2018 Real Estate Outlook - The Australian Perspective February 2018 - Active Consulting

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

2018 Real Estate Outlook The Australian Perspective February 2018

Executive summary Things look positive in 2018 for the real estate and construction industries. Although the uncertainty of previous years has not entirely gone – and some markets won’t be as buoyant as they have been – on the whole the road ahead looks more settled and business like. It will however be a very busy year on the implementation front. Multiple variables that impact the sector are beginning to settle, and as the complex ecosystem of third parties as well as regulatory requirements expands, there continues to be new frontiers and structural changes to manage. In the following pages of this Outlook, we discuss these frontiers and changes, and look forward to discussing how the trends we outline apply to your business. Alex Collinson National Lead Partner Real Estate and Construction Deloitte Australia

Contents

Market and investment

Macroeconomic backdrop 03

Outlook investment trends 07

A-REITS – Reflection on value 11

Development in Western Sydney 14

Technology

Why should companies focus on real estate fintech startups? 18

Cyber in real estate 21

Embrace robotics and cognitive automation 23

Digital finance – The new superhero 26

People

Reimagine talent and culture 30

The last word

Scenario – What if? 37

02

2018 Real Estate Outlook |

Market and investment

Macroeconomic backdrop

Australia has chalked up its 26th The good news for Australia is that global Australia remains at the

consecutive year of economic growth, economic growth has picked up during 2017,

and the clouds around Australia’s economy much of that driven by Asian economies, upper end of developed

are clearing. Commodity prices have firmed and in recent months that has translated economies for projected

up and the slowdown in mining investment into much stronger employment growth

growth is now mostly in the rear view in Australia. That growth should also lift growth, supported by

mirror. Mine approvals came to a halt a demand for capital, boosting the outlook population growth and

while ago, but it wasn’t until 2017 that the for business investment.

already approved projects were completed. linkages to Asia, but

Chart 1 – Expected GDP growth of major economies, average annual growth constrained by high

across 2017 and 2018 (forecast) household debt.

South Asia

East Asia and Pacific

9%

India

8%

China

7%

6%

New Zealand

5%

United States

Australia

United Kingdom

South Africa

4%

Euro area

3%

Japan

2%

1%

0%

But global growth is yet to translate to While the general consensus is that the

inflation. While there are encouraging next move for Australian rates will be

signs of global inflation emerging, the up, we expect no upward movements

outlook is for official Australian interest in Australian interest rates until late in

rates to stay near record lows until late in 2018 or early in 2019.

2018 or early in 2019, a blessing for real

estate markets, especially so in NSW and

Victoria and the ACT.

Chart 2 – Australian interest rates, 90 day bank bill

10%

8%

6%

4%

2%

0%

Dec 2000 Jun 2003 Dec 2005 Jun 2008 Dec 2010 Jun 2013 Dec 2015 Jun 2018 Dec 2020

03

2018 Real Estate Outlook |

Market and investment

Having said that, the Royal Commission Outlook for the residential segment

Household debt has

into the banking industry may The current residential property upswing

raise the effective cost of borrowing has seen strong price inflation, up around escalated with house prices

as banks are likely to respond by 47% across capital cities since December

– Australia’s household debt

continuing to limit lending to risky 2012 (around the beginning of the current

initiatives, including some property upswing nationally). Chart 3 shows that to income ratio is now the

development and foreign borrowers. price growth has been uneven across the

second highest in the world,

states, pulled along by the Sydney and

Melbourne markets. behind only Switzerland.

Chart 3 – Change in nominal house values, Dec 2011 – Sept 2017 (per cent)

80%

70%

60%

50%

40%

30%

20%

10%

0%

-10%

Sydney Melbourne Brisbane Adelaide Perth Hobart Darwin Canberra

Source: ABS Cat.6416

In 2017, house prices fell in Perth and Household debt has escalated with

Darwin, linked to population movements house prices – Australia’s household

and employment opportunities. Slower debt to income ratio is now the second

price growth in the Brisbane market also highest in the world, behind only the

likely reflects low employment growth Swiss. And while growth in debt has

as well as the risks of oversupply in the been most pronounced for higher

apartment segment, but this may have income households, higher debt adds

bottomed out now. to the economy’s vulnerability in the face

of a shock, and could also lead to lower

future growth (IMF 2017).1

Chart 4 – Housing debt to income

160.0

140.0

120.0

100.0

80.0

60.0

40.0

20.0

0.0

Jun Jun Jun Jun Jun Jun Jun Jun Jun Jun

1990 1993 1996 1999 2002 2005 2008 2011 2014 2017

Source: Reserve Bank of Australia

Regulators aiming to restrain increasing volume of ‘interest only’ loans to total

property debt amid concerns of an new residential mortgages, have pushed

overheating market have targeted up rates for investors. Market activity has

investor lending. Tighter lending begun cooling with house price growth

standards and restrictions on the slowing in the latter half of 2017.

1. IMF, 2017, Global Financial Stability Report, October.

04

2018 Real Estate Outlook |

Market and investment

Despite the vulnerabilities, the residential Outlook for the commercial segment •• A shift in focus to rental income growth

market generally continues to be buoyed Demand for new office space is largely for value appreciation given cap rates are

by other fundamentals. Underlying determined by white-collar employment near historical lows and further tightening

demand remains solid with strong (albeit growth. The standout performers in potential probably limited.

uneven) population growth expected to 2017 were the Melbourne and Sydney

•• Although some firms are now

continue into 2020, and jobs growth has CBD markets. Melbourne has seen

discouraging remote working, in general

been strong, especially in Victoria. particularly strong growth, while Brisbane

the trend toward flexible working

is gradually catching up to its east coast

Chart 5: Average population growth, arrangements is becoming more

competitors after an extended period of

past five years and across 2017-18 mainstream and as a result there’s likely to

weakness. Overall office vacancy rates

and 2018-19 be ongoing consolidation of office space

have continued to fall, due to positive net

requirements by large space users.

demand in CBD markets and withdrawals

VIC

2.50

in non-CBD markets. Outlook for the industrial segment

QLD

NSW

2.00

WA

The outlook for industrial space demand

1.50 The outlook for white collar employment

NT

is dependent on what is happening across

1.00 over the next few years is a positive news

SA

a range of sectors that drive demand for

TAS

0.50 story – job growth is increasingly being industrial space. Renewed global growth

0.00 driven by service-based sectors, with and the easing of inflationary risks (and

Average population growth past 5 years health care by far the front runner, and thus the delay in expected timing of interest

Average population growth 2018-2019

with professional services and education rates) has been good news for a number of

also expected to generate jobs. these sectors, and will likely buoy demand

And the outlook for construction activity Commercial construction has been for Australian industrial property.

in the near term varies across the states: a relatively disappointing part of the •• It has reduced the risk for wholesalers

•• For both NSW and Victoria, growth in Australian economic story over the past and retailers that sagging housing

housing construction has slowed from few years – it was initially hoped that prices could pose problems before

its peaks but remains at high levels and construction could fill some of the hole left wage growth improves to provide

is underpinned by strong underlying by the mining construction ‘cliff’ (after the a rising tide for the sector.

demand. In Victoria, population growth first phase of the China boom), but it didn’t

•• 2017 has seen reasonable gains in

is containing risks of oversupply. pan out that way.

engineering activity in NSW, Victoria and

•• Housing construction fell in QLD over That looks set to change in 2018, with Queensland, as work continues on a

2017, having reached its peak in mid- commercial construction set to grow over number of large infrastructure projects.

2016. Despite population growth edging the year. Building approvals have picked up We expect engineering construction

higher, housing construction is likely to since mid-2016, supported by strength in to stop detracting from the economy’s

remain relatively flat in the near term. the office, and education sectors. overall growth and become a more

Similarly for SA, the housing construction neutral contributor in the near term.

In total, there are $20 billion worth of

outlook is also relatively flat, because

office projects under construction across •• Transport investment continues to go

while approvals have picked up in late

Australia in late 2017, the largest of which from strength to strength, with more than

2017, population growth projections

is the $6 billion Barangaroo development. $95 billion worth of transport and storage

remain weak.

There are a further $8 billion worth of projects underway in the latter half of

•• WA’s housing construction has seen a projects yet to kick off. 2017 and $140 billion worth of projects in

large downturn in recent years (including planning. Much of that activity is focused

Likely trends for commercial property over

a large fall in 2017), but looks to be in the nation’s east and south.

the near term include:

stabilising, with building approvals and

•• Constrained supply in the Sydney and •• Conditions have improved for

loan approvals steadying.

Melbourne markets provide a positive manufacturing supported by an increase

Taken together with the outlook for in public sector infrastructure spending,

outlook for rental growth. The Perth and

interest rates, slowing house price growth improved global growth and an Australian

Brisbane markets have likely bottomed

(moderating the prospect of further capital dollar that, despite gaining ground in

out, with the economic and property

gains), restrictions on lending (such as on 2017, is still below the peaks of mid-2014.

outlook improving.

interest only loans and loans to investors, However, higher energy costs are weighing

as well as lending to foreign investors); we on profitability for manufacturers and

expect the current upswing to peter out could affect investment prospects. That

and enter a period of moderation rather said, $18 billion worth of manufacturing

than an abrupt adjustment. investment projects are in various stages

of planning as at late 2017.

05

2018 Real Estate Outlook |

Market and investment

Likely trends for industrial property over But forward indicators are suggesting a Likely trends for retail property over

the near term include: good basis for spending to lift in 2018, the near term include:

•• Industrial property is a tightly held including:

•• High levels of demand for centre space

market, and there are pockets of •• Strengthening employment outcomes

are set to continue in the near term –

supply constraints – strong continued

•• An improving outlook for wages growth with growth in food and hospitality uses

capital growth is expected in the

and smaller footprints for many larger

near term, buoyed by the national •• Low cost of borrowing

format retailers.

infrastructure rollout.

•• Continued (albeit slowing) wealth gains

•• There may be the potential for further

•• The trend of urban regeneration seen from housing.

yield compression in the near term,

in recent years, with industrial land The value of building approvals fell slightly concentrated at the prime/super regional

converted to mixed use for residential in the year to September 2017, ending a end of the spectrum. This is likely to be

purposes, is expected to continue. This is run of impressive gains. In terms of project driven by the low frequency that these

especially true of Melbourne and Sydney activity, there are more than $5 billion worth assets are offered to market and weight

where jobs growth is expected to be of retail projects under construction, as of capital in the sector.

concentrated in the CBD. well as a further $6 billion in the various

planning stages (Deloitte Access Economics’ •• The impact of online retailing to

•• Further growth in foreign investor

Investment Monitor, December 2017). continue to test the sector – given the

participation in the market is expected

relatively current low rate of penetration

to emerge as market sophistication and Key risks to the sector include the effect in Australia and Amazon opening its

maturity evolves. of Amazon’s recent entry and slowing doors locally!

•• Yields will eventually be pressured by growth in household wealth. We will get

Risks

a rising global and local cost of capital, a better idea of the impact of Amazon’s

There are risks to the outlook for Australian

but that doesn’t loom as a major risk for entry on bricks and mortar retailers in

property: part of today’s good news

2018. Yields may remain relatively stable coming months – and therefore demand

is also bad news. Thanks to renewed

in the coming calendar year, with some for retail floor space. But the results of a

stimulus, Chinese construction activity

opportunity for further compression in recent survey suggests that retailers are

has picked up again. But much of that

select markets. not overly alarmed by Amazon’s entry to

money is supporting the worst performing

the Australian market (Deloitte’s Retailer’s

Outlook for the retail segment State Owned Enterprises (SOEs), thereby

Christmas Survey 2017). While a third of

Retail spending is becoming more uniform increasing China’s vulnerability to a sharp

respondents believed Amazon would have

across the states as retail spending growth adjustment as the economy transitions.

a negative impact on their business, 40%

slows in the previously robust eastern states That’s also true for Australian rates. We’ve

believed it would benefit them. Continuing

(Deloitte Access Economics’ Retail Forecasts, used lower interest rates to ward off risks

a tone of confidence, looking forward to

December 2017). While the resource states of recent years, boosting property prices,

2018, 51% of respondents expected to

are still facing challenges, particularly and household debt along the way.

grow their earnings by more than 5% next

in Western Australia and the Northern year (down from 2016 expectations, where While the most likely path for the Australian

Territory, Queensland is less pressured. 60% believed this would be the case). economy doesn’t see a triggering of those

Annual retail spending growth in New South new risks (China and/or housing), they’re

Wales and Victoria has slowed significantly Despite challenges and disruption in

both plausible and relevant risks and

in the latter half of 2017, towards the the sector, demand for retail space within

worthwhile exploring further.

more modest growth seen in the slower the Australian market remains solid, in

population growth jurisdictions of South part due to the number of new large- In a later chapter we present our China

Australia and Tasmania. The ACT is also scale international entrants setting up Stumbles scenario, and step through

witnessing a significant retail slowdown after operations in Australia. how scenarios can be used for strategic

a strong period. planning for our model REIT.

Kristian Kolding leads the Deloitte Access Economic macroeconomic forecasting and policy team in Sydney. Kristian is co-author

of Deloitte’s flagship series, Building the Lucky Country, that consider future profitability models for the nation. Working closely with

Deloitte Access Economics, Chris Richardson, Kristian also forecasts the effect of policy changes on the economy.

Anthony Moeller leads the real estate advisory area of the Financial Advisory group in Sydney and is a leading provider of strategic

property advice to government and the private sector underpinned by his close working relationship with the Deloitte Access

Economics team. Anthony has 25 years’ experience in a number of leading developers, fund managers and advisory groups.

06

2018 Real Estate Outlook |

Market and investment

Outlook investment trends

Future investment models such as build to rent and capital flows.

Although often used Build to rent Research suggests similar yields could

‘Build-to-Rent’ or ‘Multifamily’ as it is be achieved in the Australian market,

synonymously in the media, known in the US, is the terminology making the sector increasingly attractive

it is important to make the used to describe institutional rental to investors as domestic commercial yields

accommodation where the whole continue to compress to comparable levels.

distinction between ‘build to development is owned and operated

The lower yields on residential build-to-

rent’ and ‘affordable housing’, by developers or groups of investors.

rent by comparison to commercial assets,

as build to rent can include Despite being relatively new to Australia, have generally being offset by a strong

the concept of build-to-rent is well capital growth profile and diversification of

a range of product types at established globally; measuring $A319bn risk across the property lifecycle.

different price points, but in total, of which $A106bn is in the

Residential build to rent has typically

United States. For the 11 markets where

does not necessarily relate MSCI measures residential real estate,

become prevalent in markets with falling

affordability, higher population growth

to low-cost/government- annualised income returns range from

and constrained supply – all factors which

3.3% (UK) to 5.7% (Canada) over the past

subsidised rental housing. 14 years, with the US sitting in the top half

are applicable to the current Australian

property climate.

of the pack, averaging 5.2%.2

2. Property Council of Australia and MSCI - Australian Property Still Performing Strongly, while Build-to-rent

has Proven itself Globally

https://www.propertycouncil.com.au/Web/News/Articles/News_listing/Web/Content/Media_Release/

National/2017/Australian_property_still_performing_strongly__build-to-rent_has_proven_itself_globally.aspx

07

2018 Real Estate Outlook |

Market and investment

However, domestically there are a number Capital flows Foreign nationals are

of government policies and taxes which Foreign capital continues to play a key role

make the build to rent model prohibitive. in driving Australia’s economic growth. not permitted to buy an

In the traditional build-to-sell model, GST The latest Australia Bureau of Statistics established residential

is recouped at the time the product is sold, data highlights the total level of foreign

whereas this mechanism does not exist for investment in Australia (including real estate dwelling in Australia,

build to rent. Land tax can also be a financial and non-real estate sectors) increased by however they are allowed

barrier, where the total land value of the $153.3bn (5%) to reach $3,192.4bn for the

development is attributed to one owner, year ended 31 December 2016. Overall to purchase off the plan or

rather than distributed across multiple the United States continues be the biggest newly constructed buildings

owners in a strata scheme, and is therefore source of foreign investment at $860.9bn,

more likely to exceed the land tax threshold. representing 27% of the total foreign and rent, sell or live in them.

investment market (Chart 1).

That said however, with its demonstrated

success overseas, the build-to-rent model For the third consecutive year China This means that foreign

is beginning to gain momentum in Australia. represents the lion’s share of foreign real investors are more active

This is driven in part by interest from estate approvals, by both value and number.

offshore capital sources, which are generally Investment from China represents 26% of in certain sectors of the

more familiar with the concept. the total value of approvals and a growth residential property market,

of 31% since 2014-2015,3 according to the

The popularity of the sector will largely

Foreign Investment Review Board (FIRB). for instance large scale

depend on whether commercial yields

continue to compress to residential levels It is important to note that FIRB approvals apartment developments,

and whether build to rent will remain a data does have significant limitations, which are concentrated

competitive alternative. With the RBA cash the most important being that approvals

rate remaining at a historic low of 1.5% and do not represent actual purchases, predominately in inner

Deloitte Access Economics anticipating the but rather provide an indication of the Melbourne and Sydney and

cash rate will be on hold until well into 2018, planned future investment. As much

the outlook does looks positive. of the FIRB data is measured by value, to a lesser extent, Brisbane.

significant one-off proposed transactions

can distort the figures.

Chart 1 – The billion dollar levels, by leading countries, of the total foreign

According to the ABS, the leading investor

investment in Australia for year end 31 December 2016 countries for the year ended 31 December

2016 were:

1000 •• United States of America $860.9b (27%)

800 •• United Kingdom $515.5b (16%)

600 •• Belgium $270.1b (9%)

400

•• Japan $213.5b (7%)

200

•• Hong Kong (SAR of China) $100.9b (3%)

0

•• Singapore $98.9b (3%).

USA UK Belgium Japan Hong Kong Singapore

(SAR of China)

Source: ABS

3. FIRB Annual Report 2015-2016 (for the year ending June 2016)

08

2018 Real Estate Outlook |

Market and investment

Victoria has the market share of foreign investment at a state level, representing Australia’s appeal

44% of the total number of foreign investment real estate approvals (Chart 2). Australia’s supportive macro-economic

The FIRB’s report notes that three-quarters of all residential real estate approvals environment and robust real estate

were for purchases in Victoria and New South Wales. This is consistent with recent fundamentals are attractive to foreign

years and reflects strong demand for residential property in Sydney and Melbourne. investors chasing yield and the opportunity

to fill a local credit market gap.

Chart 2 – Number of approvals by state and territory

Banks dominate the Australian real estate

development debt market. However, they

VIC 44%

are actively reducing their exposure ($216bn)

NSW 32%

to commercial real estate lending, leaving

QLD 17% many developers struggling to obtain

WA 4% alternative funding.

SA 2% The banks represent more than 90% of

ACT 1% the market, mortgage funds are minimal

and private debt is inadequate, creating

TAS 0%

a significant dislocation in the real estate

NT 0% debt market. This gap in the market and

lack of competition presents an immediate

Source: FIRB opportunity for a large pool of capital to

capture the growing level of demand for

The residential real estate sector represented the largest share of foreign investment development debt.

value (29%) for the financial year ending June 2016, according to FIRB data (Chart 3) Provided the underlying asset class is sound,

Chart 3 – Share of total approvals by industry sector in 2015-16, by value then the current lending environment is

providing abnormally high returns, particularly

Residential real estate 29% in a low interest rate environment. The window

Manufacturing electricity and gas 23% of opportunity for these returns is anticipated

to be 24-36 months, before more normalised

Commercial real estate 20%

capital flows return to the sector.

Minerals exploration and development 11%

The most dramatic change in active debt

Services 9%

lenders is the mortgage fund sector. The

Finance and insurance 6% GFC saw the demise for mortgage funds

Agricultural forestry and fishing 2% in Australia, which effectively became the

‘shadow banking’ sector of the debt market.

Tourism 0%

At its peak the mortgage fund sector had

FUM of $18 billion. Today the mortgage trust

Note: Totals may not add due to rounding, Corporate reorganisations are excluded (99 in 2015-16 sector is estimated to have FUM $2 billion.

Source: FIRB)

Chart 4 – There has been a dramatic reduction in competition of active real estate debt lenders since the Global Financial Crisis:

Active lenders Major banks Regional banks Mortgage funds CMBS Private/family office Total

2008 4 12 60 4 4 84

2016 4 4 6 1 10 25

However Australia’s mature and The regulatory environment, lack of political movements results in Chinese investors

comparatively stable financial markets and and economic freedom and conditions in reconsidering what and where they can

well-regulated land title system does appeal the Chinese economy, make foreign markets afford to purchase, with the Australian real

to foreign investors. Similar markets such particularly attractive to Chinese investors. estate market looking increasingly attractive.

as New Zealand and Canada have likewise In 2016, the Chinese currency depreciated Australia’s gross rental yields of 4-5% in

become havens for global capital in recent nearly 5% against the US dollar, while major cities are twice that of China’s major

years, particularly for Chinese investors. appreciating against the Australian dollar cities (Chart 5).

by nearly 12%. The impact of such currency

092018 Real Estate Outlook |

Market and investment

Chart 5 – Median apartment prices and gross yields – December 2016

1200 6%

1000 5%

800 4%

600 3%

400 2%

200 1%

0 0%

Beijing Shanghai Shenzhen Sydney Melbourne Brisbane

Median apartment price (thousands AUD) Gross rental yeild (RHS)

Source:Bloomberg, ABS, CASS, Centaline, Domain, Credit Suisse

In China urban land is state owned with Housing acquisitions in Australia by

The most dramatic change

a 70 year lease to housing owners. In Chinese investors are typically below

contrast Australian real estate is mainly the US$5 million limit and therefore the in active debt lenders is the

freehold. Rural land in China is owned by restrictions on capital outflows introduced

mortgage fund sector. The

village collectives with limited competition by the Chinese government may not have

and as a result low price growth. China a large impact for Australia.5 GFC saw the demise for

also has a 30% deposit requirement on

mortgage funds in Australia,

residential real estate purchases (which

goes up even further for buyers looking which effectively became the

to purchase a second property),

‘shadow banking’ sector of

compared to 10% in Australia.4

the debt market.

Stephen Hynes, Deloitte Financial Advisory Partner, has more than 20 years’

experience in real estate, development, funds management and property finance.

Stephen has also held a variety of senior roles within Lend Lease and Macquarie Bank.

4. Deloitte Access Economics - Juwai.com, 8 May 2017. Here’s why domestic restrictions are driving Chinese buyers abroad. Available at: https://list.juwai.com/

news/2017/05/heres-why-domestic-restrictions-are-driving-chinese-buyers-abroad

5. Deloitte Access Economics - Altmann, E. & Yang, Z., 2 May 2017. Why Chinese investors find Australian real estate so alluring. Australian Broadcasting Corporation

(ABC). Available at: http://www.abc.net.au/news/2017-05-02/why-chinese-investors-find-australian-real-estate-so-alluring/8489686

102018 Real Estate Outlook |

Market and investment

A-REITs – Reflections on value

A-REITs are one of the most public faces of real estate in Australia, given the high level of corporatisation

of the sector. Below we consider some of the trends in the current market and recent movements.

In Australia, listed A-REITs can be classified The market's perception of the cost

into a number of subsectors: Retail (45% of risk has lowered

of market capitalisation of all A-REITs),

The figure below shows the trading

Office (12%), Industrial (12%), Diversified

premiums to NTA and the dividend yields

(27%) and Alternatives (4%). When

at which the A-REIT subsectors traded

considering the asset composition of

through 2016 and 2017:

Diversified REITs, they are largely weighted

to the Office and Retail subsectors.

Premium to NTA – median Dividend yield – median

60% 8%

50%

6%

40%

30%

4%

20%

10%

2%

0%

-10% 0%

Jun-16 Sep-16 Dec-16 Mar-17 Jun-17 Sep-17 Dec-17 Jun-16 Sep-16 Dec-16 Mar-17 Jun-17 Sep-17 Dec-17

Retail REITs Diversified REITs Industrial REITs Retail REITs Diversified REITs Industrial REITs

Office REITs Alternative REITs All A-REITs Office REITs Alternative REITs All A-REITs

10 yr AU gov bond

Notes: Diversified REITs are largely exposed to Retail and Office, with some

exposure to Industrial and Residential. Consequently, its performance is not

dissimilar to the specialised Retail and Office A-REITs.

Source: CapitalIQ, Company annual reports, Deloitte analysis,

While all A-REIT subsectors have generally This decline in capitalisation rates was Retail’s Amazon moment

traded at a premium to NTA since June largely influenced by investor (local and finally arrived

2016, performance across subsectors has foreign) demand for investments with a Over the second half of 2016 and first half

been mixed and the investment themes secure income yield, underpinned by a of 2017, the retail subsector experienced

have also been different. Despite this, the view that interest rates that are likely to an increase in valuations as capitalisation

cost of risk has lowered with property be lower for longer. At the same time, the rates decreased given the wide gap that

valuations reducing the gap to market market capitalisation was weighed down had formed relative to other more secure

capitalisation and the yield differential to by an increase in government bond yields property asset classes such as office.

government bonds reducing by 90 basis (circa 80 basis points) during the first half Consequently, the median NTA premium for

points (2.5% to 1.6%). of FY17 and headwinds in the retail sector retail declined over FY17 from 26% to 4%.

as noted below.

The property valuers continue to In the second half of 2017 there were

play catch-up Since June 2017, NTA premiums have started concerns over the impending arrival of

Over the period, the overall median to rise again driven by an increase in the Amazon and the pressure on consumer

premium to NTA reduced from 21% at June market capitalisation, reflecting a view, in spending driven by low wage growth, higher

2016 to 5% at June 2017. This was primarily our opinion, that there will be further, albeit cost of living and slower house price growth.

driven by NTA growth resulting from a broad small, reductions in capitalisation rates

based reduction in capitalisation rates in applied in the underlying valuations.

underlying property valuations.

112018 Real Estate Outlook |

Market and investment

Despite this, retail malls that were able to Development activity among the large Alternative A-REITs are being priced

offer an improved shopping experience players is strong but the uplift in office for lower interest rates

and diversity of tenant mix have been able property values hasn’t necessarily flowed Alternative A-REITs are invested across a

to partially mitigate the impact from online. through to the value of development range of property types such as storage,

The recent proposed takeover of Westfield assets and this has resulted in premiums rural, education, pubs, retirement,

by Unibail-Rodamco is testament to the to replacement cost being at historical international residential, hotels and social.

global capital markets’ confidence in the highs, particularly in Sydney. Such arbitrage These alternative property assets are

continued relevance of quality malls and provides scope for a rerating of businesses generally smaller, more ‘operational’ in

an acceleration of the consolidation that is with strong development pipelines. nature, have exposure to the same risks

occurring as a response to the online shift as their tenants and tend to have a more

Industrial’s Amazon moment has

and impact on consumer expectations. concentrated tenant mix, implying greater

also arrived

risk with valuations typically based on higher

Office is already low and now waiting The significant NTA premium for Industrial

capitalisation rates.

for uplifts on developments A-REITs reflects a number of factors

For office, NTA increased by 19% between including the structural demand for quality These A-REITs have traded at higher

June 2016 and June 2017 driven by industrial sites in order to achieve supply NTA premiums relative to the traditional

lower capitalisation rates and strong chain efficiencies in the shift to e-commerce, subsectors as investors pursue yield

fundamentals. Strong economic high portfolio occupancy rates, and a particularly in the current low interest rate

fundamentals and infrastructure recognition of the security of tenure of environment. With the increase in premiums

investment, particularly in east tenants. Goodman Group continues to over the second half of 2017, and subject

coast metropolitan cities such as receive due recognition for the successful to confidence in future improvements in

Sydney, combined with a withdrawal business and platform it has built and is an earnings, we expect to see reductions in

of older stock has resulted in below outperformer in this subsector and against capitalisation rates and discount rates,

average vacancy rates for prime space A-REITs in general. especially for assets with exposure to food,

and upward pressure on rents and ageing, health and capital city hotels.

increased earnings for office A-REITs.

A-REITs continue to play it safe on debt funding and are being rewarded

The figure below shows the gearing levels (net debt to book equity)

of the various A-REIT subsectors through 2016 and 2017.

Net debt to book equity – median

80%

70%

60%

50%

40%

30%

20%

Jun-16 Sep-16 Dec-16 Mar-17 Jun-17 Sep-17 Dec-17

Retail REITs Diversified REITs Industrial REITs

Office REITs Alternative REITs All A-REITs

Source: CapitalIQ, Company annual reports, Deloitte analysis

Gearing has been relatively stable across However, in our opinion, A-REITs with

the sector for some time, with the sector lower gearing tend to trade at higher

substantially recapitalising balance sheets premiums to NTA as there is more

post GFC. Median gearing on a net debt to scope to optimise equity returns via

book equity basis has reduced slightly to the increased use of debt.

below 40% over FY17.

122018 Real Estate Outlook |

Market and investment

Transaction activity

The graphs show the capital raisings and

M&A transaction activity in the listed

A-REIT sector since the June 2016 quarter.

A-REIT – Capital raisings by quarter A-REIT – M&A activity by quarter

2500 12 2500 12

10 10

2000 2000

No. of transactions

8 8

Capital raisings

1500 1500

AUDm

AUDm

6 6

1000 1000

4 4

500 500

2 2

0 0 0 0

Jun-16 Sep-16 Dec-16 Mar-17 Jun-17 Sep-17 Dec-17 Jun-16 Sep-16 Dec-16 Mar-17 Jun-17 Sep-17 Dec-17

Total value Capital raisings Total value No. of transactions

Source: CapitalIQ, Deloitte analysis,

Since the June 2016 quarter, A-REIT capital Ribbon Darling Harbour Project ($700 Earnings increases will highlight the

raising activity has largely occurred in the million, September 2016) and Generation high quality management teams and

retail sector with the $1 billion IPO of Viva Healthcare ($670 million, June 2017). platforms in place, but in particular, are

Energy in August 2016 and circa $650 million expected to be driven by factors such as

Outlook

capital raisings each by Vicinity, Westfield developments, operational efficiencies

On the back of strong performance in

and Scentre. The investment theme spilled and optimisation (through the increased

2016 and early 2017, we expect to see

over to industrial, with a $1.1 billion raising adoption of technology). The subsectors

continued strong performance by A-REITs.

by Goodman Group in September 2017 to watch will be the diversified, retail and

However, this will be driven by earnings

and the $500 million IPO of Propertylink in industrials over the short term and office

increases and consolidation among

August 2016. over the medium term. Notwithstanding

certain players, which is likely to be offset

its perception of being stable, we can

While M&A activity in the sector has been by the long awaited increase in interest

expect to look forward to more interesting

more subdued, the median NTA premium of rates towards the end of 2018.

developments in the sector.

deals since the June 2016 quarter was 15%,

with notable transactions relating to the

Tapan Parekh is a transactional valuation specialist Partner, in Deloitte’s Mergers

& Acquisitions practice. With more than 20 years’ experience, Tapan spent seven years

in the London office of Deloitte LLP advising clients in the European market on

valuation and related aspects. Value issues related to mergers, acquisitions, disposals

and restructurings as well as independent advice to directors and stakeholders is

Tapan’s bread and butter.

Alex Collinson is the National Lead Partner – Real Estate and Construction and

an audit Partner in Deloitte Australia. Alex has served global real estate and

construction companies across the world, and in Sydney, London and Toronto in

particular. He is a Member of the Property Council of Australia’s National Accounting

Committee and is Deloitte’s representative on the Property Industry Foundation (the

industry’s charitable arm).

132018 Real Estate Outlook |

Market and investment

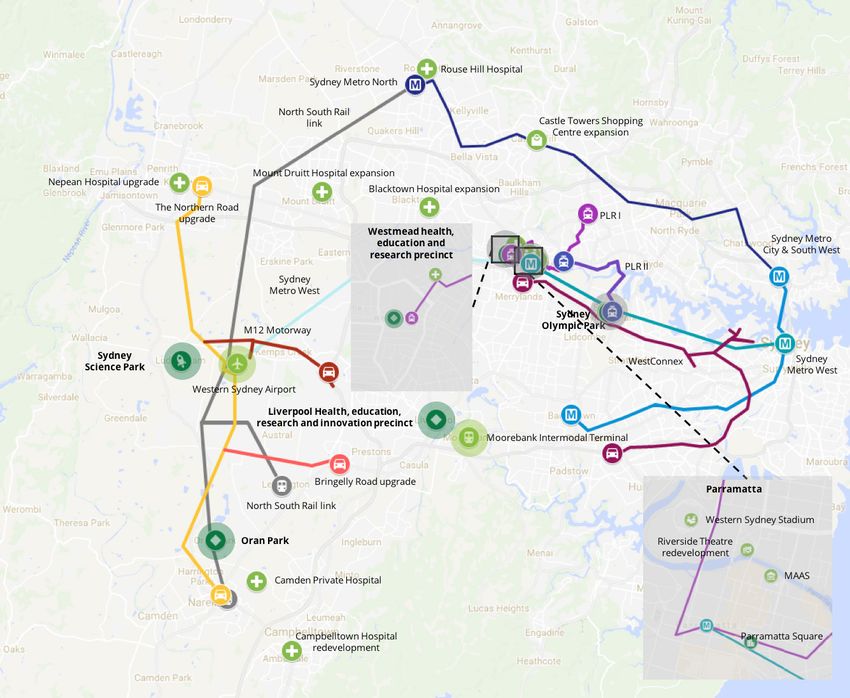

Western Sydney – Australia's development site

The surge in infrastructure development and real estate construction projects to accommodate

Sydney’s growing population has begun.

What is your Western Sydney strategy? Precincts and zones are emerging across As jobs and supporting infrastructure are

Over the past five years, Western Sydney the region, which are going to provide built, the demand for housing will continue.

has been in transition from the poor large-scale development opportunities, and Government policy decisions around land

customer to the big and shiny CBD to its lead to other local supporting development. release and planning approvals will be critical.

east to a region full of potential – with the Three better known examples include: the

The nature of the housing product provided

promise of becoming a key real estate, health precinct being created across the

should diversify as well, catering to the new

development and construction hub. South West; the aerotropolis envisaged

breed of locally based, well-paid workers. This

adjacent to the airport to house advanced

Back when people would ask: ‘Why are you will create a need for density along the new

aerospace and defence companies; and the

in Western Sydney?’ there was a stirring metro, rail and motorway corridors, and more

continued growth in industrial and logistics

recognition of the need for Western Sydney premium quality housing.

facilities around the Moorebank intermodal

to thrive in order to unlock the economic

terminal along the M4/M7 corridor.

potential in NSW, and potentially Australia.

This was also driven by the need to

accommodate our growing population.

In the following article we set out some of the key themes playing out across the region and

Today, we have moved from ambitious highlight some of the major infrastructure projects.

concepts to more practical

Infrastructure projects across the Western Sydney region

plans, many of which are under

construction. A number of major

government-backed infrastructure

projects are already underway and

others are progressing through the

planning process. These large-scale

projects are injecting confidence into

the private sector to invest in the region

through all forms of development.

A more integrated planning environment

has also helped, with the creation of the

Greater Sydney Commission and the

release of the integrated Future Transport

Strategy for NSW.

The question we

now ask, is not,

‘why are you in

Western Sydney?’

but how can you

afford not to be?

142018 Real Estate Outlook |

Market and investment

Seize the opportunity in Any concern of apartment oversupply The potential development outline within

Western Sydney in Parramatta CBD appears to be the Sydney Olympic Park Master Plan 2030

The real estate development and overblown as developers react to the will transform the area to include a mixed

investment community is constantly ‘cooler’ market conditions with a 59% residential and office precinct with 23,000

seeking opportunities in growth areas. decrease in DA-approved apartments, new residents, 34,000 new jobs by 2030,

The challenge is to identify and secure these compared with those currently under new schools catering for 5,000 students,

opportunities before your competitors. The construction for the period 2017 to 2018. all complemented by investment in leisure

boom in infrastructure project spending and and retail.

Infrastructure

investment by the private and government

With the proposed Parramatta Light Rail

sectors in Western Sydney is a catalyst for

and Sydney Metro West, the new transport

‘Seizing the opportunity

real estate and development opportunities.

While these projects are not a secret, the

system will deliver both interconnectivity early in a strategic Western

within Greater Parramatta to the Olympic

advantage is to be gained through smart

Peninsula region by 2023. It has also

Sydney location is likely to

timing. Western Sydney is a long-term play

and opportunities are plentiful.

improved routes to the Sydney CBD, with deliver above average capital

travel times down to less than 20 minutes

between Parramatta CBD and Sydney CBD.

growth in the medium term’.

Locations with current The Greater Sydney Commission has

Investment in Parramatta’s cultural

and planned concentrated precinct will attract more visitors to the

recognised the park as a precinct that

forms part of Greater Parramatta to the

investment and area. It will also include the proposed

Olympic Peninsula region and Stage 1 Light

move of the Museum of Applied Arts

development activity. and Sciences (MAAS) to the Parramatta

Rail will provide improved connectivity to

Parramatta CBD and Westmead Health

riverbank, planned expansion of

Parramatta CBD Parramatta Riverside theatres, and a

and Education precinct once completed,

expected in 2023.

30,000-capacity Western Sydney Stadium.

Statistics

The new Sydney Metro West line will

Parramatta is located approximately 25 As this expected increase in workers and

connect Sydney CBD and Parramatta, and

kilometres west of the Sydney CBD. It visitors materialises there will be a gap in

will stop at Sydney Olympic Park. Travel

is four times the size of Perth city. The the market for short-term accommodation.

times to the Sydney CBD will be halved to

Parramatta Central Business District is the Currently 857 new hotel/serviced

about 20 minutes.

second largest employment destination apartment rooms are expected to be built

to the Sydney CBD in NSW, and is growing by 2020 in Parramatta CBD, to service It will include three precincts – Stadia,

rapidly. the Parramatta CBD as well as the wider Central and Parkview that will capture

western Sydney precincts. the benefits from the recently announced

Parramatta Square is a $2bn city centre

rebuilding of ANZ Stadium. This will

renewal project, with 135,000m2 currently

under construction across three new office

Parramatta’s vision to provide civic, retail, and other amenities in

the heart of town centre, and will lead to

projects. Pre-committed tenants include create future growth and the construction of a low-rise residential

NAB, NSW Department of Education and

the NSW State Government. Approximately

opportunities, and become neighbourhood.

30,000 workers will be moving into the an even more liveable city, Stage 2 of the Parramatta Light Rail

Parramatta CBD by 2020. Parramatta CBD will improve connectivity, with a direct

office vacancy for ‘A’ grade buildings is

is finally being realised, connection to Parramatta CBD.

currently at ‘0%’. with benefits from multiple The Sydney Olympic Park will continue to

The high-rise and higher quality projects projects now underway. evolve and provide ample development/

introduced into Parramatta CBD over investment opportunities under the future

the last five years have triggered strong vision of the Masterplan 2030, with the

residential development activity.

Sydney Olympic Park Sydney West Metro, the major enabler

Developers are invested in Parramatta CBD Sydney Olympic Park (SOP), which is of growth of this precinct in the Western

in the medium to long term, with a strong located just 15 kilometres west of the Sydney region.

pipeline of residential and mixed-use Sydney CBD, houses Australia’s largest

projects at the proposal stage. sporting and entertainment precinct, which

has now matured into both residential and

commercial office locations, with significant

expansion plans.

152018 Real Estate Outlook |

Market and investment

Western Sydney Airport Liverpool and South West The health precinct will be complemented

by the emergence of new university

Western Sydney’s Airport project will be Liverpool’s vision is to re-activate its city campuses in Liverpool, that are expected

going ahead and is due for completion centre by ‘anchoring’ the Liverpool Civic to accommodate up to 9,500 new students.

by 2026. It is a unique opportunity for Place project at the southern end of the The University of Wollongong recently

Western Sydney to house Sydney’s second city (opposite end of the current Westfield completed its South Western Sydney

international airport. There will be flow-on shopping centre and Liverpool Hospital). campus, while Western Sydney University’s

benefits to the region as the development The project is scheduled to take four years. Liverpool campus, is currently under

of the ‘Aerotropolis’ will incorporate New council offices and chambers, a civic construction, with completion expected

residential, industrial and commercial plaza, amenities, as well as student, hotel, early this year (2018).

development around the airport and so and residential accommodation, are all

benefit the whole region. It is proposed planned. The investment by Liverpool Sydney Science Park

to be a 24-hour airport. Council is around of $75m.

Sydney Science Park is set over 280

The airport site at Badgerys Creek is The South West and Greater Macarthur hectares and is located in the strategic

located in Western Sydney near the New region of Western Sydney continue to ‘Western Sydney Priority Growth Area’

South Wales Government's Western be areas supplying significant housing at Luddenham. With convenient access

Sydney Employment Area, the Western growth, with detached housing in release to both the M4 and M7 motorways, it is

Sydney Priority Growth Area, and the areas and in Liverpool, Campbelltown and three kilometres north of the new airport

South West Priority Growth Area. other areas adjoining stations along an at Badgerys Creek, and 24 kilometres west

extension to the new railway line. of Parramatta. The project value is $5bn

The Western Sydney Infrastructure Plan

outlines future transport infrastructure The growth of housing in these areas is and and is expected to deliver a community

including the ‘M12 Airport Motorway’ supported by the NSW Department of that will create more than 12,000 jobs,

extending from Liverpool to the airport Planning which has identified five priority 10,000 students and be home to more

and connecting into the existing M7 precincts (out of a total of 30) that lie than 10,000 residents.

Motorway. Also under construction is a within the south western region of Sydney. Stage 1 Masterplan has been created and

$509m, two stage upgrade to Bringelly These include Glenfield, Leppington Town interest has been received from Birling

Road, which connects into the Northern Centre, Greater Macarthur Growth Area, National Avian-Laboratories Centre; CSIRO’s

Road leading past the airport. South Creek West and Western Sydney First Dedicated Innovation Zone and ‘Urban

Airport Growth Area. Living Lab’ in NSW; and Catholic Education

The NSW government is exploring six

options to connect the Western Sydney With the evolution of the Campbelltown Diocese of Parramatta – delivering NSW's

Airport with rail infrastructure to and Liverpool health, education and first STEM-inspired school.

Sydney Metro line. It is also proposed at research precincts, the South West will Conclusion

some stage to establish vital transport become an advanced medical hub for The growth potential for Parramatta,

infrastructure to the future airport. NSW/Sydney, with a residential corridor the Western Sydney Greater Region,

and transport and logistic centre. and the Greater Parramatta to the

The opportunities will become

clearer as planning progresses The existing health precinct in Olympic Peninsula region is significant.

and construction commences. Liverpool will be expanded by the The growth potential is very exciting and

development of Camden Private the opportunities that it will create will be

Hospital, and Stage 2 redevelopment game changers for NSW.

of the Campbelltown Hospital.

David Hagger leads Deloitte’s Western Sydney Real Estate and Construction

practice. David is chairman of the Western Sydney Committee of the Property Industry

Foundation. David works in corporate finance, servicing a range of corporate, private

and government clients.

Fred Ibrahim is a Director and forms part of the Real Estate Advisory and Consulting

team with a focus on Western Sydney clients. Fred has over 18 years’ of experience,

specialising predominately in property valuation and advisory services.

162018 Real Estate Outlook |

Market and investment

Top 10 infrastructure developments across the region

Status: Under construction

Capital value: $16.8b

Westconnex Start date: 2015

Expected completion: 2023

Status: Under construction/committed

Capital value: $12b

Sydney Metro City & Southwest

Start date: 2017

Expected completion: 2024

Status: Proposed

Capital value: $10.4b

Sydney Metro West

Start date: 2017

Expected completion: 2024

Status: Under construction

Capital value: $8.3b

Sydney Metro Northwest

Start date: 2014

Expected completion: 2019

Status: Proposed

Capital value: $5.3b

Western Sydney Airport

Start date: 2018

Expected completion: 2026

Status: Proposed

Capital value: $3.4b

Parramatta Light Rail I & II

Start date: 2018

Expected completion: 2023

Status: Under construction

Capital value: $1.9b

Moorebank Intermodal Terminal Start date: 2017

Expected completion: 2020

Status: Under construction

Capital value: $1.6b

Northern Road upgrade

Start date: 2016

Expected completion: 2020

Status: Proposed

Capital value: $1.25b

M12 Motorway

Start date: 2020

Expected completion: 2023

Status: Proposed

Capital value: $1.25b

ANZ Stadium Start date: 2019

Expected completion: 2022

172018 Real Estate Outlook |

Technology

Why should companies focus on Real Estate

fintech startups?

Technology startups seem to be here to stay.

Rapid advancements in technology have While venture capital (VC) remains

Globally, real estate fintech

lowered entry barriers for tech startups. the dominant funding source, there

Over the past 15 years, the cost of is substantial capital flow from non- startups increased by

establishing an internet-based startup VC investors as well, including REITs,

18% from 246 in 2008

has plummeted from $3 million in the established real estate services

1990s to just $300 today ,6 causing them companies and investors, private equity to 1,372 by 2017.

to become more synonymous with firms and high net worth individuals.

disruption and innovation.

In the five-year period between 2011

This has also meant exponential growth in and 2016, funding from non-VC sources

the real estate sector. Globally, real estate for real estate tech startups increased at a

fintech start ups increased by 18% from compound annual growth rate (CAGR)

246 in 2008 to 1,372 by 2017.7 In the same of 72.4% to $2.4 billion in 2016.9 And there

period, cumulative investments soared is an all-time record funding of $3.4 billion

from $2.2 billion to $31.3 billion.8 YTD, as of July 25, 201710.

6. “Disrupting the Disruptors: Startup Accelerators Feel Pressure to Evolve”, Knowledge@Wharton, University of Pennsylvania, July 28, 2016, http://knowledge.wharton.

upenn.edu/article/why-startup-accelerators-are-feeling-pressure-to-evolve/.

7. Venture Scanner database, data as of July 31, 2017.

8. Ibid.

9. Ibid.

10. Ibid.

182018 Real Estate Outlook |

Technology

See the NUMPERSPEAK chart over for Large crowdfunding firms, such as Fundrise Where should companies start?

more details. and RealtyMogul, have been key proponents Traditional real estate companies can

of eREITs so far.13 Even companies such as benefit by engaging with these startups

We categorise real estate (RE) tech

RealtyShares provide similar investment in different ways. Companies can make

startups into two groups – RE operations

opportunities in the Construction and Real choices based on their investing capacity,

and RE fintechs.

Estate sector as they seek to potentially the utility of a startup’s services, their need

•• RE operations – The operations-related compete with traditional REITs. As such, RE for financing, and so forth. As end users,

tech startups focus on the core real Fintech startups comprise only 5% of the real estate companies can leverage some

estate business such as property search, overall global real estate tech startup space of the online services and solutions for key

leasing, facility management, smart by investments, having raised $1.4 billion property-related decisions.

building technologies, and home services. to date. But they are certainly disrupting

Companies can also access capital by

traditional business models.14

•• RE fintechs – Our focus area of using the innovative funding and investing

discussion, are enabling financing and But this is not just an overseas story with platforms that RE fintechs have to offer.

investments in real estate. They offer investment and innovation in Australia. Alternately, they could also partner with

diverse services and solutions such as Examples include BlochExchange and the RE fintechs to help meet their financing

real estate transaction services, digital BrickX (fractionalised property trading and investment needs. Finally, real estate

lending platforms for construction and platforms) and the emergence of foreign companies can invest in the RE fintechs

real estate owners and lenders, online entrants into the local market, such as and benefit through their growth.

real estate investments options for Purple Bricks, challenging traditional

RE fintechs’ services

individuals, or investments in single- residential real estate agents.

Construction and real estate owners,

family homes for institutional investors.

How to benefit from RE fintechs? developers, and investors can use RE

The general notion was that startups would There are many ways in which traditional fintech platforms for a variety of services

threaten incumbent real estate companies. real estate companies can benefit from the – including leasing, acquisition, disposition

Certainly with the help of technology, they solutions offered by RE fintech firms. They decisions, and managing the underwriting

absolutely offer innovative solutions and can provide platforms that can expand and process, and accessing detailed financial

enhanced user experience at a relatively diversify the lender base and enable more models for property financing.

lower cost, faster pace, and user friendly individuals and institutions to get exposure

environment. However our research shows The most obvious and key benefits would

to real estate.

that while they were initially thought to be be efficiency and convenience, as these

a competitive threat, they have been more This is especially useful for US-based online and sharable solutions have the

about changing the pace of innovation than companies, which face a challenging capability to provide analysis faster, more

taking the place of the incumbents. financing environment, where traditional cheaply, and efficiently.16 As an example,

lenders such as banks are tightening lending Assess+RE provides cloud-based services

Take the case of startups that directly standards and CMBS issuances remain such as property level valuation models

compete with REITs by providing online well below their historical highs due to the and related financial analysis.17

investment avenues for individuals to implementation of the new regulations

invest in commercial real estate in the following the 2008 financial crisis. In light

US.11 Also called eREITs, their solutions of the fact that the global online lending

combine the features of nontraded REITs industry is expected to grow from $40

and crowdfunding, with lower fees.12 But billion in 2016 to more than $1 trillion in the

unlike traditional crowdfunding ventures, next five years, the growth in construction

eREITs offer multiple and diversified asset and real estate financing may very well be

lending services. led by these RE fintechs.15

11. Fundrise website https://fundrise.com/, accessed on August 4, 2017.

12. Ibid.

13. Fundrise website https://fundrise.com/; RealtyMogul website https://www.realtymogul.com/, accessed on August 4, 2017.

14. Venture Scanner database, data as of July 25, 2017.

15. Beth Mattson-Teig, “How is the CRE Industry Adapting to the Emergence of Fintech Solutions?,” National Real Estate Investor, April 25, 2017.

16. Assess+RE website https://www.assessre.com/index.html, accessed on August 4, 2017.

17. Ibid.

19You can also read