealand

Western and Southern Zealand Western and Southern Zealand

Level for Cph's environs (right-hand axis) Level for Cph's environs (right-hand axis)

Note: The series illustrate stylised financing costs, including administration margins, brokerage fees and housing taxes on the purchase of a

single-family home of 140 square metres.

Source: Statistics Denmark, Housing Market Statistics, Realkredit Danmark, Danmarks Nationalbank and own calculations.

However, demographic developments should tenants. More students thus increase the pressure

be seen also in the context of prices. Urban popu- on the rental housing market; however, to address

lation growth could be the result of the narrowing the issue of rental housing shortages, parents are

difference in the sum of financing payments and buying flats for their student and adult children,

tax payments between Copenhagen and the sur- boosting demand for owner-occupied housing.

rounding areas since the mid-2000s, cf. Box 1. The population growth in Copenhagen has

People under the age of 30 account for ap- been broad-based across age groups below 60,

proximately 60 per cent of the population grow- while the number of people in their early 60s or

th in the City of Copenhagen, reflecting mainly older than 75 has declined. However, the fall is

that more young people have migrated to towns limited and has released relatively few homes.

and cities, often to study, and that an increasing

proportion of people have remained in or around DISPOSABLE INCOME

Copenhagen after graduation. They have subse- The changes in demographic patterns should be

quently started families, so the number of children seen in the context of uneven distribution of eco-

in Copenhagen has increased. Families with chil- nomic growth across Denmark since 2008. Growth

dren tend to demand larger homes – in Copenha- has primarily taken place in the cities, especially

gen often in the form of owner-occupied homes. Copenhagen, which has also seen the largest

Students typically have low incomes and are rise in employment. As a result, the labour force

50 DANMARKS NATIONALBANK MONETARY REVIEW, 3RD QUARTER, 2014plies to other large towns and cities in Denmark.

House price of an average home rela- Chart 6

Accordingly, people who can afford owner-occu-

tive to average disposable household

income pied housing are increasingly living in the cities,

serving to increase demand. Since Copenhagen’s

Index, 2000 = 100 housing supply has not grown in line with de-

160

mand, this is reflected in higher prices.

140 The level of house prices may be seen in

relation to household disposable income, since

120

the disposable income usually finances the home

100 purchase. In the last few years, the price of an

average home has increased at the same rate as

80

the average household disposable income and

60 the ratio between the two is largely the same as

in 2004, i.e. before the surge in house prices, cf.

40

92 94 96 98 00 02 04 06 08 10 12 14 Chart 6.

Note: Household disposable income excluding pension savings INTEREST RATES AND TAXES

divided by the number of households in Denmark, i.e. The price of an average home relative to average

both owners and tenants. An average home is 140 squa-

re metres. household disposable income is a simplified way

Source: Statistics Denmark and Housing Market Statistics.

of looking at the level of house prices. The reason

is that changes in interest rates and taxes, among

other factors, are not taken into account although

in Copenhagen has expanded in recent years, they are very important in terms of current costs

while it has decreased in the rest of the country, of financing homeownership.

reflecting, inter alia, that jobholders are moving In recent years, interest rates, both short-term

to urban areas, while the unemployed and pensio- and long-term, have declined to very low levels,

ners are increasingly moving to other parts of the cf. Chart 7 (left). Low interest rates make mortga-

country. At the same time, average incomes have ge financing less expensive, helping to buoy up

risen more in Copenhagen than in the rest of the the housing market. However, a small part of the

country, due, among other factors, to an increase interest rate fall has been offset by higher admi-

in the average level of education. The same ap- nistration margins and brokerage fees, especially

Interest rate developments and housing burden Chart 7

Interest rate developments Housing burden

Per cent Per cent

8 40

35

6

30

4 25

20

2

15

0 10

00 01 02 03 04 05 06 07 08 09 10 11 12 13 14 81 84 87 90 93 96 99 02 05 08 11 14

Fixed rate, w/amortisation

30-year mortgage yield Fixed rate, w/o amortisation

Short-term mortgage yield Variable rate, w/amortisation

Variable rate, w/o amortisation

Note: The housing burden for the 2nd quarter of 2014 is based on expected developments in house prices and household disposable income

in the projection described in this Monetary Review. The housing burden illustrates stylised financing costs including administration

margins, brokerage fees and housing taxes on the purchase of a single-family home of 140 square metres as a percentage of the avera-

ge income. See Dam et al. (2011a) for further details.

Source: Statistics Denmark, Housing Market Statistics, Realkredit Danmark, Danmarks Nationalbank and own calculations.

DANMARKS NATIONALBANK MONETARY REVIEW, 3RD QUARTER, 2014 51for the most risky loans, i.e. variable rate or defer- housing stock if supply is to be reduced. Thus,

red amortisation loans. supply is fixed in the short term, and the price is

Measured in terms of Danish kroner, housing determined by demand.

taxes are relatively stable over time due, inter alia, The value of a home is comprised of the physi-

to the nominal freeze on property value tax intro- cal value of the home and its location. The phy-

duced in 2002; however, property value tax will sical value is presumably given by construction

be reduced correspondingly if the property value costs, at least in the medium term, since, with a

falls below the 2002 level. Moreover, there is a cap certain lag, housing units may be constructed in

on year-on-year increases in property tax – known the required number. Initiating new construction

as land tax – in the form of a regulation ratio. As projects will be financially attractive if the physical

a result of these rules, the effective tax rate is not value of existing housing exceeds the cost of new

the same across Denmark. In areas with rising construction. This process will continue until the

house prices since 2002, tax payments have not supply has been increased enough for the price

increased correspondingly and thus account for a of housing to have fallen to the level of construc-

lower percentage of the value of the home. Con- tion costs. If this anchoring of house prices is

versely, areas where house prices have remained generally known and understood by the market,

largely flat since 2002 have not benefited from the speculative element will be dampened, and

a lower effective tax rate. In practice, this entails unsustainable, speculation-fuelled price hikes will

that the effective tax rate on housing is lower in be limited.

Copenhagen than in large parts of the Danish Conversely, if the increase in housing demand

provinces, for example western and southern Zea- turns out to be transient in nature (a so-called

land. Copenhagen’s lower tax rate boosts demand temporary demand shock), the housing supply

and raises house prices, generating capital gains adjustment will cause the subsequent price drop

for current homeowners. to be stronger than it would otherwise have been.

Overall, current costs of financing homeow- This is because there is more housing on the

nership relative to average household disposable market than previously, potentially in the form

income have dropped sharply at the national level of upcoming housing projects, since much of the

in recent years. This is demonstrated by the devel- residential construction may have been planned

opment in the housing burden, cf. Chart 7 (right). and initiated before the reversal and would not be

Obviously, financing costs vary with the type of financially viable to cancel.

loan, but – regardless of the type of loan – the That seems to have been the case in some

housing burden is lower today than in the early places in Denmark, which experienced a residen-

2000s before house prices started soaring. This is tial construction boom in 2007, cf. Chart 8 (left),

due to the very low interest rates. although demand was already weakening and

If the home purchase is financed through a prices were falling faster than justified by the hig-

fixed-rate loan with amortisation, the housing her supply. Subsequently, residential construction

burden in the 2nd quarter of 2014 was 27 per has been very limited, indicating an oversupply of

cent, or just over 2 percentage points lower than housing. Accordingly, no further construction has

the average since 1981. For other loan types, the been required, cf. Chart 8 (right), among other

housing burden was considerably lower. things because demand is or has been falling as

a result of migration. Oversupply of housing has a

number of negative effects on the housing mar-

DEMAND AND LAND PRICES ket, cf. Box 2.

Unlike the actual housing unit, the location can-

The housing market differs from many other not be produced in unlimited numbers. Geograp-

markets in that supply responds to changes in hy largely determines whether land shortages

demand with a considerable lag. Planning and exist. In rural areas, land is in ample supply, while

completing new construction projects takes time large towns and cities have a shortage of land.

if supply is to be increased; similarly, the housing This is reflected in substantial differences in land

decay rate is slow, entailing that it takes a very prices across Denmark, cf. Chart 9 (left). In rural

long time for housing to be eliminated from the areas, the price reflects alternative land uses, typi-

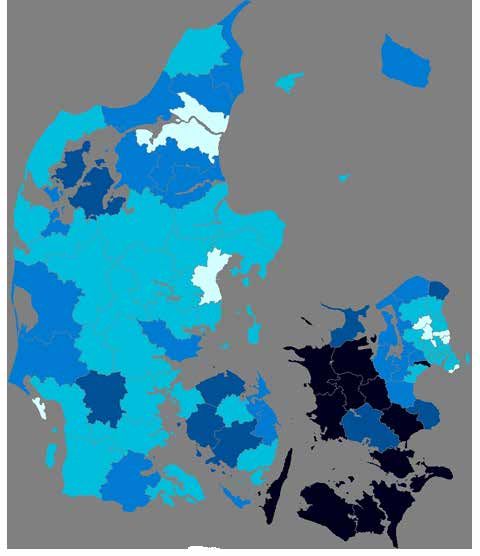

52 DANMARKS NATIONALBANK MONETARY REVIEW, 3RD QUARTER, 2014Completed construction for year-round occupation as a percentage of the existing Chart 8

housing stock in 2007 and 2013

0.0-0.6 0.7-1.1 1.2-1.7 0.0-0.6 0.7-1.1 1.2-1.7

1.8-2.1 2.2-3.3 1.8-2.1 2.2-3.3

Note: Completed construction in square metres as a percentage of the total floorage. Both for year-round occupation.

Source: Statistics Denmark.

Land prices in selected areas and development in house prices, construction costs, land Chart 9

prices and consumer prices

Land prices House and land prices, etc.

Kr. 1,000 Index, 2000 = 100 Index, 1955 = 1

3,000 150 90

Hundreder

2,500 125 75

2,000 100 60

1,500 75 45

1,000 50 30

500 25 15

0 0 0

92 94 96 98 00 02 04 06 08 10 12 55 59 63 67 71 75 79 83 87 91 95 99 03 07 11

Copenhagen environs Northern Zealand

Eastern Zealand W and S Zealand House prices Construction costs

Northern Jutland Denmark (right axis) Land prices Consumer prices

Note: Left-hand chart: simple average of prices of sold plots below 2,000 square metres for the area. For the series ”Denmark”, a price index

is shown in which Statistics Denmark has quality-adjusted data based, inter alia, on the public property valuation. Right-hand chart: all

indices illustrate developments in nominal prices and costs.

Source: Statistics Denmark.

DANMARKS NATIONALBANK MONETARY REVIEW, 3RD QUARTER, 2014 53The housing market in case of an oversupply of housing Box 2

There are considerable geographical differences in the ban migration trends will reverse anytime soon, permanent

number of homes for sale and the number of unoccupied changes in the housing supply are required if the balance

homes, cf. the chart below (left). Some are unoccupied for a between supply and demand is to be restored. As homes

short period of time while people are moving house, so the are slow to lose their value and will continue to be part of

percentage of unoccupied homes will never be zero. More- the supply for a long time even if they are not maintained,

over, some homes are unoccupied because they are used as this process will take many years. When the oversupply is

leisure homes, while the rest is de facto unoccupied. eventually absorbed, the price will, once again, be given by

In some parts of Denmark, the high percentage of ho- construction costs plus land prices.

mes for sale and unoccupied homes indicates that supply In practice, the supply will decline when homes are

exceeds demand, which will lead to lower prices. Experien- demolished or fall into such disrepair as to be uninhabi-

ce shows that some stickiness exists in this respect, since table. If a home is uninhabitable, it typically has not been

homeowners are not immediately prepared to accept a loss maintained for many years. This may be the case if house

on their home or have debt exceeding the price that would prices are low, since this provides a disincentive to maintain

ensure a sale. Consequently, the initial asking price tends to the home because the costs incurred will not be covered

be higher than the final sales price, especially if the home by a potential sale. Demolition is costly, and conversion to,

is on the market for some time in a declining price environ- say, agriculture may not be profitable. Financially, the best

ment. Moreover, people will be hesitant to buy if they expect option may be to let the home fall into disrepair and pay the

prices to fall, since they expect to be able to acquire a home taxes due. Thus, demolition subsidies, as agreed in the June

later at a lower price. This will be reflected in low turnover 2014 growth package, may help to speed up the housing

and a long time on the market in areas with an oversupply adjustment process in selected parts of the country. Alterna-

of housing. tively, demand in these areas may be boosted by improving

In most of the areas with a large supply of housing, tax deductions for commuters or by increasingly dispensing

declining demand is due to demographic changes, including from the principal residency requirement to allow homes for

rural-to-urban migration. As there are no indications that ur- year-round occupation to be used as leisure homes.

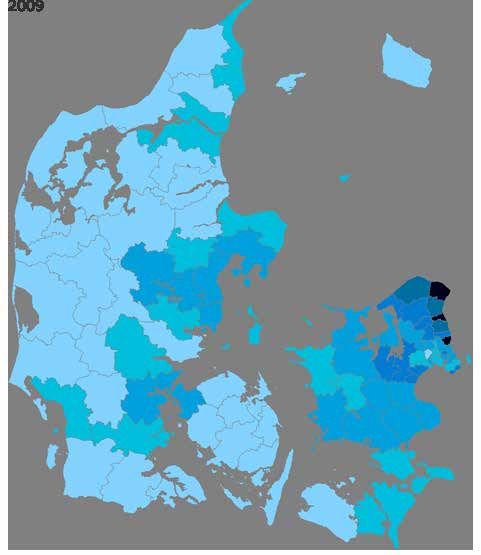

Unoccupied homes and homes for sale as a percentage of the total number of homes for

year-round occupation

2.0-3.9 4.0-5.9 6.0-7.9 1.5-1.9 2.0-2.4 2.5-2.7

8.0-9.9 10.0-32.2 2.8-2.9 3.0-3.4

Note: Left-hand chart: number of homes with no registered inhabitants as at 1 January 2014 relative to the total number of homes for year-

round occupation in the municipality. Some of the homes with no registered inhabitants are used as leisure homes. As they cannot be

identified by Statistics Denmark, they are not included in the statistics. Right-hand chart: seasonally adjusted number of homes for sale

in July 2014 relative to the number of farmhouses, detached single-family homes, terraced homes, linked homes and semi-detached

homes as well as owner-occupied flats in the area as at 1 January 2014.

Source: Statistics Denmark and Housing Market Statistics.

54 DANMARKS NATIONALBANK MONETARY REVIEW, 3RD QUARTER, 2014cally forestry and agriculture, as well as the cost of that urbanisation trends are being reversed. Hig-

land development. In urban areas, the supply can, her urban population density will produce increa-

at some point, no longer be increased. Alternati- ses in urban land values, and if the residential

vely, it will be difficult and costly to increase the area expands, this will drive up land values on the

area of building land, for instance if polluted areas outskirts of towns and cities as the alternative use

are to be cleaned up or new building land is to be changes from agriculture to residential.

created by building out into the water. Thus, land

prices will increase until demand matches supply. LAND PRICES IN A HOUSE PRICE MODEL

The scarcer the land, the more land prices need There has been a clear, long-term tendency for

to fluctuate in order for changes in demand to land prices to rise, cf. Chart 9 (right), reflecting

be adjusted to the largely fixed supply. While, to that economic growth has increased the demand

some extent, construction costs have a cyclical for land, for example for residential purposes, but

element, not least due to wage developments in also for other purposes such as agriculture.

the construction sector, land prices tend to fluctu- Hence, including land prices in a house price

ate more widely, cf. Chart 9 (right). Since land pri- model is relevant. In the model used in this article,

ces account for a much higher proportion of total it has been assumed that house prices are compo-

house prices in large towns and cities, urban price sed of two components: the price of the house it-

fluctuations will be stronger than those experien- self and the land price. The weight to be attached

ced in rural areas. to each component depends on the shortage of

The price of a building plot depends not just land available, which varies across the country.

on the discounted value of future returns, e.g. in In the model, residential construction re-

the form of housing occupancy if the plot is used sponds when the actual house price deviates

for housing construction, but also on the fact from construction costs, while land prices have

that the land could become more valuable in the no significance. In the absence of sufficiently valid

future, cf. Titman (1985). If the price of the plot is and reliable land price data, cf. Box 3, land pri-

expected to appreciate, the owner will sell it only ces are assumed to grow in line with household

at a price that is high enough to compensate him disposable income. Thus, indirectly, it is assumed

for not obtaining the expected higher price at a

later time. This may explain why the supply and

turnover of new building plots are highly limited

during periods of low or falling prices. This helps Statistics for building plot prices Boks 3

to stabilise house prices by limiting the supply of Statistics Denmark calculates a price index and the price

new housing in a weak market. per square metre and the average price of plots below

2,000 square metres. These statistics provide an indica-

However, if growth in the housing market fuels

tion of building-plot prices, although this category does

expectations that prices will continue to rise for not distinguish between the purposes of the plot, i.e. if it

some time – e.g. during a housing bubble – the is intended for housing, leisure or business purposes.

estimated option value of land could contribu- The prices in the statistics sometimes fluctuate

sharply, especially during certain periods and in certain

te to sustaining the upswing. This occurs when

areas, cf. Chart 9 (left), as the statistics are sometimes

landowners withhold plots from sale in the expe- based on very few observations – for instance because

ctation of being able to sell them later at an even a small number of trades causes random fluctuations.

higher price. This reduces supply during a period Furthermore, in its quality adjustment Statistics Denmark

eliminates many observations.

of high demand, causing the price pressure to in- More fundamentally, a house-price model also

crease. These relationships highlight that land and needs the prices of plots already built up. However, the

houses are investment objects and that expecta- statistics only contain observations of the sales prices

of unbuilt plots. That is hardly significant in rural areas,

tions of future price developments could have a

but in urban areas unbuilt plots are often located on the

considerable impact on current price movements. outskirts of towns and cities, and the location cannot be

The option value of a plot is higher in and compared with built-up plots in the town or city centre.

around towns and cities, reflecting that urban Thus prices are not available for plots located in areas

where land is scarce. These plots fetch the highest prices,

land prices are both higher and more volatile. Mo-

and their prices tend to fluctuate more, since a higher

reover, future housing demand is likely to focus supply cannot dampen price rises.

on towns and cities, since there are no indications

DANMARKS NATIONALBANK MONETARY REVIEW, 3RD QUARTER, 2014 55that the demand for scarce land is growing in line MODEL SIMULATIONS

with household disposable income. The modelled

relationship is to capture the long-term trend for House prices are influenced by a range of factors,

real house prices to rise in response to the increa- including cyclical movements, economic policy

sing shortage of land in large towns and cities, and financial conditions. Politicians decide how

while short-term movements in land prices have and how much housing should be taxed, includ-

not been modelled. ing the tax value of mortgage rate deductibility.

Thus, persistent income shocks have a per- At the same time, monetary policy impacts the

manent effect on house prices; furthermore, the housing market through interest rates. Institutio-

long-term income elasticity of housing demand nal aspects, such as the maximum permitted LTV

is assumed to be one. The latter should be seen ratio or the upper limit for deferred amortisation

in the context that housing consumption cannot mortgages, may also be significant.

exceed income, and that the saturation point will Below, the effects of a number of these fac-

occur somewhat earlier, cf. Dam et al. (2011a). tors are quantified using the house-price model

Moreover, the ratio of housing costs to disposable described above and in the Appendix. The model

income varies across the country. In towns and simulates the effects on house-price movements

cities, land is scarce and prices are high, mea- of changes in interest rates, deferred amortisation

ning that the ratio is higher than in the provinces and interest rate deductibility.

where prices are low. As more people migrate to

towns and cities, the number of people spending INTEREST RATE CHANGES AND INTEREST RATE

a large percentage of their income on housing EXPECTATIONS

costs is set to increase. While this adjustment Interest rates are important in determining hou-

process is ongoing, housing costs will absorb sing demand – and thus house prices. The impact

a higher percentage of household income. The is through the user cost, real interest rates after

increasing budget share of housing costs, at the tax accounting for a key portion of the costs of

aggregate level, in recent decades should be seen homeownership. Furthermore, short-term interest

in this context. When the shift in the settlement rates are included in the first-year payments.

patterns ends, the ratio of housing costs to hou- To illustrate the significance of interest rates

sehold income may stabilise. changes, simulations of the house-price model are

House prices under different interest rate assumptions Chart 10

Mortgage yields House prices, deviation from baseline scenario

Per cent Per cent

5 40

4 30

3 20

2 10

1 0

0 -10

14 16 18 20 22 24 26 28 30 16 19 22 25 28 31 34 37 40 43 46 49

1 year, baseline 30 years, baseline

Scenario 1

1 year, scenario 1 30 years, scenario 1

1 year, scenario 2 30 years, scenario 2 Scenario 2

Note: Left-hand chart: ”1 year” is the interest rate on a variable rate loan with a maturity of 1 year. ”30 years” is the interest rate on a 30-year

fixed rate loan. In the baseline scenario, gradual normalisation of interest rates up until 2020 is assumed. In scenario 1, interest rates are

maintained at a low level for the end of 2016 onwards. Scenario 2 entails slower normalisation of interest rates; full normalisation is not

expected to occur until 2024.

Source: Own calculations.

56 DANMARKS NATIONALBANK MONETARY REVIEW, 3RD QUARTER, 2014used. These simulations are based on Danmarks

Nationalbank’s projection presented in this Mone- Expiry of the period of deferred Chart 11

amortisation

tary Review, expanded by a technical projection

from 2017 onwards. The projection entails, inter Kr. billion

alia, a gradual increase in interest rate levels to 175

long-term levels determined on the basis of inte- 150

rest rates over recent decades. Thus, the rate of 125

interest on 1-year adjustable rate loans is increa-

100

sed to 3.5 per cent, while the 30-year interest rate

75

is increased to 5 per cent, cf. the baseline scenario

50

in Chart 10 (left). In the simulations, the baseline

scenario is compared with two different scenarios. 25

In all the simulations performed, the rate of inflati- 0

14 15 16 17 18 19 20 21 22 23

on is assumed to be just under 2 per cent a year. LTV < 60 60 < LTV < 80 80 < LTV < 100 LTV > 100

In scenario 1, both the 1-year and the 30-year

interest rates are maintained at the low level for Note: LTV is short for loan-to-value, expressing the relationship

2016 from the projection presented in this Mone- between the amount of the loan and the value of the

home.

tary Review. Short-term interest rates are part of Source: Danish mortgage banks, Danmarks Nationalbank and

the first-year payments, while long-term interest own calculations.

rates are included in the user cost. This results in a

substantial price reaction, since the model proje-

cts that in 2024, prices will be 32 per cent higher economy, cf. Andersen et al. (2014). A lower limit

than in the baseline scenario, then slowly fall for deferred amortisation would reduce LTV ratios

back, cf. Chart 10 (right). in boom periods, thereby preventing them from

In scenario 2, it is assumed that actual interest becoming excessive in recession periods.

rates rise more slowly towards their long-term The use of deferred-amortisation mortgage lo-

levels than projected by the baseline scenario. ans for owner-occupied homes and summer cot-

Again, lower interest rates lead to stronger price tages grew strongly from the introduction in 2003

movements: in 2023, prices are 11 per cent higher to the outbreak of the financial crisis, accounting

than in the baseline scenario. Prices fuel residen- for close to 50 per cent of total mortgage lending

tial construction. Higher supply and adaptive at end-2008. Since then this share has increased

household expectations of housing capital gains to more than 55 per cent. Around half the loans

mean that once price increases have peaked, they have an LTV ratio of more than 80 per cent and by

will relatively quickly fall to around zero, before far the largest number of loans has an LTV ratio

gradually stabilising. of more than 60 per cent, cf. Chart 11. This makes

The simulations illustrate that house prices households sensitive to even small declines in

are highly sensitive to interest rate movements. house prices, and mortgage banks may have to

Therefore, widespread expectations that the fund top-up collateral for bonds.

current low interest rates will persist for a number Changing the upper limit for deferred amortisa-

of years entail a substantial risk that house prices tion does not affect the user cost – it only defers

could escalate in the short to medium term. the loan repayment date. But it does have an

immediate impact on liquidity through the first-

DEFERRED AMORTISATION year payments. Calculations show that for a fully

During the most recent boom, household bor- leveraged purchase of an average home using a

rowing surged. When house prices subsequently fixed-rate mortgage, the monthly payment in the

began to fall, LTV ratios increased substantially. 2nd quarter of 2014 would e.g. have been just un-

Analyses show that the high gross debt does der kr. 850 higher with an LTV ratio of 60 per cent

not pose a serious threat to financial stability, cf. rather than 80 per cent.

Andersen (2012). On the other hand, the high As discussed above, there are strong econo-

debt may have indirect effects, since high LTV mic arguments that the first-year payments affect

ratios amplify cyclical fluctuations in the Danish housing demand. But since, based on statistical

DANMARKS NATIONALBANK MONETARY REVIEW, 3RD QUARTER, 2014 57criteria, it cannot be determined whether the first-

Effect on annual rate of price increase Chart 12

year payments indeed have a separate impact on

for house prices if the upper limit for

deferred amortisation mortgage loans is Danish house prices, it cannot be ruled out either

reduced from 80 to 60 per cent that changes in the access to deferred amortisati-

on loans may have only a modest effect on house

Percentagepoints

1.5 prices. Therefore, the reported results should be

regarded as high-range estimates.

1.0

To illustrate the importance of deferred amorti-

0.5

sation to house prices, a simulation is performed

0.0

in which the possibility of raising a deferred amor-

-0.5 tisation mortgage loan is reduced from 80 to 60

-1.0 per cent of the total value of the home. The simu-

-1.5 lation is based on the technical projection of the

-2.0

Danish economy described above, the reduction

15 20 25 30 35 40 45 50 occurring from the turn of the year 2014/15. Hig-

Low interest rate level Normal interest rate level her repayments increase the first-year payments,

causing prices to rise less than would otherwise

Note: Deviation in annual rate of price increase relative to the have been the case, cf. Chart 12. Nominal annual

baseline scenario. For the series ”Low interest rate level”

and ”Normal interest rate level”, respectively, interest

growth rates are dampened by up to 1.5 percen-

rates are as described in scenarios 1 and 2 in Chart 10 tage points, entailing that price increases remain

(left).

Source: Own calculations. positive throughout the period. Over time, the

price effect of amended rules for deferred amorti-

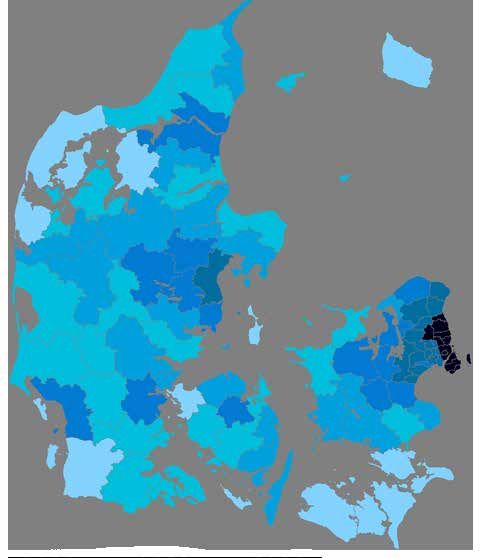

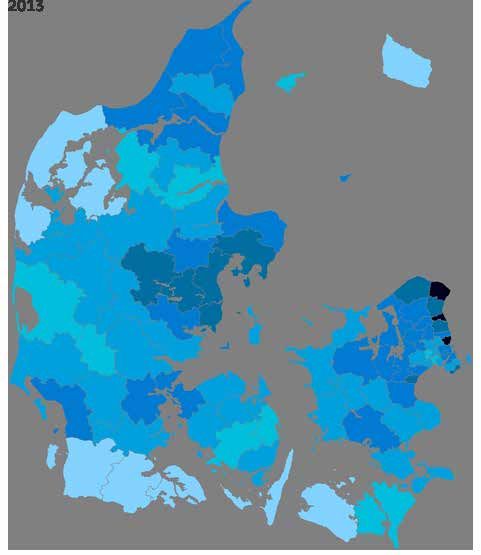

Mortgage customers with deferred amortisation for at least one loan in 2009, respective- Chart 13

ly 2013, as a percentage of the total number of mortgage customers

20-40 41-45 46-50 20-40 41-45 46-50

51-55 56-60 61-70 51-55 56-60 61-70

Source: Danish mortgage banks, Danmarks Nationalbank and own calculations.

58 DANMARKS NATIONALBANK MONETARY REVIEW, 3RD QUARTER, 2014sation will disappear, and in the long term prices

will be more or less at the same level as without Effect on annual rate of price increase Chart 14

for house prices if the tax value of in-

the change. terest rate deductibility is reduced by 2

As illustrated by the model calculation, redu- percentage points per year in 2020-24

ced access to deferred amortisation could have

Percentage points

a negative impact on house prices, but the effect 1.0

of reducing the LTV ratio from 80 to 60 per cent is

modest. Thus, there does not seem to be a strong 0.5

argument for waiting, especially since deferred

0.0

amortisation loans are most widespread in areas

where the housing market is strongest, i.e. par- -0.5

ticularly in and around the capital and Aarhus,

cf. Chart 13. Presumably, these areas will be best -1.0

set to meet stricter repayment requirements. In

-1.5

recent years, deferred amortisation has become 20 25 30 35 40 45 50 55 60

Low level of interest rates Normal level of interest rates

more prevalent in other parts of Denmark as well,

but here the share of deferred amortisation loans

remains below the level seen in the capital. Redu- Note: Deviation in the annual rate of price increase relative to

the baseline scenario. For the series ”Low level of interest

ced access to deferred amortisation would also rates” and ”Normal level of interest rates”, respectively,

be appropriate in view of the risk of an imminent interest rates are as described in scenarios 1 and 2 in

Chart 10 (left).

boom in house prices, at least in some areas. If in- Source: Own calculations.

terest rates subsequently rise, higher house prices

could be temporary, increasing the risk that some

households will be faced with very high LTV ratios.

INTEREST RATE DEDUCTIBILITY level of interest rates, as described in scenario

Interest rate deductibility is significant both in 2, the greatest impact will be in 2025, in which

terms of the user cost and the first-year payments, year the year-on-year price increases will be 1.3

since both components depend on the rate of percentage points lower than if the interest rate

interest actually paid by homeowners, i.e. the rate deductibility remains unchanged. Subsequently,

of interest after tax. Consequently, housing de- house prices will gradually approach the baseline

mand is impacted by changes in the tax value of scenario as the housing stock adjusts to the new,

interest rate deductibility. The price implications lower demand.

of lower tax deductibility of interest costs can also A lower tax value of interest rate deductibili-

be illustrated by calculations in the house-price ty increases the financing costs for a given loan

model used in this article. amount, thereby reducing the incentive for people

In the simulation, the tax value of interest rate with negative capital income to raise further debt.

deductibility is reduced3 by 2 percentage points Moreover, if interest rate deductibility is reduced,

per year during the period 2020-24, i.e. an over- the impact of interest costs on the user cost will

all fall of 10 percentage points. This will dampen increase, thus dampening house-price fluctuations

price increases, but the effect is modest, and the following a shock to housing demand.

rate of increase remains positive. At a low level A lower value of interest rate deductibility

of interest rates, as described in scenario 1, the could lead to improved household capitalisation

annual rate of price increase will be reduced for the benefit of financial stability. Changes in

by 0.6 percentage point in 2024, which will see capital-gains taxation through a reduction of the

the greatest impact, cf. Chart 14. At a normal tax value of interest rate deductibility would have

a relatively modest effect on house prices, espe-

cially in the current very low interest rate environ-

3 For people with negative net capital income, the current tax value of

interest rate deductibility is 33.6 per cent on average across munici- ment, as such changes would have only a modest

palities. The tax value of negative capital income exceeding kr. 50,000

effect on household interest payments after tax.

per person is gradually reduced by 1 percentage point a year until

2019, taking the rate to 25.6 per cent.

DANMARKS NATIONALBANK MONETARY REVIEW, 3RD QUARTER, 2014 59You can also read