2020 North Sea Appraisal and Option to Acquire Western Canadian Production - i3 Energy

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

2020 North Sea Appraisal and Option to Acquire Western Canadian Production

: MARCH 2020 i3 ENERGY (LON:i3E)

Forward looking statements

This presentation contains forward-looking statements and information that both represent i3 management's current

expectations or beliefs concerning future events and are subject to known and unknown risks and uncertainties.

A number of factors could cause actual results, performance or events to differ materially from those expressed or implied by

these forward-looking statements.

Unless otherwise stated, references to reserves, resources, production, and economic figures are based on i3 management’s un-

risked Mid-case estimates. They are preliminary figures and are subject to change. All plans are subject to i3 funding capacity.

: MARCH 2020 2

Highlights

UNLOCKING 2019 drilling programme has proven a material oil discovery at Serenity (c.200 MMstb

POTENTIAL STOIIP) and has de-risked oil migration towards Liberator West (c.400 MMstb STOIIP).

Minimum 82-day drilling contract executed with Dolphin Drilling to conduct 2020

appraisal campaign. i3 has agreed partial economic farmout of up to 10% of future net

2020 FARMOUT revenues associated with Block 13/23c to Dolphin in exchange for their 2020 drilling

AND APPRAISAL contribution of up to US$14.4 million. Farmout process remains ongoing with parties in

i3’s data room.

i3 has purchased the junior and senior secured debt of Toscana Energy Income

WCSB Corporation (TSX:TEI) from its cash resources and has executed an option agreement

PRODUCTION to acquire 100% of TEI’s shares for c.4.4 million i3e shares (total i3 dilution of up to

4%), purchasing 4.65 MMboe 2P and 1,065 boepd of production (55% oil) with potential

ACQUISITION(1) upside of 100+ MMbbls recoverable, for a total consideration of C$3.95 million.

Integration of Toscana’s high-quality management team will enable rapid expansion

GROWTH into the opportunity-rich WCSB. i3 will remain focussed on proving Serenity and

FOCUSED Liberator resources while low-cost Canadian production opportunities are captured to

provide operational cash flow and near-term shareholder distributions.

1) 2P Reserves from Toscana’s 2019 Year-end Reserves Report; 2019 average production (actual)

: MARCH 2020 3

UK North Sea Update

Planned 2020 Drilling Activity and Economic Farmout

: MARCH 2020 4

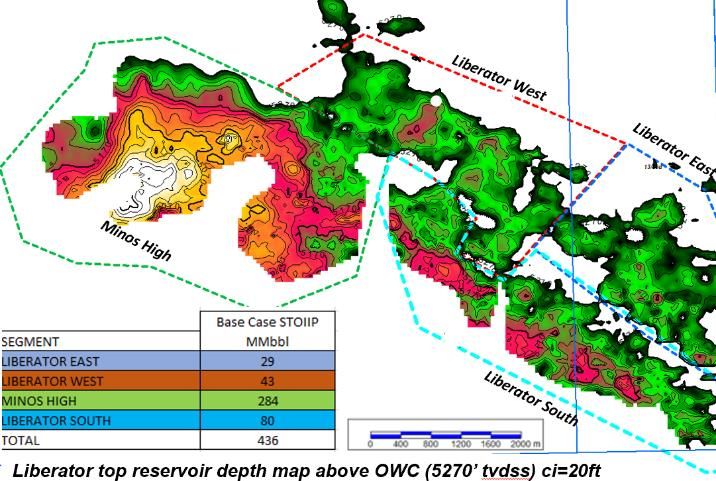

Assets: 100% WI in Serenity and Liberator

Serenity Oil Discovery Serenity Discovery

Tain Discovery

• Successful 13/23c-10 well discovered

oil in October 2019 in the world class

Captain sands reservoir

• i3 estimates 197 MMstb STOIIP based

on conservative oil column thickness

• Serenity is an amplitude supported

feature mapped by i3 as an extension

of the Tain oil field 13/23c 13/23d

• Tain discovery encountered 32° API

i3’s 100% operated interest

oil, subsequently appraised by three in 13/23c and 13/23d

wells (well 13/23b-5z tested at 6700

bopd)

Serenity Discovery

Liberator Appraisal

• 100% i3 operated working interest

• Fluid and reservoir properties

analogous to neighbouring prolific

Blake field in the Captain sands fairway

• 2019 appraisal critically proved oil

migration towards Liberator West

where relief and column height could

hold large in-place resources

• Material upside in Liberator West of

c.400 MMstb STOIIP to be appraised

following Serenity

• Phasing and timing of development

dependent on future appraisal results Post 13/23c-11 mapping

: MARCH 2020 5

2019 drilling campaign (video here)

Drilling began August 2019 using Dolphin’s Borgland Rig

• 13/23c-9 well missed expected Liberator structural high

• Upper Captain sands pinched out at 13/23c-9 location

• Provided critical vertical seismic profile which was subsequently

tied to recently reprocessed broadband seismic, resulting in

remapping of the Liberator field

• 13/23c-10 well confirmed material Serenity oil discovery

• Well found 11 feet TVD of clean, oil-filled, turbidite Captain

sands

• 13/23c-10 confirmed i3’s prognosed OWC at 5270 ft TVDSS

• Estimated STOIIP of 197 MMstb assumes a 40 ft net thickness;

expected 50% recovery factor yields potential recoverable

resources of c.100 MMbbls

• Serenity could be produced as a phased development across

existing proximal infrastructure followed by a subsea tie-back to

a dedicated FPSO or alternate local infrastructure

• 13/23c-11 Liberator Phase I appraisal well

• Found 220 ft MD of Captain sand confirming the presence of

the Liberator channel west of the 13/23d-8 discovery well

• Confirmed thin oil column above regional OWC at 5270 ft tvdss

• Residual oil column beneath the OWC partially mitigates oil

migration risk towards Liberator West

• Drilling Performance

• Excellent operational performance by Dolphin Drilling, Petrofac

Well Management, Baker Hughes and other well service

providers

• All three wells drilled safely with no environmental, health or

safety issues and all within budget

Ian Little, i3’s Drilling Manager on inspection visit to the Borgland Dolphin semi-sub rig

: MARCH 2020 6

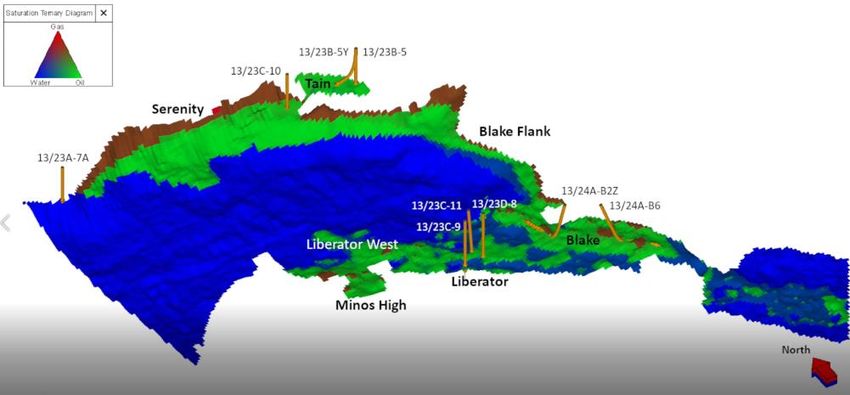

Serenity oil discovery (oil migration video here)

Serenity Discovery 2020 Appraisal Programme and Economic Farmout

• Serenity oil discovery at well 13/23c-10 (“S1”) announced • Drilling contract and net revenue sharing agreement executed

October 2019 with Dolphin Drilling

– Drilled down dip of RSRUK-operated Tain oil field (Tain – Drilling contract executed for minimum 82-day drilling

discovered in 2005, 32° API oil, flow-tested 6,700 bopd) programme expected to commence in Q3 2020 (subject to

funding)

– 13/23c-10 well encountered oil in a sequence of Captain and

Coracle sands – Dolphin drilling will receive up to a 10% net economic interest in

Block 13/23c in exchange for committing up to US$ 14.4 million

– Oil confirmed within the interval from 4740 ft to potentially

towards i3’s 2020 appraisal drilling programme

5252 ft TVDSS, 165 ft TVD sand in total

– Initial 82-day programme will focus on Serenity (two wells plus

– Net oil interval in the Captain sand was c.11 ft of high porosity

sidetracks) w/ additional two-well option totalling 78 days for

(30%) sand, thicker than in the up-dip Tain discovery as

drilling Liberator West and/or the Minos High

prognosed by i3; preliminary biostratigraphic analysis confirms

the net sand is the same as the Tain Captain sand – Wells to penetrate and delineate thickened Captain reservoir to

the West with flow test to demonstrate productivity

– An OWC was estimated at 5270 ft TVDSS using pressure

measurements, which is the regional contact seen in the – Farmout process ongoing with parties in i3’s data room

Liberator and Blake fields

– Proved on-block oil column of 622 ft TVD present in the Captain Liberator–Blake–Tain–Serenity Structural Setting and Fluid Distribution

sand

• i3-estimated P50 STOIIP of 197 MMstb based on conservative

assumptions regarding oil column thickness

– i3’s expectation is that the Captain sands thicken to the west in

Serenity as demonstrated by the c.120 ft of sand seen in the

offset 13/23a-7A (Magnolia) well situated to the west of the

field

– The P50 STOIIP of 197 MMstb assumes an average oil column

thickness of 40 ft across the field

– Due to the high relief above the OWC in the Serenity field,

recovery factors in excess of 50% should be possible

: MARCH 2020 7

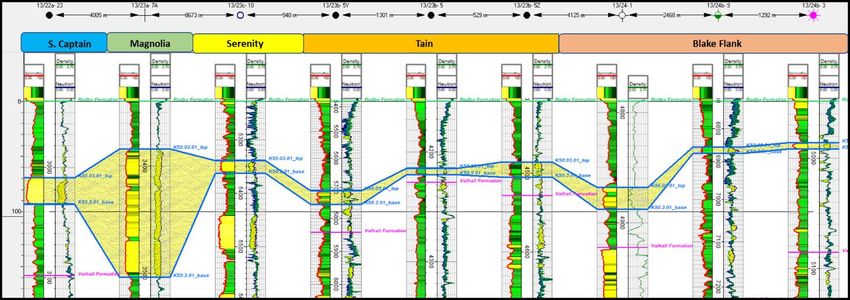

Well correlation Magnolia-Serenity-Tain-Blake Flank

8673 m

Note: Distances between wells are not to scale

Magnolia well

Serenity well

Tain wells

Significant upside potential in sand thickness

• The oil-bearing Captain sand found in the Serenity discovery S Captain well

well can be mapped off the 13/23c block to the west in the Blake Flank

Captain and Magnolia wells, through Serenity, Tain and the wells

Blake Field to the east.

• i3 expects the sand thickness in Serenity to increase to the

west, ranging from 11 ft (found in the 13/23c-10 Serenity

discovery well) to 120 ft (found in the 13/23a-7A Magnolia

well). 197 MMstb of STOIIP is based on a conservative

assumed average sand thickness of 40 feet.

: MARCH 2020 8

i3 Option to Acquire

Toscana Energy Income Corporation (TSX:TEI)

Capitalizing on Cash Flow

Assets in the Opportunity Rich

Western Canadian Sedimentary Basin

Toscana Energy: low-cost WCSB production acquisition

i3 Purchases Debt & Executes Option to Acquire TEI’s Equity 1000+ boepd from 255 (175 net) low-decline production wells

• i3 has acquired all debt of Toscana Energy Income Corporation

(TSX:TEI) and executed an option agreement to acquire 100% of TEI Nipisi

– From its cash resources, i3 purchased all rights and interests in TEI’s Clair

Hangingstone

C$24.8MM senior and C$3.2MM junior debt facilities for C$3.0MM and Marten Creek

C$0.4MM, respectively, paid 50% up front and 50% at year-end

– Upon exercise of its option, i3 will offer up to 4,399,224 i3 shares

(valued at C$0.55MM on March 27th) for the entire share capital of

Tony Creek

Toscana, resulting in up to c.4% dilution to i3’s current shareholders Bigoray

• Total cash and share consideration of C$3.95MM (US$2.8MM) buys:

Willesden

– 2019 production of approximately 1065 boepd at C$3710/boepd Green

Nevis

(US$2650/boepd) or 0.72x TEI’s 2019 field netback (revenue minus

Strachan

royalties minus opex) of C$5.5MM (US$3.9MM)

– 2P reserves of 4.65 MMboe for C$0.85/boe (US$0.61/boe)

– Long-life reserves base from low-decline well stock with 2019 average

field break-even of C$30.43/boe (US$21.74/boe) Carmangay

Weyburn

– TEI’s highly experienced team and operational organization Retlaw

– A secondary listing on the Toronto Stock Exchange

• Optimization opportunities within current portfolio to increase

YE Reserves(1) P+PDP 1P 2P

production (boe/d) by 20% - 50% through low-cost workovers or capex

• Potential company-making upside in Toscana’s Clearwater acreage, one

MMboe 2.67 3.48 4.65

of Canada’s top oil plays, with potential recoverable resources above

100 MMbbls net

BTAX NPV10

• Access to high-netback and/or distressed deal-flow provides opportunity $30.2 $32.3 $43.2

(C$MM)

to rapidly grow i3 into a business that generates significant free cash

flow

ATAX NPV10

• i3 expects to execute its option to purchase Toscana after releasing its $30.2 $31.5 $40.3

(C$MM)

2019 Annual Report

(1) Source: Sproule 2019 Toscana Year-end Reserves Report (excludes any potential upside from Clearwater acreage)

: MARCH 2020 10Strategic rationale for i3’s acquisition of TEI

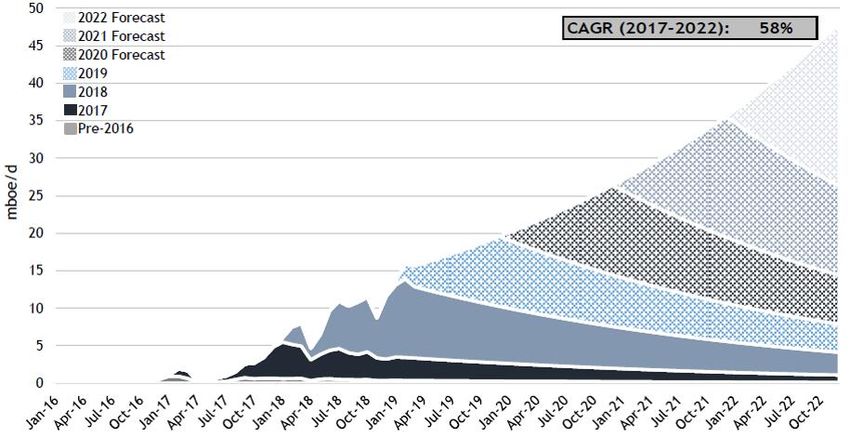

Diversification into a Production-based Portfolio 10-year Production Profiles(1)

• i3 deems it critical to spread and mitigate its

historical single-asset risk

• TEI’s low-decline production portfolio expected to

provide stable long-term cash flow under

attractive acquisition metrics making it a highly

accretive transaction for i3’s shareholders that

can be funded from cash

• Excellent acquisition metrics: 2019 WCSB M&A

and A&D transaction averages place approximate

acquisition value on TEI (55% oil) of over C$30

million on a flowing basis

• Optimization works identified within TEI’s current

production portfolio to increase production by

20% to 50% during 2020

10-year BTAX Cash Flow (MM$C)(1)

• Toscana’s 46 net sections of acreage atop the

Clearwater formation could potentially provide

many multiples of current portfolio value

• i3 is inheriting an experienced Calgary-based

management team with proven M&A credentials,

TSX listing and WCSB presence that will provide

access to other low-cost, high-return

opportunities

• The WCSB is currently out of favour due to egress

issues, a lack of access to capital, and

overleveraged but solid asset portfolios, providing

what i3 believes to be a time-limited opportunity

to grow a material production company on

favourable terms

: MARCH 2020 (1) Source: Sproule 2019 Toscana Year-end Reserves Report (excludes any potential upside from Clearwater acreage) 11Toscana’s Clearwater Formation in Marten Hills & Nipisi

A Premier Economic Play Type in AlbertaClearwater development history

• A top tier economic oil play found in the WCSB Alberta

– Shallow drill depths (400m to 650m)

– 4-8 leg open hole multi-laterals with 20-50m spacing

– No stimulation required

• Activity continues to surge

– ~ 150 wells have been spud since the beginning of 2016

(~60% occurring within the past 12 months)

– Current production (Jan 2020) has grown to >20,000 bbl/d

(>70% YoY) Saskatchewan

– Prolific development potential in a low F&D, high netback

resource play

• Delivers significant sustainable growth

• Key play participants include:

– Public companies Canadian Natural Resources

(CNQ),Cardinal Energy (CJ), Cenovus Energy (CVE) and

Highwood Oil Company (HOLC)

– Largely dominated by privates, including Spur Petroleum

(majority of production), Deltastream Energy, Crestwynd

Exploration, Mancal Energy, Rolling Hills Energy, Summerland

Energy, Turnstone Energy and Woodcote Oil

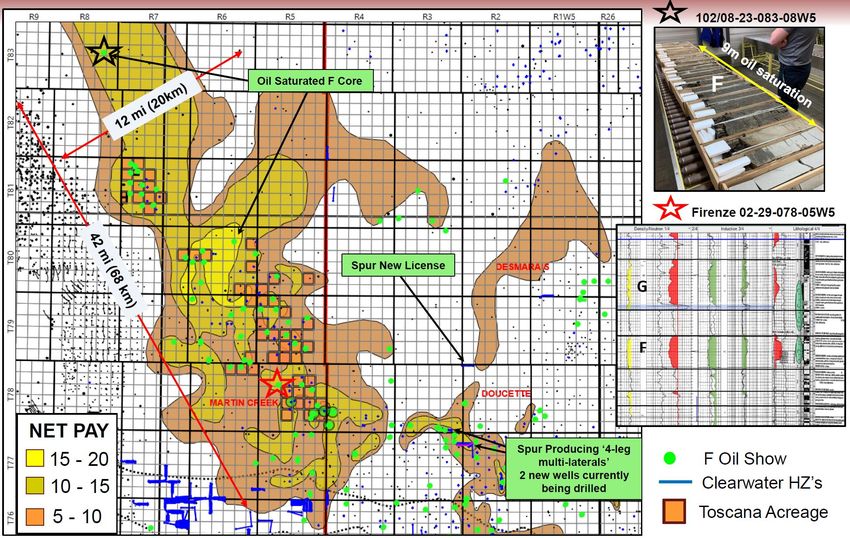

: MARCH 2020 13Clearwater F sand – oil saturated fairway

: MARCH 2020 14Asset attributes and potential development plan

• 57.6 gross (45.9 net) sections of Clearwater rights (80% avg WI)

• Majority of acreage is held-by-production

• Play fairway - 12 x 42 mile corridor with net pays >5 meters

• Competitive advantage

– Toscana has grandfathered access & right to drill in caribou range

(prior to recently implemented restrictions on mineral rights licensing)

– 166 surface pads on Toscana Lands

– Existing Clearwater well bores on all key sections

– Utilize existing infrastructure and well penetrations to de-risk future

capital spend

– >150km of operating pipeline infrastructure

• Sampling campaign (Winter 2019/20)

– Obtain oil samples throughout field – shoot/swab. Analyze live oil that

has been documented in pig traps, separator dumps and tanks

– Ascertain which samples belong to which well and sand layer

– Test oil samples for API quality, Sulphur content and viscosity

• Continue mapping individual sand layers (Winter 2019/20)

– Net pay / isopach

– Structure

• High grade drilling locations (Spring 2020)

– With mapping, sampling and continued offset operator de-risking

• Implement C$5-C$8MM, 4 to 6 well, drilling campaign (Winter

2020/21)

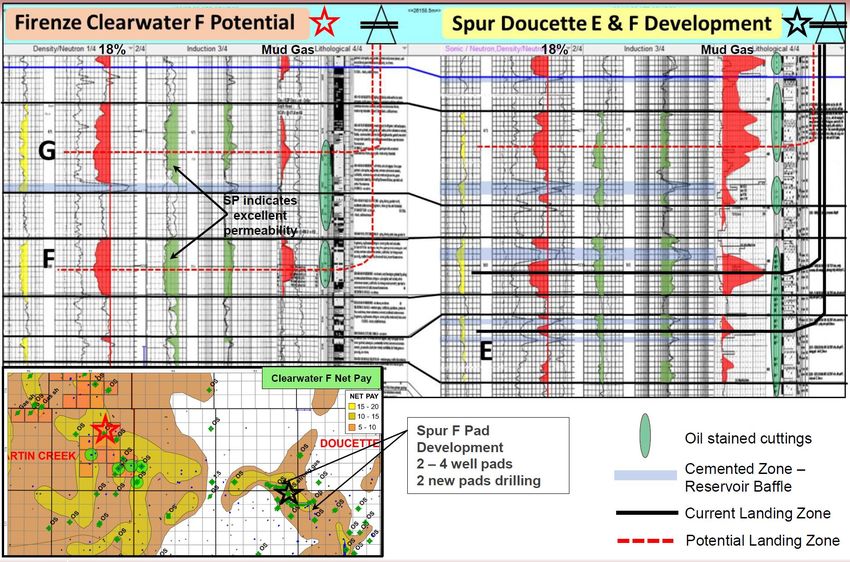

: MARCH 2020 15Clearwater geological summary

• Clearwater characterized as conventional reservoir

– Targeting marine deltaic and shore face deposits in the Upper Mannville

– Well consolidated oil-bearing formation ranging in net thickness from 5 to 35 meters in up to 8 zones

– Conventional permeability (50-1,000 mD), significant porosity (25-30%) with low water saturation (D & E Development / G Contingent Resource : MARCH 2020 17

Marten Creek and Nipisi STOIIP analysis(1)

• STOIIP of 24.2 MMbbls/section

• Acreage position (45.88 net sections)

supports STOIIP of 1.11 Bbbls

• Primary recovery:

– Assuming primary recovery of 5% = 1.21

MMbbls/section @ 4 wells (8 legs per) = 300

mbbls per well

– Total recoverable reserves of 55.5 MMbbls

• Secondary recovery:

– Assuming secondary recovery (EOR - water &

polymer floods) of 10-15% = 2.4 – 3.6

MMbbls/section @ 4 wells (8 legs per) = 625

– 900 mbbls per well

– Total recoverable reserves of 111.0 – 166.5

MMbbls

1) Toscana’s management view

: MARCH 2020 18Marten Creek and Nipisi type well economics

140

High Case Type Well Low Mid High

Mid Case DCET Costs*

120 ($MM) 1.4 1.4 1.4

Low Case

IP (bopd) 85 115 140

EUR (mbbls) 75 104 127

Barrels of Oil per Day (bbls/d)

100

IRR (%) 35 67 99

80 NPV10 ($MM) 0.59 1.3 1.8

Payout (yrs) 2.4 1.6 1.3

60

*Drilling, completion, equipping and tie-

in (“DCET”) cost estimates of C$1.4MM

40

are for one-off delineation wells; offset

operator costs have been reduced to

20 C$1MM to C$1.1MM with multi-well

pad program development

0

0 5 10 15 20 25 30

Months

• Type wells developed from the analogous Nipisi field to the South

• Input assumptions:

– Sproule Q1 2020 pricing, C$6/bbl Opex, C$4/bbl trucking and a C$4/bbl pipeline tariff to Hardisty (Western Canada

Select reference price)

– 1st year Opex + transportation per boe of C$15

– STOIIP calculations support the estimated EUR of the Type Wells

: MARCH 2020 19Clearwater – play comparables (NBF1 Sep 2019) : MARCH 2020 1) NBF = National Bank of Canada Financial Markets 20

You can also read