Climate Change Adaptation: Perspectives on Food Security in South Africa - Towards an Integrated Economic Analysis

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Climate Change Adaptation: Perspectives

on Food Security in South Africa

Towards an Integrated Economic Analysis

REPORT No. 5 FOR THE

LONG TERM ADAPTATION SCENARIOS FLAGSHIP RESEARCH PROGRAM (LTAS)

i

Table of Contents

Executive summary ............................................................................................................................... vii

1 Introduction .................................................................................................................................... 1

2 Methodology................................................................................................................................... 4

2.1 The sector model .................................................................................................................... 4

2.2 Consumer Impact study .......................................................................................................... 5

2.3 Climate Data............................................................................................................................ 7

3 Climate Change Impacts on Production and Prices ........................................................................ 9

3.1 Developing the LTAS BASE 2030 projections .......................................................................... 9

3.2 Comparing the LTAS scenarios to the base ........................................................................... 17

3.2.1 Maize ............................................................................................................................. 17

3.2.2 Wheat............................................................................................................................ 20

4 Consumer Impact Study ................................................................................................................ 23

4.1 Approach 1: The ‘BFAP Poor person’s index ......................................................................... 23

4.2 Approach 2: Staple food expenditure pattern based analysis .............................................. 25

4.2.1 Annual household food expenditure implications........................................................ 25

4.2.2 Energy intake implications of an constrained food budget .......................................... 25

4.3 Conclusion: ............................................................................................................................ 26

5 Climate Change Impacts on Agricultural Employment ................................................................. 26

6 Food security and adaptation responses ...................................................................................... 29

6.1 Small scale agriculture and food security ............................................................................. 29

6.2 Continual adaptation and technology .................................................................................. 31

6.3 Irrigation................................................................................................................................ 32

6.4 Expansion of area planted .................................................................................................... 33

7 High-level messages and Policy recommendations ...................................................................... 34

8 Future research needs with links to future adaptation work and modelling capacity ................. 36

Annexes ................................................................................................................................................. 39

ii

List of figures

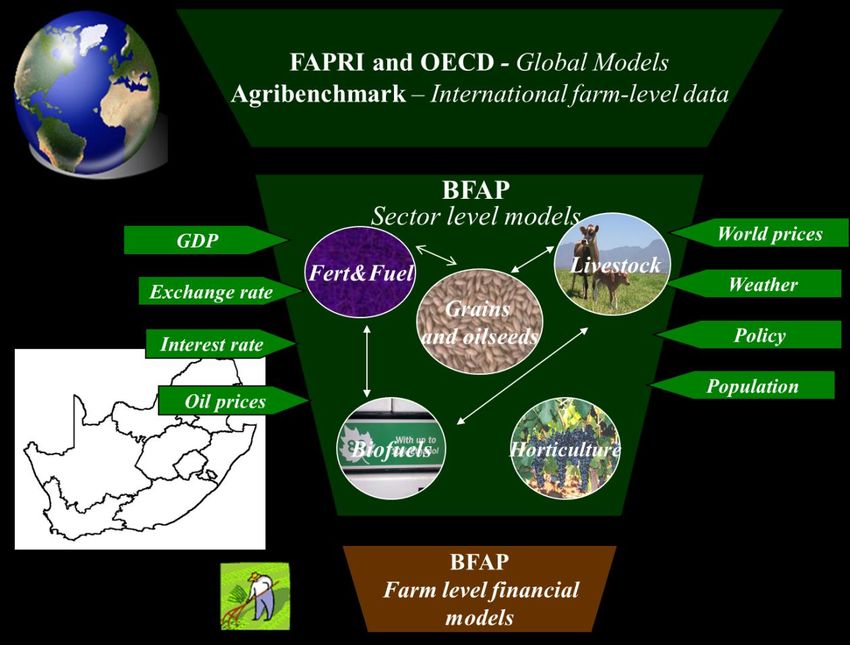

Figure 1: The BFAP modelling system ..................................................................................................... 5

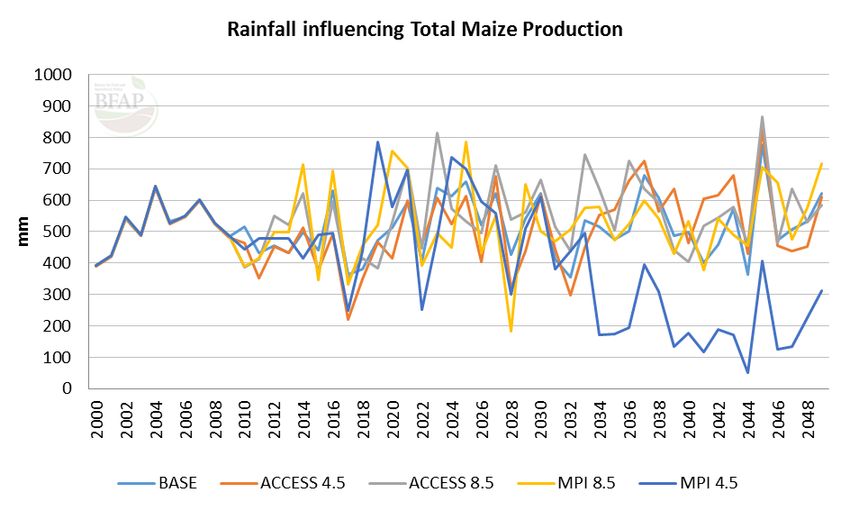

Figure 2: Rainfall for maize production: Historical and forecast .......................................................... 10

Figure 3: SA main field crop area .......................................................................................................... 11

Figure 4: Base - White maize production, consumption and yield ....................................................... 12

Figure 5: White maize price and trade space ....................................................................................... 13

Figure 6: Base - Yellow maize production, consumption and yield ...................................................... 13

Figure 7: Base Yellow maize price and trade space .............................................................................. 14

Figure 8: Base - Wheat production, consumption and yield ................................................................ 15

Figure 9: Base - Wheat price and trade space ...................................................................................... 15

Figure 10: South African Maize: Area Planted and Yield (5 year moving averages) ............................. 16

Figure 11: Precipitation influencing maize production– base versus alternative scenarios ................ 17

Figure 12: Base versus scenarios: white maize average yield .............................................................. 18

Figure 13: Base versus scenarios: white maize average SAFEX prices .................................................. 18

Figure 14: Stochastic precipitation – Base versus MPI 4.5 ................................................................... 19

Figure 15: Stochastic white maize price – Base versus MPI 4.5 ........................................................... 19

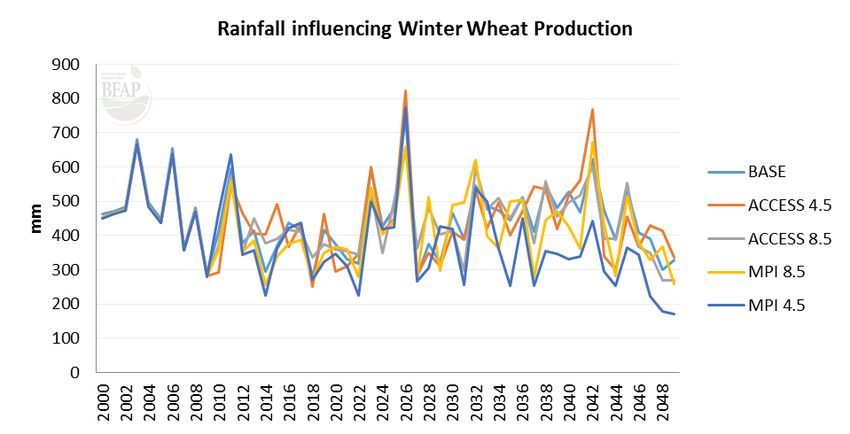

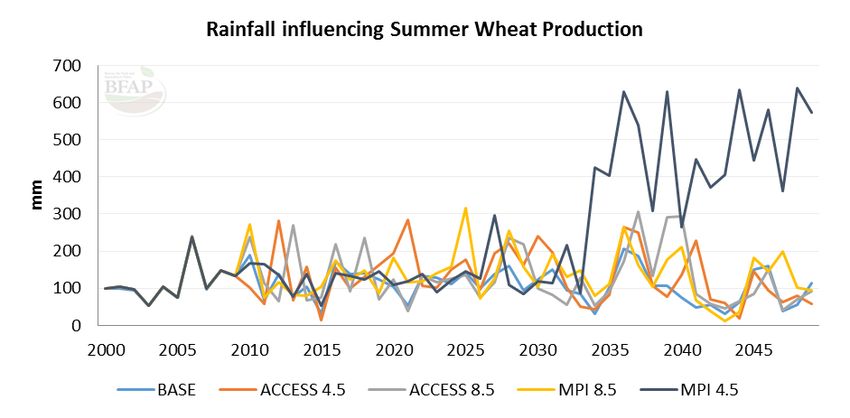

Figure 16: South African Wheat Production and Domestic Use ........................................................... 20

Figure 17: The BFAP Poor person’s index – Projected results .............................................................. 24

Figure 18: Cost share contributions of maize meal within the weighted five item food plate ............ 24

Figure 19: BFAP Employment matrix .................................................................................................... 27

Figure 20: Percentage Changes - Maize Employment .......................................................................... 28

Figure 21: Percentage Changes - Wheat Employment ......................................................................... 28

Figure 22: Reason for engaging in Agriculture ...................................................................................... 30

List of Tables

Table 1: Yield effects (% change from 2000 to 2050) by crop and management system ...................... 1

Table 2: Price outcomes of the overall scenarios ................................................................................... 2

Table 3: Composition of the BFAP Poor person’s index ......................................................................... 6

Table 4: LTAS Scenario Representative Models (2040-2050) ................................................................. 8

Table 5: Macro-economic baseline assumptions.................................................................................... 9

Table 6: Poor person food basket cost and composition ..................................................................... 23

Table 7: Compounded annual growth rates in employment ................................................................ 28

Table 8: Household sources of income, 2010 ....................................................................................... 29

Table 9: South African households’ access to agricultural land, 2010.................................................. 30

Table 10: Agricultural irrigation: Area and Method.............................................................................. 33

iii

List of abbreviations

ACCESS Australian Community Climate and Earth-System Simulator

BFAP Bureau for Food and Agricultural Policy

CF Carbon Dioxide Fertilisation

CSIRO Commonwealth Scientific and Industrial Research Organization

DSSAT Decision Support System for Agrotechnology Transfer

FAO Food and Agricultural Organisation

FAPRI Food and Agricultural Policy Research Institute

IES Income and Expenditure Survey

IFPRI International Food Policy Research Institute

GAM Generalized Additive Models

IMPACT Model for Policy Analysis of Agricultural Commodities and Trade

IPCC Intergovernmental Panel on Climate Change

IPCC AR4 Intergovernmental Panel on Climate Change Fourth Assessment Report

IPCC AR5 Intergovernmental Panel on Climate Change Fifth Assessment Report

LTAS Long Term Adaptation Scenario’s

MPI Max Planck Institute for Meteorology

NAMC National Agricultural Marketing Council

NCAR National Centre for Atmospheric Research

NoCF No Carbon Dioxide Fertilisation

OECD Organisation for Economic Co‑operation and Development

RCP Representative Concentration Pathways

SAWIS South African Weather Information Service

StatsSA Statistics South Africa

UCS Union for Concerned Scientists

WAS Water Management System

iv

1 Acknowledgements

2

3 The Long-Term Adaptation Flagship Research Programme (LTAS) responds to the South African

4 National Climate Change Response White Paper by undertaking climate change adaptation research

5 and scenario planning for South Africa and the Southern African sub-region. The Department of

6 Environmental Affairs (DEA) is leading the process in collaboration with technical research partner

7 the South African National Biodiversity Institute (SANBI) as well as technical and financial assistance

8 from the Gesellschaft für Internationale Zusammenarbeit (GIZ).

9

10 DEA would like to acknowledge the LTAS Phase 1 and 2 Project Management Team who contributed

11 to the development of the LTAS research and policy products, namely Mr Shonisani Munzhedzi, Mr

12 Vhalinavho Khavhagali (DEA), Prof Guy Midgley (SANBI), Ms Petra de Abreu, Ms Sarshen Scorgie

13 (Conservation South Africa), Dr Michaela Braun, and Mr Zane Abdul (GIZ). DEA would also like to

14 thank the sector departments and other partners for their insights to this work, in particular the

15 Department of Water Affairs (DWA), Department of Agriculture, Forestry and Fisheries (DAFF),

16 National Disaster Management Centre (NDMC), Department of Rural Development and Land Reform

17 (DRDLR), South African Weather Services (SAWS).

18

19 Specifically, we would like to extend gratitude to the groups, organisations and individuals who

20 compiled the “Climate Change Adaptation: Perspectives on Food Security in South Africa” report,

21 namely the Bureau for Food and Agricultural Policy (http://www.bfap.co.za), including Prof Ferdi

22 Meyer (University of Pretoria), Jan Greyling (University of Stellenbosch), Gerhard van der Burgh

23 (Bureau for Food and Agricultural Policy [BFAP] analyst), Hester Vermeulen (BFAP analyst), Marion

24 Muhl (University of Pretoria), and Dr Lindsay Trapnell (University of Pretoria); and Dr James Cullis

25 (Aurecon) who provided the rainfall data for the future scenarios analysed in this report.

26 Furthermore, we thank the stakeholders who attended the LTAS workshops for their feedback and

27 inputs on proposed methodologies, content and results. Their contributions were instrumental to

28 this final report.

29

30 Over the past decade Bureau for Food and Agricultural Policy (BFAP) (www.bfap.co.za) has become a

31 valuable resource to government, agribusiness and farmers by providing analyses of future policy

32 and market scenarios and measuring their impact on farm and firm profitability. BFAP is a network

33 linking individuals with multi-disciplinary backgrounds to a coordinated research system that informs

34 decision making within the Food System. The core analytical team consists of independent analysts

35 and researchers who are affiliated with the Department of Agricultural

36 Economics, Extension and Rural Development at the University of

37 Pretoria, the Department of Agricultural Economics at the University

38 of Stellenbosch, or the Directorate of Agricultural Economics at the

39 Provincial Department of Agriculture, Western Cape. BFAP

40 acknowledges and appreciates the tremendous insight of numerous

41 industry specialists over the past decade.

v1 Report overview

2 This report develops preliminary high level messages on the socio-economic and food security

3 impacts of climate change in South Africa, including consideration of impacts on South African

4 consumers and employment in the agricultural sector, and implications for adaptation. Findings are

5 preliminary because they are based on impacts only on the two main staple cereal crops only (maize

6 and wheat) of a limited set of downscaled LTAS climate scenarios.

7

8 The first objective of this study is to translate the selected climate scenarios into maize and wheat

9 production and price effects. In order to achieve this goal the results of four downscaled climate

10 models were incorporated into an econometric, recursive partial equilibrium model of the South

11 African agricultural sector. Within this model, rainfall, both in terms of the total during the

12 production season and the timing thereof, represent one of a host of variables that impact on the

13 eventual results on total area planted, total production and commodity price changes. These results

14 are compared to a baseline scenario that is generated from historic rainfall data. This study

15 therefore provides an economic perspective on the LTAS climate scenarios which bio-dynamic

16 modelling approaches are unable to do. The results also provide a simulated perspective on how

17 producers choose to respond to climate change in terms of area planted and the resulting impact on

18 the equilibrium of demand and supply in maize and wheat markets.

19

20 The second objective of this study is to incorporate these results into a consumer impact analysis in

21 order to evaluate the price effects of the respective climate scenarios on poor households. Within

22 this analysis three approaches where followed: The first is the ‘BFAP Poor person’s index’ is based on

23 the price of typical portion sizes of poor South African consumers’ typical portion sizes of the five

24 most widely consumed food items in South Africa. The second is the StatsSA Income and

25 Expenditure based analysis. The third is the balanced food plate approach that follows a balanced

26 daily food plate approach.

27

28 The third objective of this study is to evaluate the impact of these possible climate futures on

29 agricultural employment. This was achieved through incorporating the results into the BFAP

30 employment model. Collectively these results are interpreted in terms of their food security impacts,

31 both in terms of supply and access. This is translated into adaptation and mitigation

32 recommendations, policy recommendations and future research needed.

33 Chapter 1 (Introduction) provides an overview previous comparable research and will link with LTAS

34 phase 1, specifically the LTAS phase 1 report (no.3 of 6) on agriculture and forestry.

35 Chapter 2 & 3 (Methodology and Data) delivers an overview of the respective methodologies used in

36 the study and provide an overview of the data used within the relevant models.

37 Chapter 4 (Crop model results) provides the results of the partial equilibrium modelling in terms of

38 the changes in the area planted, total production, trade and price of maize and wheat due to the

39 respective climate scenarios.

40 Chapter 5 (Consumer Impact Study) presents the results of the consumer impact study.

41 Chapter 6 (Employment impacts) provides the results on the possible agricultural employment

42 impacts of the respective climate scenarios.

43 Chapter 7 (Food security and messages) this section concludes with a discussion of the food security

44 impacts, mitigation and adaptation responses, policy recommendations and future research needed.

45

vi1 Executive summary

2

3 There have been numerous studies on the effects of potential climate change on crop suitability and

4 productivity from a Southern- and South African perspective. These studies, however, do not provide

5 an integrated perspective of how the agricultural and food system could be affected under various

6 climate change scenarios from an economic and social perspective. Therefore a key need is to

7 translate the respective climate scenarios into economic impacts, both in terms of the food access

8 (price) perspective of food security but also in terms of the impact on the decision to produce, which

9 impacts on agricultural employment. This study aims to fill this gap through a stochastic partial

10 equilibrium modelling approach in order to provide high level messages on the impact of climate

11 change on South African maize and wheat production towards 2030.

12

13 Within this study precipitation data generated from various climate models that best describe drying

14 LTAS climate scenarios were evaluated through the BFAP sector model. This sector model can be

15 best described as an econometric, recursive partial equilibrium model of the South African

16 agricultural sector, which presently covers 52 commodities. The results obtained were analysed

17 further from a consumer impact and employment perspective. The objective of this study is to

18 provide high level messages on the potential impact of climate change on food security and

19 employment under a set of assumptions in order to relate these into policy recommendations that

20 will enable adaptation and mitigation. This study has a strong element of foresighting and in order to

21 achieve these objectives, a combination of modelling tools is applied. When undertaking foresighting

22 analyses, it is useful to consider the future stochastic range of key fundamental variables and not

23 only be fixated on the deterministic projections. It is far more important to explore the possible

24 ranges of key variables and how climate change can potentially have an impact on the maize and

25 wheat industries.

26

27 For this study the actual precipitation data for the period 1950 to 2000 was modelled in order to

28 provide a “real world” baseline for 2000 to 2050 to which the results obtained from the inclusion of

29 the precipitation data from the various climate models could be compared. An analysis of the results

30 from the selected climate models only showed a significant divergence after 2030. In other words, it

31 is apparent that for most of the scenarios the effects on precipitation increase towards the end of

32 the simulation period only. Therefore, in order to analyse the potential economic impacts of climate

33 on the South African maize and wheat industries, the precipitation data projected for the period

34 2034 to 2050 is introduced into the BFAP sector model for each of the scenarios, which is then

35 compared to the base case. The BFAP sector model generates absolute and percentage shocks to

36 illustrate the relative deviations from the base. The implication thereof can be best described as the

37 effect of more than 20 years of climate change on the current context. It also became clear that only

38 one of the four climate models showed a significant deviation from the base after the data was

39 allocated according national maize and wheat production regions, both in terms of total

40 precipitation and the timing thereof.

41

42 An overview of the fundamental trends within the base precipitation scenario is essential for a

43 correct interpretation of the modelled results of the respective climate scenarios Under the base

44 scenario South Africa is anticipated to remain a net exporter of white and yellow maize (i.e.

45 domestic supply exceeds demand) and a net importer of wheat, with net imports growing beyond

vii1 50% of consumption. Maize prices are therefore expected to remain at export parity levels whilst

2 wheat prices are will remain at import parity levels. Within this scenario the total area under field

3 crop production is anticipated to remain relatively stable towards 2030 around the current levels of

4 around 4.7 million hectares. This does not reflect changes in the allocation of crops within this area,

5 however, most notably the expected decline of the area planted under white maize from 1.5 million

6 hectares to 1.1 million hectares and the doubling of the soybean area from around 500 000ha to

7 more than 1 million hectares. This shift is the result of the expected continuation of the upward

8 trend in maize yields whilst the demand for white maize is expected to remain flat due to continued

9 shifts in consumer preferences in favour of bread. The area planted under yellow maize is

10 anticipated to show a small increase whilst the area under sunflower production is expected to

11 remain flat. The area planted under wheat is expected to decline slightly in favour of an increase in

12 canola production. Wheat imports are therefore expected to increase given the growing demand

13 and stable supply. Given this context one can evaluate the modelling results of the respective

14 climate models.

15

16 For the purpose of this study the data for each climate scenario (monthly precipitation per

17 quaternary catchment) was isolated according to the respective production regions in order to be

18 included in the model. One of the most interesting findings of this study is that the drying climate

19 model with the smallest decline in mean annual precipitation (MAP), the warmer/drier (MPI 4.5)

20 model, had the biggest adverse impact on maize and wheat production due to projected local

21 rainfall changes in the production areas. All the other scenarios showed a smaller deviation from the

22 base. This highlights the fact that region-specific agricultural impacts do not necessarily scale directly

23 with national rainfall changes, that probabilistic approaches of multiple scenarios are necessary for

24 comprehensive risk assessment, and that national scenarios require much more considered

25 assessment using aggregated region-specific assessments.

26

27 The modelling results of this warmer/drier (MPI 4.5) scenario shows that white maize yields are

28 anticipated to decline by 1.1 t/ha on average over the outlook period resulting in a drop in total

29 production of approximately 1.6 million tons per annum and an increase in the white maize prices of

30 16 percent. The white maize area harvested is expected to decline as explained above. Within the

31 MPI 4.5 scenario this decline is more than 200 000 hectares less than in the base case, due to

32 farmers opting to produce in response to the higher prices. Adverse climate scenarios therefore can

33 result in an increase in the area planted compared to the base due to price signals. Farmers as

34 rational economic decision makers are not confronted with a simple produce or not to produce

35 decision, but rather face a decision on expanding, contracting or shifting production to other crops

36 given prevailing prices and climate risk.

37

38 South Africa imported more than 40% of all wheat consumed in 2013 and thus the domestic price

39 moves in step with the world (import parity) price. Modelling results of the MPI 4.5 scenario show a

40 decline in domestic production that results in an increase in imports above the magnitude expected

41 in the base. As stated this does not impact on the domestic price but could have a greater negative

42 impact on the agricultural trade balance in comparison to the base scenario. The exports of other

43 agricultural product will therefore have to be increased in order to maintain a positive agricultural

44 trade balance.

45

46 This study evaluated the price impacts of the respective climate scenarios on (mostly poor)

viii1 consumers through the use of three instruments – the BFAP poor person’s index, a staple food

2 expenditure based analysis and a balanced daily food plate models. At present maize porridge and

3 brown bread contribute 73.5% of costs of a five item low income weighted food plate. In terms of

4 bread the analysis all the climate scenarios showed no deviation from the base due fact that each of

5 the scenarios, like the base, tracks the world price throughout. In terms white maize meal the MPI

6 4.5 scenario showed a small deviation from the base. The significance of this deviation decreases

7 over time due to a declining trend in white maize production per household in favour of bread.

8

9 It has to be stated, however, that the anticipated increase in the price of white maize due to the MPI

10 4.5 scenario is on top of the food basket that is anticipated to increase significantly towards 2030:

11 The BFAP poor person’s index almost doubles in price towards 2025. From a food security

12 perspective this brings the affordability of a balanced food basket prominently to the fore. From a

13 supply perspective farmers have the ability to increase production in response to high prices. In

14 terms of wheat, the country has been and will continue to act as major importer. Food security

15 therefore is not a question of supply but rather of access both in terms of financial means or own

16 supplementary production.

17

18 The maize and wheat industry does not act as major employer and is also not regarded as an

19 industry with a significant growth potential, it estimated that these industries collectively employed

20 less than 7% of the agricultural labour force in 2013. For the period 2014 to 2025 employment in the

21 maize industry is expected decline by 2% within base scenario whereas the least favourable MPI 4.5

22 scenario delivers the smallest decline (-1.1%). This is in part due to the smaller contraction in the

23 area planted in response to the increase in the maize price relative to the base case. This reduction

24 does not necessary equate to a decline in absolute agricultural employment due to the transfer of

25 are to the production of other crops – within the base scenario the area under soybean production is

26 expected to increase from 500 000 to 1 000 000 hectares. Within thin in the wheat industry the

27 converse is true with the greatest expected decline (-2.2%) in the MPI 4.5 scenario, which is twice

28 that of the base scenario.

29

30 The challenges faced due to climate change do not act on producers in isolation but rather form part

31 of the bigger collective challenges. Any adaptation strategy should therefore be directed towards

32 bigger collective of challenges. These strategies also does have to be directed towards a specific

33 group of producers, i.e. small scale or commercial, options should be sought that are scale neutral

34 and that would be beneficial to the industry regardless which climate scenario materialises. Example

35 strategies that meet this criterion include improved transport infrastructure, improvements in

36 irrigation efficiency and water management, coordinated field trials in partnership between farmers,

37 private companies and the state as discussed below.

38

39 It also has to be emphasized that farmers are already adapting to climate change. The reduction in

40 the area under wheat production serves as a good example. Farmers have opted to decrease the

41 area planted by more than half, partly in response to price decreases but also in order to decrease

42 exposure to climate risk such as too low or rainfall during harvest. Farmers are also continually doing

43 formal and informal field trials in order to identify the best suited varieties for each locality. The role

44 foreseen for the public sector is not replace these initiatives but rather to support, expand and

45 integrate the results of these respective trials. Greater cooperation between the farmers, seed

46 companies and state will improve the focus of public research and improve quality of extension

ix1 services provided, particularly for small scale farmers in close proximity of these trials.

2

3 This study showed that the area under irrigation can be expanded through new investments in

4 storage capacity. Significant gains are possible, however, within existing systems through decreases

5 in distribution loses, the adoption of more efficient irrigation systems and improvements in

6 management of existing irrigation systems. This has the potential of adding a further area of 282 000

7 hectares under production, simply by using available water. The maintenance of and improvements

8 to existing irrigation systems is therefore an imperative. Incentives for the upgrading of existing

9 systems to more efficient alternatives, for example flood irrigation to drip, would be beneficial

10 especially if incentivised by the state; alternatively the amount of water available to consumers

11 could be regulated in order to encourage investments in more efficient systems.

12

13 South Africa have been a net importer of wheat since the early 1990s but also experienced

14 significant increases in agricultural exports since. According to the MPI 4.5 climate scenario wheat

15 imports are expected to increase around 100 000tons due to a decline in production and increase in

16 consumer demand for wheat. Increasingly larger amounts of wheat will therefore have to be moved

17 between sources of supply or the respective ports, and sources of demand. A cost efficient transport

18 system is therefore an imperative in order to ensure the provision of this staple at the lowest

19 possible cost. An improvement in port, rail and road infrastructure is therefore of utmost

20 importance, especially railways. Inversely this infrastructure will also improve the competitiveness of

21 agricultural exports, particularly fruit and wine. These exports as significant earners of foreign

22 exchange currently and will continue to “afford” the substantial and growing primary food stuff

23 imports. The exports of these products will have to be expanded in future in order to maintain a

24 positive agricultural trade balance and avoid the negative effects of exchange deficits. This also

25 includes the improvement of SADC regional road and rail networks in order to enable more cost

26 efficient trade. Zimbabwe is currently one of South Africa’s biggest trade partners. Fruit and wine

27 exports to SADC is expect continue to grow whist Zambia could serve as important trade partner for

28 wheat for example.

29

30 Transport infrastructure is not limited to harbour, rail and main roads, however. A significant

31 number of (mostly rural) households have access to land and that a large percentage of them engage

32 in agricultural production as an additional source of food and to lesser extent as an additional source

33 of income. It is possible, however, that some of climate scenarios could decrease the ability of

34 households to engage in agricultural production as an additional source of food. This would result in

35 an increased need for food shipments to rural areas to address this deficit, which would put existing

36 (mostly poor) rural roads under further pressure. It is therefore essential that these rural roads

37 should be improved and properly maintained in order to increase the efficiency of transported food

38 items to these rural areas. Conversely this improved infrastructure could increase small scale

39 farmers’ ability to engage in agricultural production for income purpose through connecting them to

40 sources of demand and input supply. This is particularly important from the access perspective of

41 food security through ensuring the availability of food at the lowest possible cost or enabling small

42 scale farmers to earn an income in order to be able to purchase food items not produced.

43

44 This study has provided an essential first perspective but it is only a limited one. Maize and wheat

45 are components of a bigger production system wherein producers are continuously making

46 adjustments to the allocation of their resources in order to maximise the return to their labour and

x1 capital. A study that follows an integrated approach to a much larger number of commodities is

2 therefore needed. The expected trend in expanded soybean and canola production serves as a good

3 example of shits not reflected in this study.

4

5 One of the major trends identified is that of a continuation of the increase in wheat imports, a trend

6 that will be accelerated within some of the climate scenarios. The sector has been able maintain a

7 positive agricultural trade balance despite the increase in wheat and other imports, mainly due to

8 the strong growth in fruit and wine exports. A failure to maintain a positive trade balance will result

9 in depreciation of the Rand that in turn will result in increases in the prices of the large and growing

10 amounts of imported wheat (and rice of which 100% is imported). Ultimately this could reduce

11 access to food due to reduced affordability.

12

13 The fruit and wine sectors are perceived to be under greater risk from climate change due to their

14 sensitivity to temperature increases. Future research on the climate impacts on these crops is

15 therefore very important, and should be linked to an understanding of the economic impacts,

16 including vulnerability to possible punitive tariffs due to the carbon intensity of international

17 transport. Various strategies directed towards the expansion of the competitiveness of these

18 industries are an essential adaptation strategy and a topic also in need of future research.

19

20 The narrow focus of current research on maize and wheat production may be a result of the

21 conflation between food security and food self-sufficiency. Given the current imports of wheat, the

22 inability to increase production and the expected increase in demand puts self-sufficiency clearly of

23 the table. An integrated approach to the availability and affordability aspects of food is therefore

24 much needed in future research.

25

xi1 1 Introduction

2 There have been many studies on the effects of potential climate change on agricultural yields

3 particularly of maize in South and Southern Africa. However, what these studies lack is an integrated

4 view of how the agricultural and food system would be affected under climate change due to the

5 many complex social and economic feedbacks involved. Therefore a key need is to translate the

6 respective climate scenarios into economic impacts, both in terms of the food access (price)

7 perspective of food security but also in terms of the impact on the decision to produce, which

8 impacts on agricultural employment. This study aims to fill this gap through a partial equilibrium

9 modelling approach in order to provide high level messages on the impact of climate change on

10 South African maize and wheat production.

11

12 The International Food Policy Research Institute (IFPRI) has conducted some of the most

13 comprehensive regional and global studies on the possible impacts of climate change on agricultural

14 production and food security. A study by Nelson et al. (2009) developed possible food security

15 scenarios towards 2050 through the use their International Model for Policy Analysis of Agricultural

16 Commodities and Trade (IMPACT), which incorporates the Decision Support System for

17 Agrotechnology Transfer (DSSAT) biophysical crop simulation model. Within these models they

18 incorporated the results of two climate models in order to generate projections. These where the

19 National Centre for Atmospheric Research (NCAR) model from the USA and the Commonwealth

20 Scientific and Industrial Research Organization (CSIRO) model from Australia. Both assume the A2

21 scenario of the IPCC’s Fourth Assessment and predict a warmer climate (higher temperatures)

22 towards 2050 with an increase in both evaporation and total precipitation. The extent the expected

23 increases in precipitation show a wide disparity, however, with the NCAR model forecasting an

24 average increase of about 10%, compared to CSIRO’s 2%.

25

26 Table 1: Yield effects (% change from 2000 to 2050) by crop and management system

1) 2)

Commodity Region CSIRO NoCF NCAR NoCF CSIRO CF NCAR CF

Sub-Saharan Africa 0.3 0.6 0.5 0.8

Maize, irrigated

Developing countries -2 -2.8 -1,4 -2.1

Sub-Saharan Africa -2.4 -4.6 -0.8 -2.7

Maize, rain fed

Developing countries 0.2 -2.9 2.6 -0.8

Sub-Saharan Africa 0.7 1.4 7.3 9.7

Wheat, irrigated

Developing countries -28.3 -34.3 -20.8 -27.2

Sub-Saharan Africa -19.3 -21.9 -11.2 -15.9

Wheat, rain fed

Developing countries -1.4 -1,1 9.3 8.5

27 Source: Nelson et al, 2009

28 Notes: 1) Excluding higher atmospheric concentrations of CO2. 2) Including higher atmospheric concentrations of CO2.

29 The scenarios generated by this study are presented in Table 1 ‒ shown for both Sub-Saharan Africa

30 and developing countries, split according to whether the effects of higher atmospheric CO2

31 concentrations (carbon fertilisation, CF) or disregarded (no carbon fertilisation, NoCF) were included.

32 The results show that maize yields in sub-Saharan Africa are not affected to great extent, with

33 irrigated maize yields actually increasing. Yields for rain-fed wheat on the other hand show a decline

34 of between 11.2 to 21.9% in sub-Saharan Africa, however. Also note that the inclusion of carbon

11 fertilisation results in an increase or lower decrease in production than what is the case with the

2 without scenario. Ringler et al. (2010) concurs that wheat production will be most affected, their

3 results show an expected decline of just over 20%.

4

5 A global study on food security, farming and climate change by Nelson et al. (2010), based on the

6 same assumptions and modelling techniques. This study also included world price projects for

7 staples, as presented Table 2. These results show that real grain prices are not expected to decline as

8 they have done in most of the 20th century. The price increases vary from 31.2% for rice in the

9 optimistic scenario to 106.3% for maize in the pessimistic scenario that assumes an increase in the

10 demand for staple food due to the combination of high population and low income growth rates.

11 Ringler et al. (2010) expect increases in the prices of maize, rice, and wheat prices of 4, 7, and 15 per

12 cent above the historic climate scenario.

13

14 Table 2: Price outcomes of the overall scenarios

Scenarios Maize Rice Wheat Maize Rice Wheat

% price change, 2010 mean to 2050 mean

% price change, 2010 mean to 2050 mean with perfect mitigation

Baseline 100.7 54.8 54.2 32.2 19.8 23.1

Optimistic 87.3 31.2 43.5 33.1 18.4 23.4

Pessimistic 106.3 78.1 58.8 34.1 19.5 24.4

15 Source: Nelson et al, 2010

16 Notes: The percentage increase for the scenarios is the mean across the results for the four cli- mate scenarios, CSIRo and MIRoC GCMs

17 with the SRES A1B and B1 GHG forcings

18

19 All the studies cited above had a sub-Saharan or global focus, but studies on Southern Africa have

20 also been done. Hachigonta et al. (2013) applied the same modelling techniques as Nelson et al.

21 (2010) but assuming the IPCC’s A1B scenario towards 2050. In terms of South African maize

22 production their study projected a decrease in area planted but with an increase in average

23 production per hectare between 1.9 to 2.7 tons/hectare that results in an increase in total

24 production of 0.3 to 2.8 million tons. Three of the four models project significant productivity

25 increases in the North West province, currently one of the biggest maize producing areas but with a

26 low average yield. In the Free State province some areas currently growing maize are projected not

27 to be able to do so whilst others will see the opposite due to change in the current climate. The

28 same trend holds for the Eastern Cape. The models also forecast large areas of increased wheat

29 yields in the Free State and Mpumalanga whilst yields could come under treat in the Western Cape

30 due to decreases in rainfall. The results on the increased wheat yields, especially in Mpumalanga, is

31 somewhat suspicious given the fact that very little wheat is grown in this area, partly due to its

32 disease prone climate and rain during harvest.

33

34 Estes et al. (2013) applied both mechanistic (DSSAT, as utilised above) and empirical (Generalized

35 Additive Models, GAM) models to project the climate change impacts on the potential distribution

36 (suitability) and productivity of maize and spring wheat on a spatial level in South Africa under 18

37 downscaled climate scenarios (9 models run under 2 emissions scenarios) towards 2055. Both

38 models project that the current core maize production areas will remain suitable towards 2055 but

39 not equally so within both models. The DSSAT model projected a 9% gain, primarily along the south

21 western boundary (north-western Free State) of the baseline, while the GAM model showed a 10%

2 loss concentrated among the northern and western boundaries (see Map 1). Both models show an

3 expansion in area suitable for wheat production with the GAM and DSSAT models projecting an

4 increase of 48 and 20% respectively. The DSSAT model showed an expansion of the suitability into

5 the interior from the north-west and southeast of the current growing region, whereas GAM showed

6 gains into the interior along the entire length of its baseline suitability region, see Map 1. In terms of

7 productivity the models projected of maize and wheat the GAM model projected a change of -3.6%

8 and 6.2% respectively, compared to the 6.5% and 15.2% respectively by the DSSAT model.

9

10 Map 1: The change in areas suitable for maize and spring wheat production in 2055

11 Source: Estes et al. (2013)

12 Notes: Projected by both the Decision Support System for Agrotechnology Transfer (DSSAT) and Generalized Additive Model (GAM) models

13 under the median agreement criterion (at least 9/18 simulations agree regarding future suitability). Plots along the bottom row show the

14 percent change in suitable area (given in km2 9 1000) relative to each model’s simulated baseline suitability

15

16 The first phase of the LTAS project included a technical report (no. 3) that provided insights as to the

17 possible effects of climate change on the agricultural and forestry sectors. This was considered from

31 biophysical perspective, specifically relating to yields and changes in the climatically optimum

2 growth areas. These models illustrated a wide range of possible impacts on dry land maize yield ‒

3 ranging from a decrease in 25% to an increase of 10% depending on the scenario.1 Assuming a CO2

4 stabilisation at 450 ppm delivers results on yield impact of between -10% to +5%. The study finds

5 similar results on wheat and sunflower. The study also evaluated the impact on other agricultural

6 crops and grazing, as well as forestry production but all fall beyond the scope of this study. The study

7 also provided possible adaptation responses, which will be returned to in the last section of this

8 report, and highlighted future research needs (LTAS, 2013).

9

10 Given the above it clear that little consensus exists between the various studies but some broad

11 trends can be identified, however.

12 2 Methodology

13 The BFAP sector model is used to evaluate the effect of climate scenario’s on the price, trade and

14 production effects on these key staple crops. These results will in turn be incorporated into the BFAP

15 consumer models in order to evaluate the effect of the possible price changes especially on poorer

16 households in South Africa. The data will also be incorporated into the BFAP employment model in

17 order explore the employment effects of the scenario’s on employment within the maize and wheat

18 industries.

19 2.1 The sector model

20 Section 3 presents the results obtained through the BFAP sector model. This model was first utilised

21 in 2003 and can be described as an econometric, recursive partial equilibrium model of the South

22 African agricultural sector, which presently covers 52 commodities. Within each sector, the

23 components of supply and demand are estimated and equilibrium is established based on balance

24 sheet principles, where demand equals supply at national level. The model is solved within a closed

25 system of equations, where grains are linked to livestock through feed, implying that a shock in the

26 livestock sector is transmitted to grains and oilseeds and vice versa. The model is linked to global

27 markets through the Food and Agricultural Policy Research Institute (FAPRI) in America, as well as

28 the Aglink-Cosimo modelling system used for the annual OECD-FAO agricultural outlook.

29 Figure 1 presents a diagram of the BFAP modelling system where weather is captured as an external

30 driver of the BFAP sector model.

31

1

Depending on the scenario, with unconstrained emissions (typified by IPCC SRES A2 and IPCC AR5 8.5 W.m-2

RCP) and constrained emissions (typified by IPCC SRES B1 and IPCC AR5 4. 5 W. m-2 RCP).

41

2 Figure 1: The BFAP modelling system

3 The BFAP sector model does take biophysical elements, specifically rainfall, into account but does

4 not provide for temperature and CO2 fertilisation effects. Within this study it is assumed that the

5 negative effects of increased temperature are offset by the positive effects of CO2 fertilisation. Given

6 the results of the study by Nelson et al. (2010) discussed in Section 1 it can be assumed that carbon

7 fertilisation has a net positive effect on both wheat and maize yield. Within the model rainfall serves

8 as one of the variables that impacts on the decision to plant and eventually also impacts on the yield

9 realised by the respective crops. For this purpose precipitation in certain production areas for

10 certain months of the year is taken into account in the model.

11

12 For the purpose of this study the BFAP sector model can only be extended meaningfully to 2030 due

13 to the fact that model consists of a number of forecasted macro independent variables that are

14 currently only forecasted up to 2023 (typical 10-year outlook) and in some isolated cases up to 2030

15 by the international modelling institutions. From the long-run projections it also becomes evident

16 that beyond a certain period, a long-run equilibrium is established among markets and trends are

17 mostly unchanged until a new exogenous shock is introduced into the model.

18 2.2 Consumer Impact study

19 Section 4 presents the results of the consumer impact study. Within this study the retail prices for

20 maize meal and bread generated through the BFAP retail price transmission models will serve as the

21 main input for this analysis. The potential impact of maize and wheat price changes due to climate

22 change, especially on poorer households in South Africa will be investigated with multiple

23 approaches.

24

51 Approach 1: The ‘BFAP Poor person’s index’

2

3 The ‘BFAP Poor person’s index’ was developed based on poor South African consumers’ typical

4 portion sizes of the five most widely consumed food items in South Africa: maize porridge, brown

5 bread, sugar, tea and full cream milk (Nel and Steyn, 2002; Oldewage-Theron et al., 2005; Steyn et

6 al., 2000). The term ‘most widely consumed’ means that these food items are consumed by the

7 largest share of South African adults according to the National Food Consumption Survey and other

8 similar studies among poor South African consumers. The BFAP Poor person’s index was calculated

9 by weighing the food price data for these food items, based on the typical (cooked) daily portions of

10 very poor consumers (as obtained from the various nutritional studies listed above), in order to

11 calculate the cost of a ‘typical daily food plate’ for the poor. This index is usually calculated based on

12 the official food price database used by the NAMC for food price monitoring activities. For this

13 exercise the projected prices for brown bread and maize meal will be inserted into this model, to

14 investigate the potential impact on poor households’ basic food expenditure.

15

16 Table 3: Composition of the BFAP Poor person’s index

Category Products

Maize porridge (532g cooked portion)

Bread & cereals

Brown bread (150g portion)

Dairy Full cream milk (56g portion)

Sugary foods White sugar (22g portion)

Hot beverages Tea (2.5g dry tea portion)

17

18

19 Approach 2: Staple food expenditure based analysis

20

21 A model of the staple food consumption patterns of households from different socio-economic

22 groups in South Africa will be developed, departing from the average expenditure of the ten income

23 deciles in South Africa on main staple food commodities (StatsSA, 2012).

24 The projected prices for bread and maize meal will then be inserted into this model to estimate:

25 The potential additional expenditure on these staple foods if consumption quantities remain the

26 same at higher price levels:

27 The potentially reduced energy intake if staple food budgets remain unchanged but retail prices

28 of bread and maize meal increases.

29

30 Approach 3: A balanced daily food plate model

31

32 BFAP has been working with nutritionists to compile examples of balanced daily food plates

33 adhering to both the requirements of adequate energy intake and micronutrient composition.

34 The projected prices for bread and maize meal will then be inserted into this balanced daily food

35 plate model to estimate:

36 The potential additional expenditure on these staple foods if consumption quantities remain the

37 same at higher price levels;

38 The potentially reduced energy intake within this ‘daily food plate’ if food budgets remain

39 unchanged but retail prices of bread and maize meal increases.

61 Developing future scenarios with respect to a change in household characteristics such as food

2 expenditure patterns, class mobility and others, falls beyond the scope of this study. Hence, the

3 current characteristics will be applied in order to generate the impact of future maize meal and

4 bread prices in the analyses described above. Thus, the assumption will have to be made that

5 households will have the same characteristics 20 years into the future as is presently the case.

6 2.3 Climate Data

7 The LTAS Phase 1 developed a consensus view on the range of plausible climate scenarios for three

8 time-periods for South Africa at national and sub-national scales under a range of global emissions

9 scenarios. The time-periods considered were 2015 to 2035 (centred on ~2025, so-called short- term)

10 in addition to the previously followed approach of exploring climate change over several decades

11 into the future (centred on ~2050 (medium-term) and ~2090 (long-term).

12

13 These scenarios were developed through local and international climate modelling expertise using

14 both statistical and dynamical downscaling methodologies based on outputs from IPCC AR4 (A2 and

15 B1 emissions scenarios) and IPCC AR5 (RCP 8.5 and 4.5 Wm-2 pathways). These represent an

16 unmitigated future energy pathway (unconstrained, A2 and RCP8.5) and mitigated future energy

17 pathway (constrained, B1 and RCP4.5, or emissions scenarios equivalent to CO2 levels stabilising

18 between 450 and 500ppm).

19

20 South Africa’s climate future up to 2050 and beyond can be described by using four fundamental

21 climate scenarios at national scale, with different degrees of change and likelihood that capture the

22 impacts of global mitigation and the passing of time.

23

24 1. warmer (3°C above 1961–2000) and drier, with a substantial increase in the frequency of

31 drought events and greater frequency of extreme rainfall events.

32

33 The effect of strong international mitigation responses would be to reduce the likelihood of

34 scenarios 3 and 4. It is not possible to evaluate the effect of all the respective climate models

35 through the use of the BFAP model during the time frame of LTAs phase 2 due to the amount of

36 work required to prepare the data for analysis. It was therefore decided to conduct a preliminary

37 test of the effect of four climate models representing a range of rainfall changes at the national

38 level. A subset of scenarios was selected from those available to explore the vulnerability of wheat

39 and maize production and its effect on the food system.

40

71

2 Table 4: LTAS Scenario Representative Models (2040-2050) with calculated percentage average

3 rainfall changes

Avg. change in

LTAS Scenario Model

MAP (%)

Warmer/moderately drier ACCESS RCP 4.5 - 3.3%

Warmer/drier MPI RCP 4.5 - 1.1%

Hotter/moderately drier ACCESS RCP 8.5 - 4.3%

Hotter/drier MPI RCP 8.5 - 14%

4 Source: Aurecon (2014)

5

6 In light of the above, four CSIR CMIP5 climate models (see Table 4) were selected and the results

7 incorporated into the BFAP sector model in order to evaluate the possible price and production

8 impacts of each of these possible climate futures. The warmer models incorporate the assumptions

9 of the RCP 4.5 climate futures whilst the hotter scenarios assume the RCP 8.5 futures. Both of the

10 moderately drier scenarios are the result of the ACCESS global climate model whilst the drier

11 scenarios are the result of the MPI global model.

12

13 These models delivered actual monthly precipitation, dynamically downscaled through the CCAM

14 (conformal-cubic atmospheric model) into quaternary catchments. These quaternary catchments in

15 turn where aggregated into secondary catchments by averaging the quaternaries that constitute

16 each of the secondary catchments. The resulting secondary catchments where then grouped in

17 according to production areas and months of interest specified by the BFAP sector model. With the

18 wheat model for example, both the winter (Western Cape) and summer (Free State) production

19 areas where compared with the calculated secondary catchments, the relevant catchments within

20 each of these production areas where then identified, the precipitation data on the relevant months

21 isolated, totalled per production area and then included in the model.

22

23 As stated above this model can only provide meaningful econometric results up to 2030 due the fact

24 that forecasted data on the determining factors (dependent variables) of the model, other than

25 precipitation in this case, is only available up to this date. The problem, however, is that an analysis

26 of the precipitation data of the respective models, grouped in accordance the BFAP model, show a

27 high correlation before 2030 and only show a significant divergence thereafter. In other words, it is

28 apparent that for some of the scenarios the effects on precipitation increase towards the end period

29 (2050). Therefore, in order to analyse the potential economic impacts of climate on the South

30 African maize and wheat industries, the precipitation data projected for the period 2034 to 2050 is

31 introduced in the BFAP sector model for each of the scenarios, which is then compared to a base

32 case. The BFAP sector model generates absolute and percentage shocks to illustrate the relative

33 deviations from the base. The implication thereof can be best described as the effect of more than

34 20 years of climate change on the current context.

35

36 It was decided to use actual historic precipitation data as a base to which the modelling results of

37 the respective scenarios could be compared. For this purpose the rainfall for the period 1950 to

38 2000 was used, this data was also aggregated to secondary catchments, and allocated to the

39 relevant production areas as explained above and included in the model. The modelling results of

40 this data hence serves as a “real world” stochastic base to which the other results can be compared.

81 3 Climate Change Impacts on Production and Prices

2 3.1 Developing the LTAS BASE 2030 projections

3 Various approaches and modelling techniques can be applied in the world of foresighting and

4 developing future outcomes of agricultural markets. The methodology that BFAP has developed links

5 scenario thinking techniques to a set of empirical models at global, national and farm level. The

6 starting point for the empirical impact analyses is first to set a benchmark from where potential

7 deviations can be measured. For BFAP, this benchmark is the most basic projections that are

8 simulated in the BFAP sector model and are referred to as deterministic baseline projections. As

9 discussed in section 2.1 of this report, the BFAP sector model is a recursive partial equilibrium

10 model. The model takes the interaction between various industries like livestock, grains and oilseeds

11 into consideration and projects the future equilibrium between demand and supply for a range of

12 agricultural markets subject to a set of assumptions.

13

14 Traditionally the BFAP baseline projections provide a 10-year outlook of commodity markets, yet for

15 the purpose of this study, this baseline is extended to 2030. In other words, a future scenario is

16 simulated for the next 17 years that is grounded in a series of assumptions about the general

17 economy, agricultural policies and technological change. The typical macro-economic assumptions

18 that are used to generate the baseline are presented in Table 5. The outlook for international maize

19 and wheat prices was generated by the Food and Agricultural Policy Research Institute’s (FAPRI at

20 the University of Missouri) in February 2014. These macro-economic projections were extended to

21 2030.

22

23 Table 5: Macro-economic baseline assumptions

2014 2015 2016 2017 2018 2019 2020 2021 2022 2023

Crude Oil Persian Gulf: (USD/barrel)

101.0 95.5 100.9 105.4 109.8 114.3 117.7 121.0 124.4 127.8

SA Population (Millions) 51.2 51.4 51.7 51.9 52.1 52.3 52.6 52.8 53.0 53.3

Exchange Rate (R/USD) 11.00 10.83 11.20 11.56 11.97 12.40 12.84 13.30 13.77 14.26

Yellow maize, US nr 2 fob ($/ton) 231 215 216 218 221 224 223 222 221 218

Wheat, US HRW nr 2 fob ($/ton) 287 251 242 244 249 256 258 257 256 257

24 Source: BFAP & FAPRI, 2014

25

26 Since the BFAP sector model also takes future rainfall into consideration when projecting the area

27 planted and the yield for a specific crop, a further critical driver that has to be incorporated is the

28 future expectations of rainfall. Traditionally in this type of modelling exercise, it is assumed that

29 “normal” rainfall conditions will prevail and in BFAP’s baseline analysis “normal rainfall” is taken as

30 the average rainfall received over the past thirty years from Weather SA’s database. One can,

31 therefore, anticipate that the deterministic outlook is far less volatile than what will actually be the

32 case. In order to simulate any alternative outcome and to illustrate the impact of volatile weather

33 conditions, the model is simulated stochastically where the variability of precipitation that occurred

34 in the past, is projected into the future.

35

9You can also read