BERLIN THIS CITY'S ON A ROLL! - comfort.de

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

BERLIN

THIS CITY’S ON A ROLL!

APRIL 2017

IN FIGURES With a population of more than 3.5 million, Germany’s

capital Berlin is the country’s largest city by far. Berlin is

Federal state: Berlin

the only genuinely global German city, not just because of

Inhabitants: 3,520,031 its size but also because of its diverse and vibrant cultural

scene and its reputation as a trend-setting hub. This city

Population development: + 1.4 % has almost magnetic appeal and is experiencing substan-

tial population growth. Between 2012 and 2016 alone, a

Employees: 1,311,079

total of 194,000 new residents moved to Berlin – enough

Unemployment rate: 9.4 % people to populate a medium-sized city.

Purchasing power: 96.7 Berlin is an exceptionally large city with a very polycentric

structure. Economic disadvantages resulting from the pre-

Centrality parameters: 106.1

reunification division of the city into a western part and an

Relevant shopping centres:: eastern part, which meant a centrally planned economy for

Boulevard Berlin (C), Alexa (C), Potsdamer Platz the eastern part of the city and an “enclave” status for the

Arkaden (C), Europa-Center (C), Wilmersdorfer

Arcaden (C), Bikini Berlin (C), Das Schloss (C), Forum western part, have now been largely eliminated. This is

Steglitz (C), Mall of Berlin (C), Hallen am Borsigtum clearly evident in the positive development of employment

(S), Gropius Passagen (S) etc.

figures. The number of employees paying social security

C=City S=District P=Outskirts

contributions has risen by around 214,000 or 19% in recent

Source: state statistical offices, GfK GeoMarketing GmbH, Federal

Employment Agency years, an increase that none of the other top 7 German

cities have been able to match. Double-digit unemploy-

PRIME RETAIL RENTS ment figures are now a thing of the past in Berlin.

from 2006 - 2016 in EUR/m²

This dynamic city is a European tourist hotspot with over

80-120m² 300-500m²

31 million overnight stays and almost 13 million guests

400

(around 46% foreign) every year. This is additionally en-

350 hancing Berlin’s reputation as a tourist destination and

300 driving the development of its tourism industry (see chart

250 on page 7). The number of overnight stays has almost

doubled over the last decade.

200

150

100

THE CITY’S SIGNIFICANCE AS A

50 RETAIL LOCATION

0

06 07 08 09 10 11 12 13 14 15 16 Berlin is also a shopping metropolis with many excellent

inner city retail locations catering to the city’s fast-

expanding population, tourists and the approximately 1.8

CITY CENTRE AREA million residents of the surrounding region. Berlin’s classic

Berlin Ø > 1 Mio. Inhabitants

catchment area has 5.3 million people in it!

The Berlin retail landscape is both diverse and appealing in

Proportion

of sales in terms of store formats, retailers and locations. In fact, it

% caters to practically all consumer preferences and can

compete with other international shopping destinations.

Proportion

of retail

space in %

0 5 10 15 20 25

Source: COMFORT Research & Consulting

COMFORT City Report Berlin 2017 2 von 12

PURCHASING POWER AND There are many good reasons why international labels

CENTRALITY PARAMETERS such as Uniqlo, Forever 21, Pull & Bear, Bershka and &

Other Stories chose the capital city as the location for their

Centrality parameters Purchasing power

first stores in Germany. Various other brands, including

Berlin Under Armour and Miniso, are also waiting to make their

move as soon as they find a suitable location. Department

Düsseldorf

stores such as KaDeWe, Galeries Lafayette and Duss-

Frankfurt am Main mann das Kulturkaufhaus are unique in Germany, putting

Hamburg

Berlin on a par with London and Paris in the European

context. Berlin is today a leading fashion city that hosts top

Cologne

industry events such as the Berlin Fashion Week. Many

Munich smaller concept stores also open their first outlets in Ber-

Stuttgart

lin.

0 25 50 75 100 125 150

The Berlin retail scene is almost 5 million m² in size – cor-

Source: GfK GeoMarketing GmbH responding to around 1.4 m² of retail space per person –

and generates total revenue in the region of EUR

FASHION CENTRALITY 18 billion. Berlin effectively performs a trans-central supply

function for the city and the surrounding region of Bran-

Berlin

denburg, and it is a representative capital city for Ger-

Düsseldorf

many. This is inadequately expressed by the 2016 GfK

Frankfurt am Main centrality index ranking for Berlin of 106.1 compared with

Hamburg other German cities and in its specific fashion centrality

Cologne index ranking of approximately 153. Although Hamburg,

Munich

Munich and Cologne are far higher ranked, it’s important to

Stuttgart

remember that Berlin’s ranking is statistically depressed by

its extraordinarily large population.

0 50 100 150 200 250

Quelle: COMFORT – Research & Consulting

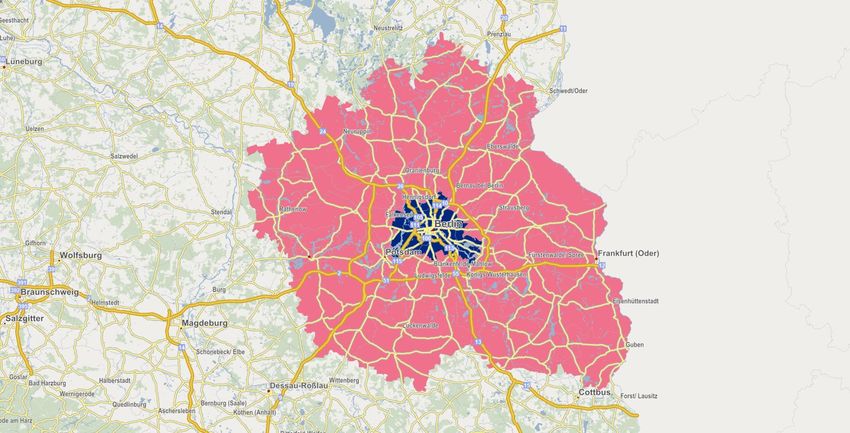

CATCHMENT AREA

Source: COMFORT – Research & Consulting, base map RegioGraph

COMFORT City Report Berlin 2017 3 von 12

With a population exceeding 3.5 million, compared with around 1.8 million in Germany’s second largest city, Ham-

burg, Berlin’s sheer size puts it in a league of its own. Retailers in Berlin operate in an equally unique environment

in terms of this city’s size, polycentrality, cosmopolitanism and international visitor public. To effectively assess the

retail situation and outlook in Berlin, it is necessary to take a differentiated approach to the various retail locations

and districts. These include all the central locations, the special locations of Potsdamer Platz and Leipziger Platz

as well as the non-central locations of Schlossstrasse in Steglitz and the Wilmersdorfer Strasse pedestrian zone,

which are very different with respect to size.

CITY RETAIL DATA

Strukturdaten München Köln

Berlin Hamburg Frankfurt Stuttgart Düsseldorf

Structual data Munich Cologne

Einzelhandelskaufkraft 2016

Retail purchasing power 2016 96,7 129,2 109,9 108,8 113,8 112,3 117,6

(Deutschland/Germany = 100,0)

Einzelhandelsverkaufsfläche 2016

Retail sales area 2016 4.800.000 1.809.000 2.690.000 1.595.000 1.150.000 994.400 996.300

in m² / sqm

Anteil der Innenstadt in m²

643.000 490.400 346.000 316.000 271.900 358.500 346.350

Share of the city centre im sqm

Anteil der Innenstadt

13,4% 27,1% 12,9% 19,8% 23,6% 36,1% 34,8%

Share of the city centre

Einzelhandelsverkaufsfläche pro Einwohner

1,4 1,2 1,5 1,5 1,6 1,6 1,6

Retail sales area per inhabitant

Flächenproduktivität in € pro m²

3.800 5.900 4.100 4.400 3.700 4.200 4.200

Space productivity in € per sqm

Flächenproduktivität Innenstadt in € pro m²

3.800 6.500 5.500 5.100 5.100 4.500 4.600

Space productivity of the city centre in € per sqm

Einzelhandelsumsatz 2016 in Mio. €

18.033,0 10.662,1 11.016,5 7.026,5 4.235,5 4.165,6 4.183,3

Retail turnover 2016 in € million

Anteil der Innenstadt in Mio. €

2.475,0 3.210,0 1.910,0 1.605,0 1.400,0 1.625,0 1.580,0

Share of the city centre in € million

Anteil der Innenstadt

13,7% 30,1% 17,3% 22,8% 33,1% 39,0% 37,8%

Share of the city centre

Einzelhandelszentralität 2016

Retail centrality 2016 106,1 114,0 112,2 121,9 102,4 119,6 116,2

(Deutschland/Germany = 100,0)

Modezentralität 2016

Fashion centrality 2016 153,3 219,1 169,1 197,8 198,4 202,3 222,7

(Deutschland/Germany = 100,0)

Einzugsgebiet / Catchment area

5,3 3,1 3,4 2,4 2,3 2,5 2,0

Einwohner in Mio. / Inhabitants in mill.

Quelle / Source: COMFORT - Research & Consulting, GfK GeoMarketing GmbH

COMFORT City Report Berlin 2017 4 von 12

PRIME RETAIL RENTS

1A-LAGE in EUR/m²

KURFÜRSTENDAMM / TAUENTZIENSTRASSE 80-120 m²

Most important and famous shopping boulevard in Berlin

Best section between KaDeWe (Kaufhaus des Westens) and Olivaer Platz 350

Diverse cross-section of retailers from the concentration of department stores 300-500 m²

on Tauentzienstrasse to the luxury retailers near Olivaer Platz

180

Highest footfall between Tauentzienstrasse and Kurfürstendamm, corner of

Uhlandstrasse

New tenants: Reserved, Diptyque, Superdry, Lush, planet sports, Asics

Rents Kurfürstendamm: approx. EUR 290/m² (small), approx. EUR 150/m²

(medium-sized)

Rents Tauentzienstrasse: approx. EUR 350/m² (small), approx. EUR 180/m²

(medium-sized)

ALEXANDERPLATZ 80-120 m²

Central shopping location catering to the eastern part of the city and

consumer counterpart to City West 250

Extremely well-connected by road and public transport: 300,000 people pass 300-500 m²

through every day

This location’s strength is mainly thanks to department stores such as Galeria 130

Kaufhof and major chain stores such as C&A, Primark, Saturn and TK Maxx

Rents are likely to increase because of high demand for retail space

New tenant: flying tiger

Rents: approx. EUR 250/m² (small), approx. EUR 130/m² (medium-sized)

FRIEDRICHSTRASSE 80-120 m²

The second-most important shopping location in the east of the city with a

wide variety of highstreet and luxury retailers 220

Most important retailers: Galeries Lafayette, Zara, H&M, Kulturkaufhaus 300-500 m²

Dussmann

Development potential on the southern section near Checkpoint Charlie 110

New tenants: ecco, Läderach Confiserie

Rents: approx. EUR 220/m² (small), approx. EUR 110/m² (medium-sized)

WILMERSDORFER STRASSE

The only real pedestrian zone in central Berlin

80-120 m²

Most shoppers here live in the core catchment area

Good amenity value as a result of several established cafés and restaurants 90

New tenants: REWE, CCC-Schuhe, Jim Block, Cross Jeans

300-500 m²

Rents: approx. EUR 90/m² (small), approx. EUR 45/m² (medium-sized)

45

COMFORT City Report Berlin 2017 5 von 12

SCHLOSSSTRASSE 80-120 m²

The most important highstreet in the affluent south-western part of Berlin

Four big shopping centres on the west side 110

Resulting surplus of available retail space, which impacts rental income 300-500 m²

Plans to redesign the retail space on the elevated basement level of the 55

Steglitzer Kreisel high-rise as part of the development project there

New tenants: UNIQLO, Change of Scandinavia, Mister Spex

Rents: approx. EUR 110/m² (small), approx. EUR 55/m² (medium-sized)

HACKESCHER MARKT 80-120 m²

Hip and trendy area for young German and international retailers

150

This lively district is the first choice location for new brands

New tenants: Ba&sh, Love Stories, Suit Supply 300-500 m²

Rents: approx. EUR 150/m² (small), approx. EUR 70/m² (medium-sized) 70

The German capital city is a trend-setting hub with major global appeal. There is still high demand for retail space

at top locations in the western part of the city, particularly Kurfürstendamm and Tauentzienstrasse, as well as Al-

exanderplatz in the east, mainly from international chain store operators. Demand from premium retailers is high-

est for modern and high quality retail space.

Kurfürstendamm 19-24, Sunglass Hut, brokered by COMFORT

The completion of the Upper West, Neue Gloria and Kudamm-Karree shopping centre development projects be-

tween 2017 and 2020 will make City West an even stronger retail location. The first centre to open will be ZOOM,

a Hines project, at Bahnhof Zoo. Tenants include Irish chain store operator Primark.

COMFORT City Report Berlin 2017 6 von 12

– DATA

Tourism – Data

TOURISM BERLIN

Berlin 2016 2016 VS. 2006

vs. 2006

Guests Overnight stays

These developments will give Breitscheidplatz, Kurfür-

35 stendamm and Joachimsthaler Strasse a new look, influ-

+ 95,3 % enced among other things by the new Superdry flagship

30 store and hip café The Barn, which is moving into the

historic premises of Cafés Kranzler. The biggest Motel

25 One, with more than 500 rooms in the Upper West high-

rise, the revitalisation of the Zoologischer Garten train

in Mio.

20 station with a big new McDonald’s restaurant and Bikini

Berlin, which has already opened, are also contributing to

15

+ 79,9 % the area’s changing face. City West is already Berlin’s

heart and soul and will be even more so in future.

10

The area surrounding Hackescher Markt is developing

5

very dynamically. It boasts a successful mix of retail, din-

0

ing and entertainment that makes it absolutely unique in

2006 2016 Berlin and sustains demand for retail space at a high and

Source: state statistical offices stable level. Friedrichstrasse is very much in demand,

especially the section between the station and Unter den Linden, and demand for the area to the south of Unter

den Linden has also stabilised. Although the Mall of Berlin shopping centre recently opened nearby, no synergies

have been evident up to now.

Bahnhofstraße 23-25, Tiger, brokered by COMFORT

COMFORT City Report Berlin 2017 7 von 12

Alexanderplatz has a high footfall (300,000 people a day) and continues to be the most important established

shopping location in the eastern part of the city. The Alexanderhaus project, a modern new development of the

entire retail area (completion in 2018) will make this location even more attractive in future.

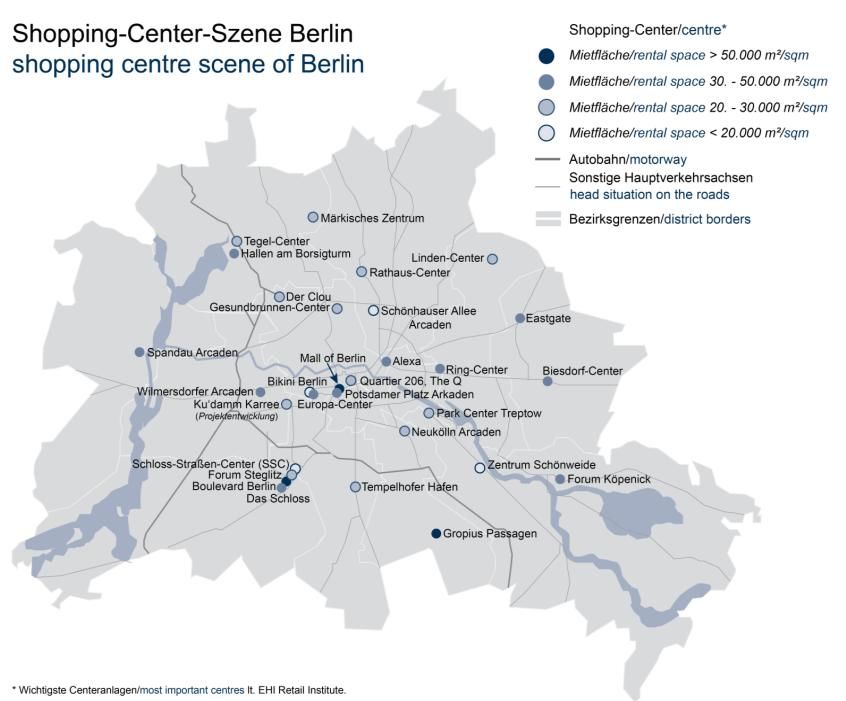

SHOPPING CENTRES

Berlin has the most shopping centres in Germany. According to the EHI Retail Institute, the city has 40 shopping

centres with total rental space of EUR 1.44 million m². No other German city has anywhere near this number of

shopping centres. The majority (32 or four-fifths) of Berlin’s shopping centres are located in non-central districts

and neighbourhoods. Schlossstrasse Steglitz is the shopping centre stronghold, with four shopping centres provid-

ing total retail space of more than 130,000 m² within a one kilometre section of the road.

On the other side of the coin, the established

central Berlin districts have relatively few

shopping centres. One exception is the tradi-

tional city centre location of Potsdamer Platz /

Leipziger Platz, which has both the Potsdamer

Platz Arkaden and the Mall of Berlin, the city’s

biggest shopping centre of all. Mall of Berlin

has around 270 shops and 76,000 m2 of retail

space to rent. It attracts many visitors and tour-

ists but has not yet won over local consumers.

Although all the largest shopping centre devel-

opments are now long completed, there are

still a few projects in the pipeline. As well as

individual new developments such as the

planned East Side Mall (a Freo development

project, already sold to RFR) opposite the

Mercedes-Benz Arena in Friedrichshain, or the

HGHI development on the Schultheiss site in Berlin-Moabit, or the private investor project at the old slaughter-

houses on Landsberger Allee, upcoming projects mainly relate to the refurbishment of old shopping centres such

as Kudamm Karree and Tegel-Center.

Schloßstraße 25, Change, brokered by COMFORT

COMFORT City Report Berlin 2017 8 von 12

INVESTMENT

As an investment location, Berlin is equal in every respect to other PURCHASE PRICE FACTOR

major European cities such as London or Paris. It is an absolute must

29,0 - 31,0

for German investors and also attracts international capital from both

institutional and private investors. The market as a whole is very mul-

tifaceted, with many different products and property sizes at diverse

locations. There has been so much hype in some areas over recent

months that purchasing prices have rocketed sky high and rents ha-

0 10 20 30 40

ven’t been able to keep pace for some time now.

Overall, surplus demand is still driving the dynamic trend in the Berlin

investment market. Prices are continuing to rise strongly with buyers paying more than 30 times the annual rent in

some cases. There has been no let-up in demand for projects on Kurfürstendamm or Tauentzienstrasse, Hacke-

scher Markt, Schlossstrasse or Friedrichstrasse. Friedrichstrasse is particularly interesting to institutional investors

due to the size of the properties there. Alexanderplatz, on the other hand, offers very few investment products as a

result of its structure. Transactions involving properties of various sizes and quality categories have taken place in

virtually all areas of Berlin in recent months. Examples include the sale of Kurfürstendamm 26a, Friedrichstrasse

79/80 and Wilmersdorfer Strasse 50–52.

In summary, demand for properties in all areas of

Berlin has not let up at all. Private and institutional

investors are making a wide range of investments,

although private investors tend to prefer the

slightly smaller properties around Hackescher

Markt, Schlossstrasse and Wilmersdorfer Strasse.

Institutional investors have no volume limits when

it comes to properties in prime locations, shopping

centres or portfolios.

The excellent rating of Berlin’s property sector,

even by European standards, is also expressed in

pwc and ULI’s renowned survey of almost 800

property experts throughout Europe, “Emerging

Trends in Real Estate Europe 2017”, which was

published at the beginning of the year. In terms of

overall performance, Berlin is the clear leader. It

leaves other major European cities such as Paris

(15th) and London (27th) trailing far behind.

Alte Schönhauser Straße 41, Sunspel, brokered by COMFORT

COMFORT City Report Berlin 2017 9 von 12

COMFORT CITY-RANKING 2017

Demography / (socio-)economy

Retail trade

Location and real estate

The COMFORT City Ranking assesses the economic basis, power of attraction, and performance of the retail trade and retail properties in city centres. The index serves

as a factually substantiated basis for negotiating rental and purchase prices of city-centre retail properties in Germany. Technically, it is a weighted index of relevant key

data and parameters relating to demography and (socio-)economics, the retail trade, location and retail properties. For the most important 60 cities, which are represented

in this HIGH STREETS report with individual city reports, a total of 35 parameters determined topically and in the same manner for each individual city are entered. Using a

scoring model, the parameters cover three major areas, within which individual sub-indicators are also analysed. In detail these are as follows:

• Demography/(socio-)economic index (Parameters for population/development, GDP, employment, unemployment, tourism, retail purchasing power)

• Retail trade index (Parameters for the catchment area: population size and level of demand, retail centrality, fashion centrality, as well as city centre sales, sales areas

and sales-area productivity)

• Location and real-estate index (Parameters for the rents of small/medium-sized spaces, location / retail space structure of the city centre, industry/operator mix in the city

centre, rental demand, intensity of demand[Overall rental space demand in m2 in relation to the available retail spaces in the city centre])

As a result of the extremely positive developments in the Berlin retail scene, particularly retail property invest-

ments and, to a slightly lesser extent, retail property rentals, Berlin has climbed up the COMFORT City Ranking to

second position behind Munich.

METROPOLITAN COMPARATIVE SCORING (IN %)

Munich

Stuttgart

Hamburg

Berlin

Frankfurt

Düsseldorf

Cologne

83 84 85 86 87 88 89 90 91 92 93

SUMMARY AND OUTLOOK

The above brief analysis of Berlin’s top retail and commercial property locations indicates a very positive outlook in

the foreseeable future.

Favourable and strongly improving demographic and economic frameworks support this prognosis. Official figures

clearly document Berlin’s impressive growth over the past three years: over 100,000 additional residents, 80,000

more employees paying social insurance contributions and some 4 million more overnight stays in hotels.

On the other hand, “soft” image factors are also contributing to these positive developments. Berlin is still THE

trend-setting German city with its mix of attitude and lifestyle, urbanity and locality, all of which give it genuine

global appeal.

COMFORT City Report Berlin 2017 10 von 12Berlin has made good progress over recent years in attracting retail companies – especially international ones – and both German and foreign investors. Few retailers who aim to be successful in the German market can afford to ignore Berlin. One good example is the internationally famous UNIQLO brand, which now has stores in various key Berlin locations and is now starting to expand to the rest of Germany from the capital. Berlin also has global- standard retail property investment opportunities, which are attracting investor capital to the city. There are very few properties available in prime locations and access to them is very restricted. This has a big impact on demand and is driving up prices in Berlin’s districts and neighbourhoods. Tauentzienstraße, KaDeWe COMFORT City Report Berlin 2017 11 von 12

CONTACT:

LEASING

RONALD STEINHAGEN

COMFORT Berlin-Leipzig

Fon: +49 30 780961-15

Mobil: +49 175 7217707

E-Mail: steinhagen@comfort.de

INVESTMENT

BJÖRN GOTTSCHLING

COMFORT Berlin-Leipzig

Fon: +49 30 780961-16

Mobil: +49 151 52744032

E-Mail: gottschling@comfort.de

RESEARCH & CONSULTING

OLAF PETERSEN

COMFORT Research & Consulting

Fon: +49 40 300858-22

Mobil: +49 175 7217720

E-Mail: petersen@comfort.de

Editor:

COMFORT Holding GmbH

Kaistraße 8A, 40221 Düsseldorf

About the COMFORT Group

The COMFORT Group has specialised in the sale and letting of commercial properties and retail units in prime city centre locations since it was

established in 1979. As a proven retail property expert, COMFORT makes its know-how available via a consultancy services portfolio which

includes expertises, second opinion appraisals and third party due diligence reports. The portfolio also includes shopping centre consultancy

and management services. The COMFORT Group is headquartered in Düsseldorf and has offices in Berlin, Düsseldorf, Hamburg, Leipzig,

Munich, Vienna and Zurich.

www.comfort.de

COMFORT Group media contact

Frank Hinz, Corporate Communications

Kaistraße 8A, 40221 Düsseldorf / Phone: +49 211 9550-144 / E-Mail: hinz@comfort.de

DEFINITIONEN

Rents in prime locations

All statements pertaining to rents are to be read with the following in mind: New rent contracts drawn up in absolutely prime business locations for fictive,

purely ground floor sales areas; ideal shop space has ground-level, step-free access, is fitted out to a high standard and, as far as possible, its layout is at a

right angle to a shop window with a minimum length of 6 m (for a size of 80–120 m²) or 10 m (for 300–500 m²); peak rents in EUR per m², per month, plus statu-

tory VAT and service charges

Purchase price factors

The purchase price factors, shown in their full range, serve as a general orientation for the currently achievable purchase price for commercial buildings (rental

income from retail > 60%, current rent at around market level) with a typical sales volume in the prime location of the respective city. Technically, the purchase

price factor represents the multiplier for calculating the purchase price of a commercial building without a maintenance backlog, when multiplied with the respec-

tive annual net rent.

Purchasing power, Centrality parameters

The purchasing power index complements the information on population size for a given location with qualitative criteria. The average value has been stan-

dardised nationwide at 100. A value above 100 signals that a location has above average purchasing power potential. However, the purchasing power index

does not provide any information as to whether the available capital is in fact spent in the location in question or not.

The centrality indicator shows whether, on balance, purchasing power is flowing into or away from a particular location. A value over 100 indicates that the

inflow of purchasing power from the surrounding area is higher than the outflow from the city. The centrality indicator thereby sheds a special light on the attrac-

tiveness of a location for the retail trade.

Fashion centrality

Analogous to the industry-wide centrality parameters (= retail centrality), the fashion centrality indicator sheds light on the situation in an important sub-sector –

the key city-centre segment fashion, which in turn comprises the two product segments clothing/textiles and shoes/leather products.

Catchment Area

Cartographic representation of geographic areas in terms of the city’s importance to their resident population as a shopping destination. Blue represents the

core city area (zone 1) and red represents the immediate and extended catchment area (zone II).

COMFORT City Report Berlin 2017 12 von 12You can also read