Barriers and opportunities to workforce development to support housing and construction: a focus on affordable housing supply in the Mid North ...

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Barriers and opportunities to workforce development to

support housing and construction: a focus on affordable

housing supply in the Mid North Coast

Report to the Australian Government,

Department of Education, Employment and Workplace Relations

June 2013

Mid North Coast Affordable Housing Report

Acknowledgements

Regional Development Australia Mid North Coast (RDA MNC) acknowledges the Department

of Education, Employment and Workplace Relations (DEEWR) for the funding provided to

undertake this project. We would also like to acknowledge and thank the many participants

who donated their time and valuable insights during the focus groups held as part of this

research project. Furthermore, we would like to thank all the stakeholders who have shared

their knowledge and ideas into this process outside of the focus group sessions. For a full

list of all stakeholders consulted during this project, please refer to Appendix 1.

Acknowledgements are also made to the research and support team involved with this

project, namely:

Research team

o Todd Green (Research & Policy Officer, RDA MNC)

o Matthew Harrison (Project Research Officer, RDA MNC)

o Cassie Crompton (Project Research Assistant, RDA MNC)

o Professor Andrew Beer (Director, Centre for Housing Urban and Regional

Planning, Adelaide University) – Project Consultant

Support team

o Peter Tregilgas (Executive Officer, RDA MNC)

o Jenni Kew (Office Manager, RDA MNC)

o Tim Welsh (Communications & IT Officer, RDA MNC)

DISCLAIMER

This publication is produced by Regional Development Australia Mid North Coast based on information

available at the time of publishing. All opinions conclusions or recommendations are reasonably held or made

as at the time of its compilation, but no warranty is made as to accuracy, reliability or completeness. Regional

Development Australia Mid North Coast does not guarantee the accuracy of the data included in this

publication and accepts no responsibility for any consequences of their use.

Page 1 of 84

Mid North Coast Affordable Housing Report

Executive Summary

This is the final report in a research project that has been undertaken for the Department of

Education, Employment and Workplace Relations (DEEWR) by Regional Development

Australia Mid North Coast to build knowledge and understanding of issues related to the

supply of additional affordable housing in the New South Wales Mid North Coast which can

support additional training and employment outcomes for the region in addition to

increasing housing supply. Funding for this project was provided through the Flexible

Funding Pool (FFP) to support the activities of Local Employment Coordinators in priority

employment areas and the Building Australia’s Future Workforce strategy.

The Mid North Coast of NSW has an older population, especially when compared with the

rest of NSW. This contributes to lower average incomes in the region, which in turn

represents a challenge for the housing construction sector and the effective supply of

affordable housing. On the other hand, while older Australians tend to have lower incomes

when compared with the rest of the population, they also have greater wealth holdings and

strategies should be considered that mobilise this wealth for investment in the region’s

housing stock.

The findings highlighted in relation to workforce development opportunities and barriers to

support construction in the Mid North Coast are:

One opportunity to increase employment and economic activity in the building and

construction sector within the region is to further examine import replacements, as

current import levels support 357 jobs outside of the region.

To increase the number of local businesses involved in larger scale projects, a

consortium of local businesses could work together to bid on these larger projects

and undertake group buying of materials to reduce costs for smaller operators.

Additional promotion of construction as a rewarding career to new and existing

entrants to the workforce. Stimulating the housing construction industry has strong

Page 2 of 84

Mid North Coast Affordable Housing Report

potential to boost employment in the region and through this the Mid North Coast

can offer a great career and lifestyle package.

For the stimulus of the housing construction market on the Mid North Coast in the

current softening labour market, particular focus should be given to targeting

existing support programs and the development of new programs where needed, to

meet the specific needs of the industry.

There are significant non-residential construction projects currently in the region, or

projects which have been awarded funds and yet to commence (including Pacific Highway

upgrade, upgrades to the Port Macquarie and Kempsey Hospitals, regional airport upgrades,

Charles Sturt University campus e.t.c). Although this does not address affordable housing,

increases in construction in the region supports the regional economy and skills

development. There is concern among local industry of the over utilisation of external

companies and employees for large projects and that options to increase local supply

include:

Supporting the formation of local consortiums where businesses team up to work

together as a group to take on big scale projects that would normally go to

companies from outside the region

Group buying of construction materials to reduce costs for smaller operators, and to

promote collaboration

Opportunity for filtering tenders through local industry companies to help local

businesses apply and keep on track with what tenders are available.

The findings highlighted in relation to identifying potential models and projects within the

affordable housing sector which are appropriate to the Mid North Coast are:

working with the Indigenous community and the Local Aboriginal Land Councils in

the region to identify and develop affordable housing;

Page 3 of 84

Mid North Coast Affordable Housing Report

Discussions be held with all relevant parties in regards to the collaborative model

proposed which utilises available land from the Department of Housing, churches or

local aboriginal land councils in combination with a collective of local builders;

Realising the potential of the older population in the Mid North Coast region to

stimulate investment in housing – both in the redevelopment of some housing stock

and in the development of new investment strategies for the region’s older

population;

Increasing the local supply of inputs into the Residential Construction sector in the

region. The sector currently imports $146 million (2010-2011 financial year) which

supports 357 jobs outside of this region. This could reduce costs of materials as well

as increase employment opportunities and boost the regional economy.

Unlocking the ability of local government to deliver affordable housing through both

new and established mechanisms; and,

Attracting new participants into the housing and land development industries in the

Mid North Coast region. Such additions have the potential to both add investment

to the sector and encourage innovation amongst existing participants.

Page 4 of 84

Mid North Coast Affordable Housing Report

Contents

Acknowledgements................................................................................................................................. 1

Executive Summary................................................................................................................................. 2

Introduction ............................................................................................................................................ 6

Affordable Housing on the Mid North Coast .......................................................................................... 7

Key Points............................................................................................................................................ 7

Introduction ........................................................................................................................................ 8

Demand for Affordable Housing ......................................................................................................... 9

Regional Demographics ................................................................................................................ 10

Supply of Affordable Housing ........................................................................................................... 23

Barriers to Supply .......................................................................................................................... 23

Stakeholder Plans and Government Programs ................................................................................. 32

Target Groups for Housing Developments on the Mid North Coast ................................................ 36

Workforce Development ...................................................................................................................... 39

Key Points.......................................................................................................................................... 39

Introduction ...................................................................................................................................... 40

Training Volumes .............................................................................................................................. 41

Issues and Completion Rates ............................................................................................................ 42

Pathways into Construction .............................................................................................................. 46

Employment Opportunities and Outcomes ...................................................................................... 47

Models and Project ideas for the Mid North Coast .............................................................................. 55

Affordable Housing Models and Financing ....................................................................................... 55

Potential Projects for the Mid North Coast ...................................................................................... 60

Consortium of Local Builders ........................................................................................................ 60

Local Aboriginal Land Councils ...................................................................................................... 61

Collaborative Model with NSW Department of Housing .............................................................. 62

Taking Advantage of Demographic Opportunities ....................................................................... 66

Mobilising Local Government Potential........................................................................................ 67

Seeking New Participants in the Housing and Development Industry ......................................... 69

Conclusions and Recommendations ..................................................................................................... 70

References ............................................................................................................................................ 73

Appendices............................................................................................................................................ 77

Page 5 of 84Mid North Coast Affordable Housing Report

Introduction

This is the final report in a research project that has been undertaken for the Department of

Education, Employment and Workplace Relations (DEEWR) by Regional Development

Australia Mid North Coast. The purpose of this research project is to identify:

The common issues, barriers, gaps and opportunities of affordable housing

development in the Mid North Coast

Workforce development opportunities and barriers to support construction in the

Mid North Coast

Potential models and/or projects within the affordable housing sector which are

appropriate to the New South Wales Mid North Coast.

The methodology used for this research project was a combination of desktop research and

analysis, the use of focus groups with key stakeholders and discussions with relevant parties

in regards to potential housing models. Desktop research and analysis was used to:

detail current issues/trends and regional data relevant to affordable housing,

construction, skills and employment,

analyse construction related apprenticeships and traineeships volumes and

completions in the region, and

explore financing mechanisms for affordable housing and available government

support programs.

The desktop research and analysis was complemented with two focus group sessions with

stakeholders involved in housing and construction in the Mid North Coast region. Focus

group participants involved representation from Real Estate Agents; Lenders; Trainers;

Housing and Construction industry bodies (HIA, MBA, CPSISC); Local Aboriginal Land

Councils; local builders and developers, Local Council planners and others. The sessions

were used to gather stakeholder input on major issues and potential solutions and

opportunities for affordable housing development in the region.

Page 6 of 84Mid North Coast Affordable Housing Report

Affordable Housing on the Mid North Coast

Key Points

Regional demographic pressures are adding to the demand for increased affordable

housing, including:

o A high percentage of elderly in the region (21%, 65 years and over) compared

with NSW (14.7%, 65 years and over).

o The median Mid North Coast income represents 67% of the NSW median

income and 29% of people over 15 years in the Mid North Coast earn less

than $299 per week compared with only 2.7% in NSW.

o A high proportion of the population identifying as Aboriginal or Torres Strait

Islander – 5.1% of the region compared with 2.5% of NSW.

o Rents and mortgages are increasing at a higher rate than incomes in the

region. Between 2006 and 2011, incomes have increased 3.4% per annum.

However, rents have increased 6.7% per annum and mortgage repayments

4.8% per annum.

o There is overcrowding present in many dwellings in the region, for example

105 households report more than 3 people living in a one bedroom dwelling

and 52 dwellings in one council area have 5 people or more living in 2

bedroom accommodation.

The residential construction sector is currently very soft and the majority of work in

this region is on alterations and additions to existing buildings, that is not new builds.

The Residential Construction sector on the Mid North Coast has declined 6.7% in

total turnover from the 2009-10 to the 2010-11 financial year.

The current stock of housing on the Mid North Coast includes only 4.3% of dwellings

committed as State Housing/housing co-operatives, community or church group

housing and there are significant waiting times for general community housing

applicants.

The main barriers to the supply of affordable housing include: expenses/financial,

planning and regulations.

Page 7 of 84Mid North Coast Affordable Housing Report

Median rental yields in the region do not exceed 4.8%. Unattractive rental yields

and current market confidence are barriers to encouraging private investment into

the housing market.

Introduction

Housing is a central component to stability of one’s life. The importance of housing is not

represented by the current affordability and accessibility of the housing market. In

particular the housing market of the Mid North Coast is under pressure to provide more

affordable housing to the local population.

This pressure within the housing market is related to particular demographics that represent

a demand for a larger proportion of affordable housing to be present in the region. A higher

percentage of elderly are concentrated in the region (21%, 65 years and over) compared

with NSW as a whole (14.7%, 65 years and over). Furthermore the Mid North Coast has a

much higher percentage of people both earning less than the NSW median income as well

as a higher percentage of people earning in the low income bracket (29.2% of people aged

over 15 in the Mid North Coast earn less than $299 a week compared with 2.7% in NSW) .

There have been a number of reports which further replicate the need for affordable

housing in the Mid North Coast.

Key points addressed in the foreword of the 2010 report ‘Going nowhere, how the planning

system and development levies are ruining NSW’ provide an adequate understanding of

why the affordable housing issue is of high importance in the Mid North Coast. Mentioned

in the foreword is the concern found by BIS Shrapnel which includes but is not limited to;

the concern that NSW is poorly prepared to deal with the challenges of an aging population.

The Mid North Coast has 36.6% of its population over 55 compared with 26.3% overall in

NSW. This suggests that if NSW as a whole has concerns regarding caring for the aging

population then the Mid North Coast in particular needs to consider the findings. These

Page 8 of 84Mid North Coast Affordable Housing Report

findings include determining the current state of the housing and construction market on

the Mid North Coast which has been described as ‘poor, slow and bad’ by stakeholders

within the region.

The demand for housing has slowed in the region and is represented by the decline in

residential construction. The Residential Construction sector on the Mid North Coast had

turnover of $775.977 million (financial year 2010-11), this represents a decline of 6.7% from

the previous financial year and this decline is on par with the New South Wales

results. Further, the Residential Construction sector maintains 2.1% of jobs in the Mid North

Coast region and the broader construction industry supports 6.5% of jobs in the region

(REMPLAN 2006). Affordability of housing has a direct impact on the construction industry

and one in which shifts employment, capital and growth in the region.

The state of the housing industry across Australia is in a slump and has been for some time

now. For the Mid North Coast this has been reflected in a slowing of the housing and

construction industries. Stakeholders within the community described the current state of

the housing and construction market as ‘bad’ but recognised that it is ‘still not as bad as

other parts of Australia’ (Focus Group Attendant 2012). Maintaining an employee in the

region is described to be ‘difficult’ as most of them left to ‘chase the dollars in the mines’

(Focus Group Attendant 2012). For the small amount of construction that is happening in

the region and that is dedicated to housing, the overall opinion was that any housing that is

being produced is not servicing the affordable housing market.

Demand for Affordable Housing

Affordable housing is described to be where no more than 30% of a household’s weekly

income is dedicated to housing costs and the household’s weekly income is in the bottom

40% of the earning population (Disnay 2007). This benchmark is to allow for other basic

needs of the household to be met. Although this is a generally accepted benchmark

Page 9 of 84Mid North Coast Affordable Housing Report

definition for ‘affordable housing’, the scope of this project is not limited to a strict

definition and has wider objectives of identifying ways to increase housing

supply/construction activity and the employment outcomes.

Regional Demographics

The demand for housing in the Mid North Coast can be exemplified by a number of cases.

Quantitative analysis of the economic conditions of the region, in particular incomes,

mortgages, rent, housing costs and demographics have an impact on the needs of the Mid

North Coast. Table 1 shows the breakdown of median rent by local government area on the

Mid North Coast and calculates the affordability of rental housing.

Table 1. Rental affordability on the Mid North Coast

Median Median Weekly % of % of local

Weekly Household income government area

Local

rent Income spent on earning below the

Government

rent income bracket that

Area ($) ($)

holds the median

household income

Port Macquarie 250 838 30% 32.5%

Taree 200 770 26% 22.7%

Bellingen 220 785 28% 35%

Coffs Harbour 255 900 28% 29.9%

Kempsey 190 752 25% 23.5%

Nambucca 195 702 28% 25.3%

Source: ABS Census of Population and Housing 2011

Page 10 of 84Mid North Coast Affordable Housing Report

The rental figures alone suggest that rental housing on the Mid North Coast is affordable to

anyone who earns the median weekly income or above. The last column in Table 1 identifies

the proportion of the population that earns a weekly household income below the median

income identified in column 3 – for example, Port Macquarie has 32.5% of its households

earning less than $800-$999 a week.

The affordability of rental properties is also skewed by the 16% of rental properties that are

managed by the State or Territory housing authority or is classified as a housing co-

operative, community or church group housing. These groups provide lower cost renting for

a proportion of those in the low income bracket. This brings down the median cost of

weekly rent for the Mid North Coast. According to Disnay (2007) the provision of this service

is falling with a 30% decrease in the opportunity to rent social housing having occurred over

the last decade.. This decrease is equivalent to an extra 100,000 social housing dwellings

today if the rate of supply had been maintained by the Australian government (Disnay

2007).

The 2012-2013 NSW budget supplied some changes that will impact affordability of housing

at various levels. The Building the State package plans to deliver $561 million towards

funding infrastructure. This intends to accelerate housing construction in NSW (NSW State

Government 2012). The benefits of this funding include first homebuyers of new homes.

The scheme identifies this group as being up to $19,245 better off once purchasing their

new home since the release of the new budget. This concentration of funding supplied to

those who are purchasing new homes plans to stimulate new home construction in NSW

(NSW State Government 2012).

Figure 1 below indicates the Mid North Coast has a large proportion of the population in the

mature age bracket. It also indicates the low proportion of 20-30 year olds in the region.

Page 11 of 84Mid North Coast Affordable Housing Report

Figure 1. Population distribution by age for Mid North Coast (2011)

Population distribution by age Mid North Coast

(2011 Census)

85 years & over 2.9%

75-84 years 7.2%

70-74 years 5.2%

65-69 years 6.5%

60-64 years 7.5%

55-59 years 7.3%

50-54 years 7.5%

45-49 years 6.8%

40-44 years 6.1%

35-39 years 5.3%

30-34 years 4.3%

25-29 years 4.1%

20-24 years 4.7%

15-19 years 6.3%

10-14 years 6.6%

5-9 years 6.0%

0-4 years 5.8%

0.0% 1.0% 2.0% 3.0% 4.0% 5.0% 6.0% 7.0% 8.0%

Source: using data from ABS Census of Population and Housing 2011

The population distribution graph is representative of the areas of concern in the region for

both affordable housing and work force development. Having such a high proportion of

elderly in the region demands particular services. Furthermore the concave nature incurring

the 20-34 year age group identifies a lack of young adults in the region. Qualitative findings

on the desires the population have in regards to their financial and lifestyle circumstance

should also be considered. Foremost, consideration of the financial status of the population

of the Mid North Coast identifies the demand for affordable housing.

Page 12 of 84Mid North Coast Affordable Housing Report

NSW incomes have had a 3.1% increase per annum between 2006 and 2011. Incomes in the

Mid North Coast have risen by 4% per annum between 2001 and 2006 and a further 3.4%

per annum between 2006 and 2011. Data reveals that although incomes in the Mid North

Coast have risen an extra 0.3 % points per annum (2006-2011) compared with NSW as a

whole, Mid North Coast income is still largely below the median income for NSW. The 2011

census data revealed the Mid North Coast median income represents only 66.8% of the

median NSW income.

In context, rent has increased 5.9% per annum between 2001 and 2006 and 6.7% per

annum between 2006 and 2011 in the Mid North Coast. Mortgage repayments have also

increased in the region from 6.1% per annum between 2001 and 2006 as well as a further

4.8% per annum between 2006 and 2011. Therefore adding to the affordability challenge is

rent and mortgage repayments increasing at a higher rate than income levels. This increased

cost of mortgages is causing a larger proportion of the region to rent as oppose to purchase

a house. Table 2 shows the breakdown of tenure type over a period of time. This identifies

the proportion of the population owning outright, repaying a mortgage and renting. It also

shows a comparison between the Mid North Coast region and NSW.

Table 2. Tenure type* of dwellings in the Mid North Coast and New South Wales

Owned with a

Owned outright mortgage Rented

Area 2001 2006 2011 2001 2006 2011 2001 2006 2011

Mid North Coast 46.6% 41.3% 39.9% 20.7% 25.8% 26.1% 27.2% 26.4% 27.4%

NSW 41.1% 33.2% 31.9% 23.3% 30.2% 31.9% 28.8% 28.4% 29.1%

Source: using data from ABS Census of Population and Housing 2011

* Figures do not equal 100% as there is a small portion of the population not stating tenure type or living in an

‘other’ tenure type.

Page 13 of 84Mid North Coast Affordable Housing Report

Table 2 demonstrates the largest decline has occurred in the proportion who own their

home outright. There has been an increase in both the percentage of the Mid North Coast

and NSW who own their home with a mortgage. Rental properties have remained similar.

This identifies that a larger proportion of the population has the potential to be placed in

housing stress. The proportion of outright home ownership has declined in the region by

6.7% points between 2001 and 2011. The process of purchasing a house is a large financial

commitment and one in which unfortunately a proportion of the Mid North Coast cannot

manage affordably.

Table 3 below advises the loan amounts that are affordable based on the median weekly

incomes in the Mid North Coast. Table 3 also indicates the median amount households in

the Mid North Coast are paying towards rent. This demonstrates that based on the actual

median mortgage repayments all areas in the Mid North Coast are paying a mortgage that

exceeds 30% of median income.

Page 14 of 84Mid North Coast Affordable Housing Report

Table 3. Affordable Mortgage in the Mid North Coast considering interest rates and median household incomes

30 year repayment period

6% interest 6.5% interest 7% interest

rate rate rate

Median weekly 30% 30% of Mortgage Mortgage Mortgage Actual

family income Income Monthly serviceable serviceable serviceable median

($) Weekly Income ($) based on 30% based on 30% of based on 30% Mortgage

($) of median median weekly of median Repayments

weekly family family income weekly family ($)

Area

income income

Coffs Harbour 1,097 329.10 1,426.10 237,500 225,500 214,400 1,575

Port Macquarie 1,008 302.40 1,310.39 218,500 207,300 197,000 1,650

Taree 930 279.00 1,209.00 201,700 191,300 181,700 1,300

Kempsey 902 270.60 1,172.59 195,500 185,500 176,200 1,300

Nambucca 853 255.90 1,108.90 184,900 175,300 166,600 1,200

Bellingen 938 281.40 1,219.39 203,400 193,000 183,300 1,300

Source: ABS Census of Population and Housing 2011

Page 15 of 84Mid North Coast Affordable Housing Report

Table 4 compares the median house sale price in 2011 on the Mid North Coast with an

affordable mortgage based on a 6% interest rate. This indicates that for every local

government area in the Mid North Coast the median house price exceeded the affordable

mortgage amount. The largest differences between median house prices and an affordable

mortgage level occur in Coffs Harbour, Port Macquarie, Nambucca and Bellingen local

government areas.

Table 4. Median house prices in the Mid North Coast compared with affordable mortgages

Median House prices 2011 Affordable Mortgage

calculated on a 6% interest

rate using 30% median

Local Government Area family income

Coffs Harbour 366,750 237,500

Port Macquarie 388,500 218,500

Taree 229,500 201,700

Kempsey 207,500 195,500

Nambucca 300,500 184,900

Bellingen 360,000 203,400

Source: Real Estate.com.au (Median house prices 2011)

Housing stress can be largely a financial concern, however there are other forms of housing

stress which are equally important and should be considered. Overcrowding in many

dwellings reiterates the need for more affordable housing in the Mid North Coast. The 2011

ABS census data reports that there are 105 households in the Mid North Coast where more

than 3 people are living in a one bedroom dwelling. In particular 17.8% of these households

are found in Coffs Harbour. Furthermore, Kempsey has 52 dwellings where 5 people or

Page 16 of 84Mid North Coast Affordable Housing Report

more are living in a 2 bedroom household. Overcrowding in houses can be an indication of

the limited affordable houses available.

The concern about the lack of affordable housing is widely spread with “nine out of ten

Australians worried about a lack of infrastructure and affordable housing given the growing

and aging population” (Advertiser 2010). The aging population is evident in NSW with a

rising median age from 35 in 2001 to 38 in 2011. The Mid North Coast has a median age of

45.6 years as of 2011; which is 7.6 years older than the state average.

These demographics influence the demand for particular housing structures. Age structure

and family composition impact what type of dwelling is needed. The construction of houses

to meet these needs will require innovative ideas surrounding what a home needs to be.

The national housing supply council has created a projection of the household arrangement

changes from 2010-2030. It projects that two-parent families will decrease from 31.4% of

households to 27.4%. Furthermore the report finds that lone households will increase from

26% to 31.6% (NHSC 2011). This will create a substantial increase in demand for different

types of dwellings with an estimated 42.7% increase in households living in flats as well as a

41.7% increase in households living in semidetached dwellings. The Australian Construction

Industry Forum reported that there will be an increase in improvements of existing housing

over the next decade.

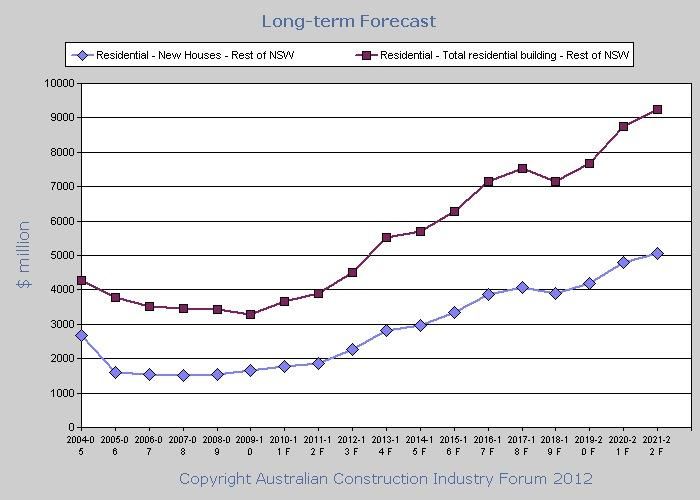

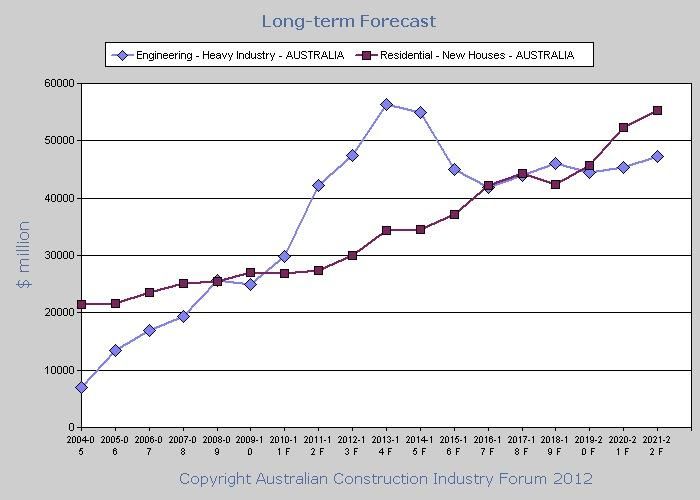

Figure 2 replicates these projected shifts with a sharper increase in 2013 for total residential

building compared with the increase in new houses. This total residential building

represents alterations on existing houses including extensions and additions.

Page 17 of 84Mid North Coast Affordable Housing Report

Figure 2. Long Term Forecast Residential building construction in the rest of NSW

(i.e. excluding capital cities)

Source: The Australian Construction Industry Forum 2012

Further, the Australian Construction Industry Forum forecasts indicate that by 2022,

alterations and additions will be valued in today’s dollars at over $70 billion. This will

surpass new home development at $25 billion, and units and townhouses at $26 billion

(ACIF 2012).

The demand for a shift in the dwelling types available in the Mid North Coast is evident with

a 0.8% increase per annum from 2006 to 2011 in separate dwelling structures compared

with a 1.7% increase per annum from 2006 to 2011 in semi-detached or terrace houses. This

could be related to a number of factors including the above shift in dwelling occupancy.

Secondly, smaller dwellings are often a more affordable option. Thirdly many people are

opting to live closer to urban areas as opposed to moving to outer suburbs. To counter the

Page 18 of 84Mid North Coast Affordable Housing Report

demand for urban living higher density housing is being built in the urban areas. This higher

density housing is described as urban infill. The Australian Construction Industry Forum

(2012) indicated this urban infill will cause many older single dwelling structures to be

removed in order to make space for higher density living. In regards to the housing needs of

the Mid North Coast consideration of dwelling types is important in catering for the large

proportion of mature aged persons living in the region.

The Mid North Coast has 36.6% of its population over 55 compared with 26.3% overall in

NSW. Having such a high percentage of elderly persons within the population of the Mid

North Coast creates specific demand issues for both affordability and dwelling type.

Research suggests that by 2021 four in every ten households will be occupied by at least one

older person, with a majority living alone or in a couple (AHURI 2004). Those living alone will

not only be dominated by an older population but a shift to single person households in all

age groups is expected. This shift is being driven by a falling marriage rate, low birth rates

and high rates of divorce and separation.

Previously home ownership for those 65 years and over has been 73% with another 6%

close to home ownership (AHURI 2004). However research by the Australian Housing and

Urban Research Institute finds that the absolute number of people entering old age as

renters will increase and a larger proportion will be in the private rental market. The Mid

North Coast will need to increase the availability of affordable housing and dwellings that

are appropriate for an aging population. At present housing construction is dominated by

family housing and has not yet adjusted to the social trends. Stakeholders in the Mid North

Coast identified that builders were encouraging their clients to build more affordable

housing that can be used for a range of purposes other than family housing. This makes for a

more affordable build as well as a good opportunity to sell off or rent out.

Alterations and additions have been one option greater numbers of households have turned

to in response to the challenge of securing affordable housing. Alterations and additions on

Page 19 of 84Mid North Coast Affordable Housing Report

existing houses have risen between 2008 and 2011. The 2007-2008 data reveals there were

976 applications for development approval for alterations and additions and in 2010-2011

this had increased to 1,229 in the Mid North Coast region. Stakeholders within our region

verified this trend with builders discussing a much larger proportion of their work is

dedicated to smaller building works, alterations and additions than in previous years.

Residential alterations and additions comprised 40% of all approvals in 2010-2011 (NSW Dpt

Planning and Infrastructure 2011). Alterations and additions are allowing children to stay in

the home for a longer period of time. Other options include secondary dwellings and granny

flats of which increased 11% from 2009-2010 to 2011 (NSW Dpt Planning and Infrastructure

2011).

State or Territory authority dwellings, housing co-operatives, community and church group

housing provide housing to those on a low income. The Mid North Coast has 4.26% of

dwellings committed as State or Territory housing/ housing co-operatives, community or

church group housing. This percentage in regards to the total amount of dwelling structures

on the Mid North Coast has had minimal change since 2001. In 2001 State or Territory

housing/housing co-operative, community or church group housing made up 4.54% of

dwellings in the Mid North Coast. This had further declined by 2006 to make up 4.30% of

dwellings on the Mid North Coast.

In addition to the social and community housing stock in the region representing only 4% of

dwellings, there are significant pressures from large waiting lists for social/community

housing in the region (Table 5) which further support the demand for affordable housing.

The majority of locations have waiting times which exceed 5 years for certain dwelling types

and several locations that have an over 10 year wait.

Page 20 of 84Mid North Coast Affordable Housing Report

Table 5. Expected wait times for general social and community housing applicants in the

region (as at 30 June 2012)

Dwelling size

Location Studio 1 bedroom 2 bedroom 3 bedroom 4 bedroom

Taree n/a 2-5 years 2-5 years 5-10 years 2-5 years

Port Macquarie 2-5 years 2-5 years 5-10 years 10+ years 10+ years

Kempsey n/a 2-5 years 2-5 years 2-5 years 2-5 years

Macksville n/a 5-10 years 5-10 years 5-10 years 5-10 years

Bellingen n/a 5-10 years 5-10 years 2-5 years 5-10 years

Dorrigo n/a 5-10 years 10+ years 5-10 years 10+ years

Coffs Harbour n/a 2-5 years 5-10 years 10+ years 5-10 years

Laurieton n/a 2-5 years 10+ years 5-10 years 5-10 years

Wauchope n/a 2-5 years 2-5 years 2-5 years Up to 2 years

Woolgoolga n/a 5-10 years 10+ years 5-10 years Up to 2 years

Crescent Head n/a 2-5 years Up to 2 years 10+ years n/a

Wingham n/a 5-10 years 10+ years 10+ years 10+ years

Nambucca n/a 5-10 years 5-10 years 5-10 years 2-5 years

Urunga n/a 5-10 years 5-10 years 2-5 years Up to 2 years

Source: NSW Government Family and Community Services, Housing NSW, Housing

Pathways waiting times. Shaded cells on the table illustrate waiting times in excess of 5

years.

The seriousness of the housing market in Australia has been identified by global

organisations. The United Nations Human Rights Council Geneva report identified Australia

as being in the grip of a ‘serious national housing crisis characterised by reductions in public

housing.... an acknowledged housing affordability crises and no real reductions in the

number of homeless’ (Kothari 2007). The report identifies 9% of indigenous peoples as

being homeless. The Mid North Coast has 5.1% of its population identifying as Aboriginal or

Torres Strait Islander compared with 2.5% of NSW’s population in 2011 (Figure 3). The high

rate of indigenous homelessness on a national level, in conjunction with this regions higher

than state average indigenous population adds to the concern regarding the issue of

accessibility and affordability of housing in the region.

Page 21 of 84Mid North Coast Affordable Housing Report

Figure 3. Proportion of population identifying as Aboriginal or Torres Strait Islander

Aboriginal and Torres Strait Islander Population

Growth

6.0%

5.0%

4.0%

3.0%

2.0%

1.0%

0.0%

2001 2006 2011

Mid North Coast NSW

Source: ABS Census of Population and Housing 2011

In addition to the current and trending demographics of the Mid North Coast adding

pressures to the demand for affordable housing, there is a considerable amount of

construction activity committed for the region which will also increase the need for

accommodation for additional workforce required during the construction phases and the

increases in employment post construction. For example, the demand on the health sector

in the Mid North Coast region could add 2,000 workers over the next five years. Some of

the key construction projects in the region include:

Upgrades to Port Macquarie Hospital ($110 million)

Upgrades to Kempsey Hospital ($80 million)

Upgrades to Port Macquarie, Kempsey and Taree airports

Pacific Highway upgrades

Construction of Charles Sturt University Port Macquarie campus

Page 22 of 84Mid North Coast Affordable Housing Report

Supply of Affordable Housing

The supply of affordable housing is not adequate for the demand identified in the Mid North

Coast Region. The stakeholders involved in the affordable housing market from both the

supply and demand side identify planning, regulatory and financial barriers as being the

most significant causes of not meeting the demand.

Barriers to Supply

Consideration of literature resulted in consultation, through focus groups, with a number of

stakeholders involved in the housing market asking ‘What are the main barriers to the

supply of affordable housing?’ The discussion returned similar answers that mirrored the

literature:

Expense/finance- related to levies, land costs and contributions. ‘The cost for a

developer to develop land can be up to $30,000 per block... which is a large financial

commitment for developers when the housing market is so slow’ (Focus Group

Attendant 2012).

Planning- including complexities, continued changes and mentions that ‘a good

amount of knowledge of planning is needed before entering the market’ (Focus

Group Attendant 2012).

Regulations- including legislations and timeframes in relation to both planning and

regulatory processes and quantity of legislative bodies.

Expense and Financial Barriers

One stakeholder identified that ‘The expense of housing compared with the incomes in

particular areas of the Mid North Coast region makes purchasing a house often

unattainable... this is reflected by the main industries of employment in the region’ (Focus

Group Attendant 2012). There is a considerable amount of employees in the region

employed on a casual basis and/or within seasonal sectors – in particular the Tourism sector

Page 23 of 84Mid North Coast Affordable Housing Report

supports 7.5% of jobs in the Mid North Coast and the Retail Trade sector supporting 14.9%

of jobs (REMPLAN 2006).

Financial barriers to supply of affordable housing are a large concern for all parties involved

in the housing industry. The obvious concern would be the personal finance of the party

wishing to invest in housing either through renting, purchasing for private use or using the

housing industry as a way to generate investment. However stakeholders identified the

large financial contribution builders are outlaying whilst lowering their profit margins to

maintain employment. Many of the stakeholders involved in the consultation process

identified the costs that builders are absorbing to keep the residential construction industry

afloat have been growing. Growth in the industry will prop up expenditure in the region and

encourage further construction.

Low rental prices can be a cause of insufficient private investment into the housing market.

Evidence of this can be viewed in the calculated rental yields of each local government area.

Rental yield according to the InvestEd group (2006) is a measure of the percentage of

income you receive back from a housing asset. Literature suggests private investment into

the housing market is an important component to improving the state of affordable

housing.

Table 6 examines the rental yield based on the median house prices and median rental cost

for each Mid North Coast local government area in 2011. For investment purposes an

attractive rental yield would be around 5.8%-6.5% and according to InvestEd Group (2006)

any yield below this would not usually be an attractive investment. First home buyers are

being encouraged to purchase through the First Home Owners Scheme. Australia has seen a

drop of first home owners as a percentage of all purchases from 21.8% in 1996 to only

17.5% in 2007 (Hill & Tiley 2010). The NSW Government Building the State package is a

stimulus to encourage first home owners to enter the market. In particular the package

Page 24 of 84Mid North Coast Affordable Housing Report

encourages first home owners to build new homes which will boost the residential

construction industry.

Table 6. Rental Yield Comparisons for the Mid North Coast

Local Median Median Rental Yield

Government House Annual

Australia prices 2011 Rent 2011

Port Macquarie 388,500 13,000 3.3%

Bellingen 360,000 11,440 3.2%

Kempsey 207,500 9,880 4.8%

Nambucca 300,500 10,140 3.4%

Taree 229,500 10,400 4.5%

Coffs Harbour 366,750 13,260 3.6%

Source: ABS Census of Population and Housing 2011

Planning and Regulation Barriers

The Australian Housing and Urban Research Institute (AHURI) have identified planning

system complexity as a concern that contributes to the affordability of houses. The

Weekend Australian (2012) reported that affordability issues are “largely the result of

planning and regulatory complexities and costs” (Studdert, 2012, p.6). The planning and

regulation systems in place on the Mid North Coast vary between local government areas.

This is identified in the region and is noted in the Port Macquarie Hastings Council’s

affordable housing strategy where it states ‘‘opportunities to streamline the development

assessment process should be explored” (SGS Economics and Planning 2006, p. 17).

Page 25 of 84Mid North Coast Affordable Housing Report

Streamlining this process would make the entire procedure more efficient for those

involved.

Section 94 contributions are one such difference between councils in the region. Additions

to existing dwellings such as granny flats involve different contributions depending on the

local government area the dwelling is located. Some council’s assume the contribution

based on the building cost and others classify it as an addition which requires a smaller

contribution fee.

The section 94 contributions also identify inconsistencies with planning systems which can

add to the financial uncertainty of developments. Section 94 or 94a contributions can be at

the discretion of councils in relation to the type of development and the impact the

development will have on community resources. This makes it difficult for costs related to

the planning process to be factored into financial planning. Stakeholders in the local region

described section 94 contributions as a factor that impacts the way in which land is utilised.

One stakeholder described this in reference to building duplexes, which are often a more

affordable option for consumers as well as making greater use of the available land.

However, the section 94 contribution incurs a higher fee for the construction of duplexes on

a single block of land; for a developer that means incurring a larger initial outlay. As the

stakeholders advised at the focus group sessions, many developers are waiting for the

market to pick up before continuing any further development and the prospect of a greater

outlay for duplexes to be built in an uncertain environment is a significant risk. The term

used by many of the stakeholders was ‘sitting on their hands’ in reference to waiting for the

market to pick up (Focus Group 2012). The supply of construction and housing services is

ready and prepared to start building for when the market demand returns.

AHURI identifies uncertain development application timeframes as a barrier to the supply of

affordable housing. Holding cost is identified by the Australian government as one such

supply side barrier. Holding costs refer to the financial cost incurred due to the lengthy

Page 26 of 84Mid North Coast Affordable Housing Report

timeframes it can take for development and purchasing to pass through the systems in place

(FAHCSIA 2012). The Housing Affordability Fund is a direct result of the government’s

attempt to lower these holding costs. Timeframes can vary depending on a range of factors.

The uneven distribution of development application timeframes on the Mid North Coast

illustrates this variance. Table 7 shows the average amount of time it takes to get

development application approval in the local government areas of the Mid North Coast.

Table 7. Average amount of days for development application processing in the Mid North

Coast by local government area 2010-2011

Mean gross Mean gross Mean gross Mean gross

time for DA days for new days for days for new

determined single alterations second

2010/2011 dwelling DA and occupancy DA

determined additions DA determined

2010/2011 determined 2010/2011

2010/2011

Local Government Area

Bellingen Shire Council 91 89 71 129

Coffs Harbour City Council 73 61 35 92

Greater Taree City Council 82 74 48 55

Kempsey Shire Council 41 39 26 53

Nambucca Shire Council 69 49 50 93

Port Macquarie-Hastings 81 62 61 130

Council

Mid North Coast 72.8 62.3 48.5 92

Source: Local Development Performance Monitoring spreadsheet 2010-2012, NSW

Department of Planning and Infrastructure

Page 27 of 84Mid North Coast Affordable Housing Report

The average number of days for a development approval on the Mid North Coast is 72.8

days which compares with an average of 59.3 days for NSW. The Mid North Coast had only

2% of all development applications refused in 2011, suggesting that the approval of

development applications is not the concern rather the timeframe it takes to gain approval.

AHURI also identifies a lack of adequate resources at the local government level as one

explanation to the timeframes associated with planning regulations. One impact on

planning regulation timeframes is the amount of staff available to process applications.

There has been a decrease of staff on the Mid North Coast allocated to development

application processing from 2007-08 to 2010-11 (Table 8).

Table 8. Distribution of equivalent full time staff allocated to Development Applications on

the Mid North Coast and equivalent change in timeframes for determination

Full time equivalent Full time equivalent % change in mean

staff 2007-2008 staff 2010-2011 time for DA

determined

2007/2008-

Local Government Area 2010/2011

Bellingen 3.5 3 -11%

Coffs Harbour 16 8.5 9%

Greater Taree 6 9 17%

Kempsey 3 2.75 -59%

Nambucca 3 3 -44%

Port Macquarie 6 6 11%

Mid North Coast 37.5 32.25 -18%

Source: Local Development Performance Monitoring Spreadsheet 2007/2008-2010/2011,

NSW Government Department of Planning and Infrastructure

Page 28 of 84Mid North Coast Affordable Housing Report

Table 8 shows the variation of staff allocations across the Mid North Coast and the increase

or decrease that has occurred, between 2007-2008 and 2010-2011, in the amount of time it

takes to process an application. The changes are exemplified when compared with the

changes in staff in the particular government areas. Changes are evident in the 17% increase

in days it takes to receive development approval in the Greater Taree area considering there

has been an increase in staff (6 to 9 FTE’s). Further changes are found with the 11% increase

in time it takes to receive development application approval in the Port Macquarie and

Hastings area as staff allocations remain the same. These cases represent the

inconsistencies mentioned in regards to planning processes. There has been an overall 18%

decrease in the amount of time it takes to receive development approval in the Mid North

Coast over the period 2007-08 to 2010-11. Further indications include the volume of

development applications that are being determined in the Mid North Coast (Table 9).

Table 9. Number of development applications processed in 2007-2008 and 2010-2011

Number of DA Number of DA % change in number

determined determined of DA's determined

Local Government Area

2007-2008 2010-2011 ‘07/’08- ‘10/’11

Bellingen Shire Council 347 269 -22%

Coffs Harbour City Council 906 1,044 15%

Greater Taree City Council 788 541 -31%

Kempsey Shire Council 310 280 -10%

Nambucca Shire Council 289 219 -24%

Port Macquarie-Hastings Council 572 576 1%

Mid North Coast 3212 2,929 -9%

Source: Local Development Performance Monitoring 2007/2008-2010/2011, NSW

Department of Planning and Infrastructure

Page 29 of 84Mid North Coast Affordable Housing Report

Table 9 identifies that there has been a 9% decrease in the number of development

applications that were determined on the Mid North Coast between 2007-2008 and 2010-

2011. Combining this data with the data presented in Table 2 allows further comparisons to

be drawn. Previously it was noted that Greater Taree has had a 33.3% increase in the

number of staff allocated to development application processing and their timeframe for

development application approval had increased by 17%, while processing 31% less

applications. The Local Development Planning Monitor 2010-2011 (NSW Dpt of Planning and

Infrastructure) identifies that it takes an average of 56 days for applicants to return further

information required to process the application. Improving these time delays would allow all

applications to be processed faster. The amount of development applications determined

can represent the amount of construction occurring/planned for the region. An increase in

development applications would be representative of an increase in planned construction. A

positive change in the timeframes associated with the development application process may

encourage further development in the Mid North Coast.

Regulation of the housing industry falls subject to different levels of government. The

National Affordable Housing Agreement identifies the responsibilities of different areas of

government when it comes to the delivery of services in relation to the housing and

homelessness sector – this is summarised in Figure 4. The housing industry is highly

regulated and a recent regulation, for example energy efficiency, is an added cost for people

building a new home (COAG 2009). Any regulatory change, such as energy efficiency, that

affects the housing industry has an impact on housing affordability. Cost effective regulation

needs to be considered in order to maintain an industry that is affordable to more of the

population.

Page 30 of 84Mid North Coast Affordable Housing Report

Figure 4. Responsibilities and roles of government for affordable housing

Source: Council of Australian Governments 2009, National Affordable Housing Agreement

Comments from the focus group identified what the stakeholders argued were measures to

make the regulation more affordable. One attendant suggested ‘doing away with the

decorations (kerb and guttering, pathways and tree lined streets)’ on developments and

letting the market maintain this area (Focus Group 2012). Another respondent suggested

this kind of approach may cause areas to be segregated by those who care for aesthetics

and those who don’t.

The regulatory governments employ policies which have a positive impact on housing

affordability when it comes to financial assistance. The federal government offers rent

assistance and home purchase assistance which are crucial to supporting a proportion of the

Page 31 of 84Mid North Coast Affordable Housing Report

population in achieving affordable housing (FAHCSIA 2012). At present none of the 6

councils within the Mid North Coast employ any affordable housing policies. Port Macquarie

Hastings Council put together a strategy in 2006. Following a discussion with Port Macquarie

Hastings Council it was identified that at present no policies have been implemented from

this strategy. All are aware of the affordable housing issues in our region and many are

working towards developing such policies to contribute to easing the housing stress on the

Mid North Coast. Some of the councils include affordable housing plans into their Local

Environmental Plans (LEP) and Development Control Plan (DCP) documents.

Stakeholder Plans and Government Programs

The Mid North Coast has a number of organisations and individuals working on strategies

relating to affordable housing. Stakeholders identify that affordable housing is of high

priority in the region. The pre-existing strategies vary in their approach from research based

strategies to hands on allocation of affordable housing. What was identified in the research

and engagement components of this project was that the region is under catered for when

it comes to affordable housing, as is much of Australia.

The Mid North Coast has particular demographics that exemplify the demand for affordable

housing in the area; a higher percentage of elderly are concentrated in the region (21%, 65

years and over) compared with NSW as a whole (14.7%, 65 years and over), and a much

higher percentage of people both earning less than the NSW median income as well as a

higher percentage of people earning in the low income bracket (29.2% of people aged over

15 in the Mid North Coast earn less than $299 a week compared with 2.7% in NSW).

One particular strategy that is in place in the region is the Mid North Coast Regional

Homelessness and Housing Working Party Forum. The party identifies the need for the

community to work more collaboratively as a region to improve outcomes for homelessness

and housing on the Mid North Coast (MNCRCSD 2012). This particular strategy aims to:

Page 32 of 84Mid North Coast Affordable Housing Report

Improve homelessness and housing outcomes for the region,

assist in furthering the aims of the state and North Coast action plans,

act as a regional body to identify challenges and generate positive solutions to these

challenges,

strengthen regional and whole of system collaboration and

act as a conduit between regional homelessness, housing services and the North

Coast Regional Homelessness Action Plan Committee and other macro committees

(MNCRCSD 2012).

Port Macquarie Hastings Affordable Housing Strategy (2006) aims to minimise the amount

of housing stress within the region. The ‘breadth of impact arising from housing stress

illustrates the need for a holistic policy response to the issue’ (SGS Economics & Planning

2006). The Port Macquarie Hastings Affordable Housing Strategy aims to leverage such a

response whilst monitoring the results within the community. The benchmark for this

strategy is to decrease the proportion of the region that is in housing stress.

The current policy settings are largely based on the assumption that pre-existing trends will

continue (AHURI 2004). Stakeholders in the Mid North Coast identified they were unhappy

with the current planning situations which limited their ability to implement affordable

housing strategies in the region. The proposed changes for the planning process as outlined

in the NSW Government ‘Green Paper’, if implemented, should make for a better

environment for those wishing to work on affordable housing to plan for future trends.

The Australian and New South Wales Governments have a number of programs in place to

assist with the affordability of housing. These programs relate to both rental properties and

home purchases in particular first home owners and encouraging construction of new

residential houses. Table 10 identifies these schemes, strategies and programs.

Page 33 of 84You can also read