An Economic Analysis of the Federal Renewable Fuel Standard (RFS)

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

An Economic Analysis of the Federal

Renewable Fuel Standard (RFS)

California’s Multi‐Faceted Carbon Regulation Scheme

Biofuels Sustainability Standards: The Next Regulatory Frontier

Jay P. Kesan, Ph.D., J.D.

Professor & Mildred Van Voorhis Jones Faculty Scholar

Biofuel Law & Regulation Group, EBI, IGBThe Federal Renewable Fuel Standard

Renewable Fuel Standards (RFS)

• The Energy Policy Act of 2005 (EPAct) (RFS1): Established minimum volumes

of renewable fuel to be used in on‐road gasoline (codified in the Clean Air Act)

• The Energy Independence and Security Act of 2007 (EISA) (RFS2) Waivers?

(Final rule required by 12/19/08) Infrastructure?

• Increases Volumetric Requirement for renewable fuel for all

transportation fuels (including non‐road gasoline and diesel)

• Limits renewable fuel sources to crops and crop residues from land

cleared or cultivated at any time prior to enactment of EISA

Application/ How far back How do renewable

enforcement historically? fuel producers

internationally? Pre‐colonial times? enforce this?Renewable Fuel Standard (RFS)

• Mandates volumetric minimums for 3 subcategories of renewable fuel

a. Advanced biofuel (anything but cornstarch ethanol)

b. Cellulosic biofuel

c. Biomass‐based diesel

Extensive/Contentious

• Requires life cycle greenhouse gas (GHG) performance standards for each

subcategory

• EPA must take into account both direct emissions and significant indirect

emissions (international included) (all stages of fuel and feedstock

production, land use changes)

• Facilities that commenced construction prior to EISA grandfathered

PLUS: EPA assessing many impacts of EISA in support of regulatory impact

analysis (RIA), including: air and water quality, direct and indirect land use change

(non‐GHG context), energy security, and economic impacts

Mandatory EPA anti‐ Extensive

backsliding and impact reportsVolumetric Requirements:

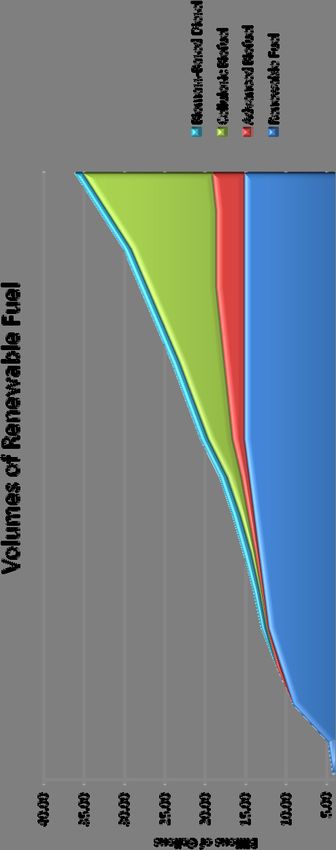

RFS1 vs. RFS2Volumetric Requirements:

RFS2A Preliminary Analysis of the Renewable Fuel Standard (RFS)

Volumetric Requirements of Renewable Fuel: RFS 1 vs. RFS 2

• Under RFS2, ethanol blending percentage exceeds 10 percent in 2013 if all

ethanol is blended into the 2006 level of motor gasoline consumption (142

billion gallons of motor gasoline)

• Ethanol blending percentage reaches about 20 percent in 2022.Objectives of Economic Analysis

• The RFS and its Incentive Scheme

– Regulatory interventions create new constraints and new incentives.

– The RFS should play a vital role in making renewable bio‐fuel

commercially viable in the future. Otherwise, the industry needs

government assistance “forever.”

– Technological progress is key to the successful development of the bio‐

fuel industry.

• Research Questions Relevant to EBI Stakeholders

– Does the RFS give bio‐fuel producers, distributors and feedstock

suppliers an incentive to improve their productivity and cost

conditions?

– What are possible mechanisms that improve the cost conditions

through large scale mandatory consumption imposed by the RFS?

– Is it likely that the RFS actually contributes to improving the cost

conditions?Short‐Run Effects of the RFS

• Policy Goal and the Policy Instrument

– The main goal of the RFS is to reduce dependence on foreign sources of

petroleum and increase domestic sources of energy.

– The policy instrument is to require renewable fuel consumption to exceed

the market clearing amount of the consumption (i.e., mandatory

consumption).

• The RFS creates an excess demand for renewable fuels.

– The price of renewable fuels will be higher under the RFS than in the

absence of the RFS, at least in the short run.

– Higher price hinders market‐based substitution process of renewable fuel.

– Renewable fuel imports will increase.

– The aggregate welfare will likely get worse – in the short run.

• These effects are against the goal of the RFS – in the short run.Ethanol (wholesale) Market

Price

S1

PRFS S2

Pmkt S3

P4 S4

Demand

Qmkt QRFS Q4 QuantityPossible Mechanisms

• In the long run, the supply curve must shift down in order that

bio‐fuel price becomes low enough to be competitive with

fossil fuel.

• What are mechanisms that improve cost conditions through

large scale mandatory consumption?

– Mechanism 1: Economies of scale and/or Marshallian externality.

– Mechanism 2: Stimulating R&D by large scale demand.

• The fruits of cost‐saving innovation are typically reaped by embedding innovation in

a product and selling that product. A producer gains more from cost‐saving

innovation as his sales increase.

• The possibility of large scale sales, imposed by the RFS, can give bio‐fuel producers

an extra incentive to invest on cost‐saving innovation.

– Mechanism 3: Reducing the degree of uncertainty.

• A market guarantee eases credit constraints. It also encourages to take R&D

investment actions now rather than postponing R&D projects.

• These two effects stimulate R&D activity.Source: Energy Information Administration

Source: Energy Information Administration

Source: Nebraska Ethanol Board

Production Capacity of US Ethanol Industry

2002 2003 2004 2005 2006 2007 2008

Production capacity

2,355 2,707 3,101 3,644 4,336 5,493 7,888

(mmgy)

Production Capacity Expansion of US Ethanol Industry

Existing Plants New Plants Share of

Total Average Total Average Expansion by

(mmgy) (mmgy) (mmgy) (mmgy) New Plants

2002‐2003 201 4.02 313 31.31 61%

2003‐2004 64 1.15 400 44.44 86%

2004‐2005 128 2.06 438 39.82 77%

2005‐2006 232 3.36 498 32.23 68%

2006‐2007 273 3.37 1,028 64.25 79%

2007‐2008 758 8.33 1,779 59.30 70%

2002‐2008 1,656 4,456 73%

Source: Renewable Fuel Association and Ethanol ProducerInsights from Ethanol Industry Data

• Ethanol consumption has grown at a rapid pace between 2002

and 2007.

– This rapid growth is mainly due to the fact that ethanol replaced MTBE.

The substitution of ethanol for gasoline was limited.

• Ethanol wholesale price declined between 1982 and 1989, was

stable during 1990s and started rising in 2002.

– Learning and/or scale effects are accountable for the price decline.

– These effects seem absent or limited during the 1990s.

– The increased demand for ethanol caused the ethanol wholesale price

to rise.

• Expansion of production capacity came mainly through new

plant construction.

– The existing plants were unlikely to enjoy the economies of scale.Discussions and Future Research

• The data show that the price of ethanol went up, although

industry faced a larger scale of ethanol demand.

– The effects of demand shift on the ethanol price dominated those of

supply shift.

– The effect of economies of scale was totally absent or limited.

– New plants did not contribute much to reducing ethanol price.

– A further examination is necessary for the mechanisms that stimulate R&D

activity.

• The RFS is unlikely to play a vital role in reducing corn ethanol

price. However, it may be effective for cellulosic ethanol

production.

• Effective policy instruments may differ, depending on the stages

of the industry life‐cycle.

– It may not be rational to apply the same policy instrument to corn ethanol

and cellulosic ethanol industries.Discussion and Future Research (Continued)

• It is worthwhile to examine empirically whether or not the RFS

effectively stimulates R&D activity.

– More specifically, we plan to look at data on patents, R&D expenditures,

scientists and engineers and so on to identify effects of the RFS on the

intensity of R&D activity.

• Discussion on economic policy to encourage university‐based

research or to help transition from invention to innovation is

missing.

– The RFS is not designed to promote university‐based research. What is

the exact role of university‐based research for the industry’s

development?

• It is important to theoretically and empirically study what kind

of incentive scheme should be employed to facilitate

technological progress in the bio‐fuel industry.California’s Multi‐Faceted Carbon Regulatory Scheme

California’s Multi‐Faceted Approach

to Carbon Emission Reduction

1. Overall carbon reduction goals: A.B. 32

• Cap and Trade (industry‐wide)

• Low Carbon Fuel Standard (LCFS)—better fuels

• Increased Auto MPG Efficiency—better vehicles

2. Increased Sourcing of Biomass‐Based Energy

3. Alternative Fuels Use

4. Land‐Use Regulations (e.g., sprawl reduction)

5. Integrated Energy Policy Reporting

6. R & D InvestmentA.B. 32 (Global Warming Solutions Act of 2006)

Goal: Reduce GHG emissions to 1990 levels by 2020 (30% reduction),

and 80% below 1990 levels by 2050

Requires: List of early action measures, GHG Emissions Inventory,

setting a 2020 emissions limit, mandatory emissions

reporting, credit for early reductions

October 2008: Draft Scoping Plan on how to achieve 2020 emissions

limit; measures in place by 2012.

Recommendations (biofuels related):

1. Regional Cap and Trade program for transportation and industrial

sources

2. Implement existing state laws:

•Low Carbon Fuel Standard (LCFS)

•Light‐duty vehicle efficiency standards (AB 1493)

3. Expansion of Renewables Portfolio Standard (RPS) to 33%

(biomass/biofuel feedstock)

4. Carbon Tax ($10‐$15/metric ton CO2)Low Carbon Fuel Standard (LCFS)

Problem: Transportation fuels currently account for 40% of

GHG emissions

Goal: Reduce average carbon intensity of transportation fuels by

10% by 2020

• LCFS will address 50% of GHG emissions related to transportation fuels

• LCFS is an early action measure under AB 32

Requirement: Fuel producers/importers must assess life cycle global

warming intensity of fuel, per unit of energy, and reduce this

over time

Compliance: Improve refinery efficiency, blend fuels with lower carbon

intensity, buy credits from other fuel providers

In combination with Federal RFS, California will need 3 bgal/yr by 2020Low Carbon Fuel Standard (LCFS)

Progress: Draft LCFS Regulation issued October 2008

•Regulated Parties (RPs) must meet yearly declining carbon intensity

requirements and submit progress/compliance reports

•RP’s can use choose between 2 lifecycle methodologies in calculating

carbon intensity

Model 1: CA‐modified GREET (sub‐pathway drafts now issuing)

Land Use + Processing + T & D + Land Use Change=total carbon intensity

Model 2: Customized (must achieve 10% more than Model 1 and sell at

least 10 million gallons)

*CARB has said that it will evaluate other

*Tesoro suit : Phase 3 RFG & LCA environmental and social components

including GMOs, biodiversity, labor rights,

*Inclusion of indirect land use income distribution, etc., and will develop

change (ILUC) requirement is guidelines in conjunction with UC and

controversial othersBiofuels Sustainability Standards: The Next Regulatory Frontier

What does “sustainable” mean?

Environmental Land Use

Climate Change

Societal Labor Conditions

Rural Development

Economic

Benefits to Society

Should Outweigh

Total CostsHow is sustainability achieved?

Voluntary International

Initiatives International (non‐biofuel)

Feedstock Specific

National

Private Sector

Multilateral Development Banks

Mandatory International

Standards National (EU/US)

Sub‐National (States)Voluntary Initiatives

Roundtable on Sustainable Biofuels (RSB) Version Zero

(8/2008)

International Global Bioenergy Partnership (GPEP)

2009?

United Nations

Various Decision‐Making

• UN‐Energy Frameworks

• Food and Agriculture Organization (FAO)

Millennium Ecosystem

• U.N. Environment Programme (UNEP) Assessment

Social and Economic

Sustainability Focus

Sustainable Agriculture

Rainforest Action Network

International Standard (2/08)

(non‐biofuel) Forest Stewardship Council 10 Principles & Criteria;

(Potential Models) 57 indicators

International Federation of

Organic Movements (IFOAM) Organic Guarantee System;

Certifier Accreditation

Fair Trade Label Organization

Generic and Product‐

Specific StandardsVoluntary Initiatives

Principles and

Roundtable on Sustainable Palm Criteria, 10/07

Feedstock Specific Better Sugarcane Initiative 2009?

Roundtable on Responsible Soy (RTRS) Draft Principles &

Criteria, 4/08

National American National Standards Institute Draft Std 5/07; Set

aside 9/08

European Committee for

Standardization Technical Committee

(CEN) formed; draft 2/09

Cramer Report (Netherlands) 5/07; 6 themes, 9

principles w/criteria &

Sustainable Biodiesel Alliance indicators

Draft Baseline Practices for

Social Fuel Stamp Sustainability, 10/08

Brazilian Law requiring

local purchasesMandatory Standards

Kyoto Protocol (GHGs)

Biodiversity Treaties (Potential Application)

International WTO Agreements/Standards Incorporation

Review of Fuel Quality

European Union Directive

Proposal for Directive on

National

Promotion and Use of

Energy from Renewable

U.S.

Sources (1/2008)

U.K. Criteria & Indicators, 11/08

Germany RTFO Sustainability Reporting

Sub‐National

(Regional, State) Biofuels Quota Law requires

compliance with EU

California environmental regulations

Currently being studied under

LCFS; lawsuit alleges cross‐

compliance evaluation

mandatoryThank you!

You can also read