Agriculture, Forestry, Fishing and Hunting in the US - IBISWorld

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

INDUSTRY REPORT 11 Agriculture, Forestry, Fishing and Hunting in the US Cornucopia of possibility: Sector revenue is expected to recover from major declines due to the pandemic John Madigan | September 2021 IBISWorld.com 1-800-330-3772 info@IBISWorld.com

Agriculture, Forestry, Fishing and Hunting in the US September 2021

Contents

COVID-19 (Coronavirus) Impact Update.............................3 COMPETITIVE LANDSCAPE.......................... 23

ABOUT THIS INDUSTRY.................................. 5 Market Share Concentration............................................. 23

Key Success Factors........................................................23

Industry Definition................................................................5 Cost Structure Benchmarks............................................. 24

Major Players...................................................................... 5 Basis of Competition......................................................... 27

Main Activities..................................................................... 5 Barriers to Entry............................................................... 27

Supply Chain....................................................................... 6 Industry Globalization........................................................ 28

INDUSTRY AT A GLANCE................................ 7 MAJOR COMPANIES...................................... 29

Executive Summary............................................................ 9 Major Players.................................................................... 29

INDUSTRY PERFORMANCE..........................10 OPERATING CONDITIONS............................ 33

Key External Drivers.........................................................10 Capital Intensity................................................................. 33

Current Performance........................................................ 11 Technology & Systems......................................................33

Revenue Volatility..............................................................34

INDUSTRY OUTLOOK.................................... 14 Regulation & Policy........................................................... 34

Industry Assistance........................................................... 35

Outlook.............................................................................. 14

Industry Life Cycle............................................................. 15 KEY STATISTICS............................................ 36

PRODUCTS & MARKETS............................... 16 Industry Data..................................................................... 36

Annual Change..................................................................36

Supply Chain..................................................................... 16 Key Ratios......................................................................... 36

Products & Services.......................................................... 16

Demand Determinants...................................................... 17 ADDITIONAL RESOURCES............................37

Major Markets....................................................................18

International Trade............................................................ 20 Additional Resources........................................................ 37

Business Locations........................................................... 21 Industry Jargon..................................................................37

Glossary............................................................................ 37

2 IBISWorld.com

Agriculture, Forestry, Fishing and Hunting in the US September 2021

COVID-19 IBISWorld's analysts constantly monitor the industry impacts of current events in real-time – here is an update of

(Coronavirus) how this industry is likely to be impacted as a result of the global COVID-19 pandemic:

Impact Update · The COVID-19 (coronavirus) pandemic roiled international trade activity, with a general global pullback

compounded by the failure to resolve the trade dispute between the United States and China.

· Inflationary concerns on the horizon may fuel further Agriculture, Forestry, Fishing and Hunting sector growth, but

may also harm sector operators' bottom lines.

· Price distortion in downstream processing markets has weakened returns for sector operators that primarily sell to

processing markets. Fresh markets have performed more strongly due to ease of access to consumers.

Note: The content in this report is currently being updated to reflect the trends outlined above.

3 IBISWorld.com

Agriculture, Forestry, Fishing and Hunting in the US September 2021 About IBISWorld IBISWorld specializes in industry research with coverage on thousands of global industries. Our comprehensive data and in-depth analysis help businesses of all types gain quick and actionable insights on industries around the world. Busy professionals can spend less time researching and preparing for meetings, and more time focused on making strategic business decisions that benefit you, your company and your clients. We offer research on industries in the US, Canada, Australia, New Zealand, Germany, the UK, Ireland, China and Mexico, as well as industries that are truly global in nature. 4 IBISWorld.com

Agriculture, Forestry, Fishing and Hunting in the US September 2021

About This Industry

Industry Definition This sector includes farms that primarily grow crops or raise livestock, as well as companies specializing in forestry

and agricultural support services. This sector also includes companies that provide land for hunting and fishing.

Major Players Tyson Foods

Cargill Inc.

Bayer AG

Syngenta

Main Activities The primary activities of this industry are:

Corn farming (except sweet corn), field and seed production

Popcorn farming, field and seed production

The major products and services in this industry are:

Crops

Animals and animal products

Forestry

Hunting and fishing

Agricultural support services

5 IBISWorld.com

Agriculture, Forestry, Fishing and Hunting in the US September 2021

Supply Chain

SIMILAR INDUSTRIES

Manufacturing in the US Corn, Wheat & Soybean Fruit & Vegetable Markets in the Agribusiness in the US

Wholesaling in the US US

RELATED INTERNATIONAL INDUSTRIES

Global Fruit & Vegetable Citrus Fruit, Nut and Other Fruit Forestry Support Services in New

Processing Growing in Australia Zealand

6 IBISWorld.comAgriculture, Forestry, Fishing and Hunting in the US September 2021

Industry at a Glance

Key Statistics Key External Drivers % = 2016–21 Annual Growth

$465.6bn 0.1% 0.4%

Revenue Trade-weighted index Per capita meat consumption

Annual Growth Annual Growth Annual Growth

0.7% 0.2%

Price of feed Price of fertilizer

2016–2021 2021–2026 2016–2026

0.4%

0.3% 0.5% Agricultural price index

$86.6bn Industry Structure

Profit

POSITIVE IMPACT

Industry Assistance Concentration

High / Steady Low

MIXED IMPACT

18.6% Life Cycle Revenue Volatility

Profit Margin Mature Medium

Annual Growth Annual Growth Technology Change Barriers to Entry

Medium Medium / Steady

2016–2021 2016–2021

Industry Globalization

-0.3pp Medium / Increasing

NEGATIVE IMPACT

Capital Intensity Regulation & Policy

2m High Heavy / Steady

Businesses Competition

High / Steady

Annual Growth Annual Growth Annual Growth

2016–2021 2021–2026 2016–2026

-0.3% 0.1%

Key Trends

Despite the stability of the sector's place in the economy,

revenue and production volumes are historically volatile

4m

Employment While exports have fluctuated, imports have grown over the

past five years

Annual Growth Annual Growth Annual Growth

2016–2021 2021–2026 2016–2026 Despite increased consolidation, demand for labor has

increased during the period

0.1% 0.4%

Price growth will likely run away as production struggles to

catch up

Most farms are family-owned, and therefore, a low

$41.6bn production year can have an effect on annual income

Wages

Farms have increasingly explored mergers and acquisitions

Annual Growth Annual Growth Annual Growth to increase profit

2016–2021 2021–2026 2016–2026 Structural challenges and shifting demand have challenged

-0.6% 0.4% sector revenue growth

7 IBISWorld.comAgriculture, Forestry, Fishing and Hunting in the US September 2021

Products & Services Segmentation

Major Players SWOT

STRENGTHS

High Profit vs. Sector Average

Low Customer Class Concentration

WEAKNESSES

High Product/Service Concentration

Low Revenue per Employee

High Capital Requirements

OPPORTUNITIES

High Revenue Growth (2016-2021)

High Performance Drivers

THREATS

Low Revenue Growth (2005-2021)

Low Outlier Growth

Low Revenue Growth (2021-2026)

8 IBISWorld.comAgriculture, Forestry, Fishing and Hunting in the US September 2021

Executive Summary Cornucopia of possibility: Sector revenue is expected to recover from

major declines due to the pandemic

As one of the oldest sectors in the United States, the Agriculture, Forestry, Fishing and Hunting sector has a

longstanding place in the economy. However, it is also one of the most historically volatile sectors. Agricultural

production can be affected by many unpredictable and unstoppable factors. Droughts, pests and disease can all

destroy crop and livestock production in a given year, resulting in drastic swings in demand and revenue. Sector

revenue has risen at an annualized rate of 0.3% to $465.6 billion over the five years to 2021. This increase,

however, is somewhat misleading since the majority of growth is expected to occur in 2021, with industry revenue

rising an animated 3.7% in 2021 alone. Additionally, structural challenges and shifting demand conditions brought

on by lingering effects of the COVID-19 (coronavirus) pandemic challenged revenue growth in 2020.

Despite declining revenue over the past five years, the sector remains strong and attractive to new companies.

Corporations have turned to this sector as a means of controlling input costs and vertically integrating. However,

despite the growing presence of large companies, more than 85.0% of farms are still family-owned, making the

sector predominately controlled by nonemployers. To contend with increased competition from corporations, many

farms have turned toward consolidation and resource pooling. In many cases, this takes the form of cooperatives

that do not share revenue, but in some cases, farms have merged to reduce costs and pool income. As a result,

sector consolidation has grown during the period, however, most notably, major vertically integrated beef processors

have begun divesting their cattle and livestock operations due to volatile market conditions and weak prices.

Nonetheless, corporate involvement and the forming of cooperatives has caused downward trend in industry

participation. Due to rising operational efficiencies, profit has risen as a result during the period.

Over the five years to 2026, sector revenue is anticipated to accelerate. Overall, growth over the next five years is

expected to be driven by an uptick in agricultural prices across the sector, however this may actually be an example

of inflationary effects of increased government spending during the pandemic coming home to roost. As a result,

sector revenue is projected to increase at an annualized rate of 0.5% to $477.8 billion over the five years to 2026.

9 IBISWorld.comAgriculture, Forestry, Fishing and Hunting in the US September 2021

Industry Performance

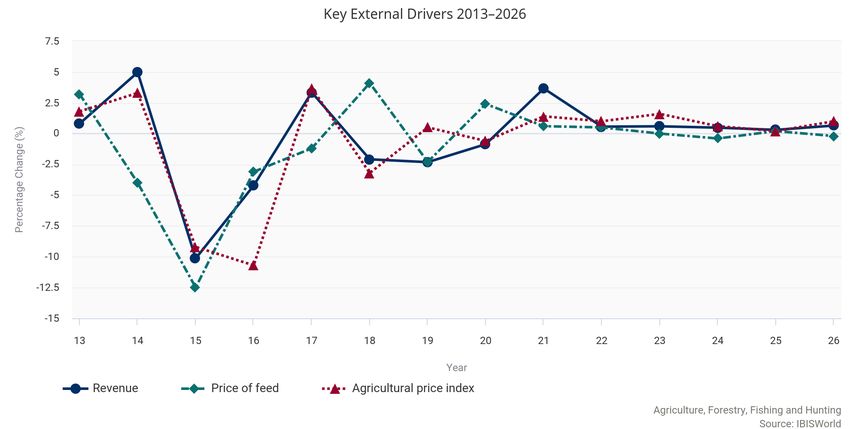

Key External Price of feed

Drivers

Feed is one of the largest input costs for livestock industries. As the price of feed increases, livestock producers

pass the increased cost onto consumers, resulting in increased revenue. Additionally, livestock feed is produced by

crop growers, so higher feed prices generate higher revenue for crop growers. In 2021, the price of feed is projected

to rise.

Agricultural price index

The agricultural price index measures the prices received for all agricultural products including crops and livestock.

As prices increase, farms are generating more revenue. The agricultural price index is a strong indicator of sector

performance. In 2021, the agricultural price index is expected to rise, representing a potential opportunity for the

sector.

Price of fertilizer

Fertilizer is a major input cost for crop growers because fertilizer is needed to grow crops. As fertilizer prices

increase, crop growers are likely to pass cost increases onto buyers, resulting in increased revenue. In 2021, the

price of fertilizer is expected to grow.

Per capita meat consumption

While the sector includes both crops and livestock, these products compete with each other. As per capita meat

consumption increases, vegetable consumption declines. Crops represent a greater portion of sector revenue, so as

meat consumption increases, overall revenue declines. In 2021, per capita meat consumption is expected to fall,

posing a potential threat to the industry.

Trade-weighted index

The trade-weighted index (TWI) measures the value of the US dollar relative to United States' largest trade partners.

As the US dollar appreciates, foreign goods become relatively less expensive, creating competition from imports. In

2021, the TWI is expected to decline.

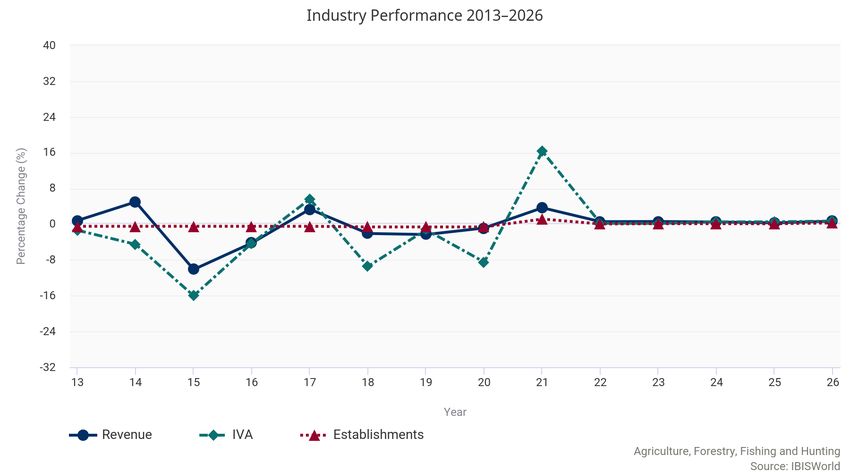

10 IBISWorld.comAgriculture, Forestry, Fishing and Hunting in the US September 2021

Current The Agriculture, Forestry, Fishing and Hunting sector has been one of the

Performance most important sectors in the US economy.

Agricultural products serve as inputs for a wide number of other industries, including food production, wood

manufacturing, biofuel production and ethanol production. The United States is also a net exporter of agricultural

goods, making the sector crucial to US GDP.

However, despite the stability of its place in the economy, revenue and production volumes are historically volatile.

Unpredictable challenges, such as droughts and disease outbreaks, can cause massive declines in crop and

livestock production. These shortages cause price fluctuations that can ripple through the sector, causing revenue

volatility. As a result of this volatility, sector revenue has risen an annualized 0.3% to $465.6 billion over the five

years to 2021, including an increase of 3.7% in 2021 alone as the sector recoups losses incurred as a result of the

COVID-19 (coronavirus) pandemic. These losses include major shifts in the markets for agricultural products, the

pinching of the downstream supply chain, and the divergence of retail and farmgate prices for agricultural products,

which caused most farmers to miss out on the growth exhibited by processors and retailers during the pandemic.

Furthermore, United States Department of Agriculture supply, demand and price data suggests trouble may still be

brewing in the sector.

PRODUCTION VOLATILITY

Overall, the sector has been affected by various exogenous and

endogenous shocks over the past five years.

Perhaps most importantly, prior to the current period, agricultural production had risen to new highs as a burgeoning

Chinese economy demanded more and more agricultural commodities, driving prices up and incurring

overproduction. As demand from China slowed, industry products began to pile up on the domestic market, causing

prices to fall due to rising supply availability. In 2016, the industry experienced declines in the wake of much larger

decreases in 2015. Since then, the industry has been volatile as supply and demand realigned. After this, the trade

war with China began, as well as the renegotiation of the North American Free Trade Agreement, which was

replaced by the United States-Mexico-Canada Agreement, which experienced further disruption regarding industry

export markets, causing domestic supplies to rise further and prices to slide as products flooded the domestic

market. Then, in 2020, the coronavirus pandemic further disrupted the sector due a pinching in the downstream

supply chain and due to a rapid increase in consumer demand. Overall, industry farmers were shut out of the rapid

price appreciation of food items because they were left holding the proverbial bag. As processing and wholesale

capacity declined as a result of the pandemic, agricultural commodities piled up at the farm gate, causing prices at

the farm gate to diverge from those at the retail out. Overall, this is expected to still weigh on the industry over the

five years to 2026, and supply and demand must engage in a continued balancing act over the next five years.

INPUT COSTS

11 IBISWorld.comAgriculture, Forestry, Fishing and Hunting in the US September 2021

The performance of the subsectors within the sector can largely be

determined by the costs of inputs.

For example, when feed prices increase, livestock producers raise prices and generate higher revenue. Meanwhile,

when fertilizer costs increase, crop growers pass the increased price on to upstream buyers, resulting in greater

revenue. However, input costs fluctuations have a smaller effect on the overall sector because feed is produced by

crop growers and fertilizer is partially produced by livestock farms. Therefore, when crop prices rise, so does the

cost of feed, and when meat and livestock prices rise, so do fertilizer costs. However, the seasonality of sector

products causes a delayed effect in downstream price changes.

More recently, operating costs have increased due to the coronavirus pandemic. Across the economy, businesses

have been forced to limit production or shut down due to the spread of the virus. For example, restaurants in cities

and states most affected by the pandemic were required to close in early 2020, causing demand from restaurants to

plummet. Meanwhile, demand from grocery stores and other retail food sellers has grown significantly as consumers

started cooking at home more. Overall, this has resulted in minimal change in demand for agricultural products, but

the markets have shifted. This has created an obstacle for many farms because they had previously only provided

products for restaurants or other large buyers. Now, these operators must invest in new equipment and new

processes to be able to sell to grocery stores or directly to consumers. However, in 2021, profit, measured as

earnings before interest and taxes, has risen from lows observed in 2020 as a result of the pandemic, accounting for

as 18.6% of revenue in 2021. Profit in 2021 is still below peaks observed prior to current period, indicating the

industry is still contending with difficulty.

While natural challenges can affect domestic production of crops and livestock, production fluctuations in other

countries can affect the value of exports. Shortages in other countries in 2016 enabled the United States to increase

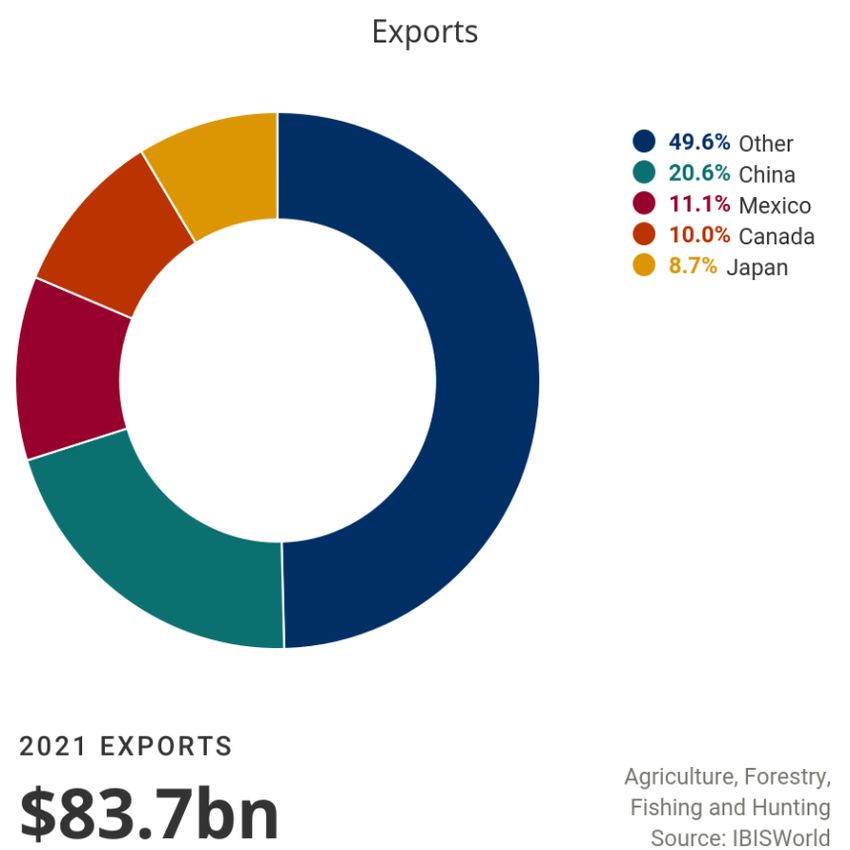

exports. However, the value of sector exports has remained largely static, increasing an annualized 0.7% $83.7

billion over the five years to 2021. Exports are expected to rebound in 2021 from lows in 2020 due to China placing

significant tariffs on US agricultural goods. These tariffs have been in retaliation to the United States placing tariffs

on Chinese steel; China is the largest buyer of US agricultural goods, so Chinese tariffs have had a significant effect

on the sector. While a trade deal between the United States and China is expected in 2021, trade is expected to

remain low due to the coronavirus pandemic, limiting international trade in nearly all sectors.

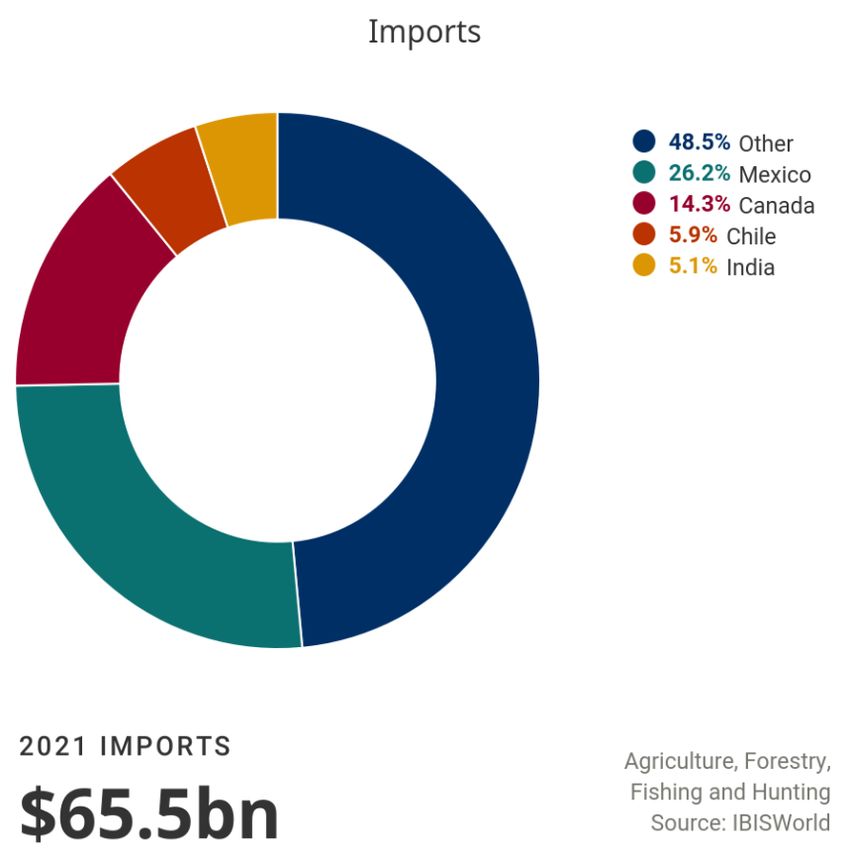

While exports have fluctuated, imports have grown over the past five years. Imports typically experience less

volatility because the United States imports products from a variety of countries, primarily importing crops that

cannot be grown domestically. The value of sector imports has grown an annualized 0.7% to $65.5 billion over the

five years to 2021.

FAMILY FARMS

Despite revenue and profit declines, the sector remains attractive due to

its stable position.

Corporations seeking to vertically integrate and control supplies have attempted to enter the sector over the past five

years. However, despite this trend, more than 85.0% of industry farms are family-owned. However, while most farms

are small independent operations, some farms have turned to consolidation as a means of competing with

corporation and limiting production costs. In many cases, this takes the form of cooperatives and resource pooling.

However, in some cases, farms have merged and combined their income. As a result, the number of sector

enterprises has declined an annualized 0.3% to 2.3 million companies over the five years to 2021.

Meanwhile, despite increased consolidation, demand for labor has increased during the period. Historically, the

agriculture sector has had low average wages, but increased demand for organic and specialty products has

created a need for skilled labor. While these products receive higher prices, they also require greater inputs,

including hands-on labor. However, in 2021, industry employment is expected to flounder due to increased

limitations on immigration and international travel. Sector employment is anticipated to rise a meager, annualized

0.1% to reach 3.5 million employees.

12 IBISWorld.comAgriculture, Forestry, Fishing and Hunting in the US September 2021

Historical Performance Data

Domestic Agricultural

Revenue IVA Establishments Enterprises Employment Exports Imports Wages Demand Price Index

Year ($m) ($m) (Units) (Units) (Units) ($m) ($m) ($m) ($m) (Index)

2012 502,932 209,001 2,371,403 2,367,454 3,464,629 90,288 58,444 38,950 471,088 105

2013 507,050 206,151 2,360,241 2,356,153 3,472,488 86,749 61,245 39,404 481,546 107

2014 532,282 196,857 2,349,132 2,344,847 3,479,965 89,507 65,208 42,088 507,982 111

2015 478,325 165,322 2,338,075 2,333,614 3,485,139 77,067 62,201 39,640 463,459 100

2016 458,151 158,268 2,327,070 2,322,472 3,483,130 80,880 63,371 42,818 440,641 89.6

2017 473,527 167,139 2,316,120 2,311,410 3,472,987 81,399 66,902 45,205 459,030 93.0

2018 463,670 151,383 2,301,785 2,296,905 3,459,480 77,871 66,365 41,818 452,165 90.0

2019 452,958 149,475 2,287,539 2,282,534 3,443,701 72,527 65,643 40,852 446,074 90.5

2020 449,088 136,797 2,273,381 2,268,153 3,418,579 79,369 64,716 40,503 434,436 90.0

2021 465,568 159,089 2,299,466 2,290,346 3,500,175 83,711 65,481 41,574 447,337 91.3

13 IBISWorld.comAgriculture, Forestry, Fishing and Hunting in the US September 2021

Industry Outlook

Outlook After a volatile five years to 2021, the Agriculture, Forestry, Fishing and

Hunting sector is anticipated to accelerate over the five years to 2026.

Steadily rising agricultural prices and growing demand for healthy and organic food will be the main drivers of

demand. However, the sector also experiences threats from the uncertainty of weather and a potential for a

continued trade war with China. Furthermore, supply and demand indicators suggest that not all is well within the

sector and it could be poised for an inflationary spike as a result of the Federal Reserve's monetary stimulus efforts.

Furthermore, international trade is expected to have minimal effect on domestic prices, since industry exports are

anticipated to rise an annualized 0.7% to reach $86.8 billion, while being offset by an annualized 0.2% increase in

industry imports to reach $66.2 billion in 2026. Assuming the sector does not contend with any unmatched

production swings, sector revenue will likely increase, rising an annualized 0.5% to $477.8 billion over the five years

to 2026.

A SECTOR DIVIDED AGAINST ITSELF CANNOT STAND

While industry revenue is anticipated to rise at an accelerated rate over

the next five years, this does not bode well for the sector nor the economy

at large and presents an example of the inflationary effects of increased

government spending coming home to roost.

Put simply, as a result of the tightening in the supply chain during the height of the pandemic and the Federal

Reserve's massive expansion if its balance sheet, the efficient market pricing mechanism appears to be failing, at

least in regard to agricultural commodities.

One need only look at the latest (April 2021) United States Department of Agriculture (USDA) global supply, demand

and price data to see that something is amiss. According to this data, in 2020, small increases in production of no

more than 2.5% yielded significant double-digit declines in prices to farmers, since a tightened supply chain caused

flooding of agricultural commodities at the farm gate as processing capacity was taken offline. Such small increases

in production yielding such outsized impacts on price is the first indicator that not all is well within the sector,

especially considering the fact that retail prices and farm gate prices for processed agricultural commodities have

diverged, with processing and retail prices rising as farm gate prices decline.

Secondly, USDA projections through April of 2021 suggest a more startling trend. Production in 2021 of almost all

agricultural commodities is expected to rise in line with previous increases exhibited in 2020, however, output prices

for farmers in nearly every commodity are expected to rise. Considering this data has such a low margin of error,

this is a disturbing outlook; by all accounts, as agricultural commodity supplies rise, due to falling scarcity their price

should decline on the open market if levels of demand hold constant.

Considering the spikes in demand which occurred in 2020 due to panic buying, it is unlikely demand will grow at

such a pace to justify upward price momentum of this magnitude in line with rising levels of production. Furthermore,

due to a tightened supply chain amid lowered operating capacity during the pandemic, particularly in the

downstream meat processing facilities, prices for finished goods have already been on the rise for consumers. Now,

with expectations that farm gate prices will rise in line with rising levels of production suggests that these price

increases will likely ripple down the supply chain to the consumer. Overall, this suggests inflation or perhaps the

brewing of a new commodities super cycle, which sources such as the Wall Street Journal and Bloomberg have

suggested may be the case. If so, price growth will likely run away as production struggles to catch up, with the

14 IBISWorld.comAgriculture, Forestry, Fishing and Hunting in the US September 2021

expectation that performance will be similar to that of the last commodities run up which burst in 2016. To be blunt,

none of this bodes well for the macroeconomic health of the economy and much remains uncertain for the

performance of the sector.

SAFETY IN THE HERD

Most farms are family-owned, and therefore, a low production year can

have an effect on annual income.

If a farm does not have significant assets, then a low production year could mean financial disaster. To combat

these situations, many farms have turned to consolidation through either mergers or cooperatives. More often, farms

create cooperative structures that enable them to pool resources and keep operating costs low. However, farms

have increasingly explored mergers and acquisitions to increase profit. As a result of this trend, the number of

enterprises is projected to continue stagnating near 2.3 million companies, exhibiting an annualized 0.1% increase

over the five years to 2026. Despite sluggishness in participation growth, demand for employment is likely to rise

due to growing demand for labor-intensive products. For example, organic crops require staff to monitor crops more

closely than traditional crops. As this trend continues, sector employment is projected to increase an annualized

0.4% to 3.6 million employees over the five years to 2026.

Performance Outlook Data

Domestic Agricultural

Revenue IVA Establishments Enterprises Employment Exports Imports Wages Demand Price Index

Year ($m) ($m) (Units) (Units) (Units) ($m) ($m) ($m) ($m) (Index)

2021 465,568 159,089 2,299,466 2,290,346 3,500,175 83,711 65,481 41,574 447,337 91.3

2022 468,217 159,406 2,300,520 2,290,525 3,513,059 84,646 65,355 41,744 448,925 92.2

2023 471,008 159,671 2,302,841 2,292,000 3,527,168 84,949 65,961 41,927 452,020 93.7

2024 473,292 160,494 2,305,268 2,293,745 3,539,473 85,563 66,063 42,085 453,791 94.3

2025 474,721 161,331 2,307,149 2,295,182 3,548,417 86,027 66,042 42,196 454,737 94.5

2026 477,808 162,449 2,313,630 2,300,963 3,566,862 86,794 66,249 42,426 457,263 95.4

2027 479,685 162,895 2,319,534 2,306,514 3,580,708 87,347 66,285 42,591 458,624 95.8

Industry Life Cycle The life cycle stage of this industry is Mature

LIFE CYCLE REASONS

Sector IVA is well below that of US GDP

Sector establishments are concentrating

Sector end markets are well-established

The Agriculture, Forestry, Fishing and Hunting sector is in the mature stage of its life cycle. Sector value added

(SVA), which measures a sector's contribution to the overall economy, is projected to rise at an annualized rate of

0.3% over the 10 years to 2026. Meanwhile, US GDP is projected to grow an annualized 2.3% during the same

period. SVA growth that is slower than GDP is typically a sign of a mature industry. Additionally, a sector's life cycle

stage is mainly illustrated by the fact that it holds a stable place in the US economy. Agricultural goods are a major

input for a wide variety of industries, so demand for this sector is consistently strong.

Additionally, the sector has experienced a moderate level of technological change. While agriculture is not typically

considered a highly advancing field, innovation in the form of genetically modified seeds and crops has significantly

changed the sector over the five years to 2021. Additionally, the sector has experienced a mild amount of

consolidation, as farms have turned to mergers as a means of cutting costs and reducing risk. As a result, the

number of enterprises is projected to decline at an annualized rate of 0.1% over the 10 years to 2026. Consolidation

is typically a sign of a sector in its mature stage.

15 IBISWorld.comAgriculture, Forestry, Fishing and Hunting in the US September 2021

Products & Markets

Supply Chain Key Buying Industries Key Selling Industries

1st Tier 1st Tier

Manufacturing in the US Manufacturing in the US

Wholesale Trade in the US Wholesale Trade in the US

Retail Trade in the US 2nd Tier

2nd Tier Utilities in the US

Consumers in the US Construction in the US

Public Administration in the US

Products & Services

CROPS

Crop growing industries account for the largest subsector in the

Agriculture, Forestry, Fishing and Hunting sector.

The crop growing subsector includes farms that grow field crops, fruits and vegetables. The largest industries within

this subsector include Corn Farming (IBISWorld report 11115); Soybean Farming (11111); Hay and Crop Farming

(11199); and Fruit and Nut Farming (11135). Collectively, this subsector is expected to account for 42.9% of sector

revenue in 2021. However, over the five years to 2021, this segment has declined as a share of revenue. This

decline has mainly been driven by falling crop prices, represented by the agricultural price index.

Over the five years to 2026, crop growing is projected to rise slightly as a share of revenue, as crop prices begin to

recover and crop growers are able to increase their revenue. The agricultural price index is expected to rise an

annualized 0.9% over the five years to 2026. This growth will likely be driven by rising demand for crops and

increased use of biofuel. Additionally, as demand for meat begins to rise, livestock farmers will likely increase their

production, and therefore, increase their demand for feed.

ANIMALS AND ANIMAL PRODUCTS

Farms that produce livestock and animal products make up the second-

largest portion of revenue.

This subsector includes farms that raise livestock for sale or consumption and farms that produce animal products,

such as milk, eggs and honey. The largest industries within this subsector are the Beef Cattle Production industry

(IBISWorld report 11211), the Dairy Farms industry (11212) and the Chicken and Turkey Meat Production industry

(11235). These industries have particularly high demand because beef and chicken are the two most popular meats,

while milk is used as an input for hundreds of products. In 2021, this subsector is expected to account for 45.2% of

sector revenue.

AGRICULTURAL SUPPORT SERVICES

16 IBISWorld.comAgriculture, Forestry, Fishing and Hunting in the US September 2021

The agricultural support services subsector includes companies that

provide services directly to other operators in the sector.

Companies in this sector offer crop support services, livestock production services and forest support services.

These services are the miscellaneous services that farms cannot often provide themselves, such as crop spraying,

livestock breeding and pest control. Revenue for this subsector has experienced steady growth over the past five

years as demand for these services are mainly stable. If farms are experiencing challenges, support service

providers can be brought in to cut costs and increase production. Meanwhile, if farms are experiencing growth, they

can hire support service providers to further increase production. As a result, over the past five years, agricultural

support services have grown as a share of sector revenue, accounting for 7.2% of revenue in 2021.

FORESTRY

Forestry is a relatively small subsector that includes logging and timber

services.

In 2021, forestry is expected to account for 3.3% of sector revenue. Despite its small size, this subsector is crucial to

the economy, as it provides resources to the construction and manufacturing sectors. This subsector has grown as a

share of revenue over the past five years because businesses have placed a greater emphasis on using domestic

supplies. However, imported lumber from Canada has threatened this subsector and has kept revenue low.

HUNTING AND FISHING

The hunting and fishing subsector is the smallest portion of the sector,

accounting for 1.4% of sector revenue in 2021.

This subsector includes hunting and trapping preserves, commercial trappers and commercial fishers. This

subsector does not include aquaculture, as that is included in livestock production. Revenue is this subsector has

increased slightly over the past five years as demand for fresh fish has grown.

Demand Demand for Agriculture, Forestry, Fishing and Hunting sector products

Determinants and services is determined by many factors, including consumer

preferences, legislation and weather.

The healthy eating index, which measures the degree to which people's diets comply with a standard diet set by the

US Department of Agriculture (USDA), typically serves as a proxy for demand for vegetables and fresh crops.

However, the USDA's target diet favors lean meat over red meat and contains limited amounts of meat, so as the

healthy eating index rises, demand for meat falls. As a result, the healthy eating index has both a positive and

negative affect on the sector. However, aside from the healthy eating index, other consumer health trends affect

demand for sector products. For example, the current trend toward organic and natural products has increased

demand for most of the sector because farms are able to sell natural products directly to consumers and at a higher

price.

Meanwhile, sector demand has been affected by biofuel production, as oilseeds, soybeans, corn and sugarcane are

all inputs to biofuel. Demand for biofuel has been volatile over the five years to 2021, as emphasis on biofuel has

declined in response to low natural gas prices. While regulation, such as the Renewable Fuel Standard Program,

which aims to increase the amount of renewable fuel used domestically by 2022, remains in place, many businesses

are less determined to use biofuel now that the price of gas is lower. However, as the price of natural gas rises over

the five years to 2026, demand for biofuel will likely rise.

Severe weather can also affect demand for agricultural products because weather largely determines prices for

crops.

17 IBISWorld.comAgriculture, Forestry, Fishing and Hunting in the US September 2021

Major Markets

FOOD PROCESSORS AND WHOLESALERS

The majority of products from the Agriculture, Forestry, Fishing and

Hunting sector are sold to food processors.

This market includes a wide variety of food processors, including dairy product producers, meat processors, fruit and

vegetable canning companies and any other food producers that use crops, vegetables, animal products or meat as

inputs. Demand from this market is high because most industry products have short shelf lives, making it difficult to

distribute products and sell them directly to consumers. For example, raw milk is rarely sold directly from farmers to

consumers because unpasteurized milk does not stay fresh for more than a few days. In 2021, food processors are

expected to account for 35.8% of sector revenue. However, over the five years to 2026, demand from this market is

likely to fall, as more consumers embrace local food sources and begin purchasing produce directly from farm

stands and farmers markets. Wholesalers account for a minimal share of revenue, accounting for 1.0% of sector

revenue in 2021.

FARMS

Sales to farms account for a significant portion of sector revenue.

While not all farms sell directly to other farms, the sale of seeds and livestock is a crucial market for some

agricultural industries. For example, wheat, barley and sorghum farms often sell crops directly to livestock farms to

use as animal feed, while chicken and turkey meat producers sell female hens to chicken egg farms. Over the five

years to 2021, the market for seeds has been increasingly dominated by genetically modified organism (GMO)

companies. For example, the Monsanto Company distributes GMO seeds for corn, soybeans, wheat and sorghum.

While GMOs have been controversial, demand for these seeds has been strong. In 2021, sales to farms are

expected to account for 21.2% of sector revenue.

EXPORTS

The market for exports within the Agriculture, Forestry, Fishing and

Hunting sector is relatively strong for certain parts of the sector.

As a whole, exports are expected to account for 17.9% of revenue in 2021. However, exports mainly come from

crop growing industries. Many crops are able to be exported in large quantities because they have long shelf lives.

For example, nearly half of all wheat, barley and sorghum grown in the United States is exported, while more than

half of US soybeans are exported. Exports also come from livestock industries, however, to a much lesser extent.

Meat is not often traded because shipping often takes too long, but livestock can be exported. For example, less

than 1.0% of Beef Cattle Production industry (IBISWorld report 11211) revenue is accounted for by exports.

GROCERY STORES, MARKETS, CONSTRUCTION, MANUFACTURING AND OTHER

Markets, grocery stores and restaurants represent a strong market for

farms that produce ready-to-eat products.

Industries with strong food service markets include the Vegetable Farming industry, the Orange and Citrus Groves

industry and the Fruit and Nut Farming industry. Sales to this market are expected to account for 9.9% of sector

18 IBISWorld.comAgriculture, Forestry, Fishing and Hunting in the US September 2021

revenue in 2021. However, this market is likely to grow over the next five years, as the trend toward farm-to-table

restaurants grows. Additionally, as consumers continue to buy produce from farmers markets and farm stands, this

market's share of the sector will continue to grow. Construction and manufacturing markets account for a minimal

share of sector revenue, accounting for 3.4% of revenue in 2021. All other markets account for 10.8% of revenue in

2021.

19 IBISWorld.comAgriculture, Forestry, Fishing and Hunting in the US September 2021

International Trade Exports in this industry are Medium and Steady

Imports in this industry are Medium and Steady

Imports

Over the five years to 2021, imports have been satisfying a growing portion of domestic demand for agricultural

goods produced within the Agriculture, Forestry, Fishing and Hunting sector. Demand for imported goods is

determined by several factors, including the value of the US dollar, production levels in other countries and weather

conditions in the United States. Imports typically serve as a fallback for sector industries that have low production in

a given year. For example, the Orange and Citrus Groves industry (IBISWorld report 11134) has been plagued by

citrus greening, a plant disease that causes trees to produce sour and inedible fruits. As a result, citrus imports have

increased as domestic groves have not been able to keep up with demand. While diseases rarely affect the entire

sector at once, severe weather conditions can result in lower-than-average crop yields and increased import

penetration. The value of imports has risen at an annualized rate of 0.7% to $65.5 billion over the five years to 2021.

As a result, imports are expected to account for 14.6% of domestic demand in 2021, up from 14.4% in 2016.

Sector imports mainly come from Mexico and Canada because many sector products cannot survive long trips from

other countries. As a result, Mexico accounts for 26.2% of imports and Canada accounts for 14.3% of imports in

2021. Additionally, the United States-Mexico-Canada Agreement enables the United States to import Mexican and

Canadian agricultural products without tariffs, making goods from these countries relatively less expensive. The

United States also imports from countries that specialize in products that cannot be produced domestically. For

example, there are few places in the United States that can grow tropical fruits, such as bananas, avocados and

mangos. As a result, in 2021, Chile accounts for 5.9% of imports, while India accounts for 5.1% of imports.

Exports

Despite import growth over the past five years, the United States continues to be a net exporter of agricultural

goods. The value of exports is mainly driven by overseas demand for US cash crops, such as corn, wheat and

sorghum. These crops are mainly exported to China, due to the country's growing economy. As a result, China

typically accounts for 20.6% of sector exports in 2021, with Mexico and Canada accounting for a respective 11.1%

and 10.0% of exports in 2021. However, in 2018, the United States and China began a trade war when the United

States imposed tariffs on Chinese steel and China retaliated with tariffs on US agricultural products. As a result,

Chinese demand for sector goods declined drastically in 2019 and 2020. Exports to China have declined sharply

over the five years to 2021 due to these tariffs. As China is an important destination for sector goods, the value of

industry exports has floundered over the five years to 2021, rising an annualized 0.7% to reach an estimated $83.7

billion in 2021. While the two countries were expected to sign a trade deal in 2020, the COVID-19 (coronavirus)

pandemic has put a hold on the deal. International trade has been limited in nearly all sectors by the pandemic, so

the trade deal has not been a priority.

20 IBISWorld.comAgriculture, Forestry, Fishing and Hunting in the US September 2021

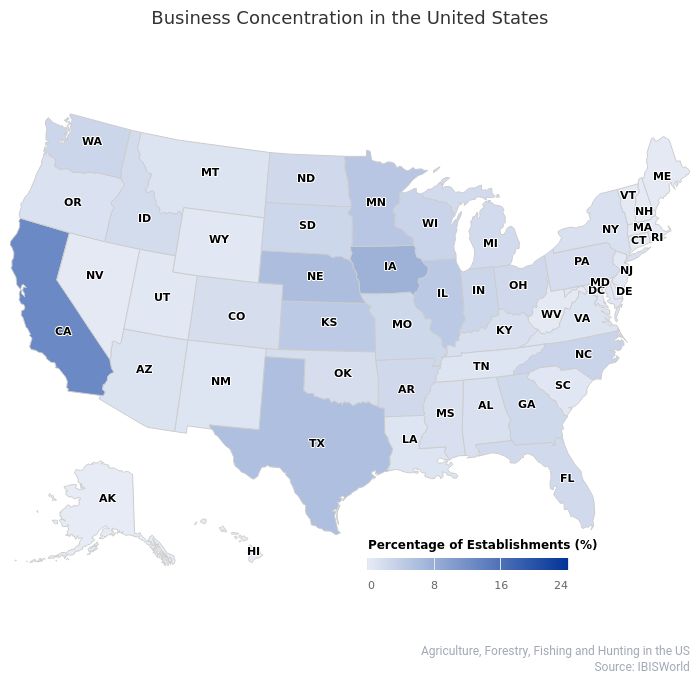

Business

Locations

The distribution of establishments in the Agriculture, Forestry, Fishing and Hunting sector is largely determined by the land and

resources available in a region. Most industries within the sector require large amounts of land and access to natural resources.

For example, crop growing industries require large areas with fertile soil, making the Plains and Southeast regions two of the most

popular areas for crops. Meanwhile, New England (0.8%), which has several major urban areas and has many areas with rocky

and coastal soil, accounts for a disproportionately small portion of sector establishments. Meanwhile, certain crops, such as

oranges and citrus, can only grow in warm climates, such as Florida and California, supporting concentration in the Southeast and

West regions.

Overall, the Plains region is the most concentrated region in the sector, accounting 29.8% of sector establishments in 2021. This

region is mainly driven by cash crops such as corn, wheat, grain and tobacco. This also supports livestock production in the region

because feed lots need access to animal feed. Additionally, Iowa and Nebraska account for 7.5% and 6.0% of sector

establishments, respectively, in 2021. As a result, this region accounts for a disproportionally large amount of the sector relative to

the region's portion of the US population.

Following the Plains, the Southeast and West regions are the next largest regions in the sector, accounting for 17.8% and 17.3%

of establishments, respectively, in 2021. The Southeast's share of sector establishments is mainly supported by the region's warm

21 IBISWorld.comAgriculture, Forestry, Fishing and Hunting in the US September 2021

climate and large population. Meanwhile, the West's share is based on population and wide variety of climates. California is the

main driver of the West, accounting for 12.8% of establishments in 2021. While California lacks the open spaces for corn and

other crops that the Plains have, the state has large areas of timber for forestry and a variety of climates to support fruit growing.

22 IBISWorld.comAgriculture, Forestry, Fishing and Hunting in the US September 2021

Competitive Landscape

Market Share

Concentration

Concentration in this industry is Low

The Agriculture, Forestry, Fishing and Hunting sector is characterized by a low level of market share concentration,

with few companies accounting for more than 5.0% of sector revenue in 2021. The agriculture sector is highly

dominated by small family-owned farms with few farms having corporate ownership. According to the 2017

Agricultural Census, more than 85.0% of farms are family-owned (latest data available). While a growing number of

farms have formed cooperatives to increase their negotiating power, only a small portion of farms have included

revenue pooling as an aspect of their cooperative structure. Consolidation in the agriculture sector mainly takes the

form of supplier contracts. This trend is most prominent in the Chicken and Turkey Meat Production industry

(IBISWorld report 11235), where large companies, such as Tyson Foods Inc., supply farms with livestock to raise

and sell back to them. This structure keeps the supplier out of the sector, but gives them control over the operations

of farms in the sector. Additionally, there is higher concentration within the forestry subsector, however, this

subsector accounts for only a small portion of total sector revenue.

Key Success IBISWorld identifies 250 Key Success Factors for a business. The most important for this industry are:

Factors

Ability to alter goods and services produced in favor of market conditions:

Farms are able to limit volatility by diversifying their crops.

Appropriate climatic conditions:

Some crops cannot be grown in the United States due to the country's climate.

Proximity to key suppliers:

Farms must limit production costs by establishing close to seed, fertilizer and feed producers.

Must comply with government regulations:

Farms must comply with US Department of Agriculture standards to sell crops in the United States.

23 IBISWorld.comAgriculture, Forestry, Fishing and Hunting in the US September 2021

Cost Structure

Benchmarks

Profit

Profit is relatively high for the sector. In 2021, profit, measured as

earnings before interest and taxes, is expected to account for 18.6% of

sector revenue, elevated over 2016 levels, but still below the peak

levels exhibited before then during the commodities bubble run-up.

However, profit varies between subsectors and between individual

industries within the sector. Additionally, profit is highly volatile because

it is largely determined by production volumes and commodity prices. In

this sector, production volumes are difficult to forecast because they

can be hindered by severe weather conditions, disease outbreaks and

animal population changes.

As a whole, the sector has struggled since 2018 when the United

States entered into a trade war with China. The United States placed

tariffs on many Chinese products, and in retaliation, China placed tariffs

on US agricultural products. This resulted in a surplus of crops in the

United States, which caused prices and profit to fall. Just as the trade

war seemed to be coming to an end in early 2020, the sector was hit by

the COVID-19 (coronavirus) pandemic. The pandemic has forced cities

and states to close schools and nonessential businesses, causing

demand for food to shift. Many farms mainly supply restaurants and

other large buyers of food, as opposed to grocery stores and other

retail buyers. While overall demand for agricultural products remains

high, farms have had to shift where they sell their products. This has

come with additional costs, which, in 2020, led to lower profit. With

expected return to growth in sector revenue, profitability is anticipated

to rise in 2021 as conditions and end markets normalize.

24 IBISWorld.comAgriculture, Forestry, Fishing and Hunting in the US September 2021

Wages

Wages are a relatively low cost for the agriculture sector. Wage costs

are expected to account for 8.9% of sector revenue in 2021, down

marginally from 9.3% in 2016. However, this cost is dragged down by

labor costs for crop growers and livestock producers. These industries

are mainly made up of family farms that rely on unpaid family labor and

temporary workers. As a result, the average wage for the sector low.

However, over the five years to 2021, wages have fallen as farms have

implemented more advanced equipment and automation. While

automation had resulted in less demand for labor, it has also created

demand for skilled labor, as more advanced machinery requires

workers with the skills to operate it. However due to the overwhelming

presence of owner operators, technically no wages are paid and

increases in more productive labor should be apparent in sector

profitability, since owner-operators will pay themselves.

Purchases

While the inputs purchased vary widely between industries within the

sector, purchase costs are consistently high throughout the sector. In

2021, purchase costs are expected to account for 30.9% of revenue.

For crop growing industries, the largest purchase costs are seeds and

fertilizer, while purchase costs for livestock production industries are

mainly made up of animal feed and livestock. Purchase costs fluctuate

year to year in response to commodity price volatility. However, price

volatility typically balances out at the sector level because livestock

industries purchase from crop growing industries. Purchase costs have

declined recently, as Chinese tariffs have reduced overseas demand

for many crops, resulting in a surplus of seeds. As a result, the price of

seeds has plummeted, causing purchase costs to decline.

Marketing

Marketing is the smallest cost for the Agriculture, Forestry, Fishing and

Hunting sector because industry operators typically sell based on

contracts. In 2021, marketing costs are expected to account for 0.6% of

sector revenue.

Depreciation

Compared with other sectors, the agriculture sector has high

depreciation costs. Depreciation serves as a proxy for capital

expenses, and operators in this sector have high capital costs because

many of the industries within the sector must invest heavily in

equipment for crop growing and livestock production. Additionally,

forestry and agricultural support services are both highly capital

intense. In 2021, depreciation costs are expected to account for 6.6%

of revenue.

25 IBISWorld.comAgriculture, Forestry, Fishing and Hunting in the US September 2021

Rent

Land is a crucial cost for the Agriculture, Forestry, Fishing and Hunting

sector, as crop growers and livestock farms need large amounts of

space. As a result, rent costs are expected to account for 7.9% of

sector revenue in 2021.

Utilities

Utilities represent a moderate cost for sector companies. This expense

includes the cost of operating equipment, watering crops, powering

facilities and all other energy needs. In 2021, utility costs are expected

to account for 6.9% of sector revenue.

Other Costs

Other costs for the sector include administrative costs, legal fees and

other general expenses. Other costs account for 19.6% of revenue in

2021.

26 IBISWorld.comAgriculture, Forestry, Fishing and Hunting in the US September 2021

Basis of Competition in this industry is High and the trend is Steady

Competition

INTERNAL COMPETITION

Competition in the Agriculture, Forestry, Fishing and Hunting sector is

moderate, with operators competing based on price and product

specialty.

Prices are highly volatile in the agriculture sector, particularly with crops and livestock because production yields can

change quickly creating shortages and surpluses. Crop farmers and livestock producers are limited in their abilities

to change prices because competition forces them to keep prices in line with the industry average. However, some

operators are able to charge higher prices for specialty products. Over the five years to 2021, demand for organic

and natural products has increased rapidly as people have become more concerned with the health and

sustainability of their food. As a result, many farms have sought out organic certification to better compete. This

pattern has been present with other food trends, such as grass-fed beef and free-range chicken and eggs. However,

while farms are able to charge higher prices for these specialty products, these products also typically carry higher

production costs. For example, organic crops require more labor than regular crops because organic farms need

labor to protect crops from pests and disease. As a result of these higher input costs, some farms will likely be

deterred from entering the market for organic and specialty products.

Additionally, consumer tastes and changing prices can lead to competition between industries within the sector. For

example, pork, chicken and beef are all substitutes for one another. Therefore, when the price of one meat

increases, demand increases for the others. This trend is present across the sector, with shifts in production and

prices of certain crops resulting in demand shifts for other crops.

EXTERNAL COMPETITION

The main source of external competition for the sector is from imports.

Severe weather conditions and production shifts in the United States cause downstream industries to purchase

goods from overseas instead of domestically. However, unlike most other sectors, the United States is a net

exporter of crops and agricultural goods, so import competition is not a threat. Aside from imports, the sector

contends with little competition from other sectors because agricultural goods are the basis of most foods and

cannot be replaced.

Barriers to Barriers to Entry in this industry are Medium and the trend is Steady

Entry

The Agriculture, Forestry, Fishing and Hunting sector has Barriers to Entry Checklist

moderate barriers to entry. While barriers vary between

subsectors, most companies seeking to enter the sector Competition High

need a high level of initial capital. For agricultural

industries, the most significant barrier is the need for large Concentration Low

amounts of land. For example, crop growers need vast

quantities of land to produce large enough crop yields to

Life Cycle Stage Mature

be financially stable. Meanwhile, livestock producers need

land for their livestock to graze or exercise. Other

subsectors also have large capital expenses. For Technology Change Medium

example, forestry industries need logging equipment,

while agricultural service industries need large equipment, Regulation & Policy Heavy

such as crop dusters and harvesters.

Industry Assistance High

Aside from the large costs of entering the sector, crop and

livestock industries also present the challenges

associated with seasonal businesses. In the simplest

terms, crops need to grow before they can be sold. In

other words, if a new farm wants to enter a crop industry,

they must have the assets to stay in business without

income until their first harvest. A bad harvest during a

farm's first year can be enough to put it out of business if

it does not have strong enough assets.

Other barriers new companies experience in this sector

include meeting the regulations set by the US Department

of Agriculture, competing with longstanding farms and

finding a staff with expertise in the field.

27 IBISWorld.comAgriculture, Forestry, Fishing and Hunting in the US September 2021

Industry Globalization in this industry is Medium and the trend is Increasing

Globalization

The Agriculture, Forestry, Fishing and Hunting sector has a moderate level of globalization. Most companies in the

sector are based in the United States. Of the largest companies participating in the sector, only Syngenta AG is

based in another country. While some large seed companies, such as the Monsanto Company and Cargill Inc., have

operations in other countries, these companies do not represent the average sector operator. Typical companies in

this sector are small independent businesses that operate in only one location. However, the sector does experience

globalization in the form of international trade. Trade does not represent a significant portion of sector operations,

but some agricultural goods are entirely imported because they cannot be produced domestically. Additionally, some

industries within the sector, including corn growers and soybean growers, derive a significant portion of revenue

from exports.

28 IBISWorld.comYou can also read